Stylized facts of price gaps in limit order books: Evidence from Chinese stocks

Abstract

Price gap, defined as the logarithmic price difference between the first two occupied price levels on the same side of a limit order book (LOB), is a key determinant of market depth, which is one of the dimensions of liquidity. However, the properties of price gaps have not been thoroughly studied due to the less availability of ultrahigh frequency data. In the paper, we rebuild the LOB dynamics based on the order flow data of 26 A-share stocks traded on the Shenzhen Stock Exchange in 2003. Three key empirical statistical properties of price gaps are investigated. We find that the distribution of price gaps has a power-law tail for all stocks with an average tail exponent close to 3.2. Applying modern statistical methods, we confirm that the gap time series are long-range correlated and possess multifractal nature. These three features vary from stock to stock and are not universal. Furthermore, we also unveil buy-sell asymmetry phenomena in the properties of price gaps on the buy and sell sides of the LOBs for individual stocks. These findings deepen our understanding of the dynamics of liquidity of common stocks and can be used to calibrate agent-based computational financial models. JEL classification: G10, C14

keywords:

Price gap, Limit order book, Liquidity, Stylized facts, Buy-sell asymmetry1 Introduction

It is a key stylized fact that returns over small time scales have power-law tails (Mandelbrot, 1963; Mantegna and Stanley, 1995; Gopikrishnan et al., 1999; Plerou et al., 1999; Bertram, 2004; Coronel-Brizio and Hernández-Montoya, 2005; Zhang et al., 2007; Pan and Sinha, 2008; Tabak et al., 2009; Mu and Zhou, 2010; Yang et al., 2013; Liang et al., 2013), which means that large price changes occur more frequently than normal distribution. This phenomenon has important application in the domain of risk management, and it is necessary to understand the origins of large price fluctuations.

It is well-documented that trading volume is a key determinant to move stock prices. The relationship between price fluctuation and trading volume over certain time period has been extensively studied (Karpoff, 1987). There is numerous evidence showing that the magnitude of price fluctuation positively correlates to the trading volume at different time scales from one minute to one month (Wood et al., 1985; Jain and Joh, 1988; Ying, 1966; Epps, 1977; Harris, 1987; Gallant et al., 1992; Richardson et al., 1986; Rogalski, 1978; Saatcioglu and Starks, 1998). The price-volume relation is usually asymmetric at the aggregate level in the sense that the price impact of a selling volume is larger than a buying volume of the same size (Karpoff, 1987). At the transaction level, theoretical and empirical analyses show that the price impact function is nonlinear (Loeb, 1983; Perold and Salomon, 1991; Zhang, 1999; Farmer, 2002; Almgren, 2003; Gabaix et al., 2003a, b; Lillo et al., 2003; Farmer and Lillo, 2004; Plerou et al., 2004; Lim and Coggins, 2005; Gabaix et al., 2006, 2007; Zhou, 2012a, c). At the transaction level, there is no buy-sell asymmetry in the price impact function (Zhou, 2012c).

Trading volume or trade size is certainly not the solo driving force of price fluctuations. Farmer et al. (2004) find that large price fluctuations of stocks traded on the London Stock Exchange are essentially independent of the volume of orders, but rather driven by liquidity fluctuations characterized by the gaps between the first few occupied price levels on the opposite limit order book. After investigating the TAQ data and order book data from the Island ECN, Weber and Rosenow (2006) argue that a large trading volume alone is not sufficient to explain large price changes and a lack of liquidity is a necessary prerequisite for the occurrence of large price fluctuations. Næs and Skjeltorp (2006) study the order flow data from the Oslo Stock Exchange and find that price fluctuations are positively correlated with trade number, a component of trading volume, and negatively correlated with different liquidity measures. Joulin et al. (2008) analyze the one-minute data of 163 USA stocks and find that news and trading volume play a minor role in causing large price changes. They conjecture that large price fluctuations are caused by the vanishing of liquidity. Based on the order flow data of Chinese stocks, Zhou (2012a) finds that trade size, bid-ask spread, price gaps, and outstanding volumes all play a significant role in driving price fluctuations.

Bid-ask spread, price gap and standing volume on the LOBs are all fundamental ingredients of liquidity. The statistical properties of bid-ask spreads and volumes have been investigated for many financial markets (Chakraborti et al., 2011; Gould et al., 2013). However, only a few studies concern with the statistical properties of price gaps in financial markets. Farmer et al. (2004) analyze the probability distribution of price gaps of a few stocks traded on London Stock Exchange and find that price gaps approximately follow a power-law distribution with the tail exponents varying from about 1.6 to 2.8. Lallouache and Abergel (2013) focus on the EUR/USD and USD/JPY foreign exchange data from the Electronic Broking Service (EBS) Spot platform. They study the relation between the average gaps (in units of ticks) and price levels in the LOB and find that decimalized gaps decrease with the price levels in both buy and sell LOBs which do not change with time.

In this work, based on the order flow data of 26 A-share stocks traded on the Shenzhen Stock Exchange, we rebuild the LOBs according to the continuous double auction mechanism. We study the empirical statistical properties of the price gaps on the buy and sell LOBs. The rest of this paper is organized as follows. Section 2 briefly introduces the database we analyze. In Section 3, we investigate the probability distributions of price gaps. Section 4 estimates the memory effect of gap series using advanced statistical methods. We further investigate its multifractal nature in Section 5. Finally, we summarize the results in Section 6.

2 Dateset

Our study is based on the order flow data of 26 liquid stocks traded on the Shenzhen Stock Exchange, covering the whole year of 2003. The Shenzhen Stock Exchange adopts the continuous double auction mechanism, which was established on December 1, 1990 and started its operation on July 3, 1991. There are two kinds of independent markets on the SZSE, i.e., A-share market and B-share market. Both of them are open to mainland Chinese companies. The A-share market is traded in CNY and restricted to domestic investors, while the B-share market is traded in HKD and only open to foreign investors before February 19, 2001 since when it has been open to the domestic investors as well. Each A-share stock forms its open price through the call auction mechanism and enters the continuous double auction period since 9:30 in the morning. We focus on the data in the continuous double auction period.

There are 26 A-share stocks in our analysis, including Ping An Bank Co., Ltd. (000001), China Baoan Group Co., Ltd. (000009), CSG Holding Co., Ltd. (000012), Konka Group Co., Ltd. (000016), Shenzhen Kaifa Technology Co., Ltd. (000021), China Merchants Property Development Co., Ltd. (000024), Great Wall Computer Shenzhen Co., Ltd. (000066), Sinopec Shengli Oil Field Dynamic Group Co., Ltd. (000406), Guangdong Provincial Expressway Development Co., Ltd. (000429), Shandong Chenming Paper Holdings Co., Ltd. (000488), Guangdong Electric Power Development Co., Ltd. (000539), Foshan Electrical and Lighting Co., Ltd. (000541), Jiangling Motors Co., Ltd. (000550), Weifu High-Technology Group Co., Ltd. (000581), Chongqing Changan Automobile Co., Ltd. (000625), Hebei Iron and Steel Co., Ltd. (000709), Xinxing Ductile Iron Pipes Co., Ltd. (000778), Faw Car Co., Ltd. (000800), Shanxi Taigang Stainless Steel Co., Ltd. (000825), Citic Guoan Information Industry Co., Ltd. (000839), Wuliangye Yibin Co., Ltd. (000858), Angang Steel Co., Ltd. (000898), Hunan TV and Broadcast Intermediary Co., Ltd. (000917), Hunan Valin Steel Co., Ltd. (000932), Sinopec Zhongyuan Petroleum Co., Ltd. (000956), and Shanxi Xishan Coal and Electricity Power Co., Ltd. (000983).

The database records the order flows of the aforementioned stocks in 2003. It contains the details of order placement and order cancellation, including the order submitting time, order price, order size and order identifier which identifies whether the submitted order is a buy order, a sell order, or a cancelation. The time stamp is accurate to 0.01 second. We rebuilt the order book with respect to the placed orders and and cancelled orders according to the price-time priority rule (Gu et al., 2008a, b, c). At each event time defined as a submitted or a cancelled order, we obtain the buy-side and sell-side LOBs, on which unexecuted limit orders occupy different price levels at , , , from low to high on the sell LOB and , , , from high to low on the buy LOB. The price gap investigated in this work is defined as the absolute logarithmic difference between the first occupied price level (best bid or best ask) and the second occupied price level on the buy or sell LOB:

| (1) |

Table 1 presents the basic statistics of the price gaps.

The second column and the ninth column of Table 1 show the order flow rate defined as the number of submitted order per minute. It is observed that the order flow rate varies remarkably from stock to stock, and not surprisingly strongly correlates with . We further find that for 4 stocks and for 22 stocks. The third and tenth columns present the ratio of the number of gaps equaling to the tick size (0.01 CNY) to the total number of gaps for each stock. The value of varies from 0.73 to 0.99 for buy LOBs and from 0.70 to 0.99 for sell LOBs. It is not unexpected that correlates strongly with . A closer scrutiny unveils that for 24 stocks.

The rest columns give the mean, median, standard deviation, skewness, and kurtosis of the gaps on each side of the LOB for each stock. These statistics vary from stock to stock. We observe strong correlations between the corresponding means of the price gaps on the buy and sell LOBs, so do the medians. Such buy-sell correlations are much weaker for other statistics. There are 22 stocks with larger mean gaps on the buy side. All the gap distributions are right skewed as expected because the mean gaps span less than two ticks. There are 24 stocks whose skewness of gaps on the buy LOB is greater than that on the sell LOB. We also find that all the gap distributions have large kurtosis and there are 23 stocks with greater kurtosis of the gaps on the buy LOBs.

| Buy LOB | Sell LOB | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Stock | mean | median | s.t.d. | skewness | kurtosis | mean | median | s.t.d. | skewness | kurtosis | |||||

| 000001 | 34.31 | 0.95 | 0.00098 | 0.00089 | 0.00036 | 8.77 | 164.4 | 30.95 | 0.94 | 0.00100 | 0.00089 | 0.00043 | 8.47 | 145.1 | |

| 000009 | 17.74 | 0.98 | 0.00201 | 0.00194 | 0.00041 | 13.84 | 456.1 | 18.96 | 0.98 | 0.00201 | 0.00193 | 0.00045 | 9.53 | 232.1 | |

| 000012 | 10.12 | 0.84 | 0.00123 | 0.00095 | 0.00088 | 9.00 | 178.2 | 9.52 | 0.81 | 0.00129 | 0.00097 | 0.00090 | 4.89 | 44.2 | |

| 000016 | 6.01 | 0.88 | 0.00151 | 0.00128 | 0.00087 | 15.94 | 672.5 | 6.39 | 0.85 | 0.00157 | 0.00128 | 0.00098 | 11.37 | 357.2 | |

| 000021 | 14.20 | 0.82 | 0.00099 | 0.00081 | 0.00062 | 5.13 | 54.6 | 14.73 | 0.79 | 0.00103 | 0.00081 | 0.00069 | 4.88 | 49.8 | |

| 000024 | 4.09 | 0.80 | 0.00129 | 0.00098 | 0.00097 | 8.84 | 189.5 | 4.87 | 0.79 | 0.00133 | 0.00098 | 0.00104 | 5.68 | 56.8 | |

| 000066 | 9.78 | 0.86 | 0.00120 | 0.00100 | 0.00074 | 21.62 | 2110.5 | 10.35 | 0.84 | 0.00125 | 0.00101 | 0.00077 | 5.46 | 59.5 | |

| 000406 | 9.67 | 0.94 | 0.00132 | 0.00122 | 0.00052 | 18.10 | 791.8 | 9.54 | 0.93 | 0.00134 | 0.00122 | 0.00055 | 13.38 | 673.7 | |

| 000429 | 3.86 | 0.94 | 0.00201 | 0.00187 | 0.00086 | 27.12 | 2217.2 | 4.26 | 0.92 | 0.00206 | 0.00187 | 0.00095 | 7.08 | 93.9 | |

| 000488 | 3.70 | 0.75 | 0.00122 | 0.00103 | 0.00107 | 12.02 | 280.9 | 3.79 | 0.75 | 0.00125 | 0.00102 | 0.00095 | 4.36 | 34.6 | |

| 000539 | 3.62 | 0.75 | 0.00143 | 0.00098 | 0.00144 | 11.33 | 295.4 | 3.46 | 0.75 | 0.00142 | 0.00098 | 0.00122 | 4.97 | 45.3 | |

| 000541 | 2.17 | 0.78 | 0.00123 | 0.00088 | 0.00122 | 14.18 | 371.5 | 2.42 | 0.72 | 0.00134 | 0.00088 | 0.00127 | 12.40 | 411.1 | |

| 000550 | 11.18 | 0.84 | 0.00116 | 0.00096 | 0.00065 | 5.37 | 65.5 | 12.08 | 0.81 | 0.00121 | 0.00097 | 0.00075 | 5.01 | 50.0 | |

| 000581 | 3.03 | 0.75 | 0.00133 | 0.00092 | 0.00117 | 9.68 | 337.3 | 3.68 | 0.71 | 0.00142 | 0.00092 | 0.00137 | 14.15 | 637.5 | |

| 000625 | 11.89 | 0.75 | 0.00108 | 0.00087 | 0.00090 | 17.44 | 1022.5 | 12.51 | 0.72 | 0.00115 | 0.00088 | 0.00092 | 5.65 | 94.6 | |

| 000709 | 7.28 | 0.97 | 0.00185 | 0.00191 | 0.00061 | 11.30 | 274.3 | 7.66 | 0.97 | 0.00185 | 0.00191 | 0.00056 | 7.42 | 134.0 | |

| 000778 | 4.88 | 0.86 | 0.00111 | 0.00090 | 0.00074 | 9.41 | 214.5 | 5.86 | 0.84 | 0.00112 | 0.00090 | 0.00069 | 6.37 | 94.5 | |

| 000800 | 17.81 | 0.90 | 0.00125 | 0.00109 | 0.00057 | 7.05 | 113.8 | 22.58 | 0.89 | 0.00126 | 0.00109 | 0.00058 | 5.33 | 57.9 | |

| 000825 | 14.01 | 0.99 | 0.00205 | 0.00201 | 0.00033 | 10.84 | 226.7 | 15.98 | 0.98 | 0.00208 | 0.00200 | 0.00058 | 10.47 | 146.7 | |

| 000839 | 20.08 | 0.83 | 0.00083 | 0.00065 | 0.00054 | 6.56 | 102.3 | 20.96 | 0.79 | 0.00087 | 0.00066 | 0.00064 | 6.06 | 77.2 | |

| 000858 | 8.91 | 0.88 | 0.00112 | 0.00097 | 0.00058 | 7.64 | 140.3 | 9.97 | 0.87 | 0.00114 | 0.00097 | 0.00063 | 6.72 | 94.8 | |

| 000898 | 17.73 | 0.99 | 0.00232 | 0.00235 | 0.00042 | 6.55 | 170.3 | 24.14 | 0.99 | 0.00230 | 0.00234 | 0.00040 | 4.43 | 76.2 | |

| 000917 | 5.98 | 0.73 | 0.00113 | 0.00080 | 0.00087 | 9.38 | 566.9 | 6.25 | 0.70 | 0.00123 | 0.00081 | 0.00104 | 4.54 | 38.2 | |

| 000932 | 11.49 | 0.99 | 0.00194 | 0.00189 | 0.00031 | 13.28 | 339.6 | 13.52 | 0.98 | 0.00194 | 0.00188 | 0.00040 | 26.16 | 1417.5 | |

| 000956 | 12.72 | 0.91 | 0.00105 | 0.00094 | 0.00049 | 7.00 | 86.5 | 14.04 | 0.89 | 0.00106 | 0.00094 | 0.00051 | 6.56 | 86.4 | |

| 000983 | 6.17 | 0.89 | 0.00144 | 0.00125 | 0.00074 | 13.33 | 981.2 | 8.34 | 0.90 | 0.00143 | 0.00125 | 0.00069 | 5.53 | 61.0 | |

3 Probability distribution

Price gap is a significant determinant of immediate price impact (Zhou, 2012a), and the distribution of price gaps is directly related to the distribution of immediate price changes (Farmer et al., 2004). In this section, we will investigate the distribution of gaps on both buy and sell LOBs for individual stocks. By looking at the empirical distributions of price gaps for the 26 stocks, we conjecture that these distributions have power-law tails:

| (2) |

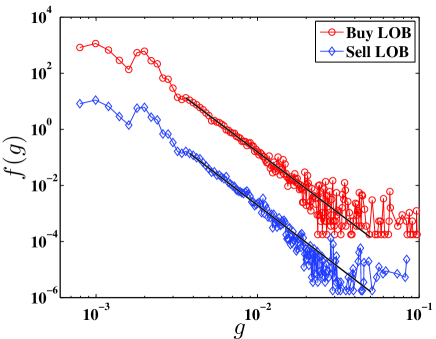

where is the power-law exponent and is the lower threshold of the scaling range of the power-law decay. We aggregate the gaps of all the stocks together and treat them as an ensemble. Figure 1 illustrates the empirical probability distributions of ensemble gaps on the buy LOB and the sell LOB. Evident power-law tails are observed. In addition, we see local humps in the distributions especially around and . These humps are caused by the discreteness of the tick size and correspond to one and two ticks. These features are more evident for individual stocks.

To have a deeper understanding of the tail behavior, we need to conduct objective analysis. Based on the Kolmogorov-Smirnov test, Clauset et al. (2009) propose an efficient quantitative method to test if the tail have a power-law form and, if so, to estimate the power-law exponent for the data greater than or equal to the threshold . We describe briefly the method of Clauset et al. (2009), which has been extensively applied in many fields. The Kolmogorov-Smirnov statistic () is defined as

| (3) |

where is the cumulative distribution of gaps and is the cumulative distribution of the best power-law fit. The threshold is determined by minimizing the statistic. Then the power-law exponent of the data in the range can be estimated using the maximum likelihood estimation (MLE) method, that is,

| (4) |

where is the number of the data points in the range . The standard error on the power-law exponent is derived from the width of the likelihood maximum, which reads

| (5) |

Applying this approach to the ensemble data shown in Fig. 1, we have with and for the buy LOB of ensemble gaps and with and . We also analyze individual stocks and present the minimal gaps, the tail exponents, and the standard deviations for each stock in Table 2. For buy LOBs, the value of varies in the range with the mean value . For sell LOBs, the tail exponent fluctuates in the range with the mean value . It is clear that the mean values and are similar to the power-law tail exponents obtained from ensemble gaps. However, the tail exponents of individual stocks have larger standard deviations. For stocks traded on the London Stock Exchange, Farmer et al. (2004) find that the tail exponents vary from about 1.6 to 2.8 and the tail exponents of gaps and returns are almost identical. They thus argue that large price changes are mainly caused by price gaps. Although the tail exponents of gaps of Chinese stocks are systemically greater than those of British stocks, the tail exponents of gaps and returns of Chinese stocks are also very close (Zhou, 2012c), seemingly supporting the conjecture of Farmer et al. (2004).

| Buy LOB | Sell LOB | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Stock | -value | -value | |||||||||

| 000001 | 0.0025 | 3.16 | 0.018 | 0.057 | 1.00 | 0.0016 | 2.98 | 0.007 | 0.057 | 1.00 | |

| 000009 | 0.0034 | 4.29 | 0.023 | 0.072 | 1.00 | 0.0035 | 4.52 | 0.020 | 0.082 | 1.00 | |

| 000012 | 0.0026 | 2.64 | 0.012 | 0.049 | 1.00 | 0.0010 | 2.16 | 0.003 | 0.059 | 1.00 | |

| 000016 | 0.0026 | 3.04 | 0.014 | 0.038 | 1.00 | 0.0022 | 3.11 | 0.010 | 0.041 | 1.00 | |

| 000021 | 0.0016 | 3.05 | 0.007 | 0.051 | 1.00 | 0.0016 | 2.84 | 0.006 | 0.058 | 1.00 | |

| 000024 | 0.0025 | 2.74 | 0.015 | 0.069 | 1.00 | 0.0026 | 2.68 | 0.013 | 0.074 | 1.00 | |

| 000066 | 0.0029 | 3.29 | 0.018 | 0.025 | 1.00 | 0.0029 | 3.22 | 0.015 | 0.041 | 1.00 | |

| 000406 | 0.0022 | 4.02 | 0.016 | 0.048 | 1.00 | 0.0022 | 4.03 | 0.014 | 0.062 | 1.00 | |

| 000429 | 0.0032 | 3.55 | 0.021 | 0.059 | 1.00 | 0.0032 | 3.11 | 0.016 | 0.060 | 1.00 | |

| 000488 | 0.0026 | 2.51 | 0.017 | 0.048 | 1.00 | 0.0028 | 2.97 | 0.018 | 0.048 | 1.00 | |

| 000539 | 0.0026 | 2.38 | 0.012 | 0.053 | 1.00 | 0.0026 | 2.47 | 0.012 | 0.076 | 1.00 | |

| 000541 | 0.0032 | 2.65 | 0.026 | 0.055 | 1.00 | 0.0032 | 3.06 | 0.024 | 0.046 | 1.00 | |

| 000550 | 0.0022 | 3.04 | 0.011 | 0.051 | 1.00 | 0.0017 | 2.66 | 0.006 | 0.060 | 1.00 | |

| 000581 | 0.0024 | 2.55 | 0.013 | 0.058 | 1.00 | 0.0024 | 2.49 | 0.011 | 0.060 | 1.00 | |

| 000625 | 0.0023 | 2.86 | 0.010 | 0.021 | 1.00 | 0.0025 | 2.95 | 0.010 | 0.039 | 1.00 | |

| 000709 | 0.0027 | 2.97 | 0.019 | 0.074 | 0.80 | 0.0027 | 3.26 | 0.019 | 0.079 | 0.99 | |

| 000778 | 0.0025 | 2.92 | 0.018 | 0.045 | 1.00 | 0.0024 | 3.23 | 0.019 | 0.055 | 1.00 | |

| 000800 | 0.0019 | 3.26 | 0.008 | 0.051 | 1.00 | 0.0028 | 3.64 | 0.015 | 0.040 | 1.00 | |

| 000825 | 0.0043 | 3.41 | 0.048 | 0.131 | 0.00 | 0.0035 | 2.93 | 0.039 | 0.106 | 0.00 | |

| 000839 | 0.0027 | 3.50 | 0.018 | 0.025 | 1.00 | 0.0027 | 3.42 | 0.015 | 0.046 | 1.00 | |

| 000858 | 0.0027 | 3.54 | 0.022 | 0.053 | 1.00 | 0.0028 | 3.42 | 0.019 | 0.063 | 1.00 | |

| 000898 | 0.0049 | 4.35 | 0.056 | 0.172 | 0.00 | 0.0049 | 4.60 | 0.069 | 0.175 | 0.00 | |

| 000917 | 0.0014 | 2.50 | 0.006 | 0.044 | 1.00 | 0.0013 | 2.19 | 0.005 | 0.044 | 1.00 | |

| 000932 | 0.0041 | 3.59 | 0.053 | 0.215 | 0.00 | 0.0042 | 3.26 | 0.046 | 0.226 | 0.00 | |

| 000956 | 0.0026 | 3.52 | 0.019 | 0.055 | 1.00 | 0.0025 | 3.67 | 0.019 | 0.061 | 1.00 | |

| 000983 | 0.0022 | 3.46 | 0.012 | 0.065 | 1.00 | 0.0022 | 3.40 | 0.012 | 0.057 | 1.00 | |

Following Clauset et al. (2009), we perform bootstrap test if the gap distributions have power-law tails. In doing so, we generate 100 realizations of gaps for each distribution. For each realization, we compute the KS statistic as follows:

| (6) |

where is the cumulative distribution of the simulated realization. We thus obtain the -value:

| (7) |

where the numerator is the number of realizations with . The meaning of this rest is that the investigated gaps have the power-law distribution with a probability of . The resulting values and the corresponding -values are given in Table 2. It is found that three stocks have a -value of zero, while other stocks have very large -values. This test confirms that most stocks have power-law tails in the gap distributions.

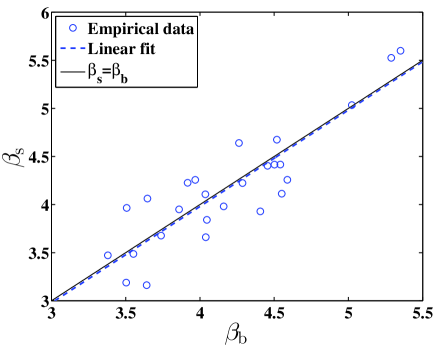

We further illustrate the relation between and in Fig. 2, and quantitatively analyze the linear relation between them using the robust regression, which reads

| (8) |

where the numbers in parentheses are the -values of the coefficients. We find that the intercept is insignificantly different from zero, while the coefficient of is evidently significant with the -value close to zero. It is clear that the fitted dash line from the robust regressing method almost overlaps with the solid line . Therefore, although there is certain buy-sell asymmetry in the tail distributions of gaps for individual stocks, the tail behaviors of gaps on the two LOBs for a same stock share great similarity.

4 Long-range correlation

In this section, we investigate if there are long-range corrections in gap time series. There are many methods proposed to estimate the memory effect of time series (Taqqu et al., 1995; Bashan et al., 2008; Barunik and Kristoufek, 2010), such as rescaled range (RS) analysis (Hurst, 1951), fluctuation analysis (FA) (Peng et al., 1992), wavelet transform module maxima (WTMM) (Holschneider, 1988; Muzy et al., 1991), detrended fluctuation analysis (DFA) (Peng et al., 1994), and detrending moving average (DMA) (Alessio et al., 2002), to list a few. We adopt the DFA and DMA algorithms, which are among the most effective and the most extensively used methods (Shao et al., 2012).

For a given price gap time series , we calculate the cumulative summation series as follows,

| (9) |

where is the sample mean of the series. The series is covered by disjoint boxes with the same size . When the whole series cannot be completely covered by boxes, we can utilize boxes to cover the series from both ends of the series. In each box, a trend function of the sub-series is determined. The residuals are calculated by

| (10) |

There are many different methods for the determination of . The local detrending functions could be polynomials, which recovers the DFA method (Peng et al., 1994; Hu et al., 2001). The local detrending function could also be the moving averages, resulting in the DMA algorithm (Vandewalle and Ausloos, 1998; Alessio et al., 2002; Xu et al., 2005; Arianos and Carbone, 2007).

The local fluctuation function in the -th box is defined as the r.m.s. of the residuals:

| (11) |

The overall fluctuation function is calculated as follows:

| (12) |

For most time series with fractal nature, one has:

| (13) |

where can be roughly viewed as the Hurst exponent. If is significantly greater than 0.5, the time series is positively correlated. If is insignificantly different from 0.5, the time series is uncorrelated. If is significantly smaller than 0.5, the time series is negatively correlated. When is compared with 0.5, statistical tests are necessary (Jiang et al., 2014).

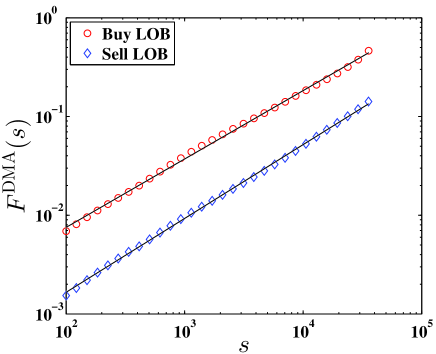

We first choose the centred detrending moving average (CDMA) method, which has a better performance than the backward detrending moving average (BDMA) method and the forward detrending moving average (FDMA) method for the positively correlated time series (Arianos and Carbone, 2007). Figure 3 presents the DMA detrended fluctuation functions with respect to the scale sizes for the gap series on both buy and sell LOBs of the stock 000016. It is obvious that the empirical data points all collapse to the fitting line, indicating an evident power-law scaling relation between the fluctuation function and the scale size :

| (14) |

where is known as the DMA scaling exponent. Using the least squares fitting method, we obtain the scaling exponent for the buy LOB and for the sell LOB of the stock 000016.

We then calculate the DMA scaling exponents for the rest stocks, and the results are listed in Table 3. The exponent varies in the range with the mean value for buy LOBs and the exponent fluctuates in the range with the mean value for sell LOBs. Since the DMA scaling exponents are obviously larger than 0.5, we conclude that the gap series process long memory for both buy and sell LOBs of 26 stocks.

| Buy LOB | Sell LOB | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Stock | ||||||||||||

| 000001 | 0.797 | 0.499 | 0.797 | 0.501 | 0.811 | 0.501 | 0.804 | 0.501 | ||||

| 000009 | 0.773 | 0.500 | 0.750 | 0.500 | 0.786 | 0.500 | 0.763 | 0.499 | ||||

| 000012 | 0.744 | 0.500 | 0.750 | 0.500 | 0.771 | 0.499 | 0.780 | 0.500 | ||||

| 000016 | 0.710 | 0.502 | 0.714 | 0.500 | 0.762 | 0.499 | 0.765 | 0.501 | ||||

| 000021 | 0.756 | 0.500 | 0.742 | 0.500 | 0.762 | 0.500 | 0.769 | 0.500 | ||||

| 000024 | 0.717 | 0.503 | 0.737 | 0.500 | 0.756 | 0.499 | 0.762 | 0.501 | ||||

| 000066 | 0.736 | 0.501 | 0.744 | 0.501 | 0.744 | 0.501 | 0.749 | 0.500 | ||||

| 000406 | 0.732 | 0.500 | 0.739 | 0.500 | 0.768 | 0.501 | 0.774 | 0.500 | ||||

| 000429 | 0.715 | 0.502 | 0.724 | 0.501 | 0.719 | 0.500 | 0.729 | 0.499 | ||||

| 000488 | 0.757 | 0.499 | 0.772 | 0.500 | 0.773 | 0.499 | 0.788 | 0.500 | ||||

| 000539 | 0.755 | 0.497 | 0.762 | 0.499 | 0.788 | 0.501 | 0.795 | 0.500 | ||||

| 000541 | 0.740 | 0.499 | 0.739 | 0.499 | 0.751 | 0.498 | 0.761 | 0.500 | ||||

| 000550 | 0.716 | 0.498 | 0.723 | 0.500 | 0.738 | 0.498 | 0.761 | 0.500 | ||||

| 000581 | 0.737 | 0.499 | 0.745 | 0.500 | 0.773 | 0.500 | 0.785 | 0.499 | ||||

| 000625 | 0.727 | 0.500 | 0.725 | 0.500 | 0.779 | 0.502 | 0.780 | 0.500 | ||||

| 000709 | 0.754 | 0.501 | 0.732 | 0.500 | 0.762 | 0.500 | 0.743 | 0.499 | ||||

| 000778 | 0.748 | 0.501 | 0.752 | 0.501 | 0.747 | 0.500 | 0.758 | 0.500 | ||||

| 000800 | 0.747 | 0.500 | 0.754 | 0.500 | 0.773 | 0.500 | 0.781 | 0.500 | ||||

| 000825 | 0.784 | 0.501 | 0.787 | 0.500 | 0.876 | 0.501 | 0.881 | 0.501 | ||||

| 000839 | 0.766 | 0.501 | 0.767 | 0.501 | 0.775 | 0.500 | 0.777 | 0.501 | ||||

| 000858 | 0.723 | 0.500 | 0.744 | 0.499 | 0.773 | 0.501 | 0.773 | 0.501 | ||||

| 000898 | 0.791 | 0.501 | 0.727 | 0.501 | 0.749 | 0.500 | 0.697 | 0.499 | ||||

| 000917 | 0.728 | 0.501 | 0.733 | 0.500 | 0.772 | 0.500 | 0.779 | 0.501 | ||||

| 000932 | 0.752 | 0.500 | 0.750 | 0.500 | 0.744 | 0.501 | 0.742 | 0.498 | ||||

| 000956 | 0.765 | 0.500 | 0.768 | 0.500 | 0.766 | 0.501 | 0.773 | 0.501 | ||||

| 000983 | 0.755 | 0.499 | 0.756 | 0.500 | 0.735 | 0.502 | 0.730 | 0.501 | ||||

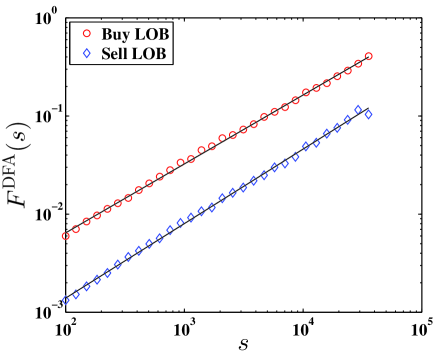

We alternatively apply the detrended fluctuation analysis (DFA) method to confirm the long memory effect in gap series. Figure 4 depicts the DFA detrended fluctuation functions as a function of the scale size for both buy and sell LOBs of the same stock 000016. We observe perfect power-law scaling relation between the fluctuation function and the scale size :

| (15) |

where is DFA scaling exponent. Using the least-squares fitting method, we obtain for the buy LOB and for the sell LOB of stock 000016.

We also estimate the memory effect of the rest stocks with the DFA method. The DFA scaling exponents of 26 stocks are presented in Table 3 as well. We find that the scaling exponent varies from 0.714 to 0.797 with the mean value for buy LOBs, and the exponent fluctuates from 0.697 to 0.881 with the mean value for sell LOBs. Since the scaling exponents calculated from the two methods obviously larger than 0.5, It is believed that the gap series on both buy and sell LOBs of 26 stocks process long memory.

On the other hand, the probability distribution of gaps may affect its memory effect. In order to test the distribution effect, we first shuffle the gap series of each stock for 100 times, then obtain the shuffled scaling exponents and based on the DMA and DFA methods, respectively. The average values of 100 shuffled gap series are also illustrated in Table 3. It is clear that the values of and for both buy and sell LOBs extremely approach to 0.5 which are obviously smaller than the original ones. So we make a conclusion that the probability distribution of gap series does not affect the memory effect, and confirm that gap series truly process significant long memory for all the 26 stocks.

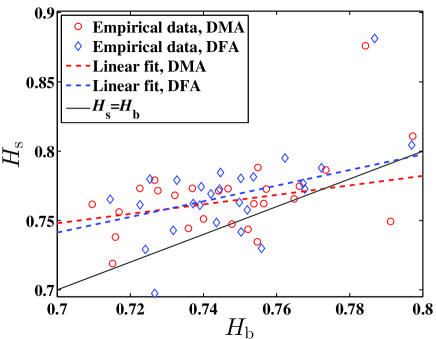

We then analyze the linear relation between and for all 26 stocks with DMA and DFA methods, which are showed in Fig. 5(a). With the robust regressing method, for the DMA method we have the following linear relation,

| (16) |

and for the DFA method we have

| (17) |

where the numbers in parentheses are the -values of the coefficients. We find that the coefficients are significant at the 10% level for the DMA method and at the 5% level for the DFA method. According to Table 3 and Fig. 5(a), most stocks have .

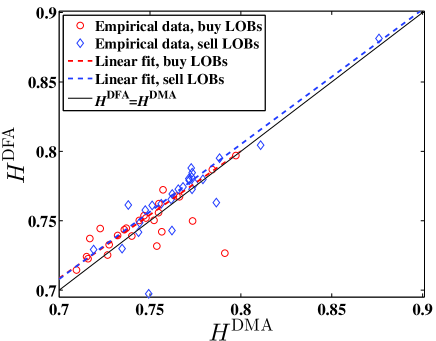

In order to compare the results obtained from the DMA method with the DFA method, we investigate the relation between the DMA scaling exponents and the DFA scaling exponents for both buy and sell LOBs of the 26 stocks. The results are presented in Fig. 5(b). We observe that and are linearly correlated. With the robust regression method, for buy LOBs we have

| (18) |

and for sell LOBs we have

| (19) |

where the numbers in parentheses are the -values of the coefficients. In the regression equation the intercept is not significant for the two methods, while the coefficients of and are significant with the -values close to zero. We conclude that both DMA and DFA methods unveil significant long-term correlations in the gap time series and both methods give quantitatively similar results.

5 Multifractal nature

We now turn to study the possible presence of nonlinear correlations in the gap time series through multifractal analysis. We adopt the multifractal detrended fluctuation analysis proposed Kantelhardt et al. (2002). We note that there are other methods that can be used for multifractal analysis (Di Matteo et al., 2005). We calculate the th-order detrended fluctuation function as follow:

| (20) |

where can take any real value except for . When , we have

| (21) |

according to L’Hôspital’s rule. Varying the values of segment size , we can determine the power-law relation between the function and the size scale ,

| (22) |

where is the MF-DFA scaling exponent. When , is exactly the DFA scaling exponent .

Figure 6 illustrates the fluctuation functions as a function of the scale sizes for the buy LOB of stock 000016. We observe that the functions for different have nice power-law scaling with respect to . Using least-squares linear regressions, we can obtain the scaling exponent . It is obvious that the scaling exponent decreases with the order . These observations are also present for price gap time series on the sell LOBs and for other stocks.

Based on the MF-DFA scaling exponent , we can calculate the multifractal scaling exponent for one dimensional time series through

| (23) |

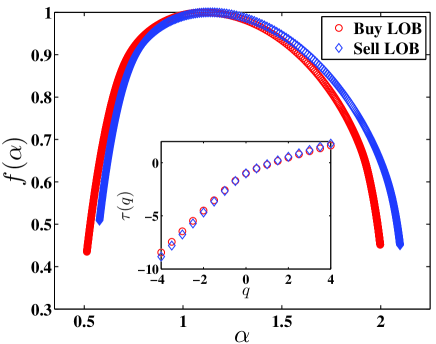

According to the standard multifractal formalism, if the scaling exponent is a nonlinear function of , the time series is considered to process multifractal nature. The scaling exponents for both buy and sell LOBs of stock 000016 are presented in the inset of Fig. 7. It is evident that the exponents is nonlinear with regard to the order , suggesting that the gap time series has multifractality.

Based on the Legendre transform, one obtains the singularity strength function and the multifractal spectrum (Halsey et al., 1986):

| (24) |

Figure 7 shows the multifractal spectra as a function of the singularity strength for both buy and sell LOBs of stock 000016.

The strength of multifractality can be quantitatively measured by the width of the multifractal spectrum, i.e., . A larger value of corresponds to stronger multifractality. We obtain that for the buy LOB and for the sell LOB of stock 000016. Since the values of are evidently larger than zero, it indicates that the gap series processes multifractality, which is consistent with the nonlinearity in the scaling exponent . The results for all the investigated stocks are listed in Table 4. The value of varies in the range with an average value for buy LOBs. The value of fluctuates in the range with an average value for sell LOBs. Since are all larger than zero, the gap time series of the 26 stocks have multifractality.

| Buy LOB | Sell LOB | ||||

|---|---|---|---|---|---|

| Stock | |||||

| 000001 | 1.27 | 0.24 | 1.18 | 0.23 | |

| 000009 | 1.34 | 0.27 | 1.30 | 0.28 | |

| 000012 | 1.48 | 0.27 | 1.43 | 0.26 | |

| 000016 | 1.48 | 0.33 | 1.52 | 0.32 | |

| 000021 | 1.37 | 0.24 | 1.43 | 0.23 | |

| 000024 | 1.63 | 0.26 | 1.60 | 0.27 | |

| 000066 | 1.44 | 0.29 | 1.42 | 0.28 | |

| 000406 | 1.43 | 0.36 | 1.38 | 0.33 | |

| 000429 | 1.41 | 0.38 | 1.57 | 0.40 | |

| 000488 | 1.52 | 0.30 | 1.53 | 0.29 | |

| 000539 | 1.86 | 0.26 | 1.89 | 0.27 | |

| 000541 | 1.80 | 0.29 | 1.91 | 0.27 | |

| 000550 | 1.40 | 0.25 | 1.41 | 0.24 | |

| 000581 | 1.83 | 0.28 | 1.80 | 0.26 | |

| 000625 | 1.39 | 0.21 | 1.34 | 0.20 | |

| 000709 | 1.38 | 0.21 | 1.40 | 0.20 | |

| 000778 | 1.57 | 0.30 | 1.57 | 0.29 | |

| 000800 | 1.31 | 0.22 | 1.20 | 0.22 | |

| 000825 | 1.25 | 0.31 | 1.12 | 0.34 | |

| 000839 | 1.29 | 0.22 | 1.31 | 0.21 | |

| 000858 | 1.50 | 0.28 | 1.49 | 0.27 | |

| 000898 | 1.34 | 0.15 | 1.31 | 0.15 | |

| 000917 | 1.49 | 0.24 | 1.62 | 0.23 | |

| 000932 | 1.38 | 0.35 | 1.36 | 0.34 | |

| 000956 | 1.33 | 0.28 | 1.32 | 0.24 | |

| 000983 | 1.50 | 0.32 | 1.50 | 0.33 | |

Multifractality may be influenced by the probability distribution of gaps. With the same test method as memory effect in Sec. 4, we first shuffle the gap series for 100 times, then calculate the width of the multifractal spectrum for each shuffled time series based on the MFDFA method. The average values from 100 shuffled series for each of the 26 stocks are also presented in Table 4. Since the values of are larger than zero, the distribution of gaps generates certain degree of spurious multifractality, which is probably due to the finite-size effect (Zhou, 2012b). For each gap time series, or is significantly greater than , which means that the multifractal nature is intrinsic and not caused by the strong linear correlations quantified in Sec. 4.

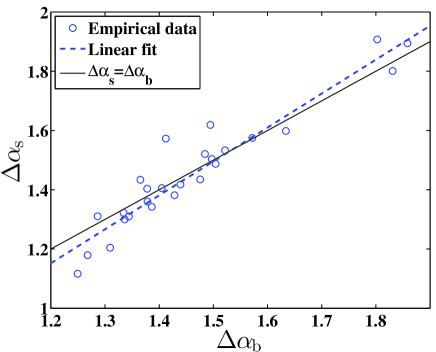

We also compare the spectrum width of buy LOBs with the ones of sell LOBs for all the stocks which are illustrated in Fig. 8. There is an evident linear relationship and a robust linear regression gives

| (25) |

where the numbers in parentheses are the -values of the coefficients. The coefficients obtained from the regression are significant at the 5% level, especially for the coefficient of whose -value is close to zero. These findings suggest that the multifractal nature changes from stock to stock and is thus not universal. Furthermore, the gap time series on the buy and sell LOBs share similar multifractal nature.

6 Conclusion

In summary, we have investigated the statistical properties of the price gaps defined as the absolute logarithmic difference between the first occupied price level and second occupied price level on the LOBs based on order flow databases of 26 liquid A-share stocks. First, we study the probability distribution of gaps in both buy and sell LOBs, and find that the cumulative distribution function follows the power-law distribution in the tail with the average scaling exponent approaching 3.2. Then we investigate the memory effect of gap series using the detrending moving average (DMA) method and the detrended fluctuation analysis (DFA) method, respectively, and obtain similar results for all the stocks considered. The result indicates that the gap series of each stock processes strong long memory with the scaling exponent significantly larger than 0.5, and the probability distribution of gaps has no impact on its memory effect. Finally, we analyze the multifractal property of gap series applying the multifractal detrended fluctuation analysis (MF-DFA) method. It is evident that the gap series have multifractal nature for both buy and sell LOBs and the probability distribution of gaps has little effect on the multifractality.

Our work conducts a systemic investigation of the statistical properties of price gaps on the limit order books. These empirical findings not only deepen our understanding of the dynamics of liquidity, but also provide stylized facts for the calibration of agent-based computational models (Li et al., 2014). For instance, the seminal order-driven stock market model of Mike and Farmer (2008) based on the statistical properties of order placement and order cancellation is able to reproduce the two main stylized facts, that is, the power-law tail distribution of returns and the absence of long-range correlations in return time series. However, it fails to reproduce the volatility clustering phenomenon. Gu and Zhou (2009) scrutinize the microscopic empirical rules of the model and improve the model by taking into account the long-term correlations in relative prices of submitted orders. They can thus reproduce the important stylized fact of volatility clustering. Along this line, one needs to check if the artificial stock market based on computational models has the unveiled stylized facts in the price gaps. If there are discrepancies between the artificial market and real markets, one can conclude that some ingredients are missing in the construction of the model and will need to modify or improve the model.

Acknowledgement

This work was partly supported by National Natural Science Foundation of China (71101052, 71131007 and 71072007), Shanghai Rising Star (Follow-up) Program (11QH1400800), Program for Changjiang Scholars and Innovative Research Team in University (IRT1028), and the Fundamental Research Funds for the Central Universities.

References

- Alessio et al. (2002) Alessio, E., Carbone, A., Castelli, G., Frappietro, V., 2002. Second-order moving average and scaling of stochastic time series. Eur. Phys. J. B 27, 197–200.

- Almgren (2003) Almgren, R. F., 2003. Optimal execution with nonlinear impact functions and trading-enhanced risk. Appl. Math. Finance 10, 1–18.

- Arianos and Carbone (2007) Arianos, S., Carbone, A., 2007. Detrending moving average algorithm: A closed-form approximation of the scaling law. Physica A 382, 9–15.

- Barunik and Kristoufek (2010) Barunik, J., Kristoufek, L., 2010. On Hurst exponent estimation under heavy-tailed distributions. Physica A 389 (18), 3844–3855.

- Bashan et al. (2008) Bashan, A., Bartsch, R., Kantelhardt, J. W., Havlin, S., 2008. Comparison of detrending methods for fluctuation analysis. Physica A 387, 5080–5090.

- Bertram (2004) Bertram, W. K., 2004. An empirical investigation of Australian Stock Exchange data. Physica A 341, 533–546.

- Chakraborti et al. (2011) Chakraborti, A., Toke, I. M., Patriarca, M., Abergel, F., 2011. Econophysics review: I. Empirical facts. Quant. Finance 11 (7), 991–1012.

- Clauset et al. (2009) Clauset, A., Shalizi, C. R., Newman, M. E. J., 2009. Power-law distributions in empirical data. SIAM Rev. 51, 661–703.

- Coronel-Brizio and Hernández-Montoya (2005) Coronel-Brizio, H. F., Hernández-Montoya, A. R., 2005. On fitting the Pareto-Levy distribution to stock market index data - Selecting a suitable cutoff value. Physica A 354, 437–449.

- Di Matteo et al. (2005) Di Matteo, T., Aste, T., Dacorogna, M. M., 2005. Long term memories of developed and emerging markets: Using the scaling analysis to characterize their stage of development. J. Bank. Finance 29, 827–851.

- Epps (1977) Epps, T. W., 1977. Security price changes and transaction volumes - Some additional evidence. J. Finance Quant. Anal. 12, 141–146.

- Farmer (2002) Farmer, J. D., 2002. Market force, ecology and evolution. Industrial and Corporate Change 11, 895–953.

- Farmer et al. (2004) Farmer, J. D., Gillemot, L., Lillo, F., Mike, S., Sen, A., 2004. What really causes large price changes? Quant. Finance 4, 383–397.

- Farmer and Lillo (2004) Farmer, J. D., Lillo, F., 2004. On the origin of power-law tails in price fluctuations. Quant. Finance 4, C7–C11.

- Gabaix et al. (2003a) Gabaix, X., Gopikrishnan, P., Plerou, V., Stanley, H. E., 2003a. A theory of power-law distributions in financial market fluctuations. Nature 423, 267–270.

- Gabaix et al. (2003b) Gabaix, X., Gopikrishnan, P., Plerou, V., Stanley, H. E., 2003b. Understanding the cubic and half-cubic laws of financial fluctuations. Physica A 324, 1–5.

- Gabaix et al. (2006) Gabaix, X., Gopikrishnan, P., Plerou, V., Stanley, H. E., 2006. Institutional investors and stock market volatility. Quart. J. Econ. 121, 461–504.

- Gabaix et al. (2007) Gabaix, X., Gopikrishnan, P., Plerou, V., Stanley, H. E., 2007. A theory of limited liquidity and large investors causing spikes in stock market volatility and trading volume. J. Eur. Econ. Assoc. 5, 564–573.

- Gallant et al. (1992) Gallant, A. R., Rossi, P. E., Tauchen, G., 1992. Stock prices and volume. Rev. Financ. Stud. 5, 199–242.

- Gopikrishnan et al. (1999) Gopikrishnan, P., Plerou, V., Amaral, L. A. N., Meyer, M., Stanley, H. E., 1999. Scaling of the distribution of fluctuations of financial market indices. Phys. Rev. E 60, 5305–5316.

- Gould et al. (2013) Gould, M. D., Porter, M. A., Williams, S., McDonald, M., Fenn, D. J., Howison, S. D., 2013. Limit order books. Quant. Finance 13 (11), 1709–1742.

- Gu et al. (2008a) Gu, G.-F., Chen, W., Zhou, W.-X., 2008a. Empirical distributions of Chinese stock returns at different microscopic timescales. Physica A 387, 495–502.

- Gu et al. (2008b) Gu, G.-F., Chen, W., Zhou, W.-X., 2008b. Empirical regularities of order placement in the Chinese stock market. Physica A 387, 3173–3182.

- Gu et al. (2008c) Gu, G.-F., Chen, W., Zhou, W.-X., 2008c. Empirical shape function of limit-order books in the Chinese stock market. Physica A 387, 5182–5188.

- Gu and Zhou (2009) Gu, G.-F., Zhou, W.-X., 2009. Emergence of long memory in stock volatilities from a modified Mike-Farmer model. EPL (Europhys. Lett.) 86 (5), 48002.

- Halsey et al. (1986) Halsey, T. C., Jensen, M. H., Kadanoff, L. P., Procaccia, I., Shraiman, B. I., 1986. Fractal measures and their singularities: The characterization of strange sets. Phys. Rev. A 33, 1141–1151.

- Harris (1987) Harris, L., 1987. Transaction data tests of the mixture of distributions hypothesis. J. Finance Quant. Anal. 22, 127–141.

- Holschneider (1988) Holschneider, M., 1988. On the wavelet transformation of fractal objects. J. Stat. Phys. 50, 963–993.

- Hu et al. (2001) Hu, K., Ivanov, P. C., Chen, Z., Carpena, P., Stanley, H. E., 2001. Effect of trends on detrended fluctuation analysis. Phys. Rev. E 64, 011114.

- Hurst (1951) Hurst, H. E., 1951. Long-term storage capacity of reservoirs. Trans. Amer. Soc. Civil Eng. 116, 770–808.

- Jain and Joh (1988) Jain, P. C., Joh, G.-H., 1988. The dependence between hourly prices and trading volume. J. Finance Quant. Anal. 23 (3), 269–283.

- Jiang et al. (2014) Jiang, Z.-Q., Xie, W.-J., Zhou, W.-X., 2014. Testing the weak-form efficiency of the WTI crude oil futures market. Physica A 405, 235–244.

- Joulin et al. (2008) Joulin, A., Lefevre, A., Grunberg, D., Bouchaud, J.-P., 2008. Stock price jumps: News and volume play a minor role. Wilmott Magazine Sep/Oct, 1–7.

- Kantelhardt et al. (2002) Kantelhardt, J. W., Zschiegner, S. A., Koscielny-Bunde, E., Havlin, S., Bunde, A., Stanley, H. E., 2002. Multifractal detrended fluctuation analysis of nonstationary time series. Physica A 316, 87–114.

- Karpoff (1987) Karpoff, J. M., 1987. The relation between price changes and trading volume: A survey. J. Finance Quant. Anal. 22, 109–126.

- Lallouache and Abergel (2013) Lallouache, M., Abergel, F., 2013. Empirical properties of the foreign exchange interdealer market, http://arxiv.org/abs/1307.5440.

- Li et al. (2014) Li, Y.-L., Zhang, W., Zhang, Y.-J., Zhang, X.-T., Xiong, X., 2014. Calibration of the agent-based continuous double auction stock market by scaling analysis. Inf. Sci. 256, 46–56.

- Liang et al. (2013) Liang, Y., Yang, G., Huang, J.-P., 2013. Progress in physical properties of Chinese stock markets. Front. Phys. 8, 438–450.

- Lillo et al. (2003) Lillo, F., Farmer, J. D., Mantegna, R., 2003. Master curve for price impact function. Nature 421, 129–130.

- Lim and Coggins (2005) Lim, M., Coggins, R., 2005. The immediate price impact of trades on the Australian Stock Exchange. Quant. Finance 5 (4), 365–377.

- Loeb (1983) Loeb, T. F., 1983. Trading costs: The critical link between investment information and results. Financial Analysts J. 39, 39–44.

- Mandelbrot (1963) Mandelbrot, B. B., 1963. The variation of certain speculative prices. J. Business 36, 394–419.

- Mantegna and Stanley (1995) Mantegna, R. N., Stanley, H. E., 1995. Scaling behaviour in the dynamics of an economic index. Nature 376, 46–49.

- Mike and Farmer (2008) Mike, S., Farmer, J. D., 2008. An empirical behavioral model of liquidity and volatility. J. Econ. Dyn. Control 32 (1), 200–234.

- Mu and Zhou (2010) Mu, G.-H., Zhou, W.-X., 2010. Tests of nonuniversality of the stock return distributions in an emerging market. Phys. Rev. E 82, 066103.

- Muzy et al. (1991) Muzy, J. F., Bacry, E., Arnéodo, A., 1991. Wavelets and multifractal formalism for singular signals: Application to turbulence data. Phys. Rev. Lett. 67, 3515–3518.

- Næs and Skjeltorp (2006) Næs, R., Skjeltorp, J. A., 2006. Order book characteristics and the volume-volatility relation: Empirical evidence from a limit order market. J. Financial Markets 9, 408–432.

- Pan and Sinha (2008) Pan, R. K., Sinha, S., 2008. Inverse cubic law of index fluctuation distribution in Indian markets. Physica A 387, 2055–2065.

- Peng et al. (1992) Peng, C.-K., Buldyrev, S. V., Goldberger, A. L., Havlin, S., Sciortino, F., Simons, M., Stanley, H. E., 1992. Long-range correlations in nucleotide sequences. Nature 356, 168–170.

- Peng et al. (1994) Peng, C.-K., Buldyrev, S. V., Havlin, S., Simons, M., Stanley, H. E., Goldberger, A. L., 1994. Mosaic organization of DNA nucleotides. Phys. Rev. E 49 (2), 1685–1689.

- Perold and Salomon (1991) Perold, A. F., Salomon, R. S. J., 1991. The right amount of assets under management. Financial Analysts J. 47, 31–39.

- Plerou et al. (1999) Plerou, V., Gopikrishnan, P., Amaral, L. A. N., Meyer, M., Stanley, H. E., 1999. Scaling of the distribution of price fluctuations of individual companies. Phys. Rev. E 60, 6519–6529.

- Plerou et al. (2004) Plerou, V., Gopikrishnan, P., Gabaix, X., Stanley, H. E., 2004. On the origin of power-law fluctuations in stock prices. Quant. Finance 4, C11–C15.

- Richardson et al. (1986) Richardson, G., Sefcik, S. E., Thompson, R., 1986. A test of dividend irrelevance using volume reactions to a change in dividend policy. J. Financial Econ. 17, 313–333.

- Rogalski (1978) Rogalski, R. J., 1978. The dependence of prices and volume. Rev. Econ. Stat. 60, 268–274.

- Saatcioglu and Starks (1998) Saatcioglu, K., Starks, L. T., 1998. The stock price-volume relationship in emerging stock markets: The case of Latin America. Int. J. Forecast. 14, 215–225.

- Shao et al. (2012) Shao, Y.-H., Gu, G.-F., Jiang, Z.-Q., Zhou, W.-X., Sornette, D., 2012. Comparing the performance of FA, DFA and DMA using different synthetic long-range correlated time series. Sci. Rep. 2, 835.

- Tabak et al. (2009) Tabak, B. M., Takami, M. Y., Cajueiro, D. O., Petitiniga, A., 2009. Quantifying price fluctuations in the Brazilian stock market. Physica A 388, 59–62.

- Taqqu et al. (1995) Taqqu, M. S., Teverovsky, V., Willinger, W., 1995. Estimators for long-range dependence: An empirical study. Fractals 3, 785–798.

- Vandewalle and Ausloos (1998) Vandewalle, N., Ausloos, M., 1998. Crossing of two mobile averages: A method for measuring the roughness exponent. Phys. Rev. E 58, 6832–6834.

- Weber and Rosenow (2006) Weber, P., Rosenow, B., 2006. Large stock price changes: Volume or liquidity? Quant. Finance 6, 7–14.

- Wood et al. (1985) Wood, R. A., McInish, T. H., Ord, J. K., 1985. An investigation of transactions data for NYSE stocks. J. Finance 40, 723–739.

- Xu et al. (2005) Xu, L. M., Ivanov, P. C., Hu, K., Chen, Z., Carbone, A., Stanley, H. E., 2005. Quantifying signals with power-law correlations: A comparative study of detrended fluctuation analysis and detrended moving average techniques. Phys. Rev. E 71, 051101.

- Yang et al. (2013) Yang, C.-X., Wang, R., Hu, S., 2013. Modeling and analysis of an agent-based model for Chinese stock market. Phys. Lett. A 377, 2041–2046.

- Ying (1966) Ying, C. C., 1966. Stock market prices and volumes of sales. Econometrica 34, 676–685.

- Zhang et al. (2007) Zhang, J.-W., Zhang, Y., Kleinert, H., 2007. Power tails of index distributions in Chinese stock market. Physica A 377, 166–172.

- Zhang (1999) Zhang, Y.-C., 1999. Toward a theory of marginally efficient markets. Physica A 269, 30–44.

- Zhou (2012a) Zhou, W.-X., 2012a. Determinants of immediate price impacts at the trade level in an emerging order-driven market. New J. Phys. 14 (9), 023055.

- Zhou (2012b) Zhou, W.-X., 2012b. Finite-size effect and the components of multifractality in financial volatility. Chaos, Solitons & Fractals 45, 147–155.

- Zhou (2012c) Zhou, W.-X., 2012c. Universal price impact functions of individual trades in an order-driven market. Quant. Finance 12 (8), 1253–1263.