Multilevel path simulation for weak approximation schemes

In this paper we discuss the possibility of using multilevel Monte Carlo (MLMC) methods for weak approximation schemes. It turns out that by means of a simple coupling between consecutive time discretisation levels, one can achieve the same complexity gain as under the presence of a strong convergence. We exemplify this general idea in the case of weak Euler scheme for Lévy driven stochastic differential equations, and show that, given a weak convergence of order the complexity of the corresponding “weak” MLMC estimate is of order The numerical performance of the new “weak” MLMC method is illustrated by several numerical examples.

Multilevel path simulation for weak approximation schemes

Denis Belomestny222This research was partially supported by the Deutsche

Forschungsgemeinschaft through the SPP 1324 “Mathematical methods for extracting quantifiable information from complex systems” and by

Laboratory for Structural Methods of Data Analysis in Predictive Modeling, MIPT, RF government grant, ag. 11.G34.31.0073. and Tigran Nagapetyan

Duisburg-Essen University, National Research University Higher School of Economics,

Weierstrass Institute for Applied Analysis and Stochastics

1 Introduction

The multilevel path simulation method introduced in Giles [7] has gained huge popularity as a complexity reduction tool in recent times. The main advantage of the MLMC methodology is that it can be simply applied to various situations and requires almost no prior knowledge on the path generating process. Any multilevel Monte Carlo (MLMC) algorithm uses a number of levels of resolution, with being the coarsest, and being the finest. In the context of a SDE simulation on the interval , level corresponds to one timestep whereas the level has uniform timesteps

Assume that a filtered probability space is given. Consider now a -dimensional process solving the following Lévy driven SDE

| (1.1) |

where is a -valued random variable, is a -dimensional Lévy process and the mapping is Lipschitz continuous and has at most linear growth on so that the solution of (1.1) is well defined. Our aim is to estimate the expectation where is a Lipschitz continuous function from to Let be an approximation for by means of a numerical discretisation with time step (for various discretisation methods for (1.1) see, e. g. Platen and Bruti-Liberati [16] or the recent review of Jourdain and Kohatsu-Higa [11]). The main idea of the multilevel approach pioneered in Giles [7] consists in writing the expectation of the finest approximation as a telescopic sum

and then applying Monte Carlo to estimate each expectation in the above telescopic sum. One important prerequisite for MLMC to work is that and are coupled in some way and this can be achieved by using the same discretised trajectories of the underlying Lévy processes to construct the consecutive approximations and The degree of coupling is usually measured in terms of the variance . It is shown in Giles [7] (see also Giles and Xia [8]), that under the assumptions

| (1.2) |

with some and the computational complexity of the resulting multilevel estimate needed to achieve the accuracy (in terms of RMSE) is proportional to

The standard way of checking the assumptions (1.2) is to prove that the underlying approximation scheme has weak convergence of order and strong convergence of order Indeed, in the latter case we have for any Lipschitz continuous function

with some constant depending on However, in recent years the so-called weak approximation schemes, i.e., schemes that, in general, fulfil only the first assumption in (1.2) became quite popular. The weak Euler scheme is a first-order scheme with , and has been studied by many researchers. Talay and Tubaro [19] show the first-order convergence of the weak Euler scheme. The fact that the convergence rate of the Euler scheme also holds for certain irregular functions under a Hörmander type condition has been proved by Bally and Talay [2] using Malliavin calculus. The Itô-Taylor (weak-Taylor) high-order scheme is a natural extension of the weak Euler scheme. In the continuous diffusion case, some new discretization schemes (also called Kusuoka type schemes) which are of order without the Romberg extrapolation have been introduced by Kusuoka [12], Lyons and Victoir [13], Ninomiya and Victoir [15], and Ninomiya and Ninomiya [14]. A general class of weak approximation methods, comprising many well known discretisation schemes, was constructed in Kohatsu-Higa and Tanaka [20]. The main advantage of the weak approximation schemes is that simple discrete random variables can be used instead of the Lévy increments. Unfortunately, due to the absence of the strong convergence, the MLMC methodology can not be directly used with the weak approximation schemes. In this paper we make an attempt to overcome this difficulty and develop a kind of “weak” MLMC approach which can be applied to various weak approximation schemes.

The plan of the paper is as follows. First, we recall the Euler scheme for (1.1) and discuss its convergence properties. Next we show how to construct the corresponding MLMC algorithm, which is able to reduce the complexity of the standard MC to order under only requirement that the Euler scheme converges weakly. Finally, we analyse the numerical performance of the presented weak MLMC algorithms.

2 Euler scheme for Lévy driven SDE

Fix some and set Denote For a fixed random vector the Euler scheme for (1.1) reads as follows

| (2.1) | |||||

The convergence of the scheme (2.1) was extensively studied in the literature. The first convergence result is due to Talay and Tubaro [19], who proved that in the case of a diffusion processes with being a Brownian motion plus drift, the scheme weakly converges with order In the case of the general Lévy processes, the convergence of (2.1) was studied in Protter and Talay [17], where it is shown that, under some assumption on the function and the driving Lévy process , the weak convergence rate can be recovered. In fact, the main drawback of the scheme (2.1) is the necessity to sample from the distribution of exactly. Although such exact sampling can be possible for particular Lévy processes (see [17] for some examples), in general this turns out to be a hard numerical problem. This is why Jacod et al [10] proposed to replace the increments of the original Lévy process by simple random vectors which are easy to simulate. It is shown in [10] that if the distributions of and are sufficiently close, then the weak convergence rate continues to hold. These results on weak convergence should be compared with ones on pathwise or strong convergence. In fact, the strong convergence rates usually depend on the characteristics of the Lévy process For example, Rubenthaler [18] studied the strong error when neglecting small jumps. He obtains the estimate of the form

with being the Lévy measure of So the rates become quite poor if diverges at zero like with close to Recently, Fournier [6] has proposed a coupling method which allows to get better rates of pathwise convergence in a one-dimensional case. He constructed an approximation satisfying

with The approximation is constructed by replacing the jumps of smaller than by an independent Brownian motion. In order to prove a bound for the Wasserstein distance between and a suitable coupling was used. Note that since is unknown, such coupling is not implementable. A similar coupling idea in the multidimensional setting was used in Dereich [3] to design a multilevel path simulation approach for (1.1).

3 Multilevel path simulation for weak Euler scheme

In order to successfully apply the multilevel approach, one needs to ensure that (1.2) hold. If the scheme (2.1) has strong convergence of order i.e.,

then the conditions (1.2) hold with However, if some approximations are used instead of the genuine increments strong convergence is not any longer guaranteed. Here we propose a general approach how to couple two consecutive approximations of in order to guarantee that the second condition in (1.2) still holds with In fact, this would lead to a complexity estimate does not matter how small is

3.1 Coupling idea

Let us fix two natural numbers (“coarse” discretisation level) and (“fine” discretisation level) with and set In order to couple the Euler approximations and we are going to couple the random matrices and We define the approximation for the increments on the coarse level in such a way that the differences

| (3.1) |

are small. In particular, we can take The idea behind this coupling is very simple: in the case of the genuine Lévy increments we would get

Suppose that are i.i.d. random vectors with moments and The following proposition holds.

Proposition 1.

Suppose that the coefficient function in (1.1) is uniformly Lipschitz and has at most linear growth, i.e.,

| (3.2) |

for any and some positive constants and Denote and suppose that are zero mean i. i. d. random vectors. Moreover, assume that then the following estimate holds

| (3.3) |

for some constants depending on and

Corollary 2.

If and for then

Discussion

First note that the conditions for (3.3) to hold are formulated not in terms of the original increments but rather in terms of their approximations For the case of the exact increments, we obviously have and provided

where is a Lévy measure of Furthermore, observe that under the assumptions of Corollary 2, the second condition in (1.2) holds with independently of the strong convergence order for the corresponding Euler scheme. Finally, let us stress that the assumptions on the coefficient function are quite weak and standard in the framework of Lévy driven SDEs. In fact, they are needed to guarantee existence and uniqueness of the solution of (1.1) (see, e.g., Ikeda and Watanabe [21]).

3.2 MLMC algorithm

Fix some and set Denote

where the columns of the matrix are i.i.d. random vectors in Now we define recursively the independent random matrices with via where each vector is coupled with and in such a way that all differences

are small. For example, one can simply put

| (3.4) |

Next, for any and any random matrix consider the approximations

with and some r. v. Finally, fix a vector of natural numbers and define a weak MLMC estimate for as follows

where and are i.i.d. copies of .

Proposition 3.

Suppose that the the function is Lipschitz continuous and that the distribution of is chosen in such a way that

| (3.5) |

for some and Then under the assumptions of Proposition 1 and Corollary 2, and under a proper choice of and the complexity of the estimate needed to achieve the accuracy (as measured by RMSE) is of order

Remark 4.

The distribution of the matrix under coupling (3.4), changes with in a rather simple way and can be found explicitly in many interesting cases (see examples below). In general, one can compute the characteristic function of each vector in a closed form, provided the characteristic function of is known explicitly. Using the Fourier inversion formula, one can then compute the density of each Let us also note that there is a lot of freedom in the choice of the finest approximation satisfying (3.5).

4 Examples

4.1 Diffusion processes

Consider now a -dimensional diffusion process solving the SDE

| (4.1) |

where is a -dimensional Brownian motion, and are Lipschitz continuous functions. Although the increments of Wiener process can be simulated exactly, we can consider the following weak Euler scheme

where and i.i.d. random variables satisfy

| (4.2) |

Under some additional assumptions on the coefficient functions and and the output function spelled out in Talay and Tubaro [19] and Bally and Talay [2], it holds

for some The simplest way of constructing a r.v. with the property (4.2) is to take

| (4.3) |

Observe that distribution of the components of the vector under coupling (3.4) in the ML algorithm, is closely related to the Binomial distribution, namely

| (4.4) |

Hence the generation of variates is straightforward when a generator of binomially distributed random variates is available. For a fixed the weak MLMC algorithm implies generation of for starting from up to . Since all probabilities of distributions for are rational numbers, table look-up or alias methods (see [4]) can be used to achieve fast single random number generation. Since the distributions of do not change between different runs of the MLMC method, all the preprocessing required can be done only once and the resulting tables can be stored. In problem-specific hardware (FPGA or ASIC) these tables can be kept in permanent shared constant storage, which is often cheap, fast and abundant. With table lookup methods this would provide worst-case single random variate generation time at the price of storing items of preprocessing data, and with alias methods it is possible to attain worst-case single random variate generation time at the price of storing items of preprocessing data. Note that the whole procedure of binomial increments generation can be implemented with the use of integer numbers only. Therefore, a good MLMC implementation for binomial increments can possibly outperform its counterpart for Normal increments.

4.2 Jump diffusion processes

Consider now a -dimensional jump diffusion process solving the SDE

| (4.5) |

where is a standard -dimensional -adapted Brownian motion and is a Poisson counting measure on with a finite intensity measure We assume and are independent, and that the mappings and are Lipschitz continuous and have at most linear growth on so that the solution of (4.5) is well defined.

Let and stands for the empty set. For any nonempty denote number of zero components of and is the number of negative components of For any mapping define the operators associated with (4.5)

where

The composite operator is defined recursively as

if and via

otherwise. Denote then the Euler scheme for (4.5) reads as follows

where are independent random variables with the law The (essentially) weak Euler scheme can be constructed by replacing the random variables and by simple approximations and respectively which satisfy

for some In particular, one can take

| (4.6) |

where Moreover, the random variables can be replaced by i.i.d. random variables satisfying

| (4.7) |

and

| (4.8) |

for all with and where is distributed according to

Remark 5.

If then coefficients functions of order with take the form

If moreover , we get

Similar results hold for multidimensional case as well. Hence for a large class of stochastic processes, including affine and polynomial processes, the conditions (4.7) and (4.8) can be viewed as generalised moment conditions.

In the corresponding ML algorithm we can use the approximation for of the form:

Then the random variables for have a binomial distribution which can be easily simulated as described in Section 4.1.

4.3 General Lévy processes

Consider a one-dimensional square integrable Lévy process of the form

for some where is a compensated Poisson random measure on with intensity measure where In order to apply the Euler approximation scheme to (1.1), we need to approximate the increments Asmussen and Rosinski [1] (see also [10]) suggested to replace the small jumps in by an appropriate Gaussian random variable. So we define

where is the same Lévy process as without its (compensated) jumps smaller than and is Gaussian random variable with the same mean and variance as the neglected jumps. The resulting Euler scheme takes the form

| (4.9) | |||||

Let us discuss the first condition in (1.2) (weak convergence). As was shown in [5] (see also[10]),

| (4.10) |

provided and

| (4.11) |

Note that each r. v. can be represented as

where and are i.i.d. random variables with the distribution

Hence the cost of generating one trajectory by means of (4.9) is of order Let us now fix two natural numbers two positive real numbers and describe the coupling between and Set

| (4.12) |

then

As a result, and

Hence the assumptions of Corollary 2 are fulfilled, provided

for some Under (4.11), this is equivalent to the relation Using the estimate (4.10), we derive the complexity of the resulting coupled multilevel scheme.

Proposition 6.

Discussion

Observe that the complexity of the standard MC algorithm for estimating is bounded above via

So the coupled MLMC approach is superior to the standard MC algorithm as long as A similar behaviour can be observed in Dereich [3] (at least for ). We can further replace the restricted Lévy jump sizes by some simple random variables using the approach presented in Section 4.2. Note that in the latter case the above complexity bounds continue to hold.

5 Numerical experiments

In this section we present numerical examples corresponding to process classes discussed in Section 4.

The MLMC algorithm is implemented according to the [7], with some changes, due to the specific structure of the simulated process. Recall, that the MLMC estimator has the form:

But the general scheme is the same for all considered problems and can be summarized in the following algorithm:

-

Input:

Requested accuracy and set the final level .

-

1.

Set

-

2.

Compute samples on levels

-

3.

Estimate and update for each level :

If the update is increased less than 1% on the levels, then go to step 5.

-

4.

Compute the additional number of samples and Go to step 3.

-

5.

If or :

,

Else: Return . -

6.

If , then

Display error: The final level is insufficient for the convergence.

Return . -

7.

Goto step 3.

In all of our numerical experiments we have chosen to be sufficiently large, so that was always satisfied.

5.1 Diffusion process

5.1.1 European max-call option

Consider a three dimensional process with independent components where each process solves one-dimensional SDE of the form (4.1) with and for some . We are interested in computing the expectation of

We chose the following parameters:

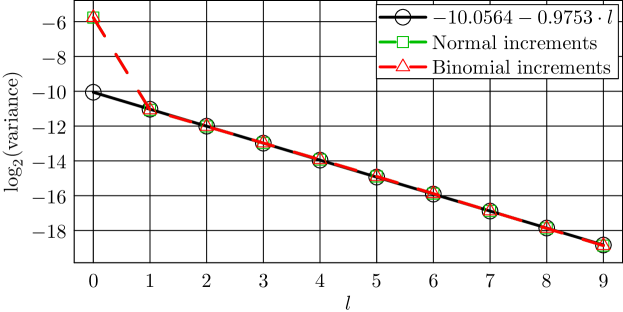

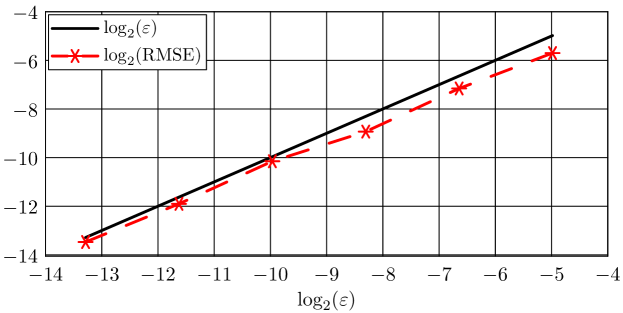

and . In fact in this case the exact solution is available and for above parameter values, we have . The variance decay is presented on Figure 5.1. In particular, the line with fits the estimated log-variances best and this is in agreement with Corollary 2. The corresponding RMSE is presented in Figure 5.2.

5.1.2 Geometric Asian option

Consider a one dimensional process where each coordinate process solves one-dimensional SDE of the form (4.1) with and for some . We are interested in computing the expectation of the functional

The parameter values are

In this case the exact value of the expectation is given by

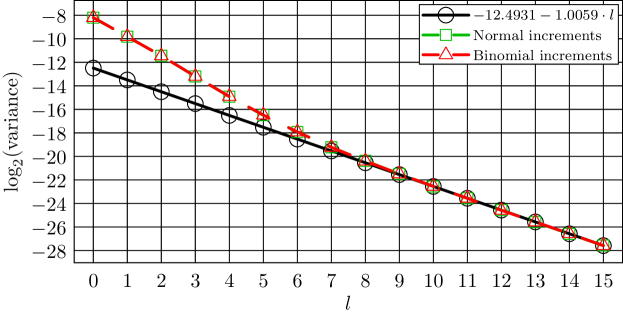

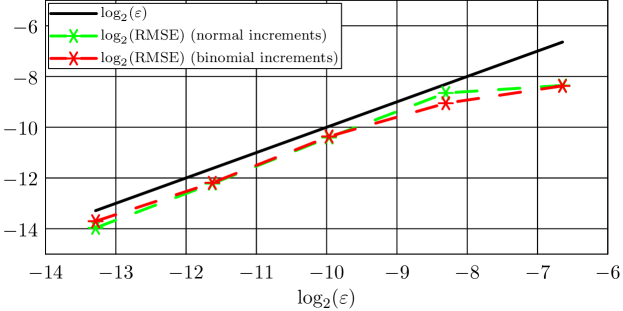

The variance decay is presented on Figure 5.3. Due the fact, that at first levels the variance decays faster than predicted, we have fitted the variance decay only on the last 6 levels with the line and got . The corresponding RMSE is presented in Figure 5.4.

5.2 Jump diffusions

Consider a jump SDE

where

and is a Poisson process with rate . We are interested in computing the expectation of

The parameters’ values are

It follows from [9] (Section 3.5) that, for above parameter values . We have performed two types of simulations with the fixed top level :

-

•

was sampled from the lognormal distribution, while the increments of the Brownian motion were modelled as normal random variables

- •

In both of those cases, the number of jumps at the level and step is generated via

| (5.1) |

One can see, that (5.1) can be implemented in the same spirit as (4.4). On the finest level we allow only for two jumps or Let us denote by the th moment of the lognormal distribution with parameters and . The random variable takes values with probabilities . The values and probabilities are obtained by solving the optimization problem:

| Minimize | |||

| Subject to | |||

The solution is

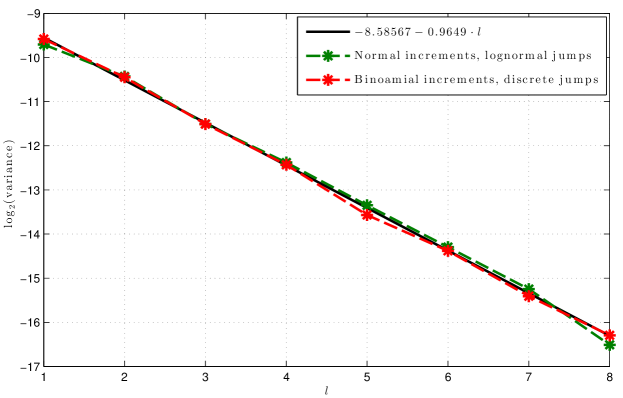

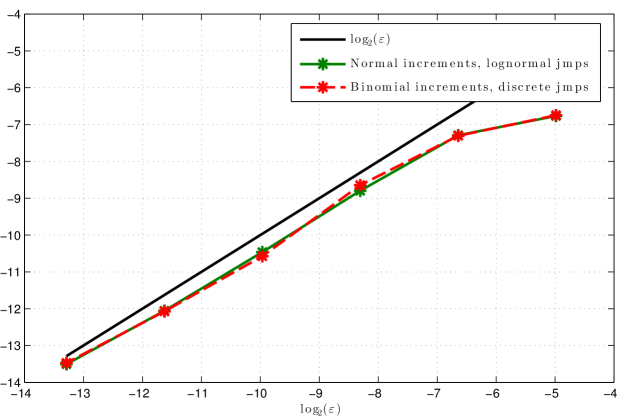

The variance decay is shown in Figure 5.5 for both types of simulations. We estimated RMSE of the ML estimate based on the weak Euler scheme based on independent runs, see Figure 5.6.

Acknowledgments

Authors are thankful to Prof. Mike Giles, Dr. Lukasz Szpruch and Dr. Sonja Cox for their helpful comments and remarks. Authors are very grateful to Vladimir Shiryaev for his assistance with the numerical experiments.

6 Proofs

Lemma 7.

Suppose that the coefficient function in (1.1) is uniformly Lipschitz and has at most linear growth, i.e.,

| (6.1) |

for any and some positive constants and Moreover, assume that then the following estimates hold

for

Proof.

Since

we have, due to independence of the increments

Using the discrete version of the Gronwall inequality (see Appendix), we get

The second inequality of the lemma is proved in the same way. ∎

6.1 Proof of Proposition 1

Due to the Lemma 7 we have

| (6.2) |

for and constants not depending on We have

Denote then we have the representation

with

and

The Lipschitz continuity of the function implies

and

As a result

for some constants and Analogously

for some Define

and note that is martingale with respect to the filtration

Hence the Doob inequality implies for any

So we have for

Finally a discrete version of Gronwall lemma (see Appendix) implies

6.2 Proof of Proposition 6

We aim to minimize

subject to

We denote

From Lagrange principle we get

So the cost has the representation

According to the restrictions on the bias we have

We now consider two cases.

-

1.

We set constant on all the levels. Then the cost is bounded from above by

-

2.

In the second case we will set

Note, that , so the bias condition is fulfilled. Then the overall cost

Combining all the cases together we get the statement.

7 Appendix

Lemma 8.

Let and be two nonnegative sequences and let be a nonnegative constant. If

then

Proof.

We have

∎

References

- [1] Søren Asmussen and Jan Rosiński. Approximations of small jumps of Lévy processes with a view towards simulation. Journal of Applied Probability, pages 482–493, 2001.

- [2] Vlad Bally and Denis Talay. The Euler scheme for stochastic differential equations: error analysis with Malliavin calculus. Mathematics and computers in simulation, 38(1):35–41, 1995.

- [3] Steffen Dereich et al. Multilevel Monte Carlo algorithms for Lévy-driven sdes with gaussian correction. The Annals of Applied Probability, 21(1):283–311, 2011.

- [4] Luc Devroye. Non-uniform random variate generation. Springer-Verlag, 1986.

- [5] El Hadj Aly Dia et al. Error bounds for small jumps of Lévy processes. Advances in Applied Probability, 45(1):86–105, 2013.

- [6] Nicolas Fournier. Simulation and approximation of Lévy-driven stochastic differential equations. ESAIM: Probability and Statistics, 15:233–248, 2011.

- [7] Michael B Giles. Multilevel Monte Carlo path simulation. Operations Research, 56(3):607–617, 2008.

- [8] Mike Giles and Yuan Xia. Multilevel Monte Carlo for exponential L’e vy models. arXiv preprint arXiv:1403.5309, 2014.

- [9] Paul Glasserman. Monte Carlo methods in financial engineering, volume 53. Springer, 2004.

- [10] Jean Jacod, Thomas G Kurtz, Sylvie Méléard, and Philip Protter. The approximate euler method for Lévy driven stochastic differential equations. Annales de l’Institut Henri Poincare (B) Probability and Statistics, 41(3):523–558, 2005.

- [11] Benjamin Jourdain and Arturo Kohatsu-Higa. A review of recent results on approximation of solutions of stochastic differential equations. In Stochastic Analysis with Financial Applications, pages 121–144. Springer, 2011.

- [12] Shigeo Kusuoka. Approximation of expectation of diffusion processes based on Lie algebra and Malliavin calculus. In Advances in mathematical economics, pages 69–83. Springer, 2004.

- [13] Terry Lyons and Nicolas Victoir. Cubature on Wiener space. Proceedings of the Royal Society of London. Series A: Mathematical, Physical and Engineering Sciences, 460(2041):169–198, 2004.

- [14] Mariko Ninomiya and Syoiti Ninomiya. A new higher-order weak approximation scheme for stochastic differential equations and the Runge–Kutta method. Finance and Stochastics, 13(3):415–443, 2009.

- [15] Syoiti Ninomiya and Nicolas Victoir. Weak approximation of stochastic differential equations and application to derivative pricing. Applied Mathematical Finance, 15(2):107–121, 2008.

- [16] Eckhard Platen and Nicola Bruti-Liberati. Numerical solution of stochastic differential equations with jumps in finance, volume 64. Springer, 2010.

- [17] Philip Protter, Denis Talay, et al. The euler scheme for Lévy driven stochastic differential equations. The Annals of Probability, 25(1):393–423, 1997.

- [18] Sylvain Rubenthaler. Numerical simulation of the solution of a stochastic differential equation driven by a Lévy process. Stochastic processes and their applications, 103(2):311–349, 2003.

- [19] Denis Talay and Luciano Tubaro. Expansion of the global error for numerical schemes solving stochastic differential equations. Stochastic analysis and applications, 8(4):483–509, 1990.

- [20] Hideyuki Tanaka, Arturo Kohatsu-Higa, et al. An operator approach for Markov chain weak approximations with an application to infinite activity Lévy driven sdes. The Annals of Applied Probability, 19(3):1026–1062, 2009.

- [21] Shinzo Watanabe and Nobuyuki Ikeda. Stochastic differential equations and diffusion processes. Elsevier, 1981.