Scalable sparse covariance estimation via self-concordance

Abstract

We consider the class of convex minimization problems, composed of a self-concordant function, such as the metric, a convex data fidelity term and, a regularizing – possibly non-smooth – function . This type of problems have recently attracted a great deal of interest, mainly due to their omnipresence in top-notch applications. Under this locally Lipschitz continuous gradient setting, we analyze the convergence behavior of proximal Newton schemes with the added twist of a probable presence of inexact evaluations. We prove attractive convergence rate guarantees and enhance state-of-the-art optimization schemes to accommodate such developments. Experimental results on sparse covariance estimation show the merits of our algorithm, both in terms of recovery efficiency and complexity.

Introduction

Convex -regularized divergence criteria have been proven to produce – both theoretically and empirically – consistent modeling in diverse top-notch applications. The literature on the setup and utilization of such criteria is expanding with applications in Gaussian graphical learning (?; ?; ?), sparse covariance estimation (?), Poisson-based imaging (?), etc.

In this paper, we focus on the sparse covariance estimation problem. Particularly, let be a collection of -variate random vectors, i.e., , drawn from a joint probability distribution with covariance matrix . In this context, assume there may exist unknown marginal independences among the variables to discover; we note that when the -th and -th variables are independent. Here, we assume is unknown and sparse, i.e., only a small number of entries are nonzero. Our goal is to recover the nonzero pattern of , as well as compute a good approximation, from a (possibly) limited sample corpus.

Mathematically, one way to approximate is by solving:

| (1) |

where is the optimization variable, where is the sample covariance and is a convex nonsmooth regularizer function, accompanied with an easily computable proximity operator (?). and .

Whereas there are several works (?; ?) that compute the minimizer of such composite objective functions, where the smooth term is generally a Lipschitz continuous gradient function, in (1) we consider a more tedious task: The objective function has only locally Lipschitz continuous gradient. However, one can easily observe that (1) is self-concordant; we refer to some notation and definitions in the Preliminaries section. Within this context, (?) present a new convergence analysis and propose a series of proximal Newton schemes with provably quadratic convergence rate, under the assumption of exact algorithmic calculations at each step of the method.

Here, we extend the work of (?) to include inexact evaluations and study how these errors propagate into the convergence rate. As a by-product, we apply these changes to propose the inexact Self-Concordant OPTimization (iSCOPT) framework. Finally, we consider the sparse covariance estimation problem as a running example for our discussions. The contributions are:

-

We consider locally Lipschitz continuous gradient convex problems, similar to (1), where errors are introduced in the calculation of the descent direction step. Our analysis indicates that inexact strategies achieve similar convergence rates as the corresponding exact ones.

-

We present the inexact SCOPT solver (iSCOPT) for the sparse covariance estimation problem, with several variations that increase the convergence rate in practice.

Preliminaries

Notation: We reserve to denote the vectorization operator which maps a matrix into a vector, by stacking its columns and, let be the inverse operation. denotes the identity matrix.

Definition 1 (Self-concordant functions (?)).

A convex function is self-concordant if . A function is self-concordant if is self-concordant .

For , we define as the local norm around with respect to . The corresponding dual norm is . We define as , and as . Note that and are both nonnegative, strictly convex, and increasing.

Problem reformulation: We can transform the matrix formulation of (1) in the following vectorized problem:

| (2) |

for , where is a convex, self-condordant function and is a proper, lower semi-continuous and non-smooth convex regularization term. For our discussions, we assume is -norm-based.

The algorithm in a nutshell

For our convenience and without loss of generality, we use the vectorized reformulation in (2). Here, we describe the SCOPT optimization framework, proposed in (?). SCOPT generates a sequence of putative solutions , according to:

| (3) |

where is a descent direction, and is a step size along this direction. To compute , we minimize the non-smooth convex surrogate of around ; observe that assumes exact evaluations of :

| (4) |

is a quadratic approximation of such that where and denote the gradient (first-order) and Hessian (second-order) information of function around , respectively.

While quadratic approximations of smooth functions (of the form ) have become de facto approaches for general convex smooth objective functions, to the best of our knowledge, there are not many works considering a composite non-smooth and non-Lipschitz gradient minimization case with provable convergence guarantees under the presence of errors in the descent direction evaluations.

Inexact solutions in (4)

An important ingredient for our scheme is the calculation of the descent direction through (4). For sparsity based applications, we use FISTA – a fast -norm regularized gradient method for solving (4) (?) – and describe how to efficiently implement such solver for the case of sparse covariance estimation where .

Given the current estimate , the gradient and the Hessian of around can be computed respectively as: Given the above, let . After calculations on (4), we easily observe that (4) is equivalent to:

| (5) |

where is smooth and convex with Lipschitz constant :

| (6) |

where denotes the minimum eigenvalue of a matrix. Combining the above quantities in a ISTA-like procedure (?), we have:

| (7) |

where we use superscript to denote the -th iteration of the ISTA procedure (as opposed to the subscript for the -th iteration of (3)). Here, and . Furthermore, to achieve an convergence rate, one can use acceleration techniques that lead to the FISTA algorithm, based on Nesterov’s seminal work (?). We repeat and extend FISTA’s guarantees, as described in the next theorem; the proof is provided in the supplementary material.

Theorem 1.

Let be the sequence of estimates generated by FISTA. Moreover, define where is the minimizer with for some global constant . Then, to achieve a solution such that:

| (8) |

the FISTA algorithm requires at least iterations. Moreover, it can be proved that:

We note that, given accuracy , satisfies (8) and in the recursion (3). In general, is not known apriori; in practice though, such a global constant can be found during execution, such that Theorem 1 is satisfied. A detailed description is given in the supplementary material.

For the sparse covariance problem, one can observe that and are precomputed once before applying FISTA iterations. Given , we compute in time complexity, while can be computed with time cost using the Kronecker product property . Similarly, can be iteratively computed in time cost. Overall, the FISTA algorithm for this problem has computational cost.

iSCOPT: Inexact SCOPT

Assembling the ingredients described above leads to Algorithm 1, which we call as the Inext Self-Concordant Optimization (iSCOPT) with the following convergence guarantees; our objective function satisfies the assumptions A.1, defined in (?); the proof is provided in the supplementary material.

Theorem 2 (Global convergence guarantee).

| (9) |

Quadratic convergence rate of iSCOPT algorithm

For strictly convex criteria with unique solution , the above proof guarantees convergence, i.e., for sufficiently large . Given this property, we prove the convergence rate towards the minimizer using local information in norm measures: as long as is away from , the algorithm has not yet converged to . On the other hand, as , the sequence converges to its minimum and , as increases.

In our analysis, we use the weighted distance to characterize the rate of convergence of the putative solutions. By (3) and given is a computable solution where , we observe:

This setting is nearly algorithmic: given and at each iteration, we can observe the behavior of through the evolution of and identify the region where this sequence decreases with a quadratic rate.

Definition 2.

We define the quadratic convergence region as such where satisfies , for some constant , and bounded and small constant .

The following lemma provides a first step for a concrete characterization of for the iSCOPT algorithm; the proof can be found in the supplementary material.

Lemma 1.

For any selection, , the iSCOPT algorithm generates the sequence such that (9) holds.

We provide a series of corollaries and lemmata that justify the local quadratic convergence of our approach in theory.

Corollary 1.

In the ideal case where is computable exactly, i.e., , the iSCOPT algorithm is identical to the SCOPT algorithm (?).

We apply the bound to simplify (9) as:

| (10) |

Next, we describe the convergence rate of iSCOPT for the two distinct phases in our approach: full step size and damped step size; the proofs are provided in the supplementary material.

Theorem 3.

Assume . Then, iSCOPT satisfies:

where , and is user-defined. I.e., iSCOPT has locally quadratic convergence rate where is small-valued and bounded. Moreover, for , .

Theorem 4.

Assume the damped-step case where . Then, iSCOPT satisfies:

where and is user-defined. I.e., iSCOPT has locally quadratic convergence rate where is small-valued and bounded. Moreover, for , .

| [1] | [2] | [3] | [4] | This work | ||||||

| # of tuning parameters | 2 | 1 | 2 | 1 | 2 | |||||

| Convergence guarantee | ✓ | ✓ | ✓ | – | ✓ | |||||

| Convergence rate | Linear | – | –† | –† | Quadratic | |||||

| Covariate distribution | Any | Gaussian | Any | Gaussian | Any | |||||

| †To the best of our knowledge, block coordinate descent algorithms have known convergence only for the case | ||||||||||

| of Lipschitz continuous gradient objective functions (?). | ||||||||||

An iSCOPT variant

Starting from a point far away from the true solution, Newton-like methods might not show the expected convergence behavior. To tackle this issue, we can further perform Forward Line Search (FLS) (?): starting from the current estimate , one might perform a forward binary search in the range . The selection of the new step size is taken as the maximum-valued step size in , as long as decreases the objective function , while satisfying any constraints in the optimization. The supplementary material contains illustrative examples which we omit due to lack of space.

Application to sparse covariance estimation

Covariance estimation is an important problem, found in diverse research areas. In classic portfolio optimization (?), the covariance matrix over the asset returns is unknown and even the estimation of the most significant dependencies among assets might lead to meaningful decisions for portfolio optimization. Other applications of the sparse covariance estimation include inference in gene dependency networks (?), fMRI imaging (?), data mining (?), etc. Overall, sparse covariance matrices come with nice properties such as natural graphical interpretation, whereas are easy to be transfered and stored.

To this end, we consider the following problem:

Problem I: Given -dimensional samples , drawn from a joint probability density function with unknown sparse covariance , we approximate as the solution to the following optimization problem for some :

A summary of the related work on the sparse covariance problem is given in Table 1 and a more detailed discussion is provided in the supplementary material.

| Model | () | Time (secs) | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| [3] | iSCOPT | iSCOPT FLS | [3] | iSCOPT | iSCOPT FLS | ||||||

| Model | Time | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| [4] | [1] | iSCOPT FLS | [4] | [1] | iSCOPT FLS | |||||

Experiments

All approaches are carefully implemented in Matlab code with no C-coded parts. In all cases, we set and . A more extensive presentation of these results can be found in the supplementary material.

Benchmarking iSCOPT: time efficiency

To the best of our knowledge, only (?) considers the same objective function as in Problem I. There, the proposed algorithm follows similar motions with the graphical Lasso method (?).

To show the merits of our approach as compared with the state-of-the-art in (?), we generate as a random positive definite covariance matrix with . In our experiments, we test sparsity levels such that and . Without loss of generality, we assume that the variables are drawn from a joint Gaussian probability distribution. Given , we generate random -variate vectors according to , where . Then, the sample covariance matrix is ill-conditioned in all cases with . We observe that the number of unknowns is ; in our testbed, this corresponds to estimation of up to variables. To compute in (6), we use a power method scheme with iterations. All algorithms under comparison are initialized with . As an execution wall time, we set seconds (1 hour). In all cases, we set .

Table 2 contains the summary of results. Overall, the proposed framework shows superior performance across diverse configuration settings, both in terms of time complexity and objective function minimization efficiency: both iSCOPT and iSCOPT FLS find solutions with lower objective function value, as compared to (?), within the same time frame. The regular iSCOPT algorithm performs relatively well in terms of computational time as compared to the rest of the methods. However, its convergence rate heavily depends on the conservative selection. We note that (4) benefits from warm-start strategies that result in convergence in Step 3 of Algorithm 1 within a few steps.

Benchmarking iSCOPT: reconstruction efficiency

We also measure the reconstruction efficacy by solving Problem I, as compared to other optimization formulations for sparse covariance estimation. We compare our estimate with: the Alternating Direction Method of Multipliers (ADMM) implementation (?), and the coordinate descent algorithm (?).

Table 3 aggregates the experimental results in terms of the normalized distance and the captured sparsity pattern in . Without loss of generality, we fix for the case and, for the case . iSCOPT framework is at least as competitive with the state-of-the-art implementations for sparse covariance estimation. It is evident that the proposed iSCOPT variant, based on self-concordant analysis, is at least one order of magnitude faster than the rest of algorithms under comparison. In terms of reconstruction efficacy, using our proposed scheme, we can achieve marginally better reconstruction performance, as compared to (?).

| Stock Abbr. | Company name | Stock Abbr. | Company name | |||

|---|---|---|---|---|---|---|

| RBS | Scotland Bank | ARC | Arc Document | |||

| AMEC | AMEC Group | UTX | United Tech. | |||

| BAC | Bank of America | RCI | Rogers Comm. | |||

| PKX | Posco | EMX | EMX Industries | |||

| FXPO | Ferrexpo | ARM | ARM Holdings | |||

| EOG | EOG Resources | AZEM | Azem Chemicals | |||

| PTR | PetroChina | NCR | NCR Electronics | |||

| BP | BP | PFE | Pfizer Inc. | |||

| DB | Deutsche Bank | RVG | Retro Virology | |||

| USB | U.S. Bank Corp. | SNY | Sanofi health | |||

| AURR | Aurora Russia | IPO | Intellectual Property | |||

| GLE | Glencore | VCT | Victrex Chemicals | |||

| IBM | IBM | PEBI | Port Erin BioFarma |

| Model | Risk | |||||

|---|---|---|---|---|---|---|

| (%) | ||||||

| (, ) | 1.4 | 0.5 | 0.0760 | 0.0065 | ||

| 1.7 | 1 | 0.0810 | 0.0078 | |||

| 2.3 | 5 | 0.0902 | 0.0158 | |||

| 2.7 | 7 | 0.1968 | 0.0188 | |||

| 3.0 | 10 | 0.2232 | 0.0223 | |||

| 3.8 | 15 | 0.2463 | 0.0267 | |||

| 4.5 | 20 | 0.2408 | 0.0307 | |||

| 4.5 | 30 | 0.4925 | 0.0375 | |||

| Model | Risk | |||||

|---|---|---|---|---|---|---|

| (%) | ||||||

| (, ) | 1.4 | 0.5 | 0.0223 | 0.0066 | ||

| 1.7 | 1 | 0.0233 | 0.0076 | |||

| 2.3 | 5 | 0.0513 | 0.0157 | |||

| 2.7 | 7 | 0.0529 | 0.0183 | |||

| 3.0 | 10 | 0.0706 | 0.0217 | |||

| 3.8 | 15 | 0.0876 | 0.0264 | |||

| 4.5 | 20 | 0.0872 | 0.0307 | |||

| 4.5 | 30 | 0.1075 | 0.0373 | |||

Sparse covariance estimates for portfolio optimization

Classical mean-variance optimization (MVO) (?) corresponds to the following optimization problem:

| (11) | ||||||

| subject to |

Here, is the true covariance matrix over a set of asset returns, denotes the true asset returns of stocks, represents a weighted probability distribution over the set of assets such that and is the total capital to be invested. Without loss of generality, one can assume a normalized capital such that . In such case, is both the risk of the investment as well as a metric of variance of the portfolio selection.

In practice, both and are unknown and MVO requires an estimation for both. Empirical estimates, such as , quickly become problematic in the large scale: the data amount required increases quadratically to be commensurate with the degree of dimensionality. Due to such difficulties, even a simple equal weighted portfolio such that , is often preferred in practice (?). Nevertheless, practitioners assume that many elements of the covariance matrix are zero, a property which is appealing due to its interpretability and ease of estimation. Moreover, there are cases in practice where most of the variables are correlated to only a few others.

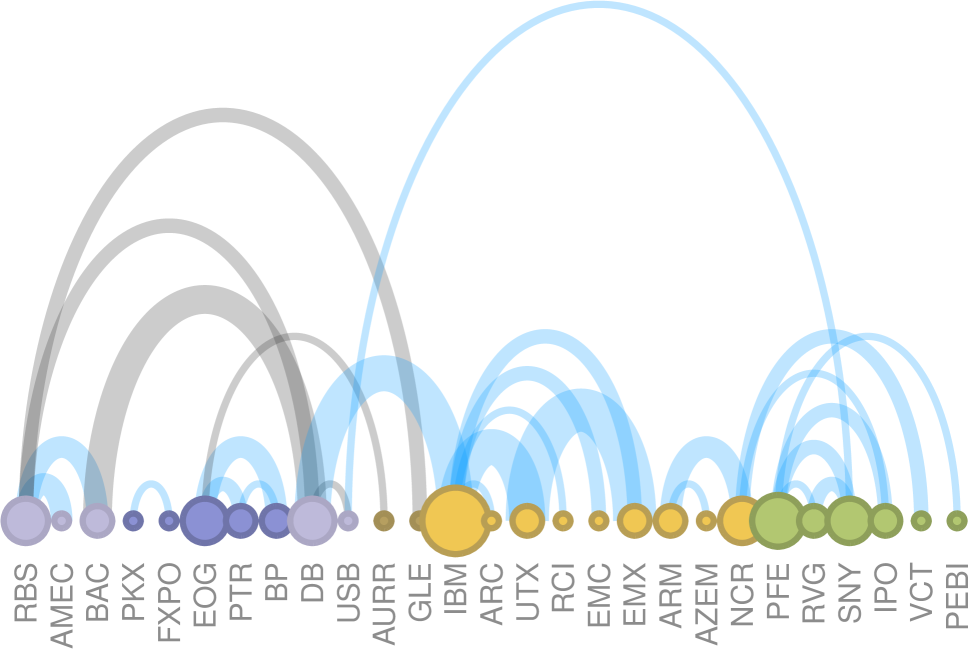

Figure 1 shows some representative correlation estimates that we observed during the period and . For this purpose, we use iSCOPT with and to solve Problem I and sort the non-diagonal elements of to keep the most important correlations. We observe in practice some strong correlations between assets, while most of the rest entries in have significantly small magnitude. This dataset contains stocks over a trading period of days, crawled from the Yahoo Finance website111http://finance.yahoo.com. Stocks are retrieved from stock markets in the America (e.g., Dow Jones, NYSE, etc.), Europe (e.g., London Stock Exchange, etc.), Asia (e.g., Nikkei, etc) and Africa (e.g., South Africa’s exchange).

Out-of-sample performance with synthetic data: It is apparent that both strong and weak correlations among stock assets are evident in practice. The behavior of non-diagonal entries in correlation matrix estimates is such that it is not easily distinguishable whether small values indicate weak dependence between variables or estimation fluctuations. Under these settings, (?) propose that small values should be considered as zeros while only large values can be considered as good covariate estimates.

To measure the performance of using a sparse covariance estimate in MVO, we assume the following synthetic case: Let be a synthetically generated Gaussian covariance matrix to represent the correlations among assets. Furthermore, assume that only entries of are sufficiently larger than the rest of the entries. In our experiments below we set and consider a time window of days (i.e., a 3- and 6-month sampling period).

Given the above, both and are calculated – we use our algorithm for the latter. Using these two quantities, we then solve (11) for and for various expected returns and record the computed minimum risk portfolios and , respectively. Finally, given and , as well as the equal-weight portfolio , we report the risk/variances achieved by the constructed portfolios, using the ground truth covariance . In Table 4, we report lower variances for portfolios trained when is used in (11), compared with the risk achieved by the equally-weighted portfolio or the sample covariance estimation where is used. However, our approach comes with some cost to compute . The empirical strategy with has the worst performance in terms of minimum risk achieved for most of our testings; we point out that, in this case, is a rank-deficient positive semidefinite matrix.

Discussion

A drawback of our approach is the combined setup of the parameters and : one needs to identify selections that perform well on-the-fly, via a trial-and-error strategy. Unfortunately, such process might be inefficient in practice, especially in high dimensional cases. An interesting question to pursue is the adaptive setup of at least one of . Such adaptive strategies have attracted a great deal of interest ; c.f., (?). One idea is to devise a path-following scheme with an adaptive selection, where the resulting scheme solves approximately a series of problems as is adaptively updated (?). We hope this paper triggers future efforts towards this research direction for further investigation.

References

- [Alqallaf et al. 2002] Alqallaf, F. A.; Konis, K. P.; Martin, R. D.; and Zamar, R. H. 2002. Scalable robust covariance and correlation estimates for data mining. In Proceedings of the eighth ACM SIGKDD international conference on Knowledge discovery and data mining, 14–23. ACM.

- [Banerjee, El Ghaoui, and d’Aspremont 2008] Banerjee, O.; El Ghaoui, L.; and d’Aspremont, A. 2008. Model selection through sparse maximum likelihood estimation for multivariate gaussian or binary data. The Journal of Machine Learning Research 9:485–516.

- [Beck and Teboulle 2009] Beck, A., and Teboulle, M. 2009. Fast gradient-based algorithms for constrained total variation image denoising and deblurring problems. Image Processing, IEEE Transactions on 18(11):2419–2434.

- [Beck and Tetruashvili 2013] Beck, A., and Tetruashvili, L. 2013. On the convergence of block coordinate descent type methods. SIAM Journal on Optimization 23(4):2037–2060.

- [Becker and Fadili 2012] Becker, S., and Fadili, J. 2012. A quasi-newton proximal splitting method. In Advances in Neural Information Processing Systems (NIPS), 2627–2635.

- [Bien and Tibshirani 2011] Bien, J., and Tibshirani, R. J. 2011. Sparse estimation of a covariance matrix. Biometrika 98(4):807–820.

- [Combettes and Wajs 2005] Combettes, P. L., and Wajs, V. R. 2005. Signal recovery by proximal forward-backward splitting. Multiscale Modeling & Simulation 4(4):1168–1200.

- [Dahl, Vandenberghe, and Roychowdhury 2008] Dahl, J.; Vandenberghe, L.; and Roychowdhury, V. 2008. Covariance selection for nonchordal graphs via chordal embedding. Optimization Methods & Software 23(4):501–520.

- [Daubechies, Defrise, and De Mol 2004] Daubechies, I.; Defrise, M.; and De Mol, C. 2004. An iterative thresholding algorithm for linear inverse problems with a sparsity constraint. Communications on pure and applied mathematics 57(11):1413–1457.

- [DeMiguel, Garlappi, and Uppal 2009] DeMiguel, V.; Garlappi, L.; and Uppal, R. 2009. Optimal versus naive diversification: How inefficient is the 1/n portfolio strategy? Review of Financial Studies 22(5):1915–1953.

- [Friedman, Hastie, and Tibshirani 2008] Friedman, J.; Hastie, T.; and Tibshirani, R. 2008. Sparse inverse covariance estimation with the graphical lasso. Biostatistics 9(3):432–441.

- [Hale, Yin, and Zhang 2008] Hale, E. T.; Yin, W.; and Zhang, Y. 2008. Fixed-point continuation for ell_1-minimization: Methodology and convergence. SIAM Journal on Optimization 19(3):1107–1130.

- [Harmany, Marcia, and Willett 2012] Harmany, Z. T.; Marcia, R. F.; and Willett, R. M. 2012. This is spiral-tap: sparse poisson intensity reconstruction algorithms—theory and practice. Image Processing, IEEE Transactions on 21(3):1084–1096.

- [Hero and Rajaratnam 2011] Hero, A., and Rajaratnam, B. 2011. Large-scale correlation screening. Journal of the American Statistical Association 106(496):1540–1552.

- [Hsieh et al. 2011] Hsieh, C.; Sustik, M.; Dhillon, I.; and Ravikumar, P. 2011. Sparse inverse covariance matrix estimation using quadratic approximation. Advances in Neural Information Processing Systems (NIPS) 24.

- [Lee, Sun, and Saunders 2012] Lee, J.; Sun, Y.; and Saunders, M. 2012. Proximal newton-type methods for convex optimization. In Advances in Neural Information Processing Systems (NIPS), 836–844.

- [Markowitz 1952] Markowitz, H. 1952. Portfolio selection. The journal of finance 7(1):77–91. Wiley Library.

- [Nesterov and Nemirovskii 1994] Nesterov, Y., and Nemirovskii, A. S. 1994. Interior-point polynomial algorithms in convex programming, volume 13. SIAM.

- [Nesterov 1983] Nesterov, Y. 1983. A method of solving a convex programming problem with convergence rate o (1/k2). In Soviet Mathematics Doklady, volume 27, 372–376.

- [Rothman 2012] Rothman, A. J. 2012. Positive definite estimators of large covariance matrices. Biometrika 99(3):733–740.

- [Schäfer and Strimmer 2005] Schäfer, J., and Strimmer, K. 2005. An empirical bayes approach to inferring large-scale gene association networks. Bioinformatics 21(6):754–764.

- [Tran-Dinh, Kyrillidis, and Cevher 2013a] Tran-Dinh, Q.; Kyrillidis, A.; and Cevher, V. 2013a. Composite self-concordant minimization. arXiv preprint arXiv:1308.2867.

- [Tran-Dinh, Kyrillidis, and Cevher 2013b] Tran-Dinh, Q.; Kyrillidis, A.; and Cevher, V. 2013b. An inexact proximal path-following algorithm for constrained convex minimization. arXiv preprint arXiv:1311.1756.

- [Varoquaux et al. 2010] Varoquaux, G.; Gramfort, A.; Poline, J.-B.; and Thirion, B. 2010. Brain covariance selection: better individual functional connectivity models using population prior. In Advances in Neural Information Processing Systems (NIPS), volume 23. 2334–2342.

- [Wang 2012] Wang, H. 2012. Two new algorithms for solving covariance graphical lasso based on coordinate descent and ecm. arXiv preprint arXiv:1205.4120.

- [Xue, Ma, and Zou 2012] Xue, L.; Ma, S.; and Zou, H. 2012. Positive definite penalized estimation of large covariance matrices. Journal of the American Statistical Association.