A Lévy process on the real line seen from its supremum and max-stable processes

Abstract.

We consider a process on the real line composed from a Lévy process and its exponentially tilted version killed with arbitrary rates and give an expression for the joint law of seen from its supremum, the supremum and the time at which the supremum occurs. In fact, it is closely related to the laws of the original and the tilted Lévy processes conditioned to stay negative and positive. The result is used to derive a new representation of stationary particle systems driven by Lévy processes. In particular, this implies that a max-stable process arising from Lévy processes admits a mixed moving maxima representation with spectral functions given by the conditioned Lévy processes.

Key words and phrases:

Conditionally positive process, Itô’s excursion theory, mixed moving maxima representation, stationary particle system2010 Mathematics Subject Classification:

Primary 60G51; secondary 60G701. Introduction

Let be a general Lévy process, but not a compound Poisson process, and assume that drifts to as . It is well-known that such a process splits at its unique supremum into two independent parts, where the post-supremum process has the law of conditioned to stay negative and the defective pre-supremum process (look backwards and down from the supremum) has the law of conditioned to stay positive, see [3, 7, 13, 9]. We note that when drifts to the term ‘conditioned to stay positive’ has certain ambiguity [16], and so we avoid using it in this case in the following. It turns out that a similar representation holds true if the process is suitably extended to the real line. This leads to an important application to Lévy driven particle systems.

Consider the Laplace exponent and assume that for some . Let be an independent Lévy process with Laplace exponent called the associated or exponentially tilted process. It is well-known that drifts to and drifts to for . Define the càdlàg process on the real line by

| (1) |

and denote by the supremum of the process and by the time at which the supremum occurs. In this paper we give an expression for the joint law of the process shifted with its supremum point into the origin, together with the supremum point, that is we specify the measure

| (2) |

In fact, this law is closely related to the law of a process obtained as the process ‘conditioned to stay negative’, see (8). The problem of multiple possible definitions of a conditioned process does not arise in our case, because as . This result holds in a more general framework where we only assume that for some the Laplace exponent is finite and the Lévy processes and are killed with arbitrary exponential rates.

In the case , the process can be seen as the process reversed in time with respect to its invariant measure , since for any and Borel subsets we have

Let be a Poisson point process (PPP) on with intensity measure and let , , be independent copies of the process . The above implies that the Poisson point process

of particles started at the ’s and moving along the trajectories of for and for , respectively, is stationary, see also Section 2.5 and references therein.

From the perspective of extreme value theory, the process of pointwise maxima of the system

| (3) |

is well-known. It follows from [6, 25, 14] that is stationary, has càdlàg paths and is max-stable. The latter means that for any and independent copies of , the process has the same distribution as (cf., [10]). For instance, if is a standard Brownian motion and , , then , , and coincides with the original definition of the Brown-Resnick process in [5]. Its extension to Gaussian random fields in [18] has become a standard model in extreme value statistics for assessing the risk of rare meteorological events.

It was asked in [25] whether for a general Lévy processes the max-stable process possesses a stochastic representation as a mixed moving maxima process

| (4) |

for some Poisson point process on with intensity measure , where is a constant. Here is the space of càdlàg functions on the real line, and is the law of a stochastic process on the real line called the spectral process. The existence of such a representation is important as it implies that the process is mixing and can be efficiently simulated. For the original Brown-Resnick process, that is , the answer is positive. Indeed, [18] prove the existence and [15] show that the spectral functions in this case are given by -dimensional (drifted) Bessel processes.

Applying the new expression for the joint law of (2) given in Corollary 1, we show that for a general Lévy processes there is a stochastic representation of as a mixed moving maxima process. More importantly, we derive the explicit distribution of the spectral processes in (4). It turns out that is the law of , that is, the process conditioned to stay negative. We envisage that Theorem 1 will find a similar application to a more general particle system, where particles can die and be born.

In Section 2 we give necessary preliminaries and state the two main theorems, that is, the identity relating the law of (2) with , and the mixed moving maxima representation of . The proof of the former is postponed to Section 3 where we use Itô’s excursion theory and the recent result from [8] to analyze the process seen from its supremum. As a side result we relate the excursion measures of the tilted process to the ones of the original process in Proposition 1. Finally, Section 4 discusses possible approaches to simulation of the process based on its mixed moving maxima representation.

2. Main results

2.1. Two Lévy processes

Let us first fix some notation. Let be a probability space equipped with a filtration , satisfying the usual conditions. Let also , be a Lévy process on this filtered probability space with characteristic triplet , that is

| (5) |

where and are the variance of the Brownian component and the Lévy measure, respectively. The so-called Laplace exponent is finite for , but may be infinite for some . For details on Lévy processes we refer the reader to [4, 20]. Throughout this work we assume that is not a process with monotone paths, neither it is a Compound Poisson Process (CPP), but see also Remark 1.

Pick such that which is equivalent to according to [20, Thm. 3.6]. One can see that for all if and if . Moreover, one can define an exponentially tilted measure with respect to , also known as the Esscher transform:

It is known that under is a Lévy process, say , with Laplace exponent , which implies that and , see e.g. [20]. Furthermore, has paths of bounded variation on compacts if and only if so does , in which case (5) can be written as

where is the linear drift, and then . This furthermore shows that is not a process with monotone paths either, and neither it is a CPP.

The case , , will be of special interest. In this case and , which follows from the convexity of on , see e.g. [20, Ch. 3]. This implies that drifts to and drifts to .

In addition, we will allow for defective (or killed) processes. We say that and are killed at rates and if they are sent to an additional ‘cemetery’ state at the times and respectively, where denotes an exponentially distributed random variable of rate independent of everything else. We let and be the life times of and respectively.

2.2. Two processes on the real line

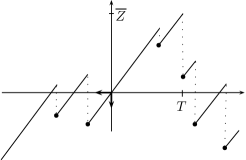

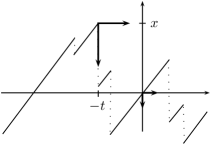

Consider two independent Lévy processes and killed at rates and (with respective life times and ) as defined in Section 2.1. Define a càdlàg process on the real line:

for and put otherwise. The left hand side of Figure 1 illustrates the construction of . Roughly speaking, the process seen with respect to ‘small’ axis is , which may help to better understand various relations in the following.

We remark that for , given that , it holds that has the same distribution as . Furthermore, if has no positive (negative) jumps then has no positive (negative) jumps either. For simplicity of notation we assume that and for any . Define the overall supremum and its time

| (6) |

It turns out that the law of the process can be described by another process which we now define. Letting

be the supremum of and its time, and the infimum of and its time, we define two post extremal processes:

| (7) | ||||

and assign and otherwise. It is well-known, see [3, 9], that and are time-homogeneous (sub-)Markov processes, such that when started away from zero their laws coincide with the laws of and started at the corresponding levels and conditioned to stay negative and positive, respectively, explaining the notations and terminology. For completeness and with almost no additional work, we provide this statement in a rigorous form in Lemma 3.

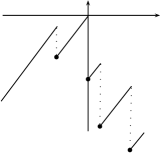

Finally, we define another càdlàg process on the real line:

| (8) |

for and put otherwise, see the right hand side of Figure 1. Roughly speaking, we find the time of supremum of for and for , delete the path in between these times and shift these supremum points into . Interestingly, the law of the processes can be easily recovered from the law of the process as shown in Theorem 1.

2.3. An identity relating the laws

Take a Lévy process (not a CPP, neither a process with monotone paths) with the Laplace exponent , and a number such that . Consider the processes and on the real line as they are defined in Section 2.2. Recall that the left parts of the processes are killed with rate and the right parts with rate . Consider the set of càdlàg paths on the real line with values in with Skorohod’s topology, and let be the corresponding Borel -algebra. Now the following result relates the laws of and .

Theorem 1.

For any and it holds that

where

| (9) |

and and are the bivariate Laplace exponents of the ascending and descending ladder processes respectively, corresponding to (without killing).

The bivariate Laplace exponents and are discussed in detail in Section 3.1, see also [20, Ch. 6.4] and [4, Ch. VI.1]. We only note at this point that these exponents are unique up to a scaling constant (coming from the scaling of local times), which clearly can be arbitrary in the above result. The proof of Theorem 1 is given in Section 3.2.

The following corollary considers non-defective processes, that is, , when and . Recall from Section 2.1 that this implies that drifts to and drifts to , that is, the supremum of is finite.

Corollary 1.

Assume that for some . Then for any and it holds that

| (10) | ||||

where

| (11) |

where the derivative is with respect to the first argument.

The only non-trivial part of its proof concerns the identification of , which is done in Section 3.1. Again, the scaling of and is arbitrary.

Remark 1.

One would expect that similar results hold true for random walks, which then can be extended to CPPs as well. On the one side analysis of random walks is less technical, but on the other side one will have to distinguish between strict and weak ascending ladder times, left-most and right-most supremum times, as well as random walks conditioned to stay positive and conditioned to stay non-negative.

2.4. Examples

The bivariate Laplace exponents and can be given explicitly in a number of cases, some of which we consider below. In all of these cases we compute the constants and . Recall that the process is constructed from the conditioned processes and , see (8). The conditioned Lévy processes can be obtained in various possible ways, which we summarize in Section 4.

2.4.1. Spectrally-negative process

Suppose is a spectrally-negative process, and so exists for all . Let be the right inverse of , i.e., is the right-most solution of . According to [20, Sec. 6.5.2] we may take

| (12) |

for , and so one easily obtains from either representation in (9) that

if . The latter assumption may be dropped, because (12) can be analytically continued to , see also (21). Note also that the denominator in the expression of is always positive.

2.4.2. Spectrally-positive process

2.4.3. Brownian motion

Clearly, the above formulas should coincide if is both spectrally-negative and spectrally-positive process, that is, is a BM. For simplicity we only consider the constant , i.e., equations (13) and (14).

In this case, with and . Hence and then , which shows that indeed the above formulas coincide and result in

So choosing and we get confirming the result in [15].

2.4.4. More general examples

There are examples of Lévy processes with both positive and negative jumps with explicit bivariate exponents and . A rather general process of this type is given by an independent sum of an arbitrary spectrally-negative Lévy process and a CPP with positive jumps characterized by a rational transform, see [21] and [1] for the particular case of positive jumps having so-called phase type distributions. Similarly, one can treat a process with arbitrary positive jumps and finite intensity negative jumps characterized by a rational transform. Here we only mention that the resulting expressions are in terms of roots of certain equations.

In general the bivariate Laplace exponents and , and hence the constants and , can be computed (at least theoretically) using a Spitzer-type identity, see e.g. [20, Thm. 6.16]. This would require triple integration, assuming that one inverts the transform to obtain the distribution of .

2.5. Stationary particles systems and mixed moving maxima processes

The results of Section 2.3 provide an alternative representation of the process on the real line. Here we apply Corollary 1 to provide a better understanding of particle systems driven by Lévy processes. We anticipate that Theorem 1 will be useful to analyze a more general particle system, where particles can die and be born.

Let be a Lévy process whose Laplace exponent fulfills for a . Suppose that and are defined as above. It is easily seen that under these assumptions the measure is invariant for both processes and . Let further be a Poisson point process on with intensity measure and let , , be independent copies of the process . We consider the system

| (15) |

of particles started at the ’s and moving along the trajectories of for and for , respectively. Then is a Poisson point process on the space of càdlàg functions on . It follows from the results of [25, 14] that the system is stationary (or translation invariant), in the sense that for any , the shifted system has the same distribution as . This kind of systems has been analyzed in [17] in the case that the particles move along Gaussian trajectories.

In the definition of , the point is an exceptional point at which each single particle changes from the trajectory of to the trajectory of . Stationarity of shows that, in fact, is not special. Furthermore, we will show that the particle system can be equivalently represented by a system , generated by scattering the starting time points of the particles uniformly over the real line and letting them move along the trajectories of processes distributed as in (8). This also provides an alternative proof that the particle system is stationary.

As mentioned in the introduction, the pointwise maximum in (3) of the particles in is a stationary, max-stable process that generalizes the Brown-Resnick process in [5]. From both a theoretical and a practical point of view, an important question is whether such a process has a stochastic representation as a mixed moving maxima process as defined in (4). It implies that the process is mixing (cf., [25, 11]) and can be efficiently simulated if the law of the spectral processes is known (cf. Section 4 for details). The equivalent representation of in terms of the conditioned process in the theorem below directly yields a mixed moving maxima representation of . We thus give an affirmative answer to the open question of [25] on the existence of such a representation and, moreover, we provide the law of the spectral processes.

Theorem 2.

Remark 2.

The constant in the above theorem has an alternative representation

This follows either directly from (10) or from a computation of using void probabilities of the PPP on the one side and the PPP on the other:

Proof.

We first introduce some notation. For two measurable spaces and , a measurable function and a measure on , denote by the pushforward measure of under , i.e., , for all . Further, let be the Borel subset of of functions that drift to , that is, , and note that . For let

Let be the Poisson point process on with intensity measure . We define the mapping by

It is straightforward to check that is measurable. Moreover, it induces a Poisson point process on which has intensity measure by a general mapping theorem (cf., [19]). In fact, for Borel sets , , we compute

| (17) | ||||

where the second last equation is a direct consequence of the identity (10). For fixed , define the measure by

for all Borel sets , and note that

Thus, is a multiple of Lebesgue measure and we obtain together with (17)

In other words, the intensity measure of factorizes and equals the intensity measure of . Finally, let be the measurable mapping

so that . The induced PPP is thus nothing else than . Furthermore, it has the same intensity measure as according to the construction of . Taking pointwise maxima within the two point processes yields the mixed moving maxima representation (16). ∎

3. Proofs

Throughout this section we write instead of and similarly for other processes which leads to somewhat cleaner expressions.

3.1. Bivariate Laplace exponents

Consider a (non-defective) Lévy process as in Section 2.1. Define the running supremum and infimum processes:

as well as all time supremum and infimum: . Let be the local time of the strong Markov process at and let be the measure of its excursions away from 0, see e.g. [4, Ch. 4]. Recall that is defined in a unique way up to a scaling constant. Let also

| (18) |

be the Laplace exponent of a bivariate ascending ladder process where and . We also write and for the analogous objects constructed from , i.e., we consider the strong Markov process (note also that is a non-decreasing process).

Following [8] we assume in the rest of this work that the local times are normalized so that

| (19) |

which implies, see e.g. [8], that

| (20) |

Let also and be the linear drifts of the subordinators and . We are ready to give a proof of Corollary 1.

Proof of Corollary 1.

We only need to compute as the limit of in (9) as . Note that , which can not happen a.s. when . Hence from (18) we find that and similarly we conclude that . Using (20) we write which results in . For arbitrary scaled we first scale them so that (19) holds, which results in the second representation of in (11). Now the first representation of in (11) is obvious. ∎

We will require the following expressions for the Laplace exponents of the ladder processes corresponding to , see also [2] and [20, Ch. 7.2].

Lemma 1.

For it holds that

| (21) |

Proof.

Moreover, we will need the following representation of the Wiener-Hopf factors

| (22) |

where and are the time of supremum and the time of infimum respectively, see [20, Thm. 6.16] and (21). This requires an additional commentary, because strictly speaking the first identity holds for , and the second for . Nevertheless these identities can be continued analytically to include arbitrary and if we can show that the left sides are finite. For this write

and recall that has the law of , and the law of , see [20, Thm. 6.16]. This shows that and the other factor can be handled in a similar way. Now we also see that

yielding

| (23) |

in view of (20).

Finally, the following technical lemma is needed to claim that the time of supremum of is a.s. not . We say that is (ir)regular upwards if is (ir)regular for .

Lemma 2.

The point is irregular upwards for if and only if is irregular upwards for .

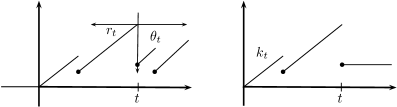

3.2. Excursion theory and splitting

In this section we adopt a very convenient notation of [13, 8] and rely on Thm. 5 in [8]. We let be the space of càdlàg paths with lifetime . The space is equipped with the Skorohod’s topology, and the usual completed filtration is generated by the coordinate process . We denote by and the laws of Lévy processes and killed at rate . Similarly, and denote the laws of and , which are the post-supremum and post-infimum processes of the killed , see (7). Furthermore, is used with the obvious meaning. Note that in this setup instead of assigning at the killing time we keep the process constant. This setup will be sufficient to prove Theorem 1.

Let be a path identically equal to 0, and define three operators on :

see Figure 2, as well as the usual shift operator: .

In the following we let be two bounded Borel functionals on and put . First, we note that

| (24) |

with , where the second follows directly from the definition of , and the first from the definition of for a time-reversed process , which has the same law as the process , see [4, Lem. II.2].

The following result is well-known, see e.g. [4, Lem. VI.6] and note that if there is a jump up at then it is necessarily the case (i) of this Lemma, and if there is a jump down at then it is the case (ii); otherwise there is no difference.

Theorem 3.

For it holds that

that is, the pre- and post-supremum processes are independent.

The following result expresses the law of pre- and post-supremum processes via excursion measures, see [8, Thm. 5]. One can either extract the following identity directly from the proof of [8, Thm. 5], or integrate the result of [8, Thm. 5] multiplied by and change the order of integration.

Theorem 4 (Chaumont).

For it holds that

It is noted that and correspond to the events and respectively. Furthermore, according to [8] at least one of and is and

| (25) |

So picking and using (20) we obtain

| (26) |

and similarly for the other term , which combined with Theorem 4 and (20) proves Theorem 3. Note also that (26) equals to according to (24) and hence it specifies the law of the conditioned process in terms of the excursion measure.

Let us show that is a time-homogeneous Markov process, such that when started in its law coincides with the law of started in and conditioned to stay above , see also [3, 9].

Lemma 3.

For it holds that

| (27) |

which furthermore can be expressed as

Proof.

According to (24) and (26) the left hand side (lhs) of (27) is given by

where the term containing results in 0, because . Next, the right hand side (rhs) immediately reduces to

Recall that is the law of the first excursion from the minimum of length larger than , see [4, Ch. IV]. The standard application of the strong Markov property of at the first time when its excursion from the minimum exceeds length yields the following identity:

where in the second term signifies that the excursion length exceeds . Here we also used the memoryless property of the exponential distribution. This finally yields

for the lhs of (27). Plugging we obtain an expression for , which then immediately leads to the result. ∎

The following identity for the pre-supremum process and will be important:

| (28) |

To see it observe that the lhs is

where the second step follows from (26), because . The final expression is clearly the rhs of (28).

Remark 3.

The following result, extending (3.8) in [2], expresses the excursion measures under measure change.

Proposition 1.

Let and be the excursion measures associated to under the measure . Then for it holds that

| (29) | |||

| (30) |

Proof.

We are now ready to give the proof of our main result.

Proof of Theorem 1.

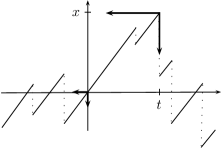

First suppose that . According to splitting at the supremum of , see Theorem 3, the post-supremum process given is independent of the rest (including the supremum and its time) and has the law of . So we are only concerned with the pre-supremum process and the supremum with its time. It is only required to show that

| (31) | ||||

where and is the law of the pre-supremum process of . Here we split the sample path of the pre-supremum process at time and apply functional to the first part and functional to the second. See also the lhs of Figure 3, where the additional axes show a convenient perspective on the sample path and its splitting.

According to (28) the lhs of (31) equals

According to Lemma 3 (the Markov property of ) the rhs of (31) reduces to

see also Remark 3. Using Proposition 1 we see that these expressions indeed coincide when , which is the left expression of in (9) according to (21).

Next suppose that . One can repeat the above arguments adjusting for the splitting at the infimum of . Instead of going this way and introducing additional notation, we simply consider the process and change measure according to : is just , see also the second part of the proof of Proposition 1. It is then required to prove for that

where under is the law of under , see the rhs of Figure 3. Similarly to the above derivation, the lhs equals

and the rhs equals to

Again using Proposition 1 we find that both sides are equal when , which is the right expression of in (9) according to (21). Note that both expressions for coincide due to (23).

4. Conditioned processes

Simulation of the process in (3) based on the particle system in (15) by simply sampling the ’s top down and adding to each of them a realization of the process is problematic. As drifts to almost surely, stationarity will only be attained locally around for finite sample sizes. The equivalent mixed moving maxima representation based on derived in Theorem 2 offers an appealing alternative sampling method (see also [24]): Simulation of the points of the Poisson point process with intensity is straightforward. To each of these points, a realization of the conditioned process has to be sampled. This is more subtle since the densities of this process are unknown in most cases. Below, we will therefore briefly list several possibilities from the literature to obtain sample paths of , where each of the options is worth consideration.

The advantage of this procedure is that the maxima are scattered uniformly over the real line and thus global stationarity is attained considerably faster than under simulation based on (see Section 3 in [15] for the case of Brownian motion). For Brown-Resnick processes which correspond to Gaussian particle systems, [22] used a similar method. There, the respective constant is not known in closed form and its computation is expensive. Thanks to formula (11), in our case this is unnecessary.

As mentioned above, simulation of the conditioned process is non-trivial. Note that in Theorem 2 is composed from and , where both and drift to . Hence for simplicity of notation in the following we assume that is a Lévy process (not a CPP) drifting to , and discuss some alternative ways known in the literature to obtain the conditionally positive process .

-

(1)

Post-infimum process: as a first option we consider our definition of as the post-infimum process, see (7).

-

(2)

Conditioned process: the process on given equals in law to the process started in and conditioned to stay positive, see Lemma 3. Moreover, [9, Thm. 2] shows that can be approximated by the conditioned process started in . If is irregular upwards then this approximation holds for strictly positive times only, because in such a case is not necessarily 0. The distribution of the initial value of can be found in [7] when has no negative jumps.

- (3)

- (4)

-

(5)

Path segments in : [3] showed that can be obtained by sticking together path segments of in the positive half-line together with an appropriate correction according to the behavior of at 0.

-

(6)

Williams’ representation: we recall this representation for a process with no positive jumps as it is given in [4, Thm. 18 and Cor. 19], and refer to [13, Thm. 4.1, Thm. 4.2] for the general case. It holds that up to its last time below , say , has the same law as time-reversed at its first passage over . Moreover, the evolution of after is independent from the past and has the law of .

- (7)

In order to avoid some possible confusion with the term ‘conditioned to stay positive’, it is noted that one can ‘condition’ (started in ) to stay positive even when does not drift to , i.e., when . In this case there are various natural ways to do so, which lead to different laws. For example, [16] shows that the following two limits result in different laws:

where and are the first passage times below 0 and above , respectively, and is an event in for some . Finally, we note that these ambiguities disappear when drifts to as required by Corollary 1.

Acknowledgements

Financial support by the Swiss National Science Foundation Projects 200021-140633/1, 200021-140686 (first author), and 200020-143889 (second author) is gratefully acknowledged.

References

- [1] S. Asmussen, F. Avram, and M. R. Pistorius. Russian and American put options under exponential phase-type Lévy models. Stochastic Process. Appl., 109(1):79–111, 2004.

- [2] E. J. Baurdoux. Some excursion calculations for reflected Lévy processes. ALEA Lat. Am. J. Probab. Math. Stat., 6:149–162, 2009.

- [3] J. Bertoin. Splitting at the infimum and excursions in half-lines for random walks and Lévy processes. Stochastic Process. Appl., 47(1):17–35, 1993.

- [4] J. Bertoin. Lévy processes, volume 121 of Cambridge Tracts in Mathematics. Cambridge University Press, Cambridge, 1996.

- [5] B. M. Brown and S. I. Resnick. Extreme values of independent stochastic processes. J. Appl. Probab., 14:732–739, 1977.

- [6] M. Brown. A property of Poisson processes and its application to macroscopic equilibrium of particle systems. Ann. Math. Statist., 41:1935–1941, 1970.

- [7] L. Chaumont. Sur certains processus de Lévy conditionnés à rester positifs. Stochastics Stochastics Rep., 47(1-2):1–20, 1994.

- [8] L. Chaumont. On the law of the supremum of Lévy processes. Ann. Probab., 41(3A):1191–1217, 2013.

- [9] L. Chaumont and R. A. Doney. On Lévy processes conditioned to stay positive. Electron. J. Probab., 10(28):948–961, 2005.

- [10] L. de Haan and A. Ferreira. Extreme Value Theory. Springer, New York, 2006.

- [11] C. Dombry. Extremal shot noises, heavy tails and max-stable random fields. Extremes, 15:129–158, 2012.

- [12] R. A. Doney. Tanaka’s construction for random walks and Lévy processes. In Séminaire de Probabilités XXXVIII, volume 1857 of Lecture Notes in Math., pages 1–4. Springer, Berlin, 2005.

- [13] T. Duquesne. Path decompositions for real Lévy processes. Ann. Inst. H. Poincaré Probab. Statist., 39(2):339–370, 2003.

- [14] S. Engelke. Brown-Resnick Processes: Analysis, Inference and Generalizations. Ph.D. thesis, available from http://hdl.handle.net/11858/00-1735-0000-000D-F1B3-2, 2013.

- [15] S. Engelke, Z. Kabluchko, and M. Schlather. An equivalent representation of the Brown–Resnick process. Statist. Probab. Lett., 81(8):1150–1154, 2011.

- [16] K. Hirano. Lévy processes with negative drift conditioned to stay positive. Tokyo J. Math., 24(1):291–308, 2001.

- [17] Z. Kabluchko. Stationary systems of Gaussian processes. Ann. Appl. Probab., 20:2295–2317, 2010.

- [18] Z. Kabluchko, M. Schlather, and L. de Haan. Stationary max-stable fields associated to negative definite functions. Ann. Probab., 37:2042–2065, 2009.

- [19] J. F. C. Kingman. Poisson processes, volume 3 of Oxford Studies in Probability. The Clarendon Press, Oxford University Press, New York, 1993. Oxford Science Publications.

- [20] A. E. Kyprianou. Introductory lectures on fluctuations of Lévy processes with applications. Universitext. Springer-Verlag, Berlin, 2006.

- [21] A. L. Lewis and E. Mordecki. Wiener-Hopf factorization for Lévy processes having positive jumps with rational transforms. J. Appl. Probab., 45(1):118–134, 2008.

- [22] M. Oesting, Z. Kabluchko, and M. Schlather. Simulation of Brown-Resnick processes. Extremes, 15:89–107, 2012.

- [23] J. W. Pitman. One-dimensional Brownian motion and the three-dimensional Bessel process. Advances in Appl. Probability, 7(3):511–526, 1975.

- [24] M. Schlather. Models for stationary max-stable random fields. Extremes, 5:33–44, 2002.

- [25] S. A. Stoev. On the ergodicity and mixing of max-stable processes. Stochastic Process. Appl., 118:1679–1705, 2008.

- [26] H. Tanaka. Time reversal of random walks in one-dimension. Tokyo J. Math., 12(1):159–174, 1989.

- [27] H. Tanaka. Lévy processes conditioned to stay positive and diffusions in random environments. In Stochastic analysis on large scale interacting systems, volume 39 of Adv. Stud. Pure Math., pages 355–376. Math. Soc. Japan, Tokyo, 2004.