A QUANTILE-BASED PROBABILISTIC

MEAN VALUE THEOREM

Abstract

For nonnegative random variables with finite means we introduce an analogous of the equilibrium residual-lifetime distribution based on the quantile function. This allows to construct new distributions with support , and to obtain a new quantile-based version of the probabilistic generalization of Taylor’s theorem. Similarly, for pairs of stochastically ordered random variables we come to a new quantile-based form of the probabilistic mean value theorem. The latter involves a distribution that generalizes the Lorenz curve. We investigate the special case of proportional quantile functions and apply the given results to various models based on classes of distributions and measures of risk theory. Motivated by some stochastic comparisons, we also introduce the ‘expected reversed proportional shortfall order’, and a new characterization of random lifetimes involving the reversed hazard rate function.

Short title: A quantile-based probabilistic mean value theorem.

1 Introduction

The quantile function, being the inverse of the cumulative distribution function of a random variable, is often invoked in applied probability and statistics. In certain cases the approach based on quantile functions is more fruitful than the use of cumulative distribution functions, since quantile functions are less influenced by extreme statistical observations. For instance, quantile functions can be properly employed to formulate properties of entropy function and other information measures for nonnegative absolutely continuous random variables (see Sunoj and Sankaran [22] and Sunoj et al. [23]). They are also employed in problems that ask for comparisons based on variability stochastic orders such as the dilation order, the dispersive order (see Shaked and Shanthikumar [20]) or the TTT transform order (cf. Kochar et al. [13]). In addition, several notions of risk theory and mathematical finance are expressed in terms of quantile functions (see, for instance, Belzunce et al. [2] and [3]).

In this paper we use the quantile functions in order to build some stochastic models and obtain various results involving distributions with support . We are motivated by previous researches in which the equilibrium distribution of nonnegative random variables plays a key role and allows to obtain probabilistic generalizations of Taylor’s theorem (see [14] and [16]) and of the mean value theorem (see [6]).

In Section 2 we present some preliminary notions on quantile function and Lorenz curve. Then, in Section 3 we obtain a probabilistic generalization of Taylor s theorem based on a suitably defined ‘quantile analogue’ of the equilibrium distribution, whose density is an extension of the Lorenz curve based on stochastically ordered random variables. Moreover, such distribution is involved in a quantile-based version of the probabilistic mean value theorem provided in Section 4. A special case dealing with proportional quantile functions is also discussed. Finally, various examples of applications are considered in Section 5: the first involves typical classes of distributions (NBU and IFR notions) and conditional value-at-risks; the second involves concepts of risk theory, as the proportional conditional value-at-risk; the third and the fourth applications are founded on distribution functions defined as suitable ratios of quantile functions, and involve the notion of average value-at-risk.

We point out that, aiming to obtain useful stochastic comparisons, in this paper we introduce two new concepts that deserve interest in the field of stochastic orders and characterizations of distributions. In Section 4 we propose the ‘expected reversed proportional shortfall order’, which is dual to a recently proposed stochastic order. In Section 5.3 we provide a new characterization of random lifetimes, expressed by stating that is decreasing for , where is the reversed hazard rate function.

Throughout the paper, denotes a random variable having the same distribution as conditional on , the terms decreasing and increasing are used in non-strict sense, and denotes the derivative of .

2 Preliminary notions

Given a random variable , let us denote its distribution function by , , and its complementary distribution function by , . The quantile function of , when existing, is given by

| (1) |

Moreover, if is differentiable, the quantile density function of is given by

| (2) |

Definition 1

A random variable in is thus nonnegative and may represent a distribution of interest in actuarial applications or in risk theory, such as an income or a loss. If , it has finite nonzero mean, and the function

| (3) |

denotes the Lorenz curve of . If the individuals of a given population share a common good such as wealth, which is distributed according to , then gives the cumulative share of individuals, from the lowest to the highest, owing the fraction of the common good. Hence, is often used in insurance to describe the inequality among the incomes of individuals. See, for instance, Singpurwalla and Gordon [21] and Shaked and Shanthikumar [19] for various applications of the Lorenz curve and its connections with stochastic orders.

It is well known that (3) is the distribution function of an absolutely continuous random variable, say , taking values in . In the following proposition we express the mean of an arbitrary function of in terms of the quantile function (1). To this aim we recall that if is an integrable function then, for all ,

| (4) |

Proposition 1

Let and let have distribution function . If is such that is integrable in , then

| (5) |

or, equivalently,

where is uniformly distributed in .

-

Proof.

Since has distribution function , the proof follows from identity , , and from Eq. (4) for and .

As an immediate application of Proposition 1 we have that the moments of , when existing, are given by:

| (6) |

Remark 1

Let , , . Then, is identically distributed to if, and only if, is equal to the reciprocal of the golden number, i.e. .

3 An analogous of Taylor’s theorem

It is well-known that the equilibrium distribution arises as the limiting distribution of the forward recurrence

time in a renewal process. Its role in applied contexts has been largely investigated (see, as example,

Gupta [10] and references therein). For instance, we recall that the iterates of equilibrium

distributions have been used

- to characterize family of distributions (see Unnikrishnan Nair and Preeth [24]),

- to construct sequences of stochastic orders (see Fagiuoli and Pellerey [8]),

- to determine properties related to the moments of random variables of interest in risk theory

(see Lin and Willmot [15]).

Moreover, a probabilistic generalization of Taylor’s theorem (studied by Massey and Whitt [16] and Lin [14]) allows to express the expectation of a functional of random variable in terms of suitable expectations involving the iterates of its equilibrium distribution.

We recall that for a random variable the density of the equilibrium distribution of and the density of are given respectively by

| (7) |

On the ground of the analogy between such densities, in this section we obtain an analogous of the probabilistic generalization of Taylor’s theorem which involves .

Theorem 1

Let ; if is a differentiable function such that is integrable on , then

| (8) |

where is uniformly distributed in .

- Proof.

Example 1

Let have Lomax distribution, with quantile function , , and mean , for and . Then, under the assumptions of Theorem 1 we have

where has density , .

Hereafter we extend the result of Theorem 1 to a more general case, in which the right-hand-side of (8) is expressed in an alternative way. Let denote the -th derivative of , for , and let .

Theorem 2

Let ; if is -times differentiable and is integrable on , for any , then

| (9) |

where is uniformly distributed in .

- Proof.

Corollary 1

-

Proof.

The proof follows from Theorem 2 by setting , .

4 An analogous of the mean value theorem

A suitable transformation investigated in Section 3 of Di Crescenzo [6] allows to construct new probability densities via differences of (complementary) distribution functions of two stochastically ordered random variables. We now aim to construct similarly new densities from differences of quantile functions, thus extending (3) to a more general case. This allows us to obtain a quantile-based version of the probabilistic mean value theorem, given in Theorem 3 below.

Let us recall some useful definitions of stochastic orders (see, for instance,

Shaked and Shanthikumar [20]). To this purpose, we denote by and the

quantile functions of two random variables and , defined as in Eq. (1).

We say that is smaller than

in the usual stochastic order (denoted by ) if

for all non-decreasing functions for which the expectations exist, or equivalently if

for all , i.e. for all ;

in the hazard rate order (denoted by ) if

is decreasing in ;

in the reversed hazard rate order (denoted by ) if

is decreasing in ;

in the likelihood ratio order (denoted by ) if

is decreasing in ;

in the star order (denoted by ) if is decreasing in

(see Section 4.B of Shaked and Shanthikumar [20]);

in the expected proportional shortfall order (denoted by ) if

is decreasing in (see

Belzunce et al. [2] for some equivalent conditions for this order).

The following result is analogous to Proposition 3.1 of Di Crescenzo [6].

Proposition 2

Let and be random variables taking values in , and such that . Then

| (12) |

is the probability density function of an absolutely continuous random variable taking values in if, and only if, .

-

Proof.

The proof immediately follows from the definition of the usual stochastic order.

We remark that, due to , the densities and are respectively monotonic decreasing and increasing, whereas density (12) is not necessarily monotonic. We also note that can be expressed as a linear combination of two densities. Indeed, under the assumptions of Proposition 2, for we have

| (13) |

Note that can be negative, in particular if and only if , and if and only if .

Remark 2

Let

be the distribution function corresponding to density (12). This is a suitable extension of the Lorenz curve (3). Indeed, assume that the individuals of a certain population share a common good such as wealth, distributed according to . Suppose that the income received by the individuals is subject to losses due to various reasons (e.g. taxes, faults, damages, etc.), distributed according to . Hence, is the net income received by the poorest fraction of the population, and thus gives the portion of the net wealth held by a portion of the population. Note that is not necessarily increasing, and thus generally it is not a quantile function.

Let us now introduce the operator on the set of all pairs of random variables and defined as in Proposition 2, such that denotes an absolutely continuous random variable having density (12). Hence, the random variable has distribution function (3), and the distribution of is similarly defined.

Example 2

(i) Let and be exponentially distributed with parameters and ,

respectively, with .

Then, is exponentially distributed with parameter 1.

(ii) Let and be uniformly distributed in and , respectively,

with .

Then, is uniformly distributed in .

Aiming to focus on some stochastic comparisons, we now introduce a new stochastic order based on the quantile function, which is dual to the expected proportional shortfall order.

Definition 2

We say that is smaller than in the expected reversed proportional shortfall order (denoted by ) if is decreasing in .

Results and properties of such an order go beyond the scope of this article, and thus will be the object of future investigation. The proof of the following results follows from the definitions of the involved notions and some straightforward calculations, and thus is omitted.

Proposition 3

Under the assumptions of Proposition 2, for ,

and we have:

(i) If , then and .

(ii) If , then and .

(iii) If , then and .

(iv) The following conditions are equivalent:

,

,

.

According to (2), hereafter and denote respectively the quantile density functions of and . The next result can be viewed as a quantile-based analogue of the probabilistic mean value theorem given in Theorem 4.1 of Di Crescenzo [6].

Theorem 3

Let and such that . Moreover, let be a differentiable function, and let and be integrable on . Then, for we have that is finite, and

| (14) |

where is uniformly distributed in .

As example, under the assumptions of Theorem 3, for , , we have:

In particular, when we get the indentity

which does not depend on .

4.1 Proportional quantile functions

Let have proportional quantile functions. For instance (see Escobar and Meeker [7]) such assumption leads to a scale-accelerated failure-time model. Let

| (15) |

with , , where is a suitable increasing and differentiable function such that is finite and . In other terms, and belong to the same scale family of distributions, with

Proposition 4

The random variables and are identically distributed if, and only if, and have proportional quantile functions as specified in (15).

-

Proof.

Since the distribution function of is given by (3), the proof thus follows.

Proposition 5

If the quantile functions of and are proportional as expressed in Eq. (15), with , then . Moreover, is identically distributed to and , with density , , and the following equality holds:

| (16) |

where is uniformly distributed in , and is a differentiable function.

We remark that the variables considered in Example 2 satisfy the assumptions of Proposition 5. Other cases are shown hereafter.

Example 3

(i) Let and have the following distribution functions, with :

If , then the assumptions of Proposition 5 are satisfied.

Hence, Eq. (16) holds, with , , and

, so that has density

, .

(ii) Let and have Pareto (Type I) distribution, with

for . If and if , then the hypotheses of Proposition 5 hold. Relation (16) is thus fulfilled, with , , and , by which has density , .

5 Applications

Let us now analyse various applications of the results given in the previous section.

5.1 Classes of distributions

Among the classes of probability distributions, wide attention is given to the following notions. Let be a nonnegative random variable; then

-

(i)

is NBU (new better that used) for all , i.e. for all and ,

-

(ii)

is IFR (increasing failure rate) for all , i.e. is logconcave,

where , for . The above notions can be expressed also in terms of the quantiles. Consider the residual of evaluated at , i.e.

| (17) |

In risk theory describes the losses exceeding . Indeed, in a population of losses distributed as , then denotes the residual of a loss whose level is equal to the th quantile, for . If has a strictly increasing quantile function , then

-

(i)

is NBU for all ,

-

(ii)

is IFR for all and .

It is worth noting that comparisons of variables defined as in (17) allow to define the lr-order of the dispersion type (see Belzunce et al. [1]). We recall that, if , the conditional value-at-risk of is given by (see Belzunce et al. [2], or Denuit et al. [5]):

| (18) |

with . (Note that in the literature some authors give different definitions for the conditional value-at-risk.) In the context of reliability theory the function given in (18) is also named ‘mean residual quantile function’, since

where is the mean residual life of a lifetime evaluated at age . Furthermore, we point out that the conditional value-at-risk is also related to the right spread function of through the following identity: (see, for instance, Fernandez-Ponce et al. [9] for several results on ). Finally, the integral in the right-hand-side of (18) is known as the ‘excess wealth transform’, and plays an essential role in the excess wealth order (cf. Section 3.C of [20]).

Remark 3

Given two nonnegative random variables and , one has for all if and only if the proportional quantile functions model holds as specified in (15).

Let us now provide a result involving NBU random variables.

Proposition 6

Let be NBU and such that for all . If is a differentiable function, and if is uniformly distributed in , then for all we have

| (19) |

where has density

- Proof.

We remark that the quantile function given in (20) is often used to model reliability data, since it represents the th percentile residual life expressed in terms of quantile, as shown in Eq. (2.7) of Unnikrishnan Nair and Sankaran [25].

In the line of Proposition 6 we now provide a similar result for IFR random variables.

Proposition 7

Let be IFR and such that is strictly decreasing for . Then, for all we have

| (21) |

where is uniformly distributed in , and has density

| (22) |

-

Proof.

Since is IFR, we have for all . The proof thus proceeds similarly as Proposition 6.

Example 4

Let , where , , are independent, identically -distributed random variables, and where is a geometric random variable independent of , , and with parameter . Then, is IFR (see Example 7.2 of Ross et al. [18]). Its quantile function and quantile density are respectively given by

From (18) we see that the conditional value-at-risk of is:

We note that is strictly decreasing in . Hence, from Proposition 7 we have, for ,

| (23) |

where is uniformly distributed in . The density of can be obtained from (22) and the above given expressions.

We remark that Propositions 6 and 7 provide identities holding for specific ranges of the involved parameters. However, a ‘local version’ of such results can be easily stated under mild assumptions. For instance Eq. (19) holds for a fixed , provided that and for such fixed . An example in which these conditions hold for some is provided when is the maximum of two independent exponential distributions with unequal parameters, whose distribution is IFRA (increasing failure rate in average) and thus NBU, but not IFR (see, for instance, Klefsjö [12]).

5.2 Risks

When comparing risks, the quantile function of plays a very important role. In fact, in this context it is known as value-at-risk and is denoted by , . However, to avoid discrepancies we adopt the notation . Given a nonnegative random variable with finite mean, we define

| (24) |

for all . The random variable is useful to compare risks of different nature, and can be viewed as proportional conditional value-at-risk because it measures the conditional upper tail from on, but proportional to . Moreover, from (17) and (24) we have for all . Hence, Eqs. (18) and (24) yield

| (25) |

In this case, we can consider conditions similar to NBU and IFR properties which are defined in terms of (24):

-

(i)

for all for all and .

-

(ii)

for all for all and .

Proposition 8

Let be such that and for all . If is a differentiable function and if is uniformly distributed in , then for all we have

| (26) |

where is a random variable with density function

- Proof.

An extension of Proposition 8 to a more general case is given hereafter. The proof is analogous, and then is omitted.

Proposition 9

Let be such that and is strictly decreasing for all . If is a differentiable function and if is uniformly distributed in , then for all such that we have

| (27) |

where is a random variable having density function

| (28) |

Example 5

Let have Rayleigh distribution, , , with . Hence, the quantile function and the quantile density of are:

Due to (18) the conditional value-at-risk of is given by

where denotes the complementary error function. It is not hard to verify that is strictly decreasing in . Moreover, since is IFR, from Proposition 7 we have, for all ,

| (29) |

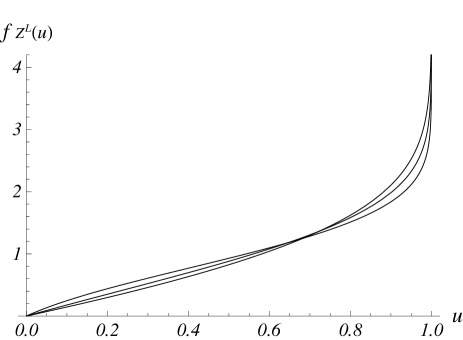

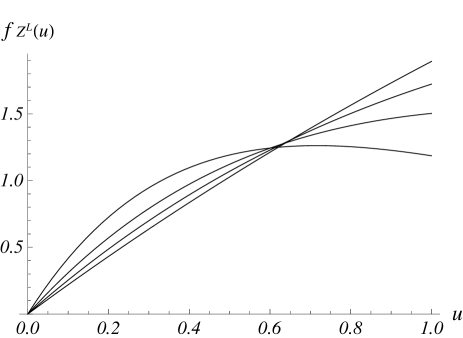

where is a differentiable function, is uniformly distributed in , and the density of can be obtained from (22). Furthermore, is strictly decreasing in . Hence, Proposition 9 yields the following indentity, for ,

| (30) |

In this case, owing to (28), for the density of is

| (31) |

We remark that such density does not depend on . Some plots of (31) are given in Figure 1.

5.3 A model involving the average value-at-risk

Let have quantile function . One can introduce a new family of random variables , , having distribution function

If represents a risk, the average value-at-risk of is defined as

| (32) |

Note that the risk measure given in (32) represents the conditional expected loss given that the loss is less than its value-at-risk. See Chapter 6 of Rachev et al. [17] for results, properties and applications in mathematical finance of . The average value-at-risk plays a significant role also in stochastic orders of interest in risk theory (see Jewitt [11]). In addition, can be viewed as the L-moment of order 1 of the reversed quantile function (see Unnikrishnan Nair and Vineshkumar [26]).

We can easily show that the mean of can be expressed in terms of as

| (33) |

Then, we have the following result, where denotes the density of .

Proposition 10

Let be such that for , and is strictly decreasing in . If is a differentiable function and if is uniformly distributed in , then for all we have

| (34) |

where is a random variable with density function

- Proof.

Let us now provide an equivalent condition for , , which was considered in Proposition 10.

Proposition 11

Let . Then, for if, and only if, is decreasing for , where is the reversed hazard rate function of .

-

Proof.

Given , we have if, and only if, for all . Hence, due to the first of (35), this property is equivalent to the following condition:

(36) Since , , condition (36) holds if, and only if,

By differentiation we see that this condition is satisfied if, and only if, for all and . Finally, by setting , with , we obtain , this giving the proof.

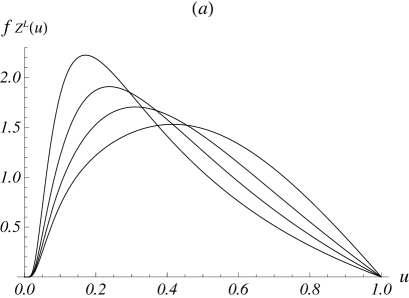

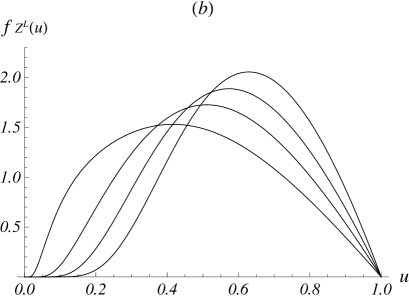

Example 6

Let have distribution function , , with . In this case, and thus is decreasing. Moreover, from (32) we have , where is the incomplete gamma function. Hence, recalling Proposition 11, the assumptions of Proposition 10 are satisfied. For instance, by setting for simplicity , for all we have

where is the logarithmic integral function. Moreover has density function

| (37) |

Some plots of are given in Figure 2.

Hereafter we show an example of distribution function that does not satisfy the conditions of Proposition 11.

5.4 A model based on increasing variables

Let have density and quantile function . We now consider a random variable , , with support and distribution function

| (38) |

From (38) it is not hard to see that

| (39) |

where is the average value-at-risk defined in (32).

Proposition 12

Let . If is a differentiable function and if is uniformly distributed in , then for all we have

| (40) |

where is a random variable with density function

-

Proof.

From (38) it is easy to see that the quantile function and the quantile density of , , are respectively given by

Note that is stochastically increasing in , since for all . Moreover, the given assumptions ensure that the mean (39) is strictly increasing in . The proof thus follows from Proposition 2 and Theorem 3.

Example 7

5.5 Concluding remarks

In our view, the main issues of this paper are given in Proposition 2 and Theorem 3. The first result allows us to construct new probability densities with support starting from suitable pairs of stochastically ordered random variables. The second result is useful to obtain equalities involving uniform- distributions and quantile functions. The cases treated in this section give only a partial view of the potentiality of Theorem 3. Indeed, we considered some special cases in which the random variables and involved in Theorem 3 belong to the same family of distributions. Other useful applications are likely to be developed under various choices of such variables, and specific selection of function . This will be the object of future research.

Acknowledgements

The research of A. Di Crescenzo and B. Martinucci has been performed under partial support by GNCS-INdAM and Regione Campania (Legge 5). J. Mulero is supported by project MTM2012-34023, “Comparación y dependencia en modelos probabilísticos con aplicaciones en fiabilidad y riesgos”, from Universidad de Murcia.

References

- [1] Belzunce, F., Hu, T., & Khaledi, B.E. (2003). Dispersion-type variability orders. Probability in the Engineering and Informational Sciences 17: 305–334.

- [2] Belzunce, F., Pinar, J.F., Ruiz, J.M., & Sordo, M.A. (2012). Comparison of risks based on the expected proportional shortfall. Insurance: Mathematics and Economics 51: 292–302.

- [3] Belzunce, F., Pinar, J.F., Ruiz, J.M., & Sordo, M.A. (2013). Comparison of concentration for several families of income distributions. Statistics and Probability Letters 83: 1036–1045.

- [4] Block, H.W., Savits, T.H., & Singh, H. (1998). The reversed hazard rate function. Probability in the Engineering and Informational Sciences 12: 69–90.

- [5] Denuit, M., Dhaene, J., Goovaerts, M., & Kaas, R. (2005). Actuarial Theory for Dependent Risks. Measures, Orders and Models. John Wiley & Sons, Chichester.

- [6] Di Crescenzo, A. (1999). A probabilistic analogue of the mean value theorem and its applications to reliability theory. Journal of Applied Probability 36: 706–719.

- [7] Escobar, L.A. & Meeker, W.Q. (2006). A review of accelerated test models. Statistical Science 21: 552–577.

- [8] Fagiuoli, E. & Pellerey, F. (1993). New partial orderings and applications. Naval Research Logistics 40: 829–842.

- [9] Fernandez-Ponce, J.M., Kochar, S.C., & Muñoz-Perez, J. (1998). Partial orderings of distributions based on right-spread functions. Journal of Applied Probability 35: 221–228.

- [10] Gupta, R.C. (2007). Role of equilibrium distribution in reliability studies. Probability in the Engineering and Informational Sciences 21: 315–334.

- [11] Jewitt, I. (1989). Choosing between risky prospects: the characterization of comparative statics results, and location independent risk. Management Science 35: 60–70.

- [12] Klefsjö, B. (1983). Some tests against aging based on the total time on test transform. Communications in Statistics Theory and Methods 12: 907–927.

- [13] Kochar, S.C., Li, X. & Shaked, M. (2002). The total time on test transform and the excess wealth stochastic orders of distributions. Advances in Applied Probability 34: 826–845.

- [14] Lin, G.D. (1994). On a probabilistic generalization of Taylor’s theorem. Statistics and Probability Letters 19: 239–243.

- [15] Lin, X.S. & Willmot G.E. (2000). The moments of the time of ruin, the surplus before ruin, and the deficit at ruin. Insurance: Mathematics and Economics 27: 19–44.

- [16] Massey, W.A. & Whitt, W. (1993). A probabilistic generalization of Taylor’s theorem. Statistics and Probability Letters 16: 51–54.

- [17] Rachev, S.T., Stoyanov, S.V., & Fabozzi, F.J. (2011). A Probability Metrics Approach to Financial Risk Measures. Wiley-Blackwell, Chichester, UK.

- [18] Ross, S.M., Shanthikumar, J.G., & Zhu, Z. (2005). On increasing-failure-rate random variables. Journal of Applied Probability 42: 797–809.

- [19] Shaked, M. & Shanthikumar, J.G. (1998). Two variability orders. Probability in the Engineering and Informational Sciences 12: 1–23.

- [20] Shaked, M. & Shanthikumar, J.G. (2007). Stochastic Orders. Springer Series in Statistics. Springer, New York.

- [21] Singpurwalla, N.D. & Gordon, A.S. (2014). Auditing Shaked and Shanthikumar’s ‘excess wealth’. Annals of Operations Research 212: 3–19.

- [22] Sunoj, S.M. & Sankaran, P.G. (2012). Quantile based entropy function. Statistics and Probability Letters 82: 1049–1053.

- [23] Sunoj, S.M., Sankaran, P.G., & Nanda, A.K. (2013). Quantile based entropy function in past lifetime. Statistics and Probability Letters 83: 366–372.

- [24] Unnikrishnan Nair, N. & Preeth, M. (2009). On some properties of equilibrium distributions of order . Statistical Methods and Applications 18: 453–464.

- [25] Unnikrishnan Nair, N. & Sankaran, P.G. (2009). Quantile-based reliability analysis. Communications in Statistics Theory and Methods 38: 222–232.

- [26] Unnikrishnan Nair, N. & Vineshkumar, B. (2010). -moments of residual life. Journal of Statistical Planning and Inference 140: 2618–2631.