Qualitative evaluation of associations by the transitivity of

the association signs

Zhichao Jiang1, Peng Ding2 and Zhi Geng1

1Peking University and 2Harvard University

Abstract: We say that the signs of association measures among three variables are transitive if a positive association measure between the variable and the intermediate variable and further a positive association measure between and the endpoint variable imply a positive association measure between and . We introduce four association measures with different stringencies, and discuss conditions for the transitivity of the signs of these association measures. When the variables follow exponential family distributions, the conditions become simpler and more interpretable. Applying our results to two data sets from an observational study and a randomized experiment, we demonstrate that the results can help us to draw conclusions about the signs of the association measures between and based only on two separate studies about and .

Key words and phrases: Association measure, causal inference, Prentice’s criterion, surrogate endpoint, Yule–Simpson Paradox.

1. Introduction

Reasoning by transitivity is commonly, at least implicitly, applied to statistical results from different studies. For association measures, however, the transitivity may not be guaranteed without conditions. For example, suppose an epidemiologic study found that irregular heart beat had a positive association with sudden death, and we also know from a clinical trial that a certain drug significantly corrects irregular heart beat. Might we conclude from these two statistical results that the drug can reduce the rate of sudden death? What conditions are required for reasoning from the known statistical results? Transitivity and its required conditions are important for reasoning from the known results of association measures cumulated by statistical inferences. For example, in a meta-analysis, some associations between variable pairs may be obtained from published papers, but the original data may not be available. What conditions are required to qualitatively evaluate an association between another pair of variables based on these known associations? There are a few statistical approaches for such qualitative reasonings. VanderWeele and Robins (2010) propose the signed directed acyclic graph (DAG) to qualitatively reason the sign of association or causal measure between two variables by the signs of directed edges on the paths between the two variables. Their approach requires both a whole DAG over all variables and the signs of all edges on each path between the two variables. VanderWeele and Tan (2012) propose an approach for propagation of bounds within the DAG framework, which requires a known DAG with edge-specific bounds. Rubin (2004) discusses how to combine the results from two randomized trials of anthrax vaccine on human volunteers and macaques, where the outcome of interest, survival when challenged with lethal doses of anthrax, is available only from macaques. Pearl and Bareinboim (2012) discuss the transportability of causal effects across different studies based on the DAG framework. Prentice (1989) proposes a criterion for surrogate endpoints in clinical trials so that a null effect of treatment on a surrogate implies a null effect of treatment on the endpoint. Chen et al. (2007) and Ju and Geng (2010) discuss the transitivity of causal effects between variable pairs of treatment, surrogate and endpoint.

In this paper, we focus on the transitivity of the signs of association measures. We introduce four association measures with different stringency levels: density, cumulative distribution, expectation and correlation levels (Cox and Wermuth, 2003; Whittaker, 1990). We say that the signs of association measures are transitive if a non-negative (or positive) association between and and a non-negative (or positive) association between and imply a non-negative (or positive) association between and . We discuss the transitivity of the signs of association measures, and present conditions and assumptions (or prior knowledge) required for the transitivity. We show that a more stringent association measure has stronger transitivity. We focus on the transitivity of the signs of association measures among three variables, and these results can be easily extended to cases with more variables. We discuss conditions for the transitivity of these association measures separately for two cases with and without the conditional independence of and given . Conditional independence is one condition of Prentice’s criterion for evaluating surrogacy of for the endpoint (Prentice, 1989). The conditions for transitivity proposed in this paper allow for qualitative assessment of the association between two variables and , by the data sampled from the marginal distributions of and or from the conditional distribution of given .

The remainder of the paper is organized as follows. Section 2 presents the definitions of four association measures and discusses their stringencies. In Section 3, we consider the transitivity of the signs of these association measures under the conditional independence of and given , and give results for an exponential family distribution. We generalize the results about transitivity without conditional independence in Section 4. We apply our theoretical results to two data sets in Section 5; we conclude with a discussion in Section 6, and give all proofs of the theorems in the Appendix.

2. Association measures and their stringencies

In this section, we introduce four commonly-used association measures and show their relative stringencies for depicting the associations.

Definition 1.

The four association measures between and are:

-

(1)

density association: (Whittaker, 1990);

-

(2)

distribution association: (Cox and Wermuth, 2003);

-

(3)

expectation association: ;

-

(4)

correlation coefficient: .

For these measures, and may be continuous, discrete or mixed random variables. For a discrete variable, we can replace the partial differentiation by the difference between two adjacent levels. For instance, when and are both binary variables, the density association is the log odds ratio

and the distribution association and expectation association are both equal to the risk difference . Moreover, if we are concerned only about the signs of the association measures, a non-negative expectation association implies that the risk ratio is greater than or equal to one, i.e. .

The density association depicts a local dependence between and around the point . An important property of the density association is

which can be identified by sampling conditionally on or , such as a case-control sampling or a follow-up study. The distribution association depicts the dependence of a global on a local , and means that given is stochastically increasing in (Cox and Wermuth, 2003). The expectation association depicts the overall dependence of on , and correlation coefficient depicts a linear association. We say that and are non-negatively associated with respect to a measure, say , if for all and , and we say that and are positively associated with respect to a measure if further strict inequality holds for some or . Let denote the independence between and , and let denote the conditional independence of and given . Generally, a non-negative association measure at a more stringent level implies a non-negative association measure at a less stringent level, as summarized in the following properties:

Property 1.

The implication relationship (Xie et al., 2008):

Property 2.

The equivalent relationship among null association measures:

Property 3.

For a bivariate normal vector , the equivalent relationship:

Property 4.

For a binary , the equivalent relationship:

Property 5.

For a binary , the equivalent relationship:

Note that all the relationships above are also true for the strict inequalities and equalities, that is, (“”, “”) in the above expressions can be changed to (“”, “”) and (“”, “”).

By the implication relationship in Property 1, the density association is the most stringent, and the correlation coefficient is the least stringent. For the case of two normal variables or two binary variables, all these association measures have the same signs (non-negative, null or positive).

3. Transitivity of association signs with conditional independence

Now we consider three variables , and discuss the conditions for the transitivity of association signs among them. Prentice (1989) uses conditional independence as a criterion for validating a surrogate , when evaluating the effect of treatment on the endpoint . We call the conditional independence assumption, where breaks the dependence between and . Note that we can have both and even when both pairs and are associated, and Table 1 is an example of this given in Birch (1963). This is nowadays called a violation of weak transitivity or of singleton transitivity (Lněnička and Matúš, 2007), in which case we may not infer the transitivity of associations only under the conditional independence assumption. It may be because the associations within different level sets have different signs. For example, the association between and within has a different sign from that between and within . In this section, we discuss the transitivity of the association signs under the conditional independence assumption, and we extend them to the case without the conditional independence assumption in Section 4.

| all | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 4 | 2 | 2 | 1 | 1 | 4 | 7 | 7 | ||||

| 2 | 1 | 4 | 2 | 1 | 4 | 7 | 7 | ||||

| all | 6 | 3 | 6 | 3 | 2 | 8 | 14 | 14 | |||

3.1 Transitivity without distributional assumptions

We shall show, under the conditional independence assumption, that the more stringent association measures, the density and distribution associations, are transitive. But the other two less stringent association measures, the expectation association and correlation, are not transitive without additional conditions or assistance from the more stringent measures. The first theorem is about the transitivity of the density association.

Theorem 1.

(Density association) Under the assumption , if

then

According to Theorem 1, we can conclude a non-negative (positive) density association between and from the prior knowledge of a non-negative (positive) density association between and and a non-negative (positive) density association between and . Notice that the transitivity of the signs is also applicable to non-positive association measures if we define or .

Although Theorem 1 gives the result for non-negative signs, it is much more important to have the result stated directly for only positive or negative signs of associations. Even if the conditions in Theorem 1 are satisfied, we may have for all and , i.e., . If strict inequalities hold for conditions (1) and (2) in Theorem 1 for any in a set of nonzero measure, then we have in this set, that is, the density association measure between and is positive. In fact, if all the variables are discrete, we will alway obtain the strict inequality unless or .

Similarly, we have the following transitivity of the distribution association.

Theorem 2.

(Distribution association) Under the assumption , if

then .

The expectation associations themselves are not transitive, and they require assistance from more stringent measures, as shown in the following theorem.

Theorem 3.

(Expectation association) Under the assumption , if

then .

Similar to Theorem 1, for Theorems 2 and 3, if there exists a set of nonzero measure in which strict inequalities hold in (1) and (2), then the corresponding association measures between and are positive.

Theorems 1 to 3 are also useful for cases with more than three variables. If we have another variable vector , then the conditions in these Theorems should be conditional on , and we can obtain the association signs of and conditional on . This is useful for models with a covariate vector .

Notice that in Theorems 1 to 3, if we have either or , we will always obtain . Condition (1) of Theorem 3 is a distribution association but not an expectation association of on . Below we give a numerical example to illustrate that the expectation association of on cannot replace condition (1) of Theorem 3.

Example 1.

We generate data under conditional independence: Bernoulli Bernoulli, where and is the indicator function. We have that , and , but we calculate that .

However, for a linear model of given , the expectation association measures are transitive, and further the transitivity can be represented by an equation of expectation associations as follows.

Corollary 1.

Under the assumption , if , then .

In Example 1, we see that does not follow a linear model given , and thus we cannot infer the transitivity of association signs. Using the implication relationship of Property 1 and Theorems 1 to 3, we summarize the transitivity of association signs in Table 2. We show the transitivity of non-negative association measures between and and between and to a non-negative association measure between and . We see from Table 2 that a non-negative association measure between and requires the same or more stringent non-negative association measures between and and between and . Notice that Table 2 is not symmetric, and the expectation association of on does not have any implication for the sign of an association measure between and unless has a linear model, as shown in the last line of Table 2. In the following example, a non-negative expectation association of on and even the most stringent non-negative density association between and do not imply a non-negative expectation association of on .

| Association | Association between and | ||||

|---|---|---|---|---|---|

| between and | |||||

| Under , . | |||||

Example 2.

| 0.6 | 0 | 0.4 | |

| 0 | 1 | 0 |

| 0.9 | 0.9 | 0.1 | |

| 0.1 | 0.1 | 0.9 |

The transitivity of the correlation coefficient signs is weaker than that of expectation association measure signs. Under the conditional independence assumption, we cannot obtain a non-negative correlation between and from a non-negative correlation of and ( and ) and another non-negative association measure between and ( and ). This is illustrated by the following example.

Example 3.

| 0.1 | 0.1 | 0.8 | |

| 0.05 | 0.05 | 0.9 |

| 0.3 | 0 | 0.2 | |

| 0.7 | 1 | 0.8 |

3.2 Transitivity in the exponential family

In the previous subsection, we exhibited sufficient conditions for non-negative and positive association measures between and , but such conditions may not be necessary. In other words, it is possible that and are non-negatively or positively associated, but and (or and ) are negatively associated. We shall show the equivalent relationship between the sign of association measure between and and that between and , under the assumptions that follows an exponential family distribution and the association between and is non-negative. Below we review the definition of the exponential family.

Definition 2.

We say that given follows an exponential family distribution if its density (or its probability mass function for a discrete ) has the form

where is a function of and .

In particular, a binomial or normal is from the exponential family. For the exponential family, we show an equivalent relationship among the signs of the density, distribution and expectation associations:

Theorem 4.

If given follows an exponential family distribution, then

The equivalent relationship is also true if (“”, “”) in the inequalities is changed to (“”, “”) and (“”, “”).

Suppose below that we have prior knowledge of the sign of association between and , and we discuss the equivalent relationships between the signs of associations between and and between and .

Corollary 2.

Assume and that given follows an exponential family distribution.

-

(1)

If and strict inequality holds for a nonzero measure set, then

-

(2)

If and strict inequality holds for a nonzero measure set, then

-

(3)

If and strict inequality holds for a nonzero measure set, then

These equivalent relationships above are also true if the inequalities (“”, “”) above are changed to strict inequalities (“”, “”) and equalities (“”, “”).

In practice, when direct measurement of is too time-consuming or costly, we may try to measure a surrogate endpoint instead and use the sign of the association between and to predict the sign of the association between and .

The results above can be extended to transitivity of causal measures. If is randomized or is conditionally independent of all potential outcomes given some covariates, then the associations between and and between and are also the causal effects of on and on , respectively. If we have prior knowledge that the conditional independence assumption holds and the association between and is non-negative, then according to Corollary 2, we may conclude that the sign of the treatment effect of on is the same as the sign of the treatment effect of on .

4. Transitivity of association signs without conditional independence

In many real applications, the conditional independence assumption may not hold. In this section, we remove the conditional independence assumption, and discuss conditions for the transitivity of these association signs.

4.1 Motivating examples

In this section, we consider two cases. In the first case as shown in Figure 1(a), is a confounder between and . In the second case as shown in Figure 1(b), has a direct path to and an indirect path to through an intermediate variable .

For Figure 1(a), our results can help us to find whether the Yule–Simpson Paradox occurs, since we can evaluate whether the conditional association sign is the same as the marginal association sign between and . Appleton et al. (1996) give an example of the Yule–Simpson Paradox, and we show the condensed form in Table 5. As shown in Table 5, the association between and is positive conditional on but negative marginally, thus the Yule–Simpson Paradox occurs.

| : age group | 18-34 | 35-54 | 55-64 | 65+ | all ages | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| : smoker | yes | no | yes | no | yes | no | yes | no | yes | no | ||||

| dead | 5 | 6 | 41 | 19 | 51 | 40 | 42 | 105 | 139 | 230 | ||||

| alive | 174 | 213 | 198 | 180 | 64 | 81 | 7 | 28 | 443 | 502 | ||||

| odds ratio | 1.02 | 1.96 | 1.61 | 1.02 | 0.68 | |||||||||

For Figure 1(b), our results are useful to draw conclusions about the effect of on based on some assumptions about the pairs and . These are generalizations of the results in Section 3 which do not allow a directed arrow from to . As shown in Table 6, we have that and , but . Thus without the conditional independence assumption, even if the pairs and are both positively associated, and may be negatively associated.

| 0.15 | 0.12 | 0.08 | 0.15 | ||

| 0.15 | 0.08 | 0.12 | 0.15 | ||

4.2 Transitivity without distributional assumptions

Analogous to Theorems 1 to 3, we give conditions for the transitivity of density, distribution and expectation association signs as follows.

Theorem 5.

(Density association) Assume . If

| (1) | ||||

| (2) | ||||

| (3) |

then we have , .

Instead of the conditional independence , we require a prior knowledge about the sign of association between and given .

If we have prior knowledge that the association between and given is non-positive, we can replace by in the assumptions. In Theorem 5, condition (1) means that the density association between and is non-negative, and condition (2) means that the density association between and conditional on is non-negative. Condition (3) is quite different and can be interpreted as a non-negative interaction of on

Theorem 6.

(Distribution association) Assume If

then , .

Theorem 7.

(Expectation association) Assume . If

then , .

Comparing conditions (2) in Theorems 5 to 7 with those in Theorems 1 to 3, we see that without the conditional independence assumption, the association between and is required to be conditional on .

There are some implications from Theorems 5 to 7. First, we do not need the joint distribution to judge whether the Yule–Simpson Paradox occurs:

Corollary 3 implies that we can assess the sign of the marginal association measure between and by the conditional distribution , and the marginal distribution of is not required.

Second, by relaxing the conditional independence assumption to the assumption of non-negative association measure between and given , the marginal associations between and are replaced by the conditional associations given . However, this condition can be weakened if the models of and are linear.

Corollary 4.

Assume that , , and . If

then we have for all .

If we have , i.e., and are non-negatively associated conditional on , then Corollary 4 is the same as Cochran (1938). But even if we have only the non-negative association between and marginally, we can still conclude that and are non-negatively associated based on the linear models in Corollary 4. Thus, we do not need to observe to judge condition (2) in Corollary 4. Provided and are positively associated conditional on , if we have two populations, one with observed and the other with observed, we can draw the conclusion about the association sign between and .

Third, when there is a fully randomized intervention on , we will have , and Theorems 5 and 7 can be further simplified.

Corollary 5.

Suppose .

-

(1)

If or is binary, then implies .

-

(2)

If , then ;

-

(3)

If , then .

Fourth, Theorems 5 to 7 can also be useful for the cases with more than three variables in the same way as Theorems 1 to 3. In addition, there is another way to use Theorems 5 to 7 in these cases. We can combine and into a vector that plays the same role as the original . It is not applicable in Theorems 1 to 3 since may not hold.

4.3 Transitivity in the exponential family

Combining Theorems 5 to 7 with the results for the exponential family in Theorem 4, we can strengthen our conclusions as follows:

Theorem 8.

Assume that given follows an exponential family distribution, and that . If

then , .

Due to the symmetry of the density association measure, we have the following corollary.

Corollary 6.

If or is binary, condition (3) in Theorem 5 is redundant.

In many randomized experiments, is binary, thus we do not need to evaluate condition (3) in Theorem 5.

5. Illustrations

In practice, it is possible that we have two or more studies conducted in different periods, locations or sub-populations. When not all variables are observed in each study, or the data may come from a conditional sampling (e.g. from sub-populations given ), generally we can obtain only local or sub-population conclusions. However, we are interested in global conclusions about the whole population. We shall illustrate how to apply our theoretical results to obtain global conclusions using two data sets.

5.1 An Observational Study: The National Longitudinal Surveys

The National Longitudinal Surveys are a set of surveys designed to gather information at multiple time points on the labor market activities and other significant life events of several groups of men and women (Toomet and Henningsen, 2008). Define if a subject graduated from college, and otherwise. Define if a subject belonged to a union, and otherwise. Let be the log of the wage.

To illustrate our theoretical results, suppose that the data set is collected from two groups, one is the union group with and the other is from the non-union group with . That is, the data set is sampled from the conditional distributions for and 1.

From the data set, we can calculate the differences of sample means of the log wage between different college levels given : meanmean () and meanmean (). Thus the college indicator has a positive expectation association on the log wage for both of the groups with and 1. Since there is no information on the distribution of from the conditional sampling given , we cannot determine whether the college indicator also has a positive association on the log wage marginally. To do that, we check the conditions in Theorem 7 as follows. For condition (1), we have the difference of observed frequencies: (), thus we have since and are binary; and for condition (2), we have the differences of sample means: meanmean () and meanmean (). Thus we can conclude that there is a positive expectation association of the college indicator on the log wage in the population.

Using the data set containing the joint distribution of , we obtain meanmean, thus confirming our conclusion. If we would like to assume that follows an exponential family distribution conditional on , then we can deduce from Corollary 2 that the density and distribution association between and are positive.

5.2 A Randomized Experiment: The Job Search Intervention Study

The Job Search Intervention Study was a randomized field experiment that investigated the efficacy of a job training intervention on unemployed workers (Vinocur and Schul, 1997; Tingley et al., 2012). The program was designed not only to increase reemployment among the unemployed, but also to enhance the mental health of the job seekers. In the JOBS II field experiment, 1,801 unemployed workers were randomly assigned to a treatment group () and a control group (). Those in the treatment group participated in job-skills workshops. In the workshops, respondents learned job-searching skills and coping strategies for dealing with setbacks in the job-search process. Those in the control group received a booklet describing job-searching tips. In the follow-up interviews, two key outcome variables were measured: a continuous variable denoting the job-search self-efficacy, and a continuous variable denoting depressive symptoms based on the Hopkins Symptom Checklist.

We randomly split the data set into two subsets with the same number of observations, and suppose that only and were observed in the first subset and only and are observed in the second subset. The goal is to qualitatively evaluate the effect of the treatment on the depressive symptoms . We assume the linear regression model: and , where . This was confirmed by the full data set ( with -value=0.36).

For the condition (1) of Corollary 4, the linear model is saturated because is binary, and we obtain with -value=0.023 from the first subset containing and .

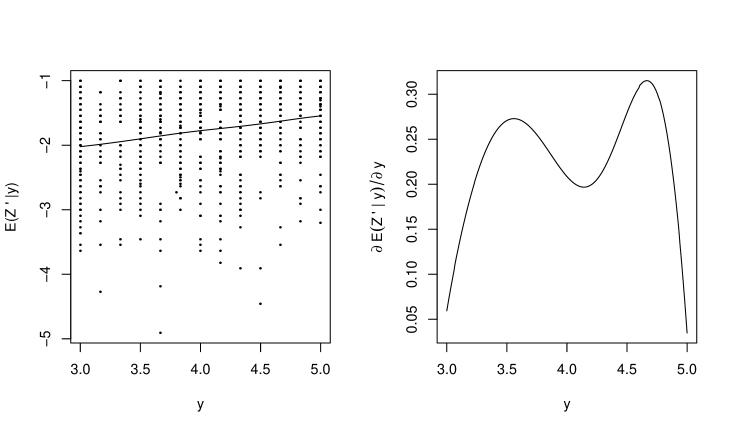

To check condition (2) of Corollary 4, we use both parametric and nonparametric approaches. First, we use the linear model and obtain the estimate of : (-value 0.001) from the second data subset of observed variables and . Next we use local polynomial regression to get nonparametric estimations of both and , which are shown in Figure 2. The scatterplot of and is also shown in the left side of Figure 2. It is seen that for any . Both approaches confirm condition (2) of Corollary 4, thus we conclude that has a non-negative association with .

From the full data set, we obtain that (-value 0.17), thus confirming our conclusion. Although the -value for is not significant, this example is useful for illustrating Corollary 4, because Corollary 4 is about only the signs of parameters and does not require the significance of the parameters. We also learn from this example that the transitivity of hypothesis testing is much more difficult than the transitivity of association signs.

6. Discussion and extensions

We have discussed the transitivity of the signs of four association measures with or without the conditional independence assumption. These four association measures have different stringencies, and more stringent association measures have stronger transitivity. Consequently, the signs or directions of stringent association measures are more easily kept for transitivity under the conditional independence assumption. We proposed conditions for the transitivity of association measures, and showed that these conditions are necessary and sufficient if the intermediate variable is from an exponential family given . The conditions can be checked by data based on marginal distributions or conditional distributions from different studies.

The problem of transportability (Frangakis and Rubin, 2002; Rubin, 2004; Pearl and Bareinboim, 2011) is related to transitivity discussed in this paper. Transportability refers to two populations sharing some features in common, but transitivity refers to variables in a single population which are not observed jointly. If we treat these variables as from different populations, then transitivity can be viewed as transportability. Pearl and Bareinboim’s approaches for transportability are for quantitative inference, and they require more restrictive conditions for the similarity between different populations, which may not be satisfied in practice. Qualitative reasoning is often used in researche studies and daily life, and it does not require such restrictive conditions.

As pointed out by a referee, several applications and generalizations beyond our paper are possible. The density association is used mostly for binary variables, and, among continuous distribution, it has been defined explicitly only for the multivariate normal distribution. Therefore, it may be of interest to find other continuous distributions which have nice properties for the density association. In this paper, the results do not require a particular DAG, and we discuss two DAGs related to our results. In fact, there are four different types of decomposable chain graphs discussed by Drton (2009), and it is worthwhile to discuss applications to these chain graphs. It may also be interesting to simplify these conditions for transitivity using the distributional results by Roverato (2013) and the conditions for traceability of paths in regression graphs by Wermuth (2012).

Acknowledgment

The authors thank a reviewer for valuable comments. This research was supported by NSFC (11171365, 11021463, 10931002).

Appendix

Lemma 1.

If is non-decreasing in and in , and is non-decreasing in for all , then is non-decreasing in .

Proof.

A proof is given by VanderWeele and Robins (2009, page 710, line 7).

As suggested by a reviewer, we give a proof for discrete variables. Suppose and is discrete, taking values , then we have

The final expression is non-negative since all differences in brackets are non-negative for .

Proof of Theorem 1. We need only to prove that for all . When is continuous, we deduce from that

| (1) | |||||

From , we know that is non-decreasing in . Again from , we have . By condition (2) in Theorem 1, we obtain

From Property 1, we get , and thus is non-decreasing in for all . Applying Lemma 1 to equation (1), we conclude that is non-decreasing in .

When is discrete, we need only to prove that, for all ,

or, equivalently,

We compute that

From conditions (1) and (2) in Theorem 1,

we have that is non-decreasing in and that is non-decreasing in for all .

Thus by Lemma 1, we conclude that .

Proof of Theorem 2. By , we have

From conditions (1) and (2) in Theorem 2, is non-increasing in , and is non-decreasing in for all . By Lemma 1, is non-increasing in .

Proof of Theorem 4.

For the exponential family, we

have that and

. Thus we obtain that and have the same sign, which implies the conclusion.

Proof of Corollary 2. The implication relationships from the signs of association measures between and to the signs of association measures between and can be deduced from Theorems 1 to 4. Below we show three implication relationships from the signs of measures between and to the signs of measures between and . From result (1) of Theorem 4, we need to show that increasing in implies increasing in . By , we have from the proof of Theorem 3 that

We use proof by contradiction; suppose that there exists such that . Then from the property of the exponential family in Theorem 4, we have for all . Because is strictly positive for a non-zero measure set, we get that from Theorem 3, which contradicts the condition of a non-negative association between and .

Results (2) and (3) of Corollary 2

can be obtained immediately from the above result (1) and Theorem 4.

Proof of Theorem 5. We need only to prove that is non-decreasing in . When is continuous, for , we have

From the assumption and condition (3) in Theorem 5, is non-decreasing in and ; from condition (1) in Theorem 5, is nondecreasing in ; and from condition (2) in Theorem 5, is non-decreasing in for all . By Lemma 1, we have that

is non-decreasing in .

When is discrete, we need only to prove that, for ,

We have that

From the assumption and condition (1) in Theorem 5,

is non-decreasing in and . From condition (2) in Theorem 5, is non-decreasing in for all .

Therefore, we have .

Proof of Theorem 6.

For , we have from the assumption and condition (2) in Theorem 6 that is non-increasing in and . From condition (1) in Theorem 6, is non-decreasing in for all . Thus we have that .

Proof of Theorem 7.

Since , we prove that using a similar argument as in the proof of Theorem 5.

Proof of Corollary 3.

We prove this only for Theorem 5. Obviously, the assumption can be evaluated by . Condition (1) in Theorem 5 can be evaluated by , which can be obtained after marginalizing over . For conditions (2) and (3), we can rewrite them as and respectively. Therefore, the assumption and conditions can all be evaluated by .

Proof of Corollary 4. From the linear model, we have and . Thus, we have if , and are non-negative.

Suppose , and we need only to prove the result for the case that but . We use proof by contradiction, and suppose that for some . Then we have . Since , we have . From the linear model of , we have . We deduce that

| (2) |

Define . We have and . From Property 1, we get . Thus we obtain

| (3) |

From equations (2) and (3),

we have , which is impossible

since the correlation coefficient cannot be larger than .

Proof of Corollary 5. We first prove results (2) and (3). Since , and , we only need for Theorem 6 and for Theorem 7. For result (1), according to Theorem 4, when or is binary, the density association is equivalent to the expectation association, thus we need only .

References

-

Appleton, D. R., French, J. M. and Vanderpump, M. P. J. (1992). Ignoring a covariate: an example of Simpson’s paradox. Am. Stat. 50, 340–341.

-

Birch, M. W. (1963). Maximum likelihood in three-way contingency tables. J. Roy. Statist. Soc. Ser. B 25, 220–233.

-

Chen, H., Geng, Z. and Jia, J. (2007). Criteria for surrogate end points. J. Roy. Statist. Soc. Ser. B 69, 919–932.

-

Cochran, W. G. (1938). The omission or addition of an independent variate in multiple linear regression. Supp. J. Roy. Statist. Soc. 5, 171–176.

-

Cox, D. R. and Wermuth, N. (2003). A general condition for avoiding effect reversal after marginalization. J. Roy. Statist. Soc. Ser. B 48, 197–205.

-

Drton, M. (2009). Discrete chain graph models. Bernoulli 15, 736–753.

-

Frangakis, C. E. and Rubin, D. B. (2002). Principal stratification in causal inference. Biometrics 58, 21–29.

-

Ju, C. and Geng, Z. (2010). Criteria for surrogate end points based on causal distributions. J. Roy. Statist. Soc. Ser. B 72, 129–142.

-

Lněnička, R. and Matúš, F. (2007). On Gaussian conditional independence structures. Kybernetika 43, 323–342.

-

Pearl, J. and Bareinboim, E. (2011). Transportability of causal and statistical relations: A formal approach. Data Mining Workshops (ICDMW), 2011 IEEE 11th International Conference on IEEE, 540–547.

-

Prentice, R. L. (1989). Surrogate endpoints in clinical trials: definition and operational criteria. Stat. Med. 8, 431–440.

-

Roverato, A. (2013). Dichotomization invariant log-mean linear parameterization for discrete graphical models of marginal independence. arXiv:1302.4641.

-

Rubin, D. B. (2004). Direct and indirect causal effects via potential outcomes. Scand. J. Stat. 31, 161–170.

-

Toomet, O. and Henningsen, A. (2008). Sample selection models in R: package sample Selection. J. Stat. Softw. 27,

http://www.jstatsoft.org/v27/i07/. -

Tingley, D., Yamamoto, T., Keele, L. and Imai, K. (2012). mediation: R package for causal mediation analysis. R package version 4.2.

http://CRAN.R-project.org/package=mediation . -

Vanderweele, T. J. and Robins, J. M. (2009). Properties of monotonic effects on directed acyclic graphs. J. Mach. Learn. Res. 10, 699–718.

-

Vanderweele, T. J. and Robins, J. M. (2010). Signed directed acyclic graphs for causal inference. J. Roy. Statist. Soc. Ser. B 72, 111–127.

-

Vanderweele, T. J. and Tan, Z. (2012). Directed acyclic graphs with edge-specific bounds. Biometrika 99, 115–126.

-

Vinokur, A. and Schul, Y. (1997). Mastery and inoculation against setbacks as active ingredients in the jobs intervention for the unempllyed. J. Consult. Clin. Psych. 65, 867–877.

-

Wermuth, N. (2012). Traceable regressions. Int. Stat. Rev. 80, 415-438.

-

Whittaker, J. (1990). Graphical Models in Applied Multivariate Statistics. New York: John Wiley & Sons.

-

Xie, X., Ma, Z. and Geng, Z. (2008). Some association measures and their collapsibility. Statistica Sinica 18, 1165–1183.

School of Mathematical Sciences, Peking University, Beijing 100871, China E-mail: (zhichaojiang@pku.edu.cn)

Department of Statistics, Harvard University, Cambridge 02138, U.S.A. E-mail: (pengding@fas.harvard.edu)

Center for Statistical Science, School of Mathematical Sciences, Peking University, Beijing 100871, China E-mail: (zhigeng@pku.edu.cn)