On queues with service and interarrival times depending on waiting times

Abstract

We consider an extension of the standard queue, described by the equation , where and . For this model reduces to the classical Lindley equation for the waiting time in the queue, whereas for it describes the waiting time of the server in an alternating service model. For all other values of this model describes a FCFS queue in which the service times and interarrival times depend linearly and randomly on the waiting times. We derive the distribution of when is generally distributed and follows a phase-type distribution, and when is exponentially distributed and deterministic.

⋆ EURANDOM,

P.O. Box 513, 5600 MB Eindhoven, The Netherlands.

⋆⋆ Eindhoven University of Technology,

Department of Mathematics & Computer Science,

P.O. Box 513, 5600 MB Eindhoven, The Netherlands.

⋆⋆⋆ Georgia Institute of Technology,

H. Milton Stewart School of Industrial & Systems Engineering,

765 Ferst Drive, Atlanta GA 30332-0205, USA.

1 Introduction

One of the most fundamental relations in queuing and random walk theory is Lindley’s recursion [11]:

| (1.1) |

In queuing theory, it represents a relation between the waiting times of the -th and -st customer in a single server queue, indicating the interarrival time between the -th and -st customer and denoting the service time of the -th customer. In the applied probability literature there has been a considerable amount of interest in generalisations of Lindley’s recursion, namely the class of Markov chains described by the recursion . For earlier work on such stochastic recursions see for example Brandt et al. [5] and Borovkov and Foss [3]. Many structural properties of this recursion have been derived. For example, Asmussen and Sigman [2] develop a duality theory, relating the steady-state distribution to a ruin probability associated with a risk process. More references in this domain can be found for example in Asmussen and Schock Petersen [1] and Seal [16]. An important assumption which is often made in these studies is that the function is non-decreasing in its main argument . For example, in [2] this assumption is crucial for their duality theory to hold.

In this paper we consider a generalisation of Lindley’s recursion, for which the monotonicity assumption does not hold. In particular, we study the Lindley-type recursion

| (1.2) |

where for every , the random variable is equal to plus or minus one according to the probabilities and , . The sequences and are assumed to be independent sequences of i.i.d. non-negative random variables. Our main goal is to derive the steady-state distribution of , when it exists.

Equation (1.2) reduces to the classical Lindley recursion [11] when for every . Furthermore, if , then (1.2) describes the waiting time of the server in an alternating service model with two service points. For a description of the model for this special case and related results see Park et al. [13] and Vlasiou et al. [20, 21, 22, 23].

Studying a recursion that contains both Lindley’s classical recursion and the recursion in [13, 20, 21, 22, 23] as special cases seems of interest in its own right. Additional motivation for studying the recursion is supplied by the fact that, for , the resulting model can be interpreted as a special case of a queuing model in which service and interarrival times depend on waiting times. We shall now discuss the latter model.

Consider an extension of the standard queue in which the service times and the interarrival times depend linearly and randomly on the waiting times. Namely, the model is specified by a stationary and ergodic sequence of four-tuples of nonnegative random variables , . The sequence is defined recursively by

where

We interpret as the waiting time and as the service time of customer . Furthermore, we take to be the interarrival time between customers and . We call the nominal service time of customer and the nominal interarrival time between customers and , because these would be the actual times if the additional shift were omitted, that is, if .

Evidently, the waiting times satisfy the generalised Lindley recursion (1.2), where we have written . This model – for generally distributed random variables – has been introduced in Whitt [24], where the focus is on conditions for the process to converge to a proper steady-state limit, and on approximations for this limit. There are very few exact results known for queuing models in which interarrival and/or service times depend on waiting times; we refer to Whitt [24] for some references.

Whitt [24] builds upon previous results by Vervaat [19] and Brandt [4] for the unrestricted recursion , where . There has been considerable previous work on this unrestricted recursion, due to its close connection to the problem of the ruin of an insurer who is exposed to a stochastic economic environment. Such an environment has two kinds of risk, which were called by Norberg [12] insurance risk and financial risk. Indicatively, we mention the work by Tang and Tsitsiashvili [17], and by Kalashnikov and Norberg [10]. In the more general framework, may represent an inventory in time period (e.g. cash), may represent a multiplicative, possibly random, decay or growth factor between times and (e.g. interest rate) and may represent a quantity that is added or subtracted between times and (e.g. deposit minus withdrawal). Obviously, the positive-part operator is appropriate for many applications [24].

This paper presents an exact analysis of the steady-state distribution of as given by (1.2) with and . For , this amounts to analysing the above-described extension where with probability , and with probability . This problem, and state-dependent queuing processes in general, is connected to LaPalice queuing models, introduced by Jacquet [9], where customers are scheduled in such a way that the period between two consecutively scheduled customers is greater than or equal to the service time of the first customer.

This paper is organised in the following way. In Section 2 we comment on the stability of the process , as it is defined by Recursion (1.2). In the remainder of the paper it is assumed that the steady-state distribution of exists. Section 3 is devoted to the determination of the distribution of when is generally distributed and has a phase-type distribution. In Section 4 we determine the distribution of when is exponentially distributed and is deterministic. At the end of each section we compare the results that we derive to the already known results for Lindley’s recursion (i.e. for ) and to the equivalent results for the Lindley-type recursion arising for .

At the end of this introduction we mention a few notational conventions. For a random variable we denote its distribution by and its density by . Furthermore, we shall denote by the -th derivative of the function . The Laplace-Stieltjes transforms (LST) of and are respectively denoted by and . To keep expressions simple, we also use the function defined as .

2 Stability

The following result on the convergence of the process to a proper limit is shown in Whitt [24]. It is included here only for completeness.

From Recursion (1.2), it is obvious that if we replace by and by , then the resulting waiting times will be at least as large as the ones given by (1.2). Moreover, when we make this change, the positive-part operator is not necessary anymore.

Lemma 1 (Whitt [24, Lemma 1]).

So if satisfies (1.2), satisfies (2.1), and converges to the proper limit , then is tight and for all , where is the limit in distribution of any convergent subsequence of . This observation, combined with Theorem 1 of Brandt [4], which implies that satisfying (2.1) converges to a proper limit if , leads to the following theorem.

Theorem 1 (Whitt [24, Theorem 1]).

The series is tight for all and . If, in addition, and is a sequence of independent vectors with

then the events are regeneration points with finite mean time and converges in distribution to a proper limit as for all and .

Naturally, for , i.e. for the classical Lindley recursion, we need the additional condition that .

Therefore, assume that the sequences and are independent stationary sequences, that are also independent of one another, and that for all , and are non-negative. Then the conditions of Theorem 1 hold, so there exists a proper limit , and for the system in steady-state we write

| (2.2) |

where “” denotes equality in distribution, where , are generic random variables distributed like , , and where and .

Remark 1.

For Equation (2.2) yields that

where (note that ). Assuming that the distribution of the random variable is continuous, the last term is equal to , which gives us that

This means that the limiting distribution of , provided that is continuous, satisfies the functional equation

| (2.3) |

Therefore, there exists at least one function that is a solution to (2.3). It can be shown that in fact there exists a unique measurable bounded function that satisfies this functional equation.

To show this, consider the space , i.e. the space of measurable and bounded functions on the real line with the norm

In this space define the mapping

Note that , i.e., is measurable and bounded. For two arbitrary functions and in this space we have

Note that the supremum appearing above is less than or equal to for and equal to for . Therefore, since for it holds that , for these values of the parameter we have a contraction mapping. Furthermore, we know that is a Banach space, therefore by the Fixed Point Theorem we have that (2.3) has a unique solution; for a related discussion, see also [20].

In the next two sections we determine the distribution of for two cases in which and are independent and i.i.d. sequences of non-negative random variables.

3 The GI/PH case

In this section we assume that is generally distributed, while follows a particular phase-type distribution. Specifically, we assume that with probability the nominal service time follows an Erlang distribution with parameter and phases, i.e.,

| (3.1) |

with LST . These distributions, i.e. mixtures of Erlang distributions, are special cases of Coxian or phase-type distributions. It is sufficient to consider only this class, since it may be used to approximate any given continuous distribution on arbitrarily close; see Schassberger [15]. Following the proof in [22], one can show that for such an approximation of , the error in the resulting waiting time approximation can be bounded.

We are interested in the distribution of . In order to derive the distribution of , we shall first derive the LST of . We follow a method based on Wiener-Hopf decomposition. A straightforward calculation yields for values of such that :

| (3.2) |

here , and are independent random variables. The Lindley-type equation for generally distributed and phase-type has already been analysed in Vlasiou and Adan [21], and the LST of the corresponding is given there. From Equation (3.8) of [21] we can readily copy an expression for the last two terms appearing in (3.2), so can now be written as

So for we have that

| (3.3) |

Cohen [6, p. 322–323] shows by applying Rouché’s theorem that the function

has exactly zeros in the left-half plane if (it is assumed that , which is not an essential restriction) or if and . Naturally, this statement is not valid if ; therefore, this case needs to be excluded from this point on. So we rewrite (3.3) as follows

| (3.4) |

The left-hand side of (3.4) is analytic for and continuous for , and the right-hand side of (3.4) is analytic for and continuous for . So from Liouville’s theorem [18] we have that both sides of (3.4) are the same -th degree polynomial, say, . Hence,

| (3.5) |

In the expression above, the constants are not determined so far, while the roots are known. In order to obtain the transform, observe that is a fraction of two polynomials of degree . So, ignoring the special case of multiple zeros , partial fraction decomposition yields that (3.5) can be rewritten as

| (3.6) |

which implies that the waiting time distribution has a mass at the origin that is given by

and has a density that is given by

All that remains is to determine the constants . To do so, we work as follows.

We shall substitute (3.6) in the left-hand side of (3.4), and express the terms and that appear at the right-hand side of (3.4) in terms of the constants . Note that the terms that appear at the right-hand side of (3.4) can also be expressed in terms of the constants . Thus we obtain a new equation that we shall differentiate a total of times. We shall evaluate each of these derivatives for and thus we obtain a linear system of equations for the constants , . The last equation that is necessary to uniquely determine the constants is the normalisation equation

| (3.7) |

To begin with, note that

| (3.8) |

with

| (3.9) |

and

| (3.10) |

Likewise, we have that

| (3.11) |

with

| (3.12) |

and

| (3.13) |

So, using (3.9) and (3.10), substitute (3.8) in the right-hand side of (3.4), and similarly for (3.11). Furthermore, as mentioned before, substitute (3.6) into the left-hand side of (3.4) to obtain an expression, where both sides can be reduced to an -th degree polynomial in . By evaluating this polynomial and all its derivatives for we obtain equations binding the constants . These equations, and the normalisation equation (3.7), form a linear system for the constants , , that uniquely determines them (see also Remark 2 below). For example, the first equation, evaluated at , yields that

since . We summarise the above in the following theorem.

Theorem 2.

Consider the recursion given by (1.2), and assume that . Let (3.1) be the distribution of the random variable . Then the limiting distribution of the waiting time has mass at the origin and a density on that is given by

In the above equation, the constants , with , are the roots of

and the constants are the unique solution to the linear system described above.

Remark 2.

Although the roots and coefficients may be complex, the density and the mass at zero will be positive. This follows from the fact that there is a unique equilibrium distribution and thus a unique solution to the linear system for the coefficients . Of course, it is also clear that each root and coefficient have a companion conjugate root and conjugate coefficient, which implies that the imaginary parts appearing in the density cancel.

Remark 3.

In case that has multiplicity greater than one for one or more values of , the analysis proceeds in essentially the same way. For example, if , then the partial fraction decomposition of becomes

the inverse of which is given by

Remark 4.

For the nominal service time we have considered only mixtures of Erlang distributions, mainly because this class approximates well any continuous distribution on and because we can illustrate the techniques we use without complicating the analysis. However, we can extend this class by considering distributions with a rational Laplace transform. The analysis in [21] can be extended to such distributions, and the analysis in Cohen [6, Section II.5.10] is already given for such distributions, so the results given there can be implemented directly.

Remark 5.

The analysis we have presented so far can be directly extended to the case where takes any finite number of negative values. In other words, let the distribution of be given by , and for , , where and . Then, for example, Equation (3.3) becomes

Following the same steps as below (3.3), we can conclude that the waiting time density is again given by a mixture of exponentials of the form

where the new constants (and the mass of the distribution at zero, given by ) are to be determined as the unique solution to a linear system of equations. The only additional remark necessary when forming this linear system is to observe that both the probability and the expectation can be expressed linearly in terms of the constants .

The case

We have seen that the case where for all , or in other words the case , had to be excluded from the analysis. Equation (3.4) is still valid if we take the constants to be defined as in Theorem 2. However, one cannot apply Liouville’s theorem to the resulting equation. The transform can be inverted directly. As it is shown in [21], the terms that remain to be determined follow by differentiating (3.4) times and evaluating at for . The density in this case is a mixture of Erlang distributions with the same scale parameter for all exponential phases. As we can see, for the resulting density is intrinsically different from the one described in Theorem 2.

The case

If and , then we are analysing the steady-state waiting time distribution of a queue. Equation (3.4) now reduces to

| (3.14) |

Earlier we have already observed that the right-hand side of (3.14) is equal to an -th degree polynomial . Inspection of the right-hand side of (3.14) reveals that it has an -fold zero in . Indeed, all zeros of the numerator of the quotient in the right-hand side cancel against zeros of the denominator, and the term

is finite for . Hence,

| (3.15) |

Combining (3.14) and (3.15), we conclude that

and since , the last equation gives us that

Thus, we have that

which is in agreement with Equation II.5.190 in [6, p. 324].

4 The M/D case

We have examined so far the case where the nominal interarrival time is generally distributed and the nominal service time follows a phase-type distribution. In other words, we have studied the case which is in a sense analogous to the ordinary queue. We now would like to study the reversed situation; namely, the case analogous to the queue.

The queue has been studied in much detail. However, the analogous alternating service model – i.e., take in (1.2), so – seems to be more complicated to analyse. As shown in [20], if , the density of satisfies a generalised Wiener-Hopf equation, for which no solution is known in general. The presently available results for the distribution of with are developed in [20], where is assumed to belong to a class strictly bigger than the class of functions with rational Laplace transforms, but not completely general. Moreover, the method developed in [20] breaks down when applied to (2.2) with not identically equal to .

We shall refrain from trying to develop an alternative approach for the case with a more general distribution for than the one treated in Section 3. Instead, we give a detailed analysis of the case: is exponentially distributed and is deterministic. This case is neither contained in the case of the previous section nor has it been treated (for the special choice of ) in [20]. Its analysis is of interest for various reasons. To start with, the model generalises the classical queue; additionally, the analysis illustrates the difficulties that arise when studying (2.2) in case is exponentially distributed and is generally distributed; finally, the different effects of Lindley’s classical recursion and of the Lindley-type recursion discussed in [20] are clearly exposed. As we shall see in the following, the analysis can be practically split into two parts, where each part follows the analysis of the corresponding model with , or .

4.1 Deterministic nominal service times

As before, consider Equation (2.2), and assume that with probability and with probability . Let be exponentially distributed with rate and be equal to , where . Furthermore, we shall denote by the mass of the distribution of at zero; that is, .

For this setting, we have from (2.2) that for ,

| (4.1) |

So, for the above equation reduces to

| (4.2) |

and for , Equation (4.1) reduces to

| (4.3) |

where we have utilised the normalisation equation

| (4.4) |

In the following, we shall derive the distribution on the interval and on the interval separately. At this point though, one should note that from Equation (2.2) it is apparent that for exponentially distributed and , the distribution of is continuous on . Also, one can verify that Equation (4.2) for reduces to Equation (4.3) for . The fact that is continuous on will be used extensively in the sequel. Notice also that from Equations (4.2) and (4.3) we can immediately see that we can differentiate for and ; see, for example, Titchmarsh [18, p. 59].

The distribution on

In all subsequent equations it is assumed that . In order to derive the distribution of on , we differentiate (4.2) once to obtain

We rewrite this equation after noticing that the second line is equal to zero, while the sum of the integrals in the first line can be rewritten by using (4.2). Thus, we have that

| (4.5) |

In order to obtain a linear differential equation, differentiate (4.1) once more, which leads to

| (4.6) |

Equation (4.6) is a homogeneous linear differential equation, not of a standard form because of the argument that appears at the right-hand side. To solve it, we substitute for in (4.6) to obtain

| (4.7) |

Then, we differentiate (4.6) once more to obtain

and we eliminate the term by using (4.7). Thus, we conclude that

| (4.8) |

For , the solution to this differential equation is given by

| (4.9) |

where and are given by

| (4.10) |

and the constants and will be determined by the initial conditions. Namely, the solution needs to satisfy (4.6) and the condition . Thus, for the first equation, substitute the general solution we have derived into (4.6). For the second equation, first rewrite (4.1) as follows:

then substitute from (4.9), and finally evaluate the resulting equation for . This system uniquely determines and . Specifically, we have that

where in the process we have assumed that . Up to this point we have that the waiting-time distribution on is given by

| (4.11) |

where and are known up to the probability . The cases for and follow directly from Equation (4.8) and will be handled separately in the sequel.

The distribution on

As before, we obtain a differential equation by differentiating (4.3) once, and substituting the resulting integrals by using (4.3) once more. Thus, we obtain the equation

which can be reduced to

| (4.12) |

Equation (4.12) is a delay differential equation that can be solved recursively. Observe that for , the term has been derived in the previous step, so for , Equation (4.12) reduces to an ordinary linear differential equation from which we can easily derive the distribution of in the interval .

For simplicity, denote by the distribution of when , and analogously denote by the density of , when . Then (4.12) states that

which leads to an expression for that is given in terms of an indefinite integral that is a function of , that is,

| (4.13) |

The constants can be derived by exploiting the fact that the waiting-time distribution is continuous. In particular, every is determined by the equation

| (4.14) |

Solving Equation (4.13) recursively, we obtain that

| (4.15) |

Observe that for , if we define the empty sum at the right-hand side to be equal to zero, then the above expression is satisfied. Notice that, since we have made use of the distribution on as it is given by (4.11), Equation (4.15) is not valid for or . From Equation (4.14) we now have that for every ,

| (4.16) |

where we have assumed that , and that for , the second sum is equal to zero. These expressions can be simplified further by observing that

Recall that and , and thus also all constants , are known in terms of . The probability that still remains to be determined will be given by the normalisation equation (4.4). Notice though, that since the waiting-time distribution is determined recursively for every interval , Equation (4.4) yields an infinite sum. The sum is well defined, since a unique density exists. The above findings are summarised in the following theorem.

Theorem 3.

Consider the recursion given by (1.2), and assume that . Let be exponentially distributed with rate and be equal to , where . Then for , , the limiting distribution of the waiting time is given by

where the constants are given by Equation (4.1) and the probability is given by the normalisation equation (4.4).

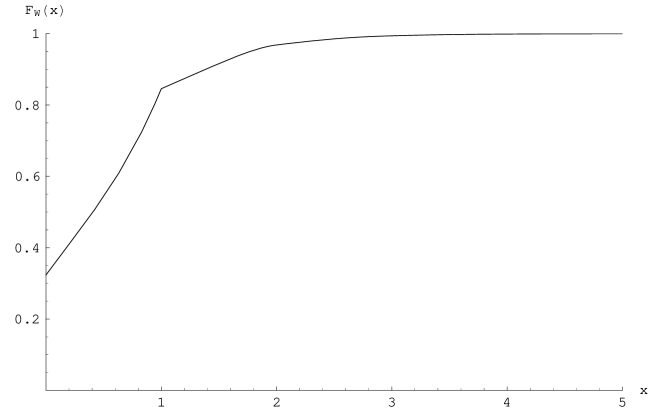

One might expect though that Equation (4.4) may not be suitable for numerically determining . However, if the probability is not too close to one, or in other words, if the system does not almost behave like an queue, then one can numerically approximate from the normalisation equation. As an example, in Figure 1 we display a typical plot of the waiting-time distribution. We have chosen , , and .

For close to one, we can see from the expressions for and that both the numerators and the denominators of these two constants approach zero. Furthermore, the denominators , that appear in the waiting-time distribution also approach zero, which makes Theorem 3 unsuitable for numerical computations for values of close to one. Moreover, we also see that very large values of the parameter may also lead to numerical problems, since is involved in the exponent of almost all exponential terms that appear in the waiting-time distribution.

As one can observe from Figure 1, and show from Theorem 3, is not differentiable for . This is not surprising, as the waiting-time distribution is defined by two different equations; namely Equation (4.2) for and Equation (4.3) for . Furthermore, from Equation (4.1) we have that

and from Equation (4.12) we have that

That is, .

The case

Observe that if then the support of is the interval . To determine the density of the waiting time, we insert into Equation (4.8). Thus, we obtain that

from which we immediately have that

for some constants and such that (4.6) is satisfied. The latter condition implies that for every the following equation must hold:

From this we conclude that is equal to zero, i.e. the waiting time has a mass at zero and is uniformly distributed on . To determine the mass and the constant we evaluate (4.1) at and we use the normalisation equation (4.4), keeping in mind that for . These two equations yield that if , then

| (4.17) |

Evidently, the density in this case is quite different from the density for , which is on a mixture of two exponentials; see (4.9).

Another way to see that , , is as follows. Recall that for and we have that . Equation (4.1) can now be written as

Replacing by shows that , which implies that and finally that , . It seems less straightforward to explain probabilistically that , given that , is uniformly distributed. With a view towards the recursion , we believe that this property is related to the fact that, if Poisson arrivals occur in some interval, then they are distributed like the order statistics of the uniform distribution on that interval; see Ross [14, Section 2.3].

The case

For the queue, Erlang [7] derived the following expression for the waiting-time distribution:

where is the traffic intensity. Recall that for the queue we have that . We see that for Equation (4.1) indeed leads to the waiting-time distribution , as it is given by Erlang’s expression for the first interval . For , one needs to recursively solve Equation (4.13) in order to obtain Erlang’s expression. However, since the recursive solution we have obtained for our model makes use of as it is given by (4.11), which is not valid for , the waiting-time distribution we have obtained in Theorem 3 cannot be extended to the case for .

The terms both in Erlang’s expression for the waiting-time distribution of an queue and in Theorem 3 alternate in sign and in general are much larger than their sum. Thus, the numerical evaluation of the sum may be hampered by roundoff errors due to the loss of significant digits, in particular under heavy traffic. For the queue, however, a satisfactory solution has been given by Franx [8] in a way that only a finite sum of positive terms is involved; thus, this expression presents no numerical complications, not even for high traffic intensities. For our model, extending Franx’s approach is a challenging problem as the representation of various quantities appearing in [8] which are related to the queue length at service initiations is not straightforward.

As we see, the waiting-time distribution in Theorem 3 is quite similar to Erlang’s expression, so we expect that eventually the solution will suffer from roundoff errors. However, a significant difference in the numerical computation between the queue and the model described by Recursion (1.2) arises when computing . For any single server queue we know a priori that . In our model, has to be computed from the normalisation equation, where the numerical complications when calculating the waiting-time distribution become apparent. In particular, as tends to , i.e. as the system behaves almost like an queue, the computation of becomes more problematic.

As a final observation, we note that the effects of Lindley’s classical recursion and of the Lindley-type recursion discussed in [20] are quite apparent. The analysis for our model is in a sense separated into two parts: the derivation of the waiting-time distribution in and in . In the first part, we see that Equation (4.6) is quite similar to the differential equation appearing in [22] for the derivation of the waiting-time distribution in case and follows a polynomial distribution. Moreover, one could use the same technique to derive a solution, but Equation (4.6) is too simple to call for such means. In the second part, we see the effects of the queue, as we eventually derive in a recursive manner. Furthermore, this model inherits all the numerical difficulties appearing in the classical solution for the queue, plus the additional difficulties of computing . For Lindley’s recursion, is known beforehand, while for the Lindley-type recursion described in [13, 20, 21, 22, 23] is derived by the normalisation equation.

Acknowledgements

The authors would like to thank Ivo Adan for his helpful remarks and his assistance in simulating this model.

References

- [1] S. Asmussen and S. Schock Petersen. Ruin probabilities expressed in terms of storage processes. Advances in Applied Probability, 20(4):913–916, December 1989.

- [2] S. Asmussen and K. Sigman. Monotone stochastic recursions and their duals. Probability in the Engineering and Informational Sciences, 10(1):1–20, January 1996.

- [3] A. A. Borovkov and S. Foss. Stochastically recursive sequences. Siberian Advances in Mathematics, 2:16–81, 1992.

- [4] A. Brandt. The stochastic equation with stationary coefficients. Advances in Applied Probability, 18(1):211–220, March 1986.

- [5] A. Brandt, P. Franken, and B. Lisek. Stationary Stochastic Models, volume 78 of Mathematische Lehrbücher und Monographien, II. Abteilung: Mathematische Monographien. Akademie-Verlag, Berlin, 1990.

- [6] J. W. Cohen. The Single Server Queue. North-Holland Publishing Co., Amsterdam, 1982.

- [7] A. K. Erlang. The theory of probabilities and telephone conversations. In E. Brockmeyer, H. L. Halstrøm, and A. Jensen, editors, The Life and Works of A. K. Erlang, number 6 in Applied Mathematics and Computing Machinery Series, pages 131–137. Acta Polytechnica Scandinavica, second edition, 1960. English translation. First published in “Nyt Tidsskrift for Matematik” B, Vol. 20 (1909), p. 33.

- [8] G. J. Franx. A simple solution for the M/D/c waiting time distribution. Operations Research Letters, 29(5):221–229, December 2001.

- [9] P. Jacquet. Subexponential tail distribution in LaPalice queues. Performance Evaluation Review, 20(1):60–69, June 1992.

- [10] V. Kalashnikov and R. Norberg. Power tailed ruin probabilities in the presence of risky investments. Stochastic Processes and their Applications, 98:211–228, 2002.

- [11] D. V. Lindley. The theory of queues with a single server. Proceedings Cambridge Philosophical Society, 48:277–289, 1952.

- [12] R. Norberg. Ruin problems with assets and liabilities of diffusion type. Stochastic Processes and their Applications, 81:255–269, 1999.

- [13] B. C. Park, J. Y. Park, and R. D. Foley. Carousel system performance. Journal of Applied Probability, 40(3):602–612, 2003.

- [14] S. M. Ross. Stochastic Processes. Wiley, New York, second edition, 1996.

- [15] R. Schassberger. Warteschlangen. Springer-Verlag, Wien, 1973.

- [16] H. L. Seal. Risk theory and the single server queue. Mitteilungen der Vereinigung schweizerischer Versicherungsmathematiker, 72:171–178, 1972.

- [17] Q. Tang and G. Tsitsiashvili. Precise estimates for the ruin probability in finite horizon in a discrete-time model with heavy-tailed insurance and financial risks. Stochastic Processes and their Applications, 108:299–325, 2003.

- [18] E. C. Titchmarsh. Theory of Functions. Oxford University Press, London, second edition, 1968.

- [19] W. Vervaat. On a stochastic difference equation and a representation of non-negative infinitely divisible random variables. Advances in Applied Probability, 11(4):750–783, December 1979.

- [20] M. Vlasiou. A non-increasing Lindley-type equation. Technical Report 2005-015, Eurandom, Eindhoven, The Netherlands, 2005. Available at http://www.eurandom.nl.

- [21] M. Vlasiou and I. J. B. F. Adan. An alternating service problem. Probability in the Engineering and Informational Sciences, 19(4):409–426, October 2005.

- [22] M. Vlasiou and I. J. B. F. Adan. Exact solution to a Lindley-type equation on a bounded support. Operations Research Letters, 35(1):105–113, January 2007.

- [23] M. Vlasiou, I. J. B. F. Adan, and J. Wessels. A Lindley-type equation arising from a carousel problem. Journal of Applied Probability, 41(4):1171–1181, December 2004.

- [24] W. Whitt. Queues with service times and interarrival times depending linearly and randomly upon waiting times. Queueing Systems, 6(4):335–351, 1990.