Option Pricing Accuracy for Estimated Heston Models

Abstract

We consider assets for which price and squared volatility are jointly driven by Heston joint stochastic differential equations (SDEs). When the parameters of these SDEs are estimated from sub-sampled data , estimation errors do impact the classical option pricing PDEs. We estimate these option pricing errors by combining numerical evaluation of estimation errors for Heston SDEs parameters with the computation of option price partial derivatives with respect to these SDEs parameters. This is achieved by solving six parabolic PDEs with adequate boundary conditions. To implement this approach, we also develop an estimator for the market price of volatility risk, and we study the sensitivity of option pricing to estimation errors affecting . We illustrate this approach by fitting Heston SDEs to 252 daily joint observations of the S&P 500 index and of its approximate volatility VIX, and by numerical applications to European options written on the S&P 500 index.

keywords:

Heston SDEs, Option pricing errors, initial boundary value problems, option price sensitivitiesPlease provide at least one JEL Classification code

1 Introduction

Option based hedging relies on accurate pricing of option contracts, generally computed after modeling the joint dynamics of the underlying asset price and squared volatility . The shortcomings of Black-Scholes models (Black and Scholes (1973)) have been well identified (see Black (1976),Melino and Turnbull (1990), Stein (1989) ), and have led to studies of a wide range of stochastic volatility models (e.g. Bates (1996), Heston (1993), Hull and White (1987), Johnson and Shanno (1987), Scott (1987), Stein and Stein (1991),Wiggins (1987)).

For option pricing, one needs to estimate the parameters of the stochastic dynamics driving and . We study here the option pricing errors due to the parameter estimation errors induced by model fitting to actual data, since these errors can indeed be sizeable for small or moderately large market data sets.

This paper focuses on computing the impact of parameter estimation errors on European option pricing, when and are driven by the classical Heston joint stochastic differential equations (SDEs). The Heston model (Heston (1993)), which has often been applied to concrete market data, does enable the numerical computation of option prices, either by Fourier inversion ( Carr and Madan (1999)) or by solving directly the well-known option pricing PDE (Achdou and

Pironneau (2005), Heston (1993)).

To fit Heston model parameters to data, we use discretized maximum likelihood parameter estimators, as developed and studied in Azencott and

Gadhyan (2009) and Azencott and

Gadhyan (2015). These estimators have explicit closed form expressions, combining sub-sampled data and . In practice volatility “data” are not directly available, and are naturally replaced by well-established estimates, such as “implied volatility” or “realized volatility”.

Volatility estimation has been intensively studied, often in combination with parameter estimation for stochastic volatility models. We refer for instance to Ait-Sahalia and Kimmel (2007) and to papers such as Andersen

et al. (2009), Atiya and Wall (2009), Bollerslev and

Zhou (2002), Broto and Ruiz (2004), Gallant and

Tauchen (1996), Genon-Catalot

et al. (1999), Jacquier

et al. (2002), Kim

et al. (1998) and Shephard (2005). Parameter estimation based on both asset and option prices data has been explored in Avellaneda

et al. (2003), Bakshi

et al. (1997), Chernov and Ghysels (2000), Duffie

et al. (2000), Fouque

et al. (2000) and Pan (2002)

See also our companion studies (see Azencott

et al. (2015b), Azencott

et al. (2015a), Ren (2014)) which analyze the impact of replacing true volatilities by realized volatilities in large classes of consistent estimators of the Heston parameters.

Heston SDEs have often been used to model actual intra-day data, even though they do not model volatility behaviour at very fine time scales. Indeed they generate log-volatility trajectories with Holder exponent close to , but (see Gatheral

et al. (2014)), for many assets and any , actual estimates of are of the order of with . This has led (see Comte

et al. (1998) and Gatheral

et al. (2014) ) to model log-volatility dynamics by stationary Ornstein-Uhlenbeck processes driven by a fractional Brownian motion with small Hurst exponent . Our study could be extended to these types of log-volatility dynamics, but at the cost of several technical complications, including a detailed accuracy analysis for model coefficients estimations. So we have deliberately restricted our paper to the simpler Heston SDEs models.

We consider generic European options on assets for which price and volatility are driven by Heston joint SDEs. The parabolic PDEs verified by option prices involve four Heston model parameters as well as the unknown market price of volatility risk. We define option price sensitivities to these five parameters through partial derivatives of the option price with respect to these parameters. We derive the five PDEs and boundary conditions satisfied by the option price sensitivities, and we outline the efficient numerical schemes we have implemented to compute these sensitivities. We present our discretized maximum likelihood estimators for SDEs parameters, as well as an estimation technique for the market price of volatility risk. We then indicate how to quantify and compute the impact of parameter estimation errors on option pricing.

Finally, we illustrate our approach by analyzing market data for options based on the S&P 500 index, using the VIX index as a proxy for the S&P 500 volatility.

2 Heston Stochastic Volatility Model

Let be the asset price at time . The squared instantaneous volatility of the returns process is defined by .

In the classical Heston model (Heston (1993)), the pair is a progressively measurable stochastic process defined on a probability space , endowed with an increasing filtration , and is driven by the following system of SDEs under the market measure ,

| (1) | |||||

| (2) |

Here and are standard Brownian motions on , adapted to the filtration , and have constant instantaneous correlation , so that . The parameter vector is required to verify the well-known constraints

| (3) |

where the last inequality ensures the almost sure positivity of as soon as . There are no constraints on the drift parameter , which as is well known does not appear at all in option pricing equations. is the “mean reverting” process studied by Feller (Feller (1951)) and originally used in (Cox et al. (1985)) to model short-term interest rates. In practice is unknown and has to be estimated from market data, which are usually sub-sampled at successive times starting with , for some fixed and positive integer . Moreover while the stock price is directly observable in the market, the squared volatility is not directly available and has to be estimated, generally by “realized volatility” or by “implied volatility”. From a theoretical point of view, our companion studies (see Azencott et al. (2015b), Azencott et al. (2015a), Ren (2014)) provide an accuracy analysis for the approximation by realized volatilities.

2.1 Option pricing PDE

A European call option based on an asset is a contract signed at time , which fixes a strike or exercise price and a maturity time or exercise date . At maturity time, the option holder has the option to buy at price , from the option writer, one share of asset .

Call the price of asset at time . The pay-off of the option at maturity time is then given by where the pay-off function is defined for by

We systematically assume that the price and the squared volatility of are driven by the joint Heston SDEs (1) (2) with coefficients verifying (3). European call option prices based on asset verify then a well-known parabolic PDE associated to the elliptic second order differential operator defined for by

| (4) |

The coefficients of involve the known risk free rate of return , and the four unknown parameters of the Heston SDEs. Note that the drift parameter of these SDEs does not appear in .

As in Heston (1993) and Ikonen and

Toivanen (2004), the classical coefficient

of in involves the market price of volatility risk , which, as in Heston’s classical presentation, is here taken to be a deterministic constant, which theoretically remains the same for all European call options based on the fixed asset (see Björk (2009)).

The emergence of in and the associated option pricing PDE is due to the fact that the squared volatility is typically a non tradable asset (see Björk (2009) ). Several empirical studies have shown that cannot be neglected ( Bakshi and Kapadia (2003), Bollerslev

et al. (2011), Buraschi and

Jackwerth (2001), Carr and Wu (2009), Eraker (2008), Fouque

et al. (2000), Lamoureux and

Lastrapes (1993)). Since our numerical applications below involve only short term options, we have safely assumed, as in Fouque

et al. (2000), that the unknown market price of risk is a constant which does not depend on time. Since is unknown, we do estimate from market data, as outlined in section 7 below.

As is well known (see Heston (1993)), the option price is of the form

where is of class 2 in and class 1 in , and is the unique solution of the parabolic PDE

| (5) |

verifying on the boundary of the following boundary conditions

| (6) | |||||

| (7) | |||||

| (8) | |||||

| (9) | |||||

| (10) |

The first condition asserts that at maturity time, the option price is equal to the option pay-off. The second condition states that when the asset price , the option price must also be . The third condition is the formal limit, as , of the PDE (5). Indeed note that, as , the elliptic operator does degenerate into the first order differential operator .

The fourth and fifth boundary conditions require the option price to be approximately linear in the asset price for large , and to be roughly independent of the squared volatility for large .

Four of the boundary conditions are standard, namely the initial value (6), the Dirichlet condition (7), and the two Neumann boundary conditions (9) and (10). But the boundary condition (8) at is of a more general type (see Glowinski (2003)).

2.2 Option price as a function of the Heston SDE parameters

The coefficients of the elliptic operator are explicitly determined by the parameter vector . Due to the specificity of the 3rd boundary condition in (6) - (10) and to the degenerescence of the elliptic operator on the boundary , classical generic results on parabolic PDEs (see Singler (2008), Yu

et al. (2003)) do not directly imply the differentiability of with respect to the vector . To prove differentiability of with respect to , we now naturally use the Heston closed formulas for .

The option price is actually a function of . For fixed, Heston showed that one can write as a linear combination of two inverse Fourier transforms

| (11) |

where and are explicit complex valued functions of and (see Heston (1993)). Heston’s formulas for and involve sums of complex values rational fractions in and of square roots of similar complex valued rational fractions.

The option price can be computed by numerical implementation of equation (11) because the two integrals in do converge fast enough as

. But in this paper, we are specifically focused on quantifying option price sensitivities to estimation errors on the parameter vector , a goal which requires computing the gradient of with respect to , denoted by

| (12) |

Formally, equation (11) yields the formula

| (13) |

The gradients and can be computed explicitly and this yields 10 quite cumbersome formulas for the 5 partial derivatives of and those of . Each such formula is a function of involving compositions of exponentials, square roots, products, and sums of complex valued rational fractions.

We have checked the absolute convergence of the 10 integrals in involved in equation (13), in particular by verifying that the modulus of their 10 integrands is for large necessarily inferior to for some positive and determined by . These extensive but tedious verifications have led us in fine to the validation of formula (13).

On the practical level, the full reliability of these formulas is slightly impaired due to the multiple ambiguities generated by simultaneously selecting the determinations of many square roots of complex rational functions (and of their derivatives). Making sure that one chooses the proper combinations of such square roots determinations in all parameter configurations is not a standard computing task, and this point led us to avoid computing by numerical implementation of equation (13).

So for concrete numerical computations of the option price gradient with respect to the parameter vector , we have definitely preferred to derive and solve the 5 parabolic PDEs (15) verified by the 5 coordinates of . This generic approach has the merit of extending easily to parameterized pairs of driving SDEs much more general than the Heston SDEs. Moreover the 5 PDE solvers used here are essentially similar and converge reasonably fast as seen below.

3 Option price sensitivity to parameters estimation errors

3.1 Option price sensitivity : definition

In practical option pricing, the parameter vector has to be estimated from price data, approximate volatility data, and/or observed option trading prices. The unavoidable estimation errors on necessarily induce option pricing errors.

We define the five sensitivities of the option pricing function with respect to small errors affecting the parameter vector by the formulas

| (14) |

where all partial derivatives are computed at the point . These option price sensitivities are hence functions of . The numerical computation of option price sensitivities has been explored in Broadie and Kaya (2004); Chan and Joshi (2010) and we propose here an alternate approach.

3.2 Option Price Sensitivity PDEs

Differentiating equation (5) with respect to each one of the coordinates of the parameter vector , one obtains the five independent PDEs verified by the 5 coordinates of the gradient , in the open domain .

| (15) | |||||

| (16) | |||||

| (17) | |||||

| (18) | |||||

| (19) |

Each one of these five PDEs is associated to five boundary conditions. The first four of these conditions are given in compact form by the following vector equations, where is the vector of with all coordinates equal to 0,

| (20) | |||||

| (21) | |||||

| (22) | |||||

| (23) |

The fifth boundary conditions are obtained by differentiating equation (8) with respect to each one of the parameters. This yields the following boundary conditions, valid for ,

| (24) |

where is the 1st order differential operator given by

| (25) |

We now outline the numerical scheme we have implemented to solve the option price PDE and the five preceding non homogeneous PDEs.

4 Numerical computation of option price sensitivities to parametric errors

In concrete numerical option pricing, the asset price and the squared volatility have obvious explicit realistic upper bounds , so it is standard computing practice to replace the unbounded domain by the bounded domain where are fixed large positive numbers.

Then will be computed as the unique function verifying the parabolic PDE (5) for in the interior of and the following five conditions on the boundary of

| (26) | |||

| (27) | |||

| (28) | |||

| (29) | |||

| (30) |

To solve the PDE (5), we discretize the elliptic operator in (4), by standard numerical schemes well known to be stable under discretization refining. Numerical schemes for option pricing are discussed in multiple papers such as Achdou and

Pironneau (2005), Ikonen and

Toivanen (2004). For European options under the Heston model, the papers Haentjens (2013) and O’sullivan and

O’sullivan (2013) both present explicit specific numerical schemes.

We apply a uniform space-time finite difference grid on the domain using the second order space discretization outlined in Ikonen and

Toivanen (2004) and the backward differentiation formula for time discretization given in Oosterlee (2003) .

Let the number of grid steps be and in the and directions respectively. Grid step sizes in each direction are denoted

At grid points, the values of are indexed as follows

4.1 Space discretization

All space partial derivatives in the parabolic PDE (5) have variable coefficients, so that in some parts of the domain the first order derivative terms may dominate the second order terms. To discretize these spatial derivatives we apply a space discretization scheme used in Ikonen and

Toivanen (2004) for American options. After discretization, becomes a matrix well studied in Ikonen and

Toivanen (2004).

Recall that M-matrices which are strictly diagonally dominant with positive diagonal elements and non-positive off diagonal elements have good stability properties (see Varga (2000), Windisch (1989)). In general is not an M-matrix but as remarked in Ikonen and

Toivanen (2004), when the time discretization of (5) has sufficiently small time steps, becomes diagonally dominant.

We apply the seven point spatial discretization scheme of Ikonen and

Toivanen (2004) to solve for the option price. We use a second order accurate finite difference scheme for the space derivatives, namely the classical central difference scheme for first order derivatives and the usual three point scheme for second order derivatives.

The corresponding finite difference operators are then

| (31) |

| (32) |

On the boundary , the derivative in the direction in (28) is evaluated by the following upwind discretization scheme (see Glowinski (2008)),

As proposed in Ikonen and Toivanen (2004), the mixed derivatives are discretized using a seven point stencil , where is given by

| (33) |

We handle the Neumann boundary conditions (29) and (30) in the same way as in Ikonen and Toivanen (2004). This space discretization leads to a semi-discrete equation,

where is an matrix and is a column vector of length . The vector of length gathers all the option price values at grid points. The vector gathers terms due to the Neumann boundary condition in the direction and does not depend on .

4.2 Time discretization

For time discretization, as in Oosterlee (2003), we use the BDF2 scheme (Backward Difference Formula), which is an implicit scheme with second order accuracy Oosterlee (2003). At time the BDF2 scheme reads,

for . The stability properties of this scheme are studied in Ikonen and Toivanen (2004) and Oosterlee (2003). At each iterate of the BDF2 scheme we require the value of the last two iterates. To obtain the 1st iterate, we use an Implicit Euler scheme Glowinski (2008) : given the initial value , we compute by

At moderate grid sizes, we have numerically verified that this choice of space-time discretization of our initial-boundary value problem gives us stable solutions for the option price. At each time step, we use an LU decomposition to solve the following system of linear equations,

| (34) |

where is the identity matrix.

Once the function has been computed on our discrete grid, we solve the sensitivity equations (15)-(19) by a numerical scheme quite similar to the scheme just described.

To evaluate the right-hand side of equations (15), we use a central difference scheme to discretize the first spatial derivatives of , a 3-point stencil similar to (32) for the second spatial derivatives of , and a 7 point stencil similar to (33) for the mixed second derivative of . The space-time discretization of the sensitivity equations is the same as above, and we can then solve these discretized equations on the same grid used to compute the option price.

We have verified empirically, by successive grid refinements, that this numerical scheme generates converging approximations for the solutions of the sensitivity equations.

5 Estimation of Parameters for Heston joint SDEs

Asset prices are directly observed, but squared volatilities are not directly observable and have to be estimated indirectly. The most common estimators of are the “implied” squared volatility derived by analysis of option prices and the “realized” squared volatility (see Andersen

et al. (2003); Barndorff-Nielsen (2002); Dacunha-Castelle and

Florens-Zmirou (1986); Garman and Klass (1980); Genon-Catalot and

Jacod (1994) for estimation of realized volatility). For our study of S&P500 daily data below, a standard approximation of is provided by a fixed multiple of the index.

In concrete contexts, the available price data are observations , where is a fixed user selected sub-sampling time, with standard values such as for daily data. The subsampled squared volatilities are not observable and are estimated by , usually computed by squaring either implied volatilities or realized volatilities.

Call the unknown parameter vector of the

Heston SDEs driving . In companion preprints (see Azencott

et al. (2015b), Azencott

et al. (2015a), Ren (2014)) we have studied how the replacement of by squared realized volatilities impacts estimation consistency for the parameter vector of the Heston SDEs. These results identify large classes of asymptotically consistent estimators of , such that the associated observable estimators of remain asymptotically consistent, provided the window length and the subsampling step are forced to depend on at specific but explicit polynomial rates. We conjecture that under adequate hypotheses, asymptotic stability results also hold for the replacement of by squared implied volatilities.

This type of asymptotic stability suggests to estimate as follows. Start with observable data ( subsampled from the asset price and from estimates of the unknown square volatility of . Concretely is computed either by squared realized volatilities or by squared implied volatilities. In Azencott and

Gadhyan (2015) we have introduced and studied at length explicit discretized maximum likelihood estimators of . Asymptotically in N, these estimators are consistent and nearly most efficient, but of course they are not directly observable since they involve the true squared volatilities . However in the explicit formulas recalled below, we then replace each by its estimate , which provides us with observable estimators of , of the form

Let us describe how the “non observable” estimator is computed from the true volatilities in Azencott and Gadhyan (2015), where it is derived by likelihood maximization after formal Euler discretization of the Heston joint SDEs. This approach leads to define the five sufficient statistics

| (35) |

These statistics almost surely verify

Our nearly maximum likelihood estimators of are then explicitly given by

| (36) |

When and with fixed and small enough, we have shown in Azencott and

Gadhyan (2015) that, with probability tending to 1, these three estimators verify all the required natural constraints (3) and converge in probability to the true parameters.

Recall that the Heston SDEs (1) - (2) involve two Brownian motions and . Once are estimated, the discretization of the SDEs (1) and (2) with time step provides natural estimates for and , for the Brownian increments and . The natural estimator of is then the empirical correlation of and , which is an explicit rational fraction involving only and .

At this point the “non observable” estimator is fully and explicitly specified in terms of .

In the preceding formulas giving and , we now replace all the by the observable , to obtain an explicit observable estimator , which is asymptotically consistent as provided is fixed and small enough. For brevity below we will often omit the subscript in since the number of observations is fixed in our data studies below.

Call the vector of parameter estimation errors. These theoretical errors are not necessarily in , because does not always have a finite second moment but any slight truncation of our estimators eliminates this difficulty in numerical applications to concrete data. The covariance matrix of provides then the -sizes of estimation errors and their correlations.

We have validated in ( Azencott and

Gadhyan (2015), Gadhyan (2010) ) that for moderately large, one can generate reasonable empirical estimates of the error covariance matrix as follows. Use the observations to compute the associated value of our vector of estimators . Then simulate a moderately large number of random diffusion trajectories of duration driven by joint Heston SDEs parameterized by . This is achieved by a standard Euler time discretization of the Heston SDEs, with very small discretization time step . The explicit estimation formulas outlined above then provide one value of the random vector for each simulated trajectory . The empirical covariance matrix of the is then a natural estimator of the covariance matrix .

6 Impact of parametric estimation errors on option pricing

To implement option pricing, we start from joint observations of the underlying asset price and squared volatility, where is a fixed known (or user selected) sub-sampling time step. As just described, we use these data to compute an estimator for the vector of Heston model coefficients.

Consider a European option based on this asset, with given strike price and maturity date . In the option pricing PDE (5), the unknown Heston model coefficients are then replaced by the estimators just computed. The option price computed by solving (5) is then affected by a (random) error . Our objective is to compute numerical bounds for this option pricing error. The option price

depends also on the underlying parameter vector and . For the moment we consider the impact of errors in the parameter vector only. The impact of estimation errors affecting will be studied separately below in section 7.

To simplify notations we often omit below the variables for and the associated variables for .

With this shorthand convention, the option pricing error is equal to the error

affecting . For large enough and small enough, the vector of estimation errors becomes arbitrarily small (see Azencott and

Gadhyan (2015)), so that one can legitimately apply a first order Taylor expansion to obtain the approximation

| (37) |

For each fixed quadruplet , parameter estimation errors have a perturbation impact on option pricing, and we quantify this impact by the -norm of . Due to equation (37), we have the approximation

| (38) |

where the gradient should be evaluated at , and denotes matrix transpose. Since is positive definite, we have for all , which implies, for all , the inequality

| (39) |

The squared -norms of estimation errors on are the diagonal terms of , so that equations (39) and (38) yield the upper bound

| (40) |

Introducing the option price sensitivities as defined in section 3.1, the last inequality becomes

| (41) |

where the individual impacts on option pricing of the estimation errors respectively affecting are defined by

| (42) |

6.1 Joint SDEs model fitting for S&P 500 and VIX

For the stock market example studied below, we fix a subsampling time and we consider that the observable data ( are subsampled from the asset price and from estimates of the unknown squared volatilities .

To illustrate how we quantify the impact of parameter estimation errors on option pricing, we study the case of two options written on the index S&P 500.

We used a dataset of joint daily observations recorded in 2006 for the S&P 500 index and its approximate annualized volatility VIX. Recall that VIX, as maintained by CBOE, estimates SPX volatility through the implied volatility of options with a 30 day maturity, and is annualized on the standard basis of 252 trading days per year (see Exchange (2003)). We consider the historical time series of and its volatility proxy as being viewed under the market measure . After fixing a conventional time interval between two successive daily observations, the daily SPX observations are denoted by where is an underlying Heston process driven by standard Heston SDEs with unknown parameter vector .

Given N joint daily data , we thus set , and we estimate the unobservable squared volatilities by where the fixed coefficient simply takes account of the fixed annualization coefficient involved in VIX.

As explained in section 5, to estimate , we then first write the explicit formulas (36) giving our consistent maximum likelihood estimators, expressed in terms of the and the ; in these formulas, we replace each by the observable estimates , and this provides us with observable asymptotically consistent estimators of .

From the data recorded in 2006, we generate the time series to which we apply our parameter estimators, as defined in equations (35) and (36). This yields the vector of estimated parameter values

| (43) |

The estimated drift is not listed since it has no impact on option pricing.

As outlined in section 5, we then fix at the estimated values just obtained to simulate 5000 trajectories of the just fitted Heston SDEs, and this enables the computation of empirical evaluations for the root mean squared errors of estimation . This easily yields the values

| (44) |

The number of joint daily observations is realistic but rather small, so that the relative errors of estimation on SDEs parameters are naturally still fairly high.

For numerical evaluations below, we consider that with reasonably high probability, the parameters belong to four intervals centered around

, and with half-widths . The product of these four intervals is then a high probability “localization box” for the true vector of unknown parameters.

7 An estimator for the market price of volatility risk

7.1 Estimation of the market price of volatility risk

To compute the option price, one first has to estimate the unknown market price of volatility risk which depends on investors preferences, liquidity concerns, risk aversion, etc. For various approaches to estimate , see for instance Björk (2009), Fouque

et al. (2000), Heston (1993), Lamoureux and

Lastrapes (1993).

In the spirit of Fouque

et al. (2000), and since in our numerical examples we consider only short term options maturing within the same short period of time, we have safely assumed that is an unknown constant, and we use a small pool of short term options to estimate as follows.

Consider benchmark options , , with strikes and maturity , written on the same underlying asset. Consider the underlying asset denoted by and its volatility are driven by SDEs (1)-(2). Call the user selected time step between observations. Then for each day , let be the closing asset price and be the average of closing bid and ask for . We will estimate the unknown constant by minimizing a distance between the predicted option price and the observed market option price across all times and all options .

Let be the solution of the option pricing PDE (5) for option . The predicted option price for day becomes

. To compare this option price predictor to the observed option price , we compute the root mean squared prediction error defined by

Let be the median price of over its lifetime. To combine option pricing accuracy across multiple options, introduce the relative size of pricing prediction errors for each . Consider any estimator of , computed from the pool of options . If takes the value , we quantify the associated prediction error by the median of relative pricing prediction errors over all benchmark options, so that

We will hence compute our estimator by minimizing the median pricing error overall , so that where is determined by

Note that our approach to estimate works just as well if we replace the median by the mean of the ; but we prefer to use the median to gain in robustness to outliers.

7.2 Numerical estimate of for options written on S&P 500

For the option pricing sensitivity results presented below, we have focused on the S&P 500 index SPX and its approximate annualized volatility VIX in the first quarter of 2007. In the previous section, we have modeled the joint process by joint Heston SDEs with sub-sampling time and parameters estimated on the basis of 252 daily observations recorded in 2006.

To estimate we have selected 16 benchmark options observed over 22 trading days. Eight of these options were maturing on Feb 17th 2007, with strike prices 1380, 1400, 1410, 1420, 1425, 1430, 1450, 1460. The other 8 options had the same strike prices but with maturity date Mar 17th 2007.

The risk free rate of return is set at . Fix any tentative value of the unknown As indicated above, for each option , we solve the pricing PDE to evaluate the mean squared difference between real and computed price over the 22 days option lifetime. We then compute the median

of the 16 relative pricing errors where is the median price of over its lifetime.

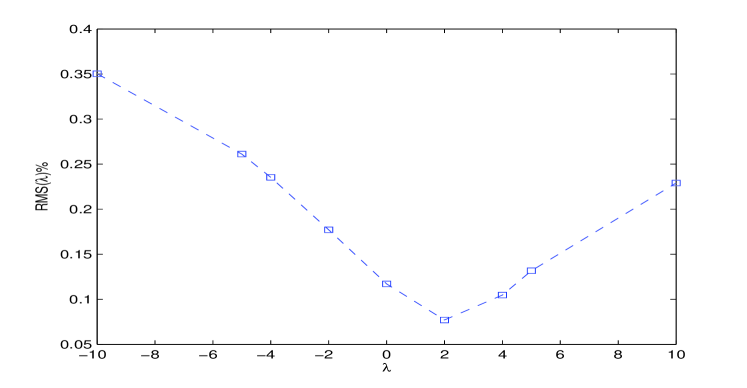

The graph of is displayed in figure 1 as a function of , which reaches a minimum of for . We thus estimate the unknown by This estimate of then enables us to compute all the of option pricing sensitivities we present for options based on S&P 500.

.

7.3 Numerical computing of option price sensitivities

We study two benchmark European options and written on the SPX index, maturing at days and days, and with identical strike price . These options were actively traded during the 1st quarter of 2007.

The time between daily observations for the underlying asset model has been conventionally set at , so in option pricing PDEs (5), the maturity must be for and for .

The risk free rate of return is set at .

As detailed in section 7 above, we assume that the market price of volatility risk is constant, and we estimate it by analysis of 16 other options written on SPX, which yields the estimate .

In the first quarter of 2007, ranged from 1370 to 1460 with median 1426, and ranged from to with median . We use these values to determine realistic domains in for the triple defined by , , , with for and for .

In these two domains, we need to solve the option pricing PDE (5) for with boundary conditions (6)-(10).

After checking numerically that for option prices are not significantly affected when the initial boundary is shifted to the position , we did implement this shift for substantial CPU reduction.

The computing domain is then

We discretize this domain by a grid of size for , and a grid of size for . As indicated in section 4, we then solve the four PDEs (15) – (18), verified by option price partial derivatives with respect to , to obtain the vector of option pricing sensitivities .

By refining the grids and , we have numerically validated that these discretizations were dense enough to accurately solve all the necessary PDEs.

Since the unknown may essentially be any point of the high probability localization box defined above in 7.3, the individual impacts on option pricing of parameter estimation errors, denoted in equation (42), are then evaluated by their upper bounds for in a large finite subgrid of .

On a standard desktop PC, solving all the option pricing and sensitivity PDEs as above required for each a CPU-time of 1 minute for option and 2 minutes for option . When the grid size increases, these CPU times are roughly linear in the grid time size and behave like low degree polynomials in the grid spatial size ; indeed, a key computational cost is the LU decomposition and backward substitution for a single matrix.

8 Impact of parameter estimation errors on option pricing

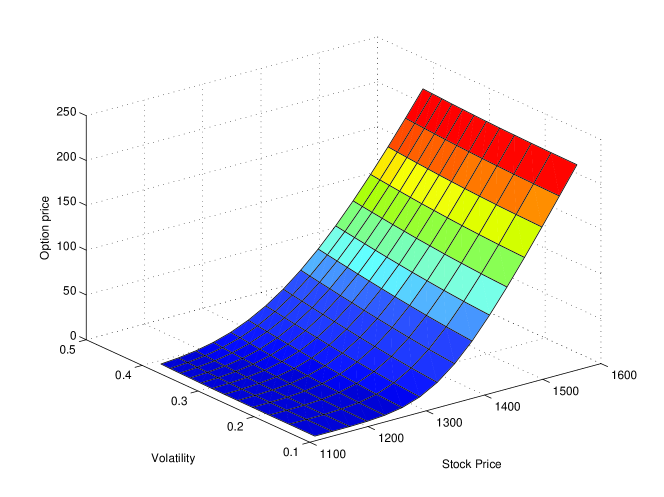

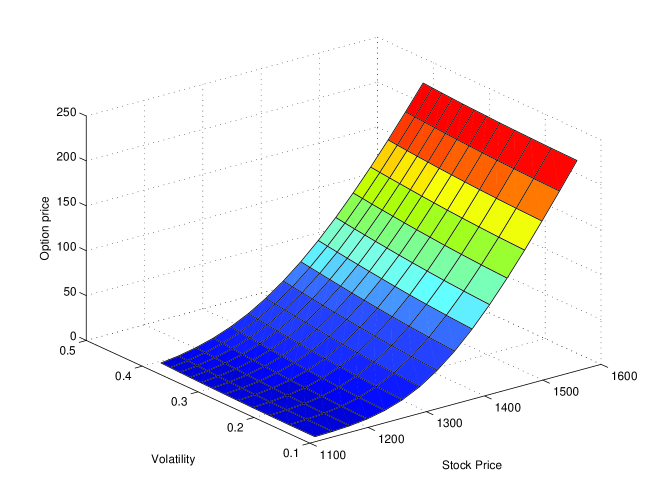

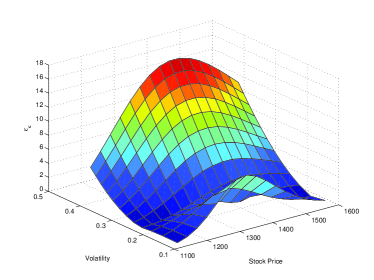

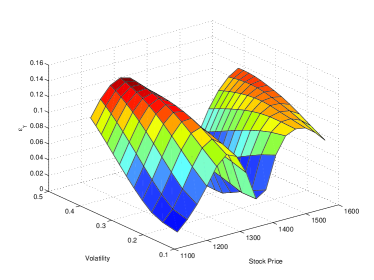

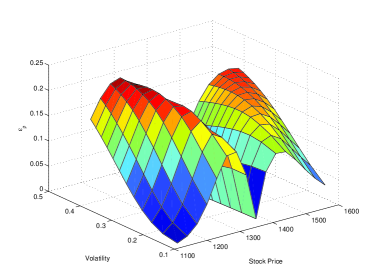

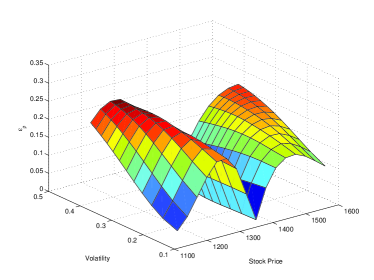

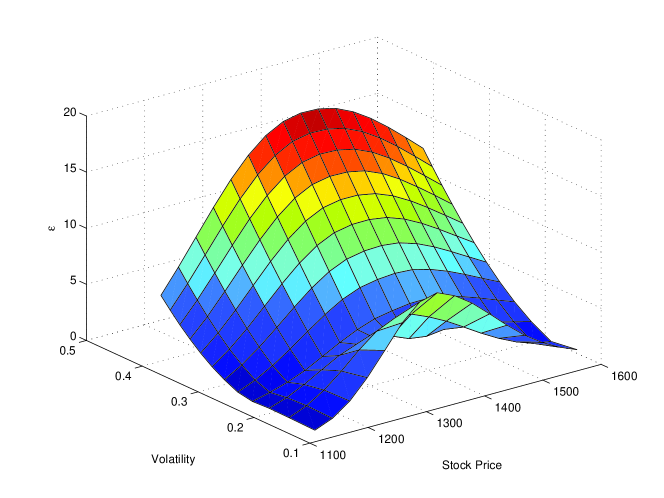

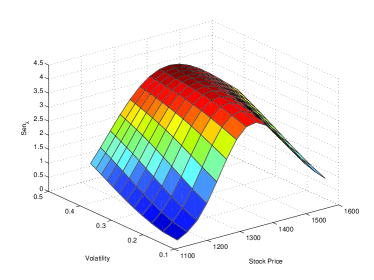

We now present numerical results for the two European options written on the SPX index, with strike price and maturities that were actually traded in 2007. The 3D-graphs in Fig. 2 display the prices of options computed at option creation time, as functions of current SPX price and VIX value with .

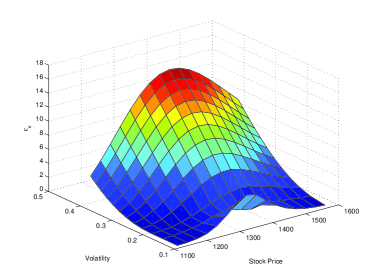

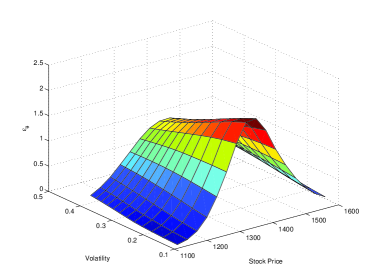

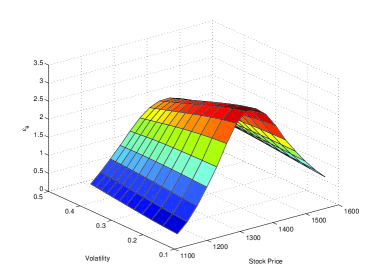

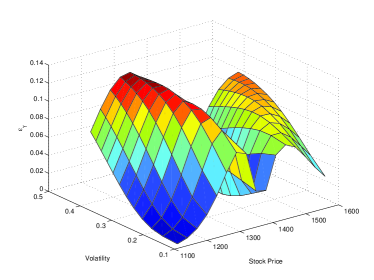

For options and , the figures Fig. 3, 4, 5, 6 display the individual impacts of parameter estimation errors on option pricing. These separate error impacts on option pricing are computed by equation (42), and are displayed in our 3D-graphs as functions of the SPX price and of its volatility, covering deep-out-of-the money cases as well as deep-in-the money cases.

Note that the estimation errors on and induce option pricing errors which tend to be decreasing functions of where and is the option strike price. Since the individual impacts of estimation errors on option price are clearly stronger for and than for and , we see that option pricing tends to be more sensitive to parameter estimation errors for options close to the money than for options far from the money.

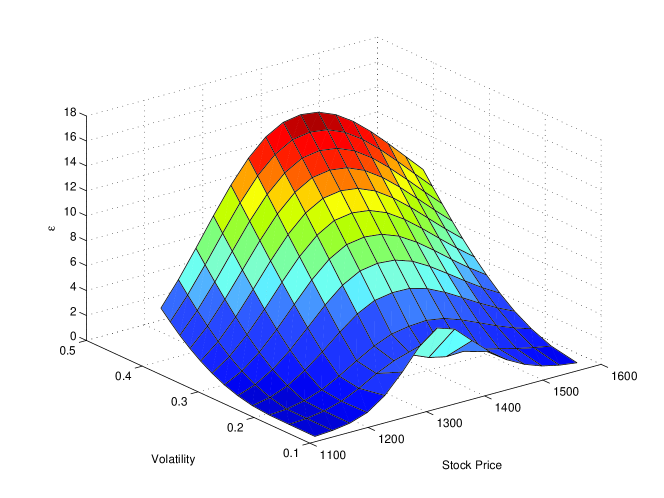

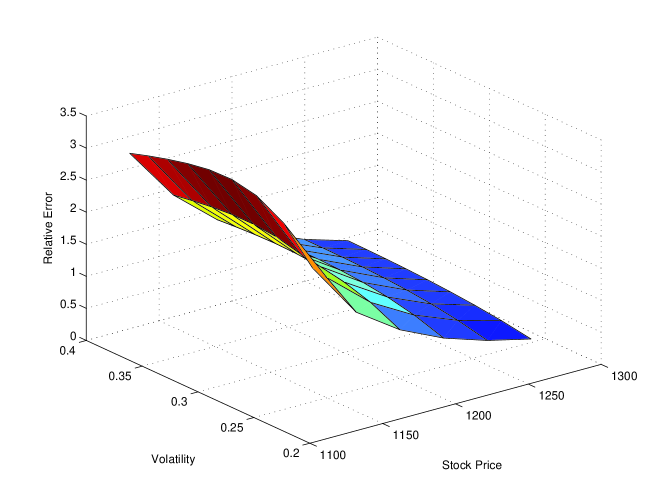

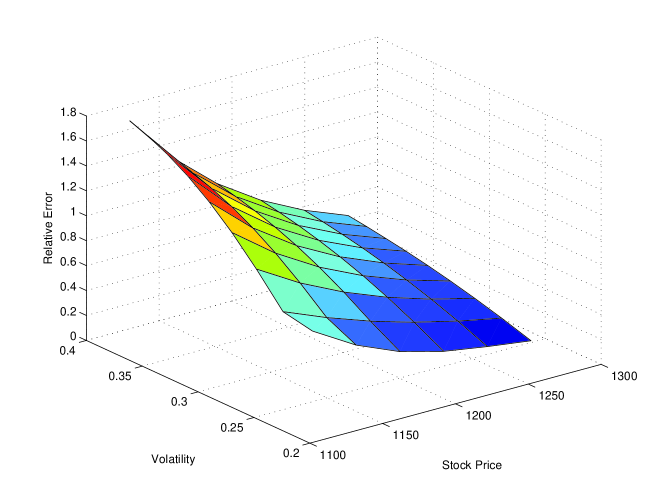

The bound on the global option pricing error induced by the combined effects of all parametric estimation errors was computed as the upper bound of the right-hand-side of equation (41) for in a large finite subgrid of the localization box and displayed in Fig. 7 and 8 as a function of current asset price and volatility.

Relative global option pricing errors are defined by and are displayed in Fig. 9 and 10 for .

8.1 Impact on option price of estimation errors in

Our estimate was derived by minimizing the median option pricing error, where the median was computed over a set of 16 benchmark options written on SPX within a short trading period. To evaluate the error of estimation affecting , we implement a rough “bootstrap” evaluation as follows. For each subset of 12 options arbitrarily selected in , one can as above compute as the median pricing accuracy over the 12 options in and then minimize in , which yields another estimate of .

The average of the shifts is a rough evaluation of the error affecting the estimate . This procedure provides here the value .

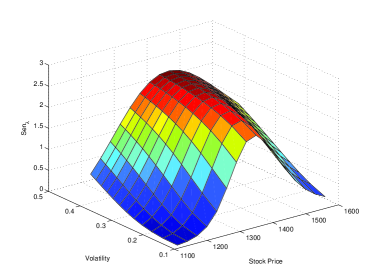

The sensitivity of the option price to errors affecting is computed by solving the adequate PDE as indicated in section 3.2. Fig. 11 displays the sensitivities of options and with respect to , computed at option creation time.

9 Conclusion

Our main goal was to quantify the impact on European call option pricing of the parameter estimation errors generated by fitting Heston joint SDEs to market data. Since volatility data are unobservable we consider that they are systematically estimated either by realized volatilities or by implied volatilities.

We have developed and numerically tested an impact quantification technique combining the computation of consistent estimators for the underlying Heston SDEs parameters, the evaluation of root mean squared accuracy for these estimators, and the numerical solution of six parabolic partial differential equations in , namely the option pricing PDE and the PDEs verified by the partial derivatives of option price with respect to model parameters.

We have also derived and implemented an algorithm to estimate the market price of volatility risk by analysis of multiple benchmark options

We have tested our approach by numerical fitting of Heston joint SDEs to the 252 daily data recorded in 2006 for the S&P 500 and VIX indices, and by studying several European call options written on S&P 500. For two such options, we compute and display the average option pricing shifts induced by errors of estimation on the SDEs coefficients, as well as by approximation errors for the market price of volatility risk. Since our algorithmic implementations are fairly fast on a standard laptop, our study strongly suggests that quantification of errors induced on option pricing by model parameters estimation errors should not be neglected, and could be systematically computed when option pricing is performed after fitting joint Heston SDEs to daily or intraday market data. Our numerical results indeed show that Heston SDEs fitting to a year of daily data can generate sizeable inaccuracies for European option pricing.

We expect that our methods will perform just as well for American options as for European options. We also plan to extend our approach to develop fast accuracy monitoring algorithms for portfolio hedging.

References

- Achdou and Pironneau (2005) Achdou, Y. and Pironneau, O., Computational methods for option pricing, 2005, Society for Industrial Mathematics.

- Ait-Sahalia and Kimmel (2007) Ait-Sahalia, Y. and Kimmel, R., Maximum likelihood estimation of stochastic volatility models. Journal of Financial Economics, 2007, 83, 413–452.

- Andersen et al. (2003) Andersen, T.G., Bollerslev, T., Diebold, F.X. and Labys, P., Modeling and forecasting realized volatility. Econometrica, 2003, 71, 579–625.

- Andersen et al. (2009) Andersen, T.G., Davis, R.A., Kreiß, J.P. and Mikosch, T.V., Handbook of Financial Time Series, 2009, Springer.

- Atiya and Wall (2009) Atiya, A.F. and Wall, S., An analytic approximation of the likelihood function for the Heston model volatility estimation problem. Quantitative Finance, 2009, 9, 289–296.

- Avellaneda et al. (2003) Avellaneda, M., Boyer-Olson, D., Friz, P. et al., Application of large deviation methods to the pricing of index options in finance. Comptes Rendus Mathematique, 2003, 336, 263–266.

- Azencott et al. (2015a) Azencott, R., Beri, A., Ren, P. and Timofeyev, I., Parametric estimation of the volatility equation in the Heston Model using indirect observations. , 2015a Pre print.

- Azencott et al. (2015b) Azencott, R., Ren, P. and Timofeyev, I., Parametric Estimation from Approximate Data: Non-Gaussian Diffusions. arXiv:1501.05370v1 [math.PR], 2015b.

- Azencott and Gadhyan (2009) Azencott, R. and Gadhyan, Y., Accurate parameter estimation for coupled stochastic dynamics. In Proceedings of the Dynamical Systems and Differential Equations. Proceedings of the 7th AIMS international conference, Arlington, Texas, DCDS Supplement, pp. 44–53, 2009.

- Azencott and Gadhyan (2015) Azencott, R. and Gadhyan, Y., Accuracy of Maximum Likelihood Parameter Estimators for Heston volatility SDEs. Journal of Statistical Physics, 2015, 159, 393–420.

- Bakshi et al. (1997) Bakshi, G., Cao, C. and Chen, Z., Empirical performance of alternative option pricing models. Journal of Finance, 1997, 52, 2003–2049.

- Bakshi and Kapadia (2003) Bakshi, G. and Kapadia, N., Delta-hedged gains and the negative market volatility risk premium. Review of Financial Studies, 2003, 16, 527–566.

- Barndorff-Nielsen (2002) Barndorff-Nielsen, O.E., Econometric analysis of realized volatility and its use in estimating stochastic volatility models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 2002, 64, 253–280.

- Bates (1996) Bates, D.S., Jumps and stochastic volatility: Exchange rate processes implicit in Deutsche Mark options. Review of financial studies, 1996, 9, 69–107.

- Björk (2009) Björk, T., Arbitrage theory in continuous time, 2009, Oxford Univ Press.

- Black and Scholes (1973) Black, F. and Scholes, M., The pricing of options and corporate liabilities. Journal of Political Economy, 1973, 81.

- Black (1976) Black, F., Studies of Stock Price Volatility Changes. , 1976.

- Bollerslev et al. (2011) Bollerslev, T., Gibson, M. and Zhou, H., Dynamic estimation of volatility risk premia and investor risk aversion from option-implied and realized volatilities. Journal of Econometrics, 2011, 160, 235–245.

- Bollerslev and Zhou (2002) Bollerslev, T. and Zhou, H., Estimating stochastic volatility diffusion using conditional moments of integrated volatility. Journal of Econometrics, 2002, 109, 33–65.

- Broadie and Kaya (2004) Broadie, M. and Kaya, O., Exact simulation of option greeks under stochastic volatility and jump diffusion models. In Proceedings of the Simulation Conference, 2004. Proceedings of the 2004 Winter, Vol. 2, pp. 1607–1615, 2004.

- Broto and Ruiz (2004) Broto, C. and Ruiz, E., Estimation methods for stochastic volatility models: a survey. Journal of Economic Surveys, 2004, 18, 613–649.

- Buraschi and Jackwerth (2001) Buraschi, A. and Jackwerth, J., The price of a smile: Hedging and spanning in option markets. Review of Financial Studies, 2001, 14, 495–527.

- Carr and Madan (1999) Carr, P. and Madan, D., Option pricing and the fast Fourier transform. Journal of Computational Finance, 1999, 2, 61–73.

- Carr and Wu (2009) Carr, P. and Wu, L., Variance risk premiums. Review of Financial Studies, 2009, 22, 1311–1341.

- Chan and Joshi (2010) Chan, J.H. and Joshi, M., First and second order greeks in the Heston model. Available at SSRN 1718102, 2010.

- Chernov and Ghysels (2000) Chernov, M. and Ghysels, E., A study towards a unified approach to the joint estimation of objective and risk neutral measures for the purpose of options valuation. Journal of Financial Economics, 2000, 56, 407–458.

- Comte et al. (1998) Comte, F., Renault, E. et al., Long memory in continuous-time stochastic volatility models. Mathematical Finance, 1998, 8, 291–323.

- Cox et al. (1985) Cox, J., Ingersoll Jr, J. and Ross, S., A theory of the term structure of interest rates. Econometrica: Journal of the Econometric Society, 1985, 53, 385–407.

- Dacunha-Castelle and Florens-Zmirou (1986) Dacunha-Castelle, D. and Florens-Zmirou, D., Estimation of the coefficients of a diffusion from discrete observations. Stochastics An International Journal of Probability and Stochastic Processes, 1986, 19, 263–284.

- Duffie et al. (2000) Duffie, D., Pan, J. and Singleton, K., Transform analysis and asset pricing for affine jump-diffusions. Econometrica, 2000, 68, 1343–1376.

- Eraker (2008) Eraker, B., The Volatility Premium. , 2008.

- Exchange (2003) Exchange, C.B.O., VIX White Paper. URL: http://www. cboe. com/micro/vix/vixwhite. pdf, 2003.

- Feller (1951) Feller, W., Two singular diffusion problems. Annals of Mathematics, 1951, 54, 173–182.

- Fouque et al. (2000) Fouque, J.P., Papanicolaou, G. and Sircar, K.R., Mean-reverting stochastic volatility. International Journal of Theoretical and Applied Finance, 2000, 3, 101–142.

- Gadhyan (2010) Gadhyan, Y., Option Pricing Accuracy for Estimated Stochastic Volatility Models. PhD thesis, University of Houston, 2010.

- Gallant and Tauchen (1996) Gallant, A.R. and Tauchen, G., Which moments to match?. Econometric Theory, 1996, 12, 657–681.

- Garman and Klass (1980) Garman, M.B. and Klass, M.J., On the estimation of security price volatilities from historical data. Journal of business, 1980, pp. 67–78.

- Gatheral et al. (2014) Gatheral, J., Jaisson, T. and Rosenbaum, M., Volatility is rough. Available at SSRN 2509457, 2014.

- Genon-Catalot and Jacod (1994) Genon-Catalot, V. and Jacod, J., Estimation of the diffusion coefficient for diffusion processes: random sampling. Scandinavian Journal of Statistics, 1994, 21, 193–221.

- Genon-Catalot et al. (1999) Genon-Catalot, V., Jeantheau, T. and Laredo, C., Parameter estimation for discretely observed stochastic volatility models. Bernoulli, 1999, 5, 855–872.

- Glowinski (2003) Glowinski, R., Handbook of numerical analysis, 2003, North-Holland Amsterdam.

- Glowinski (2008) Glowinski, R., Numerical methods for nonlinear variational problems, 2008, Springer-Verlag.

- Haentjens (2013) Haentjens, T., Efficient and stable numerical solution of the Heston–Cox–Ingersoll–Ross partial differential equation by alternating direction implicit finite difference schemes. International Journal of Computer Mathematics, 2013, 90, 2409–2430.

- Heston (1993) Heston, S., A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies, 1993, 6, 327–343.

- Hull and White (1987) Hull, J. and White, A., The pricing of options on assets with stochastic volatilities. Journal of Finance, 1987, 42, 281–300.

- Ikonen and Toivanen (2004) Ikonen, S. and Toivanen, J., Operator splitting methods for American option pricing. Applied Mathematics Letters, 2004, 17, 809–814.

- Jacquier et al. (2002) Jacquier, E., Polson, N.G. and Rossi, P.E., Bayesian analysis of stochastic volatility models. Journal of Business & Economic Statistics, 2002, 20, 69–87.

- Johnson and Shanno (1987) Johnson, H. and Shanno, D., Option Pricing when the Variance Is Changing. Journal of Financial and Quantitative Analysis, 1987, 22, 143–151.

- Kim et al. (1998) Kim, S., Shephard, N. and Chib, S., Stochastic volatility: likelihood inference and comparison with ARCH models. The Review of Economic Studies, 1998, 65, 361–393.

- Lamoureux and Lastrapes (1993) Lamoureux, C.G. and Lastrapes, W.D., Forecasting stock-return variance: Toward an understanding of stochastic implied volatilities. Review of Financial Studies, 1993, 6, 293–326.

- Melino and Turnbull (1990) Melino, A. and Turnbull, S., Pricing foreign currency options with stochastic volatility. Journal of Econometrics, 1990, 45, 239–265.

- Oosterlee (2003) Oosterlee, C., On multigrid for linear complementarity problems with application to American-style options. Electronic Transactions on Numerical Analysis, 2003, 15, 165–185.

- O’sullivan and O’sullivan (2013) O’sullivan, C. and O’sullivan, S., PRICING EUROPEAN AND AMERICAN OPTIONS IN THE HESTON MODEL WITH ACCELERATED EXPLICIT FINITE DIFFERENCING METHODS. International Journal of Theoretical and Applied Finance (IJTAF), 2013, 16.

- Pan (2002) Pan, J., The jump-risk premia implicit in options: Evidence from an integrated time-series study. Journal of financial economics, 2002, 63, 3–50.

- Ren (2014) Ren, P., Parametric Estimation of the Heston model under the Indirect Observability Framework [online]. , 2014. (accessed ????).

- Scott (1987) Scott, L.O., Option Pricing when the Variance Changes Randomly: Theory, Estimation, and an Application. Journal of Financial and Quantitative Analysis, 1987, 22, 419–438.

- Shephard (2005) Shephard, N., Stochastic Volatility.. Economics Group, Nuffield College, University of Oxford, Economics Papers, 2005.

- Singler (2008) Singler, J., Differentiability with respect to parameters of weak solutions of linear parabolic equations. Mathematical and Computer Modelling, 2008, 47, 422–430.

- Stein and Stein (1991) Stein, E. and Stein, J., Stock price distributions with stochastic volatility: an analytic approach. Review of Financial Studies, 1991, 4, 727–752.

- Stein (1989) Stein, J., Overreactions in the options market. The Journal of Finance, 1989, 44, 1011–1023.

- Varga (2000) Varga, R., Matrix Iterative Analysis, 2000, Springer, Berlin.

- Wiggins (1987) Wiggins, J., Option values under stochastic volatility: Theory and empirical estimates. Journal of Financial Economics, 1987, 19, 351–372.

- Windisch (1989) Windisch, G., M-matrices in numerical analysis, Vol. 115, , 1989, Teubner.

- Yu et al. (2003) Yu, W., Zhang, F. and Xie, W., Differentiability of C0-semigroups with respect to parameters and its application. Journal of Mathematical Analysis and Applications, 2003, 279, 78–96.