On Multiscale Methods in Petrov-Galerkin formulation

***D. Elfverson and P. Henning were supported by The Göran Gustafsson Foundation and The Swedish Research Council.

Daniel Elfverson111Department of Information Technology, Uppsala University, Box 337, SE-751 05 Uppsala, Sweden,

Victor Ginting222Department of Mathematics, University of Wyoming, Laramie, Wyoming 82071, USA,

Patrick Henning333Section de Mathématiques, École polytechnique fédérale de Lausanne, 1015 Lausanne, Switzerland

Abstract

In this work we investigate the advantages of multiscale methods in Petrov-Galerkin (PG) formulation in a general framework. The framework is based on a localized orthogonal decomposition of a high dimensional solution space into a low dimensional multiscale space with good approximation properties and a high dimensional remainder space, which only contains negligible fine scale information. The multiscale space can then be used to obtain accurate Galerkin approximations. As a model problem we consider the Poisson equation. We prove that a Petrov-Galerkin formulation does not suffer from a significant loss of accuracy, and still preserve the convergence order of the original multiscale method. We also prove inf-sup stability of a PG Continuous and a Discontinuous Galerkin Finite Element multiscale method. Furthermore, we demonstrate that the Petrov-Galerkin method can decrease the computational complexity significantly, allowing for more efficient solution algorithms. As another application of the framework, we show how the Petrov-Galerkin framework can be used to construct a locally mass conservative solver for two-phase flow simulation that employs the Buckley-Leverett equation. To achieve this, we couple a PG Discontinuous Galerkin Finite Element method with an upwind scheme for a hyperbolic conservation law.

Keywords

finite element, multiscale method, numerical homogenization, Petrov-Galerkin method, conservation law, Buckley-Leverett equation

1 Introduction

In this contribution we consider linear elliptic problems with a heterogenous and highly variable diffusion coefficient as arisen often in hydrology or in material sciences. In the following, we are looking for which solves

in a weak sense. Here, we denote

-

(A1)

, , a bounded Lipschitz domain with a piecewise polygonal boundary,

-

(A2)

a source term, and

-

(A3)

a symmetric matrix-valued function with uniform spectral bounds ,

(1.1) We call the ratio the contrast of .

Under assumptions (A1)-(A3) and by the Lax-Milgram theorem, there exists a unique weak solution to

| (1.2) |

where

The problematic term in the equation is the diffusion matrix , which is known to exhibit very fast variations on a very fine scale (i.e. it has a multiscale character). These variations can be highly heterogenous and unstructured, which is why it is often necessary to resolve them globally by an underlying computational grid that matches the said heterogeneity. Using standard finite element methods, this results in high dimensional solution spaces and hence an enormous computational demand, which often cannot be handled even by today’s computing technology. Consequently, there is a need for alternative methods, so called multiscale methods, which can either operate below linear computational complexity by using local representative elements (cf. [1, 2, 11, 18, 19, 24, 37]) or which can split the original problem into very localized subproblems that cover but that can be solved cheaply and independent from each other (cf. [5, 8, 12, 13, 17, 26, 39, 28, 29, 32, 34, 38]).

In this paper, we focus on a rather recent approach called Localized Orthogonal Decomposition (LOD) that was introduced by Målqvist and Peterseim [36] and further generalized in [25, 20].

We consider a coarse space , which is low-dimensional but possibly inadequate for finding a reliable Galerkin approximation to the multiscale solution of problem (1.2). The idea of the method is to start from this coarse space and to update the corresponding set of basis functions step-by-step to improve the approximation properties of the space. In a summarized form, this can be described in four steps: 1) define a (quasi) interpolation operator from onto , 2) information in the kernel of the interpolation operator is considered to be negligible (having a small -norm), 3) hence define the space of negligible information by the kernel of this interpolation, i.e. kern, and 4) find the orthogonal complement of with respect to a scalar product , where describes a discretization of the problem to solve. In many cases, it can be shown, that this (low dimensional) orthogonal complement space has very accurate approximation properties with respect to the exact solution. Typically, the computation of the orthogonal decomposition is localized to small patches in order to reduce the computational complexity.

So far, the concept of the LOD has been successfully applied to nonlinear elliptic problems [21], eigenvalue problems [35] and the nonlinear Schrödinger equation [22]. Furthermore, it was combined with a discontinuous Galerkin method [14, 15] and extended to the setting of partition of unity methods [23].

In this work, we are concerned with analyzing the LOD framework in Petrov-Galerkin formulation, i.e. for the case that the discrete trial and test spaces are not identical. We show that an LOD method in Petrov-Galerkin formulations still preserves the convergence rates of the original formulation of the method. At the same time, the new method can exhibit significant advantages, such as decreased computational complexity and mass conservation properties. In this paper, we discuss these advantages in detail; we give examples for realizations and present numerical experiments. In particular, we apply the proposed framework to design a locally conservative multiscale solver for the simulation of two-phase flow models as governed by the Buckley-Leverett equation. We remark that employing Petrov-Galerkin variational frameworks in the construction and analysis of multiscale methods for solving elliptic problems in heterogeneous media has been investigated in the past, see for example [27] and [17].

The rest of the paper is organized as follows. Section 2 lays out the setting and notation for the formulation of the multiscale methods that includes the description of two-grid discretization and the Localized Orthogonal Decomposition (LOD). In Section 3, we present the multiscale methods based on the LOD framework, starting from the usual Galerkin variational equation and concentrating further on the Petrov-Galerkin variational equation that is the main contribution of the paper. We establish in this section that the Petrov-Galerkin LOD (PG-LOD) exhibits the same convergence behavior as the usual Galerkin LOD (G-LOD). Furthermore, we draw a contrast in the aspect of practical implementation that makes up a strong advantage of PG-LOD in relative comparison to G-LOD. The other advantage of the PG-LOD which cannot be achieved with G-LOD is the ability to produce a locally conservative flux field at the elemental level when discontinuous finite element is utilized. We also discuss in this section an application of the PG-LOD for solving the pressure equation in the simulation of two-phase flow models to demonstrate this particular advantage. Section 4 gives two sets of numerical experiment: one that confirms the theoretical finding and the other demonstrating the application of PG-LOD in the two-phase flow simulation. We present the proofs of the theoretical findings in Section 5.

2 Discretization

In this section we introduce notations that are required for the formulation of the multiscale methods.

2.1 Abstract two-grid discretization

We define two different meshes on . The first mesh is a ’coarse mesh’ and is denoted by , where denote the maximum diameter of all elements of . The second mesh is a ’fine mesh’ denoted by with representing the maximum diameter of all elements of . By ’fine’ we mean that any variation of the coefficient is resolved within this grid, leading to a high dimensional discrete space that is associated with this mesh. The mesh is assumed to be a (possibly non-uniform) refinement of . Furthermore, both grids are shape-regular and conforming partitions of and we assume that . For the subsequent methods to make sense, we also assume that each element of is at least twice uniformly refined to create . The set of all Lagrange points (vertices) of is denoted by , and the set of interior Lagrange points is denoted by , where is either or .

Now we consider an abstract discretization of the exact problem (1.2). For this purpose, we let denote a high dimensional discrete space in which we seek an approximation of . A simple example would be the classical Lagrange Finite Element space associated with . However, note that we do not assume that is a subspace of . In fact, later we give an example for which consists of non-continuous piecewise linear functions. Next, we assume that we are interested in solving a fine scale problem, that can be characterized by a scalar product on . Accordingly, a method on the coarse scale can be described by some , which we specify by assuming

-

(A4)

is a scalar product on where is either or .

This allows us to define the abstract reference problem stated below.

Definition 2.1 (Fine scale reference problem).

We call the fine scale reference solution if it solves

| (2.1) |

where ’describes the method’. It is implicitly assumed that problem (2.1) is of tremendous computational complexity and cannot be solved by available computing resources i n a convenient time.

A simple example of is . A more complex example is the that stems from a discontinuous Galerkin approximation, in which case is different from . The goal is to approximate problem (2.1) by a new problem that reaches a comparable accuracy but one that can be solved with a significantly lower computational demand.

2.2 Localized Orthogonal Decomposition

In this subsection, we introduce the notation that is required in the formulation of the multiscale method. In particular, we introduce an orthogonal decomposition of the high dimensional solution space into the orthogonal direct sum of a low dimensional space with good approximation properties and a high dimensional remainder space. For this purpose, we make the following abstract assumptions.

-

(A5)

denotes a norm on that is equivalent to the norm that is induced by , hence there exist generic constants such that

In the same way, denotes a norm on (equivalent to the norm induced by ). Furthermore, we let denote the constant with for all . Note that might degenerate for .

-

(A6)

The coarse space is a low dimensional subspace of that is associated with .

-

(A7)

Let be an -stable quasi-interpolation (or projection) operator with the properties

-

–

there exists a generic constant (only depending on the shape regularity of and ) such that for all and

-

–

the restriction of to is an isomorphism with -stable inverse, i.e. we have for and the exists a generic such that

-

–

Typically, -projections onto can be verified to fulfill assumption (A7). Similarly, can be a quasi-interpolation of the Clément-type that is related to the -projection. An example for this case is given in equation (3.5) below. Alternatively, can be also constructed from local -projections as it is done for the classical Clément interpolation. Nodal interpolations typically do not satisfy (A7).

Using the assumption that is an isomorphism (i.e. assumption (A7)), a splitting of the space is given by the direct sum

| (2.2) |

Observe that the ’remainder space’ contains all fine scale features of that cannot be expressed in the coarse space .

Next, consider the -orthogonal projection that fulfills:

| (2.3) |

Since , we have that induces the -orthogonal splitting

Note that is a low dimensional space in the sense that it has the same dimension as . As shown for several applications (cf. [35, 21, 22]) the space has very rich approximation properties in the -norm. However, it is very expensive to assemble , which is why it is practically necessary to localize the space (respectively localize the projection). This is done using admissible patches of the following type.

Definition 2.2 (Admissible patch).

For any coarse element , we say that the open and connected set is an admissible patch of , if and if it consists of elements from the fine grid, i.e.

It is now relevant to define the restriction of to an admissible patch by

A general localization strategy for the space can be described as follows (see [20] for a special case of this localization and [36] for a different localization strategy).

Definition 2.3 (Localization of the solution space).

Let the bilinear form be a localization of on in the sense that

| (2.4) |

where acts only on or a small environment of . Let furthermore be an admissible patch associated with . Let be a local correction operator that is defined as finding satisfying

| (2.5) |

where . The global corrector is given by

| (2.6) |

A (localized) generalized finite element space is defined as

The variational formulation (2.5) is called the corrector problem associated with . Solvability of each of these problems is guaranteed by the Lax-Milgram Theorem. By its nature, the system matrix corresponding to (2.5) is localized to the patch since the support of is in . Furthermore, each of (2.5) pertaining to is designed to be elementally independent and thus attributing to its immediate parallelizability. The corrector problems are solved in a preprocessing step and can be reused for different source terms and for different realization of the LOD methods. Since is a low dimensional space with locally supported basis functions, solving a problem in is rather inexpensive. Normally, the solutions of (2.5) decays exponentially to zero outside of . This is the reason why we can hope for good approximations even for small patches . Later, we quantify this decay by an abstract assumption (which is known to hold true for many relevant applications).

Remark 2.4.

3 Methods and properties

In this section, we state the LOD in Galerkin and in Petrov-Galerkin formulation along with their respective a priori error estimates and the inf-sup stability. In the last part of this section, we give two explicit examples and discuss the advantages of the Petrov-Galerkin formulation. Subsequently we use the notation to abbreviate , where is a constant that is independent of the mesh sizes and ; and which is independent of the possibly rapid oscillations in .

In order to state proper a priori error estimates, we describe the notion of ’patch size’ and how the size of affects the final approximation. All the stated theorems on the error estimates of the LOD methods are proved in Section 5.

Definition 3.1 (Patch size).

Let be fixed. We define patches that consist of the element and -layers of coarse element around it. For all , we define element patches in the coarse mesh by

| (3.1) | ||||

The above concept of patch sizes and patch shapes can be also generalized. See for instance [23] for a LOD that is purely based on partitions of unity. Using Definition 3.1, we make an abstract assumption on the decay of the local correctors for :

-

(A8)

Let be the optimal local corrector using that is defined according to (2.5) and let . Let and for all let as in Definition 3.1. Then there exists and a generic constant that can depend on the contrast, but not on , or the variations of such that for all ,

(3.2) where, denotes the global corrector given by (2.6) for .

Assumption (A8) quantifies the decay of local correctors, by stating that the solutions of the local corrector problems decay exponentially to zero outside of . This is central for all a priori error estimates. For continuous Galerkin methods, we can obtain the optimal order for the exponent in (3.2). This means, that the -term fully vanishes. However, depending on the localization strategy (i.e. how is computed) it is also possible that takes the value and that hence a pollution term of order arises (see [20, Remark 3.8] for a discussion). For discontinuous Galerkin methods, the optimal known order is . However, even for this case it is known that the -term is rapidly overtaken by the decay, leading purely to slightly larger patch sizes (see e.g. [36]).

3.1 Galerkin LOD

This method was originally proposed in [36]: find that satisfies

| (3.3) |

Theorem 3.2 (A priori error estimate for Galerkin LOD).

The term describes the coarse part (resulting from ) of and thus is numerically homogenized (the oscillations are averaged out). In this sense, we can say that is an -approximation of and an -approximation of , respectively. Furthermore, because converges with exponential order to zero, the error is typically dominated by the first term of order O. This was observed in various numerical experiments in different works, c.f. [20, 21, 36]. In particular, a specific choice leads to a O convergence for the total -error, see also [20, 21, 36].

3.2 Petrov-Galerkin LOD

In a straightforward manner, we can now state the LOD in Petrov-Galerkin formulation: find that satisfies

| (3.4) |

A unique solution of (3.4) is guaranteed by the inf-sup stability. In practice, inf-sup stability is clearly observable in numerical experiments (see Section 4). Analytically we can make the following observations.

Remark 3.3 (Quasi-orthogonality and inf-sup stability).

The inf-sup stability of the LOD in Petrov-Galerkin formulation is a natural property to expect, since we have quasi-orthogonality in of the spaces and . This can be verified by a simple computation. Let , let and let the optimal corrector as in assumption (A8), then

with generic constants and as in (A8). This means that converges exponentially in to zero, and it is identical to zero for all sufficiently large (because then ). Writing the PG-LOD bilinear form as

we see that it is only a small perturbation of the symmetric (coercive) G-LOD version, where the difference can be bounded by the quasi-orthogonality.

Even though the quasi-orthogonality suggests inf-sup stability, the given assumptions (A1)-(A8) do not seem to be sufficient for rigorously proving it. Here, it seems necessary to leave the abstract setting and to prove the inf-sup stability result for the various LOD realizations separately. For simplification, we therefore make the inf-sup stability to be an additional assumption (see (A9) below). Later we give an example how to prove this assumption for a certain realization of the method. We also note that the inf-sup stability can be always verified numerically (for a given ) by investigating the system matrix given by the entries

for where denotes the dimension of and where denotes a basis of . To check the inf-sup stability we must compute the eigenvalues of . If their real parts are all strictly positive, we have inf-sup stability and the inf-sup constant is identical to the smallest real part of an eigenvalue. Standard approaches for computing the eigenvalues of a non-symmetric matrix are the Arnoldi method, the Jacobi-Davidson method and the non-symmetric Lanczos algorithm (cf. [40] for a comprehensive overview). Since is moderately small, the cost for applying one of the methods are still feasible.

-

(A9)

We assume that the LOD in Petrov-Galerkin formulation is inf-sup stable in the following sense: there exists a sequence of constants and a generic limit (independent of , , or the oscillations of ) such that converges with exponential speed to , i.e. there exist constants (possibly depending on , but not on , or the oscillations of ) and a generic such that . Furthermore it holds for all sufficiently large and

for all and .

The following result states that the approximation quality of the LOD in Petrov-Galerkin formulation is of the same order as for the Galerkin LOD, up to a possible pollution term depending on , but which still converges exponentially to zero.

Theorem 3.4 (A priori error estimate for PG-LOD).

Assume (A1)-(A9). Given a positive , let for all the patch be defined as in (3.1) and large enough so that the inf-sup constant in (A9) fulfills for some and let be the unique solution of (3.4). Let be the fine scale reference solution governed by (2.1). Then, the following a priori error estimate holds true

where and are the generic constants from assumption (A8) and as in (A5).

3.3 Example 1: Continuous Galerkin Finite Element Method

The previous subsection showed that the Petrov-Galerkin formulation of the LOD does not suffer from a loss in accuracy with respect to the symmetric formulation. In this subsection, we give the specific example of the LOD for the Continuous Galerkin Finite Element Method. In particular, we discuss the advantage of the PG formulation over the symmetric formulation. Let us first introduce the specific setting and the corresponding argument about the validity of (A4)-(A9) on this setting.

In addition to the assumptions that we made on the shape regular partitions and in Section 2.1, we assume that and are either triangular or quadrilateral meshes. Accordingly, for we denote

and define if is a triangulation and if it is a quadrilation. The coarse space is defined in the same fashion and since is a refinement of , assumption (A6) is obviously fulfilled. For simplicity, we also assume that the coarse mesh is quasi-uniform (which is the typical choice in applications).

The bilinear form is defined by the standard energy scalar product on that belongs to the elliptic problem to solve, i.e.

Accordingly, we set for . Hence, assumptions (A5) and (A6) are fulfilled and the solution of (2.1) is nothing but the standard continuous Galerkin Finite Element solution on the fine grid .

Next, we specify in (A7). For this purpose, let be the nodal basis function associated with the coarse grid node , i.e., . Let be the weighted Clément-type quasi-interpolation operator as defined in [9, 10]:

| (3.5) |

First we note that it was shown in [36] that is an isomorphism (but not a projection, i.e. ). Hence, exists. This is one of the properties in (A7). The - and -stability of , as well as corresponding approximation properties, were proved in [9]. It only remains to check the -stability of . Unfortunately, this property is not trivial to fulfill. First, we note that it was shown in [35] that the mapping is nothing but the -projection (see also Remark 3.9 below). Consequently, the question of -stability of is equivalent to the question of -stability of the -projection. This result is well-established for quasi uniform grids (cf. [6]) as assumed at the beginning of this section. However it is still open for arbitrary refinements. The most recent results on this issue can be found in [7, 30, 16], where the desired -stability was shown for certain types of adaptively refined meshes. To avoid complicated mesh assumptions in this paper, we simply assume to be quasi-uniform. This is not very restrictive since adaptive refinements should typically take place on the fine mesh . Alternatively, in light of [7, 30, 16], we could also directly assume that the -projection on is -stable to allow more general coarse meshes.

It remains to specify , which we define by

Let us for simplicity denote . The decay assumption (A8) was essentially proved in [20, Lemma 3.6], which established the existence of a generic constant with the properties as in (A8) such that

| (3.6) |

for all . On the other hand we have by and equation (2.5) that

| (3.7) | ||||

Hence, by plugging this result into (3.6):

which proves that assumption (A8) holds even with . The remaining assumption (A9) is less obvious and requires a proof. We give this proof for the Continuous Galerkin PG-LOD in Section 5. We summarize the result in the following lemma.

Lemma 3.5 (inf-sup stability of Continuous Galerkin PG-LOD).

For all let for . Then there exist generic constants (independent of , , or the oscillations of ) and as in assumption (A8), so that it holds

for and

where , i.e. the space of all functions from that are zero on the boundary of the coarse grid elements. Observe that converges with exponential speed to . Furthermore we have (because ) and also for all sufficiently large .

Remark 3.6.

Let for with , then the CG-LOD in Petrov-Galerkin formulation is inf-sup stable for sufficiently small . In particular, there exists a unique solution of problem (3.4).

Remark 3.7.

Lemma 3.5 does not allow to conclude to inf-sup stability for the regime . However, even though this regime is not of practical relevance, it is interesting to note that we could not observe a violation of the inf-sup stability for any value of and in any numerical experiment that we set up so far.

Since assumptions (A1)-(A9) are fulfilled for this setting, Theorems 3.2 and 3.4 hold true for the arising method. Furthermore, we have and in the estimates, meaning that the -pollution in front of the decay term vanishes. We can summarize the result in the following conclusion.

Conclusion 3.8.

Assume the (Continuous Galerkin) setting of this subsection and let denote a Petrov-Galerkin solution of (3.4). If for , then it holds

In particular, the bound is independent of .

3.4 Discussion of advantages

The central disadvantage of the Galerkin LOD is that it requires a communication between solutions of different patches. Consider for instance the assembly of the system matrix that belongs to problem (3.3). Here it is necessary to compute entries of the type

which particularly involves the computation of the term

| (3.8) |

where denote two coarse nodal basis functions and and its corresponding supports. The efficient computation of (3.8) requires information about the intersection area of any two patches and . Even if and are not adjacent or close to each other, the intersection of the corresponding patches can be complicated and non-empty. The drawback becomes obvious: first, these intersection areas must be determined, stored and handled in an efficient way and second, the number of relevant entries of the stiffness matrix (i.e. the non-zeros) increases considerably. Note that this also leads to a restriction in the parallelization capabilities, in the sense that the assembly of the stiffness matrix can only be ’started’ if the correctors are already computed. Another disadvantage is that the assembly of the right hand side vector associated with in (3.3) is much more expensive since it involves the computation of entries . First, the integration area is instead of typically . This increases the computational costs. At the same time, it is also hard to assemble these entries by performing (typically more efficient) element-wise computations (for which each coarse element has to be visited only once). Second, involves a quadrature rule of high order, since is rapidly oscillating. These oscillations must be resolved by the quadrature rule, even if is a purely macroscopic function that can be handled exactly by a low order quadrature. Hence, the costs for computing depend indirectly on the oscillations of . Finally, if the LOD shall be applied to a sequence of problems of type (1.2), which only differ in the source term (or a boundary condition), the system matrix can be fully reused, but the complications that come with the right hand side have to be addressed each time again.

The Petrov-Galerkin formulation of the LOD clearly solves these problems without suffering from a loss in accuracy. In particular:

-

•

The PG-LOD does not require any communication between two different patches and the resulting stiffness matrix is sparser than the one for the symmetric LOD. In particular, the entries of the system matrix can be computed with the following algorithm:

Let denote the empty system matrix with entries .Algorithm: assembleSystemMatrix( , , )In parallel foreach doforeach with docompute with

foreach with doupdate the system matrix:end foreachend foreachend foreachObserve that it is possible to directly add the local terms to the system matrix , i.e. the assembling of the matrix is parallelized in a straightforward way and does not rely on the availability of other results.

-

•

Replacing the source term in (1.2), only involves the re-computation of the terms for coarse nodal basis functions , i.e. the same costs as for the standard FE method on the coarse scale. Furthermore, the choice of the quadrature rule relies purely on , but not on the oscillations of .

Besides the previously mentioned advantages, there is still a memory consuming issue left: the storage of the local correctors . These local correctors need to be saved in order to express the final approximation which is spanned by the multiscale basis functions . As long as we are interested in a good -approximation of the solution, this problem seems to be unavoidable. However, in many applications we can even overcome this difficulty by exploiting another very big advantage of the PG-LOD: Theorem 3.4 predicts that alone the ’coarse part’ of , denoted by , already exhibits very good -approximation properties, i.e. if we have essentially

In contrast to , the representation of does only require the classical coarse finite element basis functions. Hence, we can use the algorithm presented earlier, with the difference that we can immediately delete after updating the stiffness matrix. Observe that even if computations have to be repeated for different source terms , this stiffness matrix can be reused again and again. Also, if a user is interested in the fine scale behavior in a local region (but the were already dropped), it is still possible to quickly re-compute the desired local corrector for the region.

As an application, consider for instance the case that the problem

describes the diffusion of a pollutant in groundwater. Here, describes the concentration of the pollutant, the (rapidly varying) hydraulic conductivity and a source term describing the injection of the pollutant. In such a scenario, there is typically not much interest in finding a good approximation of the (locally fluctuating) gradient , but rather in the macroscopic behavior of pollutant , i.e. in purely finding a good -approximation that allows to conclude where the pollutant spreads. A similar scenario is the investigation of the properties of a composite material, where describes the heterogenous material and some external force. Again, the interest is in finding an accurate -approximation. Besides, the corresponding simulations are typically performed for a variety of different source terms , investigating different scenarios. In this case, the PG-LOD yields reliable approximations with very low costs, independent of the structure of .

Remark 3.9 (Relation to the -projection).

Assume the setting of this subsection. In [35] it was shown that for all and , i.e. and are -orthogonal. This implies that

with denoting the -projection on . To verify this, let be arbitrary. Then due to we can write (with and ) and observe for all

Hence, with .

Conclusion 3.10 (Application to homogenization problems).

Assume the setting of this subsection and let denote the -projection on as in Remark 3.9. We consider now a typical homogenization setting with being a sequence of positive parameters that converges to zero. Let denote the unique cube in and let for a function that is -periodic in the second argument (hence is rapidly oscillating with frequency ). The corresponding exact solution of problem (1.2) shall be denoted by . It is well known (c.f. [3]) that converges weakly in (but not strongly) to some unique function . Furthermore, if it holds . With Theorem 3.4 together with Remark 3.9 and standard error estimates for FE problems, we hence obtain:

for . Homogenization problems are typical problems, where one is often purely interested in the -approximation of the exact solution , meaning one is interested in the homogenized solution .

As discussed in this section, the PG-LOD can have significant advantages over the (symmetric) G-LOD with respect to computational costs, efficiency and memory demand. In Subsection 4.1 we additionally present a numerical experiment to demonstrate that the approximations produced by the PG-LOD are in fact very close to the ones produced by (symmetric) G-LOD, i.e. not only of the same order as predicted by the theorems, but also of the same quality.

Remark 3.11 (Nonlinear problems).

The above results suggest that the advantages can become even more pronounced for certain types of nonlinear problems. For instance, consider a well-posed problem of the type

for a nonlinear function . Here, it is intuitively reasonable to construct as before using only the linear elliptic part of the problem. This is a preprocessing step that is done once and can be immediately deleted stiffness matrix is calculated and saved. Then we solve for that satisfies

Clearly, typical iterative solvers can be utilized to solve this variational problem. This iteration is inexpensive because it is done in and the preconstructed stiffness matrix can be fully reused within every iteration and since the other contributions are independent of . Performing iterations on the coarse space for solving nonlinear problems within the framework of multiscale finite element (MsFEMs) has been investigated (see for example [17] and [13]).

3.5 Example 2: Discontinuous Galerkin Finite Element Method

In this subsection, we apply the results of Section 3.2 to a LOD Method that is based on a Discontinuous Galerkin approach. The DG-LOD was originally proposed in [15] and fits into the framework proposed in Section 2.2. First, we show that the setting fulfills assumptions (A4)-(A8) and after we discuss the advantage of the PG DG-LOD over the symmetric DG-LOD. For simplification, we assume that is piecewise constant with respect to the fine mesh so that all of the subsequent traces are well-defined.

Again, we make the same assumptions on the partitions and as in Section 2.1 and additionally assume that and are either triangular or quadrilateral meshes. The corresponding total sets of edges (or faces for ) are denoted by (for ), where and denotes the set of interior and boundary edges, respectively.

Furthermore, for we denote the spaces of discontinuous functions with total, respectively partial, polynomial degree equal to or less than by

and define if is a triangulation and if it is a quadrilation. The coarse space is defined in the same fashion with instead of . Note that these spaces are no subspaces of as in the previous example. For this purpose, we define to be the -piecewise gradient (i.e. for and ).

For every edge/face there are two adjacent elements with . We define the jump and average operators across by

where be the unit normal on that points from to , and on by

where is the outwards unit normal of (and ). Observe that flipping the roles of and leads to the same terms in the bilinear form defined below.

With that, we can define the typical bilinear form that characterizes the Discontinuous Galerkin method:

Here, is a penalty parameter that is chosen sufficiently large and . The coarse bilinear form is defined analogously with coarse scale quantities. It is well known, that (respectively ) is a scalar product on (respectively ). Consequently (A4) is fulfilled. As a norm on that fulfills assumption (A5), we can pick

Analogously, we define to be a norm on . In this case we obtain the constant . Assumption (A6) is obviously fulfilled.

As the operator in assumption (A7) we pick the -projection on , i.e. for we have

In [15, Lemma 5] it was proved that the operator fulfills the desired approximation and stability properties. Since is a projection, we have and hence obviously also -stability of the inverse on .

The localized bilinear form in (2.4) is defined by where in and otherwise, is the element indicator function. Obviously we have for all that

In [15] the DG-LOD is presented in a slightly different way, in the sense that there exists no general corrector operator . Instead, ’basis function correctors’ are introduced. However, it is easily checkable that each of these ’basis function correctors’ is nothing but the corrector operator, defined via (2.5), applied to an original coarse basis function. Therefore, the correctors given by (2.5) are just an extension of the definition to arbitrary coarse functions. Hence, both methods coincide and are just presented in a different way.

Next, we discuss (A8). This property was shown in [15, Lemma 11 and 12], however not explicitly for the setting that we established in Definition 2.3. It was only shown for , where denotes a basis function on associated with the ’th node. However, the proofs in [15] directly generalize to the local correctors given by equation (2.5). More precisely, following the proofs in [15] it becomes evident that the availability of the required decay property (A8) purely relies on the fact, that the right hand side in the local problems is only locally supported (with a support that remains fixed, even if the patch size decreases). Therefore (A8) can be proved analogously.

Finally, assumption (A9) is not easy to verify. It is obviously fulfilled for the case , but the generalized result is harder to verify. The following result holds under some restrictions on the meshes and .

Lemma 3.12 (inf-sup stability of Discontinuous Galerkin PG-LOD).

Assume that is quasi-uniform and that there exists an exponent with such that for all

(i.e. if is also quasi-uniform we assume ). If is such that then, for sufficiently small , there exist generic positive constants such that

Hence, we have inf-sup stability for sufficiently small .

The proof is given in Section 5. We note that the inf-sup stability can be observed numerically already under weaker assumptions (see Section 4) and that it is in general ’a reasonable thing to expect’ as discussed in Remark 3.3.

In conclusion, the Discontinuous Galerkin LOD in Petrov-Galerkin formulation fulfills the assumptions of our framework (up to a discussion on (A9)). The advantages that we discussed in the previous subsection for the Petrov-Galerkin Continuous Finite Element Method in terms of memory and efficiency remains true. However, for the PG DG-LOD there is a very important additional advantage. It is known that the classical DG method has the feature of local mass conservation with respect to the elements of the underlying mesh. This can be easily checked by testing with the indicator function of an element in the variational formulation of the method. The local mass conservation is a highly desired property for various flow and transport problems. However, the DG-LOD does not preserve this property, since the indicator function of an element (whether coarse or fine) is not in the space . This problem is solved in the PG DG-LOD, where we can test with any element from and in particular with the indicator function of a coarse element. Hence, in contrast to the symmetric DG-LOD, the PG DG-LOD is locally mass conservative with respect to coarse elements . This allows for example the coupling of the PG DG-LOD for an elliptic problem with the solver for a hyperbolic conservation law, which was not possible before without relinquishing the mass conservation. We discuss this further in the next subsection.

3.6 Perspectives towards Two-Phase flow

In this subsection, we investigate an application of the Petrov-Galerkin DG-LOD in the simulation of two-phase flow as governed by the Buckley-Leverett equation. Specifically, the LOD framework is utilized to solve the pressure equation, which is an elliptic boundary value problem, and is coupled with a solver for a hyperbolic conservation law. The Buckley-Leverett equation can be used to model two-phase flow in a porous medium. Generally, the flow of two immiscible and incompressible fluids is driven by the law of mass balance for the two fluids:

| (3.9) |

Here, is a computational domain, a time interval, the unknowns describe the saturations of a wetting and a non-wetting fluid and and are the corresponding fluxes. Furthermore, describes the porosity and and are two source terms. Darcy’s law relates the fluxes with the two unknown pressures and by

Here, denotes the hydraulic conductivity, and the relative permeabilities depending on the saturations, and the viscosities, and the densities and the gravity vector. The saturations are coupled via and a relation between the two pressures is typically given by the capillary pressure relation for a monotonically decreasing capillary pressure curve . In this case, we obtain the full two-phase flow system, which consists of two strongly coupled, possibly degenerate parabolic equations. However, if we neglect the gravity and the capillary pressure (i.e. assume that ), the system reduces to the so called Buckley-Leverett system with an elliptic pressure equation and an hyperbolic equation for the saturation:

| (3.10) |

where we have , , the total mobility , the flux and the flux function . The total source is given by . Observe that (3.10) is obtained from (3.9) by summing up the equations for the saturations, using .

An application for which neglecting the capillary pressure is typically justified are oil recovery processes. Here, a replacement fluid, such as water or liquid carbon dioxide, is injected with very high rates into a reservoir to move oil towards a production well. However, often oil is trapped at interfaces of a low and a high conductivity region. This oil would become inaccessible which is why detailed simulations are required before the replacement fluid can be actually injected.

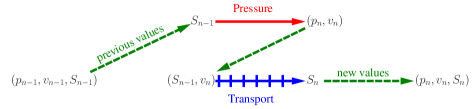

Depending on how the mobilities are chosen, the hyperbolic Buckley-Leverett problem can have one or more weak solutions (c.f. [33]). One approach for solving the problem numerically is to use an operator splitting technique as proposed in [4], which is more well-known as the (IM)plicit (P)ressure (E)xplicit (S)aturation, i.e., IMPES. Here, the hyperbolic Buckley-Leverett problem is treated with an explicit time stepping method where the flux velocity is kept constant for a certain time interval and then updated by solving the elliptic problem with the saturation from the previous time step (see Figure 1 for an illustration). Alternatively, depending on the type of the flux function , the hyperbolic problem can be also solved implicitly with a suitable numerical scheme for conservation laws (c.f. [31]) where the flux arising from the Darcy equation is, as in the previous case, only updated every fixed number of time steps.

Observe that the difficulties produced by the multiscale character of the problem are primarily related to the elliptic part of the problem. Once the Darcy problem is solved to update the flux velocity, the grid for solving the hyperbolic problem can be significantly coarsened. The reason is that is possibly still rapidly oscillating, but the relative amplitude of the oscillations is expected to remain small. In other words, just like for standard elliptic homogenization problems, behaves like an upscaled quantity with effective/homogenized functions , and .

Remark 3.13.

Any realization of the LOD involves to solve a number of local problems that help us to construct the low dimensional space . One might consider to update this space every time that the Darcy problem has to be solved with a new saturation. However, since is essentially macroscopic, it is generally sufficient to construct the space only once for and reuse the result for every time step. This makes solving the elliptic multiscale problem much cheaper after the multiscale space is assembled. A justification for this reusing of the basis can be e.g. found in [21] where it was shown that oscillations coming from advective terms can be often neglected in the construction of a multiscale basis. Under certain assumptions, the relative permeability can in fact be interpreted as a pure enforcement by an additional advection term.

4 Numerical Experiments

In this section we present two different model problems. The first one involves a LOD methods for the continuous Galerkin method. Here, we compare the results obtained with the symmetric version of the method with the results obtained for the Petrov-Galerkin version. In the second model problem, we use a PG DG-LOD for solving the Buckley-Leverett system.

4.1 Continuous Galerkin PG-LOD for elliptic multiscale problems

In this section, we use the setting established in Section 3.3. All experiments were performed with the G-LOD and PG-LOD for the Continuous Finite Element Method.

| 0 | 0.3794 | 0.3772 | 0.6377 | 0.3778 | 0.3755 | 0.6375 | |

| 1/2 | 0.2756 | 0.2381 | 0.5312 | 0.2588 | 0.2269 | 0.5628 | |

| 1 | 0.2523 | 0.1445 | 0.3637 | 0.2544 | 0.1504 | 0.3642 | |

| 3/2 | 0.2514 | 0.1355 | 0.3125 | 0.2518 | 0.1380 | 0.3162 | |

| 0 | 0.2039 | 0.2037 | 0.5048 | 0.2037 | 0.2036 | 0.5048 | |

| 1 | 0.1100 | 0.0526 | 0.2278 | 0.1139 | 0.0619 | 0.2345 | |

| 2 | 0.1073 | 0.0423 | 0.1761 | 0.1078 | 0.0453 | 0.1807 | |

| 3 | 0.1070 | 0.0366 | 0.1567 | 0.1077 | 0.0399 | 0.1600 | |

| 0 | 0.0874 | 0.0873 | 0.3563 | 0.0874 | 0.0873 | 0.3563 | |

| 2 | 0.0353 | 0.0105 | 0.0932 | 0.0357 | 0.0123 | 0.0994 | |

| 4 | 0.0351 | 0.0082 | 0.0653 | 0.0353 | 0.0093 | 0.0680 | |

| 6 | 0.0351 | 0.0080 | 0.0634 | 0.0353 | 0.0091 | 0.0662 |

| 0 | 0.3840 | 0.3815 | 0.6434 | 0.3820 | 0.3796 | 0.6432 | |

| 1/8 | 0.2985 | 0.2781 | 0.5486 | 0.2957 | 0.2753 | 0.5513 | |

| 1/4 | 0.2852 | 0.2592 | 0.5578 | 0.2718 | 0.2472 | 0.5774 | |

| 1/2 | 0.2769 | 0.2392 | 0.5386 | 0.2607 | 0.2291 | 0.5722 | |

| 3/4 | 0.2676 | 0.2052 | 0.4784 | 0.2577 | 0.1972 | 0.4956 | |

| 0 | 0.2106 | 0.2103 | 0.5190 | 0.2103 | 0.2100 | 0.5190 | |

| 1/4 | 0.1480 | 0.1375 | 0.4510 | 0.1569 | 0.1469 | 0.4486 | |

| 1/2 | 0.1372 | 0.1163 | 0.3957 | 0.1305 | 0.1089 | 0.4029 | |

| 1 | 0.1138 | 0.0535 | 0.2308 | 0.1176 | 0.0628 | 0.2372 | |

| 3/2 | 0.1117 | 0.0399 | 0.1710 | 0.1126 | 0.0437 | 0.1761 | |

| 0 | 0.0988 | 0.0984 | 0.3854 | 0.0987 | 0.0983 | 0.3854 | |

| 1/2 | 0.0637 | 0.0592 | 0.2896 | 0.0500 | 0.0442 | 0.2934 | |

| 1 | 0.0406 | 0.0211 | 0.1613 | 0.0431 | 0.0263 | 0.1690 | |

| 2 | 0.0381 | 0.0109 | 0.0957 | 0.0385 | 0.0130 | 0.1017 | |

| 3 | 0.0380 | 0.0087 | 0.0726 | 0.0382 | 0.0099 | 0.0753 |

In order to be more flexible in the choice of the localization patches , we make subsequently use of ”half” or ”quarter coarse layers”, i.e. . This can be easily accomplished by extending Definition 3.1 straightforwardly to fine grid layers, i.e. for and we define the number of fine layers by and the corresponding (broken layer) patch by , where iteratively and . This allows us a more careful investigation of the decay behavior.

Let be the solution of (2.1). In the following we denote by and the corresponding relative error norms defined by

for any . The coarse part (’the -part’) of an LOD approximation (respectively ) is subsequently denoted by (respectively ), where denotes the -projection on (see also Remark 3.9).

We consider the following model problem. Let and . Find with

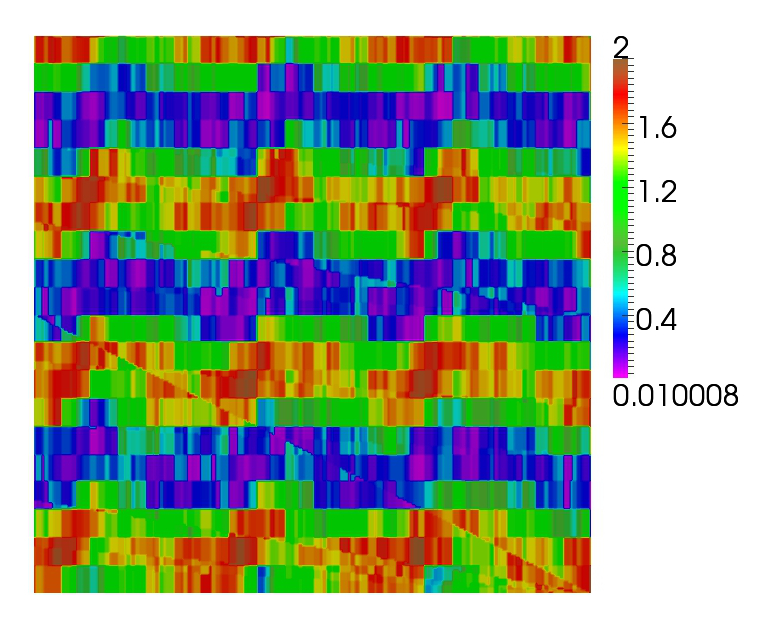

The scalar diffusion term is shown in Figure 2. It is given by

| (4.1) |

and where

The goal of the experiments is to investigate the accuracy of the PG-LOD, compared to the classical symmetric LOD. Moreover, we investigate the accuracy of the coarse part of the LOD approximation in terms of -approximation properties (see Section 3.3 for a corresponding discussion).

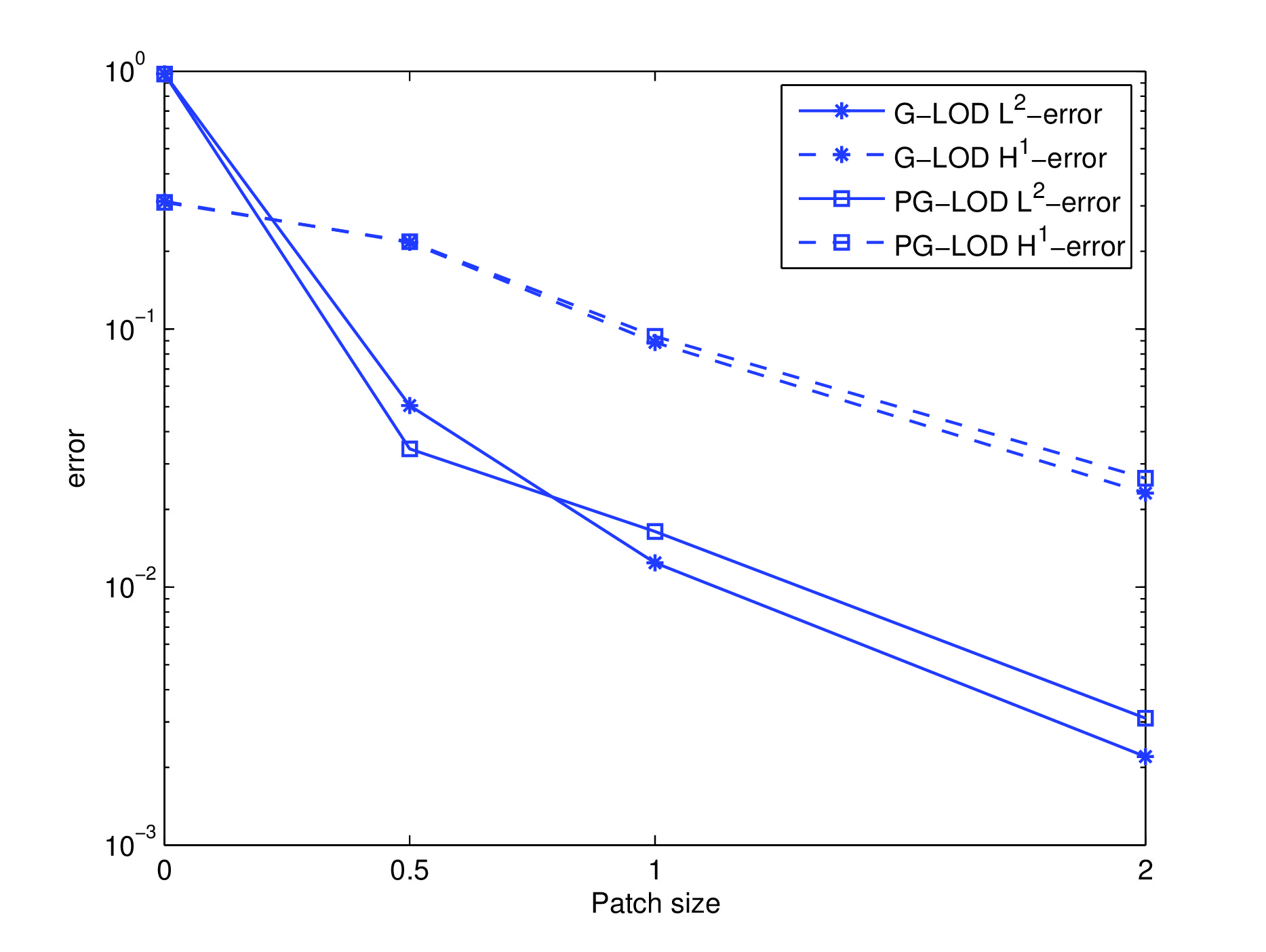

In Table 1 we can see the results for a fine grid with resolution which just resolves the micro structure of the coefficient . Comparing the relative - and -errors for the G-LOD and the PG-LOD respectively (with the reference solution ), we observe that the errors are of similar size in each case. In general, we obtain slightly worse results for the Petrov-Galerkin LOD, however the difference is so small that is does not justify the usage of the more memory-demanding (and more expensive) symmetric LOD. For both methods we observe the same nice error decay (in terms of the patch size) that was already predicted by the theoretical results. Comparing the relative -errors between and the coarse parts of the LOD-approximations, we observe that they already yield very good approximations. We also observe that they seem to be much more dominated by -error contribution than by the -error contribution (i.e. the error coming from the decay). Using patches consisting of more than fine element layers did not lead to any significant improvement, while there were still clear improvements visible for the other errors for the full G-LOD approximations. Furthermore, the linear convergence in is clearly visible for (respectively ) showing that the obtained error estimates seem to be indeed optimal.

The same observations can be made for the errors depicted in Table 2 for a fine grid with resolution . Again, the results for the (symmetric) G-LOD are slightly better than the ones for the PG-LOD, but always of the same order. The exponential convergence in for both realization is visualized in Figure 3. It is clearly observable that there is no argument for using the G-LOD when dealing with patch communication issues which are storage demanding.

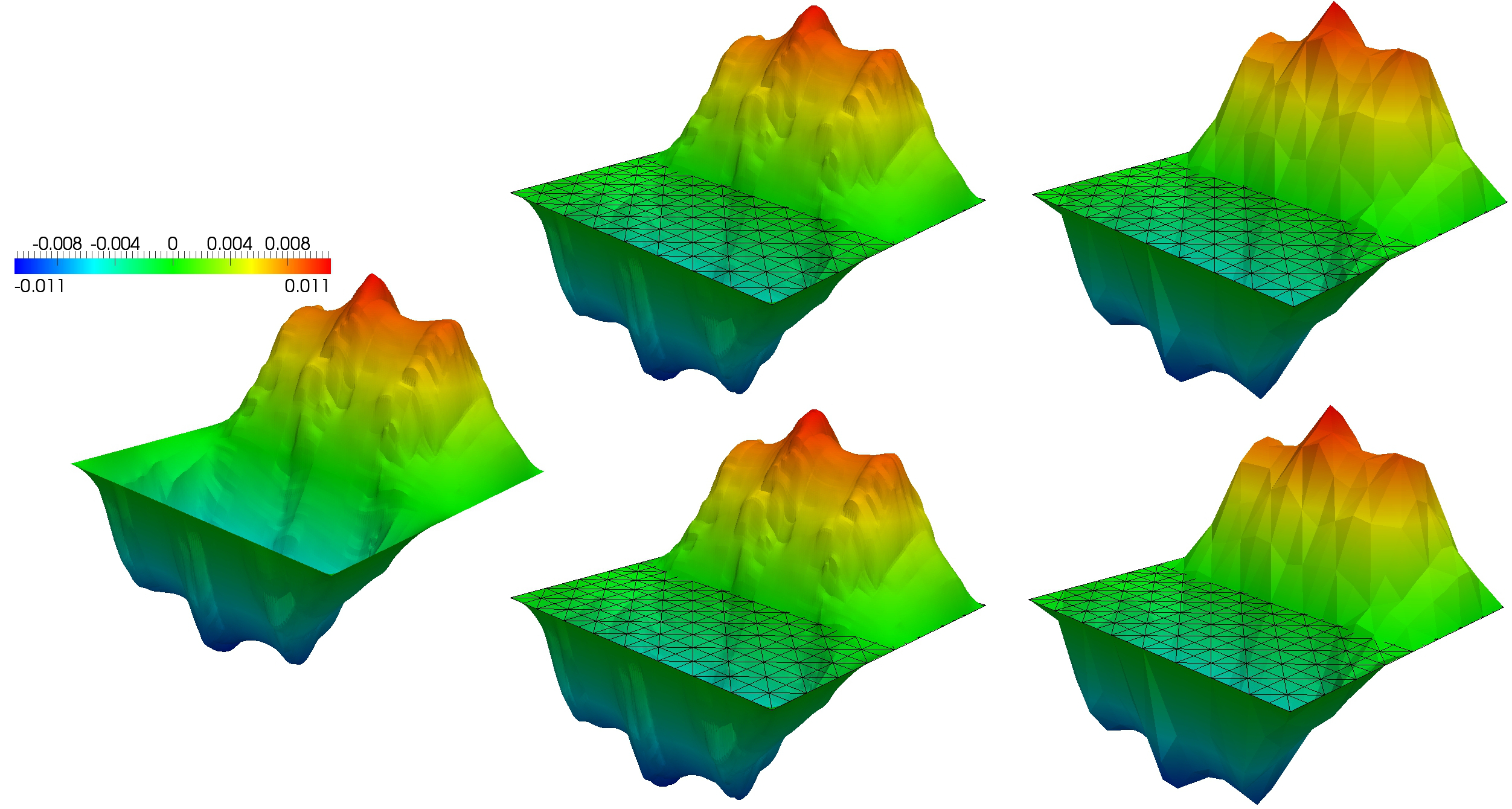

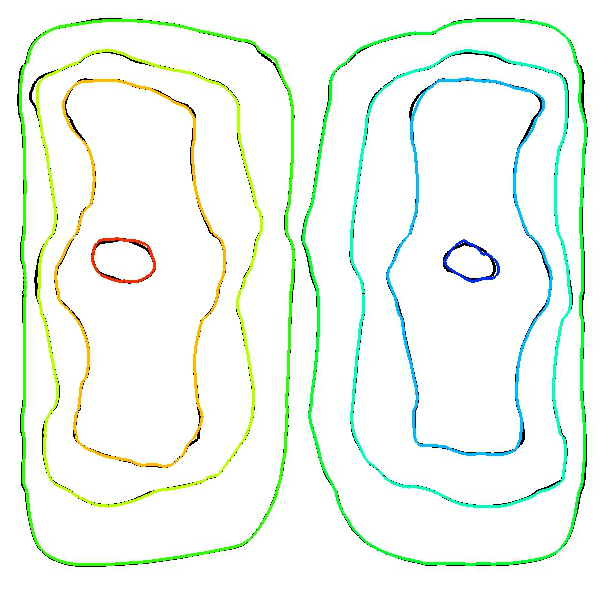

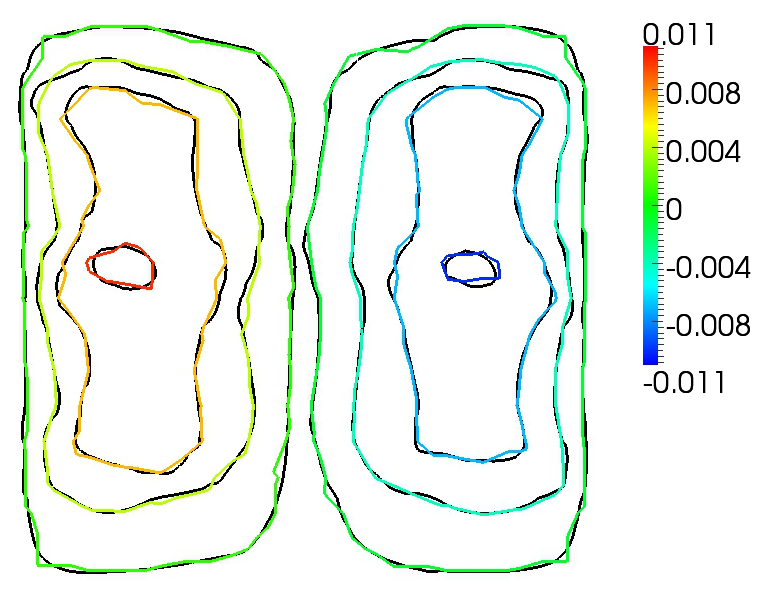

These findings are confirmed in the Figures 4 and 5. In Figure 4 we can see a visual comparison of the reference solution with the corresponding full LOD approximations (symmetric and Petrov-Galerkin). Both are almost not distinguishable for the investigated setting with . Also the coarse parts of the LOD approximations already capture all the essential behavior of the reference solution. In Figures 5 this is emphasized. Here, we compare the isolines between the reference solution and PG-LOD approximation (respectively its coarse part) and we observe that they are highly matching.

4.2 PG DG-LOD for the Buckley-Leverett equation

In this subsection we present the results of a two-phase flow simulation, based on solving the Buckley-Leverett equation as discussed in subsection 3.6. Recall that, the Buckley-Leverett equation has two parts, a hyperbolic equation for the saturation and a elliptic equation for the pressure. For that reason, we use the operator splitting technique IMPES, that we stated in subection 3.6. The elliptic pressure equation is solved by the PG DG-LOD for which a discontinuous linear finite element method is utilized that allows for recovering an elemental locally conservative normal flux. We emphasize that having a locally conservative flux is typically central for numerical schemes for solving hyperbolic partial differential equations. In this experiment we use an upwinding scheme.

Employing PG DG-LOD in this simulation proves to be a very efficient since the local correctors for the generalized basis functions only have to be computed once in a preprocessing step, this follows from the fact the saturation only influence the permeability on the macroscopic scale. The time stepping in the IMPES scheme using the PG DG-LOD for the pressure is realized through the following algorithm.

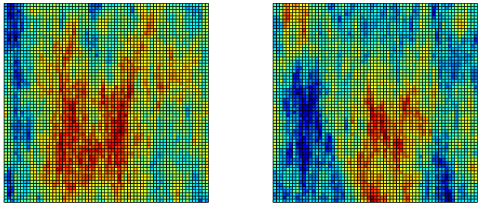

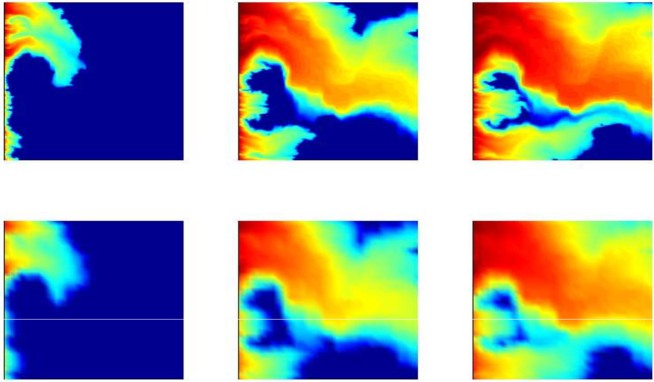

In the numerical experiment we consider the domain to be the unit square. The permeability for is given by layer 21 and 31 of the Society of Petroleum Engineering comparative permeability data (http://www.spe.org/web/csp), projected on a uniform mesh with resolution as illustrated in Figure 6.

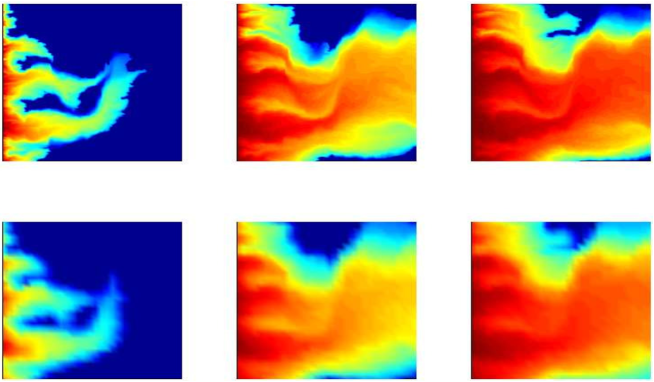

We consider a microscopic partition with mesh size size and a macroscopic partition with mesh size for . The patch size is chosen such that the overall convergence for the PG DG-LOD is not effected. A reference solution to the Buckley-Leverett equation is obtained when both the pressure and saturation equation are computed on , compared to using Algorithm 4.2 where both the pressure and saturation equation are computed on . We consider the following setup. For the pressure equation we use the boundary condition for the left boundary, for the right boundary, otherwise, and the source terms . For the saturation the initial value is on the left boundary and elsewhere. The error is defined by , where is the solution obtained by Algorithm 4.2 (at time ) and is the reference solution (at time ). The errors are measured in the -norm. In Table 3 we fix the coarse mesh size to be , and compute the error for the permeabilities and at the times , and . A graphical comparison is shown in Figure 7 and 8. The errors in the -norm is less than for both permeabilities at all times which is quite remarkable since the coarse mesh for does not resolve the data. In Table 4 we consider the test case involving permeability . We present the -errors at for different values of . We basically observe a linear convergence rate in (for fixed ) which is just what we would expect (since we only use the coarse part of the LOD pressure approximation).

| Data | |||

|---|---|---|---|

| 0.088 | 0.073 | 0.070 | |

| 0.058 | 0.087 | 0.079 |

| 0.220 | |

| 0.113 | |

| 0.073 | |

| 0.048 |

5 Proofs of the main results

In this proof section we will frequently exploit the estimate

| (5.1) |

which is a conclusion from assumption (A7). Let , then (5.1) can be verified as follows by using (A7).

5.1 Proof of Theorem 3.2

The arguments for establishing the error estimate in -norm is analogous to the standard case, see for example, [36] or [20]. We only recall the main arguments.

Proof of Theorem 3.2.

Let be the Galerkin LOD solution governed by (3.3). Utilizing the notation in (A8), we set to satisfy

and define . Using Galerkin orthogonality, we obtain for all and hence (i.e. ). This implies and consequently by energy minimization

The bound finishes the energy-norm estimate. The estimate in the -norm is established in a similar fashion using (5.1). ∎

5.2 Proof of Theorem 3.4

We begin with stating and proving a lemma that is required to establish the a priori error estimate.

Lemma 5.1.

For all with , where and , we have

| (5.2) |

Proof.

Because of and ,

and therefore with and (A7),

In the last step we used again the stability estimates for and in (A7). ∎

Proof of Theorem 3.4.

Let and be respectively the solution of (3.3) and (3.4) for . As in the statement of the theorem, is the solution of (3.4) for . By adding and subtracting appropriate terms and applying triangle inequality, we arrive at

where , , and . In the following, we estimate these three terms. Because (c.f. proof of Theorem 3.2) and by applying the Galerkin orthogonality, we get

| (5.3) |

i.e. . Furthermore, and the splitting with and (i.e. ) holds true. Because , we obtain

| (5.4) |

By Lemma 5.1, we know that . Again, we conclude that .

It remains to estimate for which we define . To simplify the notation, we subsequently denote (according to the definitions of and )

where and . By the definition of problem (3.4) we have

| (5.5) |

On the other hand, by the definition of (see Remark 2.4) and since we get

| (5.6) |

Combining (5.5) and (5.6) we get the equality

We use this equality cast as a unique solution of a self-adjoint variational equation expressed as

where is a given fixed data function written as

Since this problem is self-adjoint, we get that is equally the minimizer in of the functional

Hence we obtain

| (5.7) | ||||

where

By the boundedness of and applying (3.2) we get

| (5.8) |

We now need to estimate . By the inf-sup condition and Lemma 5.1,

| (5.9) | ||||

and thus combining it with (5.8) yields

| (5.10) |

Furthermore, in a similar fashion we use the boundedness of and (3.2) to get

| (5.11) | ||||

By adding and subtracting appropriate terms and applying triangle inequality

| (5.12) |

We use (3.2) to estimate the first and last terms in (5.12) to yield

| (5.13) |

Moreover, by the -stability of (which holds true since with being the orthogonal projection defined in (2.3)), we have

| (5.14) |

Putting back (5.14) and (5.13) to (5.12) and place it in (5.11) gives

| (5.15) | ||||

where in the last step we use the Young’s inequality for both terms, and in particular for the second term, inserting a sufficiently small so that we can later on hide the term in the left hand side of (5.7). Note that the choice of is independent of , or . Rearranging and collecting common terms in the last inequality gives

so that we need to estimate and , respectively. The stability of the second piece was established in (5.9), while the stability of the first piece is achieved by employing (A9) and (A7) in

from which we conclude that

To summarize, putting this last inequality and (5.10) to (5.7) and choosing sufficiently small gives

combining it with the existing estimates for and proves the error estimate in . Moreover, the estimate in the -norm is established in a similar fashion. This completes the proof of the theorem. ∎

5.3 Proof of Lemma 3.5 and Lemma 3.12

Next, we prove the inf-sup stability of the Continuous Galerkin LOD in Petrov-Galerkin formulation.

Proof of Lemma 3.5.

Let be an arbitrary element. To prove the inf-sup condition, we aim to show that

| (5.16) |

Let therefore for fixed . By the definitions of and , we have , where denotes the corresponding corrector given by (2.6). By we denote the corresponding global corrector for the case and the local correctors are denoted by . First, we observe that by

| (5.17) |

where we used the -stability of and according to (A7). Consequently, (5.17) implies

| (5.18) |

and thus

| (5.19) | ||||

where we have used (5.17) again to bound from below. Note here that denotes a generic constant. It remains to bound . By the orthogonality of and we have

| (5.20) |

and since is such that for all with suppsupp we get by the definition of for every

| (5.21) |

Using both equalities above and by the boundedness of and applying (5.18) yields

| (5.22) | ||||

We next estimate by applying (3.6) and establishing an analog of (3.7) for expressed as

| (5.23) |

giving (for )

| (5.24) | ||||

Thus we end up with

| (5.25) |

which when combined with (5.19) implies that there exist positive generic constants (independent of and ) such that

| (5.26) |

Since for , estimate (5.26) holds for all and the condition is not required. The relation finishes the proof. ∎

Finally, we prove the inf-sup stability of the Discontinuous Galerkin LOD in Petrov-Galerkin formulation.

Proof of Lemma 3.12.

The main arguments are similar as in the proof of Lemma 3.5. Set . Let be an arbitrary element and let for fixed . By the assumptions on and and by the definitions of and it is easy to see that

Consequently we get

| (5.27) |

Thus

| (5.28) | ||||

Using

we obtain that we have for small enough

Inserting this into (5.28) gives us

If is small enough so that is positive, the estimate concludes the inf-sup estimate. ∎

Acknowledgements. We would like to thank the anonymous referees for their valuable comments and their constructive feedback on the original manuscript which helped us to improve this article.

References

- [1] A. Abdulle. On a priori error analysis of fully discrete heterogeneous multiscale FEM. Multiscale Model. Simul., 4(2):447–459 (electronic), 2005.

- [2] A. Abdulle, W. E, B. Engquist, and E. Vanden-Eijnden. The heterogeneous multiscale method. Acta Numer., 21:1–87, 2012.

- [3] G. Allaire. Homogenization and two-scale convergence. SIAM J. Math. Anal., 23(6):1482–1518, 1992.

- [4] K. Aziz and A. Settari. Petroleum Reservoir Simulation. Applied Science Publishers, London, 1997.

- [5] I. Babuska and R. Lipton. Optimal local approximation spaces for generalized finite element methods with application to multiscale problems. Multiscale Model. Simul., 9(1):373–406, 2011.

- [6] R. E. Bank and T. Dupont. An optimal order process for solving finite element equations. Math. Comp., 36(153):35–51, 1981.

- [7] R. E. Bank and H. Yserentant. On the -stability of the -projection onto finite element spaces. Numer. Math., 126(2):361–381, 2014.

- [8] L. Bush, V. Ginting, and M. Presho. Application of a conservative, generalized multiscale finite element method to flow models. J. Comput. Appl. Math., 260:395–409, 2014.

- [9] C. Carstensen. Quasi-interpolation and a posteriori error analysis in finite element methods. M2AN Math. Model. Numer. Anal., 33(6):1187–1202, 1999.

- [10] C. Carstensen and R. Verfürth. Edge residuals dominate a posteriori error estimates for low order finite element methods. SIAM J. Numer. Anal., 36(5):1571–1587 (electronic), 1999.

- [11] W. E and B. Engquist. The heterogeneous multiscale methods. Commun. Math. Sci., 1(1):87–132, 2003.

- [12] Y. Efendiev, V. Ginting, T. Hou, and R. Ewing. Accurate multiscale finite element methods for two-phase flow simulations. J. Comput. Phys., 220(1):155–174, 2006.

- [13] Y. Efendiev, T. Hou, and V. Ginting. Multiscale finite element methods for nonlinear problems and their applications. Commun. Math. Sci., 2(4):553–589, 2004.

- [14] D. Elfverson, E. H. Georgoulis, and A. Målqvist. An adaptive discontinuous Galerkin multiscale method for elliptic problems. Multiscale Model. Simul., 11(3):747–765, 2013.

- [15] D. Elfverson, E. H. Georgoulis, A. Målqvist, and D. Peterseim. Convergence of a discontinuous Galerkin multiscale method. SIAM J. Numer. Anal., 51(6):3351–3372, 2013.

- [16] F. D. Gaspoz, C.-J. Heine, and K. G. Siebert. Optimal grading of the newest vertex bisection and -stability of the -projection. Preprint SimTech Universität Stuttgart, 2014.

- [17] V. Ginting. Analysis of two-scale finite volume element method for elliptic problem. J. Numer. Math., 12(2):119–141, 2004.

- [18] A. Gloria. An analytical framework for the numerical homogenization of monotone elliptic operators and quasiconvex energies. Multiscale Model. Simul., 5(3):996–1043 (electronic), 2006.

- [19] A. Gloria. Reduction of the resonance error—Part 1: Approximation of homogenized coefficients. Math. Models Methods Appl. Sci., 21(8):1601–1630, 2011.

- [20] P. Henning and A. Målqvist. Localized orthogonal decomposition techniques for boundary value problems. SIAM J. Sci. Comput., 36(4):A1609–A1634, 2014.

- [21] P. Henning, A. Målqvist, and D. Peterseim. A localized orthogonal decomposition method for semi-linear elliptic problems. ESAIM Math. Model. Numer. Anal., 48(5):1331–1349, 2014.

- [22] P. Henning, A. Målqvist, and D. Peterseim. Two-level discretization techniques for ground state computations of Bose-Einstein condensates. SIAM J. Numer. Anal., 52(4):1525–1550, 2014.

- [23] P. Henning, P. Morgenstern, and D. Peterseim. Multiscale partition of unity. In Meshfree Methods for Partial Differential Equations VII, volume 100 of Lecture notes in Computational Science and Engineering. Springer, Berlin, 2015.

- [24] P. Henning and M. Ohlberger. The heterogeneous multiscale finite element method for elliptic homogenization problems in perforated domains. Numer. Math., 113(4):601–629, 2009.

- [25] P. Henning and D. Peterseim. Oversampling for the Multiscale Finite Element Method. Multiscale Model. Simul., 11(4):1149–1175, 2013.

- [26] T. Y. Hou and X.-H. Wu. A multiscale finite element method for elliptic problems in composite materials and porous media. J. Comput. Phys., 134(1):169–189, 1997.

- [27] T. Y. Hou, X.-H. Wu, and Y. Zhang. Removing the cell resonance error in the multiscale finite element method via a Petrov-Galerkin formulation. Commun. Math. Sci., 2(2):185–205, 2004.

- [28] T. J. R. Hughes. Multiscale phenomena: Green’s functions, the Dirichlet-to-Neumann formulation, subgrid scale models, bubbles and the origins of stabilized methods. Comput. Methods Appl. Mech. Engrg., 127(1-4):387–401, 1995.

- [29] T. J. R. Hughes, G. R. Feijóo, L. Mazzei, and J.-B. Quincy. The variational multiscale method—a paradigm for computational mechanics. Comput. Methods Appl. Mech. Engrg., 166(1-2):3–24, 1998.

- [30] M. Karkulik, C.-M. Pfeiler, and D. Praetorius. -orthogonal projections onto finite elements on locally refined meshes are -stable. ArXiv e-print 1307.0917, 2013.

- [31] D. Kröner. Numerical schemes for conservation laws. Wiley-Teubner Series Advances in Numerical Mathematics. John Wiley & Sons Ltd., Chichester, 1997.

- [32] M. G. Larson and A. Målqvist. Adaptive variational multiscale methods based on a posteriori error estimation: duality techniques for elliptic problems. In Multiscale methods in science and engineering, volume 44 of Lect. Notes Comput. Sci. Eng., pages 181–193. Springer, Berlin, 2005.

- [33] P. G. LeFloch. Hyperbolic systems of conservation laws. Lectures in Mathematics ETH Zürich. Birkhäuser Verlag, Basel, 2002. The theory of classical and nonclassical shock waves.

- [34] A. Målqvist. Multiscale methods for elliptic problems. Multiscale Model. Simul., 9(3):1064–1086, 2011.

- [35] A. Målqvist and D. Peterseim. Computation of eigenvalues by numerical upscaling. Numer. Math., 2014.

- [36] A. Målqvist and D. Peterseim. Localization of elliptic multiscale problems. Math. Comp., 83(290):2583–2603, 2014.

- [37] M. Ohlberger. A posteriori error estimates for the heterogeneous multiscale finite element method for elliptic homogenization problems. Multiscale Model. Simul., 4(1):88–114 (electronic), 2005.

- [38] H. Owhadi and L. Zhang. Localized bases for finite-dimensional homogenization approximations with nonseparated scales and high contrast. Multiscale Modeling & Simulation, 9(4):1373–1398, 2011.

- [39] H. Owhadi, L. Zhang, and L. Berlyand. Polyharmonic homogenization, rough polyharmonic splines and sparse super-localization. ESAIM Math. Model. Numer. Anal., 48(2):517–552, 2014.

- [40] H. A. van der Vorst. Computational methods for large eigenvalue problems. In Handbook of numerical analysis, Vol. VIII, Handb. Numer. Anal., VIII, pages 3–179. North-Holland, Amsterdam, 2002.