A Note on the Pricing of Basket Options Using Taylor Approximations

Abstract.

In this paper we propose a closed-form approximation for the price of basket options under a multivariate Black-Scholes model, based on Taylor expansions and the calculation of mixed exponential-power moments of a Gaussian distribution. Our numerical results show that a second order expansion provides accurate prices of spread options with low computational costs, even for out-of-the-money contracts.

Key words and phrases:

Taylor approximations, basket options, spread options.1. Introduction

The objective of the paper is the pricing of basket options using Taylor approximations under diffusion multivariate models with constant covariance. Basket options are multivariate extensions of European calls or puts. A basket option takes the weighted average of a group of stocks as the underlying, and produces a payoff equal to the maximum of zero and the difference between the weighted average and the strike (or the opposite difference for the case of a put). Index options, whose value depends on the movement of an equity or other financial index such as the S&P500, are examples of basket options.

For the particular case of spread options, several approximations have been previously considered in the works of Kirk(1995), Carmona and Durrleman(2003), Li, Deng and Zhou(2008, 2010), Venkatramanan and Alexander(2011) where different ad-hoc approaches are studied.

As an alternative Fast Fourier Transform methods have been successfully implemented to compute spread prices under more general Levy processes, see Hurd and Zhou(2009) and Cane and Olivares(2014) and under stochastic volatility models in Depmster and Hong(2000).

The approach to pricing by Taylor expansions can be traced back to Hull and White(1987), where the price of a one dimensional derivative is calculated. On the other hand, following an idea in Pearson(1995) it can be extended to multidimensional contracts by conditioning on the remaining underlying, reducing the problem to one dimensional pricing with parameters arising from the resulting conditional distribution. It should be noticed that this technique has been used in Li, Deng and Zhou(2008) for the case of spread options. Furthermore, in Li, Deng and Zhou(2010) the Taylor expansion approximation is compared with other pricing techniques, proving to be effective and accurate for most values in the parametric space.

Although in the same spirit, in our case the expansion is done on the function resulting from the conditional price, as opposed to a development based on the conditional strike price, as previously considered by the authors cited above. Moreover, our method hinges on the calculation of mixed exponential-power moments of a Gaussian distribution, it is extended to expansions about any point and higher dimensions. Our point of view may allow for a better control on the approximation, particularly for out-of-the-money options. On a related paper, see Alvarez, Escobar and Olivares(2011), we apply a similar technique to the price of a spread option when correlation is stochastic, by expanding on the correlation matrix.

The organization of the paper is the following, in section 2 we introduce some notations, the model and derive the Taylor approximation for basket options. In section 3 we specialize the formula for spread options and compute the mixed exponential-power moments of a Gaussian law. In section 4 we discuss our numerical results.

2. Basket Derivatives and Taylor expansions

We introduce some notations. Let be a filtered probability space. We define the filtration as the -algebra generated by the random variables completed in the usual way. Denote by an equivalent martingale risk neutral measure and the expectation under .

By we denote the (constant) interest rate, represents the transpose of matrix while is a vector with components . The d-dimensional column vector of ones is denoted by .

For a -times differentiable function in and a vector with such that

, represents its mixed partial derivative of order differentiated times with respect to the variable .

The process of spot prices is denoted by and are the asset log-returns related by:

| (1) |

We analyze European Basket options whose payoff at maturity , for a strike price , is given by:

| (2) |

where are some deterministic weights and .

As examples we have spread options, defined for with payoff:

| (3) |

Also, we have 3:2:1 crack spreads with and payoff:

| (4) |

where , and are respectively the spot prices of gasoline, heating oil and crude oil.

Exchange options are derivatives whose payoff is a particular case of (3) when . Exact formulas are available in the case of a diffusion, see Margrabe(1978).

We assume a multidimensional Black-Scholes dynamics under the risk neutral probability following:

| (5) |

where is a d-dimensional vector of Brownian motions such that , for and is a positive definite symmetric matrix with components and .

We denote by the vector of log-returns, excluding the first component. The price of a basket option with maturity at and payoff is:

where:

Assuming is smooth enough, we denote the n-th order Taylor development of around the point as . It is given by:

| (7) |

where:

and .

The next proposition provides the Taylor approximation for the price of a basket option:

Proposition 1.

The n-th order Taylor approximation around of the price of a basket option with payoff , defined as , under model (5), is given by:

| (8) |

where for :

| (9) |

is the Black-Scholes price of a call option with strike price , maturity at , volatility , spot price and strike price:

| (10) |

with:

| (11) |

| (12) |

and is the covariance matrix of the vector .

Proof.

From equation (5) a straightforward application of Ito formula leads to:

| (13) |

in law, where is a random variable with a multivariate normal distribution in with zero mean and covariance matrix . Hence has also a multivariate normal distribution. Also conditionally on , the random variable has a univariate normal distribution. Thus, we can write:

| (14) |

in law, where is independent of and it has, conditionally on , a standard univariate normal distribution. Moreover it is well known, see for example Tong (1989), that and are given by equations (11) and (12) respectively.

Next, from equation (LABEL:eq:gen-price) we have:

where .

Moreover, substituting equation (14) into (LABEL:eq:pgral) we have:

where:

Applying a n-th order Taylor development around to we compute the approximated conditional price based on the first underlying and conditional on the remaining by :

| (16) |

After replacing equation (16) into the expression for above we get immediately equation (8) in Proposition 1. ∎

Remark 2.

Notice that the approximation depends only on the derivatives of the function with respect , which in turn is computed as the Black-Scholes price composed with the function and the mixed exponential-power moments of a Gaussian multivariate distribution.

Remark 3.

Sensitivities to the parameters can be computed by a similar approximation, as Greeks for a Black-Scholes option model are known. For example the delta with respect to the j-th asset can be approximated by:

3. Pricing spreads options by Taylor approximations

In order to illustrate the method studied in the previous section we consider the case of a bidimensional spread option under model (5) with covariance matrix:

We find the n-th Taylor approximation in this specific situation. Denoting by we have that:

| (17) |

where:

| (18) |

From equation (13) the conditional distribution of given is:

Thus we can write:

in law, where independent of , with

| (19) |

and

From Proposition 1 the n-th approximation simplifies to:

| (20) |

Moreover:

where:

Now, from equation (17) we have that , then the exponential-power moments can be calculated as follows:

where:

Next integrate by parts:

where is the double factorial defined as the product of all odd numbers between 1 and including both. When the set is empty, by convention, the product is equal to one.

Similarly for we have:

After gathering all pieces and substituting in equation (20) we have the following result:

Proposition 4.

Next, we compute the derivatives of the function with respect to . From the Black-Scholes pricing formula:

where:

and is the cumulated distribution function of a standard normal distribution.

The first two derivatives are computed by elementary methods.

First notice that:

Also:

where is the density function of a standard normal random variable and

Similarly the second derivative is obtained as:

with:

In particular when we develop around we have the first and second approximations given respectively by :

More generally expanding around we have the first two approximations denoted by and respectively and given by:

4. Pricing Spreads: numerical results

We consider spread options in the following benchmark numerical set:

, , , , , , and .

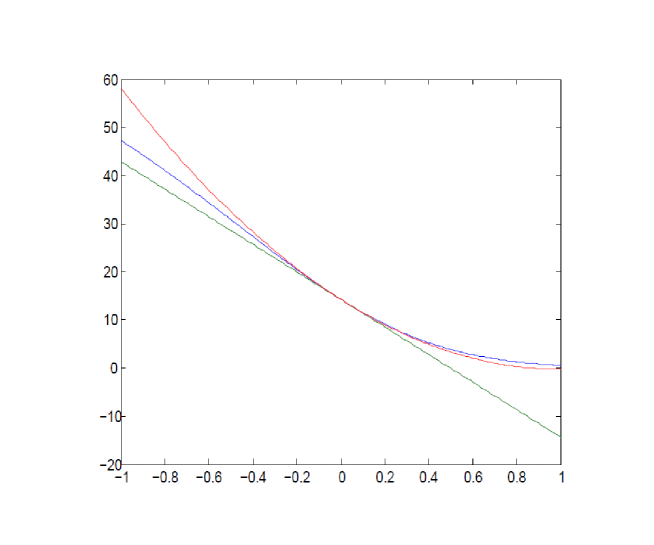

In Figure 1 the graph of the conditional price given by equation (7) is shown (blue line), together with the first and second order Taylor approximation around the mean, for the benchmark parameter set.

Notice that the first approximation underestimates the price. Not surprisingly the second approximation estimates the price fairly well for values close to the point while is less accurate for values far from the mean. Although it seems a drawback of the method it does not constitutes a serious problem as values far from the mean are unfrequent, thus the error in calculating the outer expected value by the Taylor approximation is small.

In Figure 2 a histogram for simulated returns on asset 1 (blue rectangles) and asset 2(red rectangles) is shown. Notice that only a few values of the returns lie outside the interval .

Next we compare Taylor approximations with Monte Carlo simulations. In Table 1(column 2) prices from Monte Carlo are shown for the benchmark parameters, except the correlation parameter that takes values . The number of simulations is , where a stability of order is attained. Partial Monte Carlo prices (shown in column 3) are obtained by sampling directly the one dimensional conditional price and taking the corresponding average of the payoff. It leads to a more efficient simulation algorithm as only one Brownian motion needs to be simulated, as oppose to two correlated Brownian in the standard Monte Carlo approach. It is done though at the expense of an extra evaluation of the Black-Scholes formula in every step.

Taylor prices of first and second order are shown in columns 4 and 5 of Table 1. The expansions take place around . While in some cases the first order approximation reveals significant different with Monte Carlo, second order approximation shows an improved agreement with a relative error in the order of for the parameter set considered.

| Correlation | Monte Carlo | Partial Monte Carlo | First approx. | Second approx. |

|---|---|---|---|---|

| 12.7843 | 12.7907 | 12.7889 | 12.7901 | |

| 14.9734 | 14.9826 | 13.6063 | 15.0065 | |

| 11.9525 | 11.9544 | 11.8085 | 11.9646 | |

| 15.6273 | 15.6302 | 13.2767 | 15.9238 |

For extreme values of the correlation coefficient , e.g. larger than an absolute value of , the Taylor expansions around do not work well. Nevertheless it is interesting to notice that the approximations are rather sensible to the point where the expansion is taken. Moreover, by slightly changing the latter the accuracy of the method can be considerably improved. In Table 2 spread prices for the benchmark parameters and for different expansion points are shown.

| Expansion point | Monte Carlo | Partial Monte Carlo | First approx. | Second approx. |

|---|---|---|---|---|

| 16.2463 | 16.2540 | 12.3734 | 16.3011 | |

| 16.2463 | 16.2540 | 12.2966 | 15.8566 | |

| 16.2463 | 16.2540 | 11.8434 | 12.9761 | |

| 16.2463 | 16.2540 | 12.5208 | 17.5217 | |

| 16.2463 | 16.2540 | 12.5089 | 18.2168 |

We test the Taylor expansion method for out-of-the-money contracts and compare with the price obtained via Monte Carlo with repetitions. The results are shown in Table 3. The benchmark parameters are the same, except for the spot and strike prices that are changed accordingly. again a second order Taylor expansion seem to capture the Monte Carlo prices.

| Parameters | Monte Carlo | Taylor (first order) | Taylor (second order) |

|---|---|---|---|

| 7.040956 | 5.30281 | 7.0468998 | |

| 4.8015937 | 3.442070 | 4.800319 | |

| 5.7623 | 4.3248347 | 5.7726138 | |

| 3.89825 | 2.71934 | 3.89966 | |

5. Conclusions

We present an efficient method to price basket options under a multidimensional Black-Scholes model, based on a Taylor expansion of the conditional one dimensional price resulting from fixing one of the underlying assets. The formula is given in terms of exponential-power moments of a multivariate Gaussian law and the evaluation of certain derivatives in the Black-Scholes price.

We implement it numerically in the case of spread contracts. Within the benchmark parametric set this approach is in closed agreement with the price obtained via Monte Carlo, even for deep out-of-the-money contracts, at considerable lesser computational effort. A second order development seems to be sufficient to achieve a relative error around .

References

- [1] Alvarez, A., Escobar, M., Olivares,P.(2010) Pricing two dimensional derivatives under stochastic correlation. International Journal of Financial Markets and Derivatives Volume 2, Number 4/2011, pg.265-287.

- [2] Cane, M., Olivares, P (2014) Pricing Spread Options under Stochastic Correlation and Jump-Diffusion Models by FFT working paper.

- [3] Carmona, R. and Durrleman, V.(2003). Pricing and Hedging Spread Options. SIAM Review, 45:4, 627-685.

- [4] Carmona, R., Durrelman, V. (2006) Generalizing the Black-Scholes Formula to Multivariate Contingent Claims. Journal of Computational Finance, Vol. 9, No. 2, Spring 2006.

- [5] Dempster, M.A.H. and S.S.G. Hong (2000) Spread option valuation and the fast Fourier transform. Research Papers in Management Studies, WP 26/2000

- [6] Hull, J. C., and White A. (1987) The Pricing of Options on Assets with Stochastic Volatilities Journal of Finance, 42, 281-300.

- [7] Kirk, E.(1995) Correlation in the Energy Markets, in managing energy price risk. Risk Publications and Enron, London, 71-78.

- [8] Li, M., Deng, S. and Zhou, J.( 2008) Closed-form Approximations for Spread Options Prices and Greeks. Journal of Derivatives, 15:3, 58-80.

- [9] Li, M., Zhou, J., Deng, S. J. (2010) Multi-asset spread option pricing and hedging. Quantitative Finance, 10(3), 305-324.

- [10] Margrabe, W.(1978) The value of an option to exchange one asset for another. The J. of Finance, Vol. 33, no.1, pg.177-186.

- [11] Pearson, N.(1995) An efficient approach for pricing spread options. Journal of Derivatives, pp. 76-91.

- [12] Tong, Y. L. (1989). The Multivariate Normal Distribution, Springer, Berlin.

- [13] Venkatramanan, A., Alexander, C.(2011) Closed Form Approximations for Spread Options, Applied Mathematical Finance. iFirst, 1 26, 2011 ICMA.

- [14] Zhu, J. (2000). Modular pricing of options: An Application of Fourier Analysis Lecture Notes in Economics and Mathematical Systems Springer-Verlag.