Intensity Process for a Pure Jump Lévy Structural Model with Incomplete Information

Abstract In this paper we discuss a credit risk model with a pure jump Lévy process for the asset value and an unobservable random barrier. The default time is the first time when the asset value falls below the barrier. Using the indistinguishability of the intensity process and the likelihood process, we prove the existence of the intensity process of the default time and find its explicit representation in terms of the distance between the asset value and its running minimal value. We apply the result to find the instantaneous credit spread process and illustrate it with a numerical example.

Keywords Pure jump Lévy process, unobservable random barrier, first passage time, path-dependent intensity process.

Mathematics Subject Classification (2010) 60J75, 60G55, 91G40

1 Introduction

The structural model and the intensity model are two frameworks in credit risk modelling. The structural model is based on the asset-liability structure of a firm and is economically meaningful. The default time is defined as the first time the asset value process falls below the default threshold. One needs to investigate the law of the first passage time or equivalently the running minimal process. The intensity form model is based on the the fact that default happens as a surprise to the market and default time is a totally inaccessible stopping time under a certain filtration. One models directly the intensity process that determines the default indicator process and the short-term spread of credit derivatives such as defaultable bonds and credit default swaps.

The key difference of the two models is the difference of the information sets or filtrations, see Jarrow and Protter [11]. If the asset value process is continuous and the barrier is deterministic in a structural model with complete information, then the first passage time is a predictable stopping time and does not admit an intensity process under the natural filtration. In reality, it is difficult to observe the complete information of the asset value process and the default barrier. There has been active research in the literature on the filtration expansion and its applications in the structural model with incomplete information, see Guo and Zeng [9] and Janson et al. [10].

There are two main ways of introducing the incomplete information in the first passage time model in the literature. One is to assume the incomplete information about the value process and the constant barrier. Duffie and Lando [6] discuss for a discretely observable noisy value process and find the corresponding intensity process . Kusuoka [13] extends [6] to a continuously observable noisy value process. Çetin et al. [4] derive the intensity process with the Aézma martingale and the information reduction method. The other is to assume the observable asset value process but the incomplete information on the random barrier. Giesecke [7] introduces an unobservable random barrier and concludes that if the asset value is a diffusion process then the default time is a totally inaccessible stopping time under the market information filtration but does not admit an intensity process.

In this paper we focus on the first passage time problem of a structural model for a Lévy process with finite variation and with incomplete information of the barrier. Pure jump processes are important in financial modelling as they can capture the phenomenon of infinite activities, jumps, skewness and kurtosis. For example, Madan et al. [15] use a variance gamma process for the stock price in option pricing. Madan and Schoutens [18] use a drifted subordinator for the log firm value process in a first passage time model with complete information.

In the incomplete information setup the essential mathematical quantity needed is the conditional default probability. All results in the literature on the existence of the intensity process are based on the absolute continuity of the conditional default probability and the close link between the conditional default density and the intensity. In case of pure jump processes the conditional default probability is discontinuous at the time when the asset value process reaches a new minimal and the conditional default density does not exist. This is reasonable as one would expect the conditional default probability jumps when there is a large movement of the asset value process. The main mathematical difficulty, unlike the continuous case in which the compensator of the conditional default probability is itself, is to find the compensator due to the unpredictability of the stopping time.

The objective of the paper is to show that the structural model of a pure jump Lévy process with an unobservable random barrier can be embedded into an equivalent intensity model. The key contribution of the paper is to show the existence of the intensity process and find its explicit form for a pure jump Lévy process in an incomplete information framework, which sheds the new light to the relation between the intensity process of the default time and the running minimal process of the asset value. We apply the result to find the instantaneous credit spread process that remains positive and finite, which conforms to the market observations, and that depends on the historical path of the asset value.

2 The Model and the Main Result

Let be a probability space and be an observable firm asset value process given by at time , where is a Lévy process with finite variation and . Examples include drifted subordinators, variance gamma and normal inverse Gaussian processes. Note that can be decomposed as ([14, Exercise 2.8])

| (1) |

where and , are independent pure jump subordinators with Lévy measures , , respectively, see [14, Lemma 2.14] for the definition and the properties of a subordinator. Denote by the natural filtration generated by . We assume the following assumption be satisfied in the paper:

Assumption 2.1.

Lévy measure is continuous and satisfies .

Assume that the firm defaults at the first time when the asset value is below a default threshold, i.e., the default time is defined by

where is an unobservable default barrier of the company. Assume that is a uniform variable on the interval and is independent of . Then the barrier for is a standard negative exponential variable, i.e., is a standard exponential variable, with the distribution function for , and is independent of . Note that the default barrier is unobservable but the default time is observable, we therefore define a progressive filtration expansion by ([16, Chapter VI, Section 3])

| (2) |

The default time is now a -stopping time. All filtrations involved are assumed to satisfy the usual condition.

Denote by the default indicator process, defined by . The Doob-Meyer decomposition theorem implies that there exists a unique increasing predictable process with , called the -compensator of , such that is a -martingale. If is continuous a.s. then -stopping time is totally inaccessible. If is absolutely continuous a.s. with respect to the Lebesgue measure and can be written as a.s., where is nonnegative and -progressively measurable, then is called the intensity process of , see [3] for details on compensators and intensity processes.

Denote by . If admits a Lévy density , then . We can now state the main result of the paper.

Theorem 2.2.

Let be a Lévy process with finite variation and Assumption 2.1 be satisfied. Then the -compensator of the default indicator process is absolutely continuous a.s. and the intensity process of is indistinguishable with the instantaneous likelihood process on . Moreover, using the same notation as in (1), the intensity process has the following representation

| (3) |

where is the running minimal process of and

| (4) |

Theorem 2.2 shows that the intensity process is an endogenous process that depends on the path of the asset value process . Moreover, at each time , is a decreasing function of , a financially desirable property as it means that the default intensity increases when the asset value process approaches its historical minimal level.

We next give several examples to illustrate Theorem 2.2.

Example 2.3.

(Drifted Compound Poisson Process) Let be given by

where , and are exponential variables with parameters and , respectively, and are Poisson processes with intensities and , respectively, and , , , are independent of each other. The Lévy density of on is given by . The intensity process of the default indicator process is then given by Theorem 2.2 as

Example 2.4.

(Drifted Gamma Process) Let be given by

where , is a gamma process with the mean rate , the variance rate , and the Lévy density . The intensity process of is given by

Note that in this case, hence the first term in (3) disappears.

Example 2.5.

(Variance Gamma Process [15]) Let be a variance gamma process that is generated by a drifted Brownian motion , time-changed by a gamma process , and an additional drift term , then

| (5) |

where , and . The intensity process of is given by

| (6) |

We next provide an application of Theorem 2.2 in credit risk modelling. The credit spread of a defaultable name over the time interval is defined by

where is the conditional default probability given . Using the Taylor expansion, we can find the instantaneous credit spread as

Theorem 2.2 says that is positive and finite almost surely and is given by

which conforms to the market observation that the instantaneous credit spread remains positive and finite even though the bond is near its maturity and that the bond price often drops around the time of default due to uncertainties about the closeness of the current asset value to the default threshold. For more details of the instantaneous credit spread and its term structure, see [6, 7].

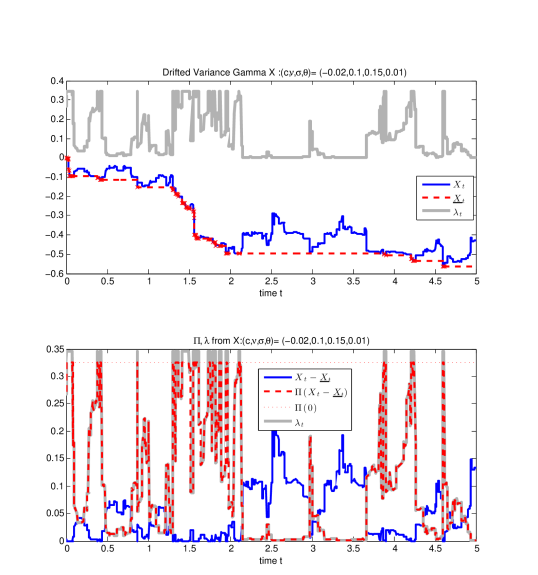

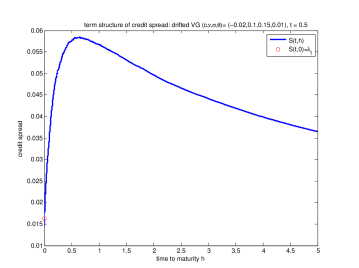

We next give a numerical example to illustrate the results. We take the variance gamma process in Example 2.5. The data used are . Figure 2.1 displays for a sample path of the asset return process , the running minimal process and the resulting intensity process . Figure 2.1 also shows the distance and its contribution to the intensity. We can observe the reciprocal relation of the intensity and the distance , which is consistent with the observation in the credit market. Note that on is bounded above by that is fully determined by the Lévy measure of . The upper bound is reached when , i.e. the process reaches a new minimal level, and the intensity at that time is above by the amount as the drift parameter . Figure 2.2, using the same sample path of Figure 2.1, shows the term structure of the credit spread at time , starting from .

3 Proof of Theorem 2.2

Theorem 2.2 is proved in four steps, detailed in the following subsections. Subsection 3.1 shows the relation of the likelihood processes under different filtration (Lemma 3.2), Subsections 3.2 and 3.3 establish the existence of the limit process for a spectrally negative Lévy process with finite variation (Proposition 3.8) and for a general Lévy process with finite variation (Proposition 3.11), and Subsection 3.4 confirms the indistinguishability of the instantaneous likelihood process and the intensity process using Aven’s condition.

3.1 Compensators and Likelihood Processes under Different Filtrations

The conditional survival probability at each time is given by

It is known ([16, Chapter VI, Theorem 11]) that there exists a unique, increasing, -predictable process , the -compensator of , such that the difference of and is a uniformly integrable -martingale. Our objective is to find .

Let and . Define a nondecreasing -predictable process by

where is the unique, increasing, -predictable compensator of -submartingale .

Theorem 3.1 ([12]).

The process is a -martingale, where .

Theorem 3.1 shows that one can transform the problem of finding the -compensator of into the problem of finding the -compensator of . If is a continuous process, then and . If is discontinuous, then finding is nontrivial, see [9].

The next result characterizes the likelihood processes under different filtrations.

Lemma 3.2.

For any Lévy process , , denote

Then,

| (7) |

Proof.

Since

we have

where the last equality comes from the independent and stationary increment property of Lévy process and adaptedness of and in . Since is the -compensator of , the Doob-Meyer decomposition says that

Combining the above gives in (7).

Next, by the optional projection theorem (Theorem 14, Chap.VI, [16] and [7]), we know that if a random variable is nonnegative and integrable, then for each , the right continuous version of is given by

| (8) |

Therefore, using the tower property of the expectation and the fact that is a -compensator of , we have

This gives in (7).∎

The next result follows immediately from Lemma 3.2.

Corollary 3.3.

Assume that exists for all a.s., then the instantaneous likelihood process on is given by

Remark 3.4.

Note that in (8) is measurable by definition. Indeed, since and are random variables on , then is -measurable. To show it is measurable, it is equivalent to show . Note that

Since for all , we can take , such that

Therefore, we have .

3.2 Spectrally Negative Lévy Process with Finite Variation

Let be a spectrally negative Lévy process with finite variation, then has a representation [14, page 56]

| (9) |

where and is a pure jump subordinator with Lévy measure . (9) is a special case of (1) with and . The Lévy measure of is on and if admits a density then . The following concept is needed in analysing the path property of .

Definition 3.5 ([14]).

Let be a Lévy process. A point is said to be irregular for an open or closed set if , where the stopping time .

We know ([5, Chapter 9, Proposition 15]) that for defined in (9), is irregular for . Hence, starting at , it takes strictly positive time to reach . If we define , then . is the first jump time of but may not be the first jump time of . We observe that is a pure-jump process as can only move when jumps and cannot jump to a pre-specified level on as can not, see [14, Exercise 5.9]. Hence, the jump size of has no atoms and is strictly negative. The number of jumps of on the interval , i.e., , is a discrete set and is a.s. finite. Moreover, we denote the arrival times of by , the inter-arrival times by , and the jump sizes by . Then we have the following lemma.

Lemma 3.6.

Proof.

The analysis above shows that is a non-explosive marked point process and can be written as , where . Since are also jump times of Lévy process and are stopping-times. We have that are i.i.d. random variables due to the strong Markov property of . ∎

Instead of investigating the exact law of , we only need to analyse the small-time behaviour of the process, which can be done with the help of the next result, called the Ballot Theorem [2, Proposition 2.7].

Lemma 3.7 ([2]).

Hence the joint distribution of is given by

| (10) |

for . The following is another version of the Ballot theorem:

for every and . Since , we have

Note as a.s., we have for almost all , there exists , such that for all , , hence and

| (11) |

The dominated convergence theorem leads to

| (12) |

Proposition 3.8.

Proof.

Recall that is a renewal-reward process, where jump size and inter-arrival times are positive random variables for all , and are i.i.d. random variables.

Denote by, for and ,

We have

Since is a pure jump subordinator, we have ([14, Lemma 4.11]) , which implies

| (15) |

Using (15) and (11), the dominated convergence theorem, continuity of , and , we obtain

Taking the limit in (3.2) gives

Here we have used the fact that if is a nonnegative function and , then

and

Remark 3.9.

Note that is continuous as is. is the Laplace exponent of from the Lévy-Khintchine formula, and for all by Assumption 2.1. Therefore, is bounded on

3.3 Lévy Process with Finite Variation

Suppose is a Lévy process with finite variation. It then has a representation (1) and we assume that Assumption 2.1 holds. Note that the path properties and techniques used in Subsection 3.2 no longer hold. In (1), denote the drift and negative jump components as

Then we first claim the following result for .

Lemma 3.10.

Proof.

For the limit (16) has been proved in the previous subsection. We now consider the case of . Note that is decreasing in and . We split the proof into two cases.

(i) : We have

Proposition 3.11.

Proof.

The expression of in (18) is an immediate result of Corollary 3.3 and (17). To prove (17) we only need to show that for all ,

| (19) |

Take any , on the set we have:

which yields

Moreover, as for all , we have almost surely,

We have

The last equality is due to the independence of and . Since a.s., which implies , we have

Let in the above inequality, we obtain

We have proved (19). ∎

Remark 3.12.

Note that if is a Lévy process with a Lévy measure and is a bounded continuous function that vanishes in a neighbourhood of zero, then ([17, Corollary 8.9])

| (20) |

In our case, we aim to compute

However, we cannot apply (20) directly as is not a Lévy process if is not a monotone process. Proposition 3.11 can be viewed as an extension for function and Lévy process with finite variation.

3.4 Indistinguishability of Likelihood Process and Intensity Process

We have proved the existence of the instantaneous likelihood process when is a Lévy process with finite variation. Heuristically the intensity process of the -compensator should be equal to on the set . However, they are not necessarily the same.

Example 3.13 ([8]).

Define a stopping time where is a Brownian motion and is a constant. Suppose is the natural filtration of . We have is a -stopping time and

I.e., for all . As is predictable under , the compensator of is , which indicates the intensity does not exist.

Aven’s condition in the next lemma provides a sufficient condition that ensures and are indistinguishable.

Lemma 3.14 ([1]).

If exists and is uniformly bounded for and , then on , is a -martingale, i.e., is the -compensator of .

With the help of the results of previous subsections, we can now present the proof of the main theorem.

Proof of Theorem 2.2. Recall (7) that on

and , and , which implies and , we have

Hence the sequence is uniformly bounded in and a.s., Lemma 3.14 gives the required conclusion that and are indistinguishable on , which leads to the expression of from Proposition 3.11. The proof of Theorem 2.2 is now complete.

Remark 3.15.

Similarly, is also bounded and with a similar argument as Aven’s condition due to the Meyer’s Laplacian approximation theorem, we can conclude that the -compensator of is where .

4 Conclusions

In this paper we discuss the intensity problem of a random time that is the first passage time of a finite variation Lévy process on a random barrier. We prove the existence of the intensity process and find its explicit representation. We compute the instantaneous credit spread process explicitly and give a numerical example for a variance gamma process to illustrate the relation between the credit spread and the distance of the asset value to its running minimal value. We thus reconcile the structural model with incomplete information and the path-dependent intensity model in this setup.

Acknowledgements. The authors thank the anonymous reviewer and the AE for their comments and suggestions that have helped to improve the previous version. Xin Dong also thanks Benoit Pham-Dang for useful discussions.

References

- [1] T. Aven, A theorem for determining the compensator of a counting process, Scandinavian J. Statistics 12 (1985) 69–72.

-

[2]

J. Bertoin,

Subordinators, Lévy Processes with No Negative Jumps, and

Branching Processes, Université

Pierre et Marie Curie, 2000.

http://webdoc.sub.gwdg.de/ebook/e/2002/maphysto/publications/mps-ln/2000/8.pdf - [3] P. Brémaud, Point Processes and Queues: Martingale Dynamics, Springer, 1981.

- [4] U. Çetin, R. Jarrow, P. Protter, Y. Yildirim, Modeling credit risk with partial information, Annals of Applied Probability 14 (2004) 1167–1178.

- [5] R. Doney, Fluctuation theory for Lévy processes, Springer, 2001.

- [6] D. Duffie, D. Lando, Term structures of credit spreads with incomplete accounting information, Econometrica 69 (2003) 633–664.

- [7] K. Giesecke, Default and information, J. Economic Dynamics and Control, 30 (2006) 2281–2303.

- [8] X. Guo, R. A. Jarrow, Y. Zeng, Credit risk models with incomplete information, Math. Operations Research 34 (2009) 320–332.

- [9] X. Guo, Y. Zeng, Intensity process and compensator: a new filtration expansion approach and the Jeulin-Yor theorem, Annals of Applied Probability 18 (2008) 120–142.

- [10] S. Janson, M. B. Sokhna, P. Protter, Absolutely continuous compensators, International J. Theoretical Applied Finance 14 (2001) 335–351.

- [11] R. Jarrow, P. Protter, Structural versus reduced form models: a new information based perspective, J. Investment management 2 (2004) 1–10.

- [12] T. Jeulin, M. Yor, Grossissement d’une filtration et semi-martingales: formules explicites, Séminaire de Probabilités XII (1978) 78–97.

- [13] S. Kusuoka, A remark on default risk models, Advances in mathematical economics 1(1999) 69-82.

- [14] A. Kyprianou, Introductory Lectures on Fluctuations of Lévy Processes with Applications, Springer, 2006.

- [15] D. B. Madan, P. P. Carr, E. C. Chang, The variance gamma process and option pricing, European Finance Review 2 (1998) 79–105.

- [16] P. Protter, Stochastic Integration and Differential Equations, 2nd Edition, Springer, 2005.

- [17] K. Sato, Lévy Processes and Infinitely Divisible Distributions, Cambridge University Press, 1999.

- [18] W. Schoutens, D. B. Madan, Break on through to the single side, J. Credit Risk 4 (2008) 3–20.