Change of numeraire in the two-marginals

martingale transport problem††thanks: This work is partially supported by the ANR project ISOTACE (ANR-12-MONU-0013). We would like to thank Robert Dalang for the support. We are also grateful to Stefano De Marco, Pierre Henry-Labordère, David Hobson and Antoine Jacquier for their helpful remarks

Abstract

In this paper we apply change of numeraire techniques to the optimal transport approach for computing model-free prices of derivatives in a two periods model. In particular, we consider the optimal transport plan constructed in Hobson and Klimmek [2015] as well as the one introduced in Beiglböck and Juillet [2012] and further studied in Henry-Labordère and Touzi [2013]. We show that, in the case of positive martingales, a suitable change of numeraire applied to Hobson and Klimmek [2015] exchanges forward start straddles of type I and type II, so that the optimal transport plan in the subhedging problems is the same for both types of options. Moreover, for Henry-Labordère and Touzi [2013]’s construction, the right monotone transference plan can be viewed as a mirror coupling of its left counterpart under the change of numeraire. An application to stochastic volatility models is also provided.

Keywords and phrases: robust hedging, model-independent pricing, model uncertainty, optimal transport, change of numeraire, forward start straddle.

JEL Classification: C61, G11, G13.

MSC Classification 2010: 91G20, 91G80.

1 Introduction

Let and be two probability measures on the positive half-line , both with unit mean and satisfying in the sense of the convex order, i.e. for all convex functions . A classical theorem by Strassen [1965] shows the existence of a discrete time martingale with and . Let denote the set of all possible laws for such discrete martingales with pre-specified marginals , . If we interpret the process as a price of a given stock, any function can be seen as a path-dependent option written on that stock.

Motivated by the issue of model uncertainty, there has recently been a flourishing of articles on the problem of finding a model-free upper (resp. lower) bound for the price of a given option , which consists in maximizing (resp. minimizing) the expectation with respect to all measures . Indeed, any such measure corresponds to some model for the price of the underlying. In the model-free setting such a price is requested to be a martingale (hence free of arbitrage) and to have pre-specified marginals and , which can be deduced as usual from the observation of European Call option prices via the Breeden-Litzenberger formula. Therefore, is the set of natural pricing measures in this context.

The upper bound , for instance, corresponds essentially to the cost of the least expensive semi-static strategy that super-replicates the given payoff. The lower bound has an analogue interpretation as sub-replication price. These optimization problems have been recently tackled using an approach based on optimal transport. In this respect, Beiglböck and Juillet [2012] perform a thorough analysis of martingale transport problems and, among other results, prove that for a certain class of payoffs the optimal probabilities are of special type, called the left-monotone and right-monotone transference plans. Later on, Henry-Labordère and Touzi [2013] provide an explicit construction of such optimal transference plans for a more general class of payoffs that satisfy the so-called generalized Spence-Mirrlees condition:

| (1.1) |

Finally, Hobson and Klimmek [2015] construct another optimal transference plan giving the model-free sub-replication price of a forward start straddle of type II, whose payoff does not satisfy the condition (1.1) above.

In this paper we study the effect of change of numeraire on the martingale optimal transport approach to model-free pricing. To our knowledge, change of numeraire has never been used so far in connection to optimal transport and robust pricing. We will focus on the optimal transference plans mentioned above in the case of marginals whose support is , i.e. we will consider positive martingales with given marginals. Our main results can be briefly stated as follows: regarding Hobson and Klimmek [2015] optimal coupling measure, it turns out that the change of numeraire exchanges forward start straddles of type I and type II with strike , where the payoff of a forward start straddle of type I is given by . As consequence, this yields that the optimal transport plan in the subhedging problems is the same for both types of forward start straddles. This complements, using a different method, the results in Hobson and Klimmek [2015] on forward start straddles of type II. On the other hand, regarding Beiglböck and Juillet [2012] and Henry-Labordère and Touzi [2013] left and right monotone optimal transport plans, the change of numeraire can be viewed as a mirror coupling for positive martingales. More precisely, we will show that the right monotone transport plan can be obtained with no effort from its left monotone counterpart by suitably changing numeraire. The effect of such a transformation on the generalized Spence-Mirrlees condition is also studied. Other invariance properties by change of numeraire will also be proved along the way. An extended version of the present paper can be found in Laachir [2015] PhD thesis.

The paper is structured as follows. We introduce in Section 2 the change of numeraire and prove its main properties. In Section 3 we consider forward start straddles and extend the results in Hobson and Klimmek [2015] to forward start straddles of type I. In Section 4, we give an application of change of numeraire to left and right monotone transference plans for positive martingales. In the last Section 5, we study the symmetric case where and are invariant by change of numeraire. This case includes the Black-Scholes model and the stochastic volatility models with no correlation between the spot and the volatility (cf. Renault and Touzi [1996]).

Notations:

-

•

Let be any random variable defined on some measurable space . We denote by the law of under some measure . For the expectation of under we indifferently use the notation or .

-

•

We denote by the set of all probability measures on , equipped with the Borel -field , and set

The subset of all measures having a positive density, say , with respect to the Lebesgue measure, is denoted by .

-

•

If , then denote their respective cumulative distribution functions. We also use the notation for the difference between the two, i.e.

-

•

For any function we use the notation , and for the cumulated expectation of any measure . Finally denotes the identity function.

2 Change of numeraire

The technique of change of numeraire was first introduced by Jamshidian [1989] in the context of interest rate models and turned out to be a very powerful tool in derivatives pricing (see Geman et al. [1995], [Jeanblanc et al., 2009, Section 2.4] and the other references therein for further details). Here we see that such techniques can be fruitfully transposed to a model-free setting.

We consider a two-period financial market with one riskless asset, whose price is identically equal to one, and one risky asset whose discounted price evolution is modelled by the process . The random variables and , modelling respectively the prices at time and , are defined on the canonical measurable space , where with and . For any , we set and . The final ingredients of our setting are the two marginals laws and , which are probability measures on, respectively, and , so that (resp. ) has law (resp. ). Throughout the whole paper, we will work under the following standing assumption:

Assumption 2.1.

The marginals and have unit mean and satisfy in the sense of the convex order, i.e. for all convex functions .

Let denote the set of all probability measures on such that , , and is a martingale. As we already claimed in the introduction, by a classical theorem in Strassen [1965], we know that the previous assumption guarantees that such a set is non-empty.

2.1 The one-dimensional symmetry operator

As a preliminary step, we first consider the change of numeraire in a static setting, i.e. for the marginal laws. Thus, we define the (marginal) symmetry operator as an operator acting on the space of probability measures on given by

| (2.2) |

where is the probability measure defined by , for any .

Remark 2.2.

Financially speaking, is the law of the riskless asset price at time measured in units of the risky one under the new probability . This is the usual change of measure associated to a change of numeraire. An analogue interpretation applies to .

Notice that if , i.e. it has unit mean, then too, since . In the case where with density , the new measure has a density too and this is given by

| (2.3) |

hence in particular we have . Moreover, is an involution, i.e. . Indeed, we have

for all bounded measurable functions . For future reference we summarize our findings in the following lemma, which also contains few more properties, such as the fact that the operator preserves the convex order.

Lemma 2.3.

Proof.

To prove property 1 it suffices to show that preserves the convex order of measures. Let such that for any convex function , . Since and have both unit mass and the same first moment, it is enough to show that for any positive constants we have

Now , and the same holds true for . Since is a convex function, the result follows. Property 2 has already been proved above, so it remains to show property 3. We show only the left-hand side equality, the same arguments can be applied to get the other one. By the definition of we have

Hence, the proof is complete. ∎

2.2 The symmetric two-marginals martingale problem

In this subsection, we consider the change of numeraire in the two-period setting. Let be the operator that assigns to every the measure defined by

| (2.4) |

Lemma 2.4.

The operator satisfies the following properties:

-

1.

is a probability in and it satisfies , i.e. is an involution.

-

2.

.

Proof.

-

1.

First, let us prove that for . The fact that has law under follows from the definition of . Regarding , by the martingale property under , we have

for all bounded measurable functions depending only on . Hence we conclude since has law under . It remains to show the martingale property:

Now by the martingale property under we obtain , which implies . The fact that is an involution follows immediately from its definition.

-

2.

In order to prove that , we note that one inclusion is implied by the property 1 in this proposition. The other inclusion is a consequence of the fact that the symmetry operator is an involution.

∎

Remark 2.5.

Notice that the symmetry operator can be seen as the projection of . Indeed, let . For any bounded measurable function , we have , where the second equality is due to the martingale property. Hence the projection of into the first coordinate of the product space equals . Similarly one can see that the projection of onto the second coordinate is .

Let be any continuous function with linear growth, i.e. for some constant . The lower and upper model-free price bounds for such a derivative can be computed by solving the following martingale optimal transport problems:

| (2.5) |

They have the interpretation of sub and super-replication prices of the payoff through a duality theory that has been developed during the last few years by several authors (see Remark 5.4).

The following proposition shows the symmetry properties of such model-free bounds with respect to the change of numeraire transformation.

Proposition 2.6.

Let us define the payoff for . Then

| (2.6) |

Proof.

We only prove the equality for , the one for can be shown using the same arguments. By the definition of we have

Using property 2 in Lemma 2.4 and the definition of , we get

which gives the result. ∎

We conclude this section by showing how the symmetry operator introduced in Proposition 2.6 acts on the space of hedgeable claims, which we define as

This set contains all the payoffs that can be replicated by investing semi-statically in the stock as well as in Vanilla options. It turns out that this set is invariant by the symmetry operator or, in other words, the set of semi-static portfolios does not depend on the choice of the numeraire.

Proposition 2.7.

The set is invariant by , i.e. .

Proof.

Let , i.e. there exist functions such that

Let for all and let

Such functions verify . We can check by direct computation that

Furthermore, since , we have the following equivalences:

Hence

i.e. . ∎

3 Model-free pricing of forward start straddles

In this section we apply our results on the change of numeraire to compute the model-free sub-replication price of a forward start straddle of type I, which complements the result obtained in Hobson and Klimmek [2015].

In their article Hobson and Klimmek [2015] consider the problem of computing a model-free lower bound on the price of an option paying at maturity. This is an example of type II forward start straddle, whose payoff for any strike is given by

| (3.7) |

while the type I forward start straddle with strike is given by

| (3.8) |

cf. Lucic [2003] and Jacquier and Roome [2015]. Hobson and Klimmek [2015] derive explicit expressions for the coupling minimizing the model-free price of an at-the-money (ATM) type II forward start straddle as well as for the corresponding sub-hedging strategy. In particular, they show that the optimal martingale coupling for such a derivative is concentrated on a three points transition where and are two suitable decreasing functions. The precise result will be recalled below. Such a characterization is obtained under a dispersion assumption [Hobson and Klimmek, 2015, Assumption 2.1] on the supports of the marginal laws: the support of is contained in a finite interval and the support of is contained in its complement . Instead of working under such a condition on the supports, we would rather impose the following standing assumption.

Assumption 3.1.

Let the following properties hold:

-

(i)

The measures and belong to ;

-

(ii)

has a single local maximizer .

The main reason for working under this assumption in the rest of the paper is twofold: first, it makes our treatment more uniform, since later we will consider Henry-Labordère and Touzi [2013] construction of the right and left monotone transference plans and their construction holds if the marginals are absolutely continuous, whence our Assumption 3.1(i). Moreover, in the case of marginals with densities, Assumption 3.1(ii) is equivalent to the dispersion assumption in Hobson and Klimmek [2015] (as we show in Remark 3.2 below) and it simplifies the study of Henry-Labordère and Touzi [2013] construction in the next section.

Remark 3.2.

Let with . Then Assumption 2.1 in Hobson and Klimmek [2015] is equivalent to our Assumption 3.1(ii). To see this, let with . First, observe that

where denotes the closure of any subset . Suppose that Assumption 2.1 in Hobson and Klimmek [2015] holds, i.e. there exist constants such that

Consequently, is decreasing on and increasing on and . Hence it admits a unique maximizer at and a unique minimizer at , whence Assumption 3.1 follows. Conversely, suppose that Assumption 3.1 holds. Then admits a global maximum in . Moreover, by the convex order of and , admits a global minimum at . Hence, for all we have , while for all we have , and finally Assumption 2.1 in Hobson and Klimmek [2015] is fulfilled.

Remark 3.3.

Let us come back to the model-free pricing of forward start straddles. Given the form of the payoff (3.8), it is very natural to try to obtain an optimal martingale coupling for its model-free sub-hedging price combining the change of numeraire techniques with Hobson and Klimmek [2015] results. For reader’s convenience, we summarize their main result in the following theorem. It is a consequence of Theorem 5.4 and Theorem 5.5 in Hobson and Klimmek [2015] applied to the particular case when the marginals have densities (see their Subsection 6.1). Therefore, its proof is omitted.

Theorem 3.4.

Let Assumption 3.1 hold. Then there exists a unique optimal coupling such that

| (3.9) |

Moreover, , with a transition kernel given by

| (3.10) |

where:

-

1.

(resp. ) is the global maximizer (resp. minimizer) of ;

-

2.

and are continuous decreasing functions solutions to the equations

(3.11) -

3.

are given by

(3.12)

Now, a simple application of change of numeraire results from the previous section gives that attains the lower bound price for the type I forward start straddle as well. This result complements the one in Hobson and Klimmek [2015] about type II forward start straddle . We show first a symmetry property of Hobson-Klimmek optimal coupling.

Proposition 3.5.

The martingale measure verifies the symmetry relation

where the symmetry operator is defined in 2.4.

Proof.

Let the pair define the measure . A simple computation shows that the measure is concentrated on . In order to get the equations satisfied by this three-band graph, recall first the symmetry relations

| (3.13) |

By definition, is characterized by the two equations

Hence, using (3.13) we have

Since the functions and are both continuous decreasing and satisfy the same equations as the pair , they are candidates. Hence, the uniqueness of the optimal coupling yields the result. ∎

At this point we can exploit a symmetry relation between type I and type II forward start straddles, which is given by

| (3.14) |

In particular, the ATM straddles, i.e. , are related by . A consequence of this is the following proposition, that states the announced result on forward start straddle of type I and concludes the section.

Proposition 3.6.

The lower bound price of the ATM forward start straddle of type I is also attained by optimal coupling , i.e.

| (3.15) |

4 Symmetry properties of left and right monotone transference plans

The optimization problems in (2.5) are strongly related to the concepts of right and left monotone transference plans. Both notions were introduced in Beiglböck and Juillet [2012], who show their existence and uniqueness for convex ordered marginals, and prove that they solve the maximization and the minimization problem in (2.5) for a specific set of payoffs of the form with differentiable with strictly convex first derivative. Henry-Labordère and Touzi [2013] extend these results to a wider set of payoffs. Moreover they also give an explicit construction of the left-monotone transference plan. In this section we want to study the symmetric property of those transference plans and show in particular that, in the case of positive martingales, the right monotone plan can be obtained from its left monotone counterpart with no effort via change of numeraire.

We start by recalling the general definition of right and left monotone transference plan.

Definition 4.1 (Beiglböck and Juillet [2012]).

A martingale measure is left-monotone (resp. right-monotone) if there exists a Borel set with such that for all and in we cannot have and (resp. and ). We denote (resp. ) the left-monotone (resp. right-monotone) transference plan with marginals .

The next result states how the two monotone transference plans relate to each other via the symmetry operators.

Proposition 4.2.

The operator exchanges left-monotone and right-monotone transference plans, i.e. and .

Proof.

We prove only the first equality, as the second follows immediately since is an involution. By definition of the right-monotone transference plan , there exists a Borel set such that and for all in we cannot have and . Let

We clearly have

Moreover, since if and only , we cannot have and . Therefore, we have , hence by uniqueness of the left-monotone transference plan (see Theorem 1.5 in Beiglböck and Juillet [2012]) we obtain . ∎

Remark 4.3.

We observe that, as a by-product of the previous result, the existence of left-monotone transference plan gives for free the existence of its right-monotone analogue via the symmetry operator and vice-versa. Moreover, notice also that the result above holds in full generality, e.g. even when the marginals do not have densities.

Building on the results in Beiglböck and Juillet [2012], Henry-Labordère and Touzi [2013] show in particular that attains the upper bound (2.5) for a larger class of payoffs verifying a generalized Spence-Mirrlees type condition (or ) (see their Theorem 5.1). We summarize their result in the following theorem.444Observe that the results in Theorem 4.4 hold under more general conditions than our Assumption 3.1(ii).

Theorem 4.4 (Henry-Labordère and Touzi [2013]).

Let be a measurable function such that the partial derivative exists and . Under Assumption 3.1, the left-monotone transference plan is the optimal coupling solving the martingale transport problem

In order to apply the change of numeraire approach, notice first that by the definition of we have

| (4.16) |

Hence, we have that holds true if and only if . This elementary remark allows to find the model-free price bounds for payoffs verifying by changing the numeraire. This is similar to what happens with the mirror coupling in [Henry-Labordère and Touzi, 2013, Remark 5.2], where the marginals have support in . The symmetry operators and permit to handle this case for -supported marginals.

To make this observation more precise, let be a payoff satisfying . Hence and by Proposition 2.6 we have

Therefore, is attained by , which is equal to by Proposition 4.2. One can prove in a similar way that if (resp. ), the lower bound in (2.5) is attained by (resp. ).

Remark 4.5.

We say that a payoff function is symmetric if it satisfies .555A way of constructing a symmetric payoff goes as follows: choose its values on first, then for , set . One may easily check that satisfies . For any symmetric payoff verifying the slightly relaxed generalized Spence-Mirrlees condition , we can use (4.16) to get , hence . Integrating with respect to twice and with respect to once, we see that is necessarily of the form , for some functions and .

4.1 Explicit constructions of left and right-monotone transference plans and change of numeraire

In this section we briefly recall the explicit construction of a left-monotone transference plan performed by Henry-Labordère and Touzi [2013] and we show how the change of numeraire can be used to generate, essentially for free, the basic right-monotone transport plan from its left-monotone counterpart via the symmetry operator. We stress that Assumption 3.1 is still in force. The explicit characterization of in Henry-Labordère and Touzi [2013] is described, for reader’s convenience, in the following theorem.

Theorem 4.6.

Let Assumption 3.1 hold. The left-monotone transference plan is given by with transition kernel

where , is the unique maximizer of and are positive continuous functions on , such that:

-

i)

, for ;

-

ii)

, for ;

-

iii)

on the interval , is decreasing, is increasing.

Moreover is the unique solution to

| (4.17) |

and is given by the relation

| (4.18) |

Proof.

We refer to Theorem 4.5 in Henry-Labordère and Touzi [2013]. More details on the case of a single maximizer can be found in Section 3.4 therein. ∎

Now, using the fact that together with the characterization of the left-monotone transference plan given in the previous theorem, we can investigate how the quantities defining and are related to each other. Notice that, since both marginals have support in , the symmetry relation we use here is different than the one in Remark 5.2 in Henry-Labordère and Touzi [2013].

Proposition 4.7.

Let Assumption 3.1 hold. Then the right-monotone transference plan is given by with transition kernel

where

-

1.

is the unique minimizer of ;

-

2.

, , for ;

-

3.

the transition probability is given by , for .

Proof.

By Lemma 2.3, if satisfy , then their images by the symmetry operator verify the same conditions, i.e : and . By Remark 3.3 one has that has a single local maximizer and Theorem 4.6 gives that there exists a left-monotone transference plan characterized as in Theorem 4.6.

To conclude, since we already know that (see Proposition 4.2), it suffices to check that the measure defined as with the kernel defined as in the statement, satisfies

for all bounded measurable functions . This can be done by direct computation using the formulas for , and given in the statement. The details are therefore omitted. ∎

Remark 4.8.

As a by-product of the previous proposition, we get the characterization of in terms of a triplet , where is the unique minimizer of and are positive continuous functions on , such that:

-

i)

, for , and , for ;

-

ii)

(resp. ) is increasing (resp. decreasing) on ;

-

iii)

the transition kernel , i.e. , is defined by

where .

Finally, one can check that and are solutions to

| (4.19) | |||||

| (4.20) |

5 The symmetric marginals case

In this section we look at the particular situation where the marginals satisfy and . In this case we will say then that the marginals and are symmetric. Note that the use of the word ‘symmetry’ in this context comes from the fact that the corresponding volatility smiles at each maturity are symmetric in log-forward moneyness. Symmetric models have been further studied by, e.g., Carr and Lee [2009] and Tehranchi [2009]. In particular, in Carr and Lee [2009] this concept is called put-call symmetry (PCS). They also give many examples of symmetric models, cf. [Carr and Lee, 2009, Sections 3 and 4].

The stochastic volatility models with zero correlation between the volatility and the spot are a classical example of a symmetric model. Consider a situation where and are the marginals at two consecutive times of some stock price process whose dynamics follows the stochastic volatility model

where and are two independent Brownian motions. Then a simple application of Girsanov’s theorem yields and (cf. [Renault and Touzi, 1996, Proposition 3.1]). This includes the Black-Scholes model as a special case.

An additional property satisfied by the symmetric models is given in the following proposition. Recall that (resp. ) denotes the unique maximizer (resp. minimizer) of .

Proposition 5.1.

Assume that and are symmetric and let Assumption 3.1 hold. Then the unique minimizer satisfies and it is given by . As a consequence .

Proof.

Let be the single maximizer of and its minimizer, the existence of which is ensured by the convex order of and . We know from Remark 3.3 that the minimizer of verifies the relation . Since and are symmetric, then . Since , we have , and consequently . ∎

Example 5.2 (The symmetric log-normal case).

We give an example of symmetric model, where the laws and are log-normal distributions

Their probability densities and cumulative distribution functions are given by

where is the error function defined by , . In this case, the maximum and minimum of can be computed explicitly. Indeed, they are solutions in of the equation

which gives

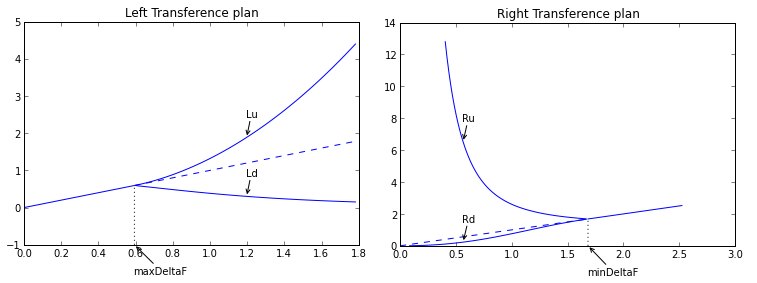

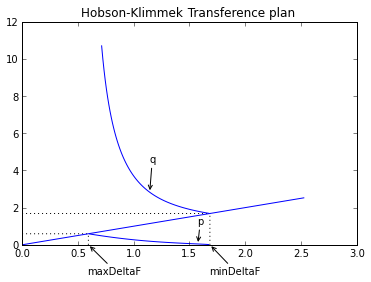

Note that . The two figures 1 and 2 below illustrate the left and right-monotone transference plans and , and the basic three-points band decreasing transference plan by Hobson and Klimmek [2015]. Figure 1 gives the behaviour of the function , showing in particular the location of its maximum and minimum .

5.1 Symmetrized payoffs have a lower model risk

In this subsection we show how the symmetry property of the marginals can be used to reduce the model risk of an option. The quantity is a natural indicator of the model risk associated to a given payoff . Obviously, model-risk free payoffs include payoffs which can be written as , since in this case. The following proposition shows that the converse is also true, under some conditions, even beyond the symmetric marginal case.

In the following proposition we will need some duality theory. We define the dual problems corresponding to and as

where (resp. ) denotes the set of all triplets such that (resp. ) for all . Moreover we say that there is no duality gap for the lower bound (resp. upper bound) if (resp. ).

Proposition 5.3.

Let be a payoff such that . Assume that the dual problem is attained and that there is no duality gap. Then, there exist functions such that

Proof.

Let be a payoff such that and let there be no duality gap. The property implies that for all . Moreover since the dual problem is attained there exist dual functions such that

and

| (5.21) |

Since all have marginals and as well as the martingale property, we have

Consequently, we have

which, combined with (5.21), gives , -a.e. for all . ∎

Remark 5.4.

We recall that Beiglböck et al. [2013] consider the two-marginals martingale minimization problem in (2.5) for upper semi-continuous payoffs with linear growth, and prove that there is no duality gap under some suitable conditions. Analogous results can be deduced for the primal maximisation problem. In general, the value functions of the corresponding dual problem is not always attained. The very recent paper Beiglböck et al. [2015] proposes a quasi-sure relaxation of the dual problem, leading to an extension of “no duality gap” result to any Borel payoff with the existence of a dual optimizer.

Now, let the marginals and be symmetric and let be any continuous payoff with linear growth. By Proposition 2.6, we have

implying . In particular, this gives for payoffs with . In financial terms, this means that the new payoff reduces the model risk. Note that . Moreover, we have , and since is an involution, we get .

On the other hand, , and because of the symmetry of around we get

Hence, realizes the minimum model risk for the portfolio .

6 Summary

In this paper we introduce change of numeraire techniques in the two-marginals transport problems for positive martingales. In particular, we study the symmetry properties of Hobson and Klimmek [2015] optimal coupling under the change of numeraire, which exchanges type I with type II forward start straddle. As a consequence, we prove that the lower bound prices are attained for both options by the Hobson-Klimmek transference plan. On the other hand, relying on the construction of Henry-Labordère and Touzi [2013] of the optimal transference plan introduced by Beiglböck and Juillet [2012], we also show that the change of numeraire transformation exchanges the left and the right monotone transference plans, so that the latter can be viewed has a mirror coupling acting of the former under a change of numeraire for positive martingales with given marginals. We conclude this paper with some numerical illustrations in the symmetric log-normal marginals case.

References

- Beiglböck and Juillet [2012] M. Beiglböck and N. Juillet. On a problem of optimal transport under marginal martingale constraints. Annals of Probability, 2012.

- Beiglböck et al. [2013] M. Beiglböck, P. Henry-Labordère, and F. Penkner. Model-independent bounds for option prices—a mass transport approach. Finance Stoch., 17(3):477–501, 2013. doi: 10.1007/s00780-013-0205-8.

- Beiglböck et al. [2015] M. Beiglböck, M. Nutz, and N. Touzi. Complete duality for martingale optimal transport on the line. arXiv preprint arXiv:1507.00671, 2015.

- Carr and Lee [2009] P. Carr and R. Lee. Put-call symmetry: extensions and applications. Math. Finance, 19(4):523–560, 2009. doi: 10.1111/j.1467-9965.2009.00379.x.

- Geman et al. [1995] H. Geman, N. El Karoui, and J.-C. Rochet. Changes of numeraire, changes of probability measure and option pricing. Journal of Applied probability, pages 443–458, 1995.

- Henry-Labordère and Touzi [2013] P. Henry-Labordère and N. Touzi. An explicit martingale version of Brenier’s theorem. Finance Stoch., 2013. Forthcoming.

- Hobson and Klimmek [2015] D. Hobson and M. Klimmek. Robust price bounds for the forward starting straddle. Finance Stoch., 19(1):189–214, 2015. doi: 10.1007/s00780-014-0249-4.

- Jacquier and Roome [2015] A. Jacquier and P. Roome. Asymptotics of forward implied volatility. SIAM Journal on Financial Mathematics, 6(1):307–351, 2015. doi: 10.1137/140960712.

- Jamshidian [1989] F. Jamshidian. An exact bond option formula. Journal of finance, pages 205–209, 1989.

- Jeanblanc et al. [2009] M. Jeanblanc, M. Yor, and M. Chesney. Mathematical methods for financial markets. Springer Science & Business Media, 2009.

- Laachir [2015] I. Laachir. Quantification of the model risk in finance and related problems. PhD thesis, Ensta-ParisTech, 2015.

- Lucic [2003] V. Lucic. Forward-start options in stochastic volatility models. Wilmott Magazine, 2003.

- Renault and Touzi [1996] E. Renault and N. Touzi. Option hedging and implied volatilities in a stochastic volatility model. Mathematical Finance, 6(3):279–302, 1996. doi: 10.1111/j.1467-9965.1996.tb00117.x.

- Strassen [1965] V. Strassen. The existence of probability measures with given marginals. Ann. Math. Statist., 36:423–439, 1965.

- Tehranchi [2009] M. Tehranchi. Symmetric martingales and symmetric smiles. Stochastic Process. Appl., 119(10):3785–3797, 2009. doi: 10.1016/j.spa.2009.07.007.