Martingale approach to optimal portfolio-consumption problems in Markov-modulated pure-jump models

Oscar López oscar.lopez@urosario.edu.coUniversidad del Rosario

Calle 12C No. 4-69

Bogotá, ColombiaRafael Serrano rafael.serrano@urosario.edu.coThe authors gratefully acknowledge the financial support of FIUR research project DVG170Universidad del Rosario

Calle 12C No. 4-69

Bogotá, Colombia

Abstract

We study optimal investment strategies that maximize expected utility from consumption and terminal wealth in a pure-jump asset price model with Markov-modulated (regime switching) jump-size distributions. We give sufficient conditions for existence of optimal policies and find closed-form expressions for the optimal value function for agents with logarithmic and fractional power (CRRA) utility in the case of two-state Markov chains. The main tools are convex duality techniques, stochastic calculus for pure-jump processes and explicit formulae for the moments of telegraph processes with Markov-modulated random jumps.

1 Introduction

The object of this paper is to study the problem of maximizing expected utility from consumption and terminal wealth in an incomplete pure-jump asset price model with jump-size distributions modulated by an underlying continuous-time finite-state Markov chain, and totally inaccessible jump times that coincide with the transition times of the Markov chain. This financial market model is an extension of the jump-telegraph model proposed by López and Ratanov [14] to the case in which the underlying Markov chain has more than two states. This generalization is mainly motivated by the empirical results of Konikov and Madan [12] that suggest that more than two regimes should be considered.

Markov-modulated regime-switching models have attracted considerable attention in financial modelling in the past 15 years as they allow for time-inhomogeneity in the asset dynamics that capture important features of financial time series such as asymmetric and heavy-tailed asset returns, time-varying conditional volatility and volatility clustering, as well as structural changes in economics conditions.

Our approach to the portfolio-consumption problem is largely based on the martingale approach and convex duality techniques for utility maximization in incomplete markets initiated by He and Pearson [7], Karatzas et al. [11], Cvitanić and Karatzas [4], and extended by Kramkov and Schachermayer [13] to the general semi-martingale setting. In the particular case of market models driven by jump-diffusion, Goll and Kallsen [6], Kallsen [10] and more recently Michelbrink and Le [15], use the martingale approach to obtain explicit solutions for agents with logarithmic and power utility functions. Callegaro and Vargiolu [3] obtain similar results in jump-diffusion models with Poisson-type jumps.

To the best of our knowledge, this is the first paper that uses the martingale approach to study the problem of maximizing utility from consumption and terminal wealth in a pure-jump model with Markov-modulated jumps. Only the optimal investment problem for jump-diffusion models studied by Bäuerle and Riedler [2] seems comparable to the formulation of the problem in the present paper. They use, however, the standard dynamic programming approach and are only able to derive some bounds on the optimal policy. Moreover, they assume that the jump-sizes do not depend on the underlying Markov chain.

The main result of this paper is a sufficient condition for existence of an optimal portfolio-consumption pair. This condition is given in terms of the solution pair of a linear backward SDE with respect to the compensated (random) counting measure associated with the marked point process consisting of the jump times and the corresponding (Markov-modulated) jumps. The coefficients of the backward SDE are related to the state-price densities via the convex conjugate of the utility functions. Although the optimality condition in the main result seems rather restrictive, in the last section we show that it simplifies significantly in the case of logarithmic utility functions.

The key assumption throughout is that the compensator of the counting measure has an (intensity) kernel that is also Markov-modulated, similar to the model proposed recently by Elliott and Siu [5]. In fact, using results on jump-telegraph processes with Markov-modulated jumps, we prove that if the underlying Markov chain takes only two values, our market model actually satisfies the main assumption, hence generalizing the model of Elliott and Siu [5].

The outline of the paper is as follows. In Section 2 we describe the stochastic setting and information structure for the market model, introduce the wealth equation and define the optimal investment problem. In Section 3, following arguments similar to Michelbrink and Le [15], we formulate and prove the main result of this paper. In section 4 we present some basic properties of the telegraph process with Markov-modulated jumps and prove that our market model satisfies the main assumption in the case of two regimes. Finally, Section 5 illustrates the main result by considering the special case of agents with logarithmic and fractional power (CRRA) utility. We also present some numerical results for the case of logarithmic utility and, using results from Section 4, we find a closed-form solution for the optimal value function in the case of two regimes.

2 Market model, wealth equation and portfolio-consumption problem

In this section we describe the stochastic setting and information structure for the market model and introduce the wealth process and utility maximization problem from consumption and terminal wealth.

We fix an finite investment horizon Let be a continuous-time Markov chain with finite state-space Let denote the jump times of the Markov chain and let denote the state of right before the -th jump.

Let be an Euclidean space with Borel -algebra For each , let denote a sequence of -valued independent random variables with distributions

For each the event represents that the economy or business cycle is in the -th state at time Let with and denote the vectors of instantaneous interest rates and stock appreciation rates in each state or regime. The financial market consists of a default-free money-market account with Markov-modulated continuously compounded return rate that is, its price process satisfies

and a risky asset or stock with price process solution of the equation

(2.1)

where is the pure-jump process with Markov-modulated jumps

For each is a measurable map, integrable with respect to the distribution Throughout, we assume that the distributions are pairwise independent, as well independent of the Markov chain

Let be the random counting measure associated with the sequence defined as

The random measure is known as marked point process or multivariate point process with mark space see e.g. Jacod and Shiryaev [8, Chapter III, Definition 1.23] or Jeanblanc et al [9, Section 8.8].

For each the counting process counts the number of marks with values in up to time The underlying filtration is defined as the filtration generated by these counting processes, augmented with the -algebra of -null events,

The predictable -algebra on is defined as the -algebra generated by adapted left-continuous processes. A real-valued process is said to be -predictable if the random function is measurable with respect to .

Similarly, a map is said to be -predictable if it is measurable with respect to the product -algebra For -predictable, we may define the stochastic integral of with respect to the random measure as follows

Using this definition, we can rewrite equation (2.1) as

(2.2)

The solution of this linear equation is given by the process

Here, denotes the stochastic (Doléans-Dade) exponential, see e.g. Jeanblanc et al [9, Section 9.4.3]. Moreover, since the price process satisfies

The log-returns of the stock process are then given by the pure-jump process with Markov-modulated random jumps

For an agent willing to invest in the financial market described above, let denote the fraction of wealth invested in the risky asset at time so that the fraction of wealth invested in the money account is Recall that a positive value for represents a long position in the risky asset, whereas a negative stands for a short position.

During the time interval the investor is allowed to consume at an instantaneous consumption rate In the following, we consider only portfolio-consumption pairs that are -predictable, satisfy the integrability condition

as well as the so-called self-financing condition, that is, for an initial wealth and a portfolio-consumption pair the wealth at time of the investor satisfies the stochastic differential equation

(2.3)

We denote with the solution to equation (2.3). In particular, if there is no consumption i.e. for all equation (2.3) is linear and its solution is given explicitly by

(2.4)

Notice that this is always positive if, for instance, short-selling is not allowed for any of the assets i.e. if for all

We can use (2.4) to find an expression for the wealth process in terms of the wealth process with initial wealth and portfolio-consumption pair as follows: consider the process

In differential form, we have Then

Since by uniqueness of solution to equation (2.3), the wealth process is a modification of

(2.5)

Notice that the portfolio-consumption pair leads to positive wealth at time if, almost surely

The class of admissible pairs for initial wealth is defined as the set of portfolio-consumption pairs for which equation (2.3) possesses an unique strong solution such that a.s. for all

We now define the utility maximization problem for optimal choice of portfolio and consumption processes.

Let and denote consumption and

investment utility functions respectively, satisfying the following conditions

(i)

and

for all

and

(ii)

for each the mappings

and

are strictly increasing, strictly concave, of class on

such that

(iii)

and

are continuous on .

Given the initial state of the Markov chain let denote the class of admissible portfolio-consumption strategies such that

where is the negative part of and We define the utility functional

and consider the following utility maximization problem from terminal wealth and consumption

(2.6)

An admissible portfolio-consumption pair is said to be optimal for the initial state and initial wealth if

3 Martingale approach and main result

Recall that the compensator of the marked point process is the unique (possibly, up to a null set) predictable random measure such that, for every predictable map the two following conditions hold

i.

The process

is predictable.

ii.

If the process

is increasing and locally integrable, then

is -local martingale (see e.g. Jeanblanc et al [9, Definition 8.8.2.1]).

The following is the main assumption for the rest of this section

Assumption A.1.

There exists with for all such that the compensator of satisfies

(3.1)

Remark 3.1.

Condition (3.1) is similar to the main assumption in the recent paper by Elliott and Siu [5]. In the next section, using properties of jump-telegraph processes, we will prove that Assumption A.1 actually holds for our market model in the case of a two-state Markov chain.

Remark 3.2.

Under Assumption A.1, the counting process is an inhomogeneous Poisson process with stochastic (Markov-modulated) intensity see e.g. Jeanblanc et al [9, Section 8.4.2] or the proof of Corollary 4.5 below.

Let denote the compensated martingale measure associated with the counting measure We define equivalent martingale probability measures via the Radon-Nikodym densities

where is the solution of the linear SDE

(3.2)

and, for each is a nonnegative-valued -predictable map satisfying a.s. In what follows, we denote

If the process satisfies then is a -martingale under and defines a probability measure on see e.g. Theorem T10 in Brémaud [1, Chapter VIII]. Moreover, the compensator measure of under satisfies

where, for each

and

Remark 3.3.

If

(3.3)

for some then and defines a probability measure on see e.g. Theorem T11 of Brémaud [1, Chapter VIII]. For the same holds if condition (3.3) is satisfied with see Remark 4.4 below.

Let denote the set of -tuples of non-negative valued -predictable maps for which is a -martingale and the following condition holds

(3.4)

Remark 3.4.

Under condition (3.4), the discounted asset price is a -local martingale. Indeed, let denote the compensated martingale measure associated under the equivalent probability measure Then, we have

and the claim follows. Moreover, since for the market model is arbitrage-free (see e.g. Remark 1 of Ratanov and Melnikov [16] for the case of two-regimes and deterministic jumps). Then, by the first fundamental theorem of asset pricing, the set is non-empty.

For each we define the state price density process by

The following is a well-known result for the state price density process usually referred to as budget constraint. We include the proof for the sake of completeness.

Proposition 3.5.

For all and we have

(3.5)

Proof.

Using the product rule for jump processes and (3.4), we have

Integrating, we get

almost surely, for all The stochastic integral in the right hand side is a -local martingale which is bounded below, hence a super martingale, and (3.5) follows.

∎

We now introduce an auxiliary functional related to the convex dual of the utility functions. Let denote either or with fixed. Let denote the inverse of so that

Then, satisfies

In particular,

(3.6)

Notice that where is the Legendre-Fenchel transform of the map The map is known as the convex dual of the utility function

For the rest of this section we fix the initial regime For we define the map

Let For each we denote and define the process and random variable as follows

By the previous Lemma, we have where is the optimal value function of the minimization problem

(3.8)

In Theorem 3.7 below, we find sufficient conditions to ensure as well as the existence of an optimal portfolio-consumption process

For each and consider the processes defined as

and

Observe that and for all Moreover, satisfies

(3.9)

that is, the process is an -martingale. Let denote the essentially unique martingale representation coefficient of with respect to the compensated measure

(3.10)

see e.g. Theorem T8 in Section VIII of Brémaud [1]. Then, the pair satisfies the linear backward SDE

(3.11)

with final condition The following is the main result of this paper

Theorem 3.7.

For and fixed, suppose there exist and a -predictable portfolio process satisfying

(3.12)

Assume also that the wealth equation (2.3) has a solution for where . Then the following assertions hold

(a)

The pair belongs to and solves the optimal portfolio-consumption problem (2.6),

(b)

the wealth process is a modification of the process ,

(c)

the optimal value function for the utility maximization (2.6) satisfies where

Proof.

We prove first part (b). Since it suffices to show that satisfies the wealth equation for the pair Notice first that, by the definition of the process satisfies the linear stochastic equation

Using integration formula for marked point processes (see e.g. Jeanblanc et al [9, Section 8.8]), the differential of is given by

and part (b) follows. In particular, we have a.s. This in turn implies

(3.13)

and part (a) follows from Lemma 3.6. Part (c) follows easily since

∎

Remark 3.8.

Although optimality condition (3.12) looks rather restrictive, as we will see in the last section, it simplifies significantly in the case of logarithmic utility functions.

4 Telegraph processes with Markov-modulated random jumps

In this section we revisit briefly the telegraph model with Markov-modulated random jumps introduced recently by López and Ratanov [14]. We assume that the Markov chain takes only two values with intensity matrix Thus, is given by the jump-telegraph process

(4.1)

We assume that the alternating tendencies and satisfy By fixing the initial state , we have the following equality in distribution

(4.2)

where the process is a jump-telegraph process as in (4.1) independent of starting from the opposite initial state .

Figure 1: A sample path of with , and initial state .

We denote and define as the density function of the random variable given the initial

(4.3)

That is, for any , we have

Recall that the holding or inter-arrival times of the Markov chain are exponentially distributed with

(4.4)

Here we have set Using (4.4) and (4.2) together with the total probability theorem, it follows that the densities functions satisfy the following system of integral equations on

where is Dirac’s delta function. This system is equivalent to the following system of coupled partial integro-differential equations on

(4.5)

with initial conditions .

Theorem 4.1.

Assume for Then the conditional expectations of the random variables satisfy

(4.6)

where

Proof.

By definition, we have

Differentiating the above equation, using the system (4.5) and integrating by parts, we obtain the following system of ODEs

with initial conditions . The unique solution of this Cauchy problem is given by (4.6).

∎

Theorem 4.2.

Assume for Then the conditional exponential moments of the random variables satisfy

(4.7)

where

and .

Proof.

By definition, we have

Differentiating the above equation, using the system (4.5) and integrating by parts, we obtain the following system of ODEs

with initial conditions . The unique solution of this Cauchy problem is given by (4.7).

∎

Theorem 4.3.

Suppose that for . Then the processes

(4.8)

and

(4.9)

are -martingales.

Proof.

Observe that is a jump-telegraph process with Then, by Theorem 4.1 we have

(4.10)

Let be fixed. Let be the value of at time and let be the value of at time By the strong Markov property, we have the following conditional identities in distribution

(4.11)

where , , and

are copies of the processes , , and , respectively, independent of

Then, using (4.10) and (4.11), we obtain

and the first part follows. Now, if we define the jump-telegraph process

then we have and by Theorem 4.2 we find that , . Using this and (4.11), we obtain

and the desired result follows.

∎

Remark 4.4.

Let denote the Radon-Nikodym densities defined in the previous section. Then with

By Theorem 4.3, if it is enough to have to guarantee that is a -martingale. In particular, and we have

Corollary 4.5.

The compensator of the -marked point process satisfies a.s.

Proof.

Using Theorem 4.3 with for it follows that the process defined as

is a -martingale. Then, for all bounded non-negative -predictable process the stochastic integral

is also a -martingale. By the Monotone Convergence Theorem, we have

Hence, the counting process is an inhomogeneous Poisson process with (Markov modulated) stochastic intensity The desired result follows from Corollary T4 (Integration Theorem) in Brémaud [1, Chapter VIII].

∎

5 Examples

5.1 Logarithmic utility

We illustrate the main result first by considering logarithmic utility functions.

Lemma 5.1.

Let Then, for all and we have a.s. for -a.e.

Proof.

In this case, we have and for Then, for

(5.1)

Hence, for all and the desired result follows.

∎

Theorem 5.2.

Let be fixed. Suppose Assumption A.1 holds true and that for each there exists satisfying for all and

(5.2)

Suppose further there exists such that

Let

Then

(a)

The portfolio-consumption pair is optimal for

(b)

The optimal wealth process satisfies

(c)

The optimal value function satisfies

Proof.

Define By (5.2) and Remark 3.3, the process belongs to By Lemma 5.1, and satisfy the assumptions of Theorem 3.7. Then the pair is optimal.

Using again (5.2), we see that the differential of satisfies

Hence, the process is a modification of In view of (5.1), we conclude and (a) follows. Assertion (b) follows from (2.5) and (c) follows from Theorem 3.7, part (c).

∎

Finally, we consider the case of two regimes for the underlying Markov chain.

Corollary 5.3.

Let now Assume that for each there exists satisfying for all as well as condition (5.2). Assume further

Then the optimal value functions satisfy

and

where

Proof.

Observe that

is a jump-telegraph process with alternating tendencies The desired result follows noting that

and using Theorem 4.1 and Theorem 5.2, part (c).

∎

Example 5.4.

To illustrate the above result, let us assume , , and . For regime we fix a parameter and assume is supported on the interval with distribution

The expected value is given by . Notice that the random variable is exponentially distributed with density function

For regime we fix another parameter and assume is supported on the interval with distribution

The expected value is given by In this case is exponentially distributed with density function

For each regime we consider the following portfolio constraints: for we restrict to the interval that is, borrowing (or short-selling of the money account) is not allowed, and for we restrict to the interval that is, short-selling of the risky asset is not allowed.

In view of these constraints, we define

(5.3)

and

(5.4)

Both maps and are strictly decreasing on their respective domains

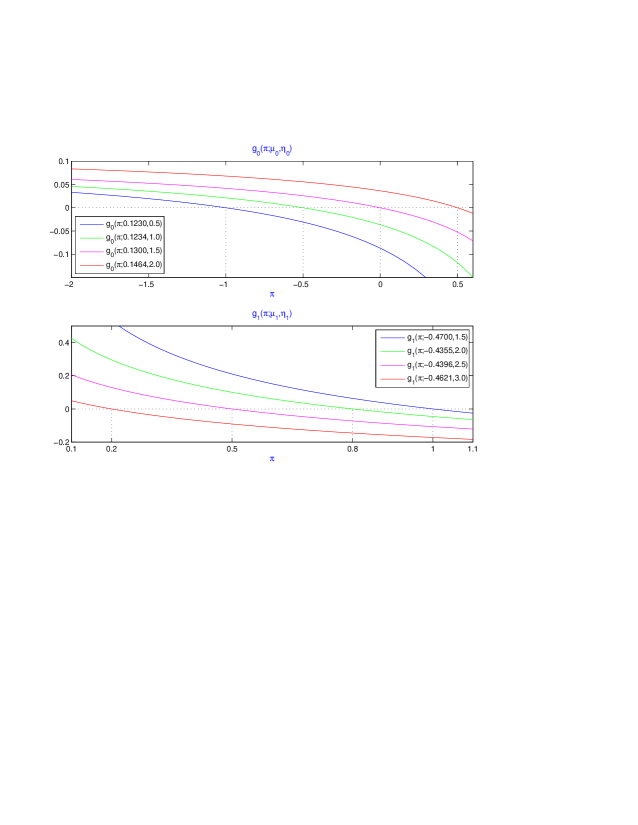

Figure 2: Plots of for different values of and .

Moreover,

Hence, if there exists a pair satisfying y , we can guarantee existence of solutions to equations and

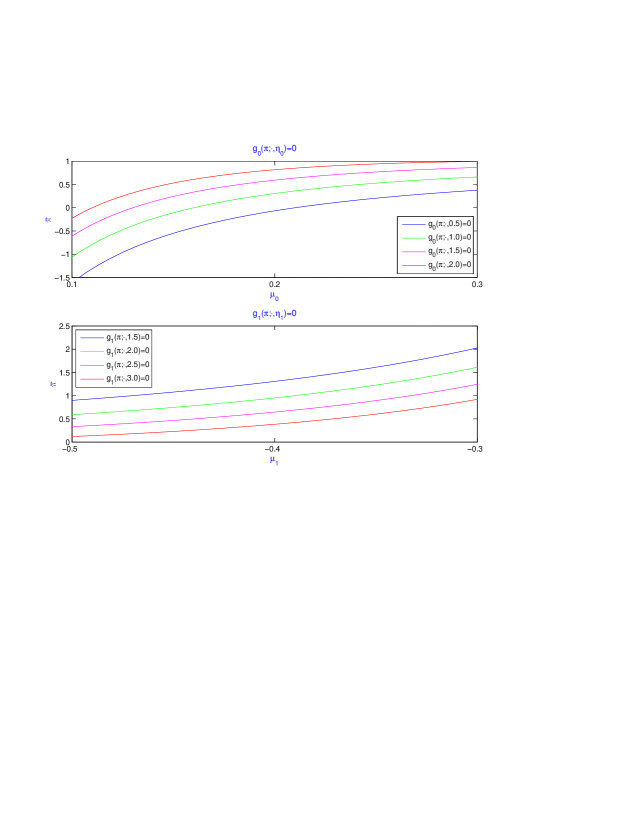

We solved these equations numerically with and Figure 2 (above) shows plots of for four different values of and which have been chosen so that the optimal portfolio proportions are given by and for each regime respectively. Figure 3 (below) plots the optimal portfolio proportion as a function of for different values of

Figure 3: Plots of optimal as function of , for different values of .

5.2 Fractional power utility

Finally, we consider CRRA fractional power utility functions with fixed.

Lemma 5.5.

Let be such that, for all

(5.5)

Then, for all we have

Proof.

Notice first that under condition (5.5) the process is a -martingale. Indeed, using integration formula for Marked point processes, we have

Then

It follows that

and

(5.6)

Hence

and

Therefore, the differential of satisfies

and the desired result follows.

∎

Theorem 5.6.

Let be fixed. Suppose Assumption A.1 holds and that for each there exists satisfying for all

(5.7)

and

(5.8)

Let and

for Then the portfolio-consumption pair is optimal for

Proof.

Define By (5.7) and Remark 3.3, the process belongs to By Lemma 5.5, and satisfy the assumptions of Theorem 3.7. Then the pair is optimal. Using (5.6) and (5.8), we conclude that and the desired result follows.

∎

Remark 5.7.

Notice that both conditions (5.7) and (5.8) turn into a very specific constraint on the mean rate of return Indeed, if there exists satisfying (5.8), then must satify condition (5.7) for this value of

On the other hand, if condition (5.7) holds, it can be plugged into (5.8) to obtain

To conclude, we have the following result for the two-regime case, which follows easily from (2.4), Theorem 4.2 and Theorem 5.5.

Corollary 5.8.

Let Assume that consumption is not allowed i.e. for all and for each there exists satisfying for all as well as conditions (5.7) and (5.8).

Then the optimal value functions satisfy

and

where

and .

References

[1]

Pierre Brémaud, Point processes and queues, Springer Series in

Statistics, Springer-Verlag, New York-Berlin, 1981.

[2]

Nicole Bäuerle and Ulrich Rieder, Portfolio optimization with jumps and

unobservable intensity process, Mathematical Finance 17 (2007),

no. 2, 205–224.

[3]

Giorgia Callegaro and Tiziano Vargiolu, Optimal portfolio for hara

utility functions in a pure jump multidimensional incomplete market, Int. J.

Risk Assessment and Management 11 (2009), no. 1/2, 180–200.

[4]

Jakša Cvitanić and Ioannis Karatzas, Convex duality in

constrained portfolio optimization, Ann. Appl. Probab. 2 (1992),

no. 4, 767–818.

[5]

Robert J. Elliott and Tak Kuen Siu, Option pricing and filtering with

hidden Markov-modulated pure-jump processes, Appl. Math. Finance

20 (2013), no. 1, 1–25.

[6]

Thomas Goll and Jan Kallsen, Optimal portfolios for logarithmic utility,

Stochastic Process. Appl. 89 (2000), no. 1, 31–48.

[7]

Hua He and Neil D. Pearson, Consumption and portfolio policies with

incomplete markets and short-sale constraints: the infinite-dimensional

case, J. Econom. Theory 54 (1991), no. 2, 259–304.

[8]

Jean Jacod and Albert Shiryaev, Limit theorems for stochastic processes,

Grundlehren der mathematischen Wissenschaften (Book 288), Springer, 2002.

[9]

Monique Jeanblanc, Marc Yor, and Marc Chesney, Mathematical methods for

financial markets, Springer Finance, Springer, London, UK, 2009.

[10]

Jan Kallsen, Optimal portfolios for exponential Lévy processes,

Math. Methods Oper. Res. 51 (2000), no. 3, 357–374.

[11]

Ioannis Karatzas, John P. Lehoczky, Steven E. Shreve, and Gan-Lin Xu,

Martingale and duality methods for utility maximization in an

incomplete market, SIAM J. Control Optim. 29 (1991), no. 3,

702–730.

[12]

Mikhail Konikov and DilipB. Madan, Option pricing using variance gamma

markov chains, Review of Derivatives Research 5 (2002), no. 1,

81–115.

[13]

D. Kramkov and W. Schachermayer, The asymptotic elasticity of utility

functions and optimal investment in incomplete markets, Ann. Appl. Probab.

9 (1999), no. 3, 904–950.

[14]

Oscar López and Nikita Ratanov, Option pricing driven by a telegraph

process with random jumps, J. Appl. Probab. 49 (2012), no. 3,

838–849.

[15]

Daniel Michelbrink and Huiling Le, A martingale approach to optimal

portfolios with jump-diffusions, SIAM J. Control Optim. 50 (2012),

no. 1, 583–599.

[16]

Nikita Ratanov and Alexander Melnikov, On financial markets based on

telegraph processes, Stochastics 80 (2008), no. 2-3, 247–268.