Dynamic Principal Components in the Time Domain

Daniel Peña and Victor J. Yohai

Daniel Peña is Professor, Statistics Department, Universidad Carlos III de Madrid, Calle Madrid 126, 28903 Getafe, España, (E-mail: daniel.peña@uc3m.es). Víctor J. Yohai is Professor Emeritus, Mathematics Department, Faculty of Exact Sciences, Ciudad Universitaria, 1428 Buenos Aires, Argentina (E-mail: victoryohai@gmail.com). This research was partially supported by Grant ECO2012-38442 from MINECOM, Spain, and Grants W276 from Universidad of Buenos Aires, PIP’s 112-2008-01-00216 and 112-2011-01- 00339 from CONICET and PICT 2011-0397 from ANPCYT, Argentina.

ABSTRACT

We propose a time domain approach to define dynamic principal components (DPC) using a reconstruction of the original series criterion. This approach to define DPC was introduced by Brillinger, who gave a very elegant theoretical solution in the stationary case using the cross spectrum. Our procedure can be applied under more general conditions including the case of non stationary series and relatively short series. We also present a robust version of our procedure that allows to estimate the DPC when the series have outlier contamination. Our non robust and robust procedures are illustrated with real datasets.

Key words: reconstruction of data; vector time series; dimensionality reduction.

1 Introduction

Dimension reduction is very important in vector time series because the number of parameters in a model grows very fast with the dimension of the vector of time series. Therefore, finding simplifying structures or factors in these models is important to reduce the number of parameters required to apply them to real data. Besides, these factors, as we will see in this paper, may allow to reconstruct with a small error the set of data and therefore reducing the amount of information to be stored. In this article, we will consider linear time series models and we will concentrate in the time domain approach. Dimension reduction is usually achieved by finding linear combinations of the time series variables which have interesting properties. Suppose the time series vector , where and we assume, for simplicity, that which will estimate the mean if the process is stationary, is zero. It is well known that the first principal component, minimizes the mean squared prediction error of the reconstruction of the vector time series, given by and, in general, the first principal components, minimize the mean squared prediction error to reconstruct the vector of time series. Let be the sample covariance matrix and let be the eigenvalues of Then is the eigenvectors of corresponding to the eigenvalue

Ku, Storer and Georgakis (1995) propose to apply principal components to the augmented observations ) that includes the values of the series up to lag These principal components provide linear combinations of the present and past values of the time series with largest variance, and using the well know properties of standard principal components we conclude that the first component obtained from this approach is a solution to the following reconstruction problem

which implies that, apart from the end effect, we minimize for each observation , for the sum .Thus, this approach does not optimize a useful reconstruction criterion.

An alternative way to find interesting linear combinations was proposed by Box and Tiao (1977) who suggested maximizing the predictability of the linear combinations . Other linear methods for dimension reduction in time series models have been given by the scalar component models, SCM, (Tiao and Tsay, 1989), the reduced-rank models (Ahn and Reinsel, 1990, Reinsel and Velu, 1998), and dynamic factor models (Peña and Box, 1987, Stock and Watson, 1988, Forni el al. 2000, Peña and Poncela 2006 and Lam and Yao 2012), among others. None of the previous mentioned methods has as a goal to reconstruct the original series by using the principal components as in the classical case.

Brillinger (1981) addressed the reconstruction problem as follows. Suppose now the zero mean dimensional stationary process Then, the dynamic principal components are defined by searching for vectors and so that if we consider as first principal component the linear combination

| (1) |

then

| (2) |

is minimum. Brillinger elegantly solved this problem by showing that is the inverse Fourier transform of the principal components of the cross spectral matrices for each frequency, and is the inverse Fourier transform of the conjugates of the same principal components. See Brillinger (1981) and Shumway and Stoffer (2000) for the details of the method. Although this result solves the theoretical problem it has the following shortcomings: (i) It can be applied only to stationary series; (ii) The optimal solution requires the unrealistic assumption that infinite series are observed, and it is not clear how to modify it when the observed series are finite; (iii) It is not clear how to robustify these principal components using a reconstruction criterion. The second shortcoming seems specially serious. In fact in Section 4 we show by means of a Monte Carlo simulation that what seems a natural modification for finite series of the Brillinger’s procedure does not work well.

In this paper we address the sample reconstruction of a vector of time series avoiding the drawbacks of Brillinger method. Our procedure provides an optimal reconstruction of the vector of time series from a finite number of lags. Some of the advantages of our procedure are: (i) it does not require stationarity and (ii) it can be easily made robust by changing the minimization of the mean squared error criterion by the minimization of a robust scale. The rest of this article is organized as follows. In Section 2 we describe the proposed dynamic principal components based on the reconstruction criterion. In Section 3 we study the particular case where the proposed dynamic principal components depend only on one lag. In Section 4 we show the results of a Monte Carlo study that compares the proposed dynamic principal components, with the ordinary principal components and those proposed by Brillinger and we show the performances of these three types of principal components in two real examples. In Section 5 we define robust dynamic principal components using a robust reconstruction criterion and illustrate in one example the good performance of this estimator to eliminate the influence of outliers. In Section 6 some final conclusions are presented. Section 7 is an Appendix containing mathematical derivations.

2 Finding time series with optimal reconstruction properties

Suppose that we observe and consider two integer numbers and We can define the first dynamic principal component with lags (first DPCk) as a vector so that the reconstruction of series as a linear combination of is optimal with the mean squared error (MSE) criterion. More precisely, suppose that given a possible factor the matrix of coefficients and are used to reconstruct the values as

where is the -th row of Let and put and then, the reconstructed series are obtained as

Therefore we can always assume that and we will use to denote the number of forward lags.

Consider the MSE loss function

| (3) |

The optimal choices of and , are given by

| (4) |

Clearly if is optimal, is optimal too. Thus, we can choose so that and We call the first DPC of order of the observed series Note that the first DPC of order corresponds to the first regular principal component of the data. Moreover the matrix contains the coefficients to be used to reconstruct the series from in an optimal way.

Let be the matrix defined by

| (5) |

where and Let be the given by

and

| (6) |

Differentiating (3) with respect to in Subsection 7.1 we get the following equation

| (7) |

Obviously, the coefficients and can be obtained using the least squares estimator, that is

| (8) |

where and is the matrix with -th row ( Then the first DPC is determined by equations (7) and (8). The second DPC is defined as the first DPC of the residuals Higher order DPC are defined in a similar manner. We will call the selected number of components.

To define an iterative algorithm to compute is enough to give and to describe how to compute once is known. According to (7) and (8) a natural such a rule is given by the following two steps:

The initial value can be chosen equal to the standard (non dynamic) first principal component, completed with zeros. The iterative procedure is stopped when

for some value

Note that we start with series of size Assuming that we consider dynamic principal components let the coefficients corresponding to the th component, Then, the number of values required to reconstruct the original series are the values of the factors plus values for the coefficients plus the intercepts Thus the proportion of the original information required to reconstruct the series is and when is large compared to and is close to In applications the number of lags to reconstruct the series, and the number of principal components, need to be chosen. Of course the accuracy of the reconstruction improves when any of these two numbers is enlarged, but also the size of the information required will also increase. For large increasing the number of components introduces more values to store than increasing the number of lags. However, we should also take into account the reduction in MSE due to enlarging each of these components. Is clear that increasing the number of lags after some point will have a negligible effect on the reduction in MSE. Then, if the level of the MSE is larger than desired, adding an additional component is call for. Thus one possible strategy will be start with one factor and increase the number of lags until the reduction of further lags is smaller than Then a new factor is introduced and the same procedure is applied. The process stops when the MSE reaches some satisfactory value. Note that this rule is similar to what is generally used for determining the number in ordinary principal components.

3 Dynamic Principal Components when

To illustrate the computation of the first DPC, let us consider the simplest case of Then, we search for and such that

| (9) |

Put and then the matrix defined in (6) can be written as

Let It is shown in the appendix that if there exists and so that

| (10) |

Note that implies that putting where we have

and therefore, in this case the first DPC is as good for reconstructing the series as the first classical PC.

Let be defined by

put and let be the dimensional matrix where and We can write and then according to the Proposal A.3.3 of Seber (1984) we have

| (11) | ||||

where is a matrix. We also have that is of the form

| (12) |

and then we get

and

| (13) |

where except for close to or to

Suppose now that is stationary, then except in both ends can be approximated by the stationary process

and the DPC is approximated as linear combinations of the geometrically and symmetrically filtered series and These series give the largest weight to the periods and respectively and the weights decrease geometrically when we move away of these values. We conjecture that in the case of the first DPC of order a similar approximation outside both ends of by an stationary process can be obtained.

4 Monte Carlo simulation and two real examples

We perform a Monte Carlo study using as vector series , generated as follows: let , i.i.d random variables with distribution N then . We compute three different principal components: (i) The ordinary principal component (OPC), (ii) the dynamic principal component (DPC proposed here with and (iii) Brillinger dynamic principal components (BDPCM) adapted for finite samples as follows:

| (14) |

where are the coefficients defined below (2) in Section 1. The values of where taken 10, 20 and 50. To reconstruct the original series with the OPC we used lags and the corresponding coefficients were obtained using least squares. To reconstruct the series with DPCk we proceed as described in Section 2. Finally, the original series were reconstructed using the BDPCM by

where the are described below (2) in Section 1. The cross spectrum matrix was computed using the function mvspec in the ASTSA package with the R software. We took two values of 100 and 500 and we make 500 replications. Table 1 shows the MSE of the prediction residuals obtained with OPC, DPCk and BDPC We observe that the procedure DPCk proposed here produces a much better reconstruction of the original series than the OPCk and the BDPC

| OPCk | DPCk | BDPCM | |||||||

| M | |||||||||

| 1 | 5 | 10 | 1 | 5 | 10 | 10 | 20 | 50 | |

| 100 | 1.31 | 0.78 | 0.67 | 0.89 | 0.018 | 0.016 | 2.05 | 2.08 | 2.17 |

| 500 | 1.42 | 0.79 | 0.66 | 0.97 | 0.034 | 0.025 | 2.03 | 2.03 | 2.03 |

4.1 Example 1

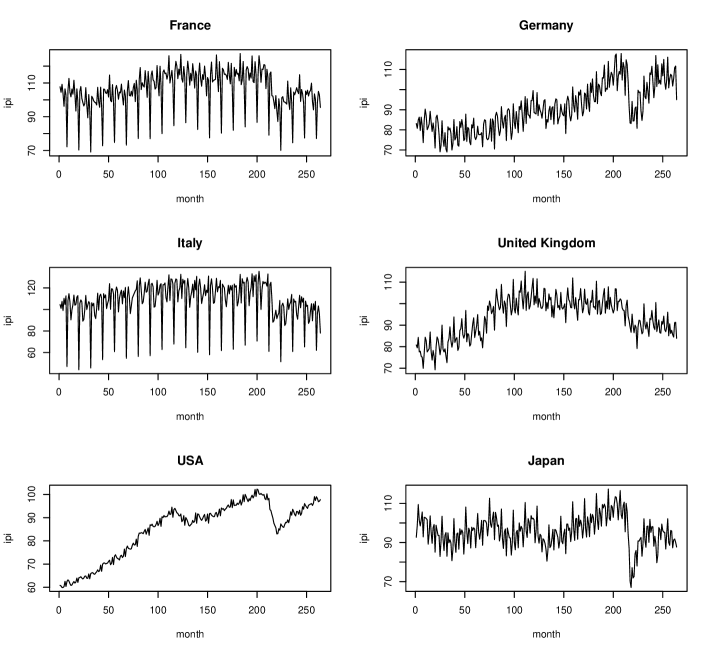

We use six series corresponding to the Industrial Production Index (IPI) of France, Germany, Italy, United Kingdom, USA and Japan. We use monthly data from January 1991 to December 2012 and the data are taken from Eurostat. The seven series are plotted in Figure 1.

Let the first DPCk. In Table 2 we show the percentage of variability explained by and using lags, computed as MSE for where is the variance of the series

We note that the reconstruction of the series using the DPC is notably better that the one obtained by means of the OPC with the same lags. Increasing the number of lags obviously improves the reconstruction obtained by both components, although the improvement is larger with the DPC. With 12 lags the reconstruction error with the first DPC is smaller then 3.5%. Table 3 includes the coefficients of the six IPI series in the ordinary PC and in the first DPC with

| PC | PC(0) | PC(1) | DPC(0) | DPC(1) |

|---|---|---|---|---|

| -0.456 | -0.456 | -0.001 | -3.951 | 3.965 |

| -0.285 | -0.275 | -0.034 | -1.509 | 1.492 |

| -0.719 | -0.750 | 0.099 | -6.548 | 6.577 |

| -0.298 | -0.269 | -0.092 | -2.114 | 2.111 |

| -0.241 | -0.198 | -0.138 | -0.787 | 0.760 |

| -0.212 | -0.212 | -0.001 | -1.885 | 1.894 |

For the OPC the coefficients in the first column in Table 3 coincide with the weights given to each country in the definition of the OPC. Thus, the first OPC gives the largest weight to Italy and then France, because of the strong seasonality of these series which have the largest variability. The second and third columns show that for reconstructing the original variables including the lag of the OPC is practically irrelevant. The fourth and fifth columns show that the DPC with one lag is almost equivalent to using the first difference of the DPC in the reconstruction of the series.

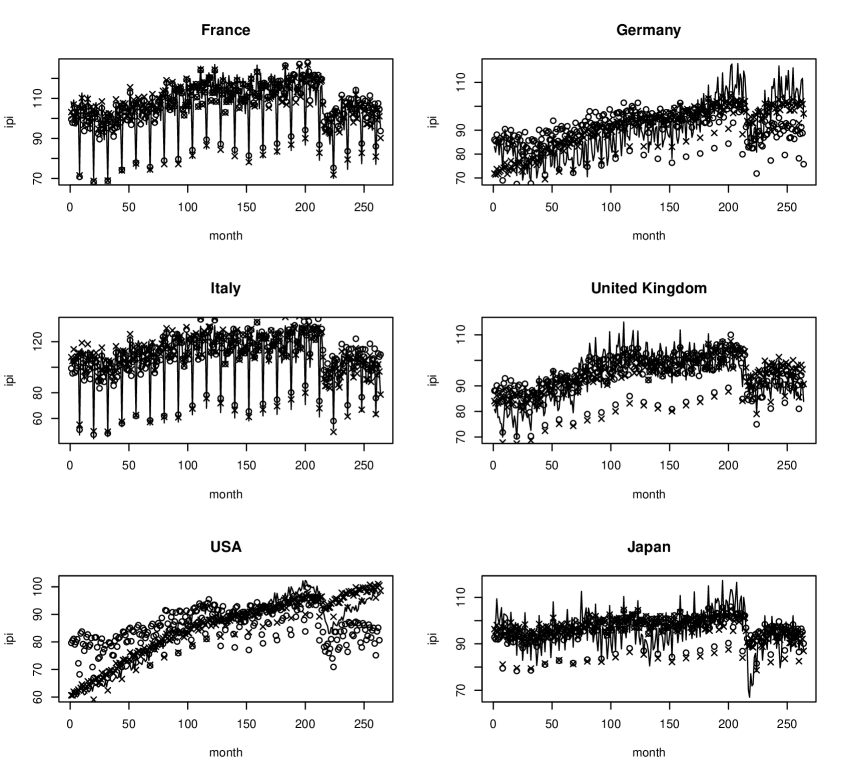

Figure 2 shows the original and reconstructed values using the first OPC and the first DPC, both with one lag. We can see that the reconstruction obtained with the DPC is clearly better than the one obtained with the OPC for Germany and USA. In the other cases the reconstruction with the DPC is still better but the differences are smaller and therefore more difficult to detect in the plots.

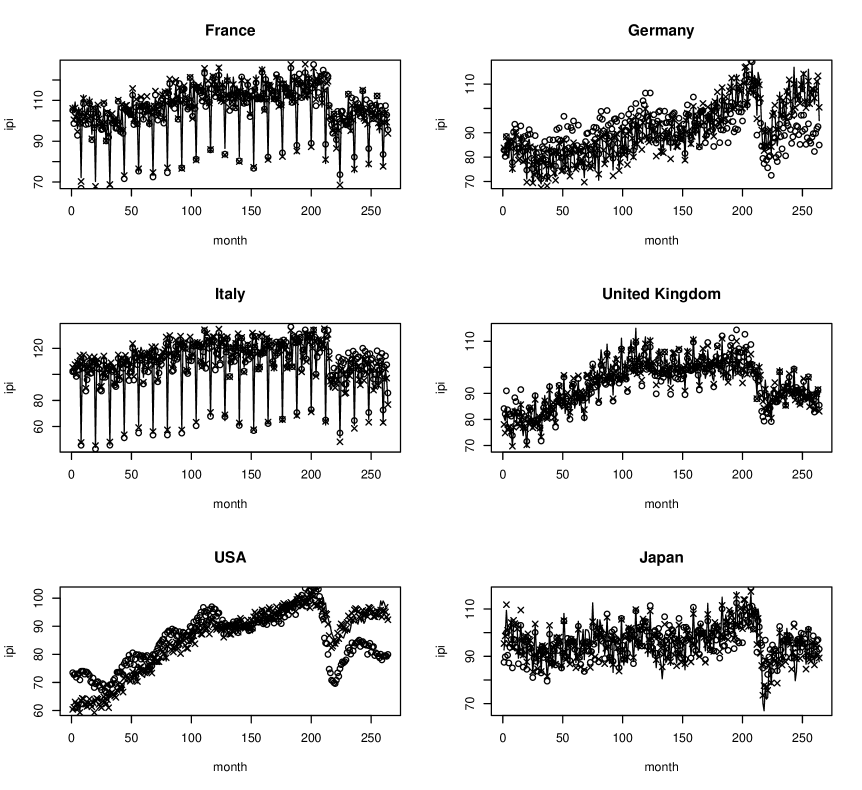

Figure 3 is similar to figure 2 but with twelve lags. Note that the reconstruction errors are significantly smaller than in the case of one lag, and that there is an important improvement of the reconstruction series when using the DPC instead of the OPC.

4.2 Example 2.

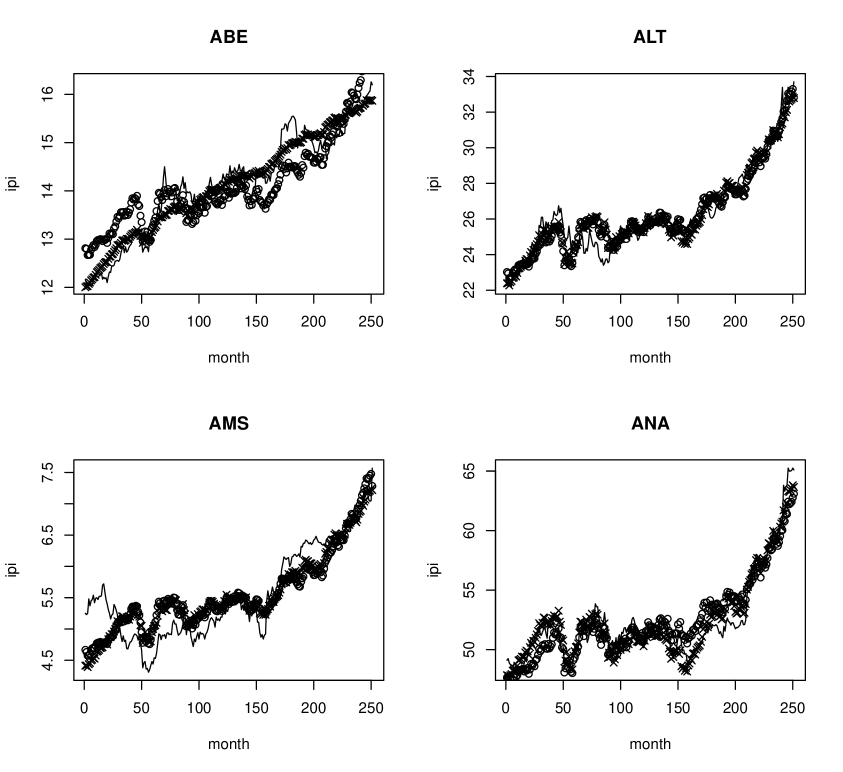

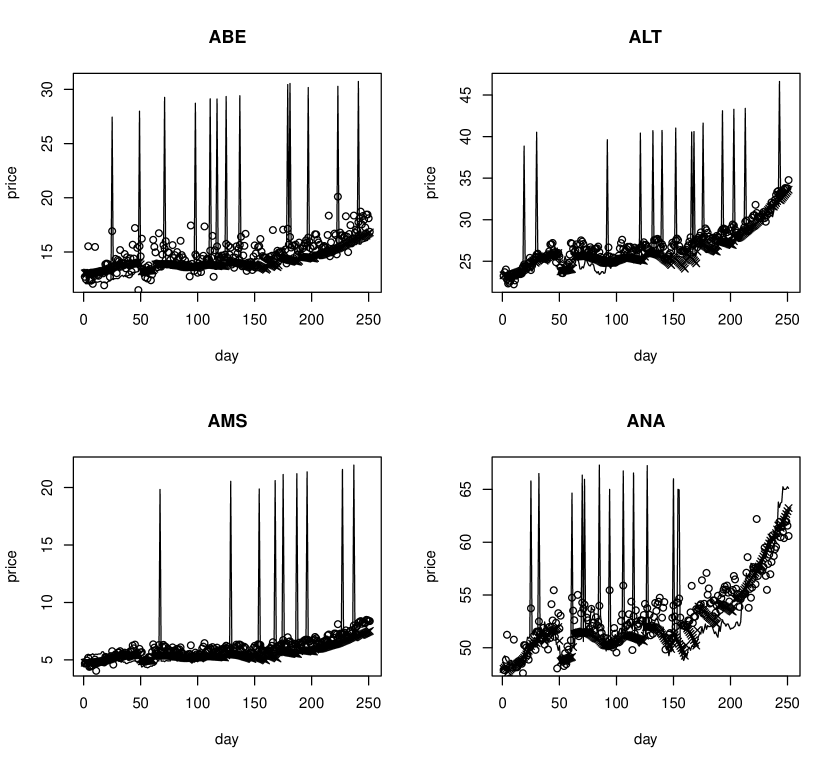

In this example the data set is composed of 31 daily stock prices in the stock market in Madrid corresponding to the 251 trading days of the year 2004. These 31 series are the main components of the IBEX (general index of the Madrid stock market). The source of the data is the Ministry of Economy, Spain. In Table 4 we show the explained variability of the reconstructed series using the DPC and OPC with different lags

| 0 | 0.598 | 0.598 |

|---|---|---|

| 1 | 0.602 | 0.822 |

| 5 | 0.610 | 0.873 |

| 10 | 0.620 | 0.881 |

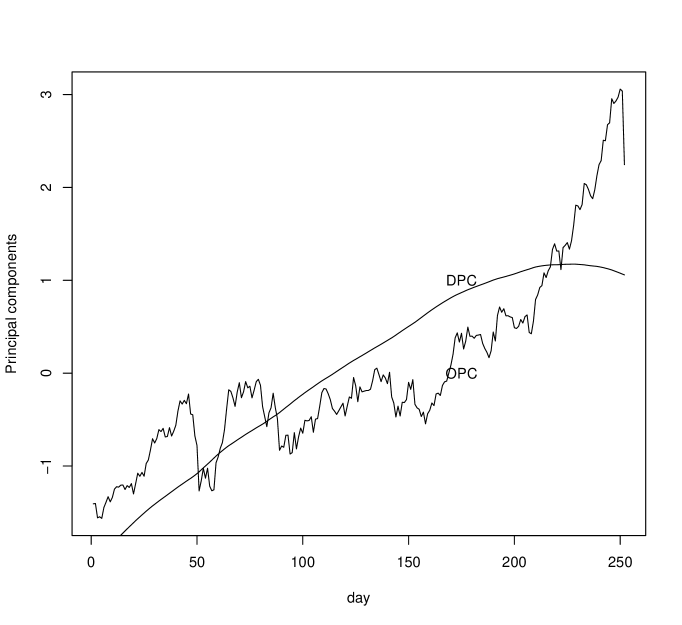

In Figure 4 we show the first four series in alphabetic order out of the thirty one and their reconstruction obtained by the first OPC and DPC with one lag. As shown in Table 4 including one lag in the OPC does not make much difference in the results, but it has a deep effect when using the DPC. In fact, in the case of the DPC, the coefficient of the one lag variable is very close but with opposite sign to the instantaneous coefficient and therefore the reconstruction is similar to the one obtained using the first difference of the first DPC without lags. Figure 5 presents the first OPC and the DPC. The dynamic principal components seems to be very useful to represent the general trend of the set of time series.

5 Robust Dynamic Principal Components

As most of the procedures minimizing the mean square error, the DPC defined by (4) is not robust. In fact a very small fraction of outliers may have an unbounded influence on For this reason we are going to study a robust alternative. One of the standard procedures to obtain robust estimates for many statistical models is to replace the minimization of the mean square scale for the minimization of a robust M-scale. This strategy was used for many statistical models, including among other linear regression (Rousseeuw and Yohai, 1984), the estimation of a scatter matrix and multivariate location for multivariate data (Davis, 1987) and to estimate the ordinary principal components (Maronna, 2005). The estimators defined by means of a robust M-scale are called S-estimators. In this section we extend the S-estimators for the case of the DPC.

Special care is required for time series with strong seasonality. The reason is that a robust procedure may take the values corresponding to a particular season which is very different to the others as outliers, and therefore downweight these values. As a consequence, the reconstruction of these observations may be affected by large errors. Thus, the procedure we present here assumes that the series have been adjusted by seasonality and therefore this problem is not present.

5.1 S-Dynamic Principal Components

Let be a symmetric, non-decreasing function for and Given a sample , the M-scale estimator is defined as the value solution of

| (15) |

If is bounded, then the breakdown point to of that is, the minimum fraction of outliers than can take to is Moreover, the breakdown point to 0, that is, the minimum fraction of inliers that can take to 0, is ). Note that if both breakdown points are 0.5 (see section 3.2.2. in Maronna, Martin and Yohai, 2006). In what follows we assume without loss of generality that . We also assume that so that both breakdowns are equal 0.5. Moreover is chosen so that where is the standard normal distribution. This condition guarantees that for normal samples is a consistent estimator of the standard deviation. One very popular family of functions is the Tukey biweight family defined by

Then, we can define the first S-DPC as follows: for let

where Define

| (16) |

| (17) |

then is the the first S-DPC and and are the coefficients to reconstruct the ’s from

Note that the only difference with the definition given in (4) is that instead of minimizing the MSE of the residuals, we minimize the sum of squares of the robust M-scales applied to the residuals of the series. Put

| (18) |

Note that satisfies

| (19) |

Define the weights

| (20) |

and

| (21) |

where . Let

be the

matrix defined by

| (22) |

the matrix with elements

and

| (23) |

Differentiating (19) with respect to we get the following equation

| (24) |

Let be the matrix with -th row ( and be the diagonal matrix with diagonal equal to . Then differentiating (19) with respect to and we get

| (25) |

Then the first S-PDC is determined by equation (18),(24)and (25). Note that the estimator defined by (4) is an S-estimate corresponding to and In this case ad then we have and for all and all Then for this case (24) and (25) become (7) and (8) respectively.

The second S-DPC is defined as the first S-DPC of the residuals Higher order S-DPC are defined in a similar manner.

One important point is the choice of At first sight, may seem a good choice, since in this case we are protected against up to 50 % of large outliers. However, the following argument shows that this choice may not be convenient. The reason is that with this choice, the procedure has the so called 50% exact fitting property. This means that when 50 % of the s are zero the scale is 0 no matter the value of the remaining values. Moreover, if 50 % of the are small the scale is small too. Then when the procedure may choose and so to reconstruct the values corresponding to 50% of the periods even if the dataset do not contain outliers.. For this reason it is convenient to choose a smaller value as as for example In that case to obtain it is required that 90% of the s be 0.

One may wonder why for regression is common to use and the 50% exact fitting property does not bring the problems mentioned above. The reason is that in this case, if there are no outliers, the regression hyperplane fitting 50% of the observations also fits the remaining 50%. This does not occur in the case of the dynamic principal components.

5.2 Computational algorithms for the S-dynamic principal components

The compute the first S-DPC we propose to use an iterative algorithm. We start the computing algorithm in step 0, and denote by and the values computed in step

The initial value can be chosen equal to a regular (non dynamic) robust principal component, for example the one proposed in Maronna (2005). Once is computed we can use this value to compute a matrix with -th row . The -th of and can be obtained using a regression S-estimate taking as response and as design matrix. Finally

Then to define the algorithm is enough to describe how to compute

once

is known. This is done in

the following three steps:

- step 1

- step 2

- step 3

-

Compute

The procedure is stopped when

where is a fixed small value.

A procedure similar to the one described at the end of Section 2 can be used to determine a convenient number of lags and components replacing the MSE by the SRS.

5.3 Example 3

We will use the data of example 2 to illustrate the performance of the robust DPC. This dataset was modified as follows: each of the 7781 values composing the dataset was modified with 5% probability adding 20 to the true value. In Table 5 we include MSE in the reconstruction of the series with the DPC. Since the DPC is very sensitive to the presence of outliers, we also compute the S-DPC. Since the MSE is very sensitive to outliers, we evaluate the performance of the principal components to reconstruct the series by using the SRS criterion. We take as the bisquare function with and These values make the M-scale consistent to the standard deviation in the Gaussian case. Table 5 gives the MSE of the non DPCk and the SRS for the DPCk and S-DPCk for and .

| MSE of the DPCk | SRS of the DPCk | SRS of the S-DPCk | |

|---|---|---|---|

| 1 | 309.70 | 106.69 | 39.84 |

| 5 | 295.84 | 119.03 | 37.81 |

| 10 | 274.74 | 111.33 | 31.95 |

Figure 6 shows the reconstruction of the four stock prices by using the DPC and the S-DPC. It can be seen, as expected, that the robust methods has a better performance.

6 Conclusions

We have proposed two dynamic principal components procedures for multivariate time series: the first one using a minimum squared error criterion to evaluate the reconstruction of the original time series and the second one based on a robust scale. These procedures, in contrast to previous ones, can also be applied for nonstationary time series. A Monte Carlo study shows that the proposed dynamic principal component based on the MSE criterion can improve considerably the reconstruction obtained by both ordinary principal components and a finite sample version of Brillinger approach. We have also shown in an example that the robust procedure based on a robust scale is not much affected by the presence of outliers.

A simple heuristic rule to determine a convenient value for the number of components, and the number of lags, is suggested. However, further research may lead to better methods to choose these parameters in order to balance accuracy in the series reconstruction and economy in the number of values stored for that purpose.

7 Appendix

7.1 Proof of (24)

Differentiating MSE with respect to for

we get

where denote minimum of and and

maximum. Then, we have

| (26) |

that can be written as

| (27) |

where and are the left and right side of (26) respectively. Putting we have

| (28) | ||||

| (29) |

and calling

| (30) |

where is given by (5)

Now we will get an expression for Putting we get

7.2 Proof of (10)

To prove (10) it is enough to show that we can find such that

| (32) |

and

| (33) |

In this case (10) holds with

| (34) |

According to (32) should satisfy

| (35) |

A necessary and sufficient condition for the existence of a real solution of this equation is that which is equivalent to

| (36) |

To prove this is enough

which is always true. Solving (35) we get that one of the roots is

and therefore and using (34) and (36) we get , proving (33).

7.3 Derivation of (24) and (25)

Differentiating (17) with respect to we get

| (38) |

where is given by (21). This equation can also be written as

| (39) |

where

and

Putting we get

| (40) |

where is the defined in (22). Putting we get

| (41) |

where is the matrix defined in (23) and Then from (39), (40) and (41) we derive (24). Differentiating (19) with respect to and we get

References

Ahn, S. K. and Reinsel, G. C. (1988). Nested reduced-rank autoregressive models for multiple time series, Journal of the American Statistical Association, 83, 849–856.

Ahn, S. K. and Reinsel, G. C. (1990). Estimation for partially nonstationary multivariate autoregressive models, Journal of the American Statistical Association, 85, 813–823.

Box, G.E.P. and Tiao, G. C. (1977). A canonical analysis of multiple time series, Biometrika, 64, 355–365.

Brillinger, D. R. (1981). Time Series Data Analysis and Theory, Expanded edition, Holden-Day, San Francisco.

Davies, P.L. (1987), Asymptotic Behavior of S-Estimators of Multivariate Location Parameters and Dispersion Matrices, The Annals of Statistics, 15, 1269-1292.

Forni, M., Hallin, M., Lippi, M. and Reichlin, L. (2000). The generalized dynamic factor model: Identification and estimation, The Review of Economic and Statistics, 82, 540–554.

Ku, W., R.H. Storer, and C. Georgakis (1995) Disturbance detection and isolation by dynamic principal component analysis. Chemometrics and Intelligent Laboratory Systems, 30, 179-196.

Lam, C. and Yao, Q. (2012) Factor modeling for high dimensional time series: Inference for the number of factors, The Annals of Statistics, 40, 2, 694-726.

Maronna, R.A. (2005) Principal Components and Orthogonal Regression Based on Robust Scales, Technometrics, 47, 264-273.

Maronna, R. A., Martin, R. D., and Yohai, V. J. (2006) Robust Statistics, Wiley, Chichester.

Peña, D. and Box, G.E.P. (1987). Identifying a simplifying structure in time series, Journal of the American Statistical Association, 82, 836–843.

Peña, D. and Poncela, P. (2006). Nonstationary dynamic factor analysis, Journal of Statistical Planning and Inference, 136,4, 1237-1256.

Reinsel, G. C. and Velu, R. P. (1998). Multivariate Reduced-Rank Regression, Springer, New York.

Rousseeuw, P.J. and Yohai, V. (1984), “Robust Regression by Means of S estimators”, in Robust and Nonlinear Time Series Analysis, edited by J. Franke, W. Härdle, and R.D. Martin, Lecture Notes in Statistics 26, Springer Verlag, New York, 256-274.

Seber, G.A.F. (1984) Multivariate observations, Wiley, New York.

Shumway, R.H. & Stoffer, D. S. (2000). Time Series Analysis and Its Applications. New York: Springer.

Stock, J.H. and Watson, M.W. (1988) Testing for Common Trends. Journal of the American Statistical Association, 83, 1097-1107.

Tiao, G. C. and Tsay, R.S. (1989). Model specification in multivariate time series. Journal of the Royal Statistical Society, Series B, 51, 157- 195.