Best prediction under a nested error model with log transformation111Supported by the Spanish grants SEJ2007-64500, MTM2012-37077-C02-01, MTM-2012-33740 and ECO-2011-25706. Part of this work was done during a research stay of the second author in the Institute of Statistics of the University of Neuchâtel.

Key words: Empirical best estimator; Mean squared error; Parametric bootstrap.

MSC 2000: primary 62D05; secondary 62G09.

Abstract: In regression models involving economic variables such as income, log transformation is typically taken to achieve approximate normality and stabilize the variance. However, often the interest is predicting individual values or means of the variable in the original scale. Back transformation of predicted values introduces a non-negligible bias. Moreover, assessing the uncertainty of the actual predictor is not straightforward. In this paper, a nested error model for the log transformation of the target variable is considered. Nested error models are widely used for estimation of means in subpopulations with small sample sizes (small areas), by linking all the areas through common parameters. These common parameters are estimated using the overall set of sample data, which leads to much more efficient small area estimators. Analytical expressions for the best predictors of individual values of the original variable and of small area means are obtained under the nested error model with log transformation of the target variable. Empirical best predictors are defined by estimating the unknown model parameters in the best predictors. Exact mean squared errors of the best predictors and second order approximations to the mean squared errors of the empirical best predictors are derived. Mean squared error estimators that are second order correct are also obtained. An example with Mexican data on living conditions illustrates the procedures.

1 Introduction

In Econometric regression models, variables such as income or expenditure are often transformed with logarithm to achieve homoscedastic errors with approximately normal distribution. However, the variable of interest remains to be the untransformed one. Target characteristics of the study variable such as the values for out-of-sample individuals or the means for specific subpopulations become then functions of the exponentials of the dependent variable in the model. However, the predictors obtained by transforming back the individual predicted values are biased. Usual bias-corrections are only approximations and optimality properties are lost. However, the exact expression for the optimal predictors can be obtained analytically for certain models. A model that is often used for small area estimation is the nested-error linear regression model proposed by Battesse, Harter and Fuller (1988) to estimate the area under production of corn and soybeans in a number of counties. In small area estimation, the lack of sample observations in some of the areas of interest is solved by linking all areas through the common regression parameters but including at the same time random area effects that represent the unexplained between area variation. The common parameters are estimated using the sample observations from all the areas together and this leads to great efficiency gains with respect to estimators that use only the area-specific sample data (direct estimators). This kind of model is used in Econometric applications as well, see e.g. Elbers, Lanjouw and Lanjouw (2003) or Molina and Rao (2010), who employed this model to estimate poverty indicators in small areas. For more details on small area estimation methods, see the monograph by Rao and Molina (2015) and the recent review by Pfeffermann (2013).

Assessing the reliability, or uncertainty, of the obtained predictors is crucial in practical applications. A popular uncertainty measure is the mean squared error (MSE), also called mean squared prediction error. MSEs of optimal predictors of small area parameters have been obtained under certain models but only for simple parameters, see e.g. Das, Jiang and Rao (2004). The MSE of an individual prediction under a nested-error model with log-transformation that is second-order correct has not been obtained yet. Moreover, when predicting the mean of the original variable in a given area, the optimal predictor is function of the predicted values for the out-of-sample individuals from that area. Since the individuals belong to the same area, due to the presence of the area effects, individual predictors are not independent. Then mean crossed product errors (MCPEs) between pairs of individual predictions are needed to derive the MSE of the predictor of the mean in that area.

Here we obtain optimal predictors for individual values of the target variable in out-of-sample units and also for small area means. Additionally, second-order asymptotic approximations for the MCPEs of pairs of individual predictions are derived, which lead to good approximations for the MSEs of predicted area means. In the small area estimation literature, this was done previously only under area-level models by Slud and Maiti (2006). Under a unit-level model, Molina (2009) dealt with estimation of exponentials of mixed effects, i.e. exponentials of linear functions of the fixed and the random effects in the model; the individual values of the original variable cannot be expressed as special cases of these parameters. Thus, the target parameters and not the same and consequently results are also different. In particular, certain crossed-product terms appearing in the MCPE that are of lower order in Molina (2009), are not negligible when predicting individual observations. In fact, those crossed-product terms are typically neglected in small area estimation applications. Here we show that these terms cannot be neglected and give their analytical expression up to terms, where is the number of areas.

Analytical approximations for the uncertainty measures have a complex shape and users might prefer to use resampling procedures such as bootstrap methods. González-Manteiga et al. (2008) proposed a parametric bootstrap method designed for finite populations under a nested error model that is suitable in this paper. However, González-Manteiga et al. (2008) proved consistency of the bootstrap MSE estimator when the target parameters are linear. For our particular non-linear parameters, consistency remains to be proved. Nevertheless, once an analytical asymptotic expression is available for the true MSE, the technique of imitation used in that paper can be followed to achieve the consistency in this paper. Thus, the theoretical results for the MSE approximation that are obtained in this paper lead automatically to the consistency of the corresponding bootstrap MSE estimators.

The paper is organized as follows. The considered model and the target quantities are introduced in Section 2. This section also gives the best predictor and first and second-stage empirical best predictors of the target quantities. Section 3 describes usual likelihood-based fitting methods. MCPEs and MSEs of first-stage empirical best predictors are obtained in Section 4, and for second-stage empirical best predictors, second-order approximations to the analogous uncertainty measures are given in Section 5. Second-order unbiased estimators of these uncertainty measures are provided in Section 6. Section 7 describes a parametric bootstrap procedure for estimation of the uncertainty. Section 8 describes the result of a simulation experiment comparing the proposed predictor with existing ones. Section 9 illustrates the procedures through the estimation of mean income in municipalities from Mexico. Finally, the proofs of all the theorems are included in the Appendix.

2 Model, target quantities and predictors

When estimating characteristics of subpopulations that have varying sizes, it seems convenient to work under a finite population setup. Here we consider that the population is finite and contains units. This population is partitioned into subpopulations , also called areas or domains, of sizes . The data is obtained from a sample of size drawn from the population . We denote by the subsample from domain , of (fixed) size , , with , and by the sample complement from area , of size , .

The goal is to predict the value of the variable of interest for an out-of-sample individual within area , or the area mean , based on a regression model for . If represents a measurement of an economical variable such as income or expenditure, it is customary to consider the logarithm of as dependent variable in a regression model. Moreover, in many applications, the available auxiliary variables do not explain sufficiently well all the between-area variation that data exhibit. Then, random area effects representing this unexplained variation are included in the model. This is typically done in small area estimation applications. Here we assume the following linear regression model with random area effects, also known as nested-error model, for the log-transformed variables ,

| (1) |

Here, is a vector containing the values of explanatory variables for -th individual in -th area, is the vector of unknown regression coefficients, is the individual error, is the random effect of area , with random effects and errors assumed to be independent, and finally and are the unknown random effects and individual error variances respectively, called variance components. We denote by the vector of variance components and by the space where these parameters lie. Notation and will refer hereafter to generic elements from and , whereas and will be the respective true values of and , where is supposed to be within the interior of . For a quantity depending on and/or , we will use many times the notation , omitting the explicit dependence on and/or .

If we intend to estimate the mean of an area with a poor sample size , the estimators that use only the area-specific observations, called direct estimators, are highly inefficient. Model (1) links all the areas through the common parameters , and , which allows us to “borrow strength” from all the areas when estimating a particular area mean. However, even though the model is assumed for , the target parameter remains to be the area mean of the untransformed variables, which can be expressed in terms of the dependent variables in the model as

Here we intend to estimate single values of the target variable in out-of-sample units and area means , when the variables in the population units follow model (1). These target quantities are special cases of a general parameter of the form , where is a measurable function and is the vector of outcomes for domain . Defining also and , the model reads

| (2) |

where is a -vector of zeros, is a -vector of ones and is the identity matrix. The covariance matrix of is equal to . Let us arrange the elements from domain into sample and out-of-sample elements, as

The “best predictor” of a general parameter is the function of the sample data with minimum mean squared error and is given by , where the expectation is taken with respect to the distribution of . The best predictor is exactly unbiased in the sense . Since by (2) we have , the desired conditional distribution is

| (3) |

with mean vector and covariance matrix given by

Under the nested-error model (1), they reduce to

| (4) | ||||

| (5) |

where , and .

Based on the conditional distribution (3) with mean vector given in (4) and covariance matrix (5), the next theorem gives closed-form expressions for the best predictors of and .

Theorem 1.

Under the nested-error model with log-transformation (1), it holds:

-

(i)

The best predictor of , for , is given by

(6) where and .

-

(ii)

The best predictor of is given by

(7)

Remark 1.

In contrast with the case of estimation of a small area mean under a nested error model without log-transformation, the best predictor of the small area mean given in (7) requires the values of the auxiliary variables for each out-of-sample unit and not only of area totals or means of the auxiliary variables. Censuses of potentially useful auxiliary variables are available for practically all European countries and many other countries all over the world.

Molina (2009) proposed the bias-corrected predictor , where , which is similar to the best predictor given in (6). However, they are not exactly the same because the target parameters in Molina (2009) are of the type , which differ from our target parameters here given by the individual observations . Nevertheless, it is interesting to study how Molina (2009)’s predictor performs for . The next result gives the relative bias of and of the naive predictor obtained by back-transforming the predicted model responses, . By this result, these two predictors are negatively biased unlike the best predictor given in (6) and .

Proposition 1.

Under model (1), it holds:

-

(i)

;

-

(ii)

.

The best predictors and depend on the true values of and , which are unknown in practice. Next we define first and second-stage empirical best (EB) predictors obtained by estimating these unknown parameters in two stages. First, define the following vectors and matrices containing the sample elements from all the areas

Then, the model for the sample units can be written as

and the covariance matrix of is given by

The first-stage EB predictor is obtained under the assumption that is known but is unknown. The maximum likelihood (ML) estimator of under normality, which is also the weighted least squares (WLS) estimator of without normality reads

| (8) |

The first-stage EB predictors of and are then

| (9) |

The next result gives asymptotic unbiasedness of at the log scale.

3 Fitting methods

A typical estimation method is maximum likelihood (ML), which provides consistent and asymptotically efficient estimators of the variance components (Miller, 1973). The ML estimator of maximizes the penalized log-likelihood, given by

| (11) |

where denotes a generic constant. The score vector is defined as . In terms of the vector , the elements of the score vector are given by

| (12) |

where , that is, and . The ML estimator of is then obtained solving the equation system together with equation (8) for . Since equations are non-linear, numerical algorithms such as Newton-Raphson or Fisher-Scoring are typically applied. These algorithms require respectively the elements of Hessian matrix or the Fisher information matrix. The Hessian matrix is defined as , where

Finally, the Fisher information matrix is , where

A drawback of ML estimator of is that is does not account for the degrees of freedom due to estimation of . Restricted ML (REML) corrects for this problem, providing estimators with bias of lower order. This is achieved by transforming the data as , where is any matrix with rank and satisfying . The REML estimator is the value of maximizing the so called restricted log-likelihood , which is the logarithm of the joint density function of the transformed data . Noting that (Searle et al. 1992, p.451), this function can be written as

| (13) |

The score vector obtained from is . Using again the relation , the elements of can be expressed as

| (14) |

The Hessian matrix obtained from is , where

Finally, the corresponding Fisher information matrix is in this case given by , with elements

4 Uncertainty of first-stage EB predictors

The reliability of a point predictor is typically assessed by its MSE. When estimating a small area mean , in virtue of (7), the MSE of a predictor can be directly obtained as a function of the MCPEs of pairs of predictors and for out-of-sample units . For this reason, in the following we focus on giving the expressions for the MCPEs of pairs of individual predictors.

Theorem 2 spells out the MCPE of the best predictors and for out-of-sample units , defined by . The mean squared error (MSE) of the best predictor of a single out-of-sample observation , is then obtained taking . For the area mean , the MSE of the best predictor is given in Corollary 1. Let be equal to 1 if and 0 otherwise, and

Theorem 2.

Under the nested-error model with log-transformation (1), the mean crossed product error of the best predictors and of and , for , is given by

Corollary 1.

The mean squared error of the best predictor of is given by

For a pair of first-stage EB predictors obtained by estimating using the WLS estimator given in (8) but assuming that is known, Theorem 3 gives the MCPE. The MSE of a single first-stage EB predictor is obtained setting . The following notation is required:

Theorem 3.

Under the nested-error model with log-transformation (1), the mean crossed product error of the first-stage EB predictors and , for , is given by

| (15) | |||

5 Uncertainty of second-stage EB predictors

In practice, the vector of variance components is also unknown. Estimation of to obtain second-stage EB predictors entails an increase in uncertainty and this increase should be accounted for in the MCPE. The additional uncertainty depends on the estimation method used for . This section gives an approximation up to terms for the MCPE of pairs of individual second-stage EB predictors when model parameters are estimated by ML or REML.

For the second-stage EB predictors and of and , for , the MCPE can be decomposed as

| (16) | |||

The first term on the right-hand side of (16) is already given in Theorem 3 above. The remaining terms will be approximated up to terms under the following assumptions, where denotes the minimum eigenvalue of :

-

(H1)

, and ;

-

(H2)

The elements of the matrix are uniformly bounded as ;

-

(H3)

;

-

(H4)

.

Theorem 4 gives an approximation for the second term on the right-hand side of (16). This result uses the additional notation

Theorem 4.

Let be the second-stage EB predictor of , with denoting either ML or REML estimator of under the nested-error model with log-transformation (1). If assumptions (H1)-(H4) hold, then

Theorem 5 gives a second-order unbiased approximation for the first of the crossed product terms in (16); the last term is analogous. For this theorem, we need to introduce additional notation. We define

| (17) |

We also define , , with , with ,

for with , , , with , , and , with , , and

Finally, we define

| (18) |

Theorem 5.

Let be the second-stage EB predictor of under the nested-error model with log-transformation (1), with denoting either ML or REML estimator of . If assumptions (H1)-(H4) hold, then for , we have

If is the REML estimator, set in .

Finally, Theorem 6 gives a second-order approximation to the MCPE of and , as a direct consequence of decomposition (16) and Theorems 3, 4 and 5.

Theorem 6.

Let be the second-stage EB predictor of under the nested-error model with log-transformation (1), with denoting either ML or REML estimator of . Under assumptions (H1)-(H4), it holds

The following corollary gives a second-order approximation to the MSE of the second-stage EB predictor of the area mean .

Corollary 2.

An approximation to the MSE of is obtained noting that

| (19) |

and applying Theorem 6 to obtain second-order approximations of and of by setting . In fact, going through all the proofs, it can be seen that the remainder term in Theorem 6 is uniformly for all and ; in other words,

where . This implies that the resulting approximation to the MSE of is also .

6 Estimation of the uncertainty

The following theorem states that replacing the unknown parameters and by their corresponding ML estimators and in leads to a bias. It also gives a second-order approximation for that bias, which can then be corrected. The proof follows closely that of Theorem 4 in Molina (2009).

Theorem 7.

Let denote either ML or REML estimator of under the nested-error model with log-transformation (1) and . If assumptions (H1)-(H4) hold, then

where

If is the REML estimator, because .

It is not difficult to see that plugging the ML estimators and for the true values and in the above bias correction terms leads to negligible bias in the sense

| (20) |

The same occurs for REML estimators of and . According to Theorem 7 and equation (20), an unbiased estimator of up to terms is given by

| (21) |

Moreover, by Molina (2009), it holds that

| (22) |

So far we have obtained unbiased estimators up to terms of the first two terms on the right-hand side of (16). Thus, in order to have an unbiased estimator of (16) of the same order, it only remains to estimate unbiasedly . The next theorem states that plugging the ML estimators and in yields an unbiased estimator of the desired order.

Theorem 8.

Let denote either ML or REML estimator of under the nested-error model with log-transformation (1) and . If assumptions (H1)-(H4) hold, then

7 Bootstrap estimation of the uncertainty

Resampling methods are very popular among practitioners due to their conceptual simplicity, which also makes them less prone to coding errors. Under the setup of this paper, the naive bootstrap procedure for finite populations proposed by González-Manteiga et al. (2008) can be applied for the estimation of the MSE of either an individual predictor or for the predicted area mean . It can also be applied to estimate the MCPE of two individual predictors and , with . Here we describe only the steps of the bootstrap procedure for estimation of the MSE of , because for the other cases is analogous.

-

1)

With the available data coming from the sample , calculate the ML estimators of the model parameters and .

-

2)

Generate bootstrap random effects , .

-

3)

Generate bootstrap errors , , .

-

4)

Generate a bootstrap population of response variables from the fitted model

(23) Let be the true mean of area in this bootstrap population.

-

5)

Let be the vector with the bootstrap elements whose subscripts are in the original sample , . Using the bootstrap sample data and , fit the bootstrap model (23), obtaining new model parameter estimators and . Calculate the bootstrap second-stage EB predictor

for and , where and .

-

6)

The bootstrap MSE of is then

(24) where indicates expectation with respect to the probability distribution induced by model (23) given the original sample data .

In practice, (24) is approximated by Monte Carlo, by repeating Steps 2)–5) a large number of times , and then averaging over the replicates. Let be the true parameter in -th replicate and be the corresponding second-stage EB predictor. The Monte Carlo approximation of (24), used here as an estimator of , is given by

| (25) |

González-Manteiga et al. (2008) proved the consistency of the bootstrap MSE of the second-stage EB predictor of a linear parameter by the technique of imitation. With the available analytical formula for the MCPE given in Theorem 6, here the result is analogous. First, by imitating the proofs of Theorems 3, 4 and 5 under the bootstrap population given the original sample data, the bootstrap MCPE can be approximated as

| (26) |

where

Since ML estimates are consistent and is a continuous function of , then is also consistent for . However, due to the presence of the bias terms listed in Theorem 7, is only first-order and not second-order unbiased for the true , that is,

For bias corrections of the naive bootstrap estimator (25) to achieve a bias in the case of linear parameters, see e.g. Butar and Lahiri (2003) and Pfeffermann and Tiller (2005). For a bias correction based on double bootstrap, see Hall and Maiti (2006a). These corrections can be directly extended to estimate our specific non-linear parameters or . These bias corrections might yield negative MSE estimates. Hall and Maiti (2006b) proposed a positive bias-corrected MSE estimate through double bootstrap, but the second-order unbiasedness property is lost. Thus, ensuring positive MSE estimate and second-order unbiased is still a challenge.

8 Simulation experiment

We carried out a simulation experiment to compare, in terms of bias and MSE under the simple mean model , the following estimators of the area means : (i) the second-stage EB predictor ; (ii) the naive predictor , where ; Molina (2009)’s predictor , for , with ; (iii) direct estimator and (iv) the estimator obtained assuming the area-level model of Fay and Herriot (1979), , where are assumed iid with , , and are independent with and , with assumed to be known and fixed to the sampling variance of the direct estimator , . We will also analyze the contribution of each term of .

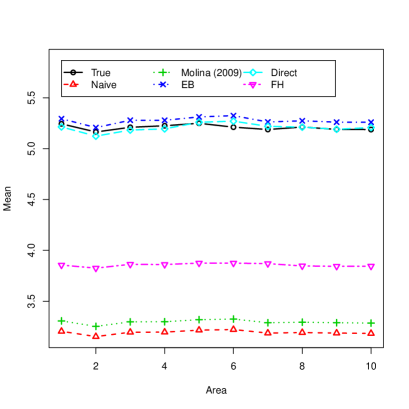

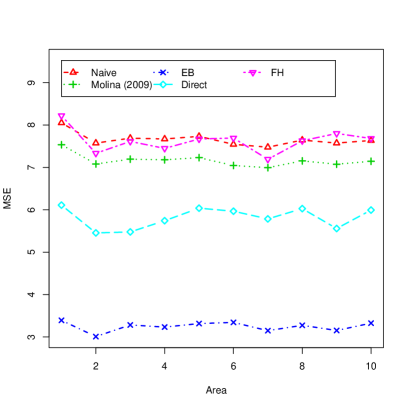

We consider a limited number of areas, , in order to analyze the small sample properties of the estimators. Population sizes of the areas are taken as , , which gives a total population size of . Model parameters are taken as , and , leading to a variance fraction . A total of Monte Carlo (MC) populations were generated from the mentioned mean model. In each MC simulation replicate, simple random samples without replacement of size were drawn independently from each area , making a total sample size of . In this case, by Proposition 1, the actual relative bias of the naive predictor amounts to . For Molina (2009)’s predictor, it is . Let us now look at the actual biases and MSEs of each type of estimator of , . Figure 1 (left) plots the MC means of the true values and of the estimators (i)–(iv) and the MSEs (right). This figure illustrates how the naive and Molina (2009)´s predictors are both considerably biased low and also how the EB predictor proposed in this paper has a negligible bias together with a substantially smaller MSE than all other estimators.

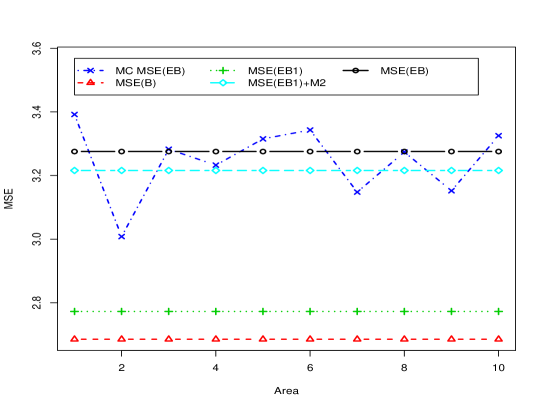

Next we analyze the contribution of each MSE term to the total in this simulation experiment. Figure 2 displays the MC approximation to labelled “MC MSE(EB)”, given in Corollary 1 labelled “MSE(B)”, given in Theorem 3 labelled “MSE(EB1)”, the same but adding the crossed-product terms given in Theorem 4, and finally the analytical approximation to obtained from Theorem 6 and Corollary 2 that includes the terms . We can clearly see that in this simulation experiment, the naive MSE estimators or underestimate the true MSE to a great extent, and the additional MSE terms of Theorems 4 and 6 seem to be necessary to avoid undesired underestimation of the MSE.

9 Estimation of mean income in municipalities from Mexico

In this section we apply the obtained results to the estimation of mean income in municipalities of the State of Mexico. Data comes from two different sources. One is the Module of Socio-economic Conditions (MCS in Spanish) from the 2010 Mexican National Survey on Income and Expense of Households (ENIGH in Spanish). The MCS collects microdata on income, health, nutrition, education, social security, quality of household, basic equipment and social cohesion in Mexico. We also have available micro data from the Census of the same year. The Census contains several of the variables also contained in the MCS, but the income variable used officially (monthly total per capita income) is collected only in the mentioned survey. Based on both data sources, we estimate mean income in each municipality that appears in the MCS survey data (many of them are not sampled by the MCS), except for one which, after a preliminary study of the considered variables, turned out to be very different from the other municipalities (outlier). This makes a total of municipalities. From these, the minimum sample size is 8 and the maximum is 2037, with a median of 96 and an average of 185.

After a preliminary check of the relationships between income and the available variables in the MCS, we selected as auxiliary variables age, , , the indicators of gender, indigenous population, activity sectors (including unemployed and inactive), composition of household, quality of dwelling, indicator of receiving social benefits, classification according to the available equipment, years of schooling, indicator of rural/urban area and the interactions between quality of dwelling with rural/urban area and of composition of household with gender. Since income distribution in Mexico is highly skewed, the model was fitted to where was selected to achieve an approximately symmetric distribution of model residuals. The Supplementary material shows the histograms of income before and after the transformation. It shows also the resulting fitted regression parameters. The fitted variance components are and , which lead to an average contribution of to the total variance of .

We computed also direct Horvitz-Thompson estimators of mean income together with their sampling variances, obtained as

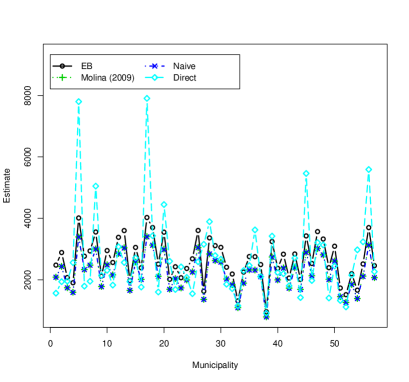

where is the inclusion probability of -th unit in the sample from municipality . The sampling variance is obtained using the following approximation for the second-order inclusion probabilities , , and noting that for all . Figure LABEL:Estimates shows EB, direct, Molina (2009) and naive estimators of mean income for the municipalities. This figure illustrates that direct estimators are somewhat unstable. According to Proposition 1, Molina (2009) and naive estimators have an average estimated relative bias of -14.77% and -14.92% respectively. In this application, both take very similar values (superposed in the plot) and their values are lower than those of EB estimators, which could be due to the mentioned theoretical bias.

Finally, boxplots of the estimated coefficients of variation (CVs) defined for any estimator as are shown in Figure 3. These boxplots show the significant reduction in CV obtained when using EB estimators instead of the default direct estimators.

APPENDIX: PROOFS

In this appendix, the Euclidean norm of a vector is denoted by . For a matrix , we consider the norms and , where denotes the maximum eigenvalue of . Asymptotic orders refer to .

PROOF OF PROPOSITION 1

The naive predictor of can be expressed in terms of the best predictor as . Now since the best predictor is unbiased, that is, , we have . The relative bias (RB) of is then . Similarly, Molina (2009) predictor can be expressed as . Taking expected value, we get . Thus, .

The next lemma is required in the proofs of several of the remaining results.

Lemma 1.

Let be the covariance matrix of , and the ML and REML Fisher-information matrices respectively, and . It holds

-

(i)

Condition (H1) implies .

-

(ii)

.

-

(iii)

Conditions (H1) and (H3) imply .

-

(iv)

Condition (H4) implies and .

PROOF OF LEMMA 1

(i) Since is symmetric and block-diagonal with blocks equal to , , we have

Now since , we have

Then, by assumption (H1), we obtain

which implies (i).

(ii) Similarly as before, we have

But again, using the expression of , we have

which is true for all and for all . Therefore, .

(iii) By the definition of , we obtain

But by the definition of eigenvalue, we have

Using (i) and assumption (H3), we finally get

which means that .

(iv) Condition (H4) implies

which is equivalent to . Moreover, note that , where and , for and , whereas . Then,

But the diagonal elements of tend to zero. Indeed

for . Then,

Now, for the second term on the right-hand side, we have

Similarly, it is easy to see that . Therefore, it holds that as for , leading to , which in turn implies

Then, similarly as we did for above, we obtain .

PROOF OF PROPOSITION 2

First of all, note that

| (27) |

On the other hand, , where is given by

| (28) |

for the vector

| (29) |

where . Replacing , for in (28) and noting that because , we obtain . Hence, the first-stage EB predictor of can be expressed as

| (30) |

Taking expected value, we get

| (31) |

Using the definition of in (29) and in (11) and taking into account that and , it is easy to see that

| (32) |

Since with , , and , we obtain

| (33) |

Replacing (33) in (32), we finally obtain

| (34) |

for and . Replacing (34) in (31), we obtain

Finally, by Lemma 1, under (H1) and (H3), we have , and using (H2), it holds and . The result then follows by (28).

PROOF OF THEOREM 1

(i) The best predictor of is equal to . Here we calculate the more general expectation , where is a non-stochastic vector of size , . Now using the conditional distribution given in (3), this expectation is given by

| (35) |

because the integral involved is equal to 1. Now (i) follows from the

expressions for and given in (4) and (5), and taking as a vector with 1 in position and the

rest of elements equal to zero.

(ii) The best predictor of is given by

| (36) |

The result then follows by straightforward application of (i).

PROOF OF THEOREM 2

For , we need to calculate

| (37) |

Since and are independent for all , the last term on the right hand side of (37) for is given by

| (38) |

In contrast, for we have

| (39) |

Observe that the expectations appearing on the right hand side of (38) and (39) are respectively the moment generating function (m.g.f.) of the independent random variables , , and , evaluated at . Since the m.g.f. of a random variable is given by , using this expression we get

| (40) |

Now we obtain . But by model (1), we know

Then,

Noting that , for and are independent, we have

| (41) | |||

Using the m.g.f.’s evaluated at of the random variables involved in (41), using the expression of and the fact that , we get

| (42) |

Finally, we calculate . Again, by model (1), it holds

Now since

then using again the m.g.f. of evaluated at , we get

Finally, using the expression of , we get

| (43) |

The result follows by replacing (40), (42) and (43) in (37).

PROOF OF COROLLARY 1

PROOF OF THEOREM 3

The mean crossed product error of a pair of individual first-stage predictors and , for , is given by

| (44) |

The second term on the right hand side of (44) is given in (40). Concerning the first term on the right hand side of (44), see that for all , using (30), we get

where the expectation on the right hand side is the m.g.f. of the normal random vector evaluated at 1, that is,

| (45) |

Concerning the remaining expectations in (44), noting that for and using (30), we can write

Replacing now and writing , we obtain

| (46) |

Similarly as before, using the m.g.f. of the normal random vectors involved in the previous expression and rearranging the terms, we obtain

| (47) |

Replacing (40), (45) and (47) in (44), we get

| (48) | |||

PROOF OF THEOREM 4

We prove it for the case in which is the ML estimator of . For the REML estimator the proof is analogous, but in fact simpler. Following the same arguments as in the proof of Theorem 1 in Molina (2009), we obtain

| (51) |

where . Using the same ideas as in Theorem 2 in Molina (2009), we get

| (52) | |||

Note that by (29), we can express in terms of as follows

| (53) |

But by assumption (H1). Moreover, . Using Lemma 1 (ii), we get

| (54) |

Now observe that by Lemma 1 (iii), we have

Since , which has bounded norm, and , by assumptions (H1)-(H3), we have

| (55) |

From (53), (54) and (55), we have obtained

| (56) |

Note also that , since

This implies , because

By (53) and (55), we get for any ,

| (57) |

Using repeatedly (57), we obtain

and using (49), we obtain

| (58) |

Replacing (58) in (52) and then (52) in (51), we get the desired result.

PROOF OF THEOREM 5

Again, we show the result for the ML estimator of , because for REML the proof is analogous but simpler. The proof is based on the following chain of results:

-

(A)

For every , there exists a subset of the sample space on which, for large , it holds

where , , , with , , , and the remainder term satisfies , for a random variable with bounded first and second moments.

-

(B)

If is the indicator function of the set , it holds that

(59) -

(C)

.

-

(D)

It holds that

(60) -

(E)

It holds that

Applying in turn (C) and (B), we obtain

Finally, writing and applying (E) and (D), we obtain

Next we give the proofs of results (A)–(E).

Proof of (A): It is obtained by applying Lemma 3 of Molina (2009)

to , where is the ML

estimator of .

Proof of (B): Applying (A) we obtain

But by Theorem 3, we know that as tends to infinity. Then, applying Hölder’s inequality and taking , we obtain

| (61) | ||||

Proof of (C): Noting that , for and , we have

| (62) | |||

For , we define the neighborhood . Using (28) and applying Hölder’s inequality, the first expectation on the right-hand side of (62) can be bounded as

But the suprema of and over are bounded. Moreover, since is normally distributed, the expected value on the right-hand side of the inequality is bounded. Now by Lemma 1 of Molina (2009) with and , we get . Therefore,

| (63) |

Similarly, we have

| (64) | |||

Replacing (63) and (64) in (62), we obtain

.

Proof of (D): Consider the first term on the left-hand side of (60), given by

Using and taking into account that

| (65) |

we obtain

| (66) |

where , with and by (56).

To calculate the expected value in (66), note that and define

| (67) |

Then, we can write

| (68) |

Moreover, denoting , , and , the vector of scores (14) can be expressed as

| (69) |

Using these expressions, we get

Using repeatedly Lemma 5(iv) of Molina (2009), we obtain

| (70) |

For the expected value , note that , where , for . However, since , we cannot express in terms of as done above. In this case, we construct an extended vector , whose distribution is , for

where . Defining also , we can express

Expressing now and in terms of similarly as in (68) and (69) by adding zero elements to the vectors and matrices multiplying , we can apply exactly the same results as used for . The result turns out to be equal to (70) with replaced by .

The rest of terms on the left-hand side of (60) are obtained following a similar procedure, by expressing the terms within the expectations as sums of products of quadratic and linear forms in multiplied by exponentials of linear forms of and then applying repeatedly Lemma 5 of Molina (2009).

Proof of (E): Note that

| (71) |

By the definition of in (65) and that of in (30), we obtain

Now applying repeatedly Hölder’s inequality, we get

| (72) |

for , noting that by the proof of Theorem 1 in Molina (2009), it holds

| (73) |

that , by Lemma 1 in Molina (2009) with , and finally taking into account that is normally distributed and that and are bounded. By a similar reasoning, we obtain

| (74) |

By (74) and (72), we obtain . The remaining results in (E) are proved similarly.

PROOF OF THEOREM 8

Similarly as before, we spell the proof for ML, since for REML estimation the proof is analogous. For , let us define the neighborhood

By a first-order Taylor expansion of around evaluated at the ML estimates , we obtain

| (75) |

where . Taking expected value, we obtain

| (76) | |||

where we have

| (77) | |||

By Lemma 1 in Molina (2009), for every , we have , where , where ; hence, . As a consequence, we have

and since , we obtain that

| (78) |

Note also that . Then, we can write

By Lemma 1 (ii) and (iii), we know that at the true value of , and . By continuity of and on , we have

Considering the facts that and , we obtain

| (79) |

By replacing (79) and (78) in (77), the desired result is obtained if the following conditions hold:

Now write (18) as , where . Now since does not depend on and

Then, we have

Therefore,

| (80) |

We know that . Moreover, it is easy to see that the suprema over of is bounded. Finally, it is also easy but cumbersome to check that

By (80), this implies

It also holds that

| (81) |

and that

| (82) |

Relations (81) and (82) imply that

Finally, (76) and (77) lead to

which is our desired result.

References

- [1]

- [2] [] Battese, G. E., Harter, R. M. and Fuller, W. A. (1988). An Error-Components Model for Prediction of County Crop Areas Using Survey and Satellite Data. Journal of the American Statistical Association, 83, 28–36.

- [3] [] Butar, F. B. and Lahiri, P. (2003). On measures of uncertainty of empirical Bayes small-area estimators. Journal of Statistical Planning and Inference, 112, 63–76.

- [4] [] Das, K., Jiang, J. and Rao, J.N.K. (2004). Mean squared error of empirical predictor. The Annals of Statistics, 32, 814–840.

- [5] [] Elbers, C., Lanjouw, J. O. and Lanjouw, P. (2003). Micro-level estimation of poverty and inequality. Econometrica, 71, 355–364.

- [6] [] González-Manteiga, W., Lombardía, M. J., Molina, I., Morales, D. and Santamaría, L. (2008). Bootstrap mean squared error of a small-area EBLUP. Journal of Statistical Computation and Simulation, 78, 443–462.

- [7] [] Hall, P. and Maiti, T. (2006). Nonparametric estimation of mean-squared prediction error in nested-error regression models. The Annals of Statistics, 34, 1733–1750.

- [8] [] Miller, J.J. (1973). Asymptotic properties of maximum likelihood estimates in the mixed model of the analysis of variance. The Annals of Statistics, 5, 746–762.

- [9] [] Molina, I. (2009). Uncertainty under a multivariate nested-error regression model with logarithmic transformation, Journal of Multivariate Analysis, 100, 963–980.

- [10] [] Molina, I. and Rao, J.N.K. (2010). Small area estimation of poverty indicators. The Canadian Journal of Statistics, 38, 369–385.

- [11] [] Pfeffermann, D. (2013). New Important Developments in Small Area Estimation, Statistical Science, 28, 40–68.

- [12] [] Pfeffermann, D. and Tiller, R. (2005). Bootstrap approximation to prediction MSE for state-space models with estimated parameters, Journal of Time Series Analysis, 26, 893–916.

- [13] [] Rao, J. N. K. and Molina, I. (2015). Small Area Estimation, Second Edition. Hoboken, NJ: Wiley.

- [14] [] Searle, S. R., Casella, G. and McCulloch, C.E. (1992). Variance Components. New York: Wiley.

- [15] [] Slud, E. and Maiti, T. (2006). Mean-squared error estimation in transformed Fay-Herriot models, Journal of the Royal Statistical Society B, 68, 239–257.

- [16]