Opportunities in a Federated Cloud Marketplace

Abstract

Recent measurement studies show that there are massively distributed hosting and computing infrastructures deployed in the Internet. Such infrastructures include large data centers and organizations’ computing clusters. When idle, these resources can readily serve local users. Such users can be smartphone or tablet users wishing to access services such as remote desktop or CPU/bandwidth intensive activities. Particularly, when they are likely to have high latency to access, or may have no access at all to, centralized cloud providers. Today, however, there is no global marketplace where sellers and buyers of available resources can trade. The recently introduced marketplaces of Amazon and other cloud infrastructures are limited by the network footprint of their own infrastructures and availability of such services in the target country and region. In this article we discuss the potentials for a federated cloud marketplace where sellers and buyers of a number of resources, including storage, computing, and network bandwidth, can freely trade. This ecosystem can be regulated through brokers who act as service level monitors and auctioneers. We conclude by discussing the challenges and opportunities in this space.

1 Introduction

Internet applications are becoming more complex and more resource-intensive. To cope with the increasing requirements and complexity of these applications, applications providers are continuously adding computational, storage, and network resources in the Internet. Some of the application providers are now among the largest infrastructure providers in the Internet [6]. Application requirements also dictate how application or infrastructure providers deploy and expand their footprint in the Internet. Some of them rely on large data centers located in strategic network locations, colocated with large Internet exchange points (IXPs) or in large metropolitan areas e.g., Amazon, Rackspace, Equinix, ThePlanet. Others rely on a number of well distributed data centers e.g., Google, Yahoo!, Microsoft, Limelight. Some others deploy highly distributed servers deep inside the network, e.g., Akamai.

For example, Akamai operates more than servers in more than locations across nearly networks [20, 23]. Google is reported to operate tens of data centers and front-end server clusters worldwide [18, 28]. Microsoft has deployed its CDN infrastructure in 24 locations around the world [13]. Amazon maintains at least 5 large data centers and caches in at least 21 locations around the world [1]. Limelight operates thousands of servers in more than 22 delivery centers and connects directly to more than 900 networks worldwide [5]. Equinix has presence in 24 data centers in North and South America, 10 data centers in Europe and 5 data centers in Asia-Pacific region [11].

Data centers are often deployed to satisfy local markets. A rough estimation of the currently operated small to medium size datacenters accounts more than 2200 co-located data centers in around 84 countries [4]. The increasing popularity of data-intensive open-source applications, such as Hadoop [2], to perform data analytics is driving the deployment of private data centers. Prime operators of such data centers are financial companies, large corporations, web service providers, just to name a few. The exact number of such data centers is unknown, but we expect that it is quite significant. Furthermore, a large number of scientific computational clusters and data centers hosted in universities and research centers also contributes to the penetration of such datacenter infrastructures. These infrastructures are typically operated by a single authority and are either dedicated to the applications run by the infrastructure owner or are leased to third parties. As the profit margins of such infrastructures go down, we anticipate that the trend of leasing storage and computational resources to third parties will inevitably increase.

The deployment and operation of storage, computation, and network infrastructures comes at a cost. Among the highest contributing factors are the cost of energy [12, 24], especially cooling, network bandwidth [23], and the administration cost that may even exceed the cost of the hardware [17]. To amortize these costs, some of the infrastructure providers have leveraged the advances that resource virtualization offers to lease resources to tenants, i.e., third parties applications. In some cases, this provides a substantial revenue flow, see for example the Amazon Web Services. Others follow this paradigm as their core business, for example Rackspace or ThePlanet.

However, the offers for resources is currently limited to the footprint of each infrastructure provider. Such a footprint may not be agile enough for the placement and operation of all the applications. This set up may not be optimal for mobile users, those with high latency or low bandwidth to major cloud providers, or those in under privileged countries. Moreover, potential buyers of resources can not freely express the requirements for resources for their applications as the configuration and presence of infrastructures may be limited. Recent studies [9] confirm our observations that a more agile allocation of resources may benefit a number of important applications. Another limitation is that there is no common interface to lease cloud and network resources from multiple cloud providers. This leads to custom solutions that cannot scale to different providers, and thus, increase the overhead to lease resources as well as increases the burden of new cloud providers to enter the market.In this paper we present a first attempt at theoretical analysis of the feasibility of a federated marketplace for cloud computing resources were resources are available for leasing under a common brokerage scheme, and we sketch the protocol design principles to materialize it.

Most of the work on incentives for leasing or sharing Internet resources has focused on peer-to-peer systems [10, 29, 27, 19]. Recently, researchers have investigated pricing schemes for virtual resources, but the focus is on releasing resources in a single datacenter [8, 7]. Work on incentives has also considered unused bandwidth resources [25, 14] and Shapley value has been used as a tool to allocate the right value for an Internet resource [22]. The community project Seattle111https://seattle.cs.washington.edu/html/ encourages individuals to altruistically donate a fraction of their computing power to others by way of peer-to-peer networking. In [31], Wood et. al. present CloudNet, a a cloud platform architecture that utilizes virtual private networks to link cloud and enterprise sites in a dynamic and adaptive manner, although this approach is still dependant on cooperation between cloud service providers and does not necessarily focus on independent, casual clouds.

2 Marketplace: Incentives, Requirements, and Case Studies

We argue for creation of a global resource marketplace where sellers and buyers of resources can trade on the specifications and price of the leased resources. First we highlight the rational behind building a federated marketplace. We then describe the requirements to enable such a cloud marketplace. We conclude with the presentation of some promising case studies.

2.1 Incentives

A global marketplace for resources increases the awareness of the available resources to a wider group of potential buyers. A potential buyer of resources can have access to resources where it needs them, when it needs them. The entry cost for the introduction of smaller sellers and buyers is also lower. This enables healthy competition and contributes to a wider spectrum of prices and offered services. It is also possible to gain access to resources very close to end-users or target groups that may not be available in the current resource marketplace.

Today, many data center resources are under-utilized. This is due to the fact that the operators of resource infrastructures provision for the peak. By taking advantage of daily cycles, it is possible to offer un-utilized resources at attractive prices. Infrastructure providers derive additional revenue and application providers have access to reduced costs for their deployment.

The buyer of resources have more degrees of freedom when expressing their needs as they are not limited to the offers of a limited number of large providers. It also enables a better negotiation of the quality and the price of resources. This can be a positive as the price of different resources may significantly differ among providers and locations [21], due to their specific footprint.

The advances of virtualization technology allows the fast reservation of resources and also allows applications to expand or shrink on-demand, over timescales of minutes. This elasticity can significantly reduce operational costs of applications and enable more flexible charging models, such as the typical pay-as-you-go policies enabled by cloud services [7].

The enhanced performance of commercial applications leads to higher revenue [16]. We foresee a unique opportunity for infrastructure and application providers to jointly increase their revenue as well as the performance of applications. It can also be a catalyst for the introduction of new applications, hence lowering the barrier for innovation.

2.2 Requirements

To enable such a resource marketplace, it is imperative to overcome a number of challenges. In the following, we outline a number of necessary conditions that must be satisfied to ensure these challenges are addressed. In later section of this paper we propose a number of incentives to ensure that these conditions are satisfied.

Truthfulness of sellers: The sellers have to unveil the true location of their resources, the type and utilization of each resource, and a suggested price per unit of usage in each location and time-of-day for each resource. The broker’s rating system and measurements of Quality of Experience (QoE) will enforce such truthfulness.

Truthfulness of buyers: The buyers of resources should truthfully unveil the real demand for a resource and the real value for the different resources in different locations and time-of-day.

Robust billing: The broker has to ensure that the best match between supply the demand of a resource takes place. The allocation of resources has to be a revenue maximization mechanism for the involved parties while leaving resources available for future requests. Negotiations between the involved parties has also to be allowed until a consensus on the price is met. Other soft incentives such as economies of scale should also be present [30]

Mature and privacy-preserving technology: Resource virtualization is the prominent technology to support the lease of a number of resources. Some privacy concerns may arise when running virtualization in the wild, in untrusted environments and with multiple tenants. We do not address the privacy issues in this paper [15].

2.3 Case Studies

To exemplify the utility of a cloud marketplace, we present a number of case-studies:

Cloud-assisted Smartphones. Increasingly, people use tablets and smartphones to perform daily tasks or access their main desktop. For most individuals, with the uptake of netbooks, many applications will not run on the device natively anymore. Access to these applications using remote desktop services requires high bandwidth and more importantly low latency. Our proposed market place can be useful for such scenarios.

Online Gaming. Some metropolitan areas host a number of data centers, either commercial or scientific ones. The peak hour for these data centers is typically during the day, with periods of low utilization in the evening, when the end-users of the data centers are going home. This is the time when the home entertainment peak hour begins. Many entertainment applications are interactive and their performance depends significantly on the end-to-end delay. A prominent example is this of online games. The operators of online games would likely prefer to use data centers very close to the end users to minimize latency and avoid a build-out of special-purpose data centers (e.g., using GPUs) to overcome the effect of large latencies to their primary data center. Medium or even micro data centers that are under-utilized can be used to host such applications and significantly improve the end-user experience. Our marketplace can enable this.

Sport events. Global-scale events such as the Olympic games can take advantage of the massively distributed infrastructure to scale the delivery of real-time or recorded video. They can also take advantage of the time-of-day effect in order to lease low cost resources and significantly reduce the delivery cost by leasing resources is non-peak local hours (lead the sun, not follow it). Our marketplace is a catalyst for this.

The midnight stock exchange analysis. There are a number of data centers in universities and research centers in metro areas such as London, Frankfurt etc. Many studies show that the cost of deploying commercial data centers can be significantly higher in these metropolitan locations. On the other hand, data analytics applications are key for stock forecasting. The need to analyze financial data is expected to grow. Through our proposed marketplace, the above mentioned data centers can be leased at low prices when they are not used; mainly at night or when they are idle.

CDNs can also lease their resources as well. CDNs utilize thousands of servers to cope with the demand for content. Still, during the non-peak hour, the utilization of such infrastructures is low. CDNs can advertise the available resources using our marketplace and have an additional flow of revenue.

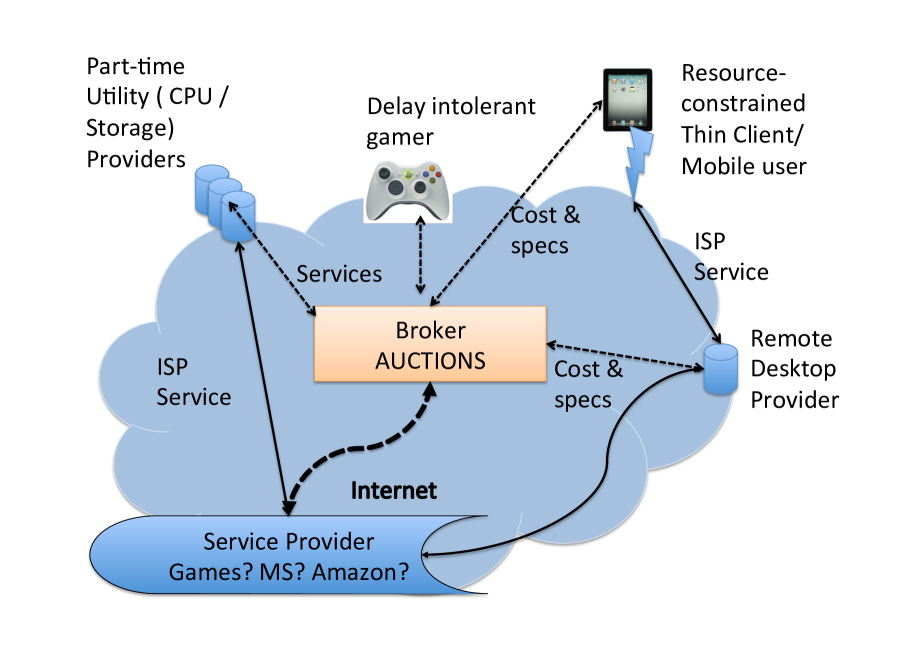

3 Participants and their roles

Figure 1 shows the participants and their interaction in our cloud marketplace ecosystem. In this section we will expand on the individual requirements of these roles.

Customer

The customer can be an individual, a small community of users (e.g., a local games store in developing countries), or a small business. This customer may have access to a thin client or a tablet device, needing to access a remote desktop service (e.g., a version of Microsoft office). Industry predictions are that more than half the web traffic will soon be on tablet devices [3]. The incentive of using a local cloud resource for the user would be that the user needs to invest less on resources, while still having low-latency and convenient access on resource constrained device like tablet. Moreover, it will enable lower delay when compared to accessing large cloud services located further away, and also likely to be at a lower cost.

Network Providers

The Network or the Internet Service Provider (ISP) delivers connectivity at a cost. The rise in Traffic Engineering (TE) and Smart/Sponsored Data Pricing [26] can increase the effect of the ISP on the market. However in this paper we assume that the ISP simply provides adequate connectivity to local cloud resources, and we don’t assume any further role for them.

Resource Providers (RP)

An RP is a cloud operator, or an organization which can provide CPU, storage, memory or remote desktop licensed software (e.g., MS Office instances). Resource Providers can act as a relay for thin clients and provide a range of services and applications (apps). The RPs will define their base rates for auctions and Quality of Service (QoS) guarantees. Their aim is to maximize their profit and utilization of their resources. Using the proposed federated cloud application marketplace, the RPs can make use of their temporary capacity and idle resources by leasing their space resources for financial gains.

Market/App Broker

A broker acts as the provider of the mobile/cloud app store, auctioneer, and reliability score keeper, without having a centralized control over the market. The broker receives requests and matches them to providers, runs auctions between RPs and completes the bidding actions on specified intervals. The broker maintains reliability scores and builds a reputation system for different RPs and active directory and resource discovery for their type of services, while setting criteria and assigning coefficients to different attributes of importance, e.g., memory and CPU. The broker collects feedback and provides reputation metrics and resolves conflicts.

4 Discussion

In this article we argued for a federated cloud-based resource marketplace. The proposed architecture in this paper is aligned with demands and services needed by users that typically have to depend on large-scale cloud offerings such as those provided by the Amazon Elastic Cloud and Web services. This trend is motivated by the increasing processing and bandwidth demands of applications such as online games as well, where companies reach for the cloud222http://online.wsj.com/article/SB10001424052702303343404577517074213415592.html to enhance the user’s visual experience and minimize delays. Our suggested approach can meet the needs of environments where latency to access large cloud services may be so large as to restrict the kinds of applications that can be used.

This is an early attempt to examine the feasibility of an open market for cloud-based resources. Our proposed resource marketplace aims to enhance the exploration of the resources that are currently available but unknown to the potential buyers, improves the agility of leasing resources in the Internet, lowers the burden for introducing new players in the resource ecosystem, and creates opportunities for new revenue flows and better services. In future work we will investigate the proposed hypothesis by obtaining real usage data from cloud services in order to take factors such as time of day and day of week into consideration when leasing resources. We also aim to improve the auctioning mechanism by use of different strategy for different resources, e.g., by matching customers with the next highest resource cloud service providers if their top resource requirement cannot be fulfilled.

Acknowledgements. This work was done while Hamed Haddadi was at AT&T Labs Research, on an EPSRC IT-as-a-Utility industrial secondment (EPSRC Ref EP/K003569/1). We acknowledge constructive feedback from Felix Cuadrado on earlier versions of this work.

References

- [1] Amazon web services. http://aws.amazon.com.

- [2] Apache hadoop. http://hadoop.apache.org/.

- [3] Cisco visual networking index: Global mobile data traffic forecast update. http://www.cisco.com/.

- [4] Data center map. http://http://www.datacentermap.com.

- [5] Limelight networks. http://www.limelightnetworks.com/platform/cdn.

- [6] B. Ager, W. Mühlbauer, G. Smaragdakis, and S. Uhlig. Web Content Cartography. In IMC, 2011.

- [7] M. Armbrust, A. Fox, R. Griffith, A. D. Joseph, R. H. Katz, A. Konwinski, G. Lee, D. A. Patterson, A. Rabkin, I. Stoica, and M. Zaharia. Above the Clouds: A Berkeley View of Cloud Computing. UC Berkeley Technical Report EECS-2009-28, 2009.

- [8] H. Ballani, P. Costa, T. Karagiannis, and A. Rowstron. The Price Is Right: Towards Location-Independent Costs in Datacenters. In HotNets, 2011.

- [9] K. Church, A. Greenberg, and J. Hamilton. On Delivering Embarrasingly Distributed Cloud Services. In HotNets, 2008.

- [10] B. Cohen. Incentives Build Robustness in BitTorrent. In Proc. of the 1st Workshop on Economics of Peer-to-Peer Systems, 2003.

- [11] Equinix. http://www.equinix.com.

- [12] A. Greenberg, J. Hamilton, D. A. Maltz, and P. Patel. The Cost of a Cloud: Research Problems in Data Center Networks. ACM CCR, 2009.

- [13] M. Inc. Windows azure. http://www.microsoft.com/windowsazure/cdn.

- [14] I. InvisibleHand Networks. http://www.invisiblehand.net.

- [15] L. Kaufman. Data security in the world of cloud computing. Security Privacy, IEEE, 7(4):61–64, July 2009.

- [16] R. Kohavi, R. M. Henne, and D. Sommerfield. Practical Guide to Controlled Experiments on the Web: Listen to Your Customers not to the HiPPO. In KDD, 2007.

- [17] M. Korupolu, A. Singh, and B. Bamba. Coupled Placement in Modern Data Centers. In IPDPS, 2009.

- [18] R. Krishnan, H. Madhyastha, S. Srinivasan, S. Jain, A. Krishnamurthy, T. Anderson, and J. Gao. Moving Beyond End-to-end Path Information to Optimize CDN Performance. In IMC, 2009.

- [19] N. Laoutaris, P. Rodriguez, and L. Massoulie. ECHOS: edge capacity hosting overlays of nano data centers. ACM CCR, 2008.

- [20] T. Leighton. Improving Performance on the Internet. CACM, 2009.

- [21] A. Li, X. Yang, S. Kandula, and M. Zhang. CloudCmp: Comparing Public Cloud Providers. In IMC, 2010.

- [22] R. T. B. Ma, D. M. Chiu, J. C. S. Lui, V. Misra, and D. Rubenstein. On Cooperative Settlement Between Content, Transit, and Eyeball Internet Service Providers. IEEE/ACM Trans. Netw., 2011.

- [23] E. Nygren, R. K. Sitaraman, and J. Sun. The Akamai Network: A Platform for High-performance Internet Applications. SIGOPS Oper. Syst. Rev., 2010.

- [24] A. Qureshi, R. Weber, H. Balakrishnan, J. Guttag, and B. Maggs. Cutting the Electric Bill for Internet-scale Systems. In SIGCOMM, 2009.

- [25] N. Semret, R. R.-F. Liao, A. T. Campbell, and A. A. Lazar. Pricing, Provisioning and Peering: Dynamic Markets for Differentiated Internet Services and Implication for Network Interconnections. IEEE J. Sel. Areas in Commun., 2002.

- [26] S. Sen, C. Joe-Wong, S. Ha, and M. Chiang. A survey of smart data pricing: Past proposals, current plans, and future trends. ACM Computing Surveys (CSUR), 46(2):15, 2013.

- [27] S. Seuken, D. Charles, M. Chickering, and S. Puri. Redundancy management for P2P backup. In ACM Electronic Commerce, 2010.

- [28] M. Tariq, A. Zeitoun, V. Valancius, N. Feamster, and M. Ammar. Answering What-if Deployment and Configuration Questions with Wise. In SIGCOMM, 2009.

- [29] L. Toka, P. Cataldi, M. D. amico, and P. Michiardi. Redundancy management for P2P backup. In INFOCOM, 2012.

- [30] S. Venticinque, R. Aversa, B. Martino, M. Rak, and D. Petcu. A Cloud Agency for SLA Negotiation and Management. In Euro-Par 2010 Parallel Processing Workshops, volume 6586, pages 587–594. Springer Berlin Heidelberg, 2011.

- [31] T. Wood, K. Ramakrishnan, P. Shenoy, and J. Van der Merwe. Enterprise-ready virtual cloud pools:vision, opportunities and challenges. Comput. J., 55(8):995–1004, Aug 2012.