Quantile estimation for Lévy measures

Abstract

Generalizing the concept of quantiles to the jump measure of a Lévy process, the generalized quantiles , for , are given by the smallest values such that a jump larger than or a negative jump smaller than , respectively, is expected only once in time units. Nonparametric estimators of the generalized quantiles are constructed using either discrete observations of the process or using option prices in an exponential Lévy model of asset prices. In both models minimax convergence rates are shown. Applying Lepski’s approach, we derive adaptive quantile estimators. The performance of the estimation method is illustrated in simulations and with real data.

Keywords: Adaptive estimation, Lévy processes, minimax convergence rates, nonlinear inverse problem, option prices.

MSC (2000): Primary: 62G05; Secondary: 60E07, 62G20, 62M05, 62M15.

1 Introduction

Whenever the modeling of random processes in biology, finance or physics requires to incorporate jumps, Lévy processes are one of the building blocks under consideration. Consequently, their statistical analysis attracted much attention in the last decades. The estimation of the jump distribution, characterized by the Lévy measure, is of particular interest. So far, only the jump density or linear functionals of it like the corresponding distribution function has been the aim estimation procedures. In the present work, we study the estimation of the (generalized) quantiles of the Lévy measure that is the inverse of the distribution function. For a given intensity the quantile is the minimal jump height such that jumps larger than are expected only times in one time unit. Equivalently a jump larger than is expected only once in time units. is analogously defined for negative jumps, see Section 2 for the precise definitions and a discussion of possible applications.

We will consider two different observation schemes: If we directly observe the Lévy process at equidistant discrete time points , the estimator relies on the increments , for , which are independent and identically distributed according to the law of . We will focus on low-frequency observations where remains fixed while .

The second observation scheme is motivated by an application in finance. Modeling an asset as exponential of a Lévy process , we use prices of put and call options to estimate the characteristics of the Lévy process under the risk-neutral measure. This allows to estimate how shocks, in the sense of large jumps, are priced into the asset. Since the observed option prices are noisy, we face a statistical problem of regression type. The error analysis of the nonparametric estimators is similar to the case of low frequent direct observations.

In a high-frequency regime, i.e. observing with , we almost see the jumps in the path and thus the estimation of the Lévy measure is relatively straight forward, see Aït-Sahalia and Jacod, (2012) for a review. As noticed by Neumann and Reiß, (2009) in the low-frequency regime, i.e. is fixed, the nonparametric estimation problem is more difficult because the number of jumps that occurred within an increment is not identifiable. Using however the Lévy–Khintchine formula which links the characteristic function of the marginal distribution and the characteristic triplet, we can estimate the jump measure by a spectral approach. This idea was initiated by Belomestny and Reiß, (2006) and then studied further, see Reiß, (2013) for an overview. The observation scheme of the option prices was first studied by Cont and Tankov, 2004b as well as Belomestny and Reiß, (2006).

With the notable exception of Belomestny, (2010), who estimates the fractional order of a Lévy process, only linear functionals of the jump measure are considered. Instead, we solve the substantially more demanding problem of estimating the nonlinear generalized quantiles in this nonlinear inverse problem. The conditions we impose on the models are very weak. We allow the whole spectrum of Lévy processes, reaching from diffusions to pure jump processes with unbounded variation and the combination of both. The quantile estimators are very robust in the sense that they do not depend on the drift and volatility parameters, which may be surprising. In both above described observation schemes we derive convergence rates for the quantile estimators (Theorems 4 and 9). In view of the literature our rates appear to be minimax optimal. As side results convergence rates for density estimation and distribution function estimation are obtained which are novel due to the studied generality of Lévy processes.

The question of adaptive estimation methods for Lévy processes in the high-frequency and low-frequency regime has been only recently addressed by Comte and Genon-Catalot, (2011) and Kappus, (2014), respectively, who apply model selection procedures. In the exponential Lévy model we provide an adaptive method of Lepski-type that achieves the optimal rates (Theorem 10) with an additional -payment for adaptivity that appears to be unavoidable. Since the exponential Lévy model is related to the low-frequency regime let us compare our results to one by Kappus, (2014) who has estimated linear functionals of the Lévy density. Profiting from the regression structure, we can handle a broad class of processes while results in Kappus, (2014) are restricted to Lévy processes of bounded variation. The model selection approach leads to a finite sample oracle inequality where the constants, however, are not explicitly determined which might be problematic for applications. Although our error analysis is completely asymptotic, our data-driven method achieves very good results in finite sample situations, as illustrated with prices of options on the German DAX-index.

In the next Section the generalized quantiles are introduced and their applications are discussed. In addition the basic estimation idea is outlined. Discrete observations of the Lévy process and the option price model are considered in Sections 3 and 4, respectively. In the latter model we construct an adaptive version of the estimator in Section 5. Simulations and a real data study based on DAX-options are given in Section 6. All proofs are postponed to Section 7.

2 Generalized quantiles and estimation principle

Due to the Lévy–Itô decomposition, any Lévy process can be represented as the sum of a deterministic drift determined by a parameter , a Brownian motion with volatility and an independent jump component. The distribution of the jump sizes is described by the Lévy measure which may have a singularity at zero, but satisfies . The process is uniquely determined by this so-called characteristic triplet .

By definition , for any Borel set , is the expected number of jumps per unit time whose size belongs to . Taking into account the possible singularity of at zero, the generalized distribution function is defined by

| (1) |

Our aim is to estimate its inverse function which we call generalized quantile function. For a given level we introduce

Hence, (resp. ) is the largest value such that jumps larger than (resp. smaller than ) have a least intensity .

Especially the distribution of large jumps, corresponding to small values of , are conveniently described using generalized quantiles. Let us discuss a few possible applications. For Lévy processes with compound Poisson jump component, the quantiles of the Lévy measure, which then are a finite measures, have very similar properties as quantiles of probability distributions. The total jump intensity of negative and positive jumps is given by and , respectively, and the quantiles can be used as measures of location, scale and skewness of the jump distribution.

These properties extend to infinite measures, too. For instance, the Bowley skewness for probability measures directly generalizes to for quantifying symmetry between positive and negative jumps of a Lévy processes. Another remarkable property is illustrated in the following example:

Example 1.

A common construction of Lévy measures is the so-called exponential tilting where a Lévy measure is multiplied by an exponential factor, i.e., for . Supposing has a Lebesgue density which is bounded outside of a neighborhood of the origin and which converges polynomially fast to zero as , it is easy to see that the quantiles corresponding to grow like as . Ploting against , the parameter thus approximately shows up as inverse of the slope for large values of .

Therefore, estimators for the generalized quantiles are important descriptive statistics for the jump behavior of Lévy processes. But there are further applications: To construct and estimate Lévy copulas, the generalized quantiles are necessary, cf. (Cont and Tankov, 2004a, , Chap. 5) and Bücher et al., (2013), and in the context of modeling prices processes, they can be used to estimate the risk within the model. One of the most popular risk measures is the value-at-risk at some level which is given by the -quantile of the distribution of the loss of the asset. The generalized quantiles of are a closely related concept which takes only the influence of shocks into account. Following this idea, the quantiles may also be useful for dynamic quantile hedging in the spirit of Föllmer and Leukert, (1999).

Now, how to estimate these quantiles? Before we rigorously introduce the estimators and study their asymptotic properties in the following two sections let us outline the general estimation principle. We follow a similar strategy as Dattner et al., (2014) who study quantile estimation in the classical deconvolution model. Compared to deconvolution, the Lévy model is harder for two reasons. First, it is a nonlinear inverse problem such that we have to linearize the estimation error and the remainder needs extra care. Second, the underlying deconvolution problem is determined by the distribution of the process itself. Consequently, there is a strong interplay between the jump measure that we want to estimate and the underlying deconvolution operator.

Assuming , is given by the Lévy–Khintchine representation in Kolmogorov’s version:

| (2) |

Differentiating twice the characteristic exponent , we obtain the estimating equation

| (3) |

As starting point we need an estimator of the characteristic function of the marginal distribution of the Lévy process for some . Using discrete observations of the Lévy process, can be estimated by the empirical measure of the increments. In the financial model the characteristic function can be estimated via the pricing formula that links and the option prices. To estimate , we will then apply the following program:

- (i)

-

(ii)

A plug-in approach yields an estimator for the distribution function.

-

(iii)

The generalized -quantiles can be estimated by minimizing the distance between the value of distribution function estimator and .

The estimator for the jump density is similar to the estimators proposed in Nickl and Reiß, (2012) as well as Kappus, (2014). However, both articles are restricted to Lévy processes with bounded variation and thus use only the first derivative of . Focusing on settings that allow for parametric rates, the distribution function estimation have been considered by Nickl and Reiß, (2012) and Nickl et al., (2014) in the low and high-frequency regime, respectively.

3 Discrete observations of the process

We observe increments of the Lévy process at equidistant time points with observation distance :

The law of will be denoted by . Using the empirical characteristic function , we obtain an empirical version of from (3):

where we multiply with the indicator function to stabilize against large stochastic errors. We define the density estimator as

where is a band-limited kernel with bandwidth satisfying for some order

| (4) |

Note that depends neither on the unknown volatility nor on the drift parameter . The distribution function can be estimated via the left and the right tail integrals

| (5) |

Owing to , the estimator is always well defined.

Assuming absolute continuity of at with respect to the Lebesgue measure, the generalized quantiles and for a given level are determined by

If has finite mass on the negative or the positive halfline, the -quantiles only exist if or , respectively. On the other hand for processes with high jump activity, i.e., as , the bias of the distribution function estimator explodes as , cf. Proposition 14. Since is not known, it is thus reasonable to estimate for some threshold and any instead of the quantiles themselves in order to stabilize the estimation problem. For finite jump activity processes with regular jump densities at zero, the threshold value may converge slowly to zero as and we conclude that holds almost surely if and the estimators take the value for all .

Using , a minimum contrast estimation approach yields the quantile estimator

for threshold values which are either fixed or which logarithmically decay to zero. Note that we only consider the distribution function outside a neighborhood of the origin and thus our estimator does not depend on the diffusion component which corresponds to a Dirac measure at zero with mass .

Since is a point estimator, for any fixed , nonparametric convergence rates depend on the local smoothness of and it is natural to assume Hölder regularity. Before specifying the exact nonparametric classes of Lévy triplets that we will consider, let us introduce some notation. For an open set the space of all functions continuous on is denoted by . The set of all functions which are Hölder-regular with index on is given by

where denotes the smallest integer strictly smaller than . If not specified differently, with denotes the -norm on the whole real line with the usual notation for the supremum norm. The bounded variation norm of a function on an interval for is defined as

Define for the open set , regularity , number of moments and radius the class of Lévy triplets

For the error analysis we distinguish between infinitely divisible distributions with polynomially decaying characteristic functions and exponentially decaying characteristic functions. For and set

| (6) |

We will see that the class corresponds to mildly ill-posed estimation problems. As shown in Trabs, 2014b a polynomial decay of is, up to a mild regularity assumption, equivalent to beeing of bounded variation near the origin and, of course, . Hence, the conditions imposed in are quite natural. Moreover, they allow to apply the Fourier multiplier theorem in Trabs, 2014b . The estimation problem in the class is severely ill-posed leading to logarithmic convergence rates. Because the rates are so slow, we only need very mild assumptions in without any additional condition on the jump measure. This class especially contains all infinite variation processes, noting that Lévy processes with a diffusion component satisfy the decay condition on only for .

The convergence rates will be established in the -sense which corresponds to the loss function of confidence intervals. Since the results hold uniformly over the given classes of Lévy processes, we define the uniform stochastic Landau symbol over a parameter set : For random variables we write if

| (7) |

Since our estimation procedure relies on a plug-in approach using the density estimator , we start with its asymptotic behavior beeing of independent interest. As in the analysis of the quantile estimator in the deconvolution model by Dattner et al., (2014), the following proposition is the first building block for showing the rates of . We will need the result for the uniform loss.

Proposition 2.

Let and let the kernel satisfy (4) with order and let be a bounded, open set which is bounded away from zero. Then we have for

-

(i)

uniformly in for

-

(ii)

uniformly in for with

In the mildly ill-posed case the rates correspond to the deconvolution problem with an error distribution whose characteristic function decays with polynomial rate . It can easily be verified that the for the pointwise loss we have the same rates without the logarithm in (i). They coincide with the convergence rates for the pointwise loss by Kappus, (2014, Thm. 3.5), who has considered only finite variation Lévy processes. Kappus, (2012) have shown that these rates are minimax optimal. In the classical density estimation the logarithm is known to be unavoidable for the uniform loss. In comparison to the deconvolution model, the logarithmic rates in (ii) appear to be sharp, too.

The distribution function estimator was studied by Nickl et al., (2014) in a high-frequency regime. For low frequency observations a modification of was considered by Nickl and Reiß, (2012). In both articles a uniform central limit theorem has been established. To this end, assumptions have been imposed which ensure that the parametric rate can be attained. Therefore, it is of interest to derive convergence rates for in more general situations. We remark that the following result could be strengthened to the uniform loss on for any , cf. (48) below.

Proposition 3.

Let be an open set, and and . Suppose the kernel satisfies (4) with order . Let and . Then:

-

(i)

We obtain uniformly in with the bandwidth

-

(ii)

The choice , for any , yields uniformly in

As expected, the convergence rates for are faster than for density estimation because we gain one degree of smoothness. In particular, we achieve the parametric rate for a Lévy process with very slowly decaying characteristic function or for sufficiently small.

Following the standard M-estimation strategy, we use a Taylor expansion to analyze the estimation error of the quantile estimators. Using that for , we obtain

for some intermediate point between and and similarly for . By continuity of and the construction of the probability of the event converges to one, cf. (46). On this event the estimation error can therefore be represented as

| (8) |

for intermediate points . If the denominator does not explode, can be estimated with the same rate as . Since the convergence rates for the density estimator and for the distribution function estimator are already established, it remains to show consistency of the quantile estimator itself. To this end, a minimal global regularity of is required. Note that assuming a bounded density would be far to restrictive for Lévy measures.

We need to specify our nonparametric classes further such that the quantiles exist. Writing for if the antiderivatives and are in , we define for a given and with

| (9) | |||

| (10) | |||

The condition especially implies that the quantiles are unique. As expected from the representation (8), we obtain the same rates for quantile estimation as for distribution function estimation.

Theorem 4.

Let and and . Suppose the kernel satisfies (4) with order and with . Then we obtain for and :

-

(i)

The bandwidth yields uniformly in

-

(ii)

The choice , for any , yields uniformly in

Remark 5.

In the parametric regime., i.e., with , we could hope for more. In view of the central limit theorem by Nickl and Reiß, (2012) a more precise analysis of the main stochastic error term, defined in (28), may lead to a central limit theorem of the distribution function estimator . Since the our analysis of (8) reveals that

a central limit theorem for immediately follows. Note that optimality of the asymptotic variance by Nickl and Reiß, (2012) in the sense of semi-parametric efficiency is proved in Trabs, (2013). Using the -method, this lower bound can be extend to a lower bound for the asymptotic variance for the quantile estimation.

Remark 6.

For high-frequency data, that is for and , we obtain in always the parametric rate . In the bandwidth should be chosen instead such that our estimates in the proof of Theorem 4 yield the almost optimal rate provided that is large enough such that the bias condition is satisfied. With stronger assumptions the latter restriction can be circumvented and the rate can be improved. In fact, in Nickl et al., (2014) we show that the parametric rate can be obtained with this estimator under suitable conditions on .

4 Observation of option prices

Let us consider the exponential Lévy model for asset prices

| (11) |

with initial value , riskless interest rate and with the driving Lévy process whose characteristic triplet is . Since Lévy processes are a quite large and flexible class of stochastic processes, important stylized facts of financial data can be reproduced, see Cont and Tankov, 2004a for properties and examples of the exponential Lévy model. At the same time the well understood probabilistic structure of Lévy processes allows to construct procedures to fit the model to real data. The nonparametric calibration of this model was studied by Cont and Tankov, 2004b ; Belomestny and Reiß, (2006) as well as Trabs, 2014a . Söhl, (2014) have derived confidence sets. An empirical study of the calibration methods can be found in Söhl and Trabs, (2014).

By arbitrage arguments the price process of an asset should be a martingale implying for all . Assuming again , this is equivalent to the martingale condition

| (12) |

which we assume throughout this section. Since we want to estimate Lévy measure under the risk-neutral measure, the procedure is based on option prices. More precisely, we observe prices of vanilla options. Let us fix a maturity , measured in years, and define the negative log–moneyness as a logarithmic transform of the strike prices . In terms of , call and put prices in model (11) are given by and , respectively. The prices can be summarized in the option function

| (13) |

We observe at a finite number of (transformed) strike prices , for , corrupted by noise

| (14) |

where are i.i.d. centered random variables with and with local noise levels . The observation errors are due to the bid–ask spread and other market frictions. By interpolating the observations using B-splines, we construct an empirical version of the option function as in Belomestny and Reiß, (2006). From the theoretical perspective linear splines are sufficient, but in applications B-splines of higher degrees may lead to better results, cf. Söhl and Trabs, (2014) for details. Since the function is related to the characteristic function of via the pricing formula, cf. Carr and Madan, (1999),

| (15) |

we obtain an estimator of given by

| (16) |

Using , we obtain a quantile estimator as described in Section 2:

- (i)

- (ii)

-

(iii)

For the quantile estimators are defined as the minimum contrast estimators

with threshold value .

These estimators are well defined on the event whose probability increases if concentrates around the true . In an idealized model Söhl, (2010) shows . Note that is different from the finite activity estimator by Belomestny and Reiß, (2006). The k-function estimator from Trabs, 2014a in the self-decomposable model relies on a similar idea but using only the first derivative of .

Since we want to concentrate on the main aspects in the error analysis and to avoid technicalities, we will work in the idealized Gaussian white noise model which was considered by Söhl, (2014) as well. Assume that the noise levels of the observations (14) are given by the values , , of some function . The observed strike prices are assumed to be the quantiles , , of a distribution with distribution function and density . Incorporating the observation errors as well as their distribution, we define the general noise level

| (18) |

For standard normal Brown and Low, (1996) have shown asymptotic equivalence in the sense of Le Cam of the nonparametric regression model (14) and the Gaussian white noise model

with a two-sided Brownian motion for on a possibly growing bounded interval. The equivalence to more general error distributions follows from Grama and Nussbaum, (2002). More details on this equivalence can be found in Söhl, (2014) and Trabs, 2014a (, Supplement).

is an empirical version of the antiderivative of . In that sense we define and analogously for and . Owing to (16), the estimation error of the is given by the Gaussian process

While in the previous section the concentration of the estimator around was obtained by the i.i.d. structure of the increments, we use here the concentration of Gaussian measures. Applying Dudley’s entropy theorem, we obtain the following path property of . This lemma is in line with the results by Söhl, (2010) and Proposition 1 in Söhl, (2014).

Lemma 7.

Grant for some . Then is twice -differentiable with derivatives

| (19) | ||||

Moreover, and have versions that are almost surely continuous and satisfy for any

In the following we may use these almost surely continuous and bounded versions. Let us first state a result on the uniform loss for the density estimator .

Proposition 8.

The convergence rates for the pointwise loss are the same without the logarithmic factor in (i). They coincide with the rates by Belomestny and Reiß, (2006) who have considered only the extreme cases: If and is a finite measure, the pointwise risk converges with rate , and if , we obtain the rate . The estimator for the k-function by Trabs, 2014a achieves the same rate as the corresponding pointwise result in Proposition 8(i). Since in the two afore mentioned papers lower bounds have been proved and the logarithm is unavoidable for uniform loss, the above rates appear to be minimax optimal.

Recalling the function classes from (9), we obtain the following convergence rates for the quantile estimators

Theorem 9.

Compared to Theorem 4, the rates in (i) are always slower. In particular, the parametric rate can never be achieved. Heuristically, this is because we estimate a derived parameter of the state price density, which is basically the second derivative of the observed option function . In the Fourier domain we see in the pricing formula (15) that decays two polynomial degrees faster than such that the ill-posedness of the statistical problem is larger. In the severely ill-posed case (ii) the rate is the same in both observation schemes since the rates are only logarithmically slow. The moment assumption is weakened to second moments, which are necessary for the identification identity (3). Instead the existence of fourth moments is implicitly imposed on the error distribution in the regression scheme. Although the theorem is stated for , the bounded variation of is not needed here and could be dropped.

5 Data-driven choice of the bandwidth

Of course the optimal bandwidth is not known to the practitioner. To provide an adaptive method, we apply the approach by Lepski, (1990) by considering a family of quantile estimators for an appropriate set of bandwidths . Following the construction in Dattner et al., (2014), we define for a constant and a sequence satisfying

To ensure that the density estimator is consistent for any , we choose the minimal bandwidth via

and define

To choose the bandwidth from which mimics the oracle bandwidth in Theorem 9, we have to estimate the standard deviation of the stochastic error. This problem is similar to the one considered by Söhl, (2014) who has determined the asymptotic distribution of the finite activity estimators by Belomestny and Reiß, (2006) and has derived confidence sets. In fact, we will only estimate an upper bound of the standard deviation. This bound should be as sharp as possible to allow for a good finite sample behavior. The main problem is that any upper bound depends on unknown quantities which have to be estimated as well with a sufficiently fast convergence rate. Our bound will not depend on any asymptotic or function class specific constants. The stochastic error is dominated by its linearization and thus we define, cf. Lemma 22,

| (20) |

with auxiliary functions, for ,

Note that are monotone decreasing in . The magnitude of the stochastic error of can then be estimated by

| (21) |

for any small . Defining

the adaptive estimator is defined as

Theorem 10.

In the mildly ill-posed case (i) the adaptive method looses a -factor compared to the oracle choice in Theorem 9. Note that our loss function is bounded thus we loose only a -factor instead of the -factor, which would appear, for instance, for the mean squared error. In view of Spokoiny, (1996) this payment for adaptivity is unavoidable. In the severely ill-posed case (ii) the rates are already logarithmically slow such that the adaptive method causes no additional loss.

6 Simulations and real data

We will illustrate the quantile estimation method in simulations from the CMGY model introduced by Carr et al., (2002). The driving Lévy process of the asset is tempered stable and may have a diffusion component. For parameters and the Lévy measure in the CMGY model is given by the Lebesgue density

With a fifth parameter the characteristic triplet of the underlying Lévy process is where the drift is determined by the martingale condition (12). For the simulations we set and which appears to be a realistic choice in view of the empirical results by Carr et al., (2002). The riskless interest rate is chosen as . The design points are constructed as -quantiles of a distribution. We simulate option prices with time to maturity corresponding to three months. According to a rule of thumb by Cont and Tankov, 2004a (cf. , p. 439), the local noise levels are chosen as 1% of the observed prices which is later assumed for the real data, too.

| RMSE | ||||||

|---|---|---|---|---|---|---|

| oracle | adaptive | oracle | adaptive | |||

| 0.5 | 0.1778 | 0.1241 | 0.346 | 4.806 | 0.444 | 2.246 |

| 1.0 | 0.1201 | 0.0868 | 0.297 | 1.396 | 0.361 | 0.741 |

| 1.5 | 0.0929 | 0.0665 | 0.185 | 0.890 | 0.434 | 0.869 |

| 2.0 | 0.0726 | 0.0563 | 0.275 | 0.867 | 0.314 | 0.670 |

| 2.5 | 0.0624 | 0.0461 | 0.233 | 0.652 | 0.424 | 0.694 |

In order to apply the estimation procedure, we have to choose some parameters. The truncation value is set to . To construct the bandwidth set , we take . To compute , we need the noise function from (18) which depends on the unknown density of the distribution of the strikes. It can be estimated from the observation points using some standard density estimation method. As in Söhl and Trabs, (2014) we will apply a triangular kernel estimator, where the bandwidth is chosen by Silverman’s rule of thumb.

To assess the performance of the estimation procedure, we compare the adaptive choice of the bandwidth to the oracle bandwidth, meaning that is chosen such that the empirical root mean squared error (RMSE) is minimized. Our simulation results are summarized in Table 1 for . Although the RMSE of the adaptive method is larger than the oracle choice, the method achieves reasonable estimation errors. Note that the sample size is relatively small. For the RMSE is about 2.7% of the true quantile for and 1.8% for . For larger values of the RMSE decays to an order of 1% of the true quantiles. The reason is that small values of correspond to rare large jumps such that the jump density is small. Consequently, the estimation error (8) is large. Since the stochastic estimation error has to be estimated by from (21), this effect is more severe for the Lepski method.

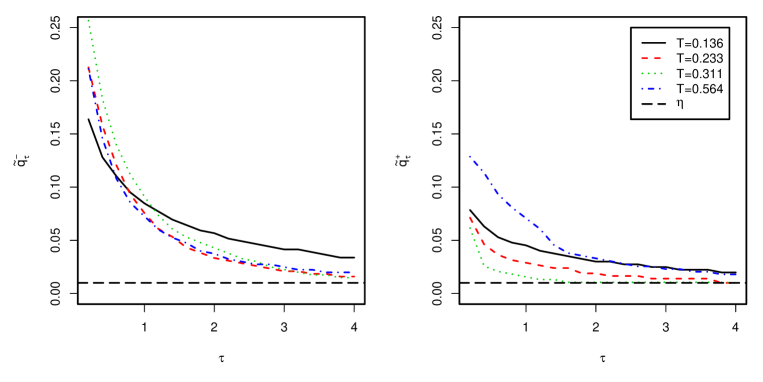

Let us finally apply the estimation method to prices of DAX options from May 29, 2008. This data set333provided by the SFB 649 “Economic Risk” has already been studied by Söhl and Trabs, (2014). Figure 1 shows the estimated quantiles for four different maturities between two and seven months and for . Due to this finer grid, the threshold value is set to . As postulated by the stylized facts on financial data, negative jumps have a higher activity. Roughly, the intensity of small jumps is larger for short maturities while the tails are more heavy for longer maturities.

7 Proofs

7.1 Error analysis for Section 3

To simplify the notation we will frequently use the definition . Note that the indicator function in the definition of equals one on with probability converging to one. This follows exactly from Lemma 5.1 by Dattner et al., (2014) and the bandwidth choices which we will consider.

7.1.1 Drift and remainder

All estimators are constructed based on the estimator of from (3). In particular, and only depend on the observations via . As shown by Nickl et al., (2014, Lem. 10) the drift has no effect on the estimators:

Lemma 11.

Let for Then are distributed according to an infinitely divisible distribution with characteristic triplet . Denoting the estimator based on and by and , respectively, it holds for all

Using

| (22) |

the estimation error can be linearized similarly to Proposition 21 in Nickl et al., (2014).

Lemma 12.

Let for

some . For satisfying

as , it holds

7.1.2 Convergence rates for distribution function estimation

Because it is a bit more difficult to derive the convergence rates for the distribution function estimator than for the density estimator, we study this problem first. The corresponding results for can the be proved analogously.

We decompose the estimation error of the distribution function estimator into

| (25) |

where is the deterministic error term, is the stochastic error term and is the error due to the unknown volatility . The error term is negligible:

Proof.

We estimate

For the bias we apply the following:

Proposition 14.

Suppose and let be an open set. If admits a Lebesgue density on in for some and if the kernel satisfies (4) with order , then

Proof.

Without loss of generality let Using Fubini’s theorem, we rewrite

| (26) |

Denoting integration by parts yields

From this representation we see for some sufficiently small that owing to and . The corresponding Hölder norm of the latter is of order . With a standard Taylor expansion argument and applying the order of the kernel, the approximation error is of the order by (26). ∎

Lemma 12 motivates the following definition of the linearized stochastic error term

| (27) |

Using (22) and defining the regularized Fourier multiplier

we decompose the linearized stochastic error further into

| (28) |

In the following, we will refer to as the main stochastic error term.

Proposition 15.

Remark 16.

Note that

Proof.

Due to , we obtain . Using Plancherel’s identity, we estimate for

Due to , we have, moreover,

| (29) |

Fubini’s theorem and Jensen’s inequality yield

| (30) |

To deal with , we note that the assumptions and imply . Moreover, and by Lemma 11 we can assume such that and . Therefore, we estimate (30) with use of the Cauchy–Schwarz inequality

| (31) |

which yields the assertion for .

Now we consider the case . The exponential decay of , the properties of , and yield

We conclude the claimed estimate for in by plugging these estimates into (30). Similarly, we estimate

For the main stochastic error term in the mildly ill-posed case we will need the following concentration result:

Proposition 17.

Let be an open set, and and let the kernel satisfy (4) with . Then there is some such that for any and

Proof.

We represent as sum of i.i.d. random variables via

Applying Plancherel’s identity, can be rewritten as

To estimate , we use to decompose into a singular component and a continuous component satisfying for

This allows to decompose

| (32) |

To estimate in (32), we apply the Fourier multiplier Theorem 5 in Trabs, 2014b to see that

for any . Consequently, because has finite fourth moments due to .

It remains to bound from (32). Using again by Lemma 11, we infer from that

| (33) |

and thus has a bounded density satisfying . Together with the Cauchy–Schwarz inequality and Plancherel’s identity we obtain

| (34) |

The derivatives of the regularized Fourier multiplier are given by

| (35) | ||||

| (36) |

To bound the -norms in (34), we use the properties of , the decay assumption on and to obtain

| (37) |

Therefore, which implies

| (38) |

Using (35), (36), , and , we deterministically bound by

The term corresponding to the singular part in the previous bound can be estimated by

For the continuous part we apply the Fourier multiplier theorem as above to see that

for any . Therefore,

| (39) |

Using (38) and (39), Bernstein’s inequality yields for some constant the claimed concentration result. ∎

Combining the previous results, we obtain minimax convergence rates for estimating the (generalized) distribution function of the jump measure.

Proof of Proposition 3.

In the following, is fixed and thus omitted in the constants. Using the error decomposition (25), Lemma 13, Proposition 14, we obtain

Using , Plancherel’s identity and Lemma 12 yield for the stochastic error from (25) and the linearized stochastic error term defined in (27)

| (40) |

provided that . The latter condition is satisfied for the choices in both cases.

Let . We conclude from (40), where is uniformly bounded and decays polynomially, and Propositions 15 and 17 for

Therefore, we obtain the rate by plugging in and similarly for .

Let us consider the case . Owing to and the exponential decay of , we obtain from (40) and Proposition 15 that

Therefore, plugging in , yields

∎

7.1.3 Uniform loss for density estimation

Applying a similar decomposition as in (25) and the linearization Lemma 12, we obtain

| (41) | ||||

for some remainder which is of order

| (42) | ||||

We will need the following concentration result for the main stochastic error term of the density estimation problem

| (43) |

where we recall . We will prove it analogously to Proposition 17.

Lemma 18.

Let and and let the kernel satisfy (4) for . If , then there is some constant , depending only on , such that for any and any

Proof.

We apply Bernstein’s inequality to the sum of the independent and centered random variables

can be estimated similarly to (34). We obtain by (33), the Cauchy–Schwarz inequality, Plancherel’s identity, (35) and (36) that

Moreover, admits the deterministic bound

Therefore, Bernstein’s inequality yields for a constant and any

Choosing for , we conclude

Proposition 2 is an immediate consequence of the following result.

Proposition 19.

Let , let the kernel satisfy (4) with order and let be a bounded, open set which is bounded away from zero. Then we have

-

(i)

uniformly in , if ,

-

(ii)

uniformly in

Proof.

We start with the error decomposition (41). By standard approximation arguments the deterministic error satisfies if for an open set , and if the kernel satisfies (4) with order . Moreover, the assumptions and imply which yields

Since is bounded away from zero, the previous display gives a uniform bound on . Using the main stochastic error term from (43), the linearized stochastic error term from (41) can be decomposed similarly to (28) into

| (44) |

To derive the appropriate bounds for and , we will distinguish again between the mildly and the severely ill-posed case.

We start with the severely ill-posed case Using Fubini’s theorem and the properties of as well as and (29), we obtain

The remainder (42) is of smaller order

Now let us consider , where we have

To bound , we note for the second and the third term in (44) that similarly to (31) with the Cauchy–Schwarz inequality and Fubini’s theorem

It remains to estimate the main stochastic term . Since is bounded, we find a finite number of points such that and . The inequalities by Young and by Cauchy–Schwarz together with yield

Together with Markov’s inequality and Lemma 18, defining this yields for sufficiently large

which converges to zero as if is chosen sufficiently large. ∎

7.1.4 Proof of Theorem 4

In view of the error representation (8), the missing ingredient to prove Theorem 4 is consistency of . We prove it similarly to Dattner et al., (2014), but since has no bounded density and we minimize on an unbounded interval the lemma is more involved.

Lemma 20.

Let and let with . Suppose the kernel satisfies (4) with order . Then we have

-

(i)

for any bandwidth satisfying and

-

(ii)

for any bandwidth satisfying and

Proof.

We adopt the general strategy of the proof of Theorem 5.7 by van der Vaart, (1998) in the classical M-estimation setting. Without loss of generality, we only consider .

Step 1: By the Hölder regularity we have for . Without loss of generality we can assume , otherwise consider . Using and monotonicity of , we obtain the uniqueness condition

| (45) |

Step 2: We construct an event with such that

| (46) |

Using , monotonicity of and (45), we conclude for

Proposition 3 implies that

| (47) |

We conclude on that . Since admits a derivative, namely , it is continuous and thus there is an intermediate point such that . Since minimizes on the interval and for and sufficiently small, we obtain (46).

Step 3: We infer from Steps 1 and 2

| (48) |

Hence, it remains to show uniform consistency of . Applying the error decomposition (25) and the estimates in Lemma 13 and Proposition 14 we obtain

According to Lemma 12 and Proposition 15, the stochastic error term can be decomposed into where is of the order claimed in Proposition 15. For the main stochastic error term is uniformly bounded as well. For the case it remains to apply Proposition 17 on an appropriate grid. For we define a grid with . Set for . Then

Noting that and , increments of can be estimated using Plancherel’s identity and Fubini’s theorem

Choosing , Markov’s inequality and Proposition 17 yield for sufficiently large and some constant

owing to . ∎

7.2 Proofs for Section 4

To prove Lemma 7, we apply some entropy arguments. To fix the notation, we define for any (pseudo-)metric on the covering number as the smallest number of -balls with radius which is necessary to cover a subset . For the entropy integral is defined as

which is finite for any if grows polynomially in .

Proof of Lemma 7.

Itô’s isometry yields

| (49) |

and similarly for and as defined in (19). From Itô’s isometry and dominated convergence we conclude that are the first and second order -derivatives of . The intrinsic covariance metric of the Gaussian process is given by

Using , the entropy integrals can be bounded exactly as in the proof of Proposition 1 by Söhl, (2014) and are of order Dudley’s theorem (e.g. Massart,, 2007, Prop. 3.18) yields then . ∎

7.2.1 Convergence rates

Since the proof strategy is the same for the observation schemes in Sections 3 and 4, we will concentrate here on the differences. The estimation error can be decomposed into where and are given in (25) and only the stochastic error

has a different probabilistic structure. We can apply Lemma 13 and Proposition 14 to estimate and . For the sake of brevity, we will frequently write

This equality is justified in -sense, but should merely be understood as notational convention. Linearizing the stochastic error term, we define analogously to (28)

Since the are almost surely bounded and has compact support, is almost surely well defined. The remainder will be bounded on the event

| (50) |

The order of the remainder in the next lemma corresponds exactly to Lemma 12 taking the bound from Lemma 7 into account.

Lemma 21.

If for some , then for any sequence satisfying as it holds and uniformly for all Lévy triplets

Proof.

follows immediately from Theorem 1 by Kappus and Reiß, (2010), cf. Lemma 5.1 by Dattner et al., (2014). To bound , we apply the argument by Neumann, (1997) and Lemma 7. We obtain on

| (51) | ||||

A straight forward computation shows on

| (52) |

where is the sum of all second order terms. Using (51), formulas (22) as well as Lemma 7, we obtain the claimed order of . ∎

Let us study the linearized stochastic error term. To apply the Lepski method later we need a sharp bound on the variance of . With the auxiliary functions, ,

we define

| (53) |

Lemma 22.

If , then is centered normal. Supposing additionally , it holds

Proof.

Since the are almost surely bounded, we can apply Plancherel’s identity which yields

By continuity and boundedness of the integral in can be approximated with Riemann sums. We conclude first that is normally distributed, cf. Section 6.2 in Söhl, (2014), and second that we can exchange the deterministic integral and the stochastic integral due to the construction of the Wiener integral as -limit. Together with Itô’s isometry and Plancherel’s identity we obtain

The formulas (22) and yield the claimed asymptotic bound. ∎

Now, we can conclude convergence rates for the distribution function estimator .

Proposition 23.

Suppose and for some . Let be an open set and Let the kernel satisfy (4) with order .

-

(i)

If , then for .

-

(ii)

If , then for .

Proof.

As in the proof of Proposition 3 we have

| (54) |

Lemmas 21 and 22 yield for the stochastic error term

In situation (i) we use integrability of to obtain

| (55) |

Therefore, the optimal bandwidth yields the claimed rate.

For exponentially decaying characteristic functions in case (ii) we infer by

| (56) |

leading to the rate optimal choice . ∎

Proposition 8 on the density estimator is an immediate consequence from the following proposition.

Proposition 24.

Suppose and for some . Let the kernel satisfy (4) with order , let be a bounded, open set which is bounded away from zero and let . Then we have

-

(i)

for any satisfying for some we have uniformly in

-

(ii)

for any satisfying for some we have uniformly in

Proof.

As in the proof of Proposition 19 we deduce from Lemma 21 that

with the linearized stochastic error term

We estimate

Since all three terms can be estimated analogously, we limit ourselves on which has the largest variance. We estimate uniformly in with use of Plancherel’s identity, Fubini’s theorem and Itô’s isometry

| (57) |

Analogously, we can estimate the distance in the intrinsic norm for any

and thus the covering number is of the order Consequently, the entropy integral can be bounded by

| (58) |

Using this entropy bound, Dudley’s theorem (e.g. Massart,, 2007, Prop. 3.18) yields

Now we can plug in the different assumptions on the decay of (in particular is smaller than for sufficiently small). ∎

To finally prove Theorem 9, we can argue as for Theorem 4. The only ingredient which remains be shown is uniform convergence for the rate optimal bandwidth . Since the remainder can be bounded uniformly in using Lemma 21, it suffices to show:

Lemma 25.

If and for some , then it holds uniformly for all

7.2.2 Adaptive method

With the previous results at hand the proof of Theorem 10 is quite similar to the one of Theorem 3.2 by Dattner et al., (2014) and thus we omit the details. In particular, the bandwidth set fulfills analogous properties as their construction, cf. their Lemma 3.1. Due to for the minimal bandwidth and with from (50), it suffices to bound all terms on the complement . Using (8), (46) and (54), the estimation error of can be bounded by

| (59) |

with probability converging to one and with a deterministic constant involving the bias and the error due to . We can verify with use of Proposition 24, (48) and Lemmas 21 and 25 for ,

| (60) |

To conclude that from (21) is an appropriate upper bound for in (59), we have to control . We again decompose it into linearization and remainder. Since is centered and normally distributed with variance bounded by from (7.2.1), the Gaussian concentration and yield for any

For the remainder, one can show, using (52) pointwise, and thus we conclude for any

provided that . Noting that the order of is the same as the order of the stochastic error of , this condition is satisfied for all by construction. In the next step, we show that is reasonably estimated by from (20).

Lemma 26.

In the situation of Theorem 10 we have for any sequence satisfying that

Proof.

Without loss of generality we only consider . The triangle inequality yields

Hence, it suffices to show

| (61) |

Let us start with where we have

Using for and , the first integral can be estimated by

References

- Aït-Sahalia and Jacod, (2012) Aït-Sahalia, Y. and Jacod, J. (2012). Analyzing the spectrum of asset returns: Jump and volatility components in high frequency data. J. Econ. Lit., 50(4):1007–50.

- Belomestny, (2010) Belomestny, D. (2010). Spectral estimation of the fractional order of a Lévy process. Ann. Statist., 38(1):317–351.

- Belomestny and Reiß, (2006) Belomestny, D. and Reiß, M. (2006). Spectral calibration of exponential Lévy models. Finance Stoch., 10(4):449–474.

- Brown and Low, (1996) Brown, L. D. and Low, M. G. (1996). Asymptotic equivalence of nonparametric regression and white noise. Ann. Statist., 24(6):2384–2398.

- Bücher et al., (2013) Bücher, A., Vetter, M., et al. (2013). Nonparametric inference on lévy measures and copulas. Ann. Statist., 41(3):1485–1515.

- Carr et al., (2002) Carr, P., Geman, H., Madan, D. B., and Yor, M. (2002). The fine structure of asset returns: An empirical investigation. J. Bus., 75(2):305–332.

- Carr and Madan, (1999) Carr, P. and Madan, D. B. (1999). Option valuation using the fast Fourier transform. J. Comput. Finance, 2:61–73.

- Comte and Genon-Catalot, (2011) Comte, F. and Genon-Catalot, V. (2011). Estimation for Lévy processes from high frequency data within a long time interval. Ann. Statist., 39(2):803–837.

- (9) Cont, R. and Tankov, P. (2004a). Financial modelling with jump processes. Chapman & Hall / CRC Press, Boca Raton, FL.

- (10) Cont, R. and Tankov, P. (2004b). Non-parametric calibration of jump-diffusion option pricing models. J. Comput. Finance, 7(3):1–49.

- Dattner et al., (2014) Dattner, I., Reiß, M., and Trabs, M. (2014). Adaptive estimation of quantiles in deconvolution with unknown error distribution. Bernoulli, to appear.

- Föllmer and Leukert, (1999) Föllmer, H. and Leukert, P. (1999). Quantile hedging. Finance Stoch., 3(3):251–273.

- Grama and Nussbaum, (2002) Grama, I. and Nussbaum, M. (2002). Asymptotic equivalence for nonparametric regression. Math. Methods Statist., 11(1):1–36.

- Kappus, (2012) Kappus, J. (2012). Nonparametric adaptive estimation for discretely observed Lévy processes. PhD thesis, Humboldt-Universität zu Berlin, Mathematisch-Naturwissenschaftliche Fakultät II.

- Kappus, (2014) Kappus, J. (2014). Adaptive nonparametric estimation for Lévy processes observed at low frequency. Stochastic Process. Appl., 124(1):730 – 758.

- Kappus and Reiß, (2010) Kappus, J. and Reiß, M. (2010). Estimation of the characteristics of a Lévy process observed at arbitrary frequency. Stat. Neerl., 64(3):314–328.

- Lepski, (1990) Lepski, O. V. (1990). A problem of adaptive estimation in Gaussian white noise. Teor. Veroyatnost. i Primenen., 35(3):459–470.

- Massart, (2007) Massart, P. (2007). Concentration inequalities and model selection, volume 1896 of Lecture Notes in Mathematics. Springer, Berlin.

- Neumann, (1997) Neumann, M. H. (1997). On the effect of estimating the error density in nonparametric deconvolution. J. Nonparametr. Stat., 7(4):307–330.

- Neumann and Reiß, (2009) Neumann, M. H. and Reiß, M. (2009). Nonparametric estimation for Lévy processes from low-frequency observations. Bernoulli, 15(1):223–248.

- Nickl and Reiß, (2012) Nickl, R. and Reiß, M. (2012). A Donsker theorem for Lévy measures. J. Funct. Anal., 263(10):3306–3332.

- Nickl et al., (2014) Nickl, R., Söhl, J., Reiß, M., and Trabs, M. (2014). High-frequency Donsker theorems for Lévy measures. Probab. Theory Related Fields, to appear. arXiv:1310.2523.

- Reiß, (2013) Reiß, M. (2013). Testing the characteristics of a Lévy process. Stochastic Process. Appl., 123(7):2808–2828. Special Issue International Year of Statistics.

- Söhl, (2010) Söhl, J. (2010). Polar sets for anisotropic gaussian random fields. Statist. Probab. Lett., 80(9-10):840 – 847.

- Söhl, (2014) Söhl, J. (2014). Confidence sets in nonparametric calibration of exponential Lévy models. Finance Stoch., 18(3):617–649.

- Söhl and Trabs, (2014) Söhl, J. and Trabs, M. (2014). Option calibration of exponential Lévy models: Confidence intervals and empirical results. J. Comput. Finance, To appear. arXiv 1202.5983.

- Spokoiny, (1996) Spokoiny, V. G. (1996). Adaptive hypothesis testing using wavelets. Ann. Statist., 24(6):2477–2498.

- Trabs, (2013) Trabs, M. (2013). Information bounds for inverse problems with application to deconvolution and Lévy models. Annales de l’Institut Henri Poincaré, to appear. arXiv 1307.6610.

- (29) Trabs, M. (2014a). Calibration of self-decomposable Lévy models. Bernoulli, 20(1):109–140.

- (30) Trabs, M. (2014b). On infinitely divisible distributions with polynomially decaying characteristic functions. Statist. Probab. Lett., 94:56–62.

- van der Vaart, (1998) van der Vaart, A. W. (1998). Asymptotic Statistics. Cambridge University Press, Cambridge.