Bootstrap-based model selection criteria for beta regressions

Abstract

The Akaike information criterion (AIC) is a model selection criterion widely used in practical applications. The AIC is an estimator of the log-likelihood expected value, and measures the discrepancy between the true model and the estimated model. In small samples the AIC is biased and tends to select overparameterized models. To circumvent that problem, we propose two new selection criteria, namely: the bootstrapped likelihood quasi-CV (BQCV) and its 632QCV variant. We use Monte Carlo simulation to compare the finite sample performances of the two proposed criteria to those of the AIC and its variations that use the bootstrapped log-likelihood in the class of varying dispersion beta regressions. The numerical evidence shows that the proposed model selection criteria perform well in small samples. We also present and discuss and empirical application.

keywords:

AIC , beta regression , bootstrap , cross validation , model selection , varying dispersionMSC:

[2010] 62J99 , 62F07 , 62F99 , 94A171 Introduction

In regression analysis, practitioners are usually interested in selecting the model that yields the best fit from a broad class of candidate models. Thus, model selection is of paramount importance in regression analysis. Model selection is usually based on model selection criteria or information criteria. The Akaike information criterion (AIC) (Akaike, 1973) is the most well-known and commonly used model selection criterion. Several alternative criteria have been developed in the literature, such as the SIC (Schwarz, 1978), HQ (Hannan and Quinn, 1979) e AICc (Hurvich and Tsai, 1989).

The AIC was proposed for estimating (minus two times) the expected log-likelihood. Using Taylor series expansion and the asymptotic normality of the maximum likelihood estimator Akaike showed that the maximized log-likelihood function is a positively biased estimator for the expected log-likelihood. After computing such bias the author derived the AIC as an asymptotically approximated correction for the expected log-likelihood. In small samples, however, the AIC is biased and tends to select models that are overparameterized (Hurvich and Tsai, 1989).

Several variants of the AIC have been proposed in the literature. The first correction of the AIC, the AICc, was proposed in Sugiura (1978) for linear regression models. Later, Hurvich and Tsai (1989) expanded the applicability of the AICc to cover nonlinear regression and autoregressive models. They showed that the AICc is asymptotically equivalent to the AIC but usually delivers more accurate model selection in finite samples. Analytical corrections to the AIC, such as AICc, can be nonetheless difficult to obtain in some classes of models (Shibata, 1997). The analytical difficulties stem from distributional and asymptotic results, as well as from certain restrictive assumptions. In order to circumvent analytical difficulties and to obtain more accurate corrections in small samples, bootstrap (Efron, 1979) variants of the AIC were considered in the literature. They have been introduced and explored in different classes of models. See, for instance, Cavanaugh and Shumway (1997), Ishiguro and Sakamoto (1991), Ishiguro et al. (1997), Seghouane (2010), Shang and Cavanaugh (2008) and Shibata (1997), who introduced the criteria known as WIC, AICb, EIC, among other denominations. Such bootstrap extensions typically outperform the AIC in finite samples. Additionally, as noted by Shibata (1997), they can be easily computed.

Both the AIC and its bootstrap variants aim at estimating the expected log-likelihood using a bias correction for the maximized log-likelihood. In this paper, we follow the approach introduced by Pan (1999) and propose an estimator for the expected log-likelihood that does not require a bias adjustment term. In particular, nonparametric bootstrap and cross validation (CV) are jointly used in a criterion called bootstrapped likelihood CV (BCV). Using the parametric bootstrap and a quasi-CV method we define a new AIC variant. It uses the bootstrapped likelihood quasi-CV (BQCV). We also propose a slice modification known as 632QCV.

Model selection criteria based on the bootstrapped log-likelihood have been explored and successfully applied to autoregressive models (Ishiguro et al., 1997), state-space models (Bengtsson and Cavanaugh, 2006; Cavanaugh and Shumway, 1997), mixed models (Shang and Cavanaugh, 2008), linear regression models (Pan, 1999; Seghouane, 2010) and logistic and Cox regression models (Pan, 1999). In this paper, we investigate model selection via bootstrap log-likelihood in the class of beta regression models. Such models were introduced by Ferrari and Cribari-Neto (2004) and are tailored for modeling responses that assume values in the standard unit interval, , such as rates and proportions. We consider the class of varying dispersion beta regressions, as described in Simas et al. (2010), Ferrari and Pinheiro (2011) and Cribari-Neto and Souza (2012). It generalizes the fixed dispersion beta regression model proposed by Ferrari and Cribari-Neto (2004). The model has two submodels, one for the mean and another one for the dispersion.

The chief goal of our paper is twofold. First, we propose new model selection criteria for beta regressions and then we numerically investigate their finite sample performances in small samples. We also provide simulation results on alternative model selection strategies. The numerical evidence shows that the criteria we propose typically yield reliable model selection in the class of beta regression models.

This paper is organized as follows. In the next section we introduce the AIC and its bootstrap extensions. We also propose two new model selection criteria. Section 3 introduces the class of beta regression models. In Section 4 we present Monte Carlo simulation results on model selection in fixed and varying beta regression models. An empirical application is presented and discussed in Section 5. Finally, some concluding remarks are offered in Section 6.

2 Akaike information criterion and bootstrap variations

The distance measure between two densities can be measured using the Kullback-Leibler (KL) information (Kullback, 1968), also known as entropy or discrepancy (Cavanaugh, 1997). The KL information can be used to select an estimated model which is closest to the true model. The AIC was derived by Akaike (1973) by minimizing the KL information. In what follows, we shall follow Bengtsson and Cavanaugh (2006) in order to formalize the notion of selecting a model from a class of candidate models.

Suppose the -dimensional vector is sampled from an unknown density , where is a -vector of parameters. The respective parametric family of densities is denoted by , where is the -dimensional parametric space. Let be the maximum likelihood estimate of . It is obtained by maximizing in , i.e., is the maximized likelihood function.

Using the AIC it is possible to select the model that best approximates from the class of families , , . For notation simplicity we will not consider different families in the class which have the same dimension. We say that is correctly specified if , where is the smallest dimensional family that contains . We say that is overspecified if but families of smaller dimension also contain . On the other hand, is underspecified if .

The KL measure can be used to determine which fitted model (i.e., which model in the collection ) is closest to . The KL distance between the true model and the candidate model is given by

where denotes expectation under . Let

| (1) |

It is possible to show that . Since does not depend on minimizing or is equivalent to minimizing the discrepancy . Therefore, the model that minimizes minus two times the expected log-likelihood, , is the closest model to the true model according to the Kullback-Leibler information.

Notice that

measures the distance between the true model and the estimated candidate model. However, it is not possible to evaluate , since it requires knowledge of density . Akaike (1973) used as an estimator for . Its bias

| (2) |

can be asymptotically approximated by , where is the dimension of .

Thus, the expected value of Akaike’s criterion,

is asymptotically equal to the expected value of , which is given by

Notice that is a biased estimator of minus two times the expected log-likelihood and the penalizing term of the AIC, , is an adjustment term for the bias given in (2).

Since the AIC is based on a large sample approximation it may perform poorly in small samples (Bengtsson and Cavanaugh, 2006). Several variants of the AIC were developed aiming at delivering more accurate model selection in small samples. Sugiura (1978) developed the AICc, which in class of linear regression models is an unbiased estimator of , that is, . Based on the results obtained by Sugiura (1978), Hurvich and Tsai (1989) extended the use of the AICc to cover nonlinear regression and for autoregressive models. The authors showed that the AICc is asymptotically equivalent to the AIC, i.e., , and typically outperforms the AIC in small samples.

According to Cavanaugh (1997), the advantage of AICc over the AIC is that the former estimates the expected discrepancy more accurately than the latter. On the other hand, a clear advantage of the AIC over the AICc is that the AIC is universally applicable, regardless of the class of models, whereas the AICc derivation is model dependent.

2.1 Bootstrap extensions of AIC

Bootstrap extensions of AIC (EIC) are criteria that use bootstrap estimators for the bias term given in (2). They typically include a bias estimate which is more accurate than in small samples, thus leading to more reliable model selection. In what follows, we shall use five different bootstrap estimators, () for . The bias estimator defines five bootstrap extensions of AIC which we denote by , . The bootstrap variants of the AIC that we shall use for model selection in the class of beta regressions have the following form:

Let be a bootstrap sample (generated either parametrically or nonparametrically) and let denote the expected value with respect to distribution of . Consider bootstrap samples and the corresponding estimates of : , . Here, each estimate is the value of that maximizes the likelihood function .

Ishiguro et al. (1997) proposed a bootstrap extension of the AIC known as the EIC. It is a particular case of the WIC (Ishiguro and Sakamoto, 1991) obtained considering independent and identically distributed (i.i.d.) observations. We shall refer to such a criterion as . It estimates the bias in (2) as

A different bootstrap-based criterion was proposed in Cavanaugh and Shumway (1997) for the selection of state-space models; we shall refer to it as . The criterion estimates the bias in (2) as

We note that and are called AICb1 and AICb2, respectively, in Shang and Cavanaugh (2008) in the context of mixed models selection based on the parametric bootstrap.

Shibata (1997) showed that and are asymptotically equivalent and proposed the following three bootstrap estimators of (2):

We shall refer to the corresponding criteria as , and .

Seghouane (2010) proposed corrected versions of the AIC for the linear regression model as asymptotic approximations to , , , and obtained using the parametric bootstrap.

2.2 Bootstrapped likelihood and cross-validation

The model selection criteria described so far aim at estimating the expected log-likelihood using a bias correction for the maximized log-likelihood function. Pan (1999), however, tried to obtain an estimator for the expected log-likelihood that does not require a bias adjustment. It uses cross-validation (CV) and bootstrap.

CV is widely used for estimating the error rate of prediction models (Efron, 1983; Efron and Tibshirani, 1997). In the context of model selection, according to Davies et al. (2005), the first CV based criterion was the PRESS (Allen, 1974). Bootstrap based model selection was introduced by Efron (1986). Breiman and Spector (1992) and Hjorth (1994) discuss the use of CV and bootstrap in model selection.

According to Efron (1983) and Efron and Tibshirani (1997), CV typically reduces bias but leads to variance inflation. Such variability can be reduced by using the bootstrap method. In the context of model selection of models, Pan (1999) introduced a method that combines nonparametric bootstrap and CV: the bootstrapped likelihood CV (BCV). BCV yields an estimator of (1) that does not entail bias correction. For a sample of size , the BCV is defined by

where is the bootstrap sample generated nonparametrically, , that is, and , and is the number of elements of . Thus, no observation of is used twice: each observation either belongs to or to .

2.3 Proposed bootstrapped likelihood quasi-CV

We shall now introduce two new model selection criteria of models that incorporate corrections for small samples. Like the BCV, these criteria provide direct estimators for the expected log-likelihood.

Let be the distribution function of the observed sample and let be the estimated distribution function, i.e., is the distribution function evaluated at the estimative . We define

| (3) | |||||

| (4) |

Suppose we have pseudo-samples obtained from and let denote the set of bootstrap replications of . We define the bootstrapped likelihood quasi-CV (BQCV) criterion as follows:

where is the expected value with respect to the distribution of .

It follows from the strong law of large numbers that

where denotes almost sure convergence.

The computation of BQCV can be performed as follows:

-

1.

Estimate using the sample ;

-

2.

Generate pseudo-samples from ;

-

3.

For each , , compute and ;

-

4.

Using the replications of compute

Based on pilot simulations, we recommend using .

The algorithm outlined above is not a genuine cross-validation scheme, hence the name quasi-CV. It is not a genuine cross-validation scheme because it does not partition the sample , but instead it treats the samples and as partitions of the same data set. In each bootstrap replication we use a procedure which is similar to the twofold CV. Here, the training sample is the pseudo-sample of the parametric bootstrap scheme, , and the validation sample is the observed sample, .

Following the approach used by Pan (1999) for obtaining the 632CV, we propose another model selection criterion, which we call 632QCV. It is a variant of the BQCV and is given by

3 The beta regression model

Many studies in different fields examine how a set of covariates is related to a response variable that assumes values in continuous interval, , such as rates and proportions; see, e.g., Brehm and Gates (1993), Hancox et al. (2010), Kieschnick and McCullough (2003), Ferrari and Cribari-Neto (2004), Smithson and Verkuilen (2006), Zucco (2008), Verhaelen et al. (2013), Whiteman et al. (2013) and Hallgren et al. (2013). Such modeling can be done using the class of beta regression models, which was introduced by Ferrari and Cribari-Neto (2004). It assumes that the response variable () follows the beta law. The beta distribution is quite flexible since its density can assume a number of different shapes depending on the parameter values. The beta density can be indexed by mean () and dispersion () parameters when written as

| (5) |

where , , , is the gamma function and is the variance function. The mean and the variance of are, respectively, by and .

Let be a vector of independent random variables, where , , has density (5) with mean and unknown dispersion . The varying dispersion beta regression model can be written as

| (6) | |||

| (7) |

where and are vectors of unknown parameters and and are observations on and independent variables, . In what follows, we denote the matrix of regressors used in the mean submodel by , i.e., is the matrix whose th line is . Likewise, is the matrix of regressors used in the dispersion submodel. When intercepts are included in the mean and dispersion submodels, , for . Additionally, and are strictly monotonic and twice differentiable link functions with domain in and image in IR. In the parameterization we use, the same link functions can be used in the mean and dispersion submodels. Commonly used link functions are logit, probit, log-log, complementary log-log and Cauchy. A detailed discussion of link functions can be found in McCullagh and Nelder (1989) and Koenker and Yoon (2009). Finally, we note that the constant dispersion beta regression model is obtained by setting , and is the identity function.

Joint estimation of and can be performed by maximum likelihood. Let and let be an -vector of independent beta random variables. The log-likelihood function is

where

The score function is obtained by differentiating the log-likelihood function with respect to the unknown parameters. Closed-form expressions for the score function and Fisher’s information matrix are given in A.

Let and be the score functions for and , respectively. The maximum likelihood estimators are obtained by solving

The solution to such a system of equations does not have a closed form. Hence, maximum likelihood estimates are usually obtained by numerically maximizing the log-likelihood function.

A global goodness-of-fit measure can be obtained by transforming the likelihood ratio as (Nagelkerke, 1991)

where is the maximized likelihood function of the model without regressors and is the maximized likelihood function of the fitted regression model. An alternative measure is the square of the correlation coefficient between and , where denotes the maximum likelihood estimator of . Such a measure, which we denote by , was proposed by Ferrari and Cribari-Neto (2004) for constant dispersion beta regressions.

4 Numerical evaluation

In this section we investigate the performances of the AIC and its bootstrap variations in small samples when used in the selection of beta regression models. All simulations were performed using the Ox matrix programming language (Doornik, 2007). All log-likelihood maximizations were numerically carried out using the quasi-Newton nonlinear optimization algorithm known as BFGS with analytic first derivatives.111For details on the BFGS algorithm, see Press et al. (1992).

We consider beta regression models with mean submodel as given in (6) and dispersion submodel as given in (7). We used Monte Carlo replications and, for each sample, bootstrapped log-likelihoods were computed. We experimented with larger values of but noticed that they only yielded negligible improvements in the model selection criteria performances. For the bootstrap extensions of AIC we investigated the use of the parametric bootstrap, , as well as the use of the nonparametric bootstrap, . We also considered alternative model selection criteria in the Monte Carlo simulations: AICc (Hurvich and Tsai, 1989), SIC (Schwarz, 1978), SICc (McQuarrie, 1999), HQ (Hannan and Quinn, 1979) and HQc (McQuarrie and Tsai, 1998).222The use of these criteria in beta regression models is done in an ad hoc manner. The covariates values were obtained as random draws; they were kept constant throughout the experiment. The logit link function was used in both submodels.

Performance evaluation of the different criteria is done as in Hannan and Quinn (1979), Hurvich and Tsai (1989), Shao (1996), McQuarrie et al. (1997), McQuarrie and Tsai (1998), Pan (1999), Shi and Tsai (2002), Davies et al. (2005), Shang and Cavanaugh (2008), Hu and Shao (2008), Liang and Zou (2008), and Seghouane (2010). For each criterion we present the frequency of correct order selection (), as well as the frequencies of underspecified () and overspecified () selected models.

The following data generating processes were used:

| (8) | |||||

| (9) | |||||

| (10) | |||||

| (11) |

The first two models, (8) and (9), entail large dispersion whereas the remaining two models, (10) and (11), have small dispersion. Considering the parameters values, we note that the regression models in (8) and (10) are easily identifiable whereas the models in (9) and (11) are weakly identifiable. In the weak identifiability scenario, variations in the covariates have different impacts on the mean response. The terminology “easily identified models” is used here in the same sense as in McQuarrie and Tsai (1998), Caby (2000) and Frazer et al. (2009). We emphasize that such a concept of model identifiability differs from the usual concept which relates to the model parameters uniqueness (Paulino and Pereira, 1994; Rothenberg, 1971). The numerical results for models with large and small dispersion are similar and, for that reason, we only present results for models with small dispersion, (10) and (11).

| AIC | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AICc | ||||||||||||

| SIC | ||||||||||||

| SICc | ||||||||||||

| HQ | ||||||||||||

| HQc | ||||||||||||

| BQCV | ||||||||||||

| 632QCV | ||||||||||||

| BCV | ||||||||||||

| 632CV | ||||||||||||

| AIC | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AICc | ||||||||||||

| SIC | ||||||||||||

| SICc | ||||||||||||

| HQ | ||||||||||||

| HQc | ||||||||||||

| BQCV | ||||||||||||

| 632QCV | ||||||||||||

| BCV | ||||||||||||

| 632CV | ||||||||||||

| AIC | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AICc | ||||||||||||

| SIC | ||||||||||||

| SICc | ||||||||||||

| HQ | ||||||||||||

| HQc | ||||||||||||

| BQCV | ||||||||||||

| 632QCV | ||||||||||||

| BCV | ||||||||||||

| 632CV | ||||||||||||

| AIC | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AICc | ||||||||||||

| SIC | ||||||||||||

| SICc | ||||||||||||

| HQ | ||||||||||||

| HQc | ||||||||||||

| BQCV | ||||||||||||

| 632QCV | ||||||||||||

| BCV | ||||||||||||

| 632CV | ||||||||||||

| AIC | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AICc | ||||||||||||

| SIC | ||||||||||||

| SICc | ||||||||||||

| HQ | ||||||||||||

| HQc | ||||||||||||

| BQCV | ||||||||||||

| 632QCV | ||||||||||||

| BCV | ||||||||||||

| 632CV | ||||||||||||

| AIC | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AICc | ||||||||||||

| SIC | ||||||||||||

| SICc | ||||||||||||

| HQ | ||||||||||||

| HQc | ||||||||||||

| BQCV | ||||||||||||

| 632QCV | ||||||||||||

| BCV | ||||||||||||

| 632CV | ||||||||||||

In all cases, the correct model order dimension is : there are three parameters in the mean submodel and three parameters in the regression structure for the dispersion. The sample sizes are and five candidate covariates are considered for both submodels. The candidate models are sequentially nested for the mean submodel, that is, the candidate model with parameters in the mean regression structure consists of the submodel with the first parameters. The dispersion submodels are also sequentially nested. Thus, for each value of we vary from to , totaling candidate models.

Since the true model belongs to the set of candidate models, the evaluation of the different selection criteria is done by counting the number of times that each criterion selects the correct model order (, or ). Three different approaches were considered. First, we used the different model selection criteria to jointly select the mean and dispersion regressors; the results are given in Tables 1 and 2. Afterwards, for a correctly specified dispersion submodel, we used the model selection criteria to select the regressors in the mean submodel; the results are given in Tables 3 and 4. Finally, for a correctly specified mean submodel, we performed model selection on the dispersion submodel; the results are presented in Tables 5 and 6. In all tables the best results are highlighted.

The figures in Table 1 show the proposed criteria yield reliable joint selection of mean and dispersion regressors in easily identifiable models. We note that for and 632QCV was the best performing criterion. For and BQCV was the best performer. Among the extensions (EIC’s) of the AIC, the criterion that stands out is the EIC3 in their two versions, both with parametric and with nonparametric bootstrap. In this scenario, the AICc stands out when compared to alternative criteria that do not make use of bootstrapped log-likelihood. It is noteworthy the poor performance of the BCV, 632CV and EIC’s criteria. When the sample size increases, the performances of the nonparametric EIC’s improve, becoming similar. The same does not hold, however, for the parametric EIC’s: and perform poorly in all sample sizes.

Under weak identifiability the good performances of the BQCV and 632QCV criteria become even more evident; see Table 2. The 632QCV criterion was the best performer for . For , BQCV outperformed the competition. It is noteworthy that for the 632QCV criterion outperformed all nonbootstrap based criteria by at least . The EIC3 performs well relative to the other bootstrap extensions when regressors are jointly selected for both submodels in a weakly identifiable model. We also note the weak performances of the BCV and 632CV criteria. The AICc clearly outperforms the AIC. For instance, the AIC selected an overspecified model in 614 replications whereas that happened only 147 times when the AICc was used.

We shall now focus on selecting regressors for the mean submodel. Here, the dispersion submodel is correctly specified and the interest lies in identifying which covariates must be included in the mean submodel. The results for a weakly identifiable model are displayed in Table 3. They again show the good finite sample performances of our two model selection criteria. For , the 632QCV criterion was the best performer. For , the best performer was BQCV, and for the criterion outperformed the competition. Once again, the best performing AIC extension was EIC3 and the BCV and 632CV criteria performed poorly. The figures in Table 3 also show that the AICc and the HQc are the best performers among the criteria that do not use bootstrapped log-likelihood.

Table 4 contains the frequencies of correct model selection for the mean submodel when the model is weakly identifiable. The criteria that stands out are the same of the previous settings. For () 632QCV (BQCV) was the best performer. The criterion tends to select models that are overspecified in small samples; see also Table 2.

In our third and final approach, the mean submodel is correctly specified and the interest lies in selecting covariates for the dispersion submodel. The results are presented in Table 5. They show that the 632QCV criterion performs well when the model is easily identifiable; indeed, it was the best performer in all sample sizes. The 632QCV criterion was the only bootstrap AIC variant that outperformed all nonbootstrap-based criteria when . For the remaining sample sizes, only BQCV and outperformed the criteria that do not employ bootstrapped log-likelihood. Table 6 presents results for a weakly identifiable model. This was the only scenario in which 632QCV was not the best performing model selection criterion for ; it still performs well, nonetheless. For larger sample sizes, , the proposed criterion was the best performer. For (), model selection based on the HQ () criterion was the most accurate.

The simulation results presented above lead to important conclusions on beta regression model selection. Such conclusions can be summarized as follows:

-

1.

The model selection criteria proposed in this paper generally work very well and lead to accurate model selection. The 632QCV criterion performed better was the sample size was small and the BQCV performed better in larger samples.

-

2.

Among the criteria that do not use the bootstrapped log-likelihood, the AICc and the HQc criteria were the best performers. The AICc stood out when the sample size was small and the HQc performed better in larger samples.

-

3.

Among the AIC extensions (EIC’s), the EIC3 was the criterion that delivered most accurate model selection. Its nonparametric bootstrap implementation () displayed the best performances in small samples and performed best in larger sample sizes.

- 4.

-

5.

The criteria that employ bootstrapped log-likelihood for beta regression model selection clearly outperform the competition.

5 Application

We use the data given in Griffiths et al. (1993, Table 15.4) on food expenditure, income and number of people in 38 households of a major city in the United States. These data were modeled by Ferrari and Cribari-Neto (2004), who used a constant dispersion beta regression. We performed model selection using the two-step model selection scheme proposed in Bayer and Cribari-Neto (2014) coupled with the BQCV and 632QCV criteria proposed in this paper. In this scheme, the dispersion is taken to be constant and the mean submodel covariates are selected; next, using the selected mean submodel, model selection is carried out in the dispersion submodel. As shown in Bayer and Cribari-Neto (2014), this selection scheme tends typically outperforms the joint selection of regressors for the the mean and dispersion submodels at a much lower computational cost. An implementation of such a model selection procedure in R language (R Core Team, 2014) with the proposed BQCV and 632QCV criteria and two-step scheme is available at http://www.ufsm.br/bayer/auto-beta-reg.zip. The file contains computer code for model selection in beta regressions and also the dataset used in this empirical application.

Following Ferrari and Cribari-Neto (2004), we model the proportion of food expenditure as a function of income and of the number of people in each household. We use the logit link function for the mean and dispersion submodels. We also include as candidate covariates for both submodels the interaction between the income and the number of people , income squared and a quadratic transformation of , that is, .

Assuming constant dispersion, the selected mean submodel, both by BQCV and by 632QCV, use and as covariates. Assuming that this is the correct submodel for mean we now select the regressors to be included in the dispersion submodel. The dispersion submodel selected by the BQCV and 632QCV criteria only includes one covariate, namely: . The parameter estimates of the selected model are presented in the Table 7.

| Parameter | Estimate | Std. error | stat | -value |

|---|---|---|---|---|

| submodel for | ||||

| (Constant) | ||||

| (Number of people) | ||||

| (Interaction) | ||||

| submodel for | ||||

| (Constant) | ||||

| (Number of people) | ||||

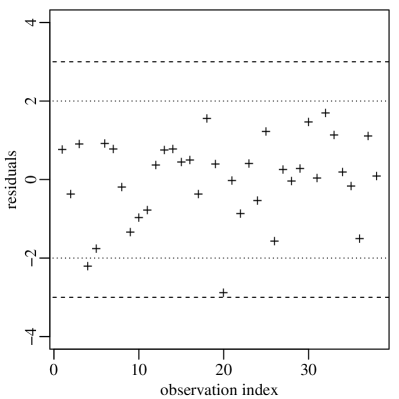

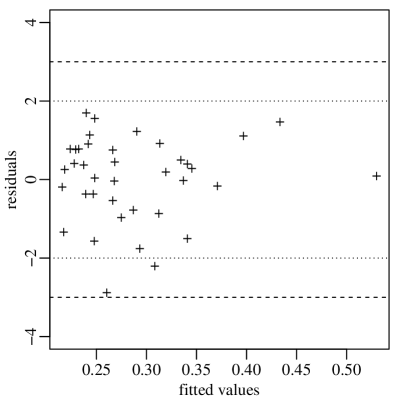

In order to determine whether the model is correctly specified we produced residuals plots; see Figure 1. For details on beta regression residuals and diagnostic tools, the reader is referred to Espinheira et al. (2008a, b) and Ferrari et al. (2011). We use ‘the standardized weighted residual 2’, which is defined as

where and is the th diagonal element of the hat matrix (for details, see Espinheira et al. (2008b) and Ferrari et al. (2011)).

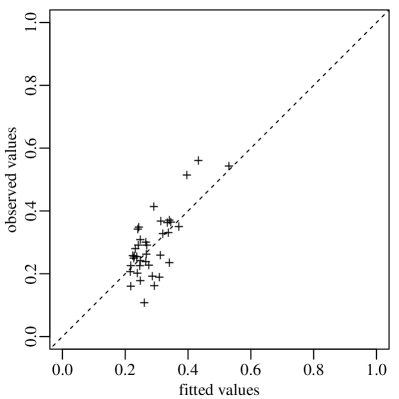

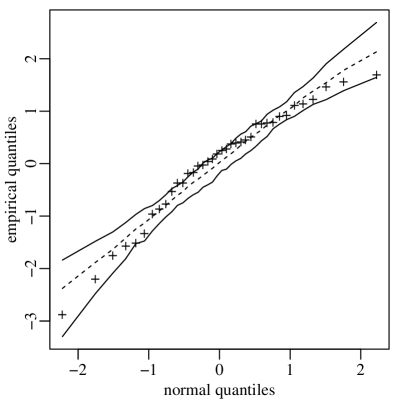

Figures 1(a) and 1(b) show that the residuals are randomly distributed around zero. There are only two atypical observations, with residuals slightly below , but still within the range . Figure 1(c) shows that the model fits the data well since the fitted values are similar to the observed response values. The simulated envelope plot, Figure 1(d), indicates that the model is correctly specified, since most points are within the envelope limits, with a few points lying on one of the envelope bands.

We note that the parameter estimates show that there is a positive relation between the mean response and the number of people in each household, as well as a negative relationship with the interaction variable (). There is also a positive relationship between the number of people in each household and the response dispersion. The varying dispersion beta regression model we selected and fitted has a pseudo- considerably larger than that of the constant dispersion model used by Ferrari and Cribari-Neto (2004): versus .

6 Conclusions

In this paper we proposed two new model selection criteria for the class of varying dispersion beta regression models. The new criteria were obtained as bootstrap variations of the AIC and provide direct estimators for the expected log-likelihood. The proposed criteria are based on the bootstrap method and on a procedure called quasi-CV. They are then called bootstrapped likelihood quasi-CV (BQCV) and 632QCV. The Monte Carlo evidence we presented favors the criteria we proposed: they typically lead to more accurate model selection than alternative criteria. We presented numerical evidence on the joint selection of regressors for the two submodels, for the mean submodel and for the dispersion submodel. An empirical application was also presented and discussed.

Acknowledgements

We gratefully acknowledge partial financial support from CAPES, CNPq, and FAPERGS.

Appendix A Score function and information matrix of the beta regression model with varying dispersion

This appendix presents the score function and the Fisher’s information matrix for the beta regression model with varying dispersion presented in Section 3.

The score function is obtained by differentiating the log-likelihood function with respect to the unknown parameters. The score function for with respect to is given by

where , , , , , and is the digamma function, i.e., , for . The score function with respect to is

where and , the th element of being .

Fisher’s information matrix for and is given by

| (12) |

where , and . Also, we have , and , where

References

- Akaike (1973) Akaike, H., 1973. Information theory and an extension of the maximum likelihood principle. In: N., P. B., F., C. (Eds.), Proceedings of the 2nd International Symposium on Information Theory. pp. 267–281.

- Allen (1974) Allen, D., 1974. The relationship between variable selection and data augmentation and a method for prediction. Technometrics 16, 125–127.

-

Bayer and Cribari-Neto (2014)

Bayer, F. M., Cribari-Neto, F., may 2014. Model selection criteria in beta

regression with varying dispersion. ArXiv paper.

URL http://arxiv.org/abs/1405.3718 - Bengtsson and Cavanaugh (2006) Bengtsson, T., Cavanaugh, J., June 2006. An improved Akaike information criterion for state-space model selection. Computational Statistics & Data Analysis 50 (10), 2635–2654.

- Brehm and Gates (1993) Brehm, J., Gates, S., 1993. Donut shops and speed traps: Evaluating models of supervision on police behavior. American Journal of Political Science 37 (2), 555–581.

- Breiman and Spector (1992) Breiman, L., Spector, P., 1992. Submodel selection and evaluation in regression: The X-random case. International Statistical Review 60, 291–319.

- Caby (2000) Caby, E., 2000. Review: Regression and time series model selection. Technometrics 42 (2), 214–216.

- Cavanaugh (1997) Cavanaugh, J., 1997. Unifying the derivations for the Akaike and corrected Akaike information criteria. Statistics & Probability Letters 33 (2), 201–208.

- Cavanaugh and Shumway (1997) Cavanaugh, J. E., Shumway, R. H., 1997. A bootstrap variant of AIC for state-space model selection. Statistica Sinica 7, 473–496.

- Cribari-Neto and Souza (2012) Cribari-Neto, F., Souza, T., 2012. Testing inference in variable dispersion beta regressions. Journal of Statistical Computational and Simulation 82 (12).

- Davies et al. (2005) Davies, S., Neath, A., Cavanaugh, J., 2005. Cross validation model selection criteria for linear regression based on the Kullback-Leibler discrepancy. Statistical Methodology 2 (4), 249–266.

-

Doornik (2007)

Doornik, J., 2007. An Object-Oriented Matrix Language Ox 5. London: Timberlake

Consultants Press.

URL http://www.doornik.com/ - Efron (1979) Efron, B., 1979. Bootstrap methods: Another look at the jackknife. The Annals of Statistics 7 (1), 1–26.

- Efron (1983) Efron, B., 1983. Estimating the error rate of a prediction rule: Improvement on cross-validation. Journal of the American Statistical Association 78 (382), 316–331.

- Efron (1986) Efron, B., 1986. How biased is the apparent error rate of a prediction rule? Journal of the American Statistical Association 81 (393), 461–470.

- Efron and Tibshirani (1997) Efron, B., Tibshirani, R., 1997. Improvements on cross-validation: The .632+ bootstrap method. Journal of the American Statistical Association 92 (438), 548–560.

- Espinheira et al. (2008a) Espinheira, P. L., Ferrari, S. L. P., Cribari-Neto, F., 2008a. Influence diagnostics in beta regression. Computational Statistics & Data Analysis 52 (9), 4417–4431.

- Espinheira et al. (2008b) Espinheira, P. L., Ferrari, S. L. P., Cribari-Neto, F., 2008b. On beta regression residuals. Journal of Applied Statistics 35 (4), 407–419.

- Ferrari and Cribari-Neto (2004) Ferrari, S. L. P., Cribari-Neto, F., 2004. Beta regression for modelling rates and proportions. Journal of Applied Statistics 31 (7), 799–815.

- Ferrari et al. (2011) Ferrari, S. L. P., Espinheira, P. L., Cribari-Neto, F., 2011. Diagnostic tools in beta regression with varying dispersion. Statistica Neerlandica 65 (3), 337–351.

- Ferrari and Pinheiro (2011) Ferrari, S. L. P., Pinheiro, E. C., 2011. Improved likelihood inference in beta regression. Journal of Statistical Computation and Simulation 81 (4), 431–443.

- Frazer et al. (2009) Frazer, L. N., Genz, A. S., Fletcher, C. H., 2009. Toward parsimony in shoreline change prediction (i): Basis function methods. Journal of Coastal Research 25 (2), 366–379.

- Griffiths et al. (1993) Griffiths, W. E., Hill, R. C., Judge, G. G., 1993. Learning and practicing econometrics. New York: Wiley.

- Hallgren et al. (2013) Hallgren, R. C., Pierce, S. J., Prokop, L. L., Rowan, J. J., Lee, A. S., 2013. Electromyographic activity of rectus capitis posterior minor muscles associated with voluntary retraction of the head. The Spine Journal In Press (0), –.

- Hancox et al. (2010) Hancox, D., Hoskin, C. J., Wilson, R. S., 2010. Evening up the score: Sexual selection favours both alternatives in the colour-polymorphic ornate rainbowfish. Animal Behaviour 80 (5), 845–851.

- Hannan and Quinn (1979) Hannan, E. J., Quinn, B. G., 1979. The determination of the order of an autoregression. Journal of the Royal Statistical Society. Series B 41 (2), 190–195.

- Hjorth (1994) Hjorth, J. S. U., 1994. Computer intensive statistical methods: Validation, model selection and Bootstrap. Chapman and Hall.

- Hu and Shao (2008) Hu, B., Shao, J., 2008. Generalized linear model selection using . Journal of Statistical Planning and Inference 138 (12), 3705–3712.

- Hurvich and Tsai (1989) Hurvich, C. M., Tsai, C.-L., 1989. Regression and time series model selection in small samples. Biometrika 76 (2), 297–307.

- Ishiguro and Sakamoto (1991) Ishiguro, M., Sakamoto, Y., 1991. WIC: an estimation-free information criterion. Research memorandum, Institute of Statistical Mathematics, Tokyo.

- Ishiguro et al. (1997) Ishiguro, M., Sakamoto, Y., Kitagawa, G., 1997. Bootstrapping log likelihood and EIC, an extension of AIC. Annals of the Institute of Statistical Mathematics 49 (3), 411–434.

- Kieschnick and McCullough (2003) Kieschnick, R., McCullough, B. D., 2003. Regression analysis of variates observed on (0, 1): Percentages, proportions and fractions. Statistical Modelling 3 (3), 193–213.

- Koenker and Yoon (2009) Koenker, R., Yoon, J., 2009. Parametric links for binary choice models: A fisherian-bayesian colloquy. Journal of Econometrics 152 (2), 120–130.

- Kullback (1968) Kullback, S., 1968. Information theory and statistics. Dover.

- Liang and Zou (2008) Liang, H., Zou, G., 2008. Improved aic selection strategy for survival analysis. Computational Statistics & Data Analysis 52, 2538–2548.

- McCullagh and Nelder (1989) McCullagh, P., Nelder, J., 1989. Generalized linear models, 2nd Edition. Chapman and Hall.

- McQuarrie (1999) McQuarrie, A., 1999. A small-sample correction for the Schwarz SIC model selection criterion. Statistics & Probability Letters 44 (1), 79–86.

- McQuarrie et al. (1997) McQuarrie, A., Shumway, R., Tsai, C.-L., 1997. The model selection criterion AICu. Statistics & Probability Letters 34 (3), 285–292.

- McQuarrie and Tsai (1998) McQuarrie, A., Tsai, C.-L., 1998. Regression and time series model selection. Singapure: World Scientific.

- Nagelkerke (1991) Nagelkerke, N. J. D., 1991. A note on a general definition of the coefficient of determination. Biometrika 78 (3), 691–692.

- Pan (1999) Pan, W., 1999. Bootstrapping likelihood for model selection with small samples. Journal of Computational and Graphical Statistics 8 (4), 687–698.

- Paulino and Pereira (1994) Paulino, C. D. M., Pereira, C. A. d. B., 1994. On identifiability of parametric statistical models. Journal of the Italian Statistical Society 3 (1), 125–151.

- Press et al. (1992) Press, W., Teukolsky, S., Vetterling, W., Flannery, B., 1992. Numerical recipes in C: The art of scientific computing, 2nd Edition. Cambridge University Press.

-

R Core Team (2014)

R Core Team, 2014. R: A Language and Environment for Statistical Computing. R

Foundation for Statistical Computing, Vienna, Austria.

URL http://www.R-project.org/ - Rothenberg (1971) Rothenberg, T. J., 1971. Identification in parametric models. Econometrica 39 (3), 577–591.

- Schwarz (1978) Schwarz, G., 1978. Estimating the dimension of a model. The Annals of Statistics 6 (2), 461–464.

- Seghouane (2010) Seghouane, A.-K., 2010. Asymptotic bootstrap corrections of AIC for linear regression models. Signal Processing 90, 217–224.

- Shang and Cavanaugh (2008) Shang, J., Cavanaugh, J., 2008. Bootstrap variants of the Akaike information criterion for mixed model selection. Computational Statistics & Data Analysis 52 (4), 2004–2021.

- Shao (1996) Shao, J., 1996. Bootstrap model selection. Journal of the American Statistical Association 91 (434), 655–665.

- Shi and Tsai (2002) Shi, P., Tsai, C.-L., 2002. Regression model selection: A residual likelihood approach. Journal of the Royal Statistical Society. Series B (Statistical Methodology) 64 (2), 237–252.

- Shibata (1997) Shibata, R., 1997. Bootstrap estimate of Kullback-Leibler information for model selection. Statistica Sinica 7, 375–394.

- Simas et al. (2010) Simas, A. B., Barreto-Souza, W., Rocha, A. V., 2010. Improved estimators for a general class of beta regression models. Computational Statistics & Data Analysis 54 (2), 348–366.

- Smithson and Verkuilen (2006) Smithson, M., Verkuilen, J., 2006. A better lemon squeezer? Maximum-likelihood regression with beta-distributed dependent variables. Psychological Methods 11 (1), 54–71.

- Sugiura (1978) Sugiura, N., 1978. Further analysts of the data by Akaike’s information criterion and the finite corrections - further analysts of the data by Akaike’s. Communications in Statistics - Theory and Methods 7 (1), 13–26.

- Verhaelen et al. (2013) Verhaelen, K., Bouwknegt, M., Carratalà, A., Lodder-Verschoor, F., Diez-Valcarce, M., Rodríguez-Lázaro, D., de Roda Husman, A. M., Rutjes, S. A., 2013. Virus transfer proportions between gloved fingertips, soft berries, and lettuce, and associated health risks. International Journal of Food Microbiology 166 (3), 419 – 425.

- Whiteman et al. (2013) Whiteman, A., Young, D. E., He, X., Chen, T. C., Wagenaar, R. C., Stern, C., Schon, K., 2013. Interaction between serum BDNF and aerobic fitness predicts recognition memory in healthy young adults. Behavioural Brain Research In Press (0), –.

- Zucco (2008) Zucco, C., 2008. The president’s “new” constituency: Lula and the pragmatic vote in Brazil’s 2006 presidential elections. Journal of Latin American Studies 40 (1), 29–49.