Bounding the Optimal Revenue of Selling Multiple Goods111Supported by the European Union FP7-ICT grant 284731 (UaESMC) and ERC Advanced Grant 321171 (ALGAME).

Abstract

Using duality theory techniques we derive simple, closed-form formulas for bounding the optimal revenue of a monopolist selling many heterogeneous goods, in the case where the buyer’s valuations for the items come i.i.d. from a uniform distribution and in the case where they follow independent (but not necessarily identical) exponential distributions. We apply this in order to get in both these settings specific performance guarantees, as functions of the number of items , for the simple deterministic selling mechanisms studied by Hart and Nisan [11], namely the one that sells the items separately and the one that offers them all in a single bundle.

We also propose and study the performance of a natural randomized mechanism for exponential valuations, called Proportional. As an interesting corollary, for the special case where the exponential distributions are also identical, we can derive that offering the goods in a single full bundle is the optimal selling mechanism for any number of items. To our knowledge, this is the first result of its kind: finding a revenue-maximizing auction in an additive setting with arbitrarily many goods.

1 Introduction

What selling mechanism should a monopolist with many heterogeneous goods deploy when facing a buyer, in order to maximize his revenue? The buyer has private valuations for the items but the seller can only have an incomplete prior knowledge of these values, in the form of a probability distribution over them. Furthermore, the buyer is strategic and selfish, meaning that if asked to submit her valuations for the goods she will lie if this is to improve her own personal gain. This is one of the most fundamental problems in auction theory, and although it has received a lot of attention from both the Economics and Computer Science communities, it still remains elusive.

1.1 Related Work

The problem is famous for demonstrating a striking dichotomy; the case of a single good is fully resolved by the seminal work of Myerson [20]: the optimal selling strategy is to just set a take-it-or-leave it price for the item, and this price is given by a very simple formula involving the probability distribution. However, for more goods, in fact even for just two and three items, our understanding of optimal mechanisms is totally insufficient. The problem seems to be qualitatively completely different and it is widely believed that no closed-form, elegant solutions are within reach (see e.g. [18, 5]).

First of all, it is known that in general determinism (i.e. setting selling prices for various bundles of goods) is not enough any more and that lotteries need to be deployed for optimality [14, 12, 17, 21, 6]. Manelli and Vincent [17] provide some sufficient conditions for deterministic mechanisms to be optimal, but these are arguably rather involved, so they were able to instantiate and verify them only for the case of two and three goods with valuations i.i.d. according to a uniform distribution. Hart and Nisan [11] have also presented a very simple sufficient condition, in the special case of two i.i.d. items, for the full-bundle mechanism (that just sets a single selling price for all the items together) to be optimal and deploy it to show that this holds for the equal-revenue distribution and, more generally, for all Pareto distributions with parameter . Finally, Daskalakis et al. [6] have shown that full-bundling is also an optimal selling strategy for two exponentially i.i.d. goods. Nothing is clearly known in this front for more than three items or other distributions, apart from the recent work of Giannakopoulos and Koutsoupias [8] where a closed-form description of a deterministic mechanism that is shown to be optimal for up to six uniformly i.i.d. items is given, and conjectured that this holds for any number of goods.

In the current paper we contribute to this line of work, by generalizing the result of [6] from to any number of goods, showing that determinism is optimal for arbitrarily many identical valuations distributed according to an exponential distribution, and in fact optimality is achieved by the simple full-bundling strategy. To our knowledge, this is the first result that provides specific description of an optimal auction for an arbitrary number of items. In fact, together with [8], they are the first such results to break the boundary of three items.

This path of discovering “simple” descriptions of optimal selling mechanisms is further being narrowed by a recent computational hardness result from Daskalakis et al. [5], where it is shown that even for independent (but not identical) valuations with finite support of size , it is #P-hard to compute exactly the optimal mechanism. However this does not exclude the possibility of a PTAS and for i.i.d. settings Cai and Huang [2] and Daskalakis and Weinberg [4] have indeed already provided such efficient algorithmic approximations.

So, given the previous discussion, it is essential to try to approximate the optimal revenue by selling mechanisms that are as simple as possible. We may lose something with respect to the total revenue objective, but on the other hand these mechanisms are much easier to understand, describe, analyze and implement, and such results may in fact enrich our understanding of the character of exact optimal auctions in general. Hart and Nisan [11] provide such solid and elegant approximation ratio guarantees (logarithmic with respect to the number of items) that hold “universally” for all product (independent) distributions, without even assuming standard regularity conditions (like e.g. in [3, 17, 20]), by studying the two most natural deterministic mechanisms: the one that treats every item independently and sells them separately to the buyer and, on the other end, the one that treats all items as a single full bundle. In particular, they prove an -approximation ratio for the former and, with the extra requirement of identical distributions, an -approximation for the latter, where is the number of goods. They also provide slightly improved guarantees for the special case of two i.i.d. goods. Li and Yao [16] further improved their results, by bringing these down to and respectively, which are also proved to be tight up to constants222In a very exciting recent result, after our paper was first made publicly available, Babaioff et al. [1] showed that combining these two simple selling mechanisms one can guarantee a constant approximation ratio of by just assuming independence of the item valuations. Yao [23] generalized their results to multi-bidder settings..

In this paper we try to specialize these general probabilistic results for the case of specific “canonical” distributions, namely the uniform and exponential ones, and we show that by doing so one can get good constant-factor, almost optimal in many cases, performance guarantees. Furthermore, in keeping up with the spirit of the line of work that studies simple but still well-performing mechanisms we also propose a very natural randomized mechanism for exponential distributions and provide good approximation guarantees for it.

Daskalakis et al. [6] and Giannakopoulos and Koutsoupias [8] have developed duality-theory frameworks for the general problem of multidimensional optimal auctions, the former having a strong measure-theoretic flavor by using classic results from optimal transport theory combined with Strassen’s theorem for stochastic dominance, and the latter resembling more in spirit traditional linear programming theory formulations.

1.2 Our Results and Techniques

Our model is the standard single-buyer multi-item additive valuations Bayesian model of McAfee and McMillan [19] which is used in many other works [17, 11, 6, 16]. Critical to the exposition is the analytical characterization of truthfulness through subgradients of convex functions given by Rochet [22].

Inspired by the elegant approach of Hart and Nisan [11], we take the opposite direction to their universal approximation guarantees for general independent distributions, and try to give better, specialized bounds for the case of uniform and exponential distributions. Our main strategy is driven by the standard technique in approximation algorithms, to use weak-duality from traditional linear programming to upper-bound the optimal objective and then use this to calculate approximation upper bounds for particular algorithms. Since the optimal revenue problem cannot be fully captured by means of traditional combinatorial LPs, we use the duality-theory framework developed in [8]. In particular, we use the weak-duality theorem (see Theorem 1) in order to get specific closed-form bounds for our settings (Theorems 2 and 3), by constructing and plugging-in appropriate feasible dual solutions (Theorems 4 and 5). This is the most technical part of the paper. This technique is completely different to previous results on approximate mechanisms for the problem which rely entirely on probabilistic analysis methods (e.g. the core-tail decomposition of [16]). Our bounds on the optimal revenue are very simple expressions, depending on the number of items . We believe that, given how notoriously difficult is the problem of exactly determining the optimal revenue, coming up with such formulas is a very useful tool for (approximate) auction analysis, and is of its own interest.

By comparing these bounds to the revenue obtained by the simple mechanisms studied in Hart and Nisan [11] we are able to give closed-form approximation guarantees with respect to the number of items , in both settings that we are interested in: for the case of i.i.d. uniform distributions (see Fig. 1) over the unit interval we show that selling the items separately is loosely -approximate and that selling in a full-bundle always performs better and is asymptotically optimal; for independent (and not necessarily identical) exponential distributions (see Fig. 3) we give a closed-form formula upper bound (27) for selling separately that can be loosely upper-bounded by .

Furthermore, if the exponential distributions are in addition identical, then we can show (Theorem 7) that selling deterministically in a full-bundle is optimal, for any number of goods. We derive this optimality as a side result of the analysis of a very simple and natural randomized selling mechanism that we propose for the setting of independent (but not necessarily identical) exponential valuations. We call it Proportional (Definition 1) and allocates the items somehow proportionally with respect to every item’s exponential distribution parameter. We compute the expected revenue of this mechanism (Theorem 6) and using again the optimal revenue bounds derived earlier, we show that Proportional’s approximation ratio is at most equal to the ratio between the maximum and minimum parameters of the independent exponential distributions. For i.i.d. settings, this ratio is of course equal to , proving optimality and Proportional reduces to full-bundling.

A final remark must be made about the choice of uniform and exponential distributions. This was not random; we wanted to study “canonical” examples of distributions, one for bounded-interval supports and one having full support . The uniform and exponential distributions are, respectively, the maximum entropy probability distributions for these two settings, intuitively being the “natural” choices if one wants to make as few assumptions as possible (see e.g. [9, Sect. 3.4.3]).

1.3 Model and Notation

The real unit interval will be denoted by and the nonnegative reals by . We will also use for any positive integer . The uniform distribution over will be denoted by and the exponential distribution with parameter by . Finally, we use the standard game-theoretic notation to denote the resulting vector if we remove ’s -th coordinate. Then, .

1.3.1 Mechanisms and Truthfulness

We study an -goods monopoly setting, where the buyer has a valuation of for good . Every is a real interval. This valuation is private information to her, and intuitively represents the amount of money she is willing to pay to get this item. The seller has only some (incomplete) prior knowledge of the player’s valuation vector in the form of a probability distribution over from which is sampled. For the purposes of this paper we will assume that is a product distribution, i.e. ’s follow independent distributions , and also that every has an almost everywhere (a.e.) differentiable density function .

A (direct revelation) selling mechanism on this setting is a protocol which, after receiving the buyer’s bid vector as input (the buyer may lie about her true valuations and misreport ), decides to sell item with probability , , for a total (for all items) price of . If one wants to restrict attention only to deterministic mechanisms, it is enough to take . However, here we optimize over the general class of randomized selling mechanisms, i.e. we allow lotteries.

More formally, a mechanism consists of an allocation function paired with a payment function . We consider the buyer having additive valuations for the items, her “happiness” when she has (true) valuations and reports to the mechanism being captured by her utility function

the sum of the value she receives from the items she manages to purchase minus the payment she has to submit to the seller for this purchase. The player is completely rational and selfish, wanting to maximize her utility and that’s why she will not hesitate to misreport instead of her private values if this is to give her a higher utility. The seller’s “happiness” is captured by the total revenue of the mechanism

| (1) |

It is standard in Mechanism Design to ask for mechanisms to respect the following two properties333We must mention here that these assumptions will be without loss to our revenue maximization objective, due to the celebrated Revelation Principle (see e.g. [20]). However, they help as simplify substantially the search for optimal selling mechanisms by narrowing the focus to truthful ones, under which we don’t have to worry about the players’ complex strategic behavior and the underlying game-theoretic equilibria.:

-

•

Individual Rationality (IR): for all .

-

•

Incentive Compatibility (IC): for all .

The IR constraint corresponds to the notion of voluntary participation, that is, the buyer cannot harm herself by taking part in the auction, while IC captures the fundamental property that truth-telling is a dominant strategy for the buyer in the underlying game, i.e. she will never receive a better utility by lying about her true bid. Mechanisms that satisfy IC are also called truthful. From now on we will focus on truthful IR mechanisms, and so we will relax notation to just , considering buyer’s utility as a function .

Rochet [22] gave a very elegant analytic characterization of truthful mechanisms (see e.g. [11] for a proof): must be a convex function with the allocation function being its subgradient; for all items and a.e. . This essentially establishes a correspondence between truthful mechanisms and utility functions. Not only does every selling mechanism induce a well-defined utility function for the buyer, but also conversely, given a nonnegative convex function that satisfies these two properties we can fully recover a corresponding mechanism from the allocation-derivative equality and (1).

1.3.2 Optimal Selling Mechanisms

This paper studies the problem of maximizing the expected seller’s revenue based on his prior knowledge of distribution , given the IR and IC constraints, thus (by (1) and the subgradient characterization) maximizing

| (2) |

over the space of nonnegative convex functions on having the property

for a.e. and all .

Following the notation in [11], we will denote by the expected revenue in (2). The optimal revenue is , i.e. the maximum revenue among all feasible truthful mechanisms. A mechanism inducing utility for which will be called an optimal mechanism.

Notice that for single-dimensional ’s, i.e. settings with a single good, the seminal work of Myerson [20] has fully settled the question of determining optimal auctions and the optimal revenue (see e.g. [15]):

| (3) |

obtained by the deterministic mechanism that sets a selling (take-it-or-leave-it) price threshold of (). For example, if then and and so by (3) we can easily compute , achieved by the optimal mechanism that sets a selling price of . Also, for the exponential distribution we have and for and so for a selling price of .

Finally, let us also provide some notation from [11] for the revenue of two simple deterministic selling mechanisms for the -items setting which are of great importance to us throughout this paper, namely the one which sells every item separately to the buyer and that which sells all items in a full bundle:

| (4) | ||||

respectively444 is the convolution of distributions , i.e. if are the random variables representing the items’ valuations, then is the distribution of the sum of the valuations, .. In particular, if for all , we have

| (5) |

where is the cdf of the Irwin-Hall distribution of the sum of independent uniform random variables over , i.e. [10]

| (6) |

In the same way, for independent exponential distributions and for i.i.d. exponential distributions, we can see that

| (7) |

where we use the shorthand notation .

2 Weak Duality

Define to be the family of all -dimensional functions , such that every is integrable and also absolutely continuous with respect to its -th coordinate, and which satisfy the following conditions a.e. in :

| (8) |

| (9) |

| (10) |

Then, we know from the duality framework developed in [8] that the optimal revenue can be bounded by the following quantity:

Theorem 1 (Weak Duality).

For every -dimensional interval and probability distribution over ,

| (11) |

We will feel free to refer to as feasible dual solutions, constraints (8)–(10) as dual constraints and to the above critical quantity as dual objective. The ties to the terminology of classical linear programming duality are obvious.

Since we are particularly interested in providing upper bounds for the optimal revenue in the case of independent uniform and exponential valuations, we specialize Theorem 1 in these cases, for ease of reference and a more clear exposition:

Theorem 2 (Weak Duality for Uniform Distributions).

Intuitively, for each item there is a dual function that, if viewed as a single dimensional function of just the -th coordinate, it has to start with the value of at the left boundary of the unit interval (condition (12)), travel all the way up to a value of at the end of the interval (condition (13)), but with a speed that is never too high: the sum of the derivatives of all ’s must not exceed at any point of the domain (condition (14)). At the same time, in order to get good bounds on the optimal revenue, these functions must stay as low as possible, so that they minimize the total volume under their curves (expression (15)). These are two contradicting objectives, and finding the right balance between them is the very essence of this duality method.

3 Uniform Domains

Theorem 4.

The optimal revenue from selling goods having uniform i.i.d. valuations over the unit interval is at mostProof.

Let

be the set of nodes of the -dimensional unit hypercube and for every node define to be the following subspace of :

A simple observation is that ’s form a valid partition of , i.e.

Now we are going to construct a feasible dual solution, that is, valid ’s, to plug them into Theorem 2. Fix some and a subspace (by fixing a ) and define as follows:

-

•

If , set for all .

-

•

Otherwise, i.e. if , set

for all , where

By this construction, and by letting range over , we have a well defined function . Each belongs to a unique partition (corresponding to a unique ), thus also well defining . So, the above definition can be written more compactly as

It is easy to check, directly from this definition, that

| (19) |

for all and and also that

| (20) |

Furthermore, if we fix some (and thus also fix the corresponding, well-defined, and ), we see from property (20) above that

| (21) |

But now we can see that Eqs. (19) and (21) are exactly properties (12), (13) and (14).

The last remaining step of the proof is to evaluate the dual objective and show that

which we do in Appendix B. ∎

Theorem 4 combined with (5) immediately gives us the following approximation ratio bound for the simple deterministic mechanism that sells the items separately:

| (22) |

A plot of this approximation ratio for the values of can be found in Fig. 1, drawn with blue color. In the same way, using the other expression of (5) together with (6) we get a bound for the approximation ratio of the deterministic full bundle mechanism, which is asymptotically optimal:

| (23) |

as . A plot of this approximation ratio for the values of can be found in Fig. 1, drawn with red color. Notice how full bundling outperforms selling separately for any number of goods .

Discussion of Theorem 4

We must mention here that one can trivially get an upper bound of for the optimal revenue , which is close to that given by Theorem 4: simply observe that by the IR constraint the seller cannot expect to extract more revenue than the buyer’s surplus, i.e. the sum of the item valuations , which for the uniform distribution has an expectation of . The two bounds are equal in the limit as the number of items grows large, however the one in Theorem 4 still gives an improvement by a factor of , which especially for a small number of goods, is not insignificant. Notice that, due to the Law of Large Numbers, the optimal revenue as will anyway tend to the expected full surplus, not only for the uniform distribution, but for any kind of independently distributed items555For more on this, see the discussion in [11]. This is the reason why, as Hart and Nisan [13] state, for our problem “the difficult case is when there is more than one but not too many goods”..

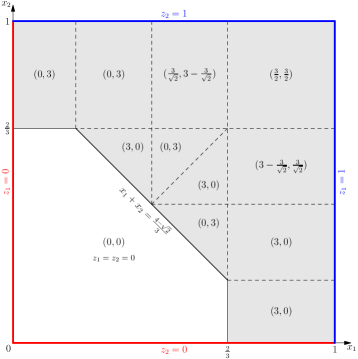

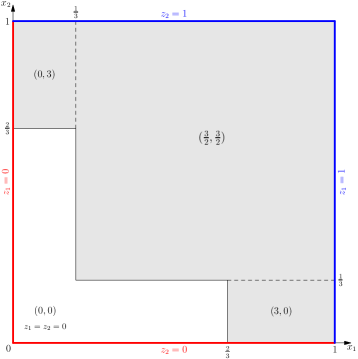

From that perspective, we believe that it is interesting to get bounds on the optimal revenue other than the trivial ones derived from using the above surplus-bound argument. To our knowledge Theorem 4 is the first such result in the literature. But, probably even more important than the improvement in the bound’s value itself, is the underlying technique of providing explicit feasible dual solutions to plug into Theorem 1: this can give new insights in the structure of good approximations of the optimal revenue, something which is known to be particularly difficult for our problem. To demonstrate this, consider for example the case of just two goods () with valuations drawn uniformly from . The dual program (12)–(14) essentially asks to allocate a total available value of among the derivatives of and over in a way that these functions start at and grow up above at the boundary of . On one hand there is the trivial way to do that, simply allocating the total weight equally: for all ; this is clearly a suboptimal solution, since the functions end up reaching a value of at the boundary’s end, way above . On the other hand, there is the optimal way to do it, given in [7] (see Fig. 2(b)). However, this construction is rather involved and very difficult to generalize, and in fact only existential proofs of optimality are know for more goods, and only up to items. So, it seems essential to find some middle ground within these two extremes, providing a good approximation to the optimal revenue but also still being simple enough to generalize for any number of items . This is exactly what the construction of the dual solutions in the proof of Theorem 4 provides. A demonstration is given in Fig. 2 for the case of two goods.

4 Exponential Domains

In the following, for positive integer and we will denote the (upper) incomplete Gamma function by

and define

| (24) |

Function is continuous and has a unique root with respect to variable . Let’s denote this root by . In fact, and also for all . So, the following function on the positive integers is well defined and nonnegative:

| (25) |

A detailed proof of all the above properties of function and calculations can be found in Appendix A.

Theorem 5.

The optimal revenue from selling goods having independent exponential valuations (with parameters ) is at most where is defined in (25). In the special case of i.i.d. exponential valuations with parameter this becomesProof.

We will construct appropriate dual variables that satisfy (16) and (17) to plug into the Weak Duality Theorem 3. For all and we define

where , and function as defined in (24). The nonnegativity of the dual variables as well as their absolute continuity is immediate from the properties of function . It is also trivial to see that condition (16) is immediately satisfied by the definition of . Regarding condition (17), for any and such that we calculate

so, by summing up we get

At the remaining case of , we have that for all . Also, since , we know that , so

Thus, in any case (17) is satisfied.

Finally, we compute the dual objective value in (18). First notice that

We perform the following change of variables in the integral:

| (26) |

where and with . Denote this subspace of where ’s range by . The Jacobian of this transformation equals and so the integral in (18) can be written as:

At the third equation above we used the following Lemma describing some known “geometric” properties of the body used in the transformation (26).

Lemma 1.

For any positive integer ,

for all (where denotes the standard Lebesgue measure).

∎

An immediate result of Theorem 5 combined with formula (7) is that for independent (not necessarily identical) exponential valuations the approximation ratio of the deterministic mechanism that sells items separately is at most

| (27) |

A plot of this approximation ratio for the values can be found in Fig. 3. The loose constant factor bound is straightforward and the proof can be found in Appendix A.

4.1 A Simple Randomized Selling Mechanism

Consider the following very simple randomized mechanism for the setting of independent exponential valuations with parameters . Without loss of generality, in the following let’s assume that . We will again be using our notation of and .

Definition 1 (Mechanism Proportional).

Sell item with probability and collect a total payment of (parameter is defined before (25)).

Essentially we sell the items with probability proportional to their parameters, normalized by the largest parameter . This mechanism is truthful, because it corresponds to the following utility function

which is obviously convex and we will use the shorthand notation

| (28) |

when this is more comfortable. Now let’s compute Proportional’s expected revenue. By (2) and the fact that this is

and by a simple integration by parts (see e.g. the derivation in [6, Sect. 2]) this can be written as

and by performing the same change of variables as in (26) in the proof of Theorem 5 we get that Proportional’s expected revenue is

which equals

by using Lemma 1. Utilizing (30) and taking into consideration that and that , integrating by parts the revenue becomes

for the first equation using (28). So we showed the following:

Theorem 6.

For goods with independent (but not necessarily identical) exponential valuations (with parameters ), mechanism Proportional has an expected revenue of

where is defined in (25).

Immediately, by combining Theorem 6 with Theorem 5, we get that Proportional’s approximation ratio is upper-bounded by

(29)

The performance of this approximation ratio bound depends heavily on the choice of the parameters . Obviously, the closer these parameters are the better the bound. However, if then this ratio can be unbounded. In such a case though, we can fall back to using the constant approximation separate selling mechanism in (27) which is at most -approximate. A very interesting consequence of (29) is for the special case of i.i.d. exponential priors, i.e. when . In that case, by (28) it is straightforward to see that Proportional reduces to the simple deterministic mechanism that sells all items in a full bundle for a price of and also the approximation ratio in (29) becomes , meaning that full bundling is optimal:

Theorem 7.

Selling deterministically in a full bundle666The optimal bundle price is , where is the parameter of the exponential distribution and is given before (25). is optimal for any number of exponentially i.i.d. goods.

Acknowledgements:

I am deeply grateful to Elias Koutsoupias for many useful discussions and guidance. I also thank an anonymous reviewer for suggesting the discussion after Theorem 4.

References

- Babaioff et al. [2014] M. Babaioff, N. Immorlica, B. Lucier, and S. M. Weinberg. A simple and approximately optimal mechanism for an additive buyer. In Proceedings of the 55th Annual Symposium on Foundations of Computer Science, FOCS ’14, 2014. URL http://arxiv.org/abs/1405.6146.

- Cai and Huang [2013] Y. Cai and Z. Huang. Simple and nearly optimal multi-item auctions. In Proceedings of the 24th Annual ACM-SIAM Symposium on Discrete Algorithms, SODA ’13, pages 564–577, 2013. URL http://epubs.siam.org/doi/abs/10.1137/1.9781611973105.41.

- Chawla et al. [2007] S. Chawla, J. D. Hartline, and R. Kleinberg. Algorithmic pricing via virtual valuations. In Proceedings of the 8th ACM Conference on Electronic Commerce, EC ’07, pages 243–251, 2007. URL http://doi.acm.org/10.1145/1250910.1250946.

- Daskalakis and Weinberg [2012] C. Daskalakis and S. M. Weinberg. Symmetries and optimal multi-dimensional mechanism design. In Proceedings of the 13th ACM Conference on Electronic Commerce, EC ’12, pages 370–387, 2012. URL http://doi.acm.org/10.1145/2229012.2229042.

- Daskalakis et al. [2013a] C. Daskalakis, A. Deckelbaum, and C. Tzamos. The complexity of optimal mechanism design. In Proceedings of the Twenty-Fifth Annual ACM-SIAM Symposium on Discrete Algorithms, SODA ’13, pages 1302–1318, 2013a. URL http://epubs.siam.org/doi/abs/10.1137/1.9781611973402.96.

- Daskalakis et al. [2013b] C. Daskalakis, A. Deckelbaum, and C. Tzamos. Mechanism design via optimal transport. In Proceedings of the 14th ACM Conference on Electronic Commerce, EC ’13, pages 269–286, 2013b. URL http://doi.acm.org/10.1145/2482540.2482593.

- Giannakopoulos [2014] Y. Giannakopoulos. A note on selling optimally two uniformly distributed goods. CoRR, abs/1409.6925, 2014. URL http://arxiv.org/pdf/1409.6925.pdf.

- Giannakopoulos and Koutsoupias [2014] Y. Giannakopoulos and E. Koutsoupias. Duality and optimality of auctions for uniform distributions. In Proceedings of the 15th ACM Conference on Economics and Computation, EC ’14, pages 259–276, 2014. doi: 10.1145/2600057.2602883. URL http://arxiv.org/abs/1404.2329. Full version in CoRR: abs/1404.2329.

- Golan et al. [1996] A. Golan, G. Judge, and D. Miller. Maximum entropy econometrics: robust estimation with limited data. Series in financial economics and quantitative analysis. Wiley, 1996. ISBN 9780471953111.

- Hall [1927] P. Hall. The distribution of means for samples of size n drawn from a population in which the variate takes values between 0 and 1, all such values being equally probable. Biometrika, 19(3/4):240–245, 1927. URL http://dx.doi.org/10.2307/2331961.

- Hart and Nisan [2012] S. Hart and N. Nisan. Approximate revenue maximization with multiple items. In Proceedings of the 13th ACM Conference on Electronic Commerce, EC ’12, pages 656–656, 2012. doi: 10.1145/2229012.2229061. URL http://arxiv.org/abs/1204.1846.

- Hart and Nisan [2013] S. Hart and N. Nisan. The menu-size complexity of auctions. In Proceedings of the 14th ACM Conference on Electronic Commerce, EC ’13, pages 565–566, 2013. doi: 10.1145/2482540.2482544. URL http://arxiv.org/abs/1304.6116.

- Hart and Nisan [2014] S. Hart and N. Nisan. How good are simple mechanisms for selling multiple goods? The Hebrew University of Jerusalem, Center for Rationality DP-666, 2014. URL http://www.ma.huji.ac.il/hart/abs/m-simple.html.

- Hart and Reny [2012] S. Hart and P. J. Reny. Maximal revenue with multiple goods: Nonmonotonicity and other observations. Technical report, The Center for the Study of Rationality, Hebrew University, Jerusalem, 2012. URL http://www.ma.huji.ac.il/hart/abs/monot-m.html.

- Hartline and Karlin [2007] J. D. Hartline and A. R. Karlin. Profit maximization in mechanism design. In N. Nisan, T. Roughgarden, É. Tardos, and V. Vazirani, editors, Algorithmic Game Theory, chapter 13. Cambridge University Press, 2007.

- Li and Yao [2013] X. Li and A. C.-C. Yao. On revenue maximization for selling multiple independently distributed items. Proceedings of the National Academy of Sciences, 110(28):11232–11237, 2013. URL http://dx.doi.org/10.1073/pnas.1309533110.

- Manelli and Vincent [2006] A. M. Manelli and D. R. Vincent. Bundling as an optimal selling mechanism for a multiple-good monopolist. Journal of Economic Theory, 127(1):1 – 35, 2006. URL http://dx.doi.org/10.1016/j.jet.2005.08.007.

- Manelli and Vincent [2007] A. M. Manelli and D. R. Vincent. Multidimensional mechanism design: Revenue maximization and the multiple-good monopoly. Journal of Economic Theory, 137(1):153 – 185, 2007. URL http://dx.doi.org/10.1016/j.jet.2006.12.007.

- McAfee and McMillan [1988] R. P. McAfee and J. McMillan. Multidimensional incentive compatibility and mechanism design. Journal of Economic Theory, 46(2):335 – 354, 1988. URL http://dx.doi.org/10.1016/0022-0531(88)90135-4.

- Myerson [1981] R. B. Myerson. Optimal auction design. Mathematics of Operations Research, 6(1):58–73, 1981. URL http://dx.doi.org/10.1287/moor.6.1.58.

- Pycia [2006] M. Pycia. Stochastic vs deterministic mechanisms in multidimensional screening. PhD thesis, MIT, 2006. URL http://pycia.bol.ucla.edu/pycia-multidimensional-screening.pdf. Chapter 3.

- Rochet [1985] J.-C. Rochet. The taxation principle and multi-time hamilton-jacobi equations. Journal of Mathematical Economics, 14(2):113 – 128, 1985. URL http://dx.doi.org/10.1016/0304-4068(85)90015-1.

- Yao [2015] A. C.-C. Yao. An -to-1 bidder reduction for multi-item auctions and its applications. In Proceedings of the 26th Annual ACM-SIAM Symposium on Discrete Algorithms, pages 92–109, 2015. doi: 10.1137/1.9781611973730.8. URL http://arxiv.org/abs/1406.3278.

Appendix A Properties of Function of Section 4

Fix some positive integer . Then is an absolutely continuous function on with derivative

| (30) |

This means that is strictly increasing in and strictly decreasing in . Also we can compute:

From the above we can deduce that has a unique root in . In fact and for all and for all .

Furthermore, we know that the incomplete gamma function has the property

| (31) |

With the help of this we can see that

for any positive integer and , so