∎

11institutetext: ⋆ Corresponding author. Email: \hrefmailto:Johannes.Mueller@fau.deJohannes.Mueller@fau.de

1 Department of Mathematics, FAU Erlangen-Nürnberg, Cauerstr. 11, 91058 Erlangen, Germany

2 ISyE, Georgia Institute of Technology, Groseclose 0205, 765 Ferst Dr, Atlanta, GA 30332, USA

3 Eurex Frankfurt AG, 60485 Frankfurt, Germany

♮

This is the Accepted Manuscript (i.e., the final draft post-refereeing) of an

article published in MMOR.

The final publication is available at Springer via

\hypersetuphidelinks,\hrefhttp://dx.doi.org/10.1007/s00186-016-0555-zhttp://dx.doi.org/10.1007/s00186-016-0555-z\hypersetupcolorlinks=true,.

Cite as: Müller JC, Pokutta S, Martin A, et al. (2017)

Pricing and clearing combinatorial markets with singleton and swap orders.

Math Meth Oper Res, 85, 155–177. \hypersetuphidelinks,\hrefhttp://dx.doi.org/10.1007/s00186-016-0555-zdoi:10.1007/s00186-016-0555-z\hypersetupcolorlinks=true,.

\hypersetuphidelinks,

Pricing and clearing combinatorial markets with singleton and swap orders††thanks: Several of the presented results are taken from the Ph.D. thesis of J. C. Müller (2014). Research was supported by Deutsche Börse AG.

Abstract

In this article we consider combinatorial markets with valuations only for singletons and pairs of buy/sell-orders for swapping two items in equal quantity. We provide an algorithm that permits polynomial time market-clearing and -pricing. The results are presented in the context of our main application: the futures opening auction problem. Futures contracts are an important tool to mitigate market risk and counterparty credit risk. In futures markets these contracts can be traded with varying expiration dates and underlyings. A common hedging strategy is to roll positions forward into the next expiration date, however this strategy comes with significant operational risk. To address this risk, exchanges started to offer so-called futures contract combinations, which allow the traders for swapping two futures contracts with different expiration dates or for swapping two futures contracts with different underlyings. In theory, the price is in both cases the difference of the two involved futures contracts. However, in particular in the opening auctions price inefficiencies often occur due to suboptimal clearing, leading to potential arbitrage opportunities. We present a minimum cost flow formulation of the futures opening auction problem that guarantees consistent prices. The core ideas are to model orders as arcs in a network, to enforce the equilibrium conditions with the help of two hierarchical objectives, and to combine these objectives into a single weighted objective while preserving the price information of dual optimal solutions. The resulting optimization problem can be solved in polynomial time and computational tests establish an empirical performance suitable for production environments.

Keywords:

Equilibrium problems Hierarchical objectives Linear programming Network flows Combinatorial auctions Futures exchangesMSC:

90C33 90C29 90C05 90C35 91B26Introduction

Futures contracts are some of the most liquid derivatives and, among other purposes, are an integral component of many hedging and risk mitigation strategies. For example, airlines regularly use futures to hedge against volatile crude prices and lock-in the current price level. These hedging strategies usually involve a rollover of the contracts from one expiration date (also called maturity) into the next when approaching the expiration date of the first. However, rolling the contracts forwards is not without risk, the so-called rollover risk. This risk consists of basically two components. The first component is the time spread risk (also called calendar spread risk), which is affected by whether the price difference between the maturing contract and the replacement contract with the extended expiration date matches the theoretical fair value. The other component, the slippage, is of an operational risk type. It is the risk of loss arising from selling off the old contracts and buying the new contracts being not perfectly simultaneous allowing for adversarial intermediate price moves or in an opening auction only one of the two orders being executed; we refer the interested reader e.g., to (Hull, 2006; Cooper, 2015) for a discussion. While the time spread risk is market inherent and hence exchange unspecific, slippage can be mitigated by the exchange by offering futures swap products, so-called combinations and various futures exchanges, such as e.g., \hrefhttp://www.eurexchange.comEUREX (European Exchange AG) offer such products. However, offering such products improves market transparency and liquidity only if those products are consistently priced and while this is ensured by arbitrageurs intraday, this is not necessarily the case for the opening auction when the market opens. In fact, it has been observed that in the opening auctions in some cases prices across products are inconsistent, creating potential arbitrage opportunities.

We present an efficient optimization model that guarantees consistent prices at the end of the opening auction while maximizing economic surplus. We further demonstrate that the model can be solved extremely fast in practice for large amounts of orders and contract types making it a prime candidate for production environments. The presented model is motivated by the product offering of EUREX, however it applies readily to various other futures exchanges.

Related work

The futures opening auction is a combinatorial auction and there exists a large body of work studying this type of auctions; we refer the interested reader to the very nice surveys of de Vries and Vohra (2003) and Blumrosen and Nisan (2007) for an introduction. It is well-known that various combinatorial auctions can be solved in polynomial time provided, e.g., if the constraint matrix is totally unimodular and the right-hand side of the clearing program is integral. As we will see later, our setup admits such an efficient formulation via a network flow formulation.

Closely related to our work is the work of Winter et al (2011), which is based on the master’s thesis of M. Rudel. The authors developed a pure linear integer program to solve the problem for at most three futures contract types. The approach heavily relies on preprocessing techniques to reduce the problem size for the three contracts case and while the underlying formulation is based on a network flow problem with orders modeled as arcs this structure is not exploited. In fact, the employed model is heavily driven by price conditions that involve binary variables. These binary variables render the underlying structure inaccessible and the properties of equilibrium conditions cannot be exploited. Our approach is highly superior as we naturally observe market equilibria conditions from the dual linear program as well as ensure volume maximization by appropriate objective function regularization. We provide a comparison of both approaches in Section 5.2.

There is also a significant amount of literature on so-called linear prices, which are also referred to as uniform prices. In the absence of integer variables the dual variables of the clearing conditions provide us with linear prices if we maximize the economic surplus. In previous work (Martin, Müller, and Pokutta, 2014) we used this property to ensure the existence of linear prices in European day-ahead electricity auctions. In this work, however, we exploit this property in order to get a computationally advantageous model formulation.

Contribution

We provide a natural formulation for the real-world problem of clearing, pricing, and maximizing the execution volume of a certain combinatorial exchange. We show that one can compute a solution to that problem by solving a single min cost flow problem. More precisely, we decompose the problem into a primal min cost flow problem with a weighted objective and a dual pricing problem that is closely related to the primal one. An optimal extreme point of the weighted problem is a welfare maximizing and volume maximizing clearing solution. Moreover we show that we can scale and round a dual optimal extreme point of the weighted problem to obtain the corresponding competitive equilibrium prices. In other words, the weighted problem is chosen in such a way that a primal optimal extreme point maximizes the executed volume while the desired equilibrium conditions are satisfied automatically: completely satisfied participants, positive bid-ask spreads, uncrossed order books, and the absence of combinatorial matching cycles.

This new formulation has three major advantages. First, the model is solvable in polynomial time with a standard solver and the numerical results indicate that the computing times are sufficiently fast for the use in production environments. In particular, the algorithm is significantly faster (two orders of magnitude) than the approach presented in Winter et al (2011). Second, the model is very flexible: in contrast to previous models it is not restricted to a limited number of different underlyings (e.g., one) or expiration dates (e.g., three). It is capable to handle all kinds of singleton and swap orders simultaneously, regardless of their underlyings or expirations dates. In particular, it can handle so-called time spread combinations and inter-product spread combinations in one single auction (see Def. 3). Third, the obtained prices are of high quality, that is, the prices for contracts are consistent with the prices for combinations.

Another important advantage of our integrated model is that the total economic surplus of all participants is maximized, i.e., it is not possible to find a solution with a higher economic surplus. In particular, our algorithm is superior to the current algorithm at EUREX which does not guarantee maximum economic surplus. In fact, the currently employed algorithm first determines prices for each contract separately, without taking combination orders into account. At that time the prices can therefore be inconsistent with respect to the crossed order books of combination orders. Nevertheless, the combination orders get triggered according to the prices of the underlying contracts and thus the market is not necessarily in a maximized surplus situation.

Electronic futures exchanges

Futures contracts are standardized financial products that are traded at futures exchanges. These exchanges provide electronic interfaces such that any trader around the world can advise his or her broker to route a buy or sell order directly to a futures exchange. The exchange collects those orders and stores them in order books [see Gould et al (2013) for a survey on limit order books]. There is one order book for each financial product. During the trading-hours (intraday), the exchange will execute all incoming orders that can be matched and immediately determine and publish the market clearing price at which these orders where executed. However, at the beginning of the trading day, the order books are not empty. On the one hand, there are the non-executed orders of the previous day, on the other hand, some participants already submit their orders before the trading day has started. For that reason, the exchange performs a so-called opening auction immediately before the trading day begins. In practice, the exchange determines a separate market clearing price for each financial product and only matches orders within an order book; dependencies between books are ignored. Our new approach performs a single computation that takes all order books into account and correctly models the relationships between all financial products.

The available financial products are futures contracts as well as futures contract combinations. We briefly recall the formal definition of these financial products. More detailed information on futures can be found in Chapter 2 in Hull (2006).

Definition 1

A futures contract is an agreement between two parties to

-

1.

Buy or sell an asset (the underlying)

-

2.

At an agreed-upon time in the future (the expiration date)

-

3.

For an agreed-upon price (the current market clearing price of the futures contract, also called futures price).

Each (underlying, expiration date)-tuple is a financial product of the futures contract type, in particular it is an exchange tradable good with its own order book. In the following, for brevity we will also refer to futures contracts simply as contracts.

Example 1

On January 4 a trader in Frankfurt wants to buy 100 troy ounces gold with delivery in June of the same year. A single gold futures contract at EUREX has the value of 100 troy ounces. The trading day starts at 8:00 in the morning. At 7:30, he submits a buy order via his online broker to the futures exchange. The order contains the information that he wants to buy one gold futures contract, with delivery in June and that he is willing to pay at most . On the same day, another trader in Darmstadt wants to sell a gold futures contract with delivery in June of the same year. At 7:45 she submits her sell order via her online broker to the exchange. The lowest price she is willing to accept amounts to . At the opening auction at 8:00 the order book only contains these two orders. The exchange executes both orders at the market clearing price of and publishes that price.

The previous example illustrates that during an auction two contracts are equal if the underlying and the expiration date coincide. As long as the auction is not terminated the contracts are not yet binding and the final price is not yet agreed-upon. In the moment when the auction terminates the contracts of the executed orders become binding and the agreed-upon price for the underlying at the expiration date is the market clearing price that was determined by the exchange.

Beside plain futures contracts, the participants can also trade contract combinations:

Definition 2

A futures contract combination (short: combination) allows for swapping one futures contract for another futures contract.

There are two different kinds of futures contract combinations:

Definition 3

A time spread combination allows for swapping two futures contracts with the same underlying but with different expiration dates. An inter-product spread combination allows for swapping two futures contracts with different underlyings but not necessarily different expiration dates.

Each 2-element set of (underlying, expiration date)-tuples is a financial product of the contract combination type, in particular it is an exchange tradable good with its own order book. It is a question of definition, which contract will be bought and which one will be sold if someone buys (or sells) a combination.

Our opening auction model follows the one that is currently employed by EUREX and many other exchanges follow a similar setup, so that our setup can be readily applied. In the opening auction there are two different order types: limit orders and market orders. If a participant submits a \hrefhttp://www.sec.gov/answers/limit.htmlimit order, then the exchange receives the following information: the ID of the financial product, whether it should be bought or sold, the maximum quantity to be bought or sold, and the limit price. The limit price specifies the highest price per unit a buyer is willing to pay or the lowest price per unit a seller is willing to accept. If a participant submits a \hrefhttp://www.sec.gov/answers/mktord.htmmarket order, the exchange only receives the ID of the financial product, whether it should be bought or sold, and the maximum quantity. Market orders have a higher priority than limit orders and the trader is accepting all prices. In an opening auction a market order can be treated as a limit order with the highest feasible limit price (defined by the exchange) if it is a buy order, or the lowest feasible limit price if it is a sell order; therefore, we do not need to model them explicitly and in the following all orders are of limit type.

A partial execution of limit orders or market orders is only feasible if the limit price coincides with the market clearing price. Fractional partial executions are infeasible, as contracts are indivisible; therefore, a partial execution must trade an integral number of contracts. For the sake of completeness, we want to mention that the fill-or-kill order type, which must either be executed entirely or not executed at all, is not available in the opening auction.

Modeling orders as directed arcs

In the opening auction, the participants express their preferences by submitting limit orders to the exchange. In order to model these limit orders we define several sets, input parameters, and variables.

Let be the set of the different contracts the participants can bid for. Hereinafter is also referred to as the contract set. Remember that a contract is characterized by its underlying asset and its expiration date. Two contracts are equal if they have the same underlying asset and the same expiration date. Let the contract set be a totally ordered set sorted in ascending order, where the first sort criterion is the underlying asset ID and the second criterion is the expiration date.

The main idea of the model is to treat the contracts as nodes in a graph and the orders as directed arcs connecting the nodes. To be able to model all orders as arcs, we introduce a super node that represents the source or sink of orders that only involve a single futures contract. The super node can be interpreted as cash. Let be the extended node set (contract set) so that becomes the new maximum. Then all orders can be modeled as arcs in .

Definition 4

A directed arc models an order for demanding and offering . The case is not allowed. The arc represents a buy order if . Otherwise, it represents a sell order. Per definition for all .

Examples for contracts :

| Arc | Buy/Sell | Product | Meaning | ||

| buy | |||||

| sell | |||||

| buy | demand contract and offer contract | ||||

| sell |

Note that the arcs and refer to the same financial product: the futures contract combination .

Remark 1

The super node is only used to visualize orders in a graph. We will omit it in the LP representation of the network flow model, as the flow conservation equation of the super node is a redundant equation and is a source of degeneracy in the dual LP.

The set of limit orders (and market orders) is denoted by and hereinafter also referred to as the order book. To model an order we use the parameters , , and with . The first parameter models the demanded/offered quantity. The second parameter is the -th entry of a price vector that represents the limit price of order . And is the -th entry of the characteristic vector of the arc associated with order . If is the arc associated with and is the smallest index, then the price vector vanishes at the entries and the entry is the limit price of order . The execution state of order is represented by a non-negative integer variable .

In other words, let be the arc associated with order , then the input parameters are filled as follows: for all

And the solution variables are interpreted as follows:

Note that the market clearing price for combinations is given by the difference of the prices of the two underlying contracts: The price of combination with is given by . Therefore, it is not necessary to model them explicitly. The market clearing prices determine the amount of money a participant has to pay or receive for the execution of his or her order. For an order the net amount of money to be paid or received is given by

| (1) |

If this amount is positive one has to pay money, otherwise one will receive money. Similarly, we can determine the net amount a participant is willing to pay for the execution of his or her order:

| (2) |

If this amount is negative the participant wants to receive money for the execution of his or her order. The difference of the two terms is the surplus:

| (3) |

The participant incurs a loss if this term is negative.

Example 2

Assume that there are three different contracts . An order for buying contract with limit price is represented by the arc and modeled as follows:

And an order for selling contract with limit price is represented by the arc and modeled by

Whereas an order for buying contract and selling contract with a minimal spread (the limit price) of at least currency units is represented by the arc and modeled by directly involving the minimal spread:

Alternatively we can also use reference prices for the two underlying contracts:

The negative limit price indicates that the buyer wants to receive at least 13 currency units. In practice, we use the first encoding since it only involves one price: the limit price of the combination order.

Observe that if we model a single buy or sell order, then the quantity vector and the price vector vanish at all but one entry. If we model a combination order, being a linear combination of a single buy and a single sell order, then the quantity vector vanishes at all but two entries. As order is a linear combination of order and , we can write and .

Derivation of an hierarchical min cost flow model to be solved by the exchange

In the opening auction, the exchange determines the orders that will be executed and the prices at which those orders are executed. The employed algorithm that performs this task implements the market rules of the exchange. These rules include quantity constraints as well as price constraints. We propose an algorithm which solves an optimization problem that couples interdependent market products, guarantees consistent prices, and covers all given market rules. The objective is to maximize the executed volume subject to the quantity and price constraints:

| (MIP) | ||||||

| clearing constraint | (4) | |||||

| price condition | (5) | |||||

| price condition | (6) | |||||

| quantity restriction | (7) | |||||

| integrality constraint | (8) | |||||

| price variable | (9) | |||||

The price conditions (5) and (6) are so-called indicator constraints, which can be modeled with linear constraints by using big-M formulations. The first price constraint ensures that no participant incurs a loss if his or her order is executed. If, for example, the order is an executed buy order, then the products market price must be smaller than or equal to the limit price of the order. The second price constraint ensures that if a buy order (sell order) is not executed entirely, then the products market price must be greater than (smaller than) or equal to the limit price. Later we will see that both price conditions together actually ensure that a solution is feasible if and only if it maximizes the economic surplus of all participants. This model property will allow us to enforce the price conditions implicitly such that we do not have to model them explicitly.

An example that illustrates the outcome of the above presented model is provided in Sect. 6.

Consider the following relaxation of (MIP). The integrality of the execution variables is relaxed, as well as the price conditions are relaxed. We also replace the objective function so that we maximize the economic surplus of all participants instead of the execution volume. The model is a so-called surplus maximization problem.

| (LP1) | |||||||

| clearing constraint | |||||||

| quantity restriction | |||||||

| quantity restriction | |||||||

The terms in square brackets denote the dual variables of the corresponding primal constraints. In the following, we see that if (LP1) is feasible, there exists an integral primal optimal solution and a dual optimal solution to (LP1). The vector is called a uniform price vector and the tuple is called a competitive equilibrium (cf. Arrow and Debreu (1954); Mas-Colell et al (1995) or Müller (2014, Thm. 2.17)). Furthermore, we will see that an integral primal-dual feasible solution pair to (LP1) is optimal if and only if it is feasible for (MIP).

Recall that a matrix of integers is totally unimodular if and only if for all vectors , whose components are integers or , every minimal face of the polyhedron contains an integral point (Hoffman and Kruskal, 1956). By construction the matrix is a node-arc incidence matrix of a directed graph and it is known that such matrices are totally unimodular. As the polyhedron of (LP1) is bounded, every minimal face is an extreme point of the polyhedron, and thus all extreme points are integral. In particular all extreme points of (LP1) that maximize the objective are integral.

Now we analyze the properties of such an optimal extreme point . For that purpose we apply the Karush-Kuhn-Tucker optimality conditions [see e.g., Boyd and Vandenberghe (2004)]. Let be integral and primal optimal to (LP1). Then there exist dual variables , and that satisfy equations (10) to (13).

| (10) | |||||

| (11) | |||||

| (12) | |||||

| (13) |

Proposition 1

These equations coincide with price conditions (5) and (6). This means that given an integral optimal solution to (LP1), there exist prices such that the price conditions hold and is feasible for (MIP). Vice versa, a feasible solution for (MIP) is optimal for (LP1), as it satisfies the price condition and thereby maximizes the economic surplus of all participants.

Now we can characterize a feasible solution to (MIP) in the following way: Any integral point of (LP1) that maximizes the economic surplus is feasible to (MIP). As the polyhedron of (LP1) is integral, also the optimal face is integral. Hence, we can maximize the execution volume subject to the constraints of (MIP) by using a linear program where the economic surplus is fixed to its optimal value obtained from (LP1):

| (LP2) | |||||

| clearing constraint | |||||

| quantity restriction | |||||

| quantity restriction | |||||

| optimality of economic surplus | |||||

Now we can construct an optimal solution to (MIP) by finding at first an optimal solution to the linear program (LP1). Then we solve (LP2) using as input to fix the economic surplus to the optimal value. An optimal extreme point of (LP2) is feasible and optimal to (MIP).

Combining both hierarchy levels in one model

In this section, we show that it is not necessary to solve the two LPs successively. Both LPs can be incorporated into just one LP. At first we describe an intuitive scaling technique based on an upper bound of the executed volume. Then we improve the scaling technique by using a smaller scaling factor which exploits the network flow structure of the model.

We know that each component of and is integral. If a solution is integral, then the objective of (LP1) is also integral. The objective of (LP2) (volume maximization) is strictly bounded from above by . We define a new objective function that is given by times the objective of (LP1) (surplus maximization) plus the objective function of (LP2):

| (16) |

Now we replace the objective in (LP1) by objective (16). An optimal solution to the resulting LP will be optimal to both (LP1) and (LP2). Thus, it is optimal to (MIP).

In practice the scaling factor might be too large, causing numerical difficulties. We will now argue that we can choose a much smaller factor that is independent of the number of orders. This becomes evident from the following proposition.

Proposition 2

(Price rounding; Müller, 2014, Proposition 1.12 Let , , , totally unimodular with , and with . If and are primal and dual optimal extreme points of

| (17) | ||||

then and with for are primal and dual optimal extreme points of

| (18) | ||||

Proof

Let be an optimal basis for the optimal solution to (17). Corollary 1.9 (resp. Theorem 1.8) in Müller (2014) yields that the basis is also optimal for (18), because .

Recall that is totally unimodular, as is totally unimodular. In particular, all of its components are or . The following equations reflect the relation between the dual variables of (18) and (17) and the basis.

We will now determine the maximal absolute distance between and .

| (19) | |||

| (20) | |||

| (21) |

Equation (21) and yield the desired result.

Note that in Proposition 2 we omit the dual variables of the lower and upper bounds, as we are only interested in the -part of a dual solution. For this reason, we call dual optimal, if it is the -part of a dual optimal solution including all dual variables, in particular those of the bounds.

Without loss of generality, let the rank of the constraint matrix of (LP1) be equal to the number of contracts . According to Proposition 2 we can use the scaling factor in objective (16) instead of . In futures opening auctions, is typically much smaller than , because the number of contracts (e.g., ) is typically much smaller than the number of orders (e.g., ). For this reason, the scaling factor causes less numerical problems than the scaling factor .

Market clearing prices and bid and ask prices

We will now explain how market clearing prices and the bid-ask prices can be recovered. For the former we present two implicit methods, both arising from the special structure of optimal solutions.

Let be an optimal solution to (LP3). We want to compute market clearing prices for all contracts such that all participants are completely satisfied, that is, if their individual surplus maximization problems

| (22) |

get maximized. These individual problems are also called oracles (de Vries and Vohra, 2003). Each oracle determines the amount a participant wants to trade at the given market clearing prices. The most straightforward explicit method to compute market clearing prices is to solve the -parameterized linear feasibility problem

| (LP4) | |||||

The model is motivated by the optimality conditions of (22), however it comes at the cost of solving yet another linear program, which is undesirable. Instead, using Proposition 2, we can directly read-off the prices as follows: If is the -part of a dual optimal extreme point of (LP3) and , then the market clearing prices are given by

| (23) |

Such a dual optimal extreme point is a by-product of the simplex method if we use it for solving (LP3).

Alternatively, we can use the following theorem, which shows how the optimal base of (LP3) can be used to obtain market clearing prices. The theorem forms the basis for the proof of the previous proposition and provides a stronger result as its scaling factor is smaller.

Theorem 4.1

(Weighted objective theorem; Müller, 2014, Theorem 1.10) Let , , unimodular with , , and , where . If is an optimal basis to (17) and is an optimal solution to (17), then with is an optimal solution to

| (24) |

The lower bound of for is as small as possible: if , the theorem becomes false in general. As in Proposition 2 above, we omit the dual variables of lower and upper bounds.

If is an optimal basis to (LP3) and , then the market clearing prices , which satisfy (22), are given by

| (25) |

where is the objective vector of (LP1) and is the constraint matrix of the clearing condition of (LP1). If we use the simplex method for solving (LP3), then the method computes the matrix in its final iteration and hence the required additional computation for the prices is simply a vector-matrix multiplication.

Finally, the bid and ask prices for each product are given by the limit prices of the best non-executed buy and sell orders of the respective product. The search for the best non-executed buy and sell orders can be done in linear time by iterating only once through all orders.

Numerical results

We will now present numerical results for various versions of our algorithms and compare them to previously employed algorithms.

Algorithms and variants

In this section, we provide five different algorithms that are based on primal optimal and dual optimal extreme points of linear programs. The first two algorithms (Algorithms 1 and 2) solve the linear program (LP3) with the weighted objective and then apply Proposition 2 to compute market clearing prices via scaling and rounding the dual variables. The only difference is the scaling factor for combining the objective functions, in the former and the naive one in latter case; we will see that the size of the scaling factor influences the computing times. Note that we could also compute the prices using a primal dual optimal basis as described in (25) [see also Alg. 1.3.1 in Müller (2014)]. This method might slightly outperform price rounding as it uses a smaller scaling factor ( versus ), however the actual price computation is slightly more expensive: matrix-vector multiplication versus rounding. Regardless, both scaling factors have the same order of magnitude and we expect that their running times also have the same order of magnitude. We will only focus on price rounding in this comparison, due to its simplicity.

Algorithm 3 solves two LPs successively: it solves (LP1) first to compute market clearing prices and reduced costs. Then it fixes all variables with positive reduced costs to the upper bound, and variables with negative reduced costs to the lower bound. The remaining free variables are used to maximize the execution volume; see Müller (2014, Section 1.4) for a discussion of this approach.

Algorithm 4 also solves two LPs successively: it solves (LP1) first to compute the market clearing prices and then (LP2) to maximize the executed volume subject to the maximized economic surplus of the first LP.

Finally, Algorithm 5 represents our initial approach proposed in Winter et al (2014): it scales the objective with the naive scaling factor, solves (LP3), and then recovers the prices using (LP4).

In the following we will provide numerical results for the previously introduced algorithms.

Comparison of Algorithm 1 using varying subroutines

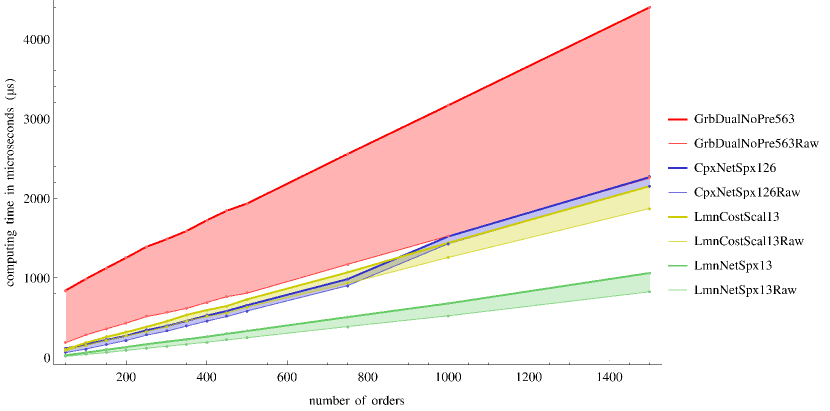

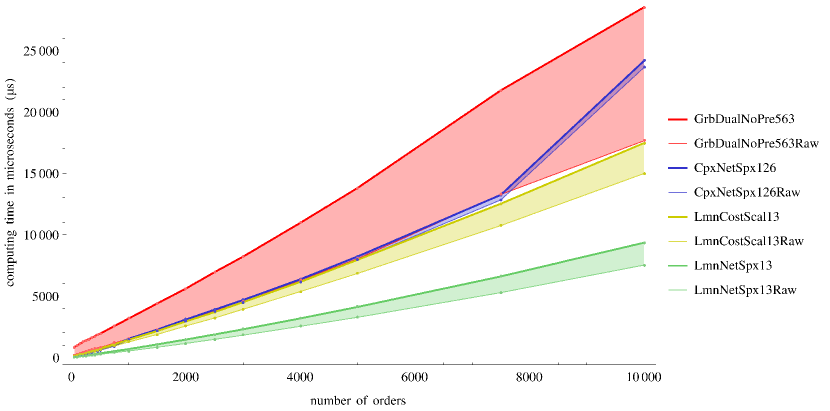

In each algorithm up to two linear programs need to be solved by a subroutine. In Algorithm 1, for instance, the subproblem (LP3) must be solved. In general, we can use the simplex method for solving these subproblems. In the case of (LP3), we can also use special purpose solvers as it is a min cost flow problem. The chosen subroutine for solving the LPs can have a huge impact on the overall running time.

We will now compare the running time of four different variants of Algorithm 1 using four different subroutines for solving (LP3). For this purpose, we solved 3000 random instances, each having 20 contracts and up to 10,000 orders. Note that (LP3) is a min cost flow problem with a large number of parallel arcs and a small number of nodes. Ahuja et al. propose to solve such problems with algorithms which handle the parallel arcs implicitly (Ahuja et al, 1993, Chapter 14.4 and 14.5) and the authors describe such a polynomial time algorithm. In order to be able to apply this algorithm to (LP3), one must transform it into a convex cost flow problem with separable piecewise linear cost functions, which can be done in polynomial time.

For our comparison here we will focus on utilizing available state-of-the-art software libraries. We compare the Lemon network simplex and the Lemon cost scaling algorithm [both from COIN-OR Lemon Graph Library (Lemon, 2014)] with CPLEX’s network simplex and Gurobi’s dual simplex; Gurobi and CPLEX are the leading mixed-integer programming solvers. The COIN-OR Lemon Graph Library (Lemon, 2014) provides several efficient implementations of min cost flow algorithms (Király and Kovács, 2012), for instance, the network simplex and the cost-scaling algorithm of Goldberg and Tarjan (Bünnagel et al, 1998).

The two graphs in Figure 1 display the average computing time111C++ program running on a Core i7-920, 6GB-DDR3, 64Bit Linux using Lemon 1.3, CPLEX 12.6. Network C-API, and Gurobi 5.6.3 without presolving. for instances with 20 contracts/nodes and a varying number of orders/parallel arcs. Each data point represents the average computing time of 50 random-instances. The instances are solved as follows: At first we load the raw instance parameters into the memory (RAM). Then, in the model creation phase, we create and load an instance of (LP3) with scaling factor into the memory of the respective solver via its application programming interface (API). Next, in the raw computing phase, we call the solver routine that starts the computations, we import the results via the API, and finally compute the prices as described in equation (23).

Figure 1 shows that in our test cases, the Lemon network simplex clearly outperforms the other three algorithms. For example, its average computing time for instances with orders amounts to only , whereas Gurobi’s dual simplex requires ; on average, instances with 10,000 orders are solved in , whereas Gurobi requires . The long total computing times of Gurobi are basically due to the fact that the creation of the LP model requires a lot of time. In contrast to Gurobi, CPLEX provides a network API that allows for a fast model creation. Due to this fast API, the CPLEX network simplex easily outperforms Gurobi’s dual simplex. Nevertheless, the Lemon cost scaling is still slightly faster than the CPLEX network simplex. We would like to stress, though, that the cost scaling algorithm is actually not a valid subroutine for Algorithm 1, as it provides arbitrary optimal solutions and does not provide the required optimal extreme points. We included this algorithm mainly for the sake of comparison.

Apart from the significantly shorter computing times, the Lemon network simplex has further advantages in comparison to CPLEX and Gurobi: as it is open source the source code can be readily modified. Moreover, it uses exact arithmetic without any numerical errors, whereas CPLEX and Gurobi use floating point operations, which are exposed to small numerical errors. These numerical errors though are of secondary importance as they can be safely ignored: due to optimal solutions being integral, rounding a flawed fractional basic solution yields the correct integral basic solution.

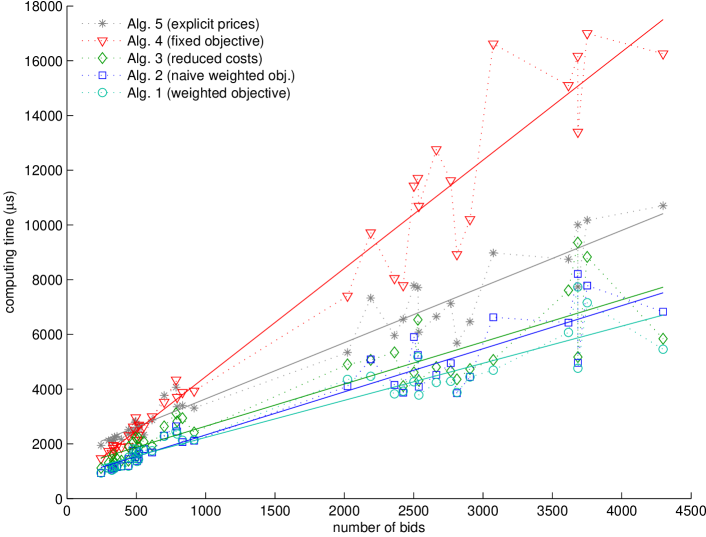

Comparison of Algorithms 1 to 5 on real-world instances

We will now compare the running times of Algorithms 1 to 5. For each algorithm we present numerical results of the algorithm variant that uses the CPLEX network simplex as a subroutine222Java program running on a Core i7-920, 6GB-DDR3, 64Bit Linux using CPLEX 12.4 and OpenJDK IcedTea6 1.12.6.. In the previous section, we used different standard solvers as subroutines for Algorithm 1 (weighted objective) and observed that the Lemon network simplex is in all likelihood the best solver for this task (see Figure 1)333Average computing time of Alg. 1 with Lemon network simplex for the real-world instances in Sec. 5.3 (20 runs per instance): (Java program running on a Core i7-920, 6GB-DDR3, 64Bit Linux using Lemon 1.3.1 and OpenJDK IcedTea7 2.6.6).. However, in this section, Algorithms 4 and 5 require an LP solver as subroutine. For this reason, we decided to use the CPLEX network simplex for all five algorithms in our comparison.

In this test, we solved 40 real-world instances with each algorithm. The instances were generated from historical order books of EUREX and were initially studied by Winter et al (2011). The proposed solution approach therein is an integer programming model444ZIMPL model running on a Pentium 4, 3.06GHz, 512MB, Windows XP SP3 using SCIP 1.1.0. solving the futures opening auction problem. For completeness, we would like to mention that the original data set has 55 instances, however only for 40 instances the order books could be fully reconstructed, which is necessary for a comparison.

Figure 2 shows the computing times of Algorithm 1 to 5. The figure suggests that the computing time is roughly linear in the number of orders, which is also consistent with the results in Section 5.2. Furthermore, we can see that Algorithm 4 (fixed objective) is the slowest one. The second slowest algorithm is Algorithm 5 (explicit prices) as its price computation via (LP4) is very time consuming. The computing times of the other three algorithms are the shortest ones and are more or less similar.

| Computing time in (average of 10 runs per instance) | |||||||

| Weighted | Naive | Reduced | Fixed | Explicit | |||

| objective | weighted obj. | costs | objective | prices | |||

| 1 LP | 1 LP | 2 LPs | 2 LPs | 2 LPs | IP model | ||

| # | Bids | Alg. 1 | Alg. 2 | Alg. 3 | Alg. 4 | Alg. 5 | Winter et al (2011) |

| 1 | 246 | 937 | 931 | 1120 | 1464 | 1947 | 270000 |

| 2 | 300 | 1115 | 1095 | 1307 | 1729 | 2121 | 80000 |

| 3 | 324 | 1037 | 1060 | 1231 | 1666 | 2112 | 70000 |

| 4 | 334 | 1161 | 1101 | 1629 | 1841 | 2157 | 750000 |

| 5 | 336 | 1170 | 1106 | 1386 | 1947 | 2140 | 970000 |

| 6 | 342 | 1102 | 1139 | 1290 | 1757 | 2251 | 90000 |

| 7 | 361 | 1184 | 1148 | 1449 | 1909 | 2273 | 530000 |

| 8 | 393 | 1192 | 1180 | 1387 | 1880 | 2167 | 500000 |

| 9 | 443 | 1186 | 1193 | 1387 | 1904 | 2360 | 210000 |

| 10 | 445 | 1511 | 1442 | 1894 | 2305 | 2520 | 340000 |

| 11 | 478 | 1821 | 1744 | 2056 | 2621 | 2477 | 120000 |

| 12 | 491 | 1473 | 1512 | 1661 | 2488 | 2786 | 140000 |

| 13 | 496 | 1807 | 1736 | 2227 | 2956 | 2829 | 250000 |

| 14 | 505 | 1355 | 1364 | 1555 | 2137 | 2468 | 110000 |

| 15 | 516 | 1441 | 1437 | 1871 | 2322 | 2665 | 630000 |

| 16 | 518 | 1695 | 1637 | 2215 | 2690 | 2608 | 700000 |

| 17 | 555 | 1774 | 1809 | 2076 | 2645 | 2327 | 130000 |

| 18 | 614 | 1747 | 1685 | 1941 | 2997 | 2871 | 220000 |

| 19 | 701 | 2277 | 2303 | 2640 | 3530 | 3769 | 80000 |

| 20 | 787 | 2454 | 2643 | 3117 | 4336 | 4071 | 480000 |

| 21 | 794 | 2363 | 2457 | 2821 | 3705 | 3360 | 110000 |

| 22 | 833 | 2132 | 2063 | 2943 | 3885 | 3399 | 110000 |

| 23 | 917 | 2155 | 2113 | 2416 | 3934 | 3307 | 8220000 |

| 24 | 2023 | 4354 | 4105 | 4906 | 7404 | 5340 | 30000 |

| 25 | 2190 | 4470 | 5089 | 5066 | 9720 | 7328 | 90000 |

| 26 | 2361 | 3828 | 4154 | 5345 | 8046 | 5957 | 100000 |

| 27 | 2424 | 3925 | 3869 | 4112 | 7788 | 6557 | 1270000 |

| 28 | 2502 | 4271 | 5907 | 4612 | 11424 | 7782 | 110000 |

| 29 | 2530 | 5180 | 5250 | 6536 | 11706 | 7710 | 220000 |

| 30 | 2537 | 3787 | 4089 | 4311 | 10686 | 6083 | 120000 |

| 31 | 2663 | 4244 | 4522 | 4806 | 12753 | 6650 | 5330000 |

| 32 | 2767 | 4286 | 4947 | 4656 | 11623 | 7130 | 450000 |

| 33 | 2812 | 3877 | 3853 | 4358 | 8922 | 5678 | 50000 |

| 34 | 2906 | 4446 | 4449 | 4734 | 10205 | 6465 | 150000 |

| 35 | 3074 | 4693 | 6626 | 5067 | 16617 | 8976 | 11970000 |

| 36 | 3616 | 6072 | 6431 | 7611 | 15096 | 8746 | 1200000 |

| 37 | 3683 | 7731 | 8211 | 9356 | 16172 | 10004 | 350000 |

| 38 | 3684 | 4764 | 4960 | 5172 | 13393 | 7731 | 40000 |

| 39 | 3751 | 7156 | 7785 | 8831 | 16996 | 10173 | 70000 |

| 40 | 4298 | 5458 | 6829 | 5844 | 16254 | 10701 | 70000 |

| avg. | 1539 | 2966 | 3174 | 3474 | 6586 | 4750 | 918250 |

Table 1 presents the average computing times of the five algorithms and the one of Winter et al (2011). Note that the computing times of Winter et al (2011) are not directly comparable as the computations where performed on a slower machine and with a different solver. However, the table shows that this method is the slowest one by a huge margin so that the difference in hard- and software is negligible. The fastest method is Algorithm 1 (weighted objective). Its average computing time amounts to only . Furthermore, we see that Algorithm 3 (reduced costs) is a reasonable alternative to Algorithm 1, since its average computing time of is only slightly longer but it is numerically more robust, as it does not scale the objective.

Furthermore, we can observe that the running time of the CPLEX network simplex depends on the size of the scaling factor: the smaller the factor, the shorter the running time (see Table 1). The polynomial network simplex variant of Orlin (1997) behaves in a qualitatively similar way. It runs in

time, where is the largest absolute objective coefficient.

Arbitrage example

We now provide an example where the new model yields a higher surplus, a higher liquidity, and a better price quality than the old one. Moreover, we show how an arbitrage trader can make a risk free profit in this situation.

Example 3

Assume that there are three orders in the order books:

-

1.

Buy 1 gold contract with delivery in June; Limit price: .

-

2.

Sell 1 gold contract with delivery in August; Limit price: .

-

3.

Sell 1 gold combination ; Limit price: .

The old auction model would not match any contracts as it would perform a separate auction for each product. The total surplus would amount to and the exchange would not publish any market clearing price because no order was executed. In the new model, all three orders can be matched. The total surplus amounts to and the exchange would, for example, publish the following market clearing prices:

-

•

June: ,

-

•

August: ,

-

•

: .

This solution is preferred to the zero solution since it increases the liquidity and price quality. Now assume that an arbitrage trader looks at the order books and submits the following three additional orders immediately before the auction starts:

-

4.

Sell 1 gold contract with delivery in June; Limit price: .

-

5.

Buy 1 gold contract with delivery in August; Limit price: .

-

6.

Buy 1 gold combination ; Limit price: .

In the old model, all 6 orders would be executed and the surplus of each product auction would be zero, but the arbitrage trader would end up with a risk free profit of (minus trading fees, e.g.: ). The exchange would publish the following inconsistent prices:

-

•

June: ,

-

•

August: ,

-

•

: , which differs from .

In the new model, the additional orders of the arbitrage trader would not be executed and would not affect the outcome of the auction.

Summary

We introduced several new methods for solving the futures opening auction problem. We showed that the problem can be modeled as a min cost flow problem with two hierarchical objectives. The primary objective is the surplus maximization and the secondary one is the volume maximization. This kind of problem can be solved efficiently by exploiting the properties of extreme point solutions, as it is done in Proposition 2 and Theorem 4.1. The resulting algorithm is very simple as it just computes a pair of primal dual optimal extreme points of a min cost flow problem with a weighted objective and then scales and rounds the dual solution. However, it is not only the simplest algorithm but also turned out to be the fastest one in our numerical tests. In those tests we also compared different standard solvers for solving the underlying optimization problems. The results suggest that the Lemon network simplex is the fastest one for this task. Due to the short computing times, our algorithm (with Lemon as a subroutine) is well suited for real-world applications.

Acknowledgements.

We want to thank M. Rudel for providing us insight into his research results and for providing us with his test data that enabled us to quickly verify our model. We also would like to thank H. Schäfer for supporting our work and D. Weninger and A. Jüttner for the helpful discussions. We thank the DFG for their support within projects A05 and B07 in CRC TRR 154. Last but not least, we would like to thank the reviewers for their valuable comments.References

- Ahuja et al (1993) Ahuja RK, Magnanti TL, Orlin JB (1993) Network flows. Prentice Hall Inc., Englewood Cliffs, NJ, theory, algorithms, and applications

- Arrow and Debreu (1954) Arrow KJ, Debreu G (1954) Existence of an equilibrium for a competitive economy. Econometrica: Journal of the Econometric Society 22(3):265–290

- Blumrosen and Nisan (2007) Blumrosen L, Nisan N (2007) Combinatorial auctions. In: Algorithmic game theory, Cambridge Univ. Press, Cambridge, pp 267–299

- Boyd and Vandenberghe (2004) Boyd S, Vandenberghe L (2004) Convex optimization. Cambridge University Press, Cambridge

- Bünnagel et al (1998) Bünnagel U, Korte B, Vygen J (1998) Efficient implementation of the Goldberg-Tarjan minimum-cost flow algorithm. Optim Methods Softw 10(2):157–174, DOI \hrefhttp://dx.doi.org/10.1080/1055678980880570910.1080/10556789808805709

- Cooper (2015) Cooper CL (2015) The Blackwell Encyclopedia of Management, vol IV Finance. Online Reference: \hrefhttp://www.blackwellreference.com/public/tocnode?id=g9780631233176_chunk_g978140511826218_ss1-6Rollover Risk. Blackwell Publishing, URL http://www.blackwellreference.com/public/book.html?id=g9780631233176_9780631233176

- de Vries and Vohra (2003) de Vries S, Vohra RV (2003) Combinatorial auctions: a survey. INFORMS J Comput 15(3):284–309, DOI \hrefhttp://dx.doi.org/10.1287/ijoc.15.3.284.1607710.1287/ijoc.15.3.284.16077

- Gould et al (2013) Gould MD, Porter MA, Williams S, McDonald M, Fenn DJ, Howison SD (2013) Limit order books. Quant Finance 13(11):1709–1742, DOI \hrefhttp://dx.doi.org/10.1080/14697688.2013.80314810.1080/14697688.2013.803148

- Hoffman and Kruskal (1956) Hoffman AJ, Kruskal JB (1956) Integral boundary points of convex polyhedra. In: Linear inequalities and related systems, Annals of Mathematics Studies, no. 38, Princeton University Press, Princeton, N. J., pp 223–246

- Hull (2006) Hull JC (2006) Options, Futures, and other Derivatives, sixth edn. Prentice Hall, New Jersey

- Király and Kovács (2012) Király Z, Kovács P (2012) Efficient implementations of minimum-cost flow algorithms. Acta Univ Sapientiae, Informatica 4(1):67–118, \hrefhttp://arxiv.org/abs/1207.6381arXiv:1207.6381

- Lemon (2014) Lemon (2014) Library for Efficient Modeling and Optimization in Networks. Version: 1.3. URL http://lemon.cs.elte.hu

- Martin et al (2014) Martin A, Müller JC, Pokutta S (2014) Strict linear prices in non-convex European day-ahead electricity markets. Optim Methods Softw 29(1):189–221, DOI \hrefhttp://dx.doi.org/10.1080/10556788.2013.82354410.1080/10556788.2013.823544, \hrefhttp://arxiv.org/abs/1203.4177arXiv:1203.4177

- Mas-Colell et al (1995) Mas-Colell A, Whinston MD, Green JR (1995) Microeconomic Theory. Oxford University Press, New York

- Müller (2014) Müller JC (2014) Auctions in Exchange Trading Systems: Modeling Techniques and Algorithms. PhD thesis, University of Erlangen-Nuremberg, DOI \hrefhttp://dx.doi.org/10.13140/2.1.1621.840510.13140/2.1.1621.8405, \hrefhttp://nbn-resolving.de/urn:nbn:de:bvb:29-opus4-53396urn:nbn:de:bvb:29-opus4-53396

- Orlin (1997) Orlin JB (1997) A polynomial time primal network simplex algorithm for minimum cost flows. Math Programming 78(2, Ser. B):109–129, DOI \hrefhttp://dx.doi.org/10.1007/BF0261436510.1007/BF02614365, network optimization: algorithms and applications (San Miniato, 1993)

- Winter et al (2011) Winter T, Rudel M, Lalla H, Brendgen S, Geißler B, Martin A, Morsi A (2011) System and method for performing an opening auction of a derivative. URL https://www.google.de/patents/US20110119170, Pub. No.: US 2011/0119170 A1. US Patent App. 12/618,410

- Winter et al (2014) Winter T, Müller JC, Martin A, Pape S, Peter A, Pokutta S (2014) Method and system for performing an opening auction of a derivative. URL http://www.google.com/patents/US20140372275, Pub. No.: US 2014/0372275 A1. US Patent App. 13/920,041