Systemic risk through contagion in a core-periphery structured banking network

Abstract

We contribute to the understanding of how systemic risk arises in a network of credit-interlinked agents. Motivated by empirical studies we formulate a network model which, despite its simplicity, depicts the nature of interbank markets better than a homogeneous model. The components of a vector Ornstein-Uhlenbeck process living on the vertices of the network describe the financial robustnesses of the agents. For this system, we prove a LLN for growing network size leading to a propagation of chaos result. We state properties, which arise from such a structure, and examine the effect of inhomogeneity on several risk management issues and the possibility of contagion.

| AMS 2010 Subject Classifications: | 60K35 ; 60H30 ; 91B30 . |

| JEL Classification: | G18 ; G21 ; G23 . |

Keywords: core-periphery bank model, financial contagion, inhomogeneous graph, interacting particles, systemic risk

1 Introduction

Interbank lending patterns and financial contagion have been in the focus of central banks and regulators already before, but predominantly since the financial crisis has started in 2007, succeeded by the government debt crisis in Europe. Consequently, there is a number of empirical studies performed by central banks dealing with issues of contagion; see e.g. [7, 9, 14, 15, 17, 20, 23]. However, as indicated in Mistrulli [14], data limitations - especially not or only partly available bilateral exposures between agents - often enforced the use of the so-called maximum-entropy method. This method actually rules out structural information about the market, while assuming that each bank lends to all others, possibly leading to over- or underestimation of contagion (cf. Mistrulli [14] for a discussion and data analysis). With respect to structural properties of interbank markets, the empirical studies [4] for the Austrian market, [18] for the Fedwire interbank payment network, [5] for the Brazilian market, and [6] for the German market share the same finding: There is a small number of highly connected big banks acting as financial intermediaries for a large number of smaller banks, which mostly do not interact directly. Our approach weakens the homogeneity assumptions by suggesting a more realistic model allowing for top-tier and lower-tier banks.

Several studies model the financial market as a random graph. Financial contagion in the market is then treated by investigating and simulating a discrete bankruptcy cascade, which is initiated by some triggering mechanism like a first passage event; see e.g. [1, 3, 10, 13]. Another approach is based on mean field models of interacting systems of diffusions as used in physics to model the evolution of particles. This yields a homogeneous financial market; see e.g. [8, 11, 12]. Our approach extends such models two-fold. Firstly, we replace the driving Brownian motion (BM) by a Lévy process, which does not require new techniques. Secondly and more important, we modify the model away from homogeneity to the above mentioned two-tier market structure, and derive for this a new limit theorem. We thus enter a new line of research that allows for more flexibility in modeling the robustness of the financial market and its agents.

Our paper is organised as follows. We introduce the two-tier financial market model in Section 2 and present subsequently the robustness process for all agents in the market. In Section 3 we prove a LLN for the new financial system, which may be interpreted as a propagation of chaos result. The limit model is further studied and used for the sake of systemic risk assessment in Section 4. We investigate the systemic risk of the market in terms of the standard deviation risk and the inverse first passage time risk. We examine in particular the effect of individual risk management decisions on the risk of contagion. The paper concludes with an outlook on future research in Section 5.

2 The contagion model

2.1 Market model

We model a credit interbank market as a weighted directed graph with a finite number of vertices . This is a common approach, see e.g. [1, 3]. While the set of vertices represents the agents in the market, information about their bilateral credit relationships is encoded in the set of edges. In the interbank market each agent manages a credit portfolio , where holds if and only if agent is a debtor of agent . We agree upon that no agent lends to herself, i.e. for all and denote by the set of debtors of agent . Correspondingly, indicates the out-degree of agent being the number of issued credits by agent in our context. The set endows every edge with an individual weight , that is, the credit issued from agent to agent corresponds to % of the total credit amount agent has issued to the overall interbank market. Consequently,

In the homogeneous graph of [3] each agent issues credits to exactly other agents from the same market so that for all . Moreover, the credit weights are assumed to be uniformly for all and 0 otherwise.

We extend this model to an inhomogeneous graph in the sense that we allow for two types of agents, the core banks and the periphery banks. There is empirical evidence for a two-tiered structure of interbank markets: top-tier banks and lower-tier banks, cf. [4, 5, 18, 20] and in particular [6], which develops a more specific core-periphery network model. In a simplified purely tiered network top-tier (core) banks can potentially lend to and borrow from any bank in the network, while lower-tier (periphery) banks exclusively interact with top-tier banks but not with banks from their own tier.

We underlay this core-periphery interbank market with the following specifying assumptions:

-

•

The interbank market is partitioned into a set of core banks and a set of periphery banks ; i.e., .

-

•

The set of debtor banks of a core bank can be partitioned into the two subsets

Analogously, for a periphery bank we set

-

•

The banks (nodes) have the following out-degree structure:

-

•

Each agent acts as a creditor and issues credits to other agents from the same market:

The adjacency matrix indicates the bilateral credit relationships between the agents of the network by entries of ones and zeros, more precisely,

| (2.1) |

In view of the two-tiered structure of the market, a block model can be employed, which is a common approach in social network analysis; cf. [22]. In our case the adjacency matrix is a block matrix composed of 4 blocks corresponding to the core and periphery decomposition of :

| (2.2) |

The block having dimension lists the credit relationships among the core banks, the block provides the information about the relationships among the periphery banks and the blocks and cover the exchange of credits between core and periphery, respectively.

The weighted adjacency matrix is defined through

Example 2.1.

[Craig and von Peter [6]] Here the blocks are specified as follows:

-

•

is a matrix of ones exceptional the zero diagonal: all core banks issue credits to all other core banks;

-

•

is a matrix of zeros: periphery banks issue no credits among each others;

-

•

is row regular, that is, each row has at least one 1: each core bank issues credits to at least one periphery bank;

-

•

is column regular, that is, each column is covered by at least one 1: at least one periphery bank issues a credit to one of the core banks.

2.2 Financial robustness

Following [3, 8], we endow each agent in our network by a measure called financial robustness which quantifies an agent’s financial constitution over time. In the following we specify this measure as a continuous-time stochastic process, where all stochastic quantities will be defined on a probability space . In our specification we suppose that the behavior of the financial robustness is related to two sources: On the one hand, an agent’s robustness depends on the robustness of its debtors. If the debtors’ robustness is low, an agent has to face higher counterparty risk and, thus, its robustness will suffer as well. On the other hand, the robustness will also be affected by any non-interbank market investment. We model this by a vector Ornstein-Uhlenbeck process given as solution of the vector stochastic differential equation (SDE)

| (2.3) |

where denotes an -dimensional mean 0 Lévy process with finite variance. The component models the interdependence resulting from the agents’ interbank market activity, whereas the Lévy process covers the impact from external market sources. By incorporating the robustness process is explicitly addressing the network structure. For our purposes this network structure is kept constant over time, which is in line with the findings of [6] about the structural stability of the German interbank market.

The following result gives the solution of the SDE (2.3) and the second order moment structure.

Proposition 2.2.

For the SDE (2.3) with and initial vector the following assertions hold.

(a)

The SDE has a unique explicit solution given by

| (2.4) |

with the matrix exponential , and is the unit matrix.

(b) The mean of the process is given by

(c) For every the covariance matrix function is given by

where is the diagonal variance matrix of .

3 Financial robustness in large networks

If we pick out one row of Eq. (2.3), then the financial robustness of agent follows the dynamic

| (3.1) |

As described above the drift term adjusts the process towards the mean robustness of agent ’s debtors. Note that the mean is calculated over with , hence this ensemble mean is independent of the driving process .

When all weights are chosen to be equal and the driving process is a Brownian motion, then this is a classical example in physics for interacting particle systems going back to McKean. We extend McKean’s mean field example of interacting diffusions to the inhomogeneous system (2.4) driven by independent Lévy processes.

We choose the weights based on the following market assumption, which are in line with with a perfectly tiered interbank market as considered in [6]. All core banks interact with each other and every periphery bank is creditor and debtor to every core bank. For the periphery banks, any credit relationship among them is excluded. Then the SDE (3.1) becomes

| (3.2) | |||||

| (3.3) |

where all Lévy processes are independent with mean , and standardized second moment for . The constants model the standard deviations of the core and periphery banks respectively. The Lévy processes are for all identically distributed, as well as the for all . Moreover, we assume the following simple scenario for the weights. For all we assume that for and for some , and also that for , so that . For all we assume that for all and for all . Then (3.2) and (3.3) read as

| (3.4) | |||||

| (3.5) |

This is a coupled system, where the robustness of the core banks is influenced by the mean robustness of all other core banks and the mean robustness of all periphery banks. The robustness of the periphery banks, on the other hand, is influenced by that of the core banks only. We prove a LLN for the empirical distributions given by the weighted sums when the system becomes large; i.e. for .

Theorem 3.1.

Assume the core-periphery model (3.4) and (3.5) with independent driving Lévy processes, which are identically distributed for all and all , respectively. Define the limit system by the dynamics

| (3.6) | |||||

| (3.7) |

where and ; i.e. is the distribution of for all and that of for all . Take the same driving Lévy processes as above and the same initial conditions for , independent of all Lévy processes. Denote . Then for every , , and a constant independent of ,

| (3.8) |

Proof.

For the proof we adapt the arguments of the proof of Theorem 1.4 of Sznitman [19] to the inhomogenous system. First note that for

Summing this equality over all , and using the fact that and for are equally distributed, respectively, we obtain for and some ( always denotes some positive constant, whose value may vary from line to line) by taking the modulus under the Lebesgue integral

Now we estimate for using the triangular inequality

Hence, the structure of this inequality is of the form ready to apply Gronwall’s Lemma, which yields

| (3.9) |

Next note that for

We take all terms under the integral corresponding to the core banks and obtain (we dropped the factor )

Then we take all terms under the integral corresponding to the periphery banks (dropped the factor ) and obtain

Now we estimate for , taking the modulus under the Lebesgue integral and use the triangular inequality

Summing the previous inequality over all , which are identically distributed, as well as all for ,

To estimate the last integral we use the fact that for all expectations are equal, and take under the integral the supremum over all . This gives for arbitrary

where the last inequality follows from the bound in (3.9). Now we take this term back under the common integral, recall that all our bounds depend on and call again simply . Then adding and subtracting in the above bound, and using the triangular inequality,

This implies

hence, by Gronwall’s Lemma,

Now we have for , since all are independent,

so that by the Cauchy-Schwarz inequality, for all ,

| (3.12) |

where does not depend on . The same argument applies for the sum over , so that we obtain from (3)

| (3.13) |

For we go back to (3.9) and, invoking (3) and (3.13), we find

This implies the result. ∎

Remark 3.2.

(1) Note that in the limit system (3.6) and (3.7) all processes are independent, so that we have propagation of chaos, meaning that for the system size getting large, all robustness processes become independent.

(2) From the result (3.8) we see that all banks are mean reverted to a mean process provided that the number of core banks gets large, and the number of core banks and periphery banks satisfy a certain growth condition. In a real market we would think of many more periphery banks than core banks, so that as would seem realistic.

4 Risk management in the core-periphery market

In order to study certain diversification effects in the core-periphery bank model we introduce, similar to [8, 11, 12], friction parameters for the core banks and the periphery banks, respectively. Hence, the model (3.4) and (3.5) is extended to

| (4.1) | |||||

| (4.2) |

Corollary 4.1.

We consider and as parameters emphasizing how strong the corresponding agent is weighting interbank activity in its investment strategy; i.e., a higher value indicates a larger investment into interbank credits. This higher value will increase the effect of the mean reversion term in the Ornstein-Uhlenbeck dynamic.

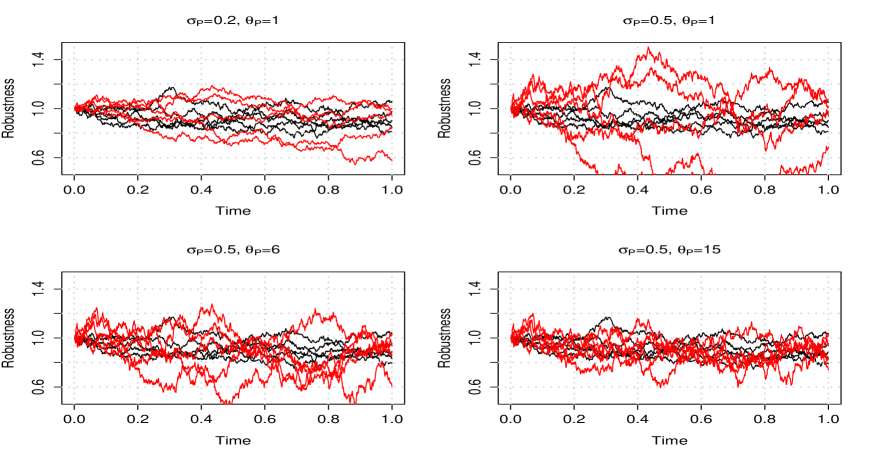

We start the discussion by a simulation study based on Eq. (2.3) for the finite network with the specific structure assumed in Theorem 3.1 and the additionally introduced friction parameters; that is

| (4.5) |

where and are diagonal matrices with diagonals and , respectively, for positive constants and . For our simulation we choose as network size with and . For all our simulations the robustness processes start in 1 and are driven by Brownian motions. Based on data in [6] we take .

4.1 Hedging changes in the market volatility

We examine the consequences of changes in the market volatilities to either core or periphery banks, based on the paths of the agents’ robustnesses. We consider different scenarios.

Initially core and periphery will face the same economic environment and we choose and , respectively. For this choice of parameters Figure 1 shows in the upper left plot sample paths of the robustness for all five core banks and five (out of 50) periphery banks. In a next step we suppose higher volatility in the market. Whereas core banks can keep the volatility of their non-interbank assets constant due to sophisticated hedging strategies; i.e., the same value holds, periphery banks do not have the resources and expertise for such methods. Hence, the standard deviation of their non-interbank assets increases to . If periphery banks do not undertake a shift of their assets but keep their investment strategy unchanged, their robustness will show a higher variation, which is confirmed by the upper right plot in Figure 1. The two lower plots in the same figure highlight that an increase of (by increased investment into interbank credits) can reduce variation.

A further analysis of the consequences of such a change in the market volatility is summarized in Table 4.1, where is the estimated robustness of one periphery bank at time based on 100 simulation runs for varying parameters of . The standard errors in brackets indicate that an increase of can indeed reduce the variation in the robustness of a periphery bank.

So far, our model suggests that periphery banks can reduce uncertainty in their robustness, resulting from higher volatility in non-interbank assets, by higher investment into interbank assets. This strategy has certain drawbacks, when a shock hits all core banks’ robustness at the same instant of time. For pointing out the resulting effect we redo the simulations and assume a reduction of all core banks’ robustness by 0.3 at and investigate the market at (immediately after the shock) and at . Such a shock, being restricted to the core, means that for a short term the robustness of core banks and periphery banks will diverge. However, due to the mean reversion in Eq. (4.5) the mean of core and periphery banks’ robustnesses will again revert to a common value in the long run (cf. Corollary 4.3 below). Table 4.1 illustrates that in a shock scenario an increased still reduces variation, but a shocked core will affect the periphery more intensive for higher values of . For smaller values of the robustness of the periphery banks exhibits a lower sensitivity with respect to the shock on the core. In this case core banks can in turn benefit from their interbank activity with more robust periphery banks. This becomes apparent in the estimates of the robustness at , which show approximately the new common robustness of core and periphery in the post-shock regime. Apparently, for the core banks can at least recover partially from the shock, which is, however, not the case any more, if becomes too large.

Overall, we conclude that periphery banks can have an incentive to invest more into the interbank market in order to hedge their volatility, however, the increase of interbank investment makes them more vulnerable for contagion resulting from a core-wide shock. The whole network will also suffer, if the periphery invests too much into the core as the increased sensitivity of the periphery with respect to the core’s constitution will have negative feedback effects on the core itself and its ability to recover from past shock events.

| without shock () | with shock () | with shock () | ||||

|---|---|---|---|---|---|---|

| 0.99 (0.34) | 0.98 (0.14) | 0.96 (0.34) | 0.70 (0.14) | 0.77 (0.33) | 0.75 (0.15) | |

| 1.00 (0.22) | 0.98 (0.14) | 0.92 (0.22) | 0.69 (0.14) | 0.71 (0.24) | 0.71 (0.15) | |

| 1.00 (0.16) | 0.98 (0.14) | 0.86 (0.16) | 0.69 (0.14) | 0.70 (0.19) | 0.70 (0.15) | |

| 1.00 (0.14) | 0.98 (0.14) | 0.81 (0.14) | 0.69 (0.14) | 0.69 (0.16) | 0.69 (0.16) | |

| 1.00 (0.13) | 0.98 (0.14) | 0.77 (0.13) | 0.69 (0.14) | 0.69 (0.15) | 0.69 (0.16) | |

| 1.00 (0.12) | 0.98 (0.14) | 0.74 (0.12) | 0.69 (0.14) | 0.69 (0.14) | 0.68 (0.16) | |

| 1.00 (0.11) | 0.98 (0.14) | 0.72 (0.11) | 0.69 (0.14) | 0.69 (0.14) | 0.68 (0.16) | |

4.2 Risk management of structural breaks in the market

In this section we want to shed light on the outcome of the previous simulations in a more concrete way by relying on first passage times.

The following corollary presents the first and second moments of the limit processes.

Corollary 4.2.

Provided there exists a stationary version of the system of Corollary 4.2, this stationary model has constant means and variances of the core and periphery banks, respectively. They are obtained from the above moments for , which yields and for and for . The resulting stationary dynamics lead to a further simplification of the original model.

Corollary 4.3.

Stationary versions of the SDEs in Corollary 4.2 are given by

where is the a.s. limit of the mean robustness of the core banks as for all .

Consequently, for a large number of core and periphery banks, we can discuss various risk measures by relying on the simple Ornstein-Uhlenbeck dynamic of Corollary 4.3. As a first risk measure we consider the standard deviation.

Definition 4.4.

For each bank we define the standard deviation risk

It is certainly one goal of every bank to keep within certain bounds and at best constant (cf. [12]). As a second risk measure we define the inverse of the mean first passage time of the robustness of an agent.

Definition 4.5.

For every bank denote the inverse first passage time risk (IFPT risk) by

where denotes the first passage time of to 0.

First passage events have also served as triggering events to start a cascading mechanism in the market (e.g. Battiston et al. [3]). For a mathematical analysis [3] approximates the first passage time of a mean reverting OU process simply by that of Brownian motion. We prefer to work with the following precise formula.

Lemma 4.6.

Assume the core-periphery bank system driven by independent Brownian motions and assume that all robustness processes are solutions to the SDEs in Corollary 4.3 with starting values for all . Define and let denote the tail and the density of the standard normal distribution. Let denote the first passage time of a generic bank to 0. Then the following hold:

| (4.6) |

Proof.

According to Prop. 4 of [21] the first passage time of an Ornstein-Uhlenbeck process

which starts in 1 to hit 0 for the first time has expectation

| (4.7) |

where is a normal random variable with mean and variance in the first and second component. Then, setting , we get

| (4.8) | |||||

so that, since , the integrand can be rewritten as

where a substitution of variables yields the final result. ∎

The first passage time of the robustness process of bank can be interpreted as default of a bank. Hence, any bank will surely aim to keep low.

We will asses the risk management of a periphery bank in a more quantitative manner, if structural breaks on the core occur. The risk measures of interest are the standard deviation risk and the IFPT for any periphery bank.

We first come back to the scenario in Section 4.1, where we have found out that for a bank with fixed target value for , when the volatility is varying, the periphery bank can hedge this by choosing an appropriate . Now we can quantify this value, namely,

| (4.9) |

for any value of . Particularly, an increase of requires an increase in , which is in line with the simulations illustrated in Figure 1. For changing from 0.2 to 0.5 (cf. Section 4.1), for instance, Eq. (4.9) suggests a required increase of from 1 to 6.25 in order to keep the standard deviation risk constant at its initial value 0.1414. Without changing the periphery bank would have to accept the standard deviation risk rising from 0.1414 to 0.3535 implying a higher uncertainty for the future robustness.

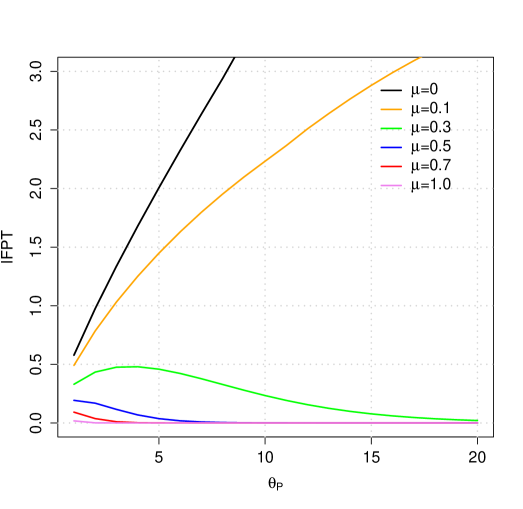

As noticed from the values in Table 4.1 larger values of , however, may reinforce the decrease of a periphery bank’s robustness, if the robustness of core banks is relatively low. This drawback of increasing becomes apparent, if one takes the IFPT risk into account. Figure 2 shows how the IFPT risk depends on for and different values of the mean robustness in the core. A reduction in by enlarging has beneficial effects on the IFPT risk only as long as stays sufficiently large. However, for values of near zero an increase of results in a massive increase of the IFPT risk.

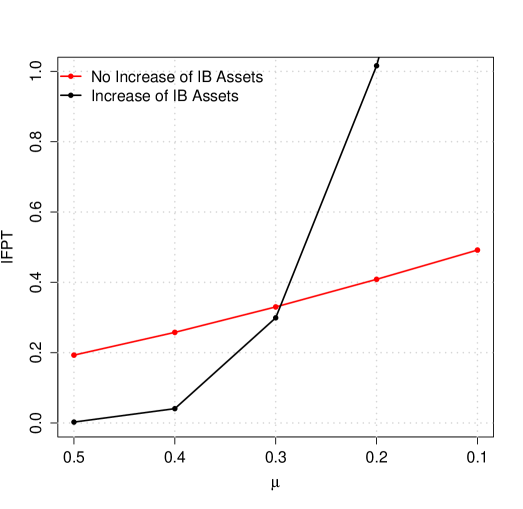

We like to substantiate this by a final example which adopts the setting of Section 4.1; i.e., we assume again an increase of volatility from to hitting the periphery. Instead of hedging we now aim at keeping the IFPT risk constant by adjusting correspondingly. For and the assumed volatility scenarios, we have computed – by applying a numerical rootfinder to Eq. (4.6) – that a periphery bank must increase from 1 to 8.6 in order to keep constant at the low level of . Otherwise, without an adjustment of the interbank investment volume, the IFPT would jump to 0.192. For an illustration, see Figure 3, which compares for both alternatives, increase of and no increase of .

Similar to the case of hedging previously, the drawback of keeping constant arises, if changes. Assume that some structural break within the core occurs, resulting from an external shock, which cuts now the mean robustness of the core banks. Figure 3 suggests that the remedy of an increased investment into interbank asset would turn out to be the worse alternative as soon as the core robustness experienced a reduction in the mean robustness of slightly more than 0.2. When such an event happens, the periphery bank’s IFPT risk would have been smaller without increasing the interbank investment for hedging the IFPT risk under increased volatility.

5 Conclusion

Based on empirical evidence we employed a hierarchical block model for modelling the interbank market as a network, in which a small number of highly connected large banks (the core) play the role of financial intermediaries for a large number of smaller banks (the periphery). We introduced the financial robustness of the agents as continuous-time stochastic processes explicitly incorporating the market structure. Further, we proved a LLN for this coupled multivariate system as the network size grows. We proved that in the limit system all processes are independent, hence, the system decouples more and more as the network enlarges. This behaviour is called propagation of chaos in the physics community.

In a first simulation approach on the core-periphery network we have pointed out that risk management decisions, although being meaningful from the perspective of a single agent may accelerate the negative effects of a system-wide distortion. Our application is based on the assumption that core banks have more expertise and resources available for performing sophisticated risk management measures in order to hedge volatility successfully on the non-interbank market. In contrast, the only possibility of periphery banks to hedge increasing volatility occurring in their non-interbank assets portfolio is provided by expanding the investment into interbank assets, that is for instance an increase of deposits at core banks. Our model and the chosen risk measures in Section 4.2 disclose some analytical tools for evaluating the risk management decisions of a periphery bank under such conditions. As in previous simulation approaches we have observed that periphery banks can hedge volatility via increasing interbank investments, however, this at first effective hedging activity may become a drawback in the case of external shocks hitting parts of the network.

In our paper we have established a framework, which gives a basis for further examination of the interbank market - particularly under the viewpoint of interaction between periphery and core banks. Further research will relax the still restrictive core-periphery model from Section 3 and prove an analogue of Theorem 3.1 with off-diagonal blocks in the core-periphery adjacency matrix allowing for a higher degree of heterogeneity by not assuming full lending relationships. Also central limit theorems, Poisson limit results and large deviation results will provide further interpretations for systemic risk.

Acknowledgement

We take pleasure in thanking Carsten Chong, Ben Craig, Jean-Dominique Deuschel, Nina Gantert, and Daniel Matthes for interesting discussions. OK and LR also appreciated discussions with the participants of the Research Seminar of the Deutsche Bundesbank, where LR presented our work.

References

- [1] H. Amini, R. Cont, and A. Minca. Resilience to Contagion in Financial Networks. Papers 1112.5687, arXiv.org, December 2011.

- [2] D. Applebaum. Lévy Processes and Stochastic Calculus. Cambridge University Press, Cambridge, 2004.

- [3] S. Battiston, D. Delli Gatti, M. Gallegati, B. C. Greenwald, and J. E. Stiglitz. Liaisons dangereuses: Increasing connectivity, risk sharing, and systemic risk. Journal of Economic Dynamics & Control, 36:pp. 1121–1141, 2012.

- [4] M. Boss, H. Elsinger, M. Summer, and S.Thurner. The network topology of the interbank market. Quantitative Finance, 4(6):677–684, 2004.

- [5] R. Cont, A. Moussa, and E.B. Santos. Network structure and systemic risk in banking systems. In J-P. Fouque and J.A. Langsam, editors, Handbook on Systemic Risk. Cambridge University Press, Cambridge, 2013.

- [6] B. Craig and G. von Peter. Interbank tiering and money center banks. Journal of Financial Intermediation, 2014. Forthcoming.

- [7] H. Degryse and G. Nguyen. Interbank exposures: An empirical examination of systemic risk in the Belgian banking system. Discussion Paper 2004-04, 2004.

- [8] J-P. Fouque and L-H. Sun. Systemic risk illustrated. In J-P. Fouque and J.A. Langsam, editors, Handbook on Systemic Risk, pages 444–452. Cambridge University Press, Cambridge, 2013.

- [9] C. H. Furfine. Interbank exposures: Quantifying the risk of contagion. Journal of Money, Credit and Banking, 35:111–28, 2003.

- [10] P. Gai and S. Kapadia. Contagion in financial networks. Bank of England working papers 383, Bank of England, March 2010.

- [11] J. Garnier, G. Papanicolaou, and T-W. Yang. Large deviations for a mean field model of systemic risk. arXiv:1204.3536v2, 2012.

- [12] J. Garnier, G. Papanicolaou, and T-W. Yang. Diversification in financial networks may increase systemic risk. In J-P. Fouque and J.A. Langsam, editors, Handbook on Systemic Risk. Cambridge University Press, Cambridge, 2013.

- [13] T. Hurd and J.P. Gleeson. A framework for analyzing contagion in banking networks. Papers 1110.4312, arXiv.org, October 2011.

- [14] P.E. Mistrulli. Assessing financial contagion in the interbank market: Maximum entropy versus observed interbank lending patterns. Temi di discussione (Economic working papers) 641, Bank of Italy, Economic Research and International Relations Area, September 2007.

- [15] J. Müller. Interbank credit lines as a channel of contagion. Journal of Financial Services Research, 29(1):37–60, 2006.

- [16] K. Sato. Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press, Cambridge, 1999.

- [17] G. Sheldon and M. Maurer. Interbank lending and systemic risk: An empirical analysis for Switzerland. Swiss Journal of Economics and Statistics, 134(4.2):685–704, 1998.

- [18] K. Soramaki, M. L. Bech, J. Arnold, R. J. Glass, and W. E. Beyeler. The topology of interbank payment flows. Physica A: Statistical Mechanics and its Applications, 379(1):317 – 333, 2007.

- [19] A. Sznitman. Topics in propagation of chaos. In P.L. Hennequin, editor, Ecole d’Eté de Probabilites de Saint-flour XIX – 1989, pages 165–251. Springer, Heidelberg, 1991.

- [20] C. Upper and A. Worms. Estimating bilateral exposures in the German interbank market: Is there a danger of contagion? European Economic Review, 48(4):827–849, 2004.

- [21] A.R. Ward and P.W. Glynn. Properties of the reflected Ornstein-Uhlenbeck process. Queueing Systems, 44:109–123, 2003.

- [22] S. Wasserman and K. Faust. Social Network Analysis: Methods and Applications. Cambridge University Press, Cambridge, 1994.

- [23] S. Wells. Financial interlinkages in the United Kingdom’s interbank market and the risk of contagion. Bank of England, Working Paper n.230, 2004.