Bayesian Optimal Control of Smoothly Parameterized Systems:

The Lazy Posterior Sampling Algorithm

Abstract

We study Bayesian optimal control of a general class of smoothly parameterized Markov decision problems. Since computing the optimal control is computationally expensive, we design an algorithm that trades off performance for computational efficiency. The algorithm is a lazy posterior sampling method that maintains a distribution over the unknown parameter. The algorithm changes its policy only when the variance of the distribution is reduced sufficiently. Importantly, we analyze the algorithm and show the precise nature of the performance vs. computation tradeoff. Finally, we show the effectiveness of the method on a web server control application.

1 Introduction

The topic of this paper is Bayesian optimal control, where the problem is to design a policy that achieves optimal performance on the average over control problem instances that are randomly sampled from a given distribution. This problem naturally arises when the goal is to design a controller for mass-produced systems, where production is imperfect but the errors follow a regular pattern and the goal is to maintain a good average performance over the controlled systems, rather than to achieve good performance even for the system with the largest errors.

In a Bayesian setting, the optimal policy (which exists under appropriate regularity conditions) is history dependent. Given the knowledge of the prior, the transition dynamics and costs, the problem in a Bayesian setting is to find an efficient way to calculate the actions that the optimal policy would take given some history. Apart from a few special cases, the optimal policy is not available analytically and requires the evaluation of an intractable integral over action sequences (Martin, 1967), forcing one to resort to use some suboptimal policy. The question is then how well the suboptimal policy performs compared to the optimal (but infeasible) policy.

This question was answered in a certain sense for finite state and action spaces by Asmuth et al. (2009) and Kolter and Ng (2009). Both works propose specific computationally efficient algorithms, which are shown to be -Bayes-optimal with probability with the exception of many steps, where for both algorithms and are both part of the input. While Kolter and Ng (2009) suggest to add an exploration bonus to the rewards while using the mean estimates for the transition probabilities and considers a finite horizon setting, Asmuth et al. (2009) consider discounted total rewards and a variant of posterior sampling, originally due to Thompson (1933) and first adapted to reinforcement learning by Strens (2000). More recently, the algorithm of Strens (2000) was revisited by Osband et al. (2013) in the context of episodic, finite MDPs. Unlike the previously mentioned algorithms, the posterior sampling algorithm requires neither the target accuracy , nor the failure probability as its inputs. Rather, the guarantee presented by Osband et al. (2013) is that the algorithm’s regret, i.e., the excess cost due to not following the optimal policy, is bounded by 111 hides poly-logarithmic factors. both with high probability and in expectation. Of course, the above is just a small sample of the algorithms developed for Bayesian reinforcement learning, but as far as we know, apart from these, there are no works on algorithms that come with theoretical guarantees. Nevertheless, the reader interested in further algorithms may consult the papers of Vlassis et al. (2012) and Guez et al. (2013) who give an excellent overview of the literature.

The starting point of our paper is that of Osband et al. (2013). In particular, just like Osband et al. (2013), we study the posterior sampling algorithm of Strens (2000). However, unlike Osband et al. (2013), we allow the state-action space to be infinite (subject to some regularity conditions discussed later) and we consider the infinite horizon, continuing setting. In fact, our results show that the issue of the cardinality of the state-action space is secondary to whether there exists a compact description of the uncertainty of the controlled system; here we consider the case when the dynamics is smoothly parameterized in some unknown parameters. As proposed by Strens (2000), the algorithm works in phases: At the beginning of each phase, a policy is computed based on solving the optimal control problem for a random parameter vector drawn from the posterior over the parameter vectors. The algorithm keeps the policy until the parameter uncertainty is reduced by a substantial margin, when a new phase begins and the process is repeated.

An important element of the algorithm is that the lengths of phases is adjusted to the uncertainty left. While in the case of episodic problems the issue of how long a policy should be kept does not arise, in a continuing problem with no episodic structure, if policies are changed too often, performance will suffer (see, e.g., Example 1 of Guez et al. (2014)). To address this challenge, for non-episodic problems, Strens (2000) suggested that the lengths of phases should be adjusted to the “planning horizon” (Strens, 2000), which however, is ill-defined for the average cost setting that we consider in this paper. The idea of ending a phase when uncertainty is reduced by a significant margin goes back at least to Jaksch et al. (2010).

Our main result shows that under appropriate conditions, the expected regret of our algorithm is , where is the number of time steps and is controlled by the precision with which the optimal control problems are solved, thus providing an explicit bound on the cost of using imprecise calculations. Thus, the main result of the paper shows that near-optimal Bayesian optimal control is possible as long as we can efficiently sample from the parameter posteriors and if we can efficiently solve the arising classical optimal control problems. Our proofs combine the proof techniques of Osband et al. (2013) with that of Abbasi-Yadkori and Szepesvári (2011).

2 Problem Setting

We consider problems when the transition dynamics is parameterized with a matrix size=,color=green!20!white,]Csaba: Why does it have to be a matrix!!?!? , which is sampled at time (before the interaction with the learner starts) from a known prior with support . Let be the state space and be the action space, be the state at time and be the action at time , which is chosen based on . It is assumed that is sampled from a fixed distribution (although, it should become clear later that this assumption is not necessary). For positive semidefinite, define , where denotes the spectral norm of matrices. The set of positive semidefinite matrices will be denoted by . Our main assumption concerning the transition law is as follows:

-

Assumption A1 (Smoothly Parameterized Dynamics) The next state satisfies , where is independent of the past and . Further, there exists a (known) map such that for any , if , with , then . size=,color=green!20!white,]Csaba: Relaxing this? Taylor series expansion of ?

size=,color=green!20!white,]Csaba: Note that (which might be easier to prove) is sufficient to meet this assumption. Indeed, if this latter is satisfied, we also have . The first part of the assumption just states that given , the dynamics is Markovian with state , while the second part demands that small changes in the parameter lead to small changes in the next state. That the map is “known” allows us to use it in our algorithms. Examples of systems that fit our assumptions include finite MDPs (where the state is represented by unit vectors) and systems with linear dynamics (i.e., when , where ). size=,color=green!20!white,]Csaba: Need to remove “linear parameterization” from intro etc.

The goal is to design a controller (also known as a policy) that at every time step , based on past states and actions , selects an action so as to minimize the expected long-run average loss . We consider any noise distribution and any loss function as long as a boundedness assumption on the variance and a smoothness assumption on the value function are satisfied (see Assumptions 4 and 4-ii below). It is important to note that we allow to be a nonlinear function of the last state-action pair, i.e., the framework allows one to go significantly beyond the scope of linear quadratic control as many nonlinear control problems can be transformed into a linear form (but with a nonlinear loss function) using the so-called dynamic feedback linearization techniques (Isidori, 1995). size=,color=green!20!white,]Csaba: Follow up in conclusion

As it was mentioned before, computing a (Bayesian) optimal policy which achieves the best expected long-run average loss is computationally challenging (Martin, 1967). size=,color=green!20!white,]Csaba: Any hardness results? Hence, one needs to resort to approximations. To measure the suboptimality of an arbitrary (history dependent) policy , we use the (expected) regret of :

Here, denotes the state-action trajectory that results from following the policy . The slower the regret grows, the closer is the performance of to that of an optimal policy. If the growth rate of is sublinear (, the average loss per time step will converge to the optimal average loss as gets large and in this sense we can say that asymptotically-optimal. Our main result shows that, under some conditions, the construction of such asymptotically-optimal policies can be reduced to the ability of efficiently sampling from the posterior of and being able to solve classical (non-Bayesian) optimal-control problems. Furthermore, our main result also implies that .

3 The Lazy PSRL Algorithm

Our algorithm is an instance of the posterior sampling reinforcement learning (PSRL) (Osband et al., 2013). As explained beforehand, this algorithm was first proposed by Strens (2000) in the context of discounted MDPs and later analyzed by Osband et al. (2013) for undiscounted episodic problems. To emphasize that the algorithm keeps the current policy for a while, we call it Lazy PSRL. The pseudocode of the algorithm is shown in Figure 1.

Recall that denotes the prior distribution of the parameter matrix . Let denote the posterior of at time based on and the last round when the algorithm chose a policy. Further, let , where is an positive definite matrix. Then, at time , Lazy PSRL sets unless in which case it chooses from the posterior : . The action taken at time step is a near-optimal action for the system whose transition dynamics is specified by . We assume that a subroutine, , taking the current state and the parameter is available to calculate such an action. The inexact nature of calculating a near-optimal action will also be taken in our analysis.

Inputs: , the prior distribution of , . , . for do if then Sample . . else . end if Calculate near-optimal action . Execute action and observe the new state . Update posterior of with to obtain . Update . end for

4 Results for Bounded State- and Feature-Spaces

In this section, we study problems with a bounded state space. The number of states might be infinite, but we assume that the norm of the state vector is bounded by a constant. Before stating our main result, we state some extra assumptions. In Section 6, we will show that these assumptions are met for some interesting special cases.

The first assumption is a restriction on the prior distribution such that a “variance term” remains bounded by a constant. size=,color=green!20!white,]Csaba: Emphasize in discussion that this assumption replaces the concentration argument of Osband et al.

-

Assumption A2 (Concentrating Posterior) Let be the -algebra generated by observations up to time . There exists a positive constant such that for any , for some -measurable random variable, letting it holds that 222We use to denote the -norm of vector .

The idea here is that is an estimate of based on past information available at time , such as a maximum aposteriori (MAP) estimate. Since is increasing at a linear rate, the assumption requires that converges to at an rate. When , this means that should converge to at this rate, which is indeed what we expect. When , again, we expect this to be true since is expected to be in the vicinity of . We emphasize that our approach is to reduce the problem to studying the “variance like terms”, as opposed to e.g. Osband et al. (2013) who reduce the question directly to a UCB type argument.

Our next assumption concerns the existence of “regular” solutions to the average cost optimality equations (ACOEs):

-

Assumption A3 (Existence of Regular ACOE Solutions) The following hold:

-

(i)

There exists such that for any , there exist a scalar and a function that satisfy the following average cost optimality equation (ACOE) for any :

(1) where is the next-state distribution given state , action and parameter .

-

(ii)

There exists such that for all , and for all , .

-

(i)

With a slight abuse of the concepts, we will call the quantity the average loss of the optimal policy, while function will be called the value function (for the system with parameter ). The review paper by Arapostathis et al. (1993) gives a number of sufficient (and sometimes necessary) conditions that guarantee that a solution to ACOE exists. In this paper, we assume that the required conditions are satisfied. Lipschitz continuity usually follows from that of the transition dynamics and the losses. size=,color=green!20!white,size=]Csaba: Will this be satisfied in the examples? Under the Lipschitzness of the cost and the transition dynamics? Which norm is used in the assumption?

A uniform lower bound on follows, for example if the immediate cost function is lower bounded. Then, if the state space is bounded, uniform boundedness of the functions follows from their uniform Lipschitzness: size=,color=green!20!white,]Csaba: Future work: Extension to depending on . Relaxing uniform boundedness?

Proposition 1.

Assume that the value function is bounded from below () and is -Lipschitz. Then, if the diameter of the state space is bounded by (i.e., ) then there exists a solution to (1) such that the range of is included in . size=,color=green!20!white,size=]Csaba: LQ problems with bounded state spaces: This is unclear at this point. Return to this later.

Proof is in Appendix B. Finally, we assume that the map is bounded:

-

Assumption A4 (Boundedness) There exist such that for all and , .

This assumption may be strong. In the next section we discuss an extension of the result of this section to the case when this assumption is not met.

The main theorem of this section bounds the regret of Lazy PSRL. In this result, we allow the oracle to return an -suboptimal action, where . By this, we mean that the action satisfies

| (2) |

Theorem 2.

In particular, the theorem implies that Lazy PSRL is asymptotically optimal as long as and it is -optimal if .

5 Forcefully Stabilized Systems

For some applications, such as robotics, where the state can grow unbounded, the boundedness assumption (Assumption 4) is rather problematic. size=,color=green!20!white,]Csaba: The example is not that apt given that our assumptions will not be satisfied. For such systems, it is common to use a stabilizing controller that is automatically turned on and is kept on as long as the state vector is “large”. The stabilizing controller, however, is expensive (uses a large amount of energy), as it is designed to be robust so that it is guaranteed to drive back the state to the safe region for all possible systems under consideration. Hence a good controller should avoid relying on the stabilizing controller.

In this section, we will replace Assumption 4 with an assumption that a stabilizing controller is available. We will use this controller to override the actions coming from our algorithm as soon as the state leaves the (bounded) safe region until it returns to it. The pseudocode of the algorithm is shown in Figure 2.

Inputs: , the prior distribution of , , the safe region . Initialize Lazy PSRL with and , . for do if then Get action from Lazy PSRL else Get action from end if Execute action and observe the new state . Feed and to Lazy PSRL. end for

We assume that the stabilizing controller is effective in the following sense:

-

Assumption A5 (Effective Stabilizing Controller) There exists such that the following holds: Pick any , and let be the sequence of state-action pairs obtained when from time step two the Markovian stabilizing controller is applied to the controlled system whose dynamics is given by : , , , . Then, for any , where is the map of Assumption 2 underlying .

The assumption is reasonable as it only requires that the trace of is bounded in expectation. Thus, large spikes, that no controller may prevent, can exist as long as they happen with a sufficiently low probability.

The next theorem shows that Stabilized Lazy PSRL is near Bayes-optimal for the system obtained from by overwriting the action by the action if is outside of the safe region :

Theorem 3.

Consider a parameterized system with the transition probability kernel family and let be a deterministic Markovian controller. Let the smooth parameterization assumption 2 hold for , the ACOE solution regularity assumption 4 hold for . Consider running the Stabilized Lazy PSRL algorithm of Figure 2 on and let the concentration assumption 4 hold along the trajectory obtained. Then, if in addition Assumption 5 holds then the regret of Stabilized Lazy PSRL against the Bayesian optimal controller of with prior and immediate cost satisfies , where and is the suboptimality of the action computed by Lazy PSRL at time step .

6 Illustration

The purpose of this section is to illustrate the results obtained. In particular, we will consider applying the results to finite MDPs and linearly parameterized controlled systems. size=,color=green!20!white,]Csaba: Ideally, this section states two results (as corollaries). The proofs should amount to verifying the conditions of the theorems. I have copied here stuff, but I did not attempt to do this.

6.1 Near Bayes-optimal Control in Finite MDPs

Consider an MDP problem with finite state and action spaces. Let the state space be and the action space be . We represent the state variable by an -dimensional binary vector that has only one non-zero element at the current state. The feature mapping for a state-action pair is an -dimensional binary vector that, similarly to the state vector, has only one non-zero element indicating a state-action pair. In particular, the feature mapping and the parameter matrix have the following form:

Let be a state and be an action. The th row of matrix is a distribution over the state space that shows the transition probabilities when we take action in state . Thus, any row of sums to one and . An appropriate prior for each row is a Dirichlet distribution. Let be positive numbers and let . Then be our “smoother”.

Let the prior for the th row of be the Dirichlet distribution with parameters : . At time , the posterior has the form , where is the number of observed transitions to state after taking action in state during the first time steps. Matrix is a diagonal matrix with diagonal elements showing the number of times a state-action pair is observed. In particular, . Vector is an -dimensional vector and its elements show the empirical frequency of transition to state from different state-action pairs. The mean of distribution is vector and we have .

The next corollary shows the performance of Lazy PSRL when applied to a finite MDP problem. The proof is in Appendix B.

Corollary 4.

Consider Lazy PSRL applied to a finite MDP problem with states, actions, and a Dirichlet prior as specified above. Suppose in time step , the action chosen is -suboptimal. Then, for any time , the regret of Lazy PSRL satisfies .

6.2 Linearly Parametrized Problems with Gaussian Noise

Next, we consider linearly parametrized problems with Gaussian noise:

| (3) |

where is a zero-mean normal random variable. The nonlinear dynamics shown in (3) shares similarities to, but allows significantly generality than the Linear Quadratic (LQ) problem considered by Abbasi-Yadkori and Szepesvári (2011). In particular, in the LQ problem, and . Further, Abbasi-Yadkori and Szepesvári (2011) assume that the noise is subgaussian.

Next, we describe a conjugate prior under the assumption that the noise is Gaussian. Without loss of generality, we assume that . A conjugate prior is appealing as the posterior has a compact representation that allows for computationally efficient sampling methods. size=,color=green!20!white,size=]Csaba: There is a bit of a problem when we use a stabilizing controller, or not? Assume that the columns of matrix are independently sampled from the following prior: . Then, by Bayes’ rule, the posterior for column of has the form of

The next corollary shows the performance of Lazy PSRL when applied to linearly parametrized problems with Gaussian noise. We assume an effective stabilizing controller is available. The proof is in Appendix B.

Corollary 5.

Consider Stabilized Lazy PSRL applied to a linearly parametrized problem with Gaussian noise. Suppose in time step , the action chosen is -suboptimal. Then, for any time , the regret of Stabilized Lazy PSRL satisfies .

7 Experiments

The purpose of this section is to illustrate the behavior of Lazy PSRL on a simple control problem. As the control problem, we choose a web server control problem. This control problem is described first, which will be followed by the description of our results.

7.0.1 Web Server Control Application

Next, we illustrate the behavior of Lazy PSRL on a web server control problem. The problem is taken from Section 7.8.1 of the book by Hellerstein et al. (2004) (this example is also used in Section 3.4 of the book by Aström and Murray (2008)). An Apache HTTP web server processes the incoming connections that arrive on a queue. Each connection is assigned to an available process. A process drops the connection if no requests have been received in the last KeepAlive seconds. At any given time, there are at most MaxClients active processes. The values of the KeepAlive and MaxClients parameters, denoted by and respectively, are chosen by a control algorithm. Increasing and results in faster and longer services to the connections, but also increases the CPU and memory usage of the server. MaxClients is bounded in , while KeepAlive is bounded in . The state of the server is determined by the average processor load and the relative memory usage . A operating point of interest of the system is given by . A linear model around the operating point is assumed, resulting in a model of the form

where is an i.i.d. sequence of Gaussian random variables, with a diagonal covariance matrix . We test and in our experiments. Note that these state and action variables are in fact the deviations from the operating point. Hellerstein et al. (2004) fitted this model to an Apache HTTP server and obtained the parameters

while the noise standard deviation was measured to be . Hellerstein et al. (2004) found that these parameters provided a reasonable fit to their data.

For control purpose, the following cost matrices were chosen (cf. Example 6.9 of Aström and Murray (2008)):

7.0.2 Numerical Results

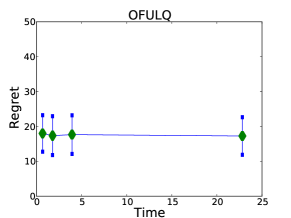

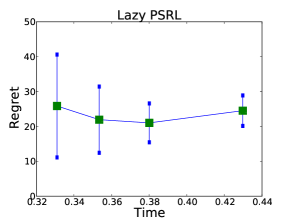

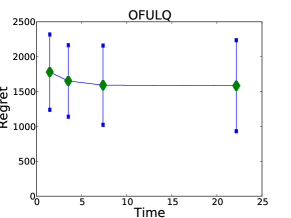

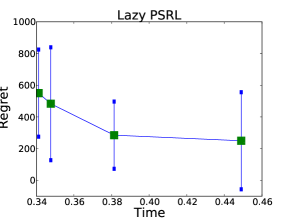

We compare the Lazy PSRL algorithm with the OFULQ algorithm (Abbasi-Yadkori, 2012) on this problem. For the Lazy PSRL algorithm, we use standard normal distribution as prior. The OFULQ algorithm is an optimistic algorithm that maintains a confidence ellipsoid around the unknown parameter and, in each round, finds the parameter and the corresponding policy that attains the smallest average loss. Specifically, the algorithm solves optimization problem , where is the average loss of the optimal policy when system dynamics is . Then, the algorithm plays action , where is the gain matrix. The objective function is not convex and thus, solving the optimistic optimization can be very time consuming. As we show next, the Lazy PSRL algorithm can have lower regret while avoiding the high computational costs of the OFULQ algorithm.

The time horizon in these experiments is . We repeat each experiment times and report the mean and the standard deviation of the observations. Figure 3 shows regret vs. computation time. The horizontal axis shows the amount of time (in seconds) that the algorithm spends to process rounds. We change the computation time by changing how frequent an algorithm updates its policy. Details of the implementation of the OFULQ algorithm are in (Abbasi-Yadkori, 2012).

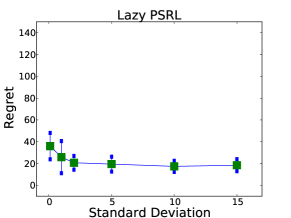

The top-left and right subfigures of Figure 3 show the regret of the algorithms when the standard deviation of the noise is . The regret of the Lazy PSRL algorithm is slightly worse than what we get for the OFULQ algorithm in this case. The Lazy PSRL algorithm outperforms the OFULQ algorithm when the noise variance is larger (bottom subfigures). We explain this observation by noting that a larger noise variance implies larger confidence ellipsoids, which results in more difficult OFU optimization problems. Finally, we performed experiments with different prior distributions. Figure 4 shows regret of the Lazy PSRL algorithm when we change the prior.

|

|

|

References

- Abbasi-Yadkori (2012) Y. Abbasi-Yadkori. Online Learning for Linearly Parametrized Control Problems. PhD thesis, University of Alberta, 2012.

- Abbasi-Yadkori and Szepesvári (2011) Y. Abbasi-Yadkori and Cs. Szepesvári. Regret bounds for the adaptive control of linear quadratic systems. In COLT, 2011.

- Arapostathis et al. (1993) A. Arapostathis, V.S. Borkar, E. Fernandez-Gaucherand, M.K. Ghosh, and S.I. Marcus. Discrete-time controlled Markov processes with average cost criterion: a survey. SIAM Journal on Control and Optimization, 31:282–344, 1993.

- Asmuth et al. (2009) J. Asmuth, L. Li, M. L. Littman, A. Nouri, and D. Wingate. A Bayesian sampling approach to exploration in reinforcement learning. In UAI, pages 19–26, 2009.

- Aström and Murray (2008) Karl J. Aström and Richard M. Murray. Feedback Systems: An Introduction for Scientists and Engineers. Princeton University Press, 2008.

- Guez et al. (2013) A. Guez, D. Silver, and P. Dayan. Scalable and efficient Bayes-adaptive reinforcement learning based on Monte-Carlo tree search. Journal of Artificial Intelligence Research, 48:841–883, 2013.

- Guez et al. (2014) A. Guez, D. Silver, and P. Dayan. Better optimism by bayes: Adaptive planning with rich models. CoRR, abs/1402.1958, 2014.

- Hellerstein et al. (2004) Joseph L. Hellerstein, Yixin Diao, Sujay Parekh, and Dawn M. Tilbury. Feedback Control of Computing Systems. John Wiley & Sons, Inc., 2004.

- Isidori (1995) A. Isidori. Nonlinear Control Systems. Springer Verlag, London, 3 edition, 1995.

- Jaksch et al. (2010) T. Jaksch, R. Ortner, and P. Auer. Near-optimal regret bounds for reinforcement learning. Journal of Machine Learning Research, 11:1563—1600, 2010.

- Kolter and Ng (2009) J. Z. Kolter and A. Y Ng. Near-bayesian exploration in polynomial time. In ICML, 2009.

- Martin (1967) J.J. Martin. Bayesian decision problems and Markov chains. John Wiley, New York, 1967.

- Osband et al. (2013) I. Osband, D. Russo, and B. Van Roy. (More) efficient reinforcement learning via posterior sampling. In NIPS, 2013.

- Strens (2000) M. Strens. A Bayesian framework for reinforcement learning. In ICML, 2000.

- Thompson (1933) W. R. Thompson. On the likelihood that one unknown probability exceeds another in view of the evidence of two samples. Biometrika, 25:285–294, 1933.

- Vlassis et al. (2012) N. Vlassis, M. Ghavamzadeh, S. Mannor, and P. Poupart. Bayesian reinforcement learning. In Marco Wieiring and Martijn van Otterlo, editors, Reinforcement Learning: State-of-the-Art, chapter 11, pages 359–386. Springer, 2012.

Appendix A Some Useful Lemmas

Lemma 6.

Let be positive definite, be positive semidefinite matrices and define , . If for all , then

Proof.

On the one hand, we have

One the other hand, thanks to , which holds for all ,

where the second inequality follows since is positive semidefinite, hence all eigenvalues of are above one and the largest eigenvalue of is , proving the first inequality. For the second inequality, note that for any positive definite matrix , . Applying this to and using the condition that , we get . Plugging this into the previous upper bound, we get the second part of the statement. ∎

Lemma 7 (Lemma 11 of Abbasi-Yadkori and Szepesvári (2011)).

Let and be positive semi-definite matrices such that . Then, we have

Appendix B Proofs

Proof of Proposition 1.

Note that if ACOE (1) holds for , then for any constant , it also holds that

As by our assumption, the value function is bounded from below, we can choose such that the is nonnegative valued. In fact, if assumes a minimizer , by this reasoning, without loss of generality, we can assume that and so for any , . The argument trivially extends to the general case when may fail to have a minimizer over . ∎

Proof of Theorem 2.

The proof follows that of the main result of Abbasi-Yadkori and Szepesvári (2011). First, we decompose the regret into a number of terms, which are then bound one by one. Define , where is the map of Assumption 2 and let be the solution of the ACOE underlying . By Assumption 4 (i), exists and for any . By Assumption 2, for any , . Hence, from (1) and (2),

where . As is a deterministic function and conditioned on , and have the same distribution,

Let be the total error due to the approximate optimal control oracle. Thus, we can bound the regret using

where the second inequality follows because and . Let denote the event that the algorithm has changed its policy at time t. We can write

where we used again that , and also Assumption 4 (ii). Define

It remains to bound and to show that the number of switches is small.

Bounding

Let be the last round before time step when the policy is changed. So . Letting , by Assumption 2,

Further,

For we have that

where the last inequality follows because is an induced norm and induced norms are sub-multiplicative. Hence, we have that

where the first inequality uses Hölder’s inequality, and the last two inequalities use Cauchy-Schwarz. By Lemma 6 in Appendix A, using Assumption 4, we have that

Denoting by the minimum eigenvalue of , a simple argument shows size=,color=green!20!white,]Csaba: Write it up, lemma in the appendix? , where in the second inequality we used Assumption 4 again. Hence,

Thus,

By Lemma 7 of Appendix A and the choice of , we have that

| (4) |

Thus,

| (by (4)) | ||||

| (by the tower rule) | ||||

| (by Assumption 4) |

Let . Collecting the inequalities, we get

Bounding

If the algorithm has changed the policy times up to time , then we should have that . On the other hand, from Assumption 4 we have . Thus, it holds that . Solving for , we get . Thus,

Putting together the bounds obtained for and , we get the desired result. ∎

Proof of Theorem 3.

First notice that 2 continues to hold if Assumption 4 is replaced by the following weaker assumption:

-

Assumption A6 (Boundedness Along Trajectories) There exist such that for all , .

The reason this is true is because 4 is used only in a context where needs to be bounded. Using that is concave, we get

With this observation, the result follows from 2 applied to Lazy PSRL and as running Stabilized Lazy PSRL for time steps in results in the same total expected cost as running Lazy PSRL for time steps in thanks to the definition of Stabilized Lazy PSRL and .

Hence, all what remains is to show that the conditions of 2 are satisfied when it is used with . In fact, 4 and 4 hold true by our assumptions. Let us check Assumption 4 next. Defining if and otherwise, we see that . Further, defining if and otherwise, we see that, thanks to the second part that of 2 applied to , for , , if and otherwise. Hence, , thus showing that 2 holds for when is replaced by . Now, Assumption B follows from Assumption 5.

∎

Proof of Corollary 4.

We prove the corollary by showing that conditions of Theorem 2 are satisfied.

Smoothly Parameterized Dynamics: Because , , and and have only one non-zero element,

where the last step holds by the fact that each row of and sum to one.

Concentrating Posterior: Let , and . We have that size=,color=green!20!white,size=]Csaba: Note to myself: Check these.

Because each row of has a Dirichlet distribution and rows of are means of these distributions, is simply the variance of the corresponding Dirichlet variable. Thus,

Boundedness: this holds by finiteness of the state space.

∎

Proof of Corollary 5.

We prove the corollary by showing that conditions of Theorem 3 are satisfied.

Smoothly Parameterized Dynamics: Because , , we have

Concentrating Posterior: Let be a random variable with probability distribution function

Notice that has the standard normal distribution. Hence . Thus, since , we have

Thus,

This shows that Assumption 4 is satisfied.

∎