∎

11institutetext: Theja Tulabandhula 22institutetext: Department of Electrical Engineering and Computer Science,

Massachusetts Institute of Technology, Cambridge, MA 02139, USA.

22email: theja@mit.edu

33institutetext: Cynthia Rudin 44institutetext: MIT Sloan School of Management,

Massachusetts Institute of Technology, Cambridge, MA 02139, USA.

44email: rudin@mit.edu

Generalization Bounds for Learning with Linear, Polygonal, Quadratic and Conic Side Knowledge

Abstract

In this paper, we consider a supervised learning setting where side knowledge is provided about the labels of unlabeled examples. The side knowledge has the effect of reducing the hypothesis space, leading to tighter generalization bounds, and thus possibly better generalization. We consider several types of side knowledge, the first leading to linear and polygonal constraints on the hypothesis space, the second leading to quadratic constraints, and the last leading to conic constraints. We show how different types of domain knowledge can lead directly to these kinds of side knowledge. We prove bounds on complexity measures of the hypothesis space for quadratic and conic side knowledge, and show that these bounds are tight in a specific sense for the quadratic case.

Keywords:

statistical learning theory generalization bounds Rademacher complexity covering numbers, constrained linear function classes side knowledge1 Introduction

Surely, for many applications the amount of domain knowledge we could potentially use within our learning processes is vastly larger than the amount of domain knowledge we actually use. One reason for this is that domain knowledge may be nontrivial to incorporate into algorithms or analysis. A few types of domain knowledge that do permit analysis have been explored quite in depth in the past few years and used very successfully in a variety of learning tasks; this includes knowledge about the sparsity properties of linear models (-norm constraints, minimum description length) or smoothness properties (-norm constraints, maximum entropy). A reason that domain knowledge is not usually incorporated in theoretical analysis is that it can be very problem specific; it may be too specific to the domain to have an overarching theory of interest. For example, researchers in NLP (Natural Language Processing) have long figured out various exotic domain specific knowledge that one can use while performing a learning task Chang et al. (2008a, b). The present work aims to provide theoretical guarantees for a large class of problems with a general type of domain knowledge that goes beyond sparsity and smoothness.

To define this large class of problems, we will keep the usual supervised learning assumption that the training examples are drawn i.i.d. Additionally in our setting, we have a different set of examples without labels, not necessarily chosen randomly. For this set of unlabeled examples, we have some prior knowledge about the relationships between their labels, which affects the space of hypotheses we are searching over within our learning algorithms. We motivate this knowledge as being obtained from domain experts. These assumptions can, for example, take into account our partial knowledge about how any learned model should predict on the unlabeled examples if they were encountered. We consider many types of side knowledge, namely constraints on the unlabeled examples leading to (i) linear constraints on a linear function class, (ii) quadratic constraints on a linear function class, and (iii) conic constraints on a linear function class. Our main contributions are:

-

•

To show that linear, polygonal, quadratic and conic constraints on a linear hypothesis space can arise naturally in many circumstances, from constraints on a set of unlabeled examples. This is in Section 2. We connect these with relevant semi-supervised learning settings.

-

•

To provide upper bounds on covering number and empirical Rademacher complexity for linearly constrained linear function classes. Bounds for the case of linear and polygonal constraints are found in Sections 3.3 and 3.4 respectively. Two of the three bounds in these sections are not original to this paper, but their application to general side knowledge with linear constraints is novel.

-

•

To provide two upper bounds on the complexity of the hypothesis space for the quadratic constraint case This can be used directly in generalization bounds. The use of a certain family of circumscribing ellipsoids and the quadratic bounds of Section 3.5 are novel to this paper.

-

•

To show that one of the upper bounds on the quadratically constrained hypothesis space we provided has a matching lower bound, also in Section 3.5. This is novel to this paper.

-

•

To provide a bound on the complexity of the hypothesis space for the conic constraint case. These bounds are in Section 3.7 and are novel to this paper.

-

•

We develop a novel proof technique for upper bounding linear, quadratic and conic constraint cases based on convex duality.

Figure 1 illustrates the various types of side knowledge.

Side knowledge can be particularly helpful in cases where data are scarce; these are precisely circumstances when data themselves cannot fully define the predictive model, and thus domain knowledge can make an impact in predictive accuracy. That said, for any type of side knowledge (sparsity, smoothness, and the side knowledge considered here), the examples and hypothesis space may not conform in reality to the side knowledge. (Similarly, the training data may not be truly random in practice.) However, if they do, we can claim lower sample complexities, and potentially improve our model selection efforts. Thus, we cannot claim that our side knowledge is always true knowledge, but we can claim that if it is true, we are able to gain some benefit in learning.

Motivating examples

Fung et al. (2002) added multiple linear constraints (polygonal constraints) to a specific ERM algorithm, the linear SVM, as a way to incorporate prior knowledge. They investigated the effect of using this type of prior knowledge for classification on a DNA promoter recognition dataset Towell et al. (1990). In this classification task, the linear constraints result from precomputed rules that are separate from the training data (this is similar to our polygonal setting where constraints are generated from knowledge about the unlabeled examples). The “leave-one-out” error from the 1-norm SVM with the additional constraints was less than that of the plain 1-norm SVM and other training-data-based classifiers such as decision trees and neural networks. This and other types of knowledge incorporation in SVMs are reviewed by Lauer and Bloch (2008) and also Le et al. (2006).

James et al. (2014) motivated the use of linear constraints with LASSO, which is also an ERM procedure. In their experiment, they estimated a demand probability function using an on-line auto lending dataset. They ensured monotonicity of the demand function by applying a set of linear constraints (similar to the poset constraints in 2.1) and compared the output to two other methods: logistic regression and the unconstrained LASSO, both of which output non-monotonic demand probability curves.

Nguyen and Caruana (2008a) considered additional unlabeled examples whose labels are partially known. In particular, they worked on a type of multi-class classification task where they know that the label of each unlabeled example belongs to a known subset of the set of all class labels. This knowledge about the unlabeled examples translates into multiple linear constraints (polygonal constraints). They provided experimental results on five datasets showing improvements over multi-class SVMs.

Gómez-Chova et al. (2008) implemented a technique (known as LapSVMs) that uses Laplacian regularization augmented with standard SVMs for two image classification tasks related to urban monitoring and cloud screening (which are both remote sensing tasks). Laplacian regularization means that the regularization term is a quadratic function of the model, derived from a set of unlabeled examples, like our quadratic setting (see Section 2.2). In both tasks, the Laplacian-regularized linear SVMs outperformed the standard SVMs in terms of overall accuracy (these improvements are of the order of 2-3% in both cases).

Shivaswamy et al. (2006) formulated robust classification and regression problems as described in Section 2.3 leading to conic constraints on the model class. For classification, they used the OCR, Heart, Ionosphere and Sonar datasets from the UCI repository to illustrate the effect of missing values and how robust SVM classification (which introduces second order conic constraints) provides better classification accuracy than the standard SVM classifier after imputation. For regression, they showed improvements in prediction accuracy of a robust version of SVR (again introducing conic constraints on the hypothesis space) as compared to a standard SVR trained after imputation on the Boston housing dataset (also from the UCI repository).

Finally, Appendix A also provides experimental results showing the advantage of using side knowledge in a ridge regression problem.

2 Linear, Polygonal, Quadratic and Conic Constraints

We are given training sample of examples with each observation belong to a set in . Let the label belong to a set in . In addition, we are given a set of unlabeled examples . We are not given the true labels for these observations. Let be the function class (set of hypotheses) of interest, from which we want to choose a function to predict the label of future unseen observations. Let it be linear, parameterized by coefficient vector and its description will change based on the constraints we place on .

Consider the empirical risk minimization problem: . Here the loss function is a Lipschitz continuous function such as the squared, exponential or hinge loss among others. This supervised learning setup encompasses both supervised classification ( is a discrete set) and regression ( is equal to ). Regularization on acts to enforce assumptions that the true model comes from a restricted class, so that is now defined as

where represents the transpose operation. Here we have appended additional constraints for regularization to the description of the hypothesis set . Especially if the training set is small, side knowledge can be very powerful in reducing the size of . Particularly if constants are small, the size of be reduced substantially.

2.1 Assumptions leading to linear and polygonal constraints

We will provide three settings to demonstrate that linear constraints arise in a variety of natural settings: poset, must-link, and sparsity on . In all three, we will include standard regularization of the form by default.

Poset:

Partial order information about the labels can be captured via the following constraints: for any collection of pairs . This gives us up to constraints of the form

can be described as: , where is the set of pairs of indices of unlabeled data that are constrained.

Must-link: Here we bound the absolute difference of labels between pairs of unlabeled examples: . This captures knowledge about the nearness of the labels. This leads to two linear constraints: These constraints have been used extensively within the semi-supervised Zhu (2005) and constrained clustering settings Lu and Leen (2004); Basu et al. (2006) as must-link or ‘in equivalence’ constraints.

For must-link constraints, is defined as:

, where is again the set of pairs of indices of unlabeled data that are constrained.

Sparsity and its variants on a subset of :

Similar to sparsity assumptions on , here we want that only a small set of labels is nonzero among a set of unlabeled examples.

In particular, we want to bound the cardinality of the support of the vector for some index set . Such a constraint is nonlinear. Nonetheless, a convex constraint of the form ( linear constraints) can be used as a proxy to encourage sparsity. The function class is defined as: .

A similar constraint can be obtained if we instead had partial information with respect to the dual norm: .

2.2 Assumptions leading to quadratic constraints

We will provide several settings to show that quadratic constraints arise naturally.

Must-link:

A constraint of the form

can be written as

with . Here is rank-deficient as it is an outer product, which leads to an unbounded ellipse; however, its intersection with a full ellipsoid (for instance, an -norm ball) is not unbounded and indeed can be a restricted hypothesis set.

Set is defined by:

, where is again the set of pairs of indices of unlabeled data that are constrained.

Constraining label values for a pair of examples: We can define the following relationship between the labels of two unlabeled examples using quadratic constraints: if one of them is large in magnitude, the other is necessarily small. This can be encoded using the inequality: . If , then gives the following quadratic constraint on with the associated rank 1 matrix being : This is not quite an ellipsoidal constraint yet because matrices associated with ellipsoids are symmetric positive semidefinite. Matrix on the other hand is not symmetric. Nonetheless, the quadratic constraint remains intact when we replace matrix with the symmetric matrix . If in addition, the symmetric matrix is also positive-definite (which can be verified easily), then this leads to an ellipsoidal constraint. The hypothesis space becomes:

Energy of estimated labels:

We can place an upper bound constraint on the sum of squares (the “energy”) of the predictions, which is:

where is a dimensional matrix with ’s as its columns.111Note that this notation is not the usual notation where observations ’s are stacked as rows.

The set is

.

Extensions like the use of Mahalanobis distance or having the norm act on only a subset of the estimates of follow accordingly.

Smoothness and other constraints on :

Consider the general ellipsoid constraint where we have added an additional transformation matrix in front of . If is set to the identity matrix, we get the energy constraint previously discussed. If is a banded matrix with and for all and remaining entries zero, then we are encoding the side knowledge that the variation in the labels of the unlabeled examples is smoothly varying: we are encouraging the unlabeled examples with neighboring indices to have similar predicted values.

This matrix is an instance of a difference operator in the numerical analysis literature. In this context, banded matrices like model discrete derivatives.

By including this type of constraint, problems with identifiability and ill-posedness of an optimal solution are alleviated. That is, as with the Tikhonov regularization on in least squares regression, constraints derived from matrices like reduce the condition number. The set is defined as:

Graph based methods: Some graph regularization methods such as manifold regularization Belkin and Niyogi (2004) also encode information about the labels of the unlabeled data. They also lead to convex quadratic constraints on . Here, along with the unlabeled examples , our side knowledge consists of an -node weighted graph with the Laplacian matrix . Here, is a -dimensional diagonal matrix with the diagonal entry for each node equal to the sum of weights of the edges connecting it. Further, is the adjacency matrix containing the edge weights , where if and if (other choices for the weights are also possible). The quadratic function is then twice the sum over all edges, of the weighted squared difference between the two node labels corresponding to the edge: Intuitively, if we have the side knowledge that this quantity is small, it means that a node should have similar labels to its neighbors. For classification, this typically encourages the decision boundary to avoid dense regions of the graph. The set is defined as: .

2.3 Assumptions leading to conic constraints

We provide two scenarios that naturally lead to conic constraints on the model class: robustness against uncertainty and stochastic constraints.

Robustness against uncertainty in linear constraints: Consider any of the linear constraints considered in Section 2.1. All of these can be generically represented as: where for each , is a function of the unlabeled sample (for instance, for Poset constraints). Further assume that each is only known to belong to an ellipsoid with both parameters and known. This can happen due to measurement limitations, noise and other factors. We want to guarantee that, irrespective of the true value of , we still have .

Borrowing a trick used in the robust linear programming literature, we can encode Lanckriet et al. (2003) the above requirement succinctly as:

which is a set of second-order cone constraints. The feasible set becomes smaller when the linear constraints are replaced with the conic constraints above.

Stochastic Programming: Consider a probabilistic constraint of the form , where is now considered a random vector. The motivation for is the same as before (see Section 2.1). If we know that is normally distributed (for instance, due to additive noise) with mean and covariance matrix , then the probabilistic constraint is the same as: , where is the inverse error function. To see this, let be a scalar random variable with mean and variance (this is equal to ). Then, our original constraint can be written as . Since , we can rewrite our constraint as: where is the cumulative distribution function for the standard normal. Further implies . Rearranging terms, we get . Finally, substituting the values for and gives us the following constraint:

which is a second order conic constraint Lobo et al. (1998).

Remark 1

A question of practical interest would be about ways to impose constraints seen in Sections 2.1, 2.2 and 2.3 in a computationally efficient manner. Fortunately, for all the cases we have considered thus far, the side knowledge can be encoded as a set of convex constraints leading to efficient algorithms (if the original empirical risk minimization problem is convex). Further, note that unlike must-link and similarity side knowledge that lead to convex constraints, cannot-link and dissimilarity knowledge is relatively harder to impose and is typically non-convex.

3 Generalization Bounds

In each of the scenarios considered in Section 2, essentially we are given unlabeled examples whose subsets satisfy various properties or side knowledge (for instance, linear ordering, quadratic neighborhood similarity, etc). This side knowledge is also shown to constrain the hypothesis space in various ways. In this section, we will attempt to answer the following statistical question: what effect do these constraints have on the generalization ability of the learned model? We will compute bounds on the complexity of the hypothesis space when the types of constraints seen in Section 2 are included.

3.1 Definition of Complexity Measures

We will look at two complexity measures: the covering number of a hypothesis set and the Rademacher complexity of a hypothesis set. Their definitions are as follows:

Definition 1

Covering Number Kolmogorov and Tikhomirov (1959): Let be an arbitrary set and a (pseudo-)metric space. Let denote set size. For any , an -cover for is a finite set (not necessarily ) s.t. with . The covering number of is where is an -cover for .

Definition 2

Rademacher Complexity Bartlett and Mendelson (2002): Given a training sample , with each drawn i.i.d. from , and hypothesis space , is the defined as the restriction of with respect to . The empirical Rademacher complexity of is

where are Rademacher random variables ( with probability and with probability ). The Rademacher complexity of is its expectation:

If instead we let in the definition, this is the Gaussian complexity of the function class. Generalization bounds often use both these quantities in their statements Bartlett and Mendelson (2002). Unless otherwise specified, the feature vectors in feature space are bounded in norm by constant and the coefficient vectors of the linear function class are bounded in norm with constant .

3.2 Complexity measures within generalization bounds

Given these definitions, a generalization bound statement can be written as follows Bartlett and Mendelson (2002): With probability at least over the training sample ,

where is the Lipschitz constant of the loss function . A relation between the empirical Rademacher complexity and covering number can be used to state the above uniform convergence statement in terms of the covering number. The relation (also known as Dudley’s entropy integral) is Talagrand (2005):

where and is a constant. Thus, we study upper bounds for covering numbers and empirical Rademacher complexities interchangeably through the rest of the paper.

3.3 Complexity results with a single linear constraint

We state two results: the first is based on volumetric arguments and bounds the covering number and the second is based on convex duality and bounds the empirical Rademacher complexity. The first is a result from Tulabandhula and Rudin (2014) while the second is new to this paper.

Volumetric upper bound on the covering number: Tulabandhula and Rudin (2014) analyzed the setting where a bounded linear function class is further constrained by a half space. The motivation there was to study a specific type of side knowledge, namely knowledge about the cost to solve a decision problem associated with the learning problem. The result there extends well beyond operational costs and is applicable to our setting where we have a bounded linear function class with a single half space constraint.

Theorem 3.1

(Theorem 2 of Tulabandhula and Rudin, 2014) Let with , and let be the marginal probability measure on . Let

with . Let . Then for all , for any sample ,

Also, defining and , the function above is:

Intuition: The function can be considered to be the normalized volume of the ball (which is 1) minus the portion that is the spherical cap cut off by the linear constraint. It comes directly from formulae for the volume of spherical caps. We are integrating over the volume of a dimensional sphere of radius and the height term is .

This bound shows that the covering number bound can depend on , which is a direct function of the unlabeled examples . As the norm increases, decreases, thus decreases, and the whole bound decreases. This is a mechanism by which side information on the labels of the unlabeled examples influences the complexity measure of the hypothesis set, potentially improving generalization.

Relation to standard results: It is known Kolmogorov and Tikhomirov (1959) that set (with being a fixed constant as before) has a bound on its covering number of the form .

Since in Theorem 3.1 the same term appears, multiplied by a factor that is at most one and that can be substantially less than one, the bound in Theorem 3.1 can be tighter.

The above result bounds the covering number complexity for the hypothesis set. Next, we will bound the empirical Rademacher complexity for the same hypothesis set as above.

Convex duality based upper bound on empirical Rademacher complexity: Consider the setting in Theorem 3.1. Let for as before. Our attempt to use convex duality to upper bound empirical Rademacher complexity yields the following bound.

Proposition 1

Let with and

with . Then,

where is a dimensional feature matrix and is a dimensional vector of Bernoulli random variables taking values in .

Intuition: We can understand the effect of the linear constraint on the upper bound through the magnitude of vector . Without loss of generality, let the expectation of the optimal value of the first minimization problem be higher (both minimization problems are structurally similar to each other except for a sign change within the norm term). For a fixed value of , this minimization problem involves the distance of vector to the scaled vector in the first term and the scaling factor itself as the second term. Thus, generally, if is large, the scaling factor can be small, resulting in a lower optimal value. We also know that larger corresponds to a tighter half space constraint. Thus, as the linear constraint on the hypothesis space becomes tighter, it makes the optimal solution and the optimal value smaller for each vector. As a result, it tightens the upper bound on the empirical Rademacher complexity.

Relation to standard results: An upper bound on each term of the operation above can be found by setting that recovers the standard upper bound of or without capturing the effect of the linear constraint .

3.4 Complexity results with polygonal/multiple linear constraints and general norm constraints

The following result is from Tulabandhula and Rudin (2013), where the authors analyze the effect of decision making bias on generalization of learning. Again, as in the single linear constraint case, the result extends beyond the setting considered in that paper. In particular, it covers all the motivating scenarios described in Section 2.1.

Let us define the matrix as matrix where and . Then, can be written as with . Define function class as

where and , and are known constants. In other words, we have linear constraints in addition to a norm constraint. As before, let be the restriction of with respect to .

Let be proportional to in the following manner:

Let be a positive number. Further, let the sets parameterized by and parameterized by and be: and Let and be the sizes of the sets and respectively. The subscript in denotes that this polyhedron is a constrained version of . Define to be equal to the product of a diagonal matrix (whose diagonal element is ) and . Define to be the smallest eigenvalue of the matrix .

Theorem 3.2

Intuition: The linear assumptions on the labels of the unlabeled examples determine the parameters that in turn influence the complexity measure bound. In particular, as the linear constraints given by the ’s force the hypothesis space to be smaller, they force to be smaller. This leads to a tighter upper bound on the covering number.

Relation to standard results: We recover the covering number bound for linear function classes given in Zhang (2002) when there are no linear constraints. In this case, the polytope is well structured and the number of integer points in it can be upper bounded in an explicit way combinatorially.

It is possible to convex duality to upper bound the empirical Rademacher complexity as we did in Proposition 1. However, the intuition is less clear, and thus, we omit the bound here.

3.5 Complexity results with quadratic constraints

Consider the set Assume that at least one of the matrices is positive definite and both are positive-semidefinite, symmetric.

Let and be the corresponding ellipsoid sets.

Upper bound on empirical Rademacher complexity: We first find an ellipsoid (with matrix ) circumscribing the intersection of the two ellipsoids and and then find a bound on the Rademacher complexity of a corresponding function class leading to our result for the quadratic constraint case. We will pick matrix to have a particularly desirable property, namely that it is tight. We will call a circumscribing ellipsoid tight when no other ellipsoidal boundary comes between its boundary and the intersection (). If we thus choose this property as our criterion for picking the ellipsoid, then according to the following result, we can do so by a convex combination of the original ellipsoids:

Theorem 3.3

(Circumscribing ellipsoids, Kahan, 1968) There is a family of circumscribing ellipsoids that contains every tight ellipsoid. Every ellipsoid in this family has and is generated by matrix , .

Using the above theorem, we can find a tight ellipsoid that contains the set easily. Note that the right hand sides of the quadratic constraints defining these ellipsoids can be equal to one without loss of generality.

Theorem 3.4

(Rademacher complexity of linear function class with two quadratic constraints) Let

with symmetric positive-semidefinite and . Then,

| (1) |

where is the matrix of a circumscribing ellipsoid of the set and is the matrix with examples ’s as its columns.

Intuition: If the quadratic constraints are such they correspond to small ellipsoids, then the circumscribing ellipsoid will also be small. Correspondingly, the eigenvalues of will be large. Since, the upper bound depends inversely on the magnitude of these eigenvalues (since it depends on ), it becomes tighter. Also, in the setting where the original ellipsoids are large and elongated but their intersection region is small and can be bounded by a small circumscribing ellipsoid, the upper bound is again tighter.

Relation to standard results: If is diagonal (or axis-aligned), then we can write the empirical complexity in terms of the eigenvalues as and this can be bounded by Kakade et al. (2008) when . In that case, all of the are .

Remark 2

Since we can choose any circumscribing matrix in this theorem, we can perform the following optimization to get a circumscribing ellipsoid that minimizes the bound:

| (2) |

This optimization problem is a univariate non-linear program.

Lower bound on empirical Rademacher complexity: We will now show that the dependence of the complexity on is near optimal.

Since is a real symmetric matrix, let us decompose into a product where is a diagonal matrix with the eigenvalues of as its entries and is an orthogonal matrix (i.e., ). Our result, which is similar in form to the upper bound of Theorem 3.4, is as follows.

Theorem 3.5

Intuition: The lower bound is showing that the dependence on is tight modulo a factor and a factor (). The factor is essentially due to the use of the relation between Gaussian and Rademacher complexities in our proof technique. On the other hand, depends on the interaction between the side knowledge about the unlabeled examples (captured through matrix ) and the feature matrix . If there is no interaction, that is, has zero valued rows for all , then the lower bound on empirical Rademacher complexity becomes equal to 0. On the other hand, when there is higher interaction between (or equivalently, ) and , then the factor grows larger, tightening the lower bound on the empirical Rademacher complexity.

The dependence of the lower bound on the strength of the additional convex quadratic constraint is captured via and behaves in a similar way to the upper bound. That is, when the constraint leads to a small circumscribing ellipsoid, the eigenvalues of are small and the lower bound is small (just like the upper bound). On the other hand, if the constraint leads to a larger circumscribing ellipsoid, the eigenvalues of are large, leading to a higher values of the lower bound (the upper bound also increases similarly).

Relation to standard results: As with the upper bound, when there is no second quadratic constraint, . The lower bound depends on the training data through the term in this case.

Comparison to the upper bound: For comparison, we see that the upper bound in Theorem 3.4 is of the form while the lower bound of Theorem 3.5 is of the form

where depends on and .

The proof for the lower bound is similar to what one would do for estimating the complexity of a ellipsoid itself (without regard to a corresponding linear function class). See also the work of Wainwright (2011) for handling single ellipsoids.

Comparison of empirical Rademacher complexity upper bound with a covering number based bound: When matrix describing a circumscribing ellipsoid has eigenvalues , then the covering number can be bounded as:

To get a tight bound, among all circumscribing ellipsoids, we should pick one that minimizes the right hand side of the bound. To do this, we solve an optimization problem involving volume minimization that is different than in (3.5). For instance, this volume minimization can be done using the following steps if at least one of the matrices among and is positive-definite:

-

•

First, and are simultaneously diagonalized by congruence (say with a non-singular matrix called ) to obtain diagonal matrices and . We can guarantee that the set of ratios obtained will be unique.

-

•

The desired ellipsoid can then be obtained by computing

and then multiplying the optimal diagonal matrix with the congruence matrix appropriately. Optimal can be found in polynomial time (for example, using Newton-Raphson).

Comparison with the duality approach to upper bounding empirical Rademacher complexity: A convex duality based upper bound can be derived as shown below.

Theorem 3.6

This upper bound looks similar to the result in Equation (1). Note that is different from in Theorem 3.4. comes from a circumscribing ellipsoid, whereas does not. Instead, the matrix is picked such that minimizes the right hand side of the bound in Equation 3. Qualitatively, we can see that if the matrix corresponding to the second ellipsoid constraint has large eigenvalues (for instance, when the second ellipsoid is a smaller sphere, or is an elongated thin ellipsoid), then is ‘small’ (the eigenvalues are small) leading to a tighter upper bound on the empirical Rademacher complexity.

Extension to multiple convex quadratic constraints: Although Section 3.5 deals with only two convex quadratic constraints, the same strategy can be used to upper bound the complexity of hypothesis class constrained by multiple convex quadratic constraints. In particular, let . Again, assume one of the matrices is positive definite. We can approach this problem in two stages. In the first step, we find an ellipsoid (with matrix ) circumscribing the intersections of the original ellipsoids and in the second step, we reuse Theorem 3.4 to obtain an upper bound in .

We will generalize Equation (3.5) to look for a circumscribing ellipsoid from the family of ellipsoids parameterized by a dimensional vector constrained to the simplex. In other words, the family of circumscribing ellipsoids is given by . We can pick one circumscribing ellipsoid from this family by minimizing the right hand side of Equation 1 over the simplex similar to Equation (3.5):

The above optimization problem is a dimensional polynomial optimization problem.

3.6 Complexity results with linear and quadratic constraints

Consider now the setting where we have both linear and quadratic constraints. In particular, we can have the assumptions leading to linear constraints and those leading to quadratic constraints hold simultaneously. In such a setting, based on Theorems 3.2 and 3.3, we can get a potentially tighter covering number result as follows. Let . Let the function class be

where , , and are known beforehand.

Let matrix be such that is circumscribed by . Defining and in the same way as in Section 3.3, we get the following corollary.

Corollary 1

The corollary holds for any that satisfies the circumscribing requirement. In particular, we can construct the ellipsoid such that it ‘tightly’ circumscribes the set using Theorem 3.3 in the same way as we did in Section 3.5. The intuition for how the parameters of our side knowledge, namely, the linear inequality coefficients and the matrices corresponding to the ellipsoids, is the same as in Sections 3.4 and 3.5. Relation to standard results have also been discussed in these sections.

Extension to arbitrary convex constraints: There are at least three ways to reuse the results we have with linear, polygonal, quadratic and conic constraints to give upper bounds on covering number or empirical Rademacher complexity of function classes with arbitrary convex constraints. Such arbitrary convex constraints can arise in many settings. For instance, when the convex quadratic constraints in Section 2.2 are not symmetric around the origin, we cannot use the results of Section 3.5 directly, but the following techniques apply. Other typical convex constraints include those arising from likelihood models, entropy biases and so on.

The first approach involves constructing an outer polyhedral approximation of the convex constraint set. For instance, if we are given a separation oracle for the convex constraint, constructing an outer polyhedral approximation is relatively straightforward. We can also optimize for properties like the number of facets or vertices of the polyhedron during such a construction. Given such an outer approximation, we can apply Theorem 3.2 to get an upper bound on the covering number of the hypothesis space with the given convex constraint.

The second approach involves constructing a circumscribing ellipsoid for the constraint set. This is possible for any convex set in general John (1948). In addition if the convex set is symmetric around the origin, the ‘tightness’ of the circumscribing ellipsoid improves by a factor , where is the dimension of the linear coefficient vector . Given such a circumscribing ellipsoid, we can apply Theorem 3.4 to get an upper bound on the empirical Rademacher complexity of the original function class with the convex constraint. The quality of both of these outer relaxation approaches depends on the structure and form of the convex constraint we are given.

The third approach is to analyze the empirical Rademacher complexity directly using convex duality as we have done for the linear and quadratic cases, and as we will do for the conic case next.

3.7 Complexity results with multiple conic constraints

Consider the function class

where we have one convex quadratic constraint and conic constraints. We can find an upper bound on the Rademacher complexity as shown below.

Theorem 3.7

(Rademacher complexity of bounded linear function class with conic constraints) Let with and let

where , are the parameters. Assume and let denote its minimum eigenvalue for . Also let . Then,

Intuition: When and are , the effect of conic constraints can influence the upper bound on the empirical Rademacher complexity and make the corresponding generalization bounds tighter. From a geometric point of view, we can infer the following: if the cones are sharp, then are high, implying a smaller empirical Rademacher complexity. Figure 2 illustrates this in two dimensions.

Relation to standard results: The looser unconstrained version of the upper bound is recovered when there are no conic constraints or when the conic constraints are ineffective (for instance, when is high, is a large offset or is small).

Remark 3

There have been some recent attempts to obtain bounds on a related measure, similar to the empirical Gaussian complexity defined here, in the compressed sensing literature that also involves conic constraints Stojnic (2009). Their objective (minimum number of measurements for signal recovery assuming sparsity) is very different from our objective (function class complexity and generalization). In the former context, there are a few results Chandrasekaran et al. (2012) dealing with the intersection of a single generic cone with a sphere () whereas in this context, we look at the intersection of multiple second order cones (explicitly parameterized by ) with balls ().

4 Related Work

It is well-known that having additional unlabeled examples can aid in learning Shental et al. (2004); Nguyen and Caruana (2008b); Gómez-Chova et al. (2008), and this has been the subject of research in semi-supervised learning Zhu (2005). The present work is fundamentally different than semi-supervised learning, because semi-supervised learning exploits the distributional properties of the set of unlabeled examples. In this work, we do not necessarily have enough unlabeled examples to study these distributional properties, but these unlabeled examples do provide us information about the hypothesis space. Distributional properties used in semi-supervised learning include cluster assumptions Singh et al. (2008); Rigollet (2007) and manifold assumptions Belkin and Niyogi (2004); Belkin et al. (2004). In our work, the information we get from the unlabeled examples allows us to restrict the hypothesis space, which lets us be in the framework of empirical risk minimization and give theoretical generalization bounds via complexity measures of the restricted hypothesis spaces Bartlett and Mendelson (2002); Vapnik (1998). While the focus of many works (e.g., Zhang, 2002; Maurer, 2006) is on complexity measures for ball-like function classes, our hypothesis spaces are more complicated, and arise here from constraints on the data.

Researchers have also attempted to incorporate domain knowledge directly into learning algorithms, where this domain knowledge does not necessarily arise from unlabeled examples. For instance, the framework of knowledge based SVMs Fung et al. (2002); Le et al. (2006) motivates the use of various constraints or modifications in the learning procedure to incorporate specific kinds of knowledge (without using unlabeled examples). The focus of Fung et al. (2002) is algorithmic and they consider linear constraints. Le et al. (2006) incorporate knowledge by modifying the function class itself, for instance, from linear function to non-linear functions.

In a different framework, that of Valiant’s PAC learning, there are concentration statements about the risks in the presence of unlabeled examples Balcan and Blum (2005); Kääriäinen (2005), though in these results, the unlabeled points are used in a very different way than in our work. Specifically, in the work of Balcan and Blum (2005), the authors introduce the notion of incompatibility between a function and the input distribution . The unlabeled examples are used to estimate the distribution dependent quantity . By imposing the constraint that models have their incompatibility with the distribution of the data source below a desired level, we restrict the hypothesis space. Their result for a finite hypothesis space is as follows:

Theorem 4.1

(Theorem 1 of Balcan and Blum, 2005) If we see unlabeled examples and labeled examples, where

then with probability , all with zero training error and zero incompatibility , we have .

Here is the finite hypothesis space of which is an element and . In the work of Kääriäinen (2005), the author obtains a generalization bound by approximating the disagreement probability of pairs of classifiers using unlabeled data. Again, here the unlabeled data is used to estimate a distribution dependent quantity, namely, the true disagreement probability between consistent models. In particular, the disagreement between two models and is defined to be . The following theorem about generalization is proposed.

Theorem 4.2

Let be the class of consistent models, that is, the set of models with zero training error. Assume the true model belongs to this class. Let be the function whose distance to the farthest function in is minimal (via metric ). Then, for all , with probability over the choice of unlabeled sample ,

Note that the randomization in both Theorems 4.1 and 4.2 is also over unlabeled data. In our theorems, we do not randomize with respect to the unlabeled data. For us, they serve a different purpose and do not need to be chosen randomly. While their results focus on exploiting unlabeled data to estimate distribution dependent quantities, our technology focuses on exploiting unlabeled data to restrict the hypothesis space directly.

5 Proofs

5.1 Proof of Proposition 1

Proof

Instead of working with the maximization problem in the definition of empirical Rademacher complexity, we will work with a couple of related maximization problems, due to the following lemma.

Lemma 1

| (4) |

Proof

Since the empirical Rademacher complexity is defined as , we will show that for any fixed vector,

| (5) |

The inequality above is straightforward to prove. Let be the optimal solution to the maximization problem on the left. Then, is a feasible point for each of the maximization problems on the right. We will look at two cases: In the first case, let . Then, clearly the first maximization problem on the right, namely, will have an optimal value greater than or equal to the left side of Equation (5). In the second case, let . Then, the second maximization problem on the right, namely, will have an optimal value greater than or equal to the left side of Equation (5). That is, in this case:

Combining the two cases, we get the Equation (5). Taking expectations over gives us the desired inequality.

Continuing with the proof of Proposition 1: Let so that . We will attempt to dualize the two maximization problems in the upper bound provided by Lemma 1 to get a bound on the empirical Rademacher complexity. Both maximization problems are very similar except for the objective. Let be the optimal value of the following optimization problem:

Thus represents the optimal value of the maximization problem inside the expectation operation in the first term of Equation (4). We will now write a dual program to the above and use weak duality to upper bound . The Lagrangian is:

where . Maximizing the Lagrangian with respect to gives us:

The dual problem is thus

Minimizing with respect to one of the decision variables, , gives the following dual problem

Thus, . Similarly we can prove an upper bound on the maximization problem appearing in the second term in the max operation in Equation (4), which will be . Thus, the empirical Rademacher complexity is upper bounded as:

∎

5.2 Proof of Theorem 3.4

Proof

Consider the set . Let . Also, let .

where follows because we are taking the supremum over the circumscribing ellipsoid; follows because is positive definite, hence invertible; (c) is by Cauchy-Schwarz (equality case); (d) uses Jensen’s inequality and (e) uses the linearity of trace and expectation to commute them along with the fact that . ∎

5.3 Proof of Theorem 3.5

Proof

Recall that we can decompose into a product where is a diagonal matrix with the eigenvalues of as its entries and is an orthogonal matrix (i.e., ). Let us define a new variable: , which is a linear transformation of linear model parameter . Then, the empirical Gaussian complexity of our function class can be written as:

where are i.i.d. standard normal random variables. We now define a new vector to be a transformed version of the random vector . That is, let . We will drop the dependence of on from the notation when it is clear from the context. The expression now becomes

| (6) |

where the inequality is because we removed the absolute sign in the right hand side expression before substituting for .

The following are the major steps in our proof:

-

•

We will analyze the Gaussian function and show it is Lipschitz in . This is proved in Lemma 2.

-

•

Then we apply Lemma 3, which is about Gaussian function concentration, to the above function. In particular, we will upper bound the variance of the Gaussian function in terms of its parameters (Lipschitz constant, matrix , etc).

-

•

We then generate a candidate lower bound for the empirical Gaussian complexity.

-

•

The upper bound on the variance of we found earlier is used to make this bound proportional to .

-

•

Finally, we use a relation between empirical Rademacher complexity and empirical Gaussian complexity to obtain the desired result.

Computing a Lipschitz constant for : The following lemma gives an upper bound on the Lipschitz constant of .

Lemma 2

The function is Lipschitz in with a Lipschitz constant bounded by .

Proof

We have

Using a new dummy variable we have:

Thus,

At (a), we used the fact that .

Now, we will upper bound using and as follows. Using the definition of we get,

Here, (b) follows because is an orthonormal matrix, (c) because and (d) because . Since, each diagonal element of is a sum of terms each upper bounded by , we have . ∎

Upper bounding the variance of using Gaussian concentration: The following lemma describes concentration for Lipschitz functions of gaussian random variables.

Lemma 3

(Concentration, Tsirelson et al., 1976) If is a vector with i.i.d. standard normal entries and is any function with Lipschitz constant (with respect to the Euclidean norm), then

Let . Then from the above tail bound, is true. Now we can bound the variance of using the above inequality and the following lemma.

Lemma 4

For a random variable , .

Proof

This is an alternate expression for the expectation of a non-negative univariate random variable in terms of its distribution function. To show this, let us assume that the density function of is . We then have and thus: So,

The first term is zero and we obtain our expression. ∎

The variance of , which is the same as the expectation of , can thus be upper bounded as follows:

| (8) |

where we used Lemma 4 for step (a) and Equation (7) for step (b) and finally substituting for .

Lower bounding the empirical Gaussian complexity: Now we will lower bound the empirical Gaussian complexity by constructing a feasible candidate to substitute for the operation in Equation (6). Later, we will use the variance upper bound on we found in the earlier section to make the bound more specific.

Let be the index at which the diagonal element . For each realization of (or equivalently ) let with the non-zero entry at coordinate . Clearly is a feasible vector in the ellipsoidal constraint seen in the complexity expression, Equation (6). Substituting it and using the definition of , we get a lower bound on the empirical Gaussian complexity:

Step (a) comes from the fact that is feasible in but not necessarily the maximum, and step (b) comes from the definition of .

Making the lower bound more specific using variance of : Note that compared to the upper bound on the related Rademacher complexity obtained in Theorem 3.4, the dependence of empirical Gaussian complexity on is weak (only via ). We will use the variance of to obtain a lower bound very similar to the upper bound in Equation (1). Rearranging the terms in the previous inequality, we get:

| (9) |

By rewriting the variance in terms of the second and first moments, using expression (5.3) and then using (9) we get

Using expression (6) again, and then rearranging the terms in the previous expression, we obtain another lower bound on the scaled Gaussian complexity, which is:

| (10) |

We can now try to bound two easier quantities and to get an expression for scaled Gaussian complexity and consequently for the empirical Rademacher complexity.

Let us start first with . By definition equals . Thus, the th coordinate of will be where represents the th coordinate of the vector. Since the are independent standard normal, their weighted sum is also standard normal with variance . Since for any normal random variable with mean zero and variance it is true that , we have

| (11) |

where represents the row of the matrix . For the second moment term of (10) that we need to bound, , we can see that

Thus,

| (12) |

Substituting the two bounds we just derived, (5.3) and (12), into (10) gives us a lower bound on the scaled Gaussian complexity:

Using the relation between Rademacher and Gaussian complexities: The empirical Gaussian complexity is related to the empirical Rademacher complexity as follows.

Lemma 5

(Lemma 4 of Bartlett and Mendelson, 2002) There are absolute constants and such that for every with ,

Using the above result gives:

Thus, we get our desired result:

| where | |||

∎

5.4 Proof of Corollary 1

Proof

Since the ellipsoid defined using circumscribes the region of intersection of ellipsoids determined by and , we have

Further, since . That is, the set is bigger than the ellipsoid defined using . Thus,

Noting that is the same as , we can use Theorem 3.2 on with and to get a bound on giving us the stated result. ∎

5.5 Proof of Theorem 3.6

Proof

Let so that . Instead of directly working with the empirical Rademacher complexity, we will dualize the two maximization problems in the upper bound given by Equation (4) of Lemma 1. Both maximization problems are very similar except for the objective. Let be the optimal value of the following optimization problem:

Thus is proportional to the first term inside the max operation in Equation (4), which gives an upper bound in the empirical Rademacher complexity. We will now write a dual program to the above and use weak duality to upper bound . The Lagrangian is:

where . Maximizing the Lagrangian with respect to gives us:

where in the last step we set . The dual problem is thus:

| , or equivalently, | |||

If we let , we are further constraining the minimization problem, yielding another upper bound of the form:

If we consider the second maximization problem that appears in Equation (4), we can similarly upper bound its optimal value with the same minimization problem as . One intuitive reason why the same minimization problem serves as an upper bound is because the hypothesis class is closed under negation. Thus, we get an upper bound on the empirical Rademacher complexity as:

where recall that . Fix any feasible . Let (it corresponds to an ellipsoid as well since ). Then,

We can minimize the right hand side over to get the desired result. ∎

5.6 Proof of Theorem 3.7

Proof

The core idea of the proof is to come up with an intuitive upper bound on the empirical Rademacher complexity of using convex duality. We have already seen the use of convex duality in Proposition 1 and Theorem 3.6. Recall the definition of the empirical Rademacher complexity of a function class :

where are i.i.d. Bernoulli random variables taking values in with equal probability. Now define a new vector to be the random vector . As in the previous proofs, instead of directly working with the empirical Rademacher complexity, we will dualize the two maximization problems in the upper bound given by Equation (4) of Lemma 1. Let . That is, is the optimal value of the first maximization problem (ignoring factor ) appearing on the right hand side of Equation (4):

| (13) |

The Lagrangian of the problem can be written as Boyd and Vandenberghe (2004):

where and for we have . For any set of feasible values of , the objective of the SOCP in Equation (13) is upper bounded by . Thus, . We will analyze this maximization problem as the first step towards a tractable bound on .

In the second step, we will minimize over variable (one of the dual variables) to get an upper bound on in terms of . These two steps are shown below:

First step: After rearranging terms and completing squares, we get the following dual objective to be minimized over dual variables and .

The second to last equality above is obtained by completing the squares (in terms of ) and the last equality is due to the fact that the optimal value is obtained when . The resulting term is now a function of the remaining variables ( and ) and serves as an upper bound to for any feasible values of and .

Second step: Since when is convex and the feasible set is convex, we now minimize with respect to to get the following upper bound:

where the above statement follows because for a problem of the form with , the optimal solution is .

Continuing, we now optimize over the remaining variables as follows:

| (14) |

An upper bound on can be obtained by finding a set of optimal or feasible values for . Note that since , and exists. Obtaining the optimal value of the minimization in Equation (14) is difficult analytically. Instead, we will pick a suitable feasible value for . Plugging this feasible value will give us an upper bound on . In particular, let . Then, setting gives us a feasible value for each . Thus,

Dualizing the second maximization problem in Equation (4) also gives us the same upper bound as obtained above for . That is, if , then the same analysis as above (replacing with ) gives:

We can now come up with the desired upper bound for the empirical Rademacher complexity using Equation (4):

In the case when there are no active conic constraints, we cannot use this bound. Instead, we can recover the well known standard bound by removing the terms related to conic constraints in Equation (14) and obtain only . Combining both bounds we get,

∎

6 Conclusion

In this paper, we have outlined how various side information about a learning problem can effectively help in generalization. We focused our attention on several types of side information, leading to linear, polygonal, quadratic and conic constraints, giving motivating examples and deriving complexity measure bounds. This work goes beyond the traditional paradigm of ball-like hypothesis spaces to study more exotic, yet realistic, hypothesis spaces, and is a starting point for more work on other interesting hypothesis spaces.

Appendix A: Quantifying the impact of side knowledge

Here we describe an experiment222The source code is available at https://github.com/thejat/supervised_learning_with_side_knowledge. that we did to demonstrate the impact of side knowledge encoded as polygonal (which subsumes linear), quadratic and conic constraints. Our goal was to compare predictive accuracies of a model that used side knowledge to a baseline model that did not use side knowledge.

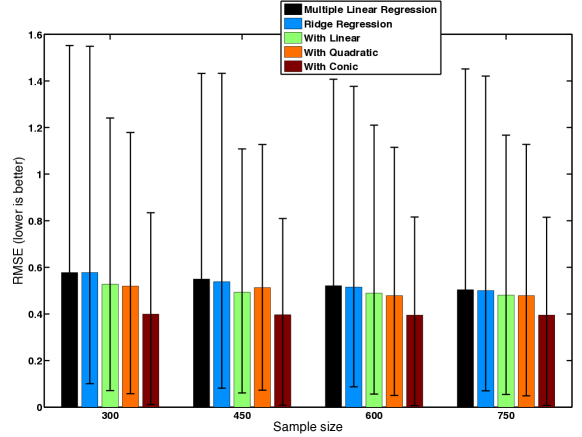

Algorithm setups and performance measure: We measured performance in terms of RMSE (Root Mean Squared Error) for models obtained from five setups: (1) multiple linear regression, (2) ridge regression, (3) ridge regression with polygonal constraints, (4) ridge regression with convex quadratic constraints, and (5) ridge regression with multiple conic constraints.

Dataset: The dataset for this problem was generated using a multidimensional Gaussian distribution (with a fixed covariance matrix). The number of features was set to 60. A coefficient vector was arbitrarily chosen and the response variable was computed as a linear function of the coefficient vector and the feature vector with some additional Gaussian noise. Three types of samples (feature-label pairs) were generated: (a) A test sample of size 750 was kept aside during learning. The prediction performance numbers reported in Figure 3 were computed on this sample. (b) A “knowledge sample” of size 120 was generated in order to incorporate side knowledge as polygonal, quadratic and conic constraints. For all three types of side knowledge, the same “knowledge sample” was used, but different side knowledge was derived from it for the different algorithm setups. For polygonal (or multiple linear) constraints, a poset constraint (see Section 2.1) of the form was constructed for each pair of points in the knowledge set and a subset were chosen for use in the convex formulation (1200 linear constraints out of a possible 7140). A quadratic constraint of the form was constructed to impose a smoothness side knowledge (see Section 2.2). For this, the examples in the knowledge set were first sorted according to to be monotonic and the rows of were reordered accordingly before being used in the constraint. The right hand side parameter of the quadratic constraint was defined to be and was a matrix with and for . One conic constraint for each example in the knowledge set was generated of the form (see Section 2.3). Here, the parameter was a fixed positive real number and is the true underlying coefficient vector. Knowledge of the true underlying coefficient vector is not necessary to impose such conic constraints in practice (and was used here for ease of simulation only). (c) Thirty separate training samples of size 750 were generated. Thus, each time a model was trained, it was trained on one of 30 training sets, using constraints derived from the “knowledge sample” (if it was an algorithm setup that used side knowledge) and tested on the test set.

Experimental Setup: For each training sample (there are 30 of them), and for each of the 5 setups, we constructed a model by solving a convex program. (For the ridge regression methods, we also performed 5-fold cross validation to choose the hyper-parameter corresponding to the -norm regularization term.) We then evaluated each model on the test sample and computed the RMSE. Further, to show dependence on training set size, for each training sample, we changed the data that we used from 300 examples to the full 750 examples (4 training set sizes - 300, 450, 600, 750). In summary, we learned (5 algorithm setups)*(4 training set sizes)*(30 training sets) = 600 models in this experiment, not including cross validation. Figure 3 shows the median RMSE (with 25th and 75th quantiles as whiskers) that we obtain across the 30 models.

Results: We expected a performance increase over standard multiple linear regression when we impose polygonal, quadratic and conic constraints. As seen from Figure 3, this is indeed true. Most prominently, the distribution of RMSE error values shifts downwards when side knowledge is used. As the sample size increases, the difference in performance between a ridge regression model learned without side knowledge and those learned with side knowledge decreases as expected; the side knowledge becomes less useful when more data are available to learn from.

References

- Balcan and Blum [2005] M.F. Balcan and A. Blum. A PAC-style model for learning from labeled and unlabeled data. In Proceedings of Conference on Learning Theory, pages 69–77. Springer, 2005.

- Bartlett and Mendelson [2002] Peter L. Bartlett and Shahar Mendelson. Gaussian and Rademacher complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3:463–482, 2002.

- Basu et al. [2006] Sugato Basu, Mikhail Bilenko, Arindam Banerjee, and Raymond J Mooney. Probabilistic semi-supervised clustering with constraints. In Semi-supervised learning, pages 71–98. Cambridge, MA. MIT Press, 2006.

- Belkin and Niyogi [2004] M. Belkin and P. Niyogi. Semi-supervised learning on riemannian manifolds. Machine Learning, 56(1):209–239, 2004.

- Belkin et al. [2004] Mikhail Belkin, Irina Matveeva, and Partha Niyogi. Regularization and semi-supervised learning on large graphs. In Proceedings of Conference on Learning Theory, pages 624–638. Springer, 2004.

- Boyd and Vandenberghe [2004] Stephen P Boyd and Lieven Vandenberghe. Convex optimization. Cambridge university press, 2004.

- Chandrasekaran et al. [2012] Venkat Chandrasekaran, Benjamin Recht, Pablo A Parrilo, and Alan S Willsky. The convex geometry of linear inverse problems. Foundations of Computational Mathematics, 12(6):805–849, 2012.

- Chang et al. [2008a] M Chang, Lev Ratinov, and Dan Roth. Constraints as prior knowledge. In ICML Workshop on Prior Knowledge for Text and Language Processing, pages 32–39, 2008a.

- Chang et al. [2008b] Ming-Wei Chang, Lev-Arie Ratinov, Nicholas Rizzolo, and Dan Roth. Learning and inference with constraints. In AAAI Conference on Artificial Intelligence, pages 1513–1518, 2008b.

- Fung et al. [2002] Glenn M Fung, Olvi L Mangasarian, and Jude W Shavlik. Knowledge-based support vector machine classifiers. In Proceedings of Neural Information Processing Systems, pages 521–528, 2002.

- Gómez-Chova et al. [2008] Luis Gómez-Chova, Gustavo Camps-Valls, Jordi Munoz-Mari, and Javier Calpe. Semisupervised image classification with laplacian support vector machines. Geoscience and Remote Sensing Letters, IEEE, 5(3):336–340, 2008.

- James et al. [2014] G. M James, C Paulson, and P Rusmevichientong. The constrained lasso. working paper, 2014.

- John [1948] Fritz John. Extremum problems with inequalities as subsidiary conditions. Studies and Essays Presented to R. Courant on his 60th Birthday, January 8, 1948, pages 187–204, 1948.

- Kääriäinen [2005] Matti Kääriäinen. Generalization error bounds using unlabeled data. In Proceedings of Conference on Learning Theory, pages 127–142. Springer, 2005.

- Kahan [1968] W. Kahan. Circumscribing an ellipsoid about the intersection of two ellipsoids. Canadian Mathematical Bulletin, 11(3):437–441, 1968.

- Kakade et al. [2008] S.M. Kakade, K. Sridharan, and A. Tewari. On the complexity of linear prediction: Risk bounds, margin bounds, and regularization. Proceedings of Neural Information Processing Systems, 22, 2008.

- Kolmogorov and Tikhomirov [1959] Andrey Nikolaevich Kolmogorov and Vladimir Mikhailovich Tikhomirov. -entropy and -capacity of sets in function spaces. Uspekhi Matematicheskikh Nauk, 14(2):3–86, 1959.

- Lanckriet et al. [2003] Gert RG Lanckriet, Laurent El Ghaoui, Chiranjib Bhattacharyya, and Michael I Jordan. A robust minimax approach to classification. The Journal of Machine Learning Research, 3:555–582, 2003.

- Lauer and Bloch [2008] Fabien Lauer and Gérard Bloch. Incorporating prior knowledge in support vector machines for classification: A review. Neurocomputing, 71(7):1578–1594, 2008.

- Le et al. [2006] Quoc V Le, Alex J Smola, and Thomas Gärtner. Simpler knowledge-based support vector machines. In Proceedings of the 23rd international conference on Machine learning, pages 521–528. ACM, 2006.

- Lobo et al. [1998] Miguel Sousa Lobo, Lieven Vandenberghe, Stephen Boyd, and Hervé Lebret. Applications of second-order cone programming. Linear algebra and its applications, 284(1):193–228, 1998.

- Lu and Leen [2004] Zhengdong Lu and Todd K Leen. Semi-supervised learning with penalized probabilistic clustering. In Proceedings of Neural Information Processing Systems, pages 849–856, 2004.

- Maurer [2006] Andreas Maurer. The Rademacher complexity of linear transformation classes. In Proceedings of Conference on Learning Theory, pages 65–78. Springer, 2006.

- Nguyen and Caruana [2008a] Nam Nguyen and Rich Caruana. Classification with partial labels. In Proceedings of the 14th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 551–559. ACM, 2008a.

- Nguyen and Caruana [2008b] Nam Nguyen and Rich Caruana. Improving classification with pairwise constraints: a margin-based approach. In Machine Learning and Knowledge Discovery in Databases, pages 113–124. Springer, 2008b.

- Rigollet [2007] Philippe Rigollet. Generalization error bounds in semi-supervised classification under the cluster assumption. Journal of Machine Learning Research, 8:1369–1392, 2007.

- Shental et al. [2004] Noam Shental, Aharon Bar-Hillel, Tomer Hertz, and Daphna Weinshall. Computing Gaussian mixture models with EM using equivalence constraints. In Proceedings of Neural Information Processing Systems, volume 16, pages 465–472, 2004.

- Shivaswamy et al. [2006] Pannagadatta K Shivaswamy, Chiranjib Bhattacharyya, and Alexander J Smola. Second order cone programming approaches for handling missing and uncertain data. The Journal of Machine Learning Research, 7:1283–1314, 2006.

- Singh et al. [2008] Aarti Singh, Robert Nowak, and Xiaojin Zhu. Unlabeled data: Now it helps, now it doesn’t. In Proceedings of Neural Information Processing Systems, pages 1513–1520, 2008.

- Stojnic [2009] Mihailo Stojnic. Various thresholds for l1-optimization in compressed sensing. arXiv preprint arXiv:0907.3666, 2009.

- Talagrand [2005] M. Talagrand. The generic chaining. Springer, 2005.

- Towell et al. [1990] Geofrey G Towell, Jude W Shavlik, and M Noordewier. Refinement of approximate domain theories by knowledge-based neural networks. In Proceedings of the Eighth National Conference on Artificial Intelligence, pages 861–866. Boston, MA, 1990.

- Tsirelson et al. [1976] B. S. Tsirelson, I. A. Ibragimov, and V. N. Sudakov. Norms of gaussian sample functions. In Proceedings of the Third Japan–U.S.S.R. Symposium on Probability Theory. Lecture Notes in Math., volume 550, pages 20–41. Springer, 1976.

- Tulabandhula and Rudin [2013] Theja Tulabandhula and Cynthia Rudin. Machine learning with operational costs. Journal of Machine Learning Research, 14:1989–2028, 2013.

- Tulabandhula and Rudin [2014] Theja Tulabandhula and Cynthia Rudin. On combining machine learning with decision making. Machine Learning, 97(1-2):33–64, 2014.

- Vapnik [1998] Vladimir Naumovich Vapnik. Statistical learning theory, volume 2. Wiley New York, 1998.

- Wainwright [2011] Martin Wainwright. Metric entropy and its uses (Chapter 3). Unpublished draft, 2011.

- Zhang [2002] Tong Zhang. Covering number bounds of certain regularized linear function classes. Journal of Machine Learning Research, 2:527–550, 2002.

- Zhu [2005] Xiaojin Zhu. Semi-supervised learning literature survey. Technical Report 1530, Computer Sciences, University of Wisconsin-Madison, 2005.