Non-Asymptotic Mean-Field Games

Abstract

Mean-field games have been studied under the assumption of very large number of players. For such large systems, the basic idea consists to approximate large games by a stylized game model with a continuum of players. The approach has been shown to be useful in some applications. However, the stylized game model with continuum of decision-makers is rarely observed in practice and the approximation proposed in the asymptotic regime is meaningless for networks with few entities. In this paper we propose a mean-field framework that is suitable not only for large systems but also for a small world with few number of entities. The applicability of the proposed framework is illustrated through various examples including dynamic auction with asymmetric valuation distributions, and spiteful bidders.

Keywords: Nonasymptotic, approximation, games with few decision-makers.

1 Introduction

Recently there have been renewed interests in large-scale interaction in several research disciplines, with its uses in wireless networks, big data, cyber-physical systems, financial markets, intelligent transportation systems, smart grid, crowd safety, social cloud networks and smarter cities.

In mathematical physics, most of models are analyzed in the asymptotic regime when the size of the system grows without bounds. As an example, the McKean-Vlasov model [13, 14, 16] for interacting particles is analyzed when the number of particles tends to infinity. Such an approach is referred to as mean field approach. The seminal works of Sznitman [19] in the 1980s and the more recent work of Kotolenez & Kurtz [18] show that the asymptotic system provides a good approximation of the finite system in the following sense: For any tolerance level there exists a population size such that for any the error gap between the solution of the infinite system and the system with size is at most Moreover, the work in [18] shows that the number is in order of for a class of smooth functions, where denotes the dimension of the space. Thus, for this current theory does not give an approximation that is meaningful.

In queueing theory, the number of customers is usually assumed to be large or follows a certain distribution with unbounded support (e.g., exponential, Poisson etc) and the buffer size (queue) can be infinite. However, many applications of interests such as airport boarding queues, supermarket queues, restaurant queue, iphone/ipad waiting queue involve a finite number of customers/travelers. Approximation by a continuum of decision-makers may not reflect the reality. For example the number of clients in the supermarket queue cannot exceed the size of available capacity of markets and there is a certain distance between the clients to be respected. In other words, human behaviors are not necessarily like standard fluid dynamics. In game theory, the rapidly emerging field of mean-field games [4] is addressing behavioral and algorithmic issues [1] for mathematical models with continuum of players. We refer the reader to [5] for a survey on (asymptotic) mean field games.

The classical works mentioned above provide rich mathematical foundations and equilibrium concepts in the asymptotic regime, but relatively little in the way of computational and representational insights that would allow for few number of players. Most of the mean-field game models consider a continuum of players, which seems not realistic in terms of most applications of interests. Below we give some limitations of the asymptotic mean-field approaches in engineering and in economics:

-

•

In wireless networks, the number of interacting nodes at the same slot in the same range is finite and currently the capacity/bandwidth of the system is limited. Therefore, a mean-field model for infinite capacity and infinite number of nodes is not plausible. The result of infinite system may not capture the real system with only few number of nodes.

-

•

In most of the current markets, the number of traders is finite. In that context it is well known that the Bayesian-Cournot game may not have an ex-post equilibrium whenever the number of traders is finite. However, the infinite game with continuum of traders has a pure (static mean-field) equilibrium. If our prediction is the ”mean-field equilibrium”, in what sense the (static) mean-field ex-post equilibrium [30] captures the finite system?

Our primarily goal in this article is to provide a simple and easy to check condition such that mean-field theory can be used for finite-scale which we call non-asymptotic mean-field approach. We investigate the nonasymptotic mean-field under two basic conditions. The first condition is indistinguishability (or interchangeability) of the payoff functions. The indistinguishability property is easy to verify. The indistinguishability assumption is implicitly used in the classical (static) mean-field analysis including the seminal works of Aumann 1964 [15], Selten 1970 [17], Schmeidler 1973. This assumption is also implicitly used in the dynamic version of mean-field games by Jovanovic & Rosenthal 1988[2], Benamou & Brenier 2000 [3] and Lasry & Lions 2007 [4]. The second condition is the (regularity) smoothness of the payoff functions. The regularity property is relatively easy to check.

Based on these two conditions, we present a simple approximation framework for finite horizon mean-field systems. The framework can be easily extended to infinite horizon case. The non-asymptotic mean field approach is based on a simple observation that the many effects of different actions cancel out when the payoff is indistinguishable. Nevertheless, it can lead to a significant simplification of mathematical mean-field models in finite regime. The approach presented here is non-asymptotic and is unrelated to the mean-field convergence that originates from law of large numbers (and its generalization to de Finetti-Hewitt-Savage functional mean-field convergence) in large populations. The non-asymptotic mean field approach holds even when there are only few players in a game, or few nodes in a network.

The idea presented here is inspired from the works in [21, 22, 20] on the so-called averaging principle. These previous works are limited to static and one-shot games. Here we use that idea not only for static games but also for dynamic mean-field games. One of the motivations of the asymptotic mean field game approach is that it may reduce the complexity analysis of large systems. The present work goes beyond that. We believe that if the complexity of the infinite system can be reduced easily then, the finite system can also be studied using a non-asymptotic mean-field approach.

In order to apply the mean-field approach to a system with arbitrary number of players, we shall exploit more the structure of objective function and the main assumption of the model which is the indistinguishability property, i.e., the performance index is unchanged if one permutes the label of the players. This is what we will do in this work. The aggregative structure of the problem and the indistinguishability property of the players are used to derive an error bound for any number of players. Interestingly, our result holds not only for large number of players but also for few number of players. For example, for players, there is no systematic way to apply the theory developed in the previous works [4, 15] but the non-asymptotic mean-field result presented here could be applied. The non-asymptotic mean-field result does not impose additional assumptions on the payoff function. We show that the indistinguishability property provides an accurate error bound for any system size. We show that the total equilibrium payoff with heterogeneous parameters can be approximated by the symmetric payoff where the symmetry is the respect to the mean of those parameters. These parameters can be a real number, vector, matrix or a infinite functional. The proof of the approximation error is essentially based on a Taylor expansion which cancels out the first order terms due to indistinguishability property.

We provide various examples where non-asymptotic mean-field interaction is required and the indistinguishability property could be exploited more efficiently. We present of queueing system with only few servers where closed-form expression of the waiting time is not available and the use of the present framework gives appropriate bounds. As second main example focuses on dynamic auctions with asymmetric bidders that can be self-interested, malicious or spiteful. In models of first-price auctions, when bidders are ex ante heterogeneous, deriving explicit equilibrium bid functions is an open issue. Due to the boundary-value problem nature of the equilibrium, numerical methods remain challenging issue. Recent theoretical research concerning asymmetric auctions have determined some qualitative properties these bid functions must satisfy when certain conditions are met. Here we propose an accurate approximation based on non-asymptotic mean field game approach and examine the relative expected payoffs of bidders and the seller revenue (which is indistinguishable) to decide whether the approximate solutions are consistent with theory.

The remainder of the paper is structured as follows. In Section 2 we present a mean field system with arbitrary number of interacting entities and propose a nonasymptotic static mean field framework. In Section 3 we extend our basic results in a dynamic setup. In Section 4 we present applications of nonasymptotic mean-field approach to collaborative effort game, approximation of queueing delay performance and computation of error bound of equilibrium bids in dynamic auction with asymmetric bidders.

We summarize some of the notations in Table 1.

| Symbol | Meaning |

|---|---|

| set of potential minor players | |

| cardinality of | |

| action space | |

| action of player | |

| global payoff function of the major player | |

| indicator function. | |

| strategy of player | |

| long-term payoff of player with horizon |

2 Mean-field system for arbitrary number of entities

Consider an interactive system with entities (players) consisting of generic minor players and one major player (called designer). The major player has a binary decision set. It consists to propose () or not to propose () a secondary game between the minors, thus its action set is Each of the minor players has to make a decision. Each decision variable of a minor player belongs to a Polish111A Polish space is a Separable topological space for which there exists a compatible metric such that is a complete metric space. Here, ”‘separable”’ means has a countable dense subset. space Each minor player has a payoff function where is the action of the major player. The major player has its own payoff function that could be the global performance of the minor players or another generic payoff. The payoff function of the major player is captured by a certain function which we call global payoff function.

The collection

defines a game in strategic-form (or normal form).

Since the action set of the major player reduces to a binary set, the decision will be driven by the comparison between and The payoff when the continuation game is not proposed can be fixed a certain constant. Therefore we focus on the analysis of the payoff which we denote by Similarly, is denoted simply by

2.1 Main Assumptions on the structure of payoff function

Assumption A0: Indistinguishability. We assume that the global payoff function is invariant by permuting the index of the minor players, i.e.,

for every permutation where

To verify , it suffices to check for pairwise interchangeability, i.e., permutation of any two of the coordinates. In mathematics, the indistinguishability property is sometimes referred as symmetric function, i.e., one whose value at any n-tuple of arguments is the same as its value at any permutation of that tuple.

Assumption A1: Smoothness. We assume that the objective function is (locally) twice differentiable with the respect to the variables.

It is important to notice that the assumption A0 can be easily checked by designers, engineers and non-specialists. In practice, A0 will result in functions that can be expressed in terms of the mean or other aggregative terms such as etc. Assumption A0 is implicitly used in [15, 17, 2, 4].

Our goal is provide a useful approximation and error bound for the global payoff in an equilibrium or in function of the parameters of the game.

2.2 Applicability of the payoff structure

These type of payoff functions have wide range of applications:

In economics and financial markets, the market price (of products, good, phones, laptops, etc) is influenced by the total demand and total supply. Examples include

-

•

Public good222Goods are called public if one person’s consumption of them does not preclude consumption by others. Typical examples are television programs and uncongested roads. provisioning with total payoff

-

•

Beauty contest games with payoff

-

•

Cournot oligopoly model with payoff

In queueing theory, the task completion of data centers or servers is influenced by the mean of how much the other data centers/servers can serve. In resource sharing problems, the utility/disutility of a player depends on the demand of the other players. Examples include cost sharing in coalitional system and capacity and bandwidth sharing in cloud networking. In wireless networks, the performance of a wireless node is influenced by the interference created by the other transmitters. In congestion control, the delay of a network depends on the aggregate (total) flow and the congestion level of the links/routes.

2.3 Approximation for static games

Next we provide the basic results that hold for both non-asymptotic and asymptotic static systems.

Result 1.

Assume that and hold. Then, the following results hold:

-

•

where and

(1) is the Dirac measure concentrated at the point

(2) -

•

The structure of the payoff function implies that the first order term in the Taylor expansion is cancelled out.

-

•

The cross-derivatives are independent of the labels:

Note that this theorem can be used for games with continuous action space as well as for games with discrete action space via mixed extensions. Examples of games that satisfy A0-A1 includes Prisoner Dilemma, Battle of Sex, Hawk-Dove, coordination games, anti-coordination games, minority games, matching pennies, etc.

Proof.

The first item is immediately proved by using the indistinguishability property in the definition of directional derivative. For the second item we use the first item and the relation (1). The first order derivative term is

| (3) | |||

| (4) |

The third item uses another exchange of positions between and ∎

Result 2.

Suppose that the payoff function satisfies the assumptions and Assume that is in a small neighborhood of the mean vector i.e., there is a small positive number which may depend on and the function such that then and

where

Result 3.

Assume that hold. Then, the explicit error bound for arbitrary number of players is is in order of

where

Proof.

Let be the second order error term.

On the other hand, one has

| (6) |

This implies that

Hence,

and we get the exact error for arbitrary system size. ∎

Remark 1.

In order to compute the error bound, one needs only , and The expression of the function is not required for vector with non-symmetric components. This allows us to provide an approximation result for unknown payoff function as illustrated in Subsection 4.2.

Remark 2.

If is bounded by and then

| (8) | ||||

| (9) |

In particular, if the finite regime has a solution in a certain sense, that is close to a vector with symmetric component then, the non-asymptotic mean-field approach provides automatically an solution for any number of players This is a non-asymptotic result in the sense that it holds for all range of system size Also, by choosing one gets an error bound in order of Note that can be very small even if is not large. For example, with players and , one gets an error bound in order of which is satisfactory in terms of computational accuracy.

3 Dynamic setup

In this section we provide very useful approximation results for dynamic interactive systems [31]. We consider a finite horizon with length

3.1 Non-asymptotic mean-field optimization

Consider a major player who controls also the action to be dictated to minor entities. Assume that the major player aims to achieve a certain goal with objective function given by the choice variables that the major player dictates to the minor entities. The objective function is where satisfies assumptions and is the choice variable at time Let be the sequence of mean actions and set

Result 4.

An explicit error bound for with arbitrary number of minor entities is given by

where

and and

See Result 5 below for a proof.

3.2 Non-asymptotic mean-field stochastic games

Consider a stochastic game [28, 23] with minor players and one major player (designer). Time is discrete. Time space is where Each player has its individual state which evolves according to a Markovian process. The action space a player depends on its current space, A pure strategy of player at time is a mapping from history up to to the current action space Denote by the strategy of player For The instantaneous payoff function of player is where is the state-action distribution, which satisfies the indistinguishability property with the respect to the other players. We assume that the payoff function is smooth.

The long-term payoff of player is

where is the terminal payoff. A strategy profile is a (Nash) equilibrium if no player can improve her payoff by unilateral deviation, i.e., for every player

Let be the value function of the bidder , i.e., it is the supremum, over all possible bidding strategies, of the expectation of the payoff starting from an initial state when the other players strategy profile is

Taking the expectation over the other players state, the recursive Bellman-Kolmogorov equation is given by

where and define the transition probabilities between the states.

Result 5.

Let where

and

Assume the state transition is continuous. Then the total term payoff is in order of for any

Due to the indistinguishability property one can use result 3 to at each time . Any time is bounded by

Based on this we derive a bound on the payoff

| (10) | |||

| (11) |

where is the final state when the average action is played by all the minor players and

and

Taking the absolute value, one obtains the following inequality:

| (12) | |||

| (13) | |||

| (14) |

where

Now, a small changes in the action may change the state, and hence the term is changed. Using the continuity of the state transition we take a uniform bound by considering the supremum:

| (15) | |||

| (16) |

For the same state, the error bound is Thus, the global error is bounded by

Since the above inequality holds for a generic symmetric vector which is the average action, it is in particular true when evaluated at a symmetric Nash equilibrium actions (if it exists) of the minor players.333The existence of symmetric equilibria in symmetric stochastic games uses standard point fixed existence condition. In that case, we recursively use the value iteration relation for each minor player

Summing up over at the optimal strategies of the minor players (if any) yields

Applying the local error bound and iterating times gives

4 Applications

4.1 Collaborative effort

Consider players. Each player can choose an action in the closed interval The geometric aggregate given by over In order to preserve the differentiability at the origin we consider the payoff as Then, the following statements hold:

-

•

We observe that the payoff functions are indistinguishable. The payoff functions satisfy which remains the same by interchanging the indexes.

-

•

The pure strategies effort and effort are equilibria. Moreover, is a strong-equilibrium (resilience to any deviation of any size ). Indeed,

If all the players do the maximum effort, i.e., then every player receives the maximum payoff and no player has incentive to deviate. This is clearly a pure Nash equilibrium. Suppose now that a subset of players (a coalition) deviates and jointly chooses an action that is different than , then the payoff of all the players is lower than In particular, the members of the coalition gets a lower payoff than . Since this analysis holds for any coalition of any size, the action profile is a Strong Nash equilibrium.

-

•

We define the analogue of the price of anarchy (PoA) for payoff-maximization problem as the ratio between the worse equilibrium payoff and the social optimum. If one of the players does effort (no effort) then the payoff of every player will be zero and no player can improve its payoff by unilateral deviation. This means that is a pure Nash equilibrium. Note that the equilibrium payoff at this equilibrium is the lowest possible payoff that a player can receive, i.e., is the worse equilibrium in terms of payoffs. Hence, and the ratio between the global optimum and the equilibrium payoff is which is infinite.

Clearly, the price of stability (the ratio between the best equilibrium payoff and the social optimum) is .

-

•

We say that a pure symmetric strategy is an evolutionarily stable strategy [29] if it is resilient by small perturbation as follows: For every there exists an such that

for all

We now show that the pure strategy effort (i.e., the action profile ) is not an Evolutionarily Stable Strategy. Indeed, if the left hand side of the above inequality is which is not strictly greater than

The non-asymptotic mean-field approach allows us to link the geometric mean with the arithmetic mean action. We remark that the geometric mean as a payoff, satisfies the indistinguishability property and it is smooth in the positive orthant. Here is the identity function because when the all the actions are identical, the geometric mean coincides with the arithmetic mean. In order to illustrate the error bound in the non-asymptotic mean field let consider two decision-makers. We expand the payoff for an asymmetric input level of size Let

| (17) | |||||

| (18) |

Here, Thus,

In particular, If and then and One has,

Now, if is near zero, i.e., and with then and Thus,

The above calculus illustrates that if the system is indistinguishable we can work directly with the mean of the mean-field with error where captures the asymmetry level of the system.

Next we illustrate the usefulness of our approximation of waiting time in a queueing system with multiple servers.

4.2 Queueing mean-field games

Consider servers and a system with arrival and service rate of for server Assume that the customers are indistinguishable in terms of performance index. Each customer will be assigned to one of the non-busy servers with a certain probability, (if any). If not, the customer joins a queue and will be in waiting list. Our goal is to investigate the delay, i.e., the propagation delay and the expected waiting time (WT) in the queue. Let the expected propagation delay to be Using [6], we determine the waiting time in the case of similar service rates . Let The transition rate (continuous time) is given by

The steady states are easily determined by setting

The probability that all servers are busy is

Hence, the waiting response time for the symmetric setup

The computation of in the asymmetric setting is highly complex and is still not well understood. The question is to know if non-asymptotic mean field approach can provide a useful approximation of it. To do so, we check the main assumptions and Clearly WT is regular (in for small ) and satisfies the indistinguishability property. Then, using nonasymptotic mean-field approach,

| (19) | ||||

| (20) |

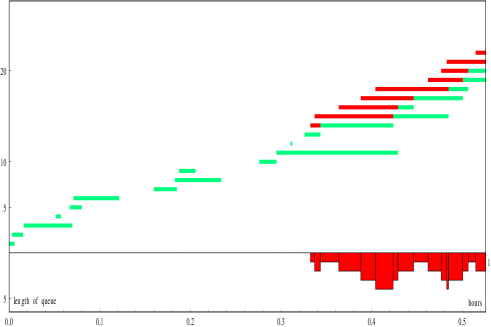

In Figure 1, we observe the following:

4.3 Auction with asymmetric bidders

4.3.1 Static setup

The theory of auctions as games of incomplete information originated in 1961 in the work of Vickrey. A seller has an object to sell. She adopted a first-price auction rule. Consider a first-price auction with asymmetric bidders. There are bidders for the object. Each bidder independently submit a single bid without seeing the others’ bids. If there is only one bidder with the highest bid, the object is sold to the bidder with biggest bid. The winner pays her bid, that is, the price is the highest (or first price bid). If there is more than one bidder, the object goes to each of these bidders with equal probability. The bidder has a valuation of the object. The random variable has a cumulative distribution function with support where A strategy of bidder is a mapping from valuation to a bid space: The risk-neutral payoff of bidder is Using the independence of the valuation , the risk-neutral payoff can written as The information structure of auction game is as follows. Each bidder knows its value, bid but not the valuation of the other bidders. Each bidder knows the valuation cumulative distribution of the others. The structure of the game is common knowledge. We are interested in the equilibria, equilibrium payoffs and revenue of the seller. Existence of equilibrium of auction games have been widely studied ([7, 8, 9]).

Clearly, no bidder would bid an amount that is greater than her value because of negative payoff. By fixing the bidding strategy of the others one has attempted to compute the best response correspondence. Any increase in the bid will decrease the gain but increase the probability of winning. This is a sort of tradeoff between the profit and the probability of winning.

We differentiate the function

In order to find an equilibrium one needs to solve Ordinary Differential Equations (ODEs) with boundary conditions.

| (21) |

| (22) |

The inverse of the function is the optimal strategy There is no need to mention that this is intractable even with small number of bidders. Even for three bidders we do not understand clearly how the solutions behave in function of

Why this is not a simple ODE problem?

Non-standard existence theorem is needed: We cannot apply the standard local existence and uniqueness theorem to the ODE with initial value (lowest bid) because by the right-hand-side terms in the ODEs are unbounded at In addition, the equilibrium satisfies but the term is unknown. Due to these difficulties, explicit solutions of (21) and (22) are not available.

Non-standard numerical method is needed:

Since explicit solutions are open issues, one may ask if it is possible to solve the problem numerically. According to the recent work in [21], the numerical implementation of the system (21) , (22) remains a challenging task. One of the well-known numerical methods consists to solve to find among the solutions of ODEs together with the initial conditions, that satisfy the highest equilibrium bid constraint. Such an approach is known as forward-shooting method. However, the forward-shooting method of Marshall et al. [24] do not converge to the solution due to approximation near with the derivative It has been shown in [21] that for the special case of power law (i.e. ), a dynamical system approach can be used with the change of variable

In the backward approach, one searches for the value of by solving Equation (21) backward in subject to the end condition and looking for the value of for which the initial value coincides with However, the standard backward-shooting method is inherently unstable, specially when the bids are near The authors in [25] showed that the backward-shooting method is unstable even in the symmetric case.

If all the functions are the same, and hence equal to then, we know from Vickrey 1961 that the symmetric equilibrium is

which is obtained as follows:

Instead of ODEs we have one ODE to solve. The ODE is

| (23) |

where the value distribution of the bidders. Using the bijection function and the fact that Hence, where is the strategy. This means that By simple integration between the minimum value and one gets

Hence,

Nonasymptotic mean field approach provides a useful error bound in this open problem

For asymmetric distribution we are able to get a precise error bound when the distribution are close to their arithmetic mean, the equilibrium strategies and payoffs can be approximated in a perturbed range. To do so, we use a non-asymptotic mean field approach over function space. First remark that the revenue of the seller, satisfies the indistinguishability property, since it is, up to a constant, the integral of the product We rewrite the function as where and

Using result 3, one gets

-

•

Good approximate of the asymmetric equilibrium strategies,

-

•

Equilibrium payoff with deviation order of

Example 1.

Note that the Optional Second Price auction is currently used in Doubleclick Ad Exchange. Examples of Ad exchanges are RightMedia, adBrite, OpenX, and DoubleClick. The idea is described as follows [12, 11]:

-

•

User visits the webpage of publisher that has, say, a single slot for ads.

-

•

Publisher contacts the exchange E with where is the minimum price p(w) is willing to take for the slot in and is the information about user that shares with

-

•

The exchange E contacts ad networks with , where is information about provided by , and is the information about provided by may be potentially different from .

-

•

Each ad network returns on behalf of its customers which are the advertisers; is its bid, that is, the maximum it is willing to pay for the slot in page and is the ad it wishes to be shown. Each ad network may have multiple advertisers. The ad networks may also choose not to return a bid.

-

•

Exchange determines a winner for the ad slot among all s and its price satisfying via an auction (first or second price).

-

•

Exchange returns winning ad to publisher p(w) and price to ad network

-

•

The publisher serves webpage with ad to user (the impression of ad ).

Note that from the click of the user to the impression of the ad there are many intermediary interactive processes. Auction is one them and an important one because it determines the winner ad network. While it is reasonable to consider large population of users over internet, the number of concurrent ad networks remains finite and there a room for non-asymptotic mean-field analysis for the revenue. As a user may click several times over webpages, the dynamic auction framework seems more realistic. We examine the dynamic auction in subsection 4.4.1.

4.3.2 Spiteful bidders

A player might be losing the auction of a long-term project. Yet she continues to participate in the auction because she wants to minimize the negative payoff on losing by making her competitor, who would win the auction, pay a high price for the win. This negative dependence of payoff on others’ surplus is referred to as spiteful behavior. Below we show how our nonasymptotic mean-field framework can be applied to that scenario.

A spiteful player maximizes the weighted difference of her own payoff and his competitors’ payoffs for all The payoff of a spiteful player is

| (24) |

Obviously, setting to zero yields a selfishness (whose payoff equals his exact profit) whereas defines a completely malicious player (jammer) whose only goal is to minimize the profit of other players. Note that for altruistic player we would be considering a payoff in the form

The payoff of a spiteful player is

| (25) | |||||

As mentioned above the main difficulty is that the private values distribution are asymmetric. Denote that by the equilibrium bid strategy. Even when bidders are selfish (), the above analysis shows that the explicit expression of is NOT a trivial task. However, for symmetric type distribution, and symmetric coefficient the payoff function reduces to

Using the fact that the derivative of with the respect to is given by The first order optimality condition yields to

In particular for uniform distribution over the Bayes Nash equilibrium strategy for spiteful player satisfies the ODE:

It is easy to check that is a solution of the above ODE. The symmetric equilibrium is increasing and convex with We now evaluate the revenue of the seller in equilibrium for .

| (26) | |||||

Now we compare the revenue with where

and

4.4 Fast algorithm for computing approximate equilibrium

We construct a fast algorithm for computing approximate equilibrium. Recall that the first optimality equation can be written as

Define the functional

We consider polynomial expansion of inverse-bid functions. The function is written in a flexible functional form

We truncate this polynomial to order and replace it in the first order optimality equation. Denote Taking in account boundary conditions, one gets that

has a minimum and the minimizer is the equilibrium inverse bid strategy Hence, it is reasonable to consider the functional when each of function belongs the subspace the set of polynomial with degree at most This is space with dimension The problem becomes

Remember that is the highest bid that is submitted in equilibrium. It is therefore an unknown. Thus, we add this into the optimization problem. Hence one has unknown variables to find. Using a grid decomposition of the domain with points inside, we arrive at a nonlinear least-squares algorithm for selecting and by solving which yields

The points on a grid will be chosen uniformly spaced, i.e.

Standard Newton-Gauss-Seidel methods provide a very fast convergence rate to a solution if the initial guess if appropriately chosen. However the choice of initial data and guess need to be conducted.

We propose a numerical scheme for optimal bidding strategies. First we solve the initial-value problem that starts at near but not equal to so that the denominator do not vanish. ODE starts at and moves forward. We fix the starting function to

where is the limit in of the derivative, , are positive constant. and is the equivalent fractional derivative approximation around To find the solution we take the intersection The solution is

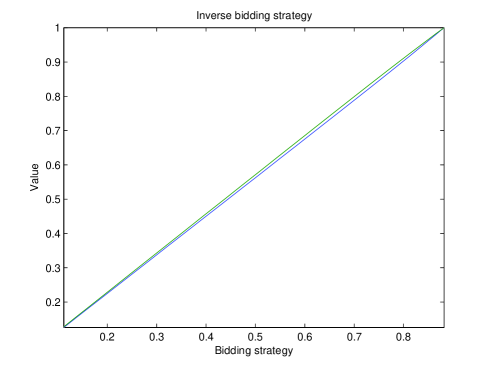

Figure 2 represents the inverse optimal bidding strategy for the cumulative distributions The x-axis represents the optimal bidding strategy and the y-axis is the inverse optimal bidding strategy of the two players. For that case We observe in Figure 2 that the second curve is around the first one plus

For we do not understand yet the behavior of . However, we are able to provide a useful approximation for asymmetric distribution in function of their deviation to the mean. Moreover the approximation holds for the revenue of the seller (auctioneer).

4.4.1 Dynamic auction with asymmetric bidders

We now explain how our framework can be extended in a dynamic setting. What is the motivation for dynamic auction? Currently a large proportion of internet users employ search engines to locate information [26]. For example, search engines are used to obtain an instantaneous selection of offers from various providers operating in the cyberspace. Internet auctions, on the other hand, connect potential sellers and buyers from different locations in a virtual auction. Buyers also often get multiple purchase opportunities over time. This is most obvious in the case of today’s online auction markets: eBay has auctions for physical goods closing every second, while Google’s Doubleclick and Microsoft’s Advertising Exchange trade online advertisements at a much faster rate. This creates the possibility for buyers to inter-temporally substitute, adjusting their current bids to account for the option value of waiting for future purchasing opportunities.

In sponsored search auctions, such as those run by Google (AdWords) or Bing (adCenter), a query to a search engine triggers an auction for positions on the page returned by the query. Advertisers bid for positions or slots, and successful bids result in ads being displayed alongside results to the query. The slots are ordered, where higher slots are more valuable. Under a dynamic auction mechanism for slots, an agent places a single bid, bids are ranked by weight and ranked bids determine the slot allocation. If an advert displayed in a slot is clicked, then the advertiser pays the price to be in the current slot, a Pay-Per-Click payment model.

In order to capture the practical observation, we model the problem as dynamic auction between buyers and sellers. We specially focus on the buyers side. Since measurement are done in discrete time unit, we start with a discrete time model. The work in [26] considered repeated second-price auctions under homogeneous valuation distributions and budget constraints. Most auctions involve bidders that are heterogeneous ex ante. For example ad networks may not have homogeneous valuation distribution for the advertisers. Therefore, Here we consider asymmetric distribution as well.

Time space is where is the length of the horizon. Since budget is limited for the entire day or month, we transform the long-term budget constraints into an iterative budget state equation for bidder

where is the remaining budget of bidder for the corresponding contract frame, is the total cost for the bid (if winner). The state is subject to positivity constraint: almost surely. It clearly limits the action space at time to the set of bids such that Let be the function The individual state bidder is the pair This generates a stochastic game with Markovian transition. Each bidder maximizes her long-term payoff given by

A history of a bidder is at time is a collection A bidding strategy of at time is a mapping from the history to the restricted bid space

The game is played as follows. At opportunity every player ,

-

•

realizes his current value distributed according to

-

•

submits a bid where denotes his bidding strategy at auction ;

-

•

updates his information set based on the results obtained in auction Specifically, he forms a set of beliefs about the distribution of the bidding profile of the players distributed according to

Let be the value function of the bidder , i.e., it is the supremum, over all possible bidding strategies, of the expectation of the payoff starting from an initial budget when the other bidder strategy profile is

Based on the classical Bellman optimality criterion, we immediately get the following result. The proof is therefore omitted.

Result 6.

Given the optimal strategy of a player satisfies

| (28) | |||||

where is the highest bid of the other players than

Let

Let Then the optimal bidding strategy is

The value iteration is given by

| (29) | |||||

For the symmetric setup we drop the index

Result 7 (Symmetric beliefs).

Given the optimal strategy of a generic player satisfies

| (30) | |||||

where is the highest bid of the other players than

Let This implies that the optimal bidding strategy is

The value iteration is given by

| (31) | |||||

Proof.

The proof follows as a corollary of result 6. ∎

To complete the value iteration system we choose a terminal payoff

Result 8 (Non-asymptotic mean-field).

Let where

and

Then, the long-term revenue of the seller is in order of for any

Proof.

The proof of the first statement is a direct extension of result 3 to the time space ∎

Remark 3.

As a consequence of the Result 8, if depends on and satisfies for some then, the error gap between the finite regime and the infinite regime in equilibrium is in order of which can be very small even for small but large

If then the error gap at time reduces to and hence the global error in is at most

Note that is a significant improvement of the mean-field approximation since the use of mean-field convergence à la de Finetti [18] gives a convergence order of The use of the indistinguishability property of the payoff function helps us to provide a more precise error.

4.5 Scaled auction problem

Using a scaling factor to the starting state (budget) and horizon, the value

has a certain limit when goes to Let Let Then, the value is solution of the following differential game

subject to

and Let be the instantaneous payoff from the above formulation. Introduce the Hamiltonian

The value satisfies the Hamilton-Jacobi-Bellman equation

4.6 Continuous time game with incomplete information

We consider a particular state dynamics given by drift , independent individual Brownian motion and a common Brownian motion . The instantaneous cost is Define the Hamiltonian as and let be an equilibrium cost value. Following [10], the value satisfies

where is the divergence operator. Considering minor players where the evolution of the measure is now replaced by the evolution of beliefs in a Bayesian mean field game, the long-term cost function of a player is which in order of where is the average measure (belief). Thus, the non-asymptotic mean field game approach allows us to understand the behavior of the equilibrium cost when the players have different beliefs (incomplete information game) which are near the average belief measure.

4.7 Extensions

4.7.1 Near-indistinguishable games

In this section we assume that the payoff functions are strictly positive and satisfy a near-indistinguishability property defined as follows:

Definition 1 (Non-scalable notion).

The game with payoffs is near-indistinguishable if it is indistinguishable for a certain small i.e. there exists an indistinguishable function such that

Definition 2 (Scalable notion).

The game with payoffs is scalable near-indistinguishable if it is scalable indistinguishable for a certain small i.e. there exists an indistinguishable function such that

The following result follows from the definition of near-indistinguishability.

Result 9.

Result 5 extends to near-indistinguishable case with an approximation given by

for the first type (non-scalable) and

where comes from the scalable near-indistinguishability error (second type, scalable notion) and is the heterogeneity gap between action profile and

4.7.2 Discussions

One of the main motivations to study mean field games is the possibility to reduce the high complexity of interactive dynamical systems into a low-complexity and easier to solve ones. However, the infinite mean field game system suggests a continuum of players may not be realistic in many cases of interests. Then, the question addressed in this paper is to know whether the mean field game ideas can be used in the finite regime. We show that the answer is positive for important classes of payoff functions.

An important statement is that if the asymptotic mean-field system can reduce the computational complexity then, the same analysis can be conducted in the finite regime. Moreover, the non-asymptotic mean field game model developed here does not require additional assumptions than the classical ones (namely A0 and A1) used in asymptotic mean field game theory. If the indistinguishability assumption fails but still the asymptotic mean field system is easily solvable then, one can classify the finite system too by class/and type and hence reduce into a game with less number of classes (than players) and in each class the indistinguishability property holds. We refer to such games as indistinguishability per class games. Interestingly our approximation results extends to near-indistinguishable games as well as to indistinguishable per class games.

5 Concluding remarks

We have presented a mean field framework where the indistinguishability property can be exploited to cover not only the asymptotic regime but also the non-asymptotic regime. In other words, our approximation is suitable not only for large systems but also for a small system with few players. The framework can be used to approximate unknown functions in heterogeneous systems, in optimization theory as well as in game theory.

This work suggests several paths for future research. First, the approach introduced here can be used in several applications, starting from other queueing and auctions formats, in particular to private information models where strategies are functions of types. Second, more progress needs to be done by considering a less restrictive action and belief spaces that are far from the mean of the mean field. The smoothness condition on the objective function may not be satisfied in practice. Finally, we would like to understand how large the deviation of the non-asymptotic result is compared to a symmetric vector (non-alignment level).

References

- [1] H. Tembine, Distributed Strategic Learning for Wireless Engineers, CRC Press/ Taylor & Francis, 496 pages, May 2012, ISBN: 9781439876442.

- [2] Jovanovic, Boyan and Rosenthal, Robert W. Anonymous sequential games, Journal of Mathematical Economics, Elsevier, vol. 17(1), pp. 77-87, February 1988.

- [3] J. D. Benamou, Y. Brenier, A computational fluid mechanics solution to the Monge-Kantorovich mass transfer problem. Numer. Math., vol. 84, pp. 375-393, 2000.

- [4] J.M. Lasry and P.L. Lions. Mean field games. Japan. J. Math., 2:229-260, 2007.

- [5] J.-M. Lasry, P.-L. Lions, and O. Gueant. Mean field games and applications. Paris-Princeton lectures on Mathematical Finance, 2010

- [6] L. Kleinrock. Queueing Systems, volume I and II. John Wiley and Sons, 1975.

- [7] E. S. Maskin and J. G. Riley. 2000. Asymmetric auctions. Rev. Econom. Stud. 67, 413-438.

- [8] Lebrun B: First-price auctions in the asymmetric n bidder case. International Economic Review 40:125-142, (1999)

- [9] Lebrun B: Uniqueness of the equilibrium in first-price auctions. Games and Economic Behavior 55:131-151, 2006.

- [10] P. L. Lions, Mean field games, Workshop mean-field games and applications, 2011.

- [11] Y. Mansour, S. Muthukrishnan and N. Nisan. Doubleclick Ad Exchange Auction, 2012.

- [12] S. Muthukrishnan. Ad exchanges: Research issues. In Proc. WINE. LNCS, New York, 1-12

- [13] M. Kac. Foundations of kinetic theory. Proc. Third Berkeley Symp. on Math. Statist. and Prob., 3:171-197, 1956.

- [14] D. A. Dawson. Critical dynamics and fluctuations for a mean-field model of cooperative behavior. Journal of Statistical Physics, 31:29-85, 1983.

- [15] Aumann R.: Markets with a continuum of traders. Econometrica, 32, 1964.

- [16] Villani C.: Optimal transport : old and new, Springer, Berlin, 2009.

- [17] Selten, R. Preispolitik der Mehrprodktenunternehmung in der statischen Theorie, Springer-Verlag. 1970

- [18] P. Kotolenez and T. Kurtz. Macroscopic limits for stochastic partial differential equations of McKean-Vlasov type. Probability theory and related fields, 146(1):189-222, 2010

- [19] A. S. Sznitman. Topics in propagation of chaos. In P.L. Hennequin, editor, Springer Verlag Lecture Notes in Mathematics 1464, Ecole d’Ete de Probabilites de Saint-Flour XI (1989), pages 165-251, 1991.

- [20] G. Fibich, A. Gavious, and E. Solan, Averaging principle for second-order approximation of heterogeneous models with homogeneous models, Proceedings of the National Academy of Sciences of the United States of America, doi: 10.1073/pnas.1206867109, PNAS, 2012.

- [21] G. Fibich and N. Gavish. Asymmetric first-price auctions: A dynamical systems approach, Mathematics of research operations, vol. 37 no. 2 219-243, May 2012.

- [22] Fibich, G. and Gavious, A., Asymmetric first-price auctions - a perturbation approach, Mathematics of Operational Research, 28, 836-852 (2003)

- [23] H. Tembine, J.-Y. Le Boudec, R. El Azouzi, E. Altman: Mean Field Asymptotics of Markov Decision Evolutionary Games and Teams, International Conference Game Theory for Networks, Istanbul,Turkey, 2009.

- [24] Marshall R. C., M. J. Meurer, J.-F. Richard, W. Stromquist. Numerical analysis of asymmetric first price auctions. Games Econom. Behav. 7(2) 193-220. 1994.

- [25] Fibich G., N. Gavish. Numerical simulations of asymmetric first-price auctions. Games Econom. Behav. 72(2) 479-495. 2011.

- [26] R. Gummadi P. Key, A. Proutiere, Repeated Auctions under Budget Constraints: Optimal bidding strategies and Equilibria, May 2012

- [27] Vickrey, W.: Counterspeculation, auctions, and competitive sealed tenders. J. Finance 16, 8-37.1961.

- [28] Shapley L. S.: Stochastic games. PNAS 39 (10): 1095-1100, 1953.

- [29] J. Maynard Smith and G. R. Price, The logic of animal conflict, Nature 246 (5427), 15-18, 1973.

- [30] H. Tembine, Mean field stochastic games, notes 2010.

- [31] D. Bauso, B. M. Dia, B. Djehiche, H. Tembine, R. Tempone, Mean-Field Games for Marriage, PLoS One, 2014, accepted and to appear.

Hamidou Tembine (S’06-M’10-SM’13) received his M.S. degree from Ecole Polytechnique and his Ph.D. degree from University of Avignon. His current research interests include evolutionary games, mean field stochastic games, distributed strategic learning and applications. In 2014 Tembine received the Outstanding Young Researcher Award from IEEE ComSoc. He was the recipient of 5 best paper awards and has co-authored two books. More details can be found at tembine.com