Minimax Estimation of Functionals of Discrete Distributions

Abstract

We propose a general methodology for the construction and analysis of essentially minimax estimators for a wide class of functionals of finite dimensional parameters, and elaborate on the case of discrete distributions, where the support size is unknown and may be comparable with or even much larger than the number of observations . We treat the respective regions where the functional is “nonsmooth” and “smooth” separately. In the “nonsmooth” regime, we apply an unbiased estimator for the best polynomial approximation of the functional whereas, in the “smooth” regime, we apply a bias-corrected version of the Maximum Likelihood Estimator (MLE).

We illustrate the merit of this approach by thoroughly analyzing the performance of the resulting schemes for estimating two important information measures: the entropy and . We obtain the minimax rates for estimating these functionals. In particular, we demonstrate that our estimator achieves the optimal sample complexity for entropy estimation. We also demonstrate that the sample complexity for estimating , is , which can be achieved by our estimator but not the MLE. For , we show the minimax rate for estimating is for infinite support size, while the maximum rate for the MLE is . For all the above cases, the behavior of the minimax rate-optimal estimators with samples is essentially that of the MLE (plug-in rule) with samples, which we term “effective sample size enlargement”.

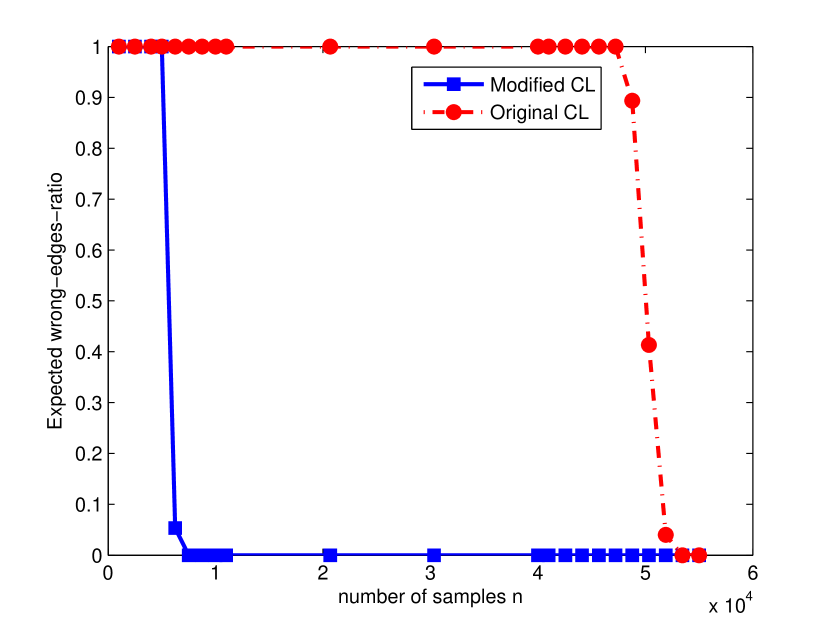

We highlight the practical advantages of our schemes for the estimation of entropy and mutual information. We compare our performance with various existing approaches, and demonstrate that our approach reduces running time and boosts the accuracy. Moreover, we show that the minimax rate-optimal mutual information estimator yielded by our framework leads to significant performance boosts over the Chow–Liu algorithm in learning graphical models. The wide use of information measure estimation suggests that the insights and estimators obtained in this work could be broadly applicable.

Index Terms:

Mean squared error, entropy estimation, nonsmooth functional estimation, maximum likelihood estimator, approximation theory, minimax lower bound, polynomial approximation, minimax-optimality, high dimensional statistics, Rényi entropy, Chow–Liu algorithmI Introduction and main results

Given independent samples from an unknown discrete probability distribution , with unknown support size , consider the problem of estimating a functional of the distribution of the form:

| (1) |

where is a continuous function. Among the most fundamental of such functionals is the entropy [1],

| (2) |

which plays significant roles in information theory [1]. Another information theoretic quantity which is closely related to the entropy is the mutual information, which for discrete random variables can be defined as

| (3) |

where denote, respectively, the distributions of random variables , , and the pair .

We are also interested in the family of information measures :

| (4) |

The significance of functional can be seen via the connection , where is the Rényi entropy [2], emerging in answering fundamental questions in information theory [3],[4, 5]. The functional is also called Gini impurity, which is widely used in machine learning [6].

Over the years, the use of information theoretic measures, especially entropy and mutual information, has extended far beyond the information theory community, and is deeply imbued in fundamental concepts from various disciplines. In statistics, one of the popular criteria for objective Bayesian modeling [7] is to design a prior on the parameter to maximize the mutual information between the parameter and the observations. In machine learning, the so-called infomax[8] criterion states that the function that maps a set of input values to a set of output values should be chosen or learned so as to maximize the mutual information between the input and output, subject to a set of specified constraints. This principle has been widely adopted in practice, for example, in decision tree based algorithms in machine learning such as C4.5 [9], one tries to select the feature at each step of tree splitting to maximize the mutual information (called information gain principle [10]) between the output and the feature conditioned on previous chosen features. Other measures in feature selection have been proposed, such as the Gini impurity (used in CART [6]), variance reduction [6], and many of them can be incorporated as special cases of what we study in this paper. We emphasize that in some applications, mutual information arises naturally as the only answer, for example, the well known Chow–Liu algorithm [11] for learning tree graphical models relies on estimation of the mutual information, which is a natural consequence of maximum likelihood estimation. Recently, it was shown [12] that mutual information is the unique measure of relevance for inference in the presence of side information to satisfy a natural data processing property.

We also mention genetics [13], image processing [14], computer vision [15], secrecy [16], ecology [17], and physics [18] as fields in which information theoretic measures are widely used. There are some other functionals that can be loosely categorized as information theoretic measures, such as the association measures quantifying certain dependency relations of random variables [19], and divergence measures [20].

In most applications, the underlying distribution is unknown, so we cannot compute these information theoretic measures exactly. Hence, in nearly every problem that uses information theoretic measures, we need to estimate these quantities from the data, which is what we study in this paper. Our contributions are threefold. (i) We show that when the number of observations is comparable to the parameter dimension (a relevant regime in the “big data” era), the prevailing approaches (such as plug-in of the maximum likelihood estimator) can be highly sub-optimal. (ii) We propose new and computationally efficient algorithms that are essentially optimal in terms of the worst case squared error risk. That is, we both characterize the fundamental limits on estimation performance, and propose practical algorithms that essentially achieve them. Our results establish that for such functional estimation scenarios, replacing the plug-in (maximum likelihood) estimator by our practical and essentially minimax optimal estimators yields an effective enlargement of the sample size from to , which can make a significant difference in practice. (iii) We demonstrate the efficacy of our schemes by a comparison with existing procedures in the literature, as well as illustrate performance boosts over traditional schemes on both real and simulated data.

Notation: We use the notation to denote that there exists a universal constant such that . Notation is equivalent to and . Notation means that , and is equivalent to . The sequences are non-negative.

I-A Our estimators

Our main goal in this work is to present a general approach to the construction of minimax rate-optimal estimators for functionals of the form (1) under loss. To illustrate our approach, we describe and analyze explicit constructions for the specific cases of entropy and , from which the construction for any other functional of the form (1) will be clear. Our estimators for each of these two functionals are agnostic with respect to the support size , and achieve the minimax rates (i.e. the performance of our approaches when we do not know the support size does not degrade compared with the case where the support size is known).

Our approach is to tackle the estimation problem separately for the cases of “small ” and “large ” in and estimation, corresponding to treating regions where the functional is nonsmooth and smooth in different ways. As we describe in detail in the sections to follow, where we give a full account of our estimators, in the nonsmooth region, we rely on the best polynomial approximation of the function , by employing an unbiased estimator for this approximation. The best polynomial approximation for a function on domain with order no more than is defined as

| (5) |

where is the collection of polynomials with order at most on . The part pertaining to the smooth region is estimated by a bias-corrected maximum likelihood estimator. We apply this procedure coordinate-wise based on the empirical distribution of each observed symbol, and finally sum the respective estimates.

We now look at the specific cases of entropy and separately. For the entropy, after we obtain the empirical distribution , for each coordinate , if , we (i) compute the best polynomial approximation for in the regime , (ii) use the unbiased estimators for integer powers to estimate the corresponding terms in the polynomial approximation for up to order , and (iii) use that polynomial as an estimate for . If , we use the estimator to estimate . Then, we add the estimators corresponding to each coordinate. Our estimator for is very similar to that of entropy, with the only difference that we conduct polynomial approximation for with order , and use the estimator when .

We remark that our estimator is both conceptually and algorithmically simple, with complexity linear in the number of samples . Indeed, the only non-trivial computation required is the best polynomial approximation for functions, which is data independent and can be done offline before obtaining any samples from the experiment. Moreover, the coefficients of the best polynomial approximation of different orders can be preprocessed and stored in advance in the implementation of our approach. We demonstrate in Section V that the best polynomial approximation step can be performed efficiently using modern machinery from approximation theory and numerical analysis.

I-B Main results

Simple as our estimators are to describe and implement, they can be shown to be near “optimal” in the strong sense we now describe. We adopt the conventional statistical decision theoretic framework [21]. Regarding the task of estimating functional , the risk of an arbitrary estimator is defined as

| (6) |

where the expectation is taken with respect to the distribution that generates the observations used by . Apparently, the risk is a function of both the unknown distribution and the estimator , and our goal is to minimize this risk. Since is unknown, we cannot directly minimize it, but if we want to do well no matter what the true distribution is, we may want to adopt the minimax criterion [21][7], and try to minimize the maximum risk

| (7) |

where denotes the set of all discrete distributions with support size . The estimator that minimizes the maximum risk above is called the minimax estimator, and the corresponding risk is called the minimax risk. The exact computation of the minimax risk and the minimax estimator for general seems intractable. Although the maximum risk in (7) is a convex function of (supremum of convex functions is convex), minimizing this function involves computation of the objective function via , which is a non-convex optimization problem. Moreover, even if we can compute it exactly, the minimax estimator will surely depend on the support size , which is unknown to the statistician in many applications.

Hence, we slightly relax the requirement, and seek minimax rate-optimal estimators with maximum (worst-case) risk equal to the minimax risk up to a multiplicative constant. In other words, we want to design estimator such that there exist two universal positive constants that do not depend on the problem configuration (such as the support size and sample size ), for which

| (8) |

As it turns out, it is possible to construct estimators for a wide class of functionals, which do not rely on the knowledge of support size . A brief description of the constructions is given in Section I-A. We find it intriguing that our estimators, which are minimax rate-optimal, are intimately connected to the problem of best (minimax) polynomial approximation, which is a convex optimization problem. In some sense, we have transformed the difficult-to-solve minimax and convex problem of minimizing the maximum risk in (7) into another efficently solvable minimax and convex problem of minimizing the maximum deviation of a polynomial from a given function, which turns out to have been studied extensively in approximation theory for more than a century.

To ease the presentation, we consider the “Poissonized” observation model [22, Pg. 508], since we can show that the minimax risks under the Multinomial model and Poisson model are essentially the same (cf. Lemma 16). Moreover, adopting the Poisson model significantly reduces the length of the proofs, and we emphasize that similar analysis can also go through for Multinomial settings, with more nuanced analysis. In the Poisson setting, we first draw a Poisson random number , and then conduct the sampling times. Consequently, the observed number of occurrences of each symbol are independent [23, Thm. 5.6].

We have the following characterization of the minimax risk for entropy estimation.

Theorem 1.

Suppose . Then the minimax risk of estimating entropy satisfies

| (9) |

Our estimator achieves this bound without knowledge of the support size under the Poisson model.

The following is an immediate consequence of Theorem 1.

Corollary 1.

For our entropy estimator, the maximum risk vanishes provided . Moreover, if , then the maximum risk of any estimator for entropy is bounded from zero.

It was first shown in [24] that one must have for consistently estimating the entropy. However, the entropy estimators based on linear programming proposed in Valiant and Valiant [24, 25] have not been shown to achieve the minimax risk. Another estimator proposed by Valiant and Valiant [26] has only been shown to achieve the minimax risk in the restrictive regime of . Wu and Yang [27] independently applied the idea of best polynomial approximation to entropy estimation, and obtained its minimax rates. The minimax lower bound part of Theorem 1 follows from Wu and Yang [27]. We also remark that, unlike the estimator we propose, the estimator in Wu and Yang [27] relies on knowledge of the support size , which generally may not be known.

For the functional , we have the following.

Theorem 2.

Suppose when we estimate . Then we have the following characterizations of the minimax risk.

-

1.

. If we also have , then

(10) -

2.

.

(11)

Our estimators achieve this bound without knowledge of the support size under the Poisson model.

One immediate corollary of Theorem 2 is the following.

Corollary 2.

For our estimators of , the maximum risk vanishes provided . Moreover, if , then the maximum risk of any estimator for is bounded from zero.

The minimax lower bound we present in Theorem 2111In a previous version of the manuscript, there is a gap between our minimax lower bound and the achievability in Theorem 2. Partially inspired by Wu and Yang [27], we modified the proof by using an argument similar to that in the lower bound proof of [27], thereby closing the gap. significantly improves on Paninski’s lower bound in [28], which states that if , then the maximum risk of any estimator for , is bounded from zero.

The next two theorems correspond to estimation of , .

Theorem 3.

Suppose . Under the Poissonized model, our estimator satisfies

| (12) |

In other words, our estimator achieves an convergence rate of regardless of the support size. This also turns out to be the minimax rate, as shown by the following result.

Theorem 4.

Suppose . There exists a universal constant such that if then

| (13) |

where the infimum is taken over all possible estimators .

Table I summarizes the minimax rates and the convergence rates of the MLE in estimating and . When the rates have two terms, the first and second terms represent respectively the contributions of the bias and the variance. When there is a single term, only the dominant term is retained. Conditions for these results are presented in parentheses.

| Minimax rates | rates of MLE | |

| (Thm. 1,[27]) | [29] | |

| (Thm. 2) | [29] | |

| (Thm. 2) | [29] | |

| (Thm. 3,4) | [29] | |

| [29] |

From a sample complexity perspective (i.e. how should the number of samples scale with the support size to achieve consistent estimation), Table I implies the results in Table II.

| MLE | Minimax rate-optimal | |

|---|---|---|

Our work (including the companion paper [29]) is the first to obtain the minimax rates, minimax rate-optimal estimators, and the maximum risk of MLE for estimating , and entropy in the most comprehensive regime of pairs. Evident from Table I is the fact that the MLE cannot achieve the minimax rates for estimation of , and when . In these cases, our estimators have performance with samples essentially the same as the MLE with samples, and it is the best possible. In other words, the minimax rate-optimal schemes enlarge the “effective sample size” from to . Furthermore, all the improvements we have are in the bias, which is the dominating factor in the risk. This observation suggests a simple way to obtain the minimax rates from the rates of the MLE. One need merely find the bias term in the expression of MLE rates, and replace the term by . This simple rule is intimately connected to the rationale behind the construction and analysis of our estimators, on which we elaborate in Section II.

We also note that Table II is a “lossy compression” of Table I. Indeed, it did not reflect the important improvement of our estimator over the MLE in estimating . However, it is more transparent about the increase of difficulty in estimation when we decrease . Indeed, when , the sample complexity in estimating , becomes super-polynomial in , which implies that the problem has become extremely challenging. Indeed, the limiting case of corresponds to estimating the support size of a discrete distribution, which has long been known impossible to do consistently without additional assumptions [30][31].

I-C Discussion of main results

Within the scope of estimating entropy of discrete distributions from i.i.d. samples, the reader should be aware of different problem formulations, so as not to be confused by seemingly contradictory results. The problem we consider in this paper is to estimate the entropy for all possible distributions supported on elements, a setting for which we obtain Theorem 1. However, one may impose some additional structure on the distribution , and thus restrict attention to smaller uncertainty sets of distributions. One may expect different answers depending on the size and nature of the uncertainty sets. One of the popular alternative settings is to assume that the distribution comes from a uniform distribution with unknown support size . Note that it is a great simplification of the problem, indeed, there is only one parameter to estimate. Correspondingly, we only need samples to consistently estimate the support size, and the entropy under this setting [32], which is much smaller than the required samples in our setting, cf. Theorem 1.

Some readers may be concerned that the minimax decision theoretic framework we adopt is too pessimistic. In some sense, it characterizes the worst-case performance over all possible distributions , and it would be disappointing if our estimator fails to behave reasonably for distributions lying in a strict subset of not including the worst case distribution. Regarding this question, Brown [33, 34] argued that the minimax idea has been an essential foundation for advances in many areas of statistical research, including general asymptotic theory and methodology, hierarchical models, robust estimation, optimal design, and nonparametric function analysis. Second, the statistics community in general uses the adaptive estimation framework to alleviate the pessimism of minimaxity [35]. Specifically, one specifies a nested sequence of subsets of , and tries to construct an estimator that achieves simultaneously the minimax rates over each of the subsets without knowing the subset to which the active parameter actually belongs. It was shown recently in another related paper [36] that along the nested subsets , our estimator (without knowing nor ) simultaneously achieves the minimax rates over for all . Most surprisingly, the maximum risk of our estimator over for every and with samples is still essentially that of the MLE with samples, further reinforcing the effectiveness of our estimator.

It is instructive to consider our results in the context of the intriguing connections and differences between three important problems in information theory: entropy estimation, estimating a discrete distribution under relative entropy loss, and minimax redundancy in compressing i.i.d. sources. Table III summarizes the known results.

| entropy estimation | estimation of distribution | compression with blocklength | |

|---|---|---|---|

| [22] | [37, 38] | [39] | |

| large | [24] | [40] | [41, 42] |

Table III conveys several important messages. First, in the asymptotic regime, there is a logarithmic factor between the redundancy of the compression and distribution estimation problems. Indeed, since compression requires use of a coding distribution that does not depend on the data, the redundancy of compression will definitely be larger than the risk under relative entropy in estimating the distribution. However, in the large alphabet setting, the problems are equally difficult - the phase transition of vanishing risk for both compression and distribution estimation happen when is linear in the support size .

Second, the large alphabet setting shows that estimation of entropy is considerably easier than both estimating the corresponding distribution, and compression. It is somewhat surprising and enlightening, since there has been a well-received tradition to apply data compression techniques to estimate entropy, even beyond the information theory community, e.g. [43, 44], whereas one of the implications of Table III is that the approach of entropy estimation via compression can be highly sub-optimal.

If we plot the phase transitions of for estimating using with respect to , we obtain Figure 1.

We observe a sharp phase transition at , as the sample size requirement shifts from to , depending on whether is in the left or right neighborhood of 1, respectively. Hence, is a critical point in that consistent estimation requires a number of measurements super-linear or constant in the size of the alphabet according to whether or .

Combining Table III and Figure 1 leads to the interesting observation that, in high dimensional asymptotics, estimating a functional of a distribution could be easier (e.g. ) or harder (e.g. ) than estimating the distribution itself. This observation taps into another interesting interpretation of the functional . In information theory, the random variable is known as the information density, and plays important roles in characterizing higher order fundamental limits of coding problems [45, 46]. The functional can be interpreted as the moment generating function for random variable as

| (14) |

It is shown in Valiant and Valiant [24] that the distribution of can be estimated using samples. Since moment generating functions can determine the distribution under some conditions, it is indeed plausible to see that the problem of estimating , or the moment generating function of , is either easier or harder than estimating the distribution of itself for various values of .

We now briefly shift our focus towards estimation of Rényi entropy , which is closely related to the functional via . Acharya et al.[47] considered the estimation of , and demonstrated that the sample complexity for estimating may exhibit a different behavior than that of estimating for certain values of . It was also shown in [47] that for , the sample complexity is , which can be achieved by a bias-corrected MLE. Second, for non-integer , [47] showed that the sample complexity for estimating is between and , and that it suffices to take samples for the MLE to be consistent. By a partial application of results from the present paper, [47] also showed that for , the sample complexity for estimating is between and . However, certain questions remain unanswered. For example, it was not clear, for , whether the MLE indeed requires samples, and whether there exist estimators that can consistently estimate with samples. We provide partial answers to these questions below by focusing on the case when . First, we show in Theorem 5 that simply plugging in the novel estimator from Theorem 3 to the definition of results in an estimator that needs at most samples when .

Theorem 5.

In words, with high probability is close to the Rényi entropy provided . In contrast, the MLE requires samples for estimating , as is implied by the following theorem.

Theorem 6.

For any and any constant , there exist some such that the MLE satisfies

| (16) |

where is the MLE of .

To conclude this discussion, we conjecture that plugging in our minimax rate-optimal estimators for into the definition of results in minimax rate-optimal estimators for for all .

II Motivation, methodology, and related work

II-A Motivation

Existing theory proves inadequate for addressing the problem of estimating functionals of probability distributions. A natural estimator for functionals of the form (1) is the maximum likelihood estimator (MLE), or plug-in estimator, which simply evaluates , where is the empirical distribution of the data. How well does the MLE perform? Interestingly, if and we focus on i.i.d. observations from a distribution with support size , then the problem of estimating becomes a classical problem when is fixed, and the number of observations . This maximum likelihood estimator is asymptotically efficient [48, Thm. 8.11, Lemma 8.14] in the sense of the Hájek convolution theorem [49] and the Hájek–Le Cam local asymptotic minimax theorem [50]. It is therefore not surprising to encounter the following quote from the introduction of Wyner and Foster [51] who considered entropy estimation:

“The plug-in estimate is universal and optimal not only for finite alphabet i.i.d. sources but also for finite alphabet, finite memory sources. On the other hand, practically as well as theoretically, these problems are of little interest. ”

In light of this, is it fair to say that the entropy estimation problem is solved in the finite alphabet setting? It was observed in Paninski [52] that the maximum of over distributions with support size is of order (a tight bound is also given by Lemma 15 in the appendix). Since classical asymptotics (with the Delta method [48, Chap. 3]) show that

| (17) |

a naive interpretation of (17) might be that it suffices to take samples to guarantee the consistency of . Such an interpretation could however be very misleading. It was already observed in Paninski [52] that if , then the maximum risk of any entropy estimator would be unbounded as grows.

This apparent discrepancy shows that (17) is not valid when might be growing with , and it is of utmost importance to obtain risk bounds for estimators of entropy and other functionals of distributions in the latter regime. Indeed, in the modern era of high dimensional statistics, we often encounter situations where the support size is comparable to, or much larger than the number of observations. For example, half of the words in the collected works by Shakespeare appeared only once [30].

It was shown in the companion paper [29] that for , the maximum risk of the MLE can be written as

| (18) |

where the first term corresponds to the squared bias (defined as ), and the second term corresponds to the variance (defined as ). Then we can understand this mystery: when we fix and let , the variance dominates and we get the expression in (17). However, when and may grow together, the bias term will not vanish unless . Thus we conclude that in the large alphabet setting of entropy estimation, it is the bias that dominates the risk, and we have to reduce bias to improve the estimation accuracy.

The fact that the bias dominates the risk in entropy estimation in the large alphabet setting has been known, see [53, 52]. However, a general recipe to overcome the bias has defied many attempts. We briefly review some of the approaches in the literature.

One of the earliest investigations on reducing the bias of MLE in entropy estimation is due to Miller [53], who showed that, for any fixed distribution supported on elements, for each symbol , we have

| (19) |

Summing up both sides shows that is nearly up to the error term . Hence, the so-called Miller–Madow bias-corrected entropy estimator is defined by , whose maximum risk in estimating entropy was shown to be bounded from zero if by [52][29]. Thus, it still requires samples to consistently estimate the entropy, which is the same as MLE.

Another popular approach in estimating entropy is based on using the Dirichlet prior smoothing. Dirichlet smoothing may carry two different meanings in terms of entropy estimation:

- •

- •

It was shown in [58] that both approaches require at least to be consistent.

The jackknife [59] is another popular technique in reducing the bias. However, it was shown by Paninski [52] that the jackknifed MLE also requires samples to consistently estimate entropy.

Given the fact that is both necessary and sufficient, the approaches mentioned above are far from optimal. We note that the problem of estimating entropy of discrete distributions from i.i.d. observations on large alphabets has been investigated in various disciplines by many authors, with many approaches difficult to analyze theoretically. Among them we mention the Miller–Madow bias-corrected estimator and its variants [53, 60, 61], the jackknified estimator [62], the shrinkage estimator [63], the Bayes estimator under various priors [56, 64], the coverage adjusted estimator [65], the Best Upper Bound (BUB) estimator [52], the B-Splines estimator [66], and [67][68][69][70] etc.

In what follows, we explain in detail our step by step approach to this problem, and arrive at minimax rate-optimal estimators for the entire range of functional estimation problems considered.

II-B How did we come up with our scheme?

Existing literature implied that it is possible to come up with consistent entropy estimators that require sublinear samples. The earliest indication to this effect appeared in Paninski [28], but only an existential proof based on the Stone–Weierstrass theorem was provided. It was therefore a breakthrough when Valiant and Valiant [24] introduced the first explicit entropy estimator requiring a sublinear number of samples. They [24] showed that samples are both necessary and sufficient to consistently estimate the entropy of a discrete distribution. However, the entropy estimators based on linear programming proposed in Valiant and Valiant [24, 25] have not been shown to achieve the minimax rate. Another estimator proposed by Valiant and Valiant [26] has only been shown to achieve the minimax rate in the restrictive regime of . Moreover, the scheme of [24] can only be applied to functionals that are Lipschitz continuous with respect to a Wasserstein metric, which can be roughly understood as those functionals that are equally “smooth” or “smoother” than entropy. Notably, this does not include the functional and other interesting nonsmooth functionals of distributions. Also, it is not clear whether these techniques generally lead to minimax rate-optimal estimators. Readers are referred to Valiant’s thesis [71] for more details.

Conceivably, there is a fundamental connection between the smoothness of a functional, and the hardness of estimating it. The ideal solution to this problem would be systematic and capture this trade-off for nearly every functional. Such a comprehensive view of functional estimation has yet to be realized. George Pólya [72] commented that “the more general problem may be easier to solve than the special problem”. This motivated our present work, in which we provide a general framework and procedure for minimax estimation of functionals with non-asymptotic performance guarantees. To make things transparent, let us now start from scratch and demonstrate how our solution has a natural construction.

Suppose we would like to propose a general method to construct minimax rate-optimal estimators for functionals of the form (1). What are the prerequisites that any method must satisfy? Based on our analysis above, the following criteria appear natural:

-

1.

Asymptotic efficiency. As modern asymptotic statistics [48] tells us, if the function in (1) is differentiable on , then the MLE is asymptotically efficient. In other words, no matter how we adjust the MLE in finite sample settings, we have to ensure that when the number of samples go to infinity while remains fixed, our estimator is very similar to the MLE.

-

2.

Bias reduction. As our analysis of MLE [29] indicates, the MLE usually has large bias and small variance in high dimensions. Hence, the general method has to reduce bias in finite samples.

Let us attempt to understand an estimator’s bias more carefully. In the simplest setting, consider a Binomial random variable , and suppose we wish to estimate the scalar based on . Denote by an arbitrary estimator for . The bias of can be written as

| (20) |

Equation (20) conveys two important messages. First, the only form of that can be estimated without bias is polynomials with order no more than . Indeed, if is an unbiased estimator for , then , for all . Thus, is a polynomial of with order no more than because is such a polynomial. Conversely, any polynomial of whose order is no more than can be estimated without bias using . Indeed, for all ,

| (21) |

Second, the bias as a function of corresponds to a polynomial approximation error. In other words, it is the difference between a function and a polynomial . This viewpoint was first proposed by Paninski [52], who made the important connection between the analysis of bias and approximation theory. Starting from the seminal work of Chebyshev, a central problem in approximation theory [73], polynomial approximation, is targeted at designing polynomials that approximate any continuous function as well as possible. It then appears natural to choose the coefficients in a way that the resulting polynomial approximates the function optimally.

One may initially be tempted to use the Taylor series to approximate . However, a more careful inspection indicates that the Taylor polynomial is inappropriate for approximating general continuous functions. Even setting aside questions of convergence, Taylor polynomials are not defined for functions that are not infinitely differentiable. Even for functions that are analytic (such as ), one can show that truncating the Taylor series up to order results in maximum error on , but there exists a polynomial with order whose maximum approximation error is asymptotically [73], which is the so called best approximation polynomial. The best polynomial approximation is targeted at computing the polynomial that minimizes the maximum deviation of the polynomial from the function . It is known that for any continuous function on a compact interval, there exists a unique best approximation polynomial for any order. Adopting this rationale, we may try to solve the following problem:

| (22) |

where we seek minimizing the maximum value of . It gives us the best uniform control of the bias since we do not know a priori.

Applying advanced tools from approximation theory, Paninski [52] tried the idea mentioned above, which unfortunately did not result in improved estimators. It turns out that this idea, while improving significantly in the bias, results in a blowing up of the variance term. Indeed, the squared bias of the estimator designed above can be shown to be . Taking , the bias term will vanish, but the variance term will diverge, because Paninski [52] already showed that if , for any , the maximum risk of any estimators for entropy will be bounded from zero.

In fact, there is a simpler way to understand why the global scale polynomial approximation idea of the form (22) does not work. It is destined to fail because it violates the first prerequisite of any general method to improve MLE in functional estimation. Indeed, this scheme does not behave like the MLE even if .

This observation leads us to combine some core ideas that finally constitute our scheme. First, one needs to use approximation theory to reduce bias. Second, one cannot do approximation on a global scale (such as ), but can only approximate the function locally. Fortunately, the measure concentration phenomenon allows us to do approximation locally. For example, upon observing , we have , which vanishes as . Finally, where should we approximate? Intuitively, the bias is mainly due to the set of points where the function changes abruptly. For or , the most “nonsmooth” point is .

To sum up, we need to approximate locally around the “nonsmooth” points to reduce bias. Natural as this statement may seem, there are some parameters to be carefully specified. For this subsection we only consider or . We detail the construction of our scheme by posing the following natural questions:

-

1.

If we approximate function in interval , how should we choose ?

-

2.

If we use a polynomial with order to approximate in , how should we choose ? What should we do after obtaining the polynomial?

-

3.

What should we do in interval ?

Let us now answer these questions in the order in which they were asked. The value should always be chosen to be the smallest number such that we can localize the parameter . In other words, suppose we observe . Then, should be chosen to ensure that if , is a constant, then with high probability. Similarly, if , is a constant, then with high probability. It turns out that fulfills this goal (cf. Lemma 21).

Regarding the second question, the value should always be chosen to be the largest number such that the increased variance does not exceed the bias. Indeed, if we use order approximation, then we essentially go back to the idea (22) that increases the variance too much such that the resulting estimator does not have vanishing risk. It turns out for and , is the correct order for which we need to conduct the best polynomial approximation. Suppose we have obtained the best polynomial approximation of order for function over regime . Noting that any polynomial of order no more than can be estimated without bias using the estimator in (21), we use the corresponding unbiased estimator to estimate this -order polynomial, thereby ensuring that the bias of this estimator when is exactly the polynomial approximation error in approximating over .

The third question refers to the scheme in the “smooth” regime. Interestingly, it was already observed in 1969 by Carlton [60] that Miller’s bias correction formula (19) should only be applied when . In other words, Miller’s formula (19) is relatively accurate when . In our case, since we have already chosen , in the smooth regime we have . We use the first order bias-correction in this regime inspired by Miller, whose rationale is the following.

For Binomial random variable , denote the empirical frequency by . Then it follows from Taylor’s theorem that

| (23) | ||||

| (24) |

where is the second derivative of . We define the first order bias-corrected estimator of by

| (25) |

Taking , , which is exactly the Miller–Madow bias corrected entropy estimator. Taking , we have the corresponding bias corrected estimator

| (26) |

Figure 2 demonstrates the estimators for and pictorially, where is the empirical frequency of -th symbol. An important observation is that our estimator naturally satisfies the first prerequisite of any improved method for functional estimation as discussed above. Indeed, as , all the observations will fall in the “smooth” regime, and in the smooth regime our estimators are very similar to the MLE, which naturally implies that they are also asymptotically efficient in the sense of Hájek and Le Cam [48].

The idea of approximation in the context of estimation has appeared before. Nemirovski [74] pioneered the use of approximation theory in functional estimation in the Gaussian white noise model (see Nemirovski [75] for a comprehensive treatment). Later, Lepski, Nemirovski, and Spokoiny [76] considered estimating the norm of a regression function, and utilized trigonometric approximation. Cai and Low [77] used best polynomial approximation to estimate the norm of a Gaussian mean.

We conclude this subsection by comparing any minimax rate-optimal estimator with our estimator. If we consider entropy, Theorem 1 demonstrates that when is not too large, the risk is dominated by the first term , which corresponds to the squared bias of our estimator in the “nonsmooth” regime. Further, it is shown in Wu and Yang [27] that in the worst case, the risk contributed by the “nonsmooth” regime (i.e. ) is at least of order . These observations together imply that the gist of any successful scheme should contribute squared bias nearly . However, the bias always corresponds to a polynomial approximation error, and in the interval , it roughly corresponds to a polynomial with order . The squared bias corresponds to a polynomial whose error in approximating in is nearly the same as the best approximation polynomial with order . The theory of strong uniqueness in approximation theory [78] states that any polynomial whose approximation property is close to the best approximation must be close to the best approximation polynomial. Thus, we conclude that any successful scheme must inherently conduct near-best polynomial approximation in the “nonsmooth” regime, which is what we do in our scheme. Similar arguments also explain and Theorem 2, 3, and 4.

II-C Related work

The problem of estimating functionals of parameters is one that has been studied extensively in such fields as statistics, information theory, computer science, physics, neuroscience, psychology, and ecology, to name a few. Different communities have focused on different aspects of this general problem, and some seemingly different problems can be recast as functional estimation ones. Below we review some of the core ideas in various communities.

II-C1 Statistics

Consider a sequence of independent and identically distributed (i.i.d.) random variables taking values in , . We would like to obtain a good estimate of the functional . In general, this problem differs from that of seeking a good estimate of the parameter . The most natural and ambitious aim towards this problem is to seek the “optimal” estimator given exactly samples, which falls in the realm of finite sample theory in statistics [7]. There is no consensus on what criterion best evaluates how “good” an estimator is in a finite sample sense. Over the years, various criteria for goodness have been proposed and analyzed, including the uniform minimum variance unbiased estimator (UMVUE), the minimum risk equivariant estimator (MRE), and the minimax estimator, among others. However, generally it is difficult to obtain estimators for functionals satisfying any of the finite sample optimality criteria mentioned above. Further, even if we obtained an estimator that is or is close to being optimal for the parameter under a finite sample criterion, the plug-in approach need not result in an optimal estimator for under some finite sample criterion.

In light of these shortcomings, there seems to be a perception that estimation under finite sample optimality criteria is not amenable to a general mathematical theory [79]. Classical asymptotic theory is usually the refuge. The beautiful theory of Hájek and Le Cam [49, 50, 22] showed that, under mild conditions, there exist systematic methods to construct an asymptotically efficient estimator for the finite dimensional parameter , where if is differentiable at , is also asymptotically efficient for estimating [48, Lemma 8.14]. Furthermore, it is also known that if the functional is non-differentiable, then it is nearly impossible to get an elegant mathematical theory [80].

The question of estimating functionals of finite dimensional parameters being satisfactorily answered under classical asymptotics, functional estimation in various nonparametric settings has been a strong area of focus since. There are several profound contributions in this area, of which we only mention a few. The most developed theory deals with linear functionals, for example, see [81, 82, 83, 84, 79, 85, 86, 87, 88, 89, 90, 91, 92, 93, 94, 95, 96]. Another well studied situation deals with the case of “smooth” functionals, see [97, 98, 74, 99, 100, 101, 102, 103, 104, 105, 106, 107, 108], among others. Estimation of non-smooth functionals is an extremely difficult problem, and is still largely open [76]. In particular, the problem of estimating differential entropy , where is a density, remains fertile ground for research, cf. [109, 110, 111, 112, 113, 114, 115, 116, 117, 118, 119]. Similar situations are also true for estimating the entropy of a discrete distribution supported on a countably infinite alphabet, cf. [120, 51, 121, 122, 123].

II-C2 Information theory

In the information theory community, following the seminal work of Shannon [124], the focus has been on estimating entropy rates of general stationary ergodic processes with fixed (usually small) support (alphabet) sizes. Outside of the favored binary alphabet, printed English contributed the other interesting example of support size (including the “space”). Cover and King [125] gave an overview of the entropy rate estimation literature until 1978. Soon after the appearance of universal data compression algorithms proposed by Ziv and Lempel [126, 127], the information theory community started applying these ideas in entropy rate estimation, e.g. Wyner and Ziv [128], and Kontoyiannis et al. [129]. Verdú [130] provides an overview of universal estimation of information measures until 2005. Jiao et al. [131] constructed a general framework for applying data compression algorithms to establish near-optimal estimators for information rates, with a focus on directed information.

II-C3 Computer science, physics, neuroscience, psychology, ecology, etc

Much of the efforts in computer science, physics, neuroscience, psychology, ecology, and related fields have focused on some special functionals of particular interest. For example, the problem of estimating Shannon entropy from a finite alphabet source with i.i.d. observations has been investigated extensively. Section II-A and II-B summarize some of the efforts.

II-C4 Modern era: high dimensions and non-asymptotics

The current era of “big data” abounds with applications in which we no longer operate in the asymptotic regime of large sample sizes. This sample scarcity regime necessitates going beyond classical asymptotic analysis and considering finitely many samples in high dimensions. Indeed, the recent successes of finite-blocklength analysis in information theory [45], and compressed sensing in statistics [132, 133] have demonstrated the benefit of carefully analyzing practical sample sizes. There are also ample recent examples in statistics approaching classical questions from a high dimensional perspective, cf. [134, 135, 136, 137, 138]. The machine learning community has the tradition of favoring non-asymptotic analysis, and usually pose the question of the sample complexity for achieving accuracy with probability, cf. [139, 140, 141]. The information theoretic counterpart of high dimensional statistics might be the large alphabet setting, with exciting recent advances (cf. [142, 41, 143, 144, 42, 145]).

With the above as context, our work revisits the framework of functional estimation for finite dimensional models, with a focus on high dimensional and non-asymptotic analysis.

II-D General methodology for functional estimation

II-D1 Review: general methods of estimation

We begin by reviewing the existing general approaches to estimation. Maximum likelihood is the most widely used statistical estimation technique, which emerged in modern form 90 years ago in a series of remarkable papers by Fisher [146, 147, 148]. As evidence of its ubiquity, the Google Scholar search query “Maximum Likelihood Estimation” yields approximately articles, patents and books. Indeed, in his response to Berkson [149] in 1980, Efron explains the popularity of maximum likelihood:

“The appeal of maximum likelihood stems from its universal applicability, good mathematical properties, by which I refer to the standard asymptotic and exponential family results, and generally good track record as a tool in applied statistics, a record accumulated over fifty years of heavy usage. ”

Over the years, the following folk theorem seems to have been tacitly accepted by applied scientists:

Theorem 7 (“Folk Theorem”).

For a finite dimensional parametric estimation problem, it is “good” to employ the MLE.

From the perspective of mathematical statistics, however, maximum likelihood is by no means sacrosanct. As early as in 1930, in his letters to Fisher, Hotelling raised the possibility of the MLE performing poorly [150]. Subsequently, various examples showing that the performance of the MLE can be significantly improved upon have been proposed in the literature, cf. Le Cam [151] for an excellent overview. However, as Stigler [150, Sec. 12] discussed in his 2007 survey, while these early examples created a flurry of excitement, for the most part they were not seen as debilitating to the fundamental theory. Perhaps because these examples did not provide a systematic methodology for improving the MLE.

In 1956, Stein [152] observed that in the Gaussian location model (where is the identity matrix), the MLE for , is inadmissible [7, Chap. 1] when . Later, James and Stein [153] showed that an estimator that appropriately shrinks the MLE towards zero achieves uniformly lower risk compared to the risk of the MLE. The shrinkage idea underlying the James–Stein estimator has proven extremely fruitful for statistical methodology, and has motivated further milestone developments in statistics, such as wavelet shrinkage [154], and compressed sensing [132, 133].

One interpretation of the shrinkage idea is that, when one desires to estimate a high dimensional parameter, the MLE may have a relatively small bias compared to the variance. Shrinking the MLE introduces an additional bias, but reduces the overall risk by reducing the variance substantially. A natural question now arises: what about situations wherein the bias is the dominating term? Does there exist an analogous methodology for improving over the performance of the MLE in such scenarios? A precedent to this line of questioning can be found in the 1981 Wald Memorial Lecture by Efron [155] entitled “Maximum Likelihood and Decision Theory”:

“…the MLE can be non-optimal if the statistician has one specific estimation problem in mind. Arbitrarily bad counterexamples, along the line of estimating from , are easy to construct. Nevertheless the MLE has a good reputation, acquired over 60 years of heavy use, for producing reasonable point estimates. Useful general improvements on the MLE, such as robust estimation, and Stein estimation, are all the more impressive for their rarity. ”

For the aforementioned example, Efron [155] argued that the reason the MLE may not be a good estimate for , is that it has a large bias. In particular, the statistician may prefer the uniform minimum variance unbiased estimator (UMVUE), to estimate . As we discussed in the presentation of our main results, the bias is usually the dominating term in estimation of functionals of high-dimensional parameters. Notably, the two general improvements of the MLE, namely robust estimation and shrinkage estimation, are not designed to handle functional estimation problems such as the one presented by Efron. Also, as Efron himself observed, the statistician cannot always rely on the UMVUE to save the day, since these are generally very hard to compute, and may not always exist [155, Remark C, Sec. 7]. Thus, there is a need to address, both in scope and methodology, the improvement over the MLE for problems where the bias is the leading term. Such a solution could be considered the dual of the idea of shrinkage, since the trade-off between bias and variance is now reversed, i.e., one might want to sacrifice the variance to reduce the bias.

II-D2 Approximation: dual of shrinkage

Our main results in this paper imply that Theorem 7 is far from true in high-dimensional non-asymptotic settings. Now, we aim to abstract our scheme in estimating functionals of type (1), and distill a general methodology for estimating functionals of parameters of any finite dimensional parametric families.

Consider estimating of a parameter for an experiment , with a consistent estimator for , where is the number of observations. Suppose the functional is analytic222A function is analytic at a point if and only if its Taylor series about converges to in some neighborhood of . everywhere except at . A natural estimator for is , and we know from classical asymptotics [48, Lemma 8.14] that if the model satisfies the benign LAN (Local Asymptotic Normality) condition [48] and is asymptotically efficient for , then is also asymptotically efficient for for . Note that this general framework naturally encompasses the family of probability functionals as a special case. To see this, let be the -dimensional probability simplex, where denotes the support size. For functionals of the form (1), if is analytic on , it is clear that denotes the boundary of the probability simplex. One natural candidate for is the empirical distribution, which is an unbiased estimator for any .

We propose to conduct the following two-step procedure in estimating .

-

1.

Classify Regime: Compute , and declare that we are operating in the “nonsmooth” regime if is “close” enough to . Note that is not analytic at any . Otherwise declare we are in the “smooth” regime;

-

2.

Estimate:

-

•

If falls in the “smooth” regime, use an estimator “similar” to to estimate ;

-

•

If falls in the “nonsmooth” regime, replace the functional in the “nonsmooth” regime by an approximation (another functional) which can be estimated without bias, then apply an unbiased estimator for the functional .

-

•

II-D3 Details of “Approximation”

While this general recipe appears clean in its description, there are several problem-dependent features that one needs to design carefully – namely

Question 1.

How to determine “nonsmooth” regime? What is the size of it?

Question 2.

What approximation should we choose to approximate in the “nonsmooth” regime?

Question 3.

What does “ ‘similar’ to ” mean precisely? What exactly do we do in the “smooth” regime?

The careful reader may have realized that Questions 1,2, and 3 resemble the questions we asked in Section II-B. Answers to these questions draw on additional problems we investigated [156] beyond these in the present paper.

-

1.

Question 1

We should always choose the “nonsmooth” regime to be the smallest regime such that we can still localize the parameter . In other words, when we observe in the “nonsmooth” regime, we should be able to infer with high probability that is also in the “nonsmooth” regime. Similarly, we should also be able to localize the parameter in the “smooth” regime. A concrete case would be the following. Say we observe , and we would like to estimate a functional which is not analytic at . How should we define the “nonsmooth” regime? Noting that , it turns out we can set the “nonsmooth” regime to be (cf. Lemma 21).

-

2.

Question 2

We should always choose an approximation that can be estimated without bias. This requirement leads us to the general theory of unbiased estimation, which was pioneered by Halmos [157] and Kolmogorov [158]. For a comprehensive survey the readers are referred to the monograph by Voinov and Nikulin [159].

There is a delicate trade-off: the approximation should be estimated without bias, but also should approximate the functional well, and at the same time not incur too much additional variance. These three requirements yield a highly non-trivial interplay between approximation theory and statistics, of which our understanding is as yet incomplete.

For functionals in (1), the separability of each essentially reduces the problem from multivariate to univariate, for which best polynomial approximation plays an important role in the optimal solution. Similar stories are true for the Gaussian setting, e.g. estimating where is the mean of a normal vector. Modern approximation theory provides mature machinery of polynomial approximation in one dimension, with various profound results developed over the last century. The best approximation error rate :

(27) where is the collection of polynomials with order at most on , is a crucial object in approximation theory as well as our general methodology. Quantifying and obtaining the polynomial that achieves it turned out to be extremely challenging. Remez [160] in 1934 proposed an efficient algorithm for computing the best polynomial approximation, and it was recently implemented and highly optimized in Matlab by the Chebfun team [161, 162]. Regarding the theoretical understanding of , de la Vallée-Poussin, Bernstein, Ibragimov, Markov, Kolmogorov and others have made significant contributions, and it is still an active research area. Among others, Bernstein [163, 164] and Ibragimov [165] showed various exact limiting results for some important classes of functions like and . For example, we have

Theorem 8.

[164] The following limit exists for all :

(28) where is a constant bounded as

(29) where denotes the Gamma function.

Regarding bounds on for any finite , Korneichuk [166, Chap. 6] provides a comprehensive study. For a comprehensive treatment of modern approximation theory, DeVore and Lorentz [73], Ditzian and Totik [167] provide excellent references. For the most up-to-date review of polynomial approximation, we refer the readers to Bustamante [168].

We emphasize that the discussions above refer to approximation in dimension one. The general multivariate case is extremely complicated. Rice [169] wrote:

“The theory of Chebyshev approximation (a.k.a. best approximation) for functions of one real variable has been understood for some time and is quite elegant. For about fifty years attempts have been made to generalize this theory to functions of several variables. These attempts have failed because of the lack of uniqueness of best approximations to functions of more than one variable. ”

Another related paper [156] showed that the non-uniqueness can cause serious trouble: some polynomial that can achieve the best approximation error rate cannot be used in our general methodology in functional estimation. What if we relax the requirement of computing the best approximation in multivariate case, and only want to analyze the best approximation rate (i.e., the best approximation error up to a multiplicative constant)? That turns out also to be extremely difficult. Ditzian and Totik [167, Chap. 12] obtained the error rate estimate on simple polytopes333A simple polytope in is a polytope such that each vertex has edges. , balls, and spheres, and it remained open until Totik [170] generalized the results to general polytopes. For results in balls and spheres, the readers are referred to Dai and Xu [171]. We still know little about regimes other than polytopes, balls, and spheres.

We do not know whether in general polynomial approximation can achieve the minimax rates in general settings. Probably other approximation bases need be chosen for certain problems.

-

3.

Question 3

Note that we have assumed is analytic in the “smooth” regime. For various statistical models (like Gaussian and Poisson), any analytic functional admits unbiased estimators. We propose to use Taylor series bias correction [172] in the “smooth” regime, where the order of the Taylor series may vary between problems.

II-E Remaining content

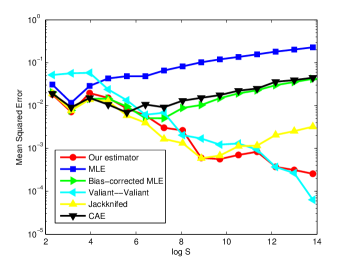

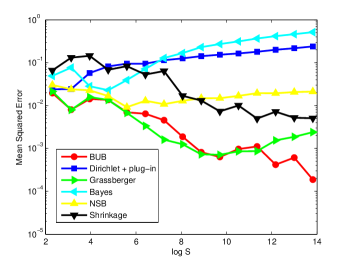

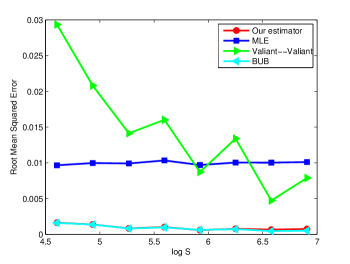

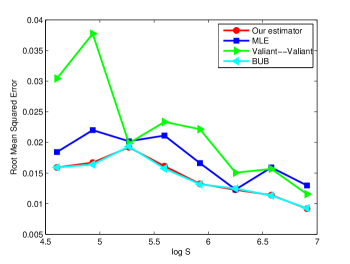

The rest of the paper is organized as follows. Section III details the construction of our estimators and and their analysis. In Section IV we present our general approach for proving minimax lower bounds and apply it to establish Theorems 2 and 4. Section V presents a few experiments demonstrating the practical advantages of our estimators in entropy estimation, mutual information estimation, entropy rate estimation, and learning graphical models. Complete proofs of the remaining theorems and lemmas are provided in the appendices.

III Estimator construction and analysis

Throughout our analysis, we utilize the Poisson sampling model, which is equivalent to having a -dimensional random vector such that each component in has distribution , and all coordinates of are independent. For simplicity of analysis, we conduct the classical “splitting” operation [173] on the Poisson random vector , and obtain two independent identically distributed random vectors , such that each component in has distribution , and all coordinates in are independent. For each coordinate , the splitting process generates a random variable such that , and assign . All the random variables are conditionally independent given our observation .

For simplicity, we re-define as , and denote

| (30) |

where are positive constants to be specified later. For simplicity we assume is always a non-negative integer. Note that are functions of , where we omit the subscript for brevity. We remark that the “splitting” operation is used to simplify the analysis, and is not performed in the experiments. We also note that for random variable such that ,

| (31) |

for any . For a proof of this fact we refer the readers to Withers [172, Example 2.8].

III-A Estimator construction

Our estimator , is constructed as follows.

| (32) |

where

| (33) | ||||

| (34) | ||||

| (35) |

We explain each equation in detail as follows.

-

1.

Equation (32):

Note that and are i.i.d. random variables such that . We use to determine whether we are operating in the “nonsmooth” regime or not. If , we declare we are in the “nonsmooth” regime, and plug in into function . If , we declare we are in the “smooth” regime, and plug in into .

-

2.

Equation (33):

The coefficients are coefficients of the best polynomial approximation of over up to degree , i.e.,

(36) where denotes the set of algebraic polynomials up to order . Note that in general depends on , which we do not make explicit for brevity. Lemma 4 shows that for ,

(37) Thus, we can understand as a random variable whose expectation is nearly 444Note that we have removed the constant term from the best polynomial approximation. It is to ensure that we assign zero to symbols we do not see. the best approximation of function over .

-

3.

Equation (34):

Any reasonable estimator for should be upper bounded by the value one. We cut off by upper bound , and define the function , which means “lower part”.

-

4.

Equation (35):

The function (standing for “upper part”) is nothing but a product of an interpolation function 555The usage of the interpolation function was partially inspired by Valiant and Valiant [26]. and the bias-corrected MLE. The careful reader may note that the bias-corrected MLE is not exactly the same as what we used before in (25). It is because here we are using the Poisson model instead of the Multinomial model. In the Poisson model, the bias correction formula should be modified to

(38) The interpolation function is designed to make a smooth function on . Indeed, when , were it not for the interpolation function, would be unbounded for close to zero. Note that and are dependent on . We omit this dependence in notation for brevity. The interpolation function is defined as follows:

(39) The following lemma characterizes the properties of the function appearing in the definition of . In particular, it shows that is four times continuously differentiable.

Lemma 1.

For the function on defined as follows,

(40) we have the following properties:

(41) (42) The function is depicted in Figure 3.

![[Uncaptioned image]](/html/1406.6956/assets/x1.png)

Figure 3: The function over interval .

Similarly, we define our estimator for entropy as

| (43) |

where

| (44) | ||||

| (45) | ||||

| (46) |

The coefficients are defined as follows. We first define

| (47) |

and then define

| (48) |

Figure 4 is designed to provide pictorial explanation of our scheme in the “nonsmooth” regime for entropy estimation. The curve is the functional we want to estimate, and the horizontal axis represents the possible values of . We take , and use a -order best polynomial approximation for function over regime . It is evident from the curve that the expectation is very close to the true function , but the expectation of the MLE , and the function itself are both far from . It demonstrates the nuanced nature of our scheme: we first construct a polynomial (equal to ) that approximates the function very well, then we design the function to make sure its expectation is the good approximation. Plugging in may seem less sensible than plugging into at first glance, but Figure 4 vividly demonstrates that in fact plugging into is far more accurate in estimating .

![[Uncaptioned image]](/html/1406.6956/assets/x2.png)

III-B Estimator analysis

We demonstrate our analysis techniques via the proof of Theorem 2 and 3, and note that similar techniques allow us to establish Theorem 1.

The next two lemmas show that the estimators have desirable bias and variance properties when the true probability is not too small.

Lemma 2.

Suppose . For , we have

| (50) |

For ,

| (51) |

For ,

| (52) |

For ,

| (53) |

Lemma 3.

If ,

| (54) |

| (55) |

The following two lemmas characterize the performance of and when is not too large.

Lemma 4.

If , we have

| (56) |

and for large enough, we can take , where is the constant appearing in Lemma 19. If we also have , then

| (57) |

For the entropy, if , we have

| (58) |

When is large enough, can be taken to be , which is given in Lemma 20. If we also have , then

| (59) |

Lemma 5.

With the machinery established in Lemma 2, 3, 4, and 5, we are now ready to bound the bias and variance of each summand in our estimators. Define,

| (62) |

where , and is independent of . Apparently, we have

| (63) |

and each of the summands are independent. Hence, it suffices to analyze the bias and variance of thoroughly for all values of in order to obtain a risk bound for . We break this into three different regimes. In the first case when , we shall show that the estimator essentially behaves like , which is a good estimator when is small. In the second case when , we show that our estimator uses either or , which are both good estimators in this case. In the last case , we show that our estimator behaves essentially like , which has good properties when is not too small.

We denote as the bias of .

Lemma 6.

Suppose , . Then,

-

1.

when ,

(64) (65) -

2.

when ,

(66) (67) -

3.

when ,

(68) (69)

Now the result of Theorem 2 follows easily from Lemma 6. We have

| (70) | ||||

| (71) | ||||

| (72) |

and

| (73) | ||||

| (74) | ||||

| (75) | ||||

| (76) |

Here we have used the fact that

| (77) |

since is a concave function when .

Combining the bias and variance bounds, we have

| (78) | |||

| (79) |

where is a constant that is arbitrarily small. Note that when , we can remove the middle term in the risk bound, since when , the first term dominates, otherwise the third term dominates.

The proof of Theorem 1 is essentially the same as that for Theorem 2, with the only differences being replacing Lemma 2 with Lemma 3, applying the entropy part of Lemma 4 and Lemma 15. The proof of Theorem 3 is slightly more involved, and we need to split the analysis into four different regimes.

Lemma 7.

Suppose . Setting , we have the following bounds on and .

-

1.

when ,

(80) (81) -

2.

when ,

(82) (83) -

3.

when ,

(84) (85)

Now the result of Theorem 3 follows easily from Lemma 7. First, the total bias can be bounded by

| (86) | ||||

| (87) | ||||

| (88) | ||||

| (89) | ||||

| (90) |

Second, the total variance is bounded by

| (91) | ||||

| (92) | ||||

| (93) | ||||

| (94) | ||||

| (95) | ||||

| (96) |

IV Minimax lower bounds for estimating

There are two main lemmas that we employ towards the proof of the minimax lower bounds in Theorem 2 and 4. The first lemma is the Le Cam two-point method. Suppose we observe a random vector which has distribution where . Let and be two elements of . Let be an arbitrary estimator of a function based on . Le Cam’s two-point method gives the following general minimax lower bound.

Lemma 8.

The second lemma is the so-called method of two fuzzy hypotheses presented in Tsybakov [174]. Suppose we observe a random vector which has distribution where . Let and be two prior distributions supported on . Write for the marginal distribution of when the prior is for . Let be an arbitrary estimator of a function based on . We have the following general minimax lower bound.

Lemma 9.

[174, Thm. 2.15] Given the setting above, suppose there exist such that

| (101) | ||||

| (102) |

If , then

| (103) |

where are the marginal distributions of when the priors are , respectively.

Here is the total variation distance between two probability measures on the measurable space . Concretely, we have

| (104) |

where , and is a dominating measure so that .

IV-A Minimax lower bound for Theorem 2 ()

Note that the minimax lower bound in Theorem 2 consists of two parts when . Hence, for , it suffices to first show that

| (105) |

and then show

| (106) |

in order to obtain the desired conclusion via the relation .

Regarding (105), we have the following theorem.

Theorem 9.

For , we have

| (107) |

where the infimum is taken over all possible estimators .

Proof.

Applying this lemma to our Poissonized model , we know that for ,

| (108) | |||

| (109) | |||

| (110) | |||

| (111) |

then Markov’s inequality yields

| (112) | |||

| (113) | |||

| (114) |

where we are operating under the Poissonized model.

Fix to be specified later. Letting

| (115) | ||||

| (116) |

direct computation yields

| (117) | ||||

| (118) |

and

| (119) | |||

| (120) | |||

| (121) |

Hence, by choosing , we know that

| (122) |

under the Poissonized model. Applying Lemma 16, we know that under the Multinomial model, the non-asymptotic minimax lower bound is

| (123) |

The proof is complete. ∎

Now we start the proof of (106) in earnest. For , (106) follows directly from (105) if , or equivalently, . Hence, we only need to consider the case where , which implies that . Since the condition is also treated as an assumption in Theorem 2 for , we adopt it throughout the following proof.

We construct the two fuzzy hypotheses required by Lemma 9. Similar construction was applied in proving minimax lower bounds in [76] and [77].

Lemma 10.

For any given positive integer , there exist two probability measures and on that satisfy the following conditions:

-

1.

, for ;

-

2.

,

where is the distance in the uniform norm on from the function to the space of polynomials of no more than degree .

The two probability measures and can be understood as the solution to the optimization problem of maximizing , with the constraint that , for , . Wu and Yang [27] gave an explicit construction of the measures and from the solution of the best polynomial approximation problem for general functions on an interval. In some sense, the two probability measures and are chosen to be those that differ the most in terms of the expectations of the functions we care about (here is ), with the same moments up to a certain order. Hence, they are difficult to distinguish via samples, but the corresponding functional values are maximally apart from each other.

According to Lemma 17, we have

| (124) |

Since we have assumed and , we represent

| (125) |

for some constant , which implies that

| (126) |

Note that

| (127) |

Define

| (128) |

where are positive constants (not depending on ) that will be determined later. Without loss of generality we assume that is always a positive integer.

For a given integer , let and be the two probability measures possessing the properties given in Lemma 10. Let and let be the measures on defined by for . It follows from Lemma 10 that:

-

1.

, for ;

-

2.

.

Let and be the product priors . We assign these priors to the length- vector . Under or , we have almost surely

| (129) |

hence

| (130) |

We decompose as

| (131) |

where

| (132) |

We argue that it suffices to show the minimax lower bound in Theorem 2 holds when we replace by . Indeed, we just showed that

| (133) | ||||

| (134) | ||||

| (135) |

Hence, if there exists an estimator that violates the minimax lower bound for in Theorem 2, then will violates the same minimax lower for estimating , which will contradict what we show below.

For , we denote the marginal distribution of by , whose pmf can be computed as

| (136) |

We define in a similar fashion.

Lemma 11.

The following bounds are true if :

| (137) | ||||

| (138) | ||||

| (139) | ||||

| (140) | ||||

| (141) | ||||

| (142) |

Setting

in Lemma 9, it follows from Chebyshev’s inequality and that

| (143) | ||||

| (144) | ||||

| (145) | ||||

| (146) |

and

| (147) | ||||

| (148) | ||||

| (149) | ||||

| (150) |

Also, it follows from the general fact that (which follows easily from a coupling argument [175]) that

| (151) |

Applying Lemma 9, we have

| (152) |

According to Markov’s inequality, we have

| (153) |

IV-B Minimax lower bound for Theorem 4 ()

First we assume that . Similar to Lemma 10, we construct two measures as follows for .

Lemma 12.

For any and positive integer , there exist two probability measures and on such that

-

1.

, for all ;

-

2.

,

where is the distance in the uniform norm on from the function to the space spanned by .

Based on Lemma 12, two new measures can be constructed as follows: for , the restriction of on is absolutely continuous with respect to , with the Radon-Nikodym derivative given by

| (154) |

and . Hence, are both probability measures on , with the following properties

-

1.

;

-

2.

, for all ;

-

3.

.

The construction of measures are inspired by Wu and Yang [27].

The following lemma characterizes the properties of using well-developed tools from approximation theory [167]. Similar results can be found in Wu and Yang [27] in which they treated the logarithmic function.

Lemma 13.

For , there exists a universal positive constant such that

| (155) |

Define

| (156) |

with universal positive constants to be determined later. Without loss of generality we assume that is always a positive integer. By the choice of we know that

| (157) |

Let and let be the measures on defined by for . It then follows that

-

1.

;

-

2.

, for all ;

-

3.

.

Let and be product priors which we assign to the length- vector . Note that may not be a probability distribution, we consider the set of approximate probability vectors

| (158) |

with universal constant to be specified later, and further define the minimax risk under the Poissonized model for estimating with as

| (159) |

The equivalence of the minimax risk under the Multinomial model (defined in (202)) and is established in the following lemma.

Lemma 14.

For any , we have

| (160) |

In light of Lemma 14, it suffices to consider to give a lower bound of . Denote

| (161) | ||||

| (162) | ||||

| (163) |

and

| (164) |

Applying Chebyshev’s inequality and the union bound yields that

| (165) | ||||

| (166) | ||||

| (167) | ||||

| (168) | ||||

| (169) |

where (169) follows from (157). Denote by the conditional distribution defined as

| (170) |

Now consider as two priors and as the corresponding marginal distributions. Setting

| (171) | ||||

| (172) | ||||

| (173) | ||||

| (174) | ||||

| (175) |

we have . The total variational distance is then upper bounded by

| (176) | ||||

| (177) | ||||

| (178) | ||||

| (179) |