Formal Hypothesis Tests for Additive Structure in Random Forests

Abstract

While statistical learning methods have proved powerful tools for predictive modeling, the black-box nature of the models they produce can severely limit their interpretability and the ability to conduct formal inference. However, the natural structure of ensemble learners like bagged trees and random forests has been shown to admit desirable asymptotic properties when base learners are built with proper subsamples. In this work, we demonstrate that by defining an appropriate grid structure on the covariate space, we may carry out formal hypothesis tests for both variable importance and underlying additive model structure. To our knowledge, these tests represent the first statistical tools for investigating the underlying regression structure in a context such as random forests. We develop notions of total and partial additivity and further demonstrate that testing can be carried out at no additional computational cost by estimating the variance within the process of constructing the ensemble. Furthermore, we propose a novel extension of these testing procedures utilizing random projections in order to allow for computationally efficient testing procedures that retain high power even when the grid size is much larger than that of the training set.

1 Introduction

As scientific data grows larger and becomes easier to collect, traditional statistical models often prove insufficient for fully capturing the underlying process. Learning algorithms, on the other hand, adapt well to a variety of data types and produce accurate predictions, but their inherent complexity and black-box nature makes addressing even the simplest scientific questions significantly more difficult. This work provides a formal statistical test for determining variable interactions whenever ensemble learning methods like random forests are used as the primary modeling tool.

Additive models were suggested by Friedman and Stuetzle, (1981) and further developed and made popular by Stone, (1985) and Hastie and Tibshirani, (1990). An underlying regression function is said to be additive if

for some functions . If the regression function cannot be written as, or at least well-approximated by, a sum of univariate functions, then an interaction exists between some subset of the covariates. Many methods have been developed to estimate the additive functions including a method based on marginal integration by Linton, (1995), a wavelet method suggested by Amato and Antoniadis, (2001), a tree-based method by Lou et al., (2013), and the most popular class based on backfitting algorithms as found in Buja et al., (1989), Opsomer and Ruppert, (1998, 1999), and Mammen et al., (1999).

The popularity of additive models and their ease of interpretation has inspired hypothesis tests to assess whether observed data should be modeled in an additive fashion. Versions of these lack-of-fit tests have been proposed by Barry, (1993), Eubank et al., (1995), Dette and Derbort, (2001), Derbort et al., (2002), and De Canditiis and Sapatinas, (2004). Fan and Jiang, (2005) further extend these procedures to also evaluate whether the additive components belong to a particular parametric class. Even when additive models are not used as the primary analytical tool, scientists often utilize these and related interaction detection methods to determine which variables contribute additively to the response; when no interactions are detected, the levels of one feature may be changed without affecting the contribution to the response made by the others.

Their utility notwithstanding, additive models can often fail to fully capture the signal hidden within modern complex data, even when relatively little signal results from variable interactions. On the other hand, learning algorithms like bagged trees and random forests introduced by Breiman, (1996, 2001), are robust to a variety of regression functions and are considered something of a gold standard in terms of predictive accuracy. Though this accuracy continues to drive their popularity, little is understood about the underlying mathematical and statistical properties of these ensemble methods. Thus, while practitioners routinely rely on such methods to make predictions, when standard results such as confidence intervals or p-values from hypothesis tests for variable importance or interactions need reported, those practitioners are forced to move to an entirely different modeling technique and rely on more well-established procedures. At best, the ensembles might be used to better inform which hypotheses to test and/or which variables should be included in a simpler model.

Recently however, important progress has been made in understanding the asymptotic properties of these ensemble methods by considering a subsampling approach in lieu of the traditional bootstrapping procedure. Mentch and Hooker, (2016) show that when proper subsamples are used to construct individual trees, the ensemble predictions can be seen as extensions of classical U-statistics and as such, are asymptotically normal. Wager et al., (2014) apply recent results on the infinitesimal jackknife (Efron,, 2014) to produce estimates of standard errors for subsampled random forest predictions and Wager and Athey, (2015) later demonstrate the consistency of such an approach. Most recently, Scornet et al., (2015) provided the first consistency results for Breiman’s original random forest procedure when subsampling is employed and the underlying regression function has an additive form.

This paper continues in this recent trend by developing formal hypothesis tests for additivity in ensemble learners like bagged trees and random forests. These tests allow practitioners to formally investigate the manner in which features contribute to the response when simpler, more direct tools are insufficient and to our knowledge, represent the first formal procedures for investigating the structure of the underlying regression function within the context of ensemble learning. That is, statistically valid results such as p-values may be gathered directly from the ensemble instead of relying on ad hoc measures or appealing to a simplified model. In Section 2 we propose a formal test for feature significance by imposing a grid structure on the covariate space and in Section 3 we demonstrate that this additional structure further allows for tests of additivity. In Section 4 we incorporate random projections to extend our procedure to the situation where a large test grid is needed, so as to accommodate potential high dimensional settings. Finally, in Sections 5 and 6, we provide simulations to investigate the power of our hypothesis tests and apply our testing procedures to an ecological dataset.

2 Hypothesis tests for feature significance

Recent theory has demonstrated that a subsampling approach to constructing supervised ensembles like random forests may allow these learners to be reigned in within the realm of traditional statistical inference. Specifically, Mentch and Hooker, (2016) show that by controlling the subsample growth rate, individual predictions are asymptotically normal thereby paving the way for a formal method of evaluating variable (feature) significance. As a simple example, consider a setting with just two features and where the response observed according to . To test the significance of , we can generate a test set consisting of points and build two subsampled ensembles and . Both ensembles employ the same subsamples, but is constructed using both and whereas is built using only . Predictions at each point in are then made with each ensemble and Mentch and Hooker, (2016) show that the vector of differences in predictions has a multivariate normal limiting distribution with mean and variance . Given consistent estimators of these parameters, can be used as a test statistic to formally evaluate the hypotheses

| (1) | ||||

Though asymptotically valid, this procedure requires building separate ensembles for each feature of interest. We demonstrate here that imposing additional structure on the test set allows us to both avoid training an additional set of trees and also perform tests for additivity.

Define a grid consisting of total test points as in Figure 1 with levels and levels so that the point in the grid has true value and predicted value . In the case of categorical covariates, these grid levels are naturally occurring while in the case of continuous covariates, these levels can be specified as appropriate (e.g. based on quantiles of the observed data). Let and represent the vectorized versions of these true and predicted values so that and define

as the average response at the level across all grid levels . For each point in the grid, the difference in predictions can be written in vectorized form as for an difference matrix of rank . In this case, where is the identity matrix, is the matrix of 1’s, and denotes the standard tensor product. Let denote the covariance of and a consistent covariance estimate of the predictions. Then we can define so that forms a consistent estimate of the covariance of the projected predictions . Then and since we can equivalently write the hypotheses in (1) as

can be used as a test statistic.

Asymptotically, this test statistic has a distribution and thus can be compared to the quantile to achieve a test with type 1 error rate ; if the test statistic is larger than this critical value, we reject the null hypothesis and conclude that is significant.

This testing procedure readily extends to the more general case of features . Let and form a partion of so that and are disjoint and ; the set denotes the reduced set of features and represents the additional features that we want to test for significance. To test the hypotheses

we simply repeat the testing procedure in the above example, replacing the levels and with appropriately redefined grid levels the feature sets and , respectively. Note that in this case, each grid point now corresponds to the value of a vector of features.

It is also worth noting that Mentch and Hooker, (2016) suggest comparing predictions generated with the full training set to not only those produced with the reduced set , but also to those generated with and a permuted version of in order to rule out the possibility that the ensemble is simply making use of additional noise. The procedure we propose above avoids this potential confusion by utilizing the projection matrix .

3 Tests for additivity

We now demonstrate that this grid structure also allows for formal tests of additivity.

Tests for total additivity

Again assume that our training set consists of only two features and that the response is observed according to . Tests for total additivity assess whether the entire underlying regression function is equal to, or at least well-approximated by, a sum of functions with disjoint domains. When each function is univariate, this simply means that there are no interactions between any covariates but a more general case is also discussed below. In the simple 2-dimensional case, the hypotheses of interest are

| (2) | ||||

Again define a 2-dimensional grid of test points as in Figure 1 so that each point in the grid has true value , predicted value , and vectorized versions and . Define to be the mean of all predictions in the grid and define

as the mean prediction at the level across all levels , and the mean prediction at the level across all levels , respectively. If the features are additive, (i.e. under the null hypothesis) all points in the grid can be written as where is the true mean expected prediction across all points in the grid. Thus, we may equivalently write the hypotheses in (2) as

The natural test statistic is then which can be written as where difference matrix is given by

Thinking of the and grid levels as factor levels of and , we have degrees of freedom and has rank . As in Section 2, let denote the covariance of so that we can write and use as our test statistic. Note that this testing procedure for total additivity is identical to the procedure for testing significance but in the final two steps we calculate an alternative difference matrix and test statistic.

This procedure also naturally extends to the case of features . To test hypotheses of the form

| (3) | ||||

we require a -dimensional grid of test points so that given levels of each feature , our grid contains a total of test points. Further, define

to be the average prediction over all points in the grid at the level defined on the feature, . As in the 2-dimensional case, we can rewrite the hypotheses in (3) as

and write as . Again, we define to be the covariance of so that and we can use as our test statistic, where .

Importantly, the additive functions need not be univariate. Define a (disjoint) partition of the feature space so that . We can test hypotheses of the form

in exactly the same fashion by appropriately defining levels of an -dimensional grid of test points.

Tests for partial additivity

We now handle the case where we are interested in testing only whether a proper subset of features contribute additively to the response. Suppose that our training set consists of three features , and and we are interested in testing

| (4) | ||||

Rejecting this null hypothesis means that an interaction exists between and but implies nothing about potential interactions between and or between and . Hooker, (2004) uses the size of the deviation of from partial additivity as a means of identifying the bivariate and higher-order interactions required to reconstruct some percentage of the variation in the values of . This is also referred to as the Sobol index for the , interaction (Sobol,, 2001). Define a 3-dimensional grid of test points with , and levels of and , respectively and continuing with the dot notation, define

to be the average prediction over all levels of the feature in the grid at the and levels and , and the average prediction over all levels of the feature in the grid at the and levels and , respectively. If there is no interaction between and , then at all levels in the grid. Thus, we can rewrite the hypotheses in (4) as

and use the empirical analogues of these parameters to conduct the testing procedure. Once again, we can write as for the appropriate difference matrix . Defining as the covariance of , we can write and use as our test statistic, where . Note that since we must now account for two-way interactions, we have degrees of freedom and is of rank . As was the case in testing for total additivity, the testing procedure remains identical with the appropriate difference matrix and test statistic calculated in the final steps.

This same testing procedure can also be performed when our training set consists of features and we are interested in determining whether an interaction exists between and . Denote the set of all features except and as so that our hypotheses become

Now, instead of the third dimension of the grid containing levels of the single feature , these are now vector levels and the testing procedure remains identical. Likewise, and may be treated as vectors of features by redefining the grid levels as levels of the appropriate vector.

Remark: The testing procedures above as well as those defined in Section 2 were derived assuming equal weight is placed on each point in the test grid. In some cases, it may be advantageous to instead differentially weight grid points, for example based on the local density of observations. This alternative approach based on minimizing a weighted sum of squared errors is outlined in Appendix A. For a more thorough review of when such an alternative may be preferred, we refer the reader to Hooker, (2007).

4 Random Projections

The above procedures require estimating a covariance matrix of size proportional to the number of points in the test grid. However, estimating the variance parameters with too small an ensemble can result in a significant overestimate of the variance, thereby substantially reducing the power of our testing procedures; see Mentch and Hooker, (2016) for a more complete discussion. Thus, in situations where large grids and/or complex additive forms are of interest, it may become computationally infeasible to directly obtain an accurate covariance estimate. In light of this, we further extend our above procedures to make use of random projections.

Random projections have a long-established history as a dimension-reduction method. The Johnson-Lindenstrauss Lemma (Johnson and Lindenstrauss,, 1984) provides that orthogonal projections from high dimensional spaces into lower dimensional spaces approximately preserve the distances between the projected elements. Lopes et al., (2011) and Srivastava et al., (2015) leverage this result to produce a high-dimensional extension of Hotelling’s classic test to the case. Specifically, given two multivariate samples and , the data is projected via a random projection matrix into a reduced dimension where an analogous testing procedure can be well-defined. In the latter work, the authors denote this test RAPTT (Random Projection T-Test) and for each projection matrix , the projected test statistic and p-value are given by

and

where , is the (pooled) sample covariance matrix, and denotes the -distribution with numerator and denominator degrees of freedom and , respectively. RAPTT proceeds by sampling random projection matrices thereby obtaining a total of of the test statistics and p-values defined above. The final test statistic in the procedure with level is defined as the average across the p-values, and the null hypothesis of equal means is rejected whenever where is chosen such that .

In our context, we consider a training set of size , an ensemble consisting of trees, each of which is built with a subsample of size , and we are interested in predicting at total test points. Recall from Section 2 that the simplest form of test statistic that can be used to evaluate variable importance is given by where is the vector of ensemble predictions, and is the corresponding covariance matrix estimate. Given predictions at each of locations, we can think of our data as an matrix so that for a set of random projection matrices and reduced dimension , we can write each projected test statistic as

| (5) |

The grid structure can also be incorporated in a straightforward manner. Though we utilize a difference matrix to project into the space of additive models, so long as the elements of the are independently generated continuous random variables, the overall projection has rank with probability 1. The original test statistic is given by where and so the test statistic and p-value incorporating a random projection become

and

respectively, where and denotes the cdf of the . For replicates of this randomized testing procedure, we can define our final test statistic as in the same fashion as RAPTT, where we reject whenever and is chosen such that .

4.1 Defining the Testing Parameters

The procedures developed in the preceding sections require a number of user-specified parameters. First, as noted in Srivastava et al., (2015), the choice of reduced dimension is an important consideration that can influence the power of projection-based testing procedures. In our case, the covariance parameters are difficult to estimate accurately on large grids and thus, though the procedure is well-defined for , this practical restriction necessitates a relatively small projected dimension . In many cases, we see a significant drop in power when testing on grids consisting of more than approximately 30 points, so choosing should be reasonable and computationally feasible in most situations. Further, note that because is small, little dependence remains between the resulting p-values. Under the null hypothesis, each p-value is uniformly distributed on and the mean of independent standard uniform random variables follows a Bates distribution, so the final cutoff can be well approximated by the quantile of this distribution.

The ideal method of sampling the random projection matrices is of less concern; Srivastava et al., (2015) show that any semi-orthogonal matrix with elements generated from a continuous distribution with finite second moment satisfies the necessary conditions to perform the projection-based tests. For our situation, we recommend generating such matrices by sampling individual elements from a standard normal distribution, orthogonalizing via a process such as Gram-Schmidt, and selecting the appropriate submatrix. Such a procedure is straightforward and can be implemented in most software packages.

Algorithm 1 makes the random-projection-based testing procedure explicit, using the internal variance estimation procedure proposed in Mentch and Hooker, (2016). For a particular query point of interest , the asymptotic variance of the prediction is given by

where represents the variance between tree-based predictions at given a single common training point , denotes the between-tree variance, and . The algorithm makes use of the parameters and in order to structure the ensemble in such a fashion so as to readily post-compute consistent estimates of and . The parameter corresponds to the number of conditional expectation estimates computed in the definition of and is the number of Monte Carlo samples used to estimate each conditional expectation so that in this case, . Though the ensemble need not be constructed in such a fashion, the internal estimation procedure allows us to easily select a small projected dimension and also allows for the covariance estimates to be computed at no additional cost to the original ensemble.

Finally, the levels of the test grid are an important consideration. As with all supervised learning procedures, these test points should be concentrated near the observed data so as to minimize the effects of extrapolation. However, with tree-based procedures, choosing grid points that appear in the original sample can also be problematic. Because the trees in random forests are grown to near full-depth without pruning, predictions made arbitrarily close to points in the training sample can suffer from overfitting and as a result, create the artificial appearance of interactions. Lastly, because predictions are based on localized averaging, grid points should be selected away from the boundary of the feature space to avoid edge effects. In most situations, uniformly spaced grid points in the interior of the feature space should produce tests with high power that preserve the level of the test.

5 Simulations

We now provide simulations to investigate the power of our proposed testing procedures. Suppose first that we have two features and and that our responses are generated according to where we set to assess -level and to evaluate power with . We first test for total additivity on 1000 datasets when and 1000 datasets where , taking our empirical -level as the proportion of tests that incorrectly reject the null hypothesis (when ) and our estimate of power as the proportion of tests that correctly reject the null hypothesis (when ). For reference, we also built 1000 linear regression models using the traditional t-test to determine whether the interaction is significant and recorded the empirical -level and power of this testing procedure. This was repeated for data sets of size of 250, 500, and 1000 using subsample sizes of 30, 50, and 75 respectively and the results are shown in Table 1. The test grid was selected as a grid with levels 0.2, 0.4, 0.6, and 0.8. In each case, our test for total additivity using a subbagged ensemble performed nearly exactly as well as the traditional t-test.

| Method | -level | Power | |

|---|---|---|---|

| Linear Model | 250 | 0.056 | 1.000 |

| Subbagged Ensemble | 0.065 | 0.954 | |

| Linear Model | 500 | 0.048 | 1.000 |

| Subbagged Ensemble | 0.047 | 0.998 | |

| Linear Model | 1000 | 0.046 | 1.000 |

| Subbagged Ensemble | 0.020 | 0.999 |

We also selected a number of more complex regression functions that have been used in previous publications related to testing additivity, such as De Canditiis and Sapatinas, (2004) and Barry, (1993), to further investigate -level and power. Each estimate is the result of 1000 simulations with a sample size of 500, subsample size of 50, and a test grid (with levels 0.2, 0.4, 0.6, and 0.8) in the 2-dimensional tests for total additivity and a grid (with levels 0.3, 0.5, and 0.7) in the 3-dimensional tests for total and partial additivity. In each case the features were selected uniformly at random from , the responses generated according to with with chosen to take values , or , and the covariance estimated via the internal estimation procedure. The results are shown in Table 2 where the first line for each model gives the rejection probability for the tests defined here. Note that even though the response in the first two models does not depend on , this additional feature was still included in the training sets and the same test for total additivity was performed. In each case, we see that our false rejection rate is very conservative and we also maintain high power. Note that in each of these simulations, the variance estimation parameters were selected as and . These parameters assignments are smaller than those chosen in Mentch and Hooker, (2016) and the authors note that these smaller ensemble sizes often lead to an overestimate of the variance thus resulting in the conservative test results (low -levels) seen in Table 2.

Model Test Noise s.d. Model Test Noise s.d. (a) T 0.009 0.007 0.000 (h) T 0.085 0.702 1.000 0.025 0.031 0.000 0.305 0.927 1.000 (b) T 0.002 0.000 0.000 (i) P 0.001 0.007 0.948 0.028 0.011 0.000 0.002 0.028 0.998 (c) T 0.008 0.008 0.007 (j) T 0.006 0.029 0.948 0.045 0.060 0.059 0.021 0.089 0.999 (d) T 0.002 0.003 0.001 (k) T 1.000 1.000 1.000 0.000 0.001 0.001 1.000 1.000 1.000 (e) T 0.003 0.007 0.007 (l) P 0.158 0.874 1.000 0.005 0.019 0.012 0.011 0.222 0.959 (f) P 0.000 0.000 0.002 (m) T 0.907 1.000 1.000 0.000 0.001 0.008 0.987 1.000 1.000 (g) P 0.000 0.001 0.014 (n) P 0.051 0.722 0.999 0.000 0.006 0.066 0.136 0.898 1.000

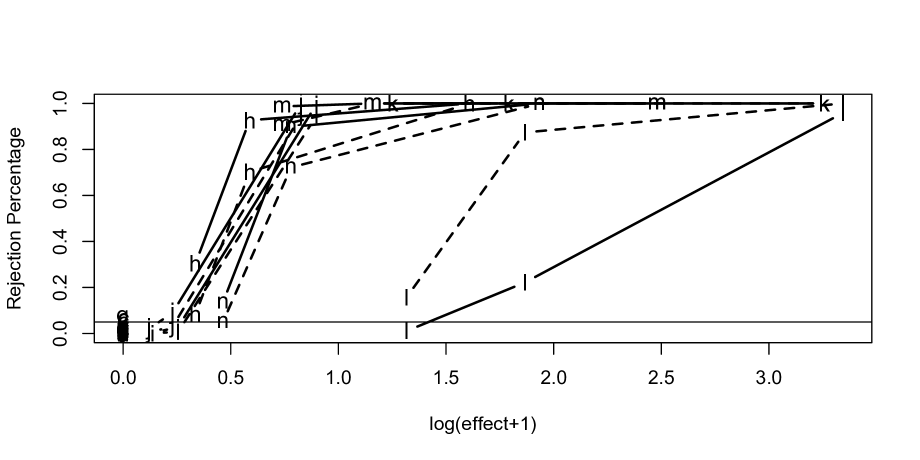

Next, we repeated these simulations on the same functions, this time employing our tests that utilize random projections. In the 2-dimensional tests for total additivity, we use a grid so that and in the 3-dimensional tests for total additivity and the tests for partial additivity, we use a grid so that . The results are shown in Table 2 in the second row for each model. Note that in these tests, we maintain a reasonable type 1 error rate but achieve significantly more power due to the finer resolution of the test grid. These results are also presented graphically in Figure 2 where we can see that the tests utilizing random projections tend to have higher power. The only exception to this is model (l) with where the complexity of the response surface and the choice of evaluation points likely affected the outcome.

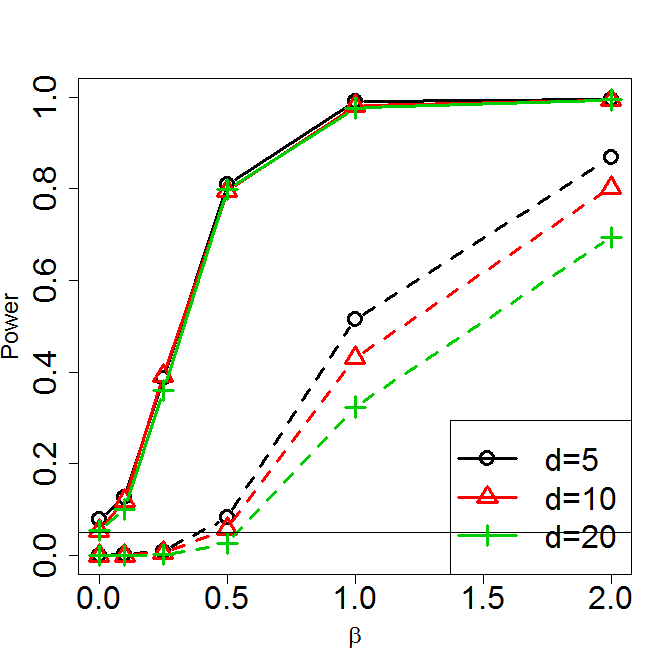

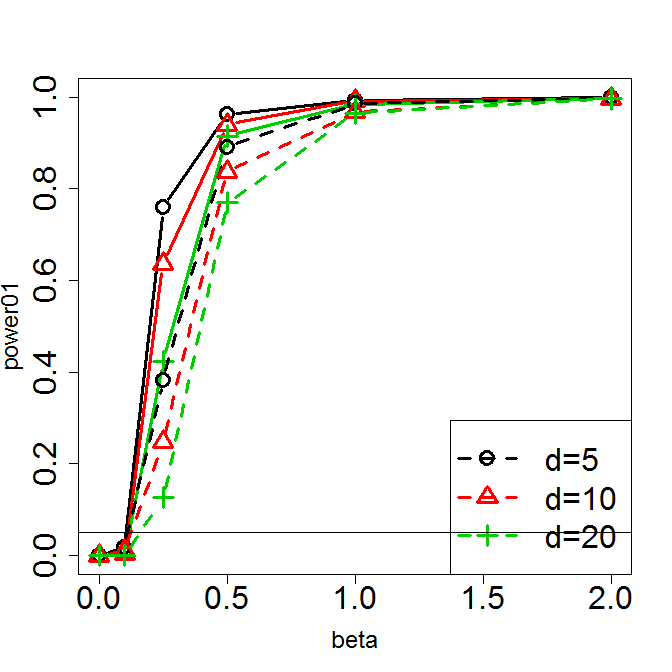

The computational effort required to perform these tests is proportional to the dimension and overall size of the chosen grid. That is, tests of a particular form may be carried out at little additional computational cost for larger dimensions of the covariate space. To demonstrate this point, we first examine a test of total additivity. Here we again employ the model where covariates are sampled uniformly from , takes values , and , and is chosen to be either or . Here represents the dimension of nuisance covariates and is taken to be one of , , , , , , giving the strength of the interaction. For each combination of and , we employ a grid with points selected uniformly in [-0.6, 0.6] and utilize 1000 random projections with . Selecting interior grid points in [-0.6, 0.6] helps avoid the potential edge effects common in tree-based methods when predicting near the boundary of the feature space. For each of these settings, we generated 1000 datasets of 500 observations from which we obtained a random forest with subsamples of size 50 and conducted tests of total and partial additivity. The results of this simulation are given in left two panels of Figure 3 where we see that these tests achieve approximately the correct level at , but quickly produce high power. We observe an expected drop in power with increasing error variance, but relative insensitivity to nuisance dimensions.

| Total Additivity | Partial Additivity | Variable Importance |

|---|---|---|

|

|

|

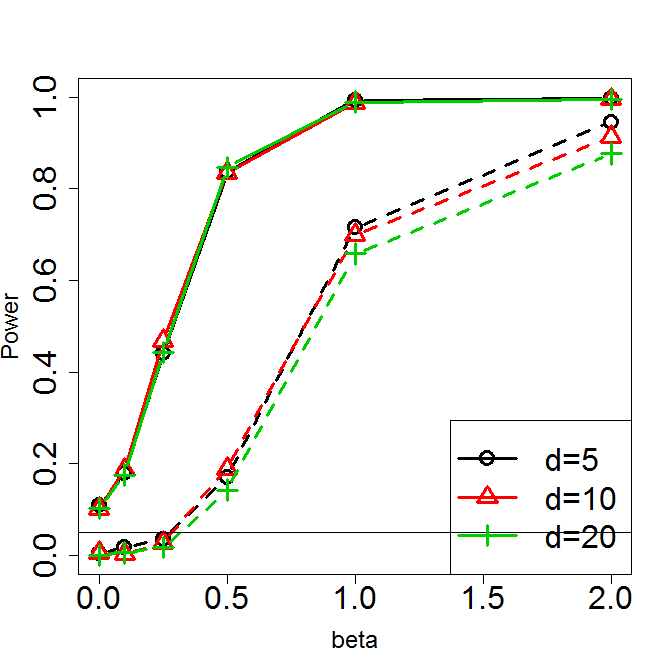

We next extend this experiment to testing the importance of a group of variables. Here we employ the model

under the same data generation scheme. Here we test the joint significance of while also including further signal from . As above, we used , 10 or 20 additional nuisance covariates and is taken to be one of , , , , , , giving the strength of the signal from the first three covariates. The are again normal with standard deviation 0.1 or 1. The right panel in Figure 3 shows the empirical power of the test of importance for the vector based on 1000 simulations of datasets of size 500 and subsamples of size 50. For each combination of and , we employ a grid with points selected uniformly in [-0.6, 0.6] and utilize 1000 random projections with . We observe approximately the correct -level at with power increasing with , resulting in power of approximately 0.8 at . These results are in agreement with Biau, (2012) in which it is suggested that random forests are largely able ignore nuisance covariates with power decreasing only marginally with larger nuisance dimension .

6 Real data

We now demonstrate our testing procedures on a dataset provided by a team of ornithologists at the Cornell University Lab of Ornithology. This dataset was compiled in an effort to determine how pollution levels affect the change in Wood Thursh population. The data consists of 3 pollutant features, mercury deposition (), acid deposition (), and soil PH level () as well as 2 non-pollutant features, elevation () and abundance (). We begin our analysis by testing whether the pollutant and non-pollutant features are additive:

| (6) |

In this case we have two feature sets, and and we performed a test for total additivity using 4 levels of each set – the 0.20, 0.40, 0.60, and 0.80 quantiles of each feature – for a total of 16 test points. Our test statistic was 52.30, larger than the critical value, the 0.95 quantile of the , of 16.92 so we reject the null hypothesis in (6) and conclude that an interaction exists between the pollutant and non-pollutant features. This result was confirmed by our random projection test, which consisted of 1000 random projections to a dimension of using a test grid. In this case, the final averaged p-value was only 0.0043, far below the critical value of 0.485.

Next, we investigated how the pollutants contributed to the response. Based on preliminary investigations, ebird researchers suspected an interaction between mercury and acid deposition ( and ) but were unsure of the relationship between soil PH () and and . In performing these tests for partial additivity, our test grid consisted of 3 points for each feature set, the 0.30, 0.50, and 0.70 quantiles of each feature for a total of 27 test points and a critical value, the 0.95 quantile of the , of 21.03. Our test for partial additivity between and ,

yielded a significant result with a test statistic of 41.00 so our test supports the belief that an interaction exists between and . Again, this result was supported by our random projection test, which consisted of 1000 random projections to a dimension of using a test grid, for a total of 125 test points. The final averaged p-value was only 0.0064, far below the critical value of 0.485.

Our test for partial additivity between and the vector

yielded a test statistic of 36.43, above the critical value of 21.03, so once again we reject the null hypothesis and conclude that an interaction exists between and . This result was again supported by the random projection test based on 1000 random projections to a dimension of using a test grid. We find a final averaged p-value of 0.225, which, though larger than in the previous tests, is still far below the critical value of 0.485.

7 Discussion

This work harnesses desirable asymptotic properties of subsampled ensemble learners to develop formal hypothesis tests for additivity in random forests and suggests that traditional scientific and statistical questions need not be seen as a sacrifice of less interpretable learning procedures. Our tests require the definition of a reasonably sized test grid in order achieve reasonably accurate covariance estimates while preserving power. When larger grids or more complex additive forms are required, we appeal to random projections and demonstrate that our tests still maintain very high power.

Many of the above demonstrations employed a version of random forests in which each covariate remains eligible at each split (subbagged ensembles), though we point out that the theory established in previous work such as Mentch and Hooker, (2016), Wager and Athey, (2015), and Scornet et al., (2015) allows for most general subsampled random forests implementations, or in fact any ensemble-type learner that conforms to the regularity conditions to be used. We caution however that the predictive improvement often seen with random forests is generally attributed to the increased independence between trees and thus should be expected to be less dramatic in these cases where subsamples are used in lieu of the traditional bootstrap samples.

Finally, it is important to note that the particular additive forms for which the testing procedures were developed were chosen only because of their scientific utility. Testing procedures for alternative additive forms can be developed in a similar manner by establishing appropriate model parameters from an ANOVA set-up and defining the difference matrix accordingly. These methods can also be extended to provide formal statistical guarantees for the screening procedures described in Hooker, (2004).

References

- Amato and Antoniadis, (2001) Amato, U. and Antoniadis, A. (2001). Adaptive wavelet series estimation in separable nonparametric regression models. Statistics and Computing, 11(4):373–394.

- Barry, (1993) Barry, D. (1993). Testing for additivity of a regression function. The Annals of Statistics, pages 235–254.

- Biau, (2012) Biau, G. (2012). Analysis of a Random Forests Model. The Journal of Machine Learning Research, 98888:1063–1095.

- Breiman, (1996) Breiman, L. (1996). Bagging predictors. Machine Learning, 24:123–140.

- Breiman, (2001) Breiman, L. (2001). Random Forests. Machine Learning, 45:5–32.

- Buja et al., (1989) Buja, A., Hastie, T., and Tibshirani, R. (1989). Linear smoothers and additive models. The Annals of Statistics, pages 453–510.

- De Canditiis and Sapatinas, (2004) De Canditiis, D. and Sapatinas, T. (2004). Testing for additivity and joint effects in multivariate nonparametric regression using fourier and wavelet methods. Statistics and Computing, 14(3):235–249.

- Derbort et al., (2002) Derbort, S., Dette, H., and Munk, A. (2002). A test for additivity in nonparametric regression. Annals of the Institute of Statistical Mathematics, 54(1):60–82.

- Dette and Derbort, (2001) Dette, H. and Derbort, S. (2001). Analysis of variance in nonparametric regression models. Journal of multivariate analysis, 76(1):110–137.

- Efron, (2014) Efron, B. (2014). Estimation and accuracy after model selection. Journal of the American Statistical Association, 109(507):991–1007.

- Eubank et al., (1995) Eubank, R., Hart, J. D., Simpson, D., Stefanski, L. A., et al. (1995). Testing for additivity in nonparametric regression. The Annals of Statistics, 23(6):1896–1920.

- Fan and Jiang, (2005) Fan, J. and Jiang, J. (2005). Nonparametric inferences for additive models. Journal of the American Statistical Association, 100(471):890–907.

- Friedman and Stuetzle, (1981) Friedman, J. H. and Stuetzle, W. (1981). Projection pursuit regression. Journal of the American statistical Association, 76(376):817–823.

- Hastie and Tibshirani, (1990) Hastie, T. J. and Tibshirani, R. J. (1990). Generalized Additive Models, volume 43. CRC Press.

- Hooker, (2004) Hooker, G. (2004). Discovering additive structure in black box functions. In Proceedings of the tenth ACM SIGKDD international conference on Knowledge discovery and data mining, pages 575–580. ACM.

- Hooker, (2007) Hooker, G. (2007). Generalized functional anova diagnostics for high-dimensional functions of dependent variables. Journal of Computational and Graphical Statistics, 16(3).

- Johnson and Lindenstrauss, (1984) Johnson, W. B. and Lindenstrauss, J. (1984). Extensions of lipschitz mappings into a hilbert space. Contemporary mathematics, 26(189-206):1.

- Linton, (1995) Linton, O. (1995). A kernel method of estimating structured nonparametric. Biometrika, 82(1):93–100.

- Lopes et al., (2011) Lopes, M., Jacob, L., and Wainwright, M. J. (2011). A more powerful two-sample test in high dimensions using random projection. In Advances in Neural Information Processing Systems, pages 1206–1214.

- Lou et al., (2013) Lou, Y., Caruana, R., Gehrke, J., and Hooker, G. (2013). Accurate intelligible models with pairwise interactions. In Proceedings of the 19th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 623–631. ACM.

- Mammen et al., (1999) Mammen, E., Linton, O., Nielsen, J., et al. (1999). The existence and asymptotic properties of a backfitting projection algorithm under weak conditions. The Annals of Statistics, 27(5):1443–1490.

- Mentch and Hooker, (2016) Mentch, L. and Hooker, G. (2016). Quantifying uncertainty in random forests via confidence intervals and hypothesis tests. Journal of Machine Learning Research, 17:1–41.

- Opsomer and Ruppert, (1998) Opsomer, J. D. and Ruppert, D. (1998). A fully automated bandwidth selection method for fitting additive models. Journal of the American Statistical Association, 93(442):605–619.

- Opsomer and Ruppert, (1999) Opsomer, J. D. and Ruppert, D. (1999). A root-n consistent backfitting estimator for semiparametric additive modeling. Journal of Computational and Graphical Statistics, 8(4):715–732.

- Scornet et al., (2015) Scornet, E., Biau, G., and Vert, J.-P. (2015). Consistency of random forests. The Annals of Statistics, 43(4):1716–1741.

- Sobol, (2001) Sobol, I. M. (2001). Global sensitivity indices for nonlinear mathematical models and their monte carlo estimates. Mathematics and computers in simulation, 55(1-3):271–280.

- Srivastava et al., (2015) Srivastava, R., Li, P., and Ruppert, D. (2015). RAPTT: An Exact Two-Sample Test in High Dimensions Using Random Projections. Journal of Computational and Graphical Statistics, (just-accepted).

- Stone, (1985) Stone, C. J. (1985). Additive regression and other nonparametric models. The annals of Statistics, pages 689–705.

- Wager and Athey, (2015) Wager, S. and Athey, S. (2015). Estimation and inference of heterogeneous treatment effects using random forests. arXiv preprint arXiv:1510.04342.

- Wager et al., (2014) Wager, S., Hastie, T., and Efron, B. (2014). Confidence intervals for random forests: The jackknife and the infinitesimal jackknife. Journal of Machine Learning Research, 15:1625–1651.

Appendix

Appendix A The generalized approach

The testing procedures developed in Sections 2 and 3 were derived by choosing the model parameters that minimized the sum of squared error (SSE) with equal weight placed on each point in the test grid. Instead, we may wish to differentially weight points on the grid. For example, in the above tests for partial additivity, we can select and to minimize the weighted SSE

where can be taken as individual features or interpreted more generally as vectors of features and the weights are specified by the user. Hooker, (2007) recommends basing such weights on an approximation to the density of observations near . This procedure takes the form of a weighted ANOVA. In particular, define to be the vector concatenating the and and as in the previous sections let be the vector containing the . Further, let be the matrix defined so that produces the corresponding and let be a diagonal matrix containing the weights. Then we can write

and we know that the solution that minimizes this weighted SSE is given by

so that under the null hypothesis

has mean 0. Further, letting denote the covariance of , the variance of is given by

so that

has a distribution, where remains as defined in the standard procedures developed in Sections 2 and 3. For equal weighting ( given by the identity matrix), these calculations reduce to the averages employed above, and for the sake of simplicity we have restricted ourselves to this choice. Note also that this generalized WLS approach can be applied to more general forms of additivity as well as those tests for total additivity developed in the previous section.