Detecting relevant changes in time series models

Abstract

Most of the literature on change-point analysis by means of hypothesis testing considers hypotheses of the form vs. , where and denote parameters of the process before and after a change point. This paper takes a different perspective and investigates the null hypotheses of no relevant changes, i.e. , where is an appropriate norm. This formulation of the testing problem is motivated by the fact that in many applications a modification of the statistical analysis might not be necessary, if the difference between the parameters before and after the change-point is small. A general approach to problems of this type is developed which is based on the CUSUM principle. For the asymptotic analysis weak convergence of the sequential empirical process has to be established under the alternative of non-stationarity, and it is shown that the resulting test statistic is asymptotically normal distributed. Several applications of the methodology are given including tests for relevant changes in the mean, variance, parameter in a linear regression model and distribution function among others. The finite sample properties of the new tests are investigated by means of a simulation study and illustrated by analyzing a data example from economics.

Keywords: change-point analysis, CUSUM, relevant changes, precise hypotheses, strong mixing, weak convergence under the alternative

AMS Subject Classification: 62M10, 62F05, 62G10

1 Introduction

The analysis of structural breaks in a sequence of random variables has a long history. Early work on this problem can be found in Page, (1954, 1955) who investigated quality control problems. Since these seminal papers numerous authors have worked on the problem of detecting structural breaks or change-points in various statistical models [see Chow, (1960), Brown et al., (1975), Krämer et al., (1988), among others]. Usually methodology is firstly developed for independent observations and – in a second step – extended to more complex dependent processes. Prominent examples of change-point analysis are the detection of instabilities in mean and variance [see Horváth et al., (1999) and Aue et al., 2009a among others]. These results have been extended to more complex regression models [see Andrews, (1993) and Bai and Perron, (1998)] and to change-point inference on the second order characteristics of a time series [see Berkes et al., 2009a , Wied et al., (2012) and Preuss et al., (2014)]. A rather extensive list of references can be found in the recent work of Aue and Horváth, (2013) who described how popular procedures investigated under the assumption of independent observations can be modified to analyse structural breaks in data exhibiting serial dependence.

A large portion of the literature attacks the problem of structural breaks by means of hypothesis testing instead of directly focusing on e.g. estimating the potential break points [compare the introduction in Jandhyala et al., (2013)]. Usually the hypothesis of no structural break is formulated as

| (1.1) |

where denotes a (not necessarily finite dimensional) parameter of the distribution of the random variable , such as the mean, variance, etc. The alternative is then formulated (in the simplest case of one structural break) as

| (1.2) |

where denotes the (unknown) location of the change-point. If the null hypothesis of structural breaks has been rejected, the location of the change has to be estimated [see Csörgo and Horváth, (1997) or Bai and Perron, (1998) among others] and the statistical analysis has to be modified to address the different stochastic properties before and after the change-point.

The present work is motivated by the observation that such a modification of the statistical analysis might not be necessary if the difference between the parameters before and after the change-point is rather small. For example, in risk management situations, one is interested in fitting a suitable model for forecasting Value at Risk from “uncontaminated data”, that means from data after the last change-point [see e.g. Wied, (2013)]. But in practice, small changes in the parameter are perhaps not very interesting because they do not yield large changes in the Value at Risk. The forecasting quality might only improve slightly, but this benefit could be negatively overcompensated by transaction costs. On the other hand, as an illustration with real interest rates at the end of this paper indicates a relevant difference can potentially be linked to significant real-world events. One could also think of an application to inflation rates in the sense that only “large” changes call for interventions of for example the European Central Bank.

With this point of view it might be more reasonable to replace the hypothesis (1.2) by the null hypothesis of no relevant structural break, that is

| (1.3) |

where and are the parameters before and after the change-point, denotes a (semi-)norm on the parameter space and is a pre-specified constant representing the “maximal” change accepted by statisticians without modifying the statistical analysis. Note that this formulation of the change-point problem avoids the consistency problem as mentioned in Berkson, (1938), that is: any consistent test will detect any arbitrary small change in the parameters if the sample size is sufficiently large. Moreover, the “classical” formulation of the change-point problem in formula (1.1) does not allow to control the type II error if the null hypothesis of no structural break cannot be rejected, and as a consequence the statistical uncertainty in the subsequent data analysis (under the assumption of stationarity) cannot be quantified. On the other hand, a decision of “no small structural” break at a controlled type I error can be easily achieved by interchanging the null hypothesis and alternative in (1.3). The relevance of testing hypotheses of the form (1.3), which are also called precise hypotheses in the literature [see Berger and Delampady, (1987)], has nowadays been widely recognized in various fields of statistical inference including medical, pharmaceutical, chemistry or environmental statistics [see Chow and Liu, (1992), Altman and Bland, (1995), Roy, (1997), McBride, (1999)]. On the other hand – to our best knowledge – the problem of testing for relevant structural breaks has not been discussed in the literature so far.

In this paper we present a general approach to address this problem, which is based on the CUSUM principle. The basic ideas are illustrated in Section 2 for the problem of detecting a relevant change in the mean of a multivariate sequence of independent observations. The general methodology is introduced in Section 3 and is applicable to several other situations including changes in the variance, the parameter in regression models and changes in the distribution function (the nonparametric change-point problem). It turns out that - in contrast to the classical change-point problem - testing relevant hypotheses of the type (1.3) requires results on the weak convergence of the sequential empirical process under non-stationarity (more precisely under the alternative ), which - to our best knowledge - have not been developed so far. The reference which is most similar in spirit to investigations of this type is Zhou, (2013), who considered the asymptotic properties of tests for the classical hypothesis of a change in the mean, i.e. , under local stationarity. The present paper takes a different and more general perspective using weak convergence of the sequential empirical process in the case . These asymptotic properties depend sensitively on the dependence structure of the basic time series and are developed in Section 4 for the concept of strong mixing triangular arrays [see Withers, (1975) or Liebscher, (1996)]. Although the analysis of the sequential process under non-stationarities of the type (1.2) is very complicated, the resulting test statistics for the hypothesis of no relevant structural break have a very simple asymptotic distribution, namely a normal distribution. Consequently, statistical analysis can be performed estimating a variance and using quantiles of the standard normal distribution. In Section 5 we illustrate the methodology and develop tests for the hypothesis (1.3) of a relevant change in the mean, variance, parameters in a linear regression model and distribution function. In particular, we also consider the situation of testing for a change in the mean with possibly simultaneously changing variance, which occurs frequently in applications. Note that none of the classical change-point tests are able to address this problem. In fact it was pointed out by Zhou, (2013) that the classical CUSUM approach and similar methods are not pivotal in this case leading to severe biased testing results. Section 6 presents some finite sample evidence for some of the testing problems revealing appealing size and power properties and Section 7 gives an illustration to a data example from economics.

2 Relevant changes in the mean - motivation

This section serves as a motivation for the general approach discussed in Section 3 and for illustration purposes we consider independent -dimensional random variables with common positive definite variance , such that for some unknown

The case of a variance simultaneously changing with the mean will be discussed in Section 5.1. We are interested in the problem of testing for a relevant change in the mean, that is

| (2.1) |

where denotes the Euclidean norm on . For this purpose we consider the CUSUM statistic defined by

and note that a straightforward computation gives

If we have

where . A similar calculation for the case yields

Consequently, we obtain

and therefore it is reasonable to consider the statistic

as an estimator of the distance (a bias correction addressing for the term will be discussed later). The following result specifies the asymptotic properties of this statistic. Throughout this paper the symbol means weak convergence in the appropriate space under consideration.

Theorem 2.1.

For any we have as

| (2.3) |

where the asymptotic variance is given by

| (2.4) |

Proof. We start calculating the covariance Cov using the decomposition

where

For this purpose we first assume that and note that Cov in this case. Moreover, the remaining covariances are obtained as follows

which gives if . A similar calculation for the case finally yields

It can be shown (note that for illustration purposes the random variables are assumed to be independent and a corresponding statement under the assumption of a strong mixing process is given in Section 4) that an appropriately standardized version of the process converges weakly, that is

where and denotes a vector of independent Brownian bridges on the interval . This gives for the random variable in (2.3)

It is well known that the distribution on the right hand side is a centered normal distribution with variance.

and it follows by a straightforward but tedious calculation that this expression is given in (2.4).

The test statistic for the hypothesis (2.1) is finally defined as

where and are consistent estimators of and , respectively. Note that this definition corrects for the additional bias in (2) which is asymptotically negligible. The null hypothesis of no relevant change-point is finally rejected, whenever

| (2.5) |

where is the -quantile of the standard normal distribution and is an appropriate estimator of . An estimator of the change-point can be obtained by the argmax-principle, that is

| (2.6) |

[see Carlstein, (1988)]. For the estimation of the residual variance we denote by

| (2.7) |

the estimates of the mean “before” and “after” the change-point and define a variance estimator by

| (2.8) |

This yields

| (2.9) |

as an estimation of , where . An alternative estimator could be obtained by replacing the estimator in (2.9) by

It will be shown in Section 3.3 that the test defined by (2.5) is consistent and has asymptotic level .

3 Testing for relevant changes - a general approach

3.1 General formulation of the problem

Let denote -dimensional random variables such that

| (3.1) |

where and denote continuous distribution functions before and after the change-point. Let denote a (possibly infinite dimensional) Hilbert space with (semi-)norm , define as the set of all bounded functions and consider . We denote by

| (3.4) |

a given function defining the parameter of interest. Typical examples include the mean () or the distribution function (). We are interested in testing the hypothesis of no relevant change in the functional , that is

| (3.5) |

where is a pre-specified constant. If with , then denotes always the Euclidean norm, if not specified otherwise.

Our general approach will be based on an estimator of the distance by a CUSUM type statistic. For this purpose we assume for a moment linearity of the functional in (3.4), that is

| (3.6) |

for all . We introduce the statistic

| (3.7) |

where , and the inequality is understood component-wise. Note that for fixed the function is a distribution function and that a straightforward calculation yields

| (3.8) |

We also introduce the function

| (3.9) |

and note that vanishes on if and only if . If

denotes the (linear) operator defined by

we obtain from (3.6) and (3.9) for the function the representation

| (3.10) |

Consequently, the norm of this function is given by

| (3.11) |

which can be used as the basis for estimating the distance between the parameters and . Before we explain the construction of this estimate in more detail, we “remove” assumption (3.6) and consider more general nonlinear functionals.

In this case the situation is slightly more complicated and we assume throughout this paper that there exists a mapping

| (3.12) |

such that the difference between and can be expressed as a functional of the function in (3.8), that is

| (3.13) |

For linear functionals such a representation is obvious as shown in the preceding paragraph. Other examples where assumption (3.13) is satisfied include linear regression models or the detection of relevant changes in the correlation and will be discussed in Section 5.3 and 5.4.

For the construction of an estimate of we note that it follows by similar arguments as given in Section 2 that the function satisfies

| (3.14) |

Observing (3.11) and (3.14) we see that the distance

| (3.15) |

between the parameters and can be expressed as a functional of , which can easily be estimated by a sequential empirical process defined in (3.7). The null hypothesis (3.5) is then rejected for large values of this estimator. In the following discussion we will derive the asymptotic properties of this estimator, which can be used for the calculation of critical values for a test of the null hypothesis (3.5) of no relevant change.

3.2 Estimating

In order to estimate the distance we recall the definition of the sequential empirical process in (3.7) and its asymptotic expectation defined in (3.8). Observing assumption (3.13) we consider the processes

| (3.16) |

and

| (3.17) |

Note that and are and -valued processes. If we make the following assumption

| (3.18) |

where means weak convergence in and is a centered, -dimensional Gaussian process with covariance kernel

Remark 3.1.

Note that the weak convergence results of the type (3.18) have been investigated for numerous types of stationary stochastic processes [see Horváth et al., (1999), Aue et al., 2009a or Dehling et al., (2013)]. However, the detection of relevant change-points by testing hypothesis of the form (3.5) requires weak convergence results in the

non-stationary situation (3.1), for which – to our best knowledge – no results are available. In particular, as it will be demonstrated in Section 4, the distribution of the limiting processes

depends on the distribution functions , and the change-point in a complicated way. Only

in the case it simplifies to the standard situation, which is usually considered in change-point analysis.

Intuitively many results for stationary processes mentioned in the cited references should also be available in the non-standard situation (3.1), but

the limiting distribution is more complicated and

this has to be worked out for each case under consideration. In Section 4 we illustrate the general arguments for this generalization in the case of a strong mixing process (satisfying (3.1)).

In the same section similar results will be established for the sequential process , that is

| (3.19) |

where denotes a centered -dimensional Gaussian process on with covariance kernel

Consequently, if the functional in (3.12) is (for example) Hadamard differentiable, weak convergence of the process is a consequence of the representation (3.16) and (3.19). Some details are given in Remark 3.2 below. However, many functionals of interest in change-point analysis (such as the mean or variance) do not satisfy this property, and for this reason we also state (3.18) as a basic assumption, which has to be checked in concrete applications. An example where (3.19) can be used directly consists in the problem of detecting a relevant change in the distribution function and will be given in Section 5.5.

Theorem 3.1.

If and the assumptions (3.18) and (3.6) are satisfied, then

where is defined in (3.11) and . Here the asymptotic variance is given by

| (3.20) |

where the matrix is defined by

| (3.21) |

Proof. Let denote the inner product on . Observing the representation

it follows from assumption (3.18) that

Now the continuous mapping theorem yields

and standard arguments show that the random variable on the right hand side is normally distributed with mean and variance

Remark 3.2.

A similar statement can be derived under the assumption (3.19) if the function in (3.13) is Hadamard differentiable at the point (tangentially to an appropriate subset, if necessary). In this case it follows from (3.19) and the same arguments as given in the proof of Theorem 3.1 that

where denotes the Hadamard derivative of and is the interproduct on the (not necessarily finite dimensional) Hilbert space . The details are omitted for the sake of brevity.

3.3 Testing for relevant changes

It follows from Theorem 3.1 and (3.14) that

| (3.22) |

where the asymptotic variance is given by

| (3.23) |

and is defined in (3.20). In the following discussion let denote a consistent estimator of the change-point , such that

| (3.24) |

whenever and

| (3.25) |

whenever , where denotes a -valued random variable. Typically the argmax-estimator satisfies (3.24) and (3.25), where for some Gaussian process [for a recent review on the relevant literature see Jandhyala et al., (2013)]. Consequently, if is an estimator of , we obtain by an estimate of the asymptotic variance in (3.23). This yields for the statistic

the weak convergence

| (3.26) |

whenever , while

| (3.27) |

if .

Theorem 3.2.

Proof. Define and assume that the null hypothesis holds. If it follows from (3.26) that the probability of rejection by the decision rule (3.28) is given by

Similarly, if (which implies , we obtain from (3.27) and (3.25)

| (3.30) |

Consequently, the test, which rejects the null hypothesis whenever (3.28) is satisfied, is an asymptotic level -test. On the other hand, under the alternative , a similar argument shows that , which proves consistency.

The choice of the estimators and depends on specific examples under consideration and will be discussed in more detail in Section 6, where we illustrate the methodology by several examples.

4 Strong mixing processes

Assumptions (3.18) and (3.19) are crucial for the asymptotic analysis presented in Sections 3.2 and 3.3. If (i.e. there exists no structural break) they have been verified in several situations. For example, Deo, (1973) proved that

| (4.1) |

if the process is stationary and strong mixing with mixing coefficients converging sufficiently fast to , that is for some . Here denotes a Gaussian process with covariance structure

These results can be extended to other concepts of dependency and to the sequential empirical process defined in (3.7), and for some recent results in this direction we refer to the work of Berkes et al., 2009b and Dehling et al., (2013).

However, these results are not applicable anymore in the problem of detecting relevant change-points by means of a test for the hypothesis (1.3), because statements of the form (3.18) or (3.19) are required for the case in order to obtain the asymptotic distribution in Theorem 3.1. In this case the process under consideration is not stationary anymore. Additional difficulties appear because one has to work under the assumption of a triangular array, and it will be necessary to reflect this fact in our notation throughout this section, that is

| (4.2) |

where and are the distribution functions before and after the change-point. We assume throughout this section that and are continuous. In principle, it should be possible to extend the results for the case to the case for most of the commonly used dependency concepts, but a general discussion is very complicated and beyond the scope of the present paper. For these reasons we restrict ourselves to the case of strong mixing triangular arrays in the subsequent discussion and investigate assumptions (3.18) and (3.19) in this case. Other concepts of dependency could be treated similarly.

To be precise, consider the triangular array in (4.2) and define for the -field generated by the random variable . We denote by

the strong mixing coefficients of the triangular array and assume that for some

| (4.3) |

as . Moreover, for let denote strictly stationary processes, such that for each

| (4.4) | |||||

| (4.5) |

The interpretation of this assumption is as follows: there exist two regimes and and the process under consideration switches from one regime to the other. The following statement specifies the weak convergence of the sequential empirical process

| (4.6) |

Theorem 4.1.

Let denote a triangular array of strong mixing random variables of the form (4.2), such that (4.3), (4.4) and (4.5) hold, then a standardized version of the process converges weakly in , that is

Here is defined in (3.8), denotes a centered Gaussian process with covariance kernel

| (4.7) |

and the kernels and are defined by

| (4.8) |

Proof. Recalling the definition of and in (4.6) and (3.8), respectively, we obtain the decomposition

| (4.9) |

uniformly with respect to , where the processes and are defined by

and the random variables are defined by

| (4.10) |

Observing (4.4) and (4.5) it then follows from Bücher, (2014) that

where and are two centered independent Gaussian processes with covariance structure

| (4.13) |

Consequently, the processes and its sum are asymptotically tight [see Section 1.5 in van der Vaart and Wellner, (1996)], and in order to prove weak convergence of the process it remains to establish the weak convergence of the finite dimensional distributions. For this purpose we use the Crámer-Wold device and show for all

| (4.14) |

where is the Gaussian process defined in Theorem 4.1. For the sake of a clear exposition we restrict ourselves to the case and begin with a calculation of the covariance of and . If we can use the same arguments as in Bücher, (2014) and obtain

Similarly, if we have

Finally, if we have by assumption (4.3)

where the random variables are defined in (4.10). If we use a sequence satisfying and and obtain by the same arguments

Using similar arguments for the remaining cases it follows from assumptions (4.4) and (4.5) that

where denotes the centered Gaussian process defined in Theorem 4.1.

In order to prove asymptotic normality of the statistic we introduce the notation

where the random variably are defined by

and we use a central limit theorem for triangular arrays of strong mixing random variables [see Theorem 2.1 in Liebscher, (1996), where ]. For this purpose we note that it follows from the discussion in the previous paragraph that and that it is easy to see that

Similarly, it follows that the condition

of Theorem 2.1 in Liebscher, (1996) is also satisfied. Therefore this result shows that

where the asymptotic variance is defined in (LABEL:limvar). This proves the convergence of the finite dimensional distributions and completes the proof of Theorem 4.1.

As pointed out, there exist many cases where assumption (3.19) (as established by Theorem 4.1 for strong mixing triangular arrays) is not satisfied. In this case it is necessary to prove (3.18) for the specific functional under consideration. A general statement can be obtained if the functional of interest is linear. The proof is obtained by similar arguments as given for Theorem 4.1 and therefore omitted.

Theorem 4.2.

5 Applications: detecting relevant change-points

In this section we discuss several examples to illustrate the theory developed in Section 3. In particular, we concentrate on the detection of relevant changes in the mean, variance, coefficients in linear regression, correlation and a relevant change in the distribution itself. In order to be precise we assume that the assumptions of Theorem 4.1 and 4.2 in Section 4 are satisfied. Similar results can be derived for alternative dependency concepts.

5.1 Relevant changes in the mean

The most prominent example of change-point analysis in model (3.1) consists in the investigation of structural breaks in the mean

While the “classical” change-point problem versus has been investigated by numerous authors [see Csörgo and Horváth, (1997) for a survey of methods for the independent case and Aue and Horváth, (2013) for an extension to dependent data], we did not find any references on testing the hypotheses (2.1) of relevant change-points in the mean. Note that in contrast to the discussion of Section 2 and to most of the literature, we do not assume that the stochastic features of the process besides the mean coincide before and after the breakpoint. In particular, the variances or more generally the dependency structures before and after the change-point can be different, although the means and are “close”, i.e. . Theorem 4.2 establishes condition (3.18), where the covariance kernel of the limiting process is defined in (4.2) and (4.19) with . Consequently, the corresponding asymptotic variance in (3.22) is given by

| (5.1) | |||||

where and are defined in Theorem 4.2 with .

5.2 Structural breaks in the variance

Following Aue et al., 2009a we consider a triangular array of -dimensional random variables with constant mean and investigate the problem of detecting a relevant change in the variance. This means that the functional of interest is given by

where is the distribution function. Note that in contrast to the mean discussed in Section 5.1 this functional is not linear. However, if and denote the common mean and the variance before and after the break, respectively, a straightforward calculation yields the representation

where

Consequently, assumption (3.13) is satisfied and we obtain from Theorem 4.2 the weak convergence of the process

to a centered Gaussian process with covariance kernel (4.2) and (4.19), where

A straightforward but tedious calculation shows that the limiting variance in (3.22) is given by

where and are defined in Theorem 4.2 with .

5.3 Linear regression models

Early results on change-point inference in linear regression models can be found in Kim and Siegmund, (1989), Hansen, (1992), Andrews, (1993), Kim and Cai, (1993) and Andrews et al., (1996). More recent work on this problem has been done by Chen et al., (2013) and Nosek and Skzutnika, (2013), among others. In this section we introduce the problem of testing for relevant changes in the parameters of a regression model. To be precise, we consider the common linear regression model

where and are independent strictly stationary processes and

In the notation of Section 3 and 4 we have

where and are the joint distribution functions before and after the change-point, respectively. Note that the marginal distribution of the predictor satisfies by these assumptions.

In order to construct tests for the null hypothesis of no relevant change

| (5.2) |

we assume that the matrix

| (5.3) |

is non-singular and note that the parameter can be represented as

| (5.4) |

However, due to the nonlinearity of this representation, it is more difficult to derive a representation of the form (3.13). For this purpose consider the functional

defined on the set of all bounded functions for which the integrals exist (for each ) and which satisfy . The analog of the quantity (3.8) is given by

and it follows by a straightforward calculation that

Assume for a moment that the matrix in (5.3) is known, then we obtain from Theorem 4.2 that the process

converges weakly to a centered Gaussian process, that is

where , is defined in (5.3) and is a centered Gaussian process with covariance kernel defined by (4.2) and (4.19), where

| (5.6) |

and denote the components of the process considered in Theorem 4.1, that is

However, the estimation of the matrix yields an additional effect, which makes the asymptotic analysis of the process substantially more complicated. It is already visible in the decomposition

where denotes the common estimate of the matrix defined in (5.3). In order to explain this effect in more detail we restrict ourselves to one-dimensional models. The general case can be treated exactly in the same way with some extra matrix algebra. To be precise, define the empirical process , where

Similar arguments as given in Section 4 show

| (5.7) |

where , and denotes a two-dimensional centered Gaussian process with covariance matrix

where and the matrices and are defined by

Now an application of the functional Delta-method [see van der Vaart and Wellner, (1996)] yields

where and denote the components of the limiting process in (5.7). A tedious calculation yields for the covariance structure of this process

Observing (5.3) we have by similar arguments as given in Section 2 that

where the asymptotic variance is given by

| (5.9) | |||||

From these considerations a test for the hypothesis of a relevant change in the parameters of the linear regression model can easily be constructed as indicated in Section 2 and 3 with

| (5.10) |

see Section 6.2 for details, where we also investigate the finite sample properties of the test for the hypotheses (5.2).

5.4 Relevant changes in correlation

Let denote two-dimensional random variables with existing second moments. Following Wied et al., (2012) we assume that and we are interested in a relevant change-point in the correlation, that is

where for some

| (5.11) |

and

denotes the correlation of the distribution function . Consider the functional

defined on the set of functions such that all integrals exist. If and denote the distributions of the two-dimensional vector before and after the change-point and

then a straightforward but tedious calculation yields a representation of the form (3.13), that is

Recall the definition , and define , then it follows that

| (5.12) |

where

and

| (5.13) |

denote the common estimators of the moments and . Similar arguments as given in Section 4 yield

where is a centered Gaussian process with covariance structure

with

and we have assumed that there exist strictly stationary processes , such that for each

Now weak convergence of the process follows by the functional Delta-method and a tedious calculation using the same arguments as in Section 5.3. The details are omitted for the sake of brevity.

5.5 Relevant changes in the distribution

In order to investigate the problem of a relevant change with respect to the distribution in a univariate sequence of the form (4.2) we consider the distance

| (5.15) |

on the set of all distribution functions with existing first moment. In this case the null hypothesis of no relevant change in the distribution function is formulated as

| (5.16) |

In order to estimate the distance we define as the set of all functions , such that for each the integral

| (5.17) |

exists (for all ). Note that this set contains the set of all functions of the form defined in (3.8), such that and have moments of order one [see Székely and Rizzo, (2005), p. 73]. We consider the functional defined by , then

| (5.18) |

In this case it follows from Theorem 4.1 that assumption (3.19) is satisfied, and as a consequence we obtain

| (5.19) |

where the limiting process is defined by

and the covariance kernel of this process is given by

Defining

and observing the representation

we have

| (5.20) |

where is the limiting process defined in (5.19). Note that the right hand side of (5.20) is normal distributed with variance

Consequently, we obtain

and the test for the hypotheses of relevant change-points can be constructed following the arguments given in Section 3.3 with . The finite sample properties of the corresponding test for the hypothesis (5.15) will be investigated in Section 6.

6 Finite sample properties

In this section, we illustrate the application of the new testing procedure and provide some finite sample evidence. For the sake of brevity we investigate three cases: the detection of relevant changes in the mean, parameter of a linear regression model and a relevant change in the distribution function. Similar results can be obtained for the other testing problems considered in Section 5 but are not displayed here for the sake of brevity. In all examples under consideration, we performed replications of the test (3.28) at significance level . Note that the structure of this test is the same in all cases under consideration, but the estimation of the change-point and the asymptotic variance differ from example to example and the details will be explained below. We also note that it follows from the proof of Theorem 3.2 that the power of the test (3.28) is approximately given by

| (6.1) |

Similarly, we obtain a formula for the -value of the test, that is

| (6.2) |

where is the distribution function of the standard normal distribution. These formulas will be helpful to understand some properties of the test (3.28).

6.1 Testing for relevant changes in the mean

At first, we look at the test for changes in the mean as discussed in Section 5.1 focussing on a one-dimensional sample . In this case the test statistic is obtained as

where and . The null hypothesis of no relevant change in the mean with potentially different variances before and after the change-point is rejected whenever (3.28) holds. The estimator of the asymptotic variance is obtained from formula (5.1) in Section 5.1 by replacing the unknown quantities and by their empirical counterparts , and [see formula (2.7) and (2.8) in Section 2]. For the estimation of the long-run variances and in (5.1) one has to account for potential serial dependence, and we consider a kernel-based estimator as described in Andrews, (1991) in the two different subsamples. More precisely we choose the Bartlett kernel and a data-adaptive bandwidth

with the estimated AR parameter for the sample before the estimated break point (note that this choice is optimal for an process). The estimator of is then defined by

with and an analogue expression is used for the estimation of the quantity in (5.1). The choice of the bandwidth has no big impact in the case of serial independence, but reduces size distortions if there is high serial dependence.

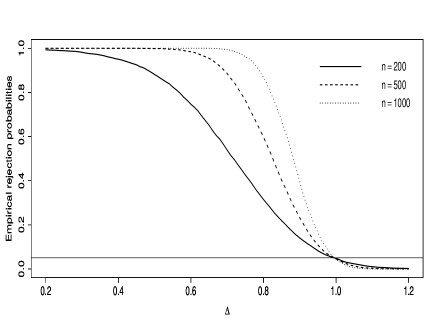

In Figure 1 we display the rejection probabilities of the test (3.28) for sample sizes

and independent normally distributed random variables with mean in the first half and mean in the second half of the sample, i.e. .

The variance is constant and equal to . The left part of Figure 1 presents the empirical rejection probabilities of the test (3.28) for fixed , where

the parameter , which defines the size of a relevant change in the hypothesis (2.1), varies in the interval . We observe that the power of the test decreases in as predicted by

formula (6.1).

For , the power is approximately , which shows that the test keeps its nominal level.

The right part of Figure 1 displays the power curve of the test (3.28) for the same sample sizes and , where the “true” difference varies in the interval . As expected, the power curve is U-shaped with a minimum at

[note that the power of the test converges to zero in this case - see formula (3.30) in the proof of Theorem 3.2]. Again the nominal level is well approximated at the boundary of the null hypothesis,

that is . We also observe that the type I error is much smaller inside the interval .

Figures as displayed in the left part of Figure 1 are useful to obtain the minimal size of the parameter in (2.1) such that the null hypothesis of no relevant change of size is rejected at controlled type I error, while the figure in the right part directly display the power function of the test (3.28). Both types essentially provide the same information and for the sake of brevity we focus in the following discussion only on the power function. Moreover, due to the obvious symmetry, we just present the values for .

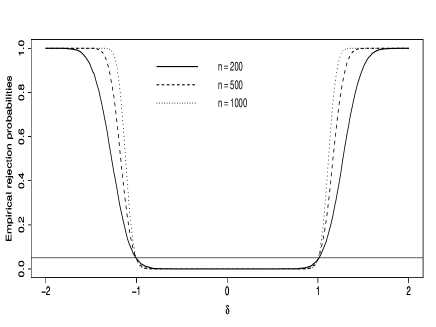

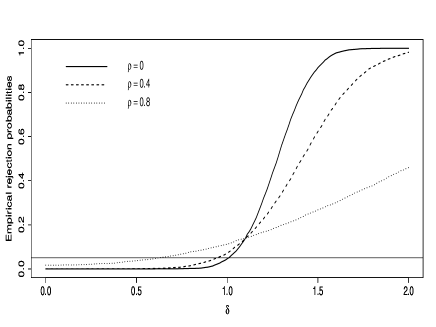

In Figure 2 we analyze the effect of changes in the variances on the testing procedure, where the sample size is fixed as and the setting is the same as in Figure 1. The left part of the figure shows the power of the test (3.28) for the null hypothesis of no relevant change in the mean, where the variances are the same before and after the change-point and given by . We observe that the approximation of the nominal level is rather accurate at the point . Moreover, the rejection probabilities decrease in . Note that there is essentially no power for because in this case the variance is dominating the mean and it is difficult to distinguish between signal and mean. Moreover, in this case the level of the test is not very well approximated, which is due to the fact that it is difficult to estimate the change-point accurately under a large signal to noise ratio.

In the right part of Figure 2 we display the effect of changing variances in the same setting as in the left part where the variance in the first half is equal to and in the second half given by . We do not observe substantial differences with respect tot the quality of the approximation of the nominal level. Compared to the case of constant variances the power is in general lower for and higher for . These empirical findings reflect the asymptotic theory, because the asymptotic variance of the estimator is a linear and increasing function of and [see formula (5.1)] and it follows from (6.1) that the power of the test (3.28) is decreasing with this variance.

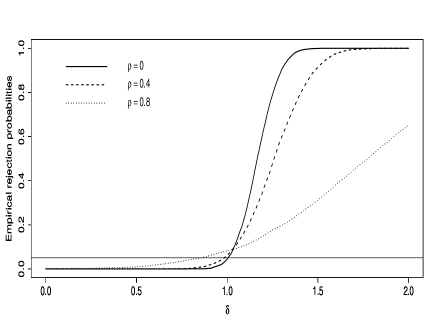

Finally, we investigate the effect of serial dependence on the test (3.28) for the null hypothesis of no relevant change in the the mean. For this purpose we generate and realizations of an process with AR parameter , mean zero and standard normal distributed innovations using the R-function arima.sim. Note that such a process fulfills a strong mixing condition with mixing coefficients that decay exponentially [see for example Doukhan, (1994), Theorem 6, p. 99.]. After that, we add to the last realizations. Figure 3 shows the serial dependence has an impact on the quality of the approximation of the nominal level if the sample size is . Moreover, the power decreases with increasing correlation. These properties have also been observed by other authors in the context of CUSUM-type testing procedures [see Xiao and Phillips, (2002) and Aue et al., 2009b ]. Moreover, using the asymptotic theory from Section 5 we can also give a precise explanation of these observations. For the AR(1) model under consideration the quantities in (5.1) are given by . Consequently the asymptotic variance is increasing with and by formula (6.1) the power is decreasing.

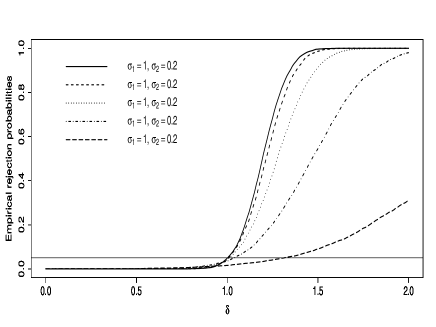

6.2 Testing for relevant changes in the parameters of a regression

In this section we investigate the problem of testing for a relevant change in the slope parameter of the regression model

based on a sample of independent bivariate random vectors . The test statistic is defined as

where and . The null hypothesis (5.2) of no relevant change in the parameter is rejected whenever (3.28) is satisfied, where the estimator of the asymptotic variance can be obtained from formula (5.9) and (5.10) in Section 5.3. Here we replace the unknown quantities and by , , the OLS-estimates and from the two subsamples before and after the estimated change-point and the estimators

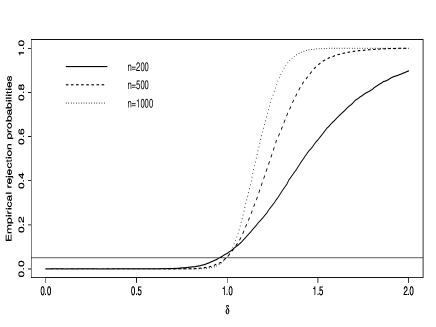

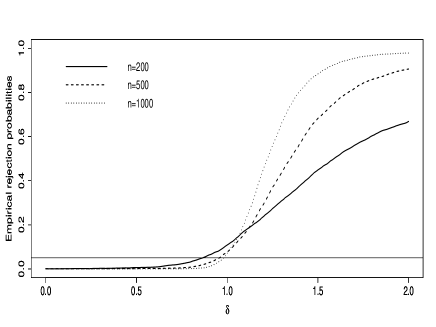

where and are the least squares residuals form the sample before and after the estimated change-point. In the case of serial dependence the estimators and have to be modified appropriately as indicated in Section 6.1 and the details are omitted for the sake of brevity. In the left part of Figure 4 we display the power of the test (3.28) for the null hypothesis of no relevant change in the parameter , where in the first half and of the sample and the explanatory variables and errors in the linear regression model are independent identically standard normal distributed. The approximation of the nominal level is rather accurate and the power is increasing with the sample size. On the other hand, the power of the test for a change in the slope is lower than the power for the test for change of the same size in the mean as considered in Figure 1111Additional simulations show that this power difference still exists if we do not account for serial dependence in the mean test, that means if we consider and the analogue formula for ..This observation can be easily explained by the asymptotic representation of the probability of rejection in (6.1) which is a decreasing function of the asymptotic variance . For the test of the null hypothesis of no relevant change in the mean and slope these variances are given by and , respectively [see (5.1) and (5.9),(5.10)]. In the right part of Figure 4 we display the results for heavy-tailed predictors , that is , where denote a -distribution with degrees of freedom. Note the -distribution is standardized such that Var. We observe a less accurate approximation of the nominal level if the sample size is . Moreover, distributed regressors yield also a loss in power. This observation can also be explained by formula (6.1), where the asymptotic variance is given by and for the normal and -distribution, respectively.

6.3 Relevant changes in the distribution function

We conclude this section with a brief finite sample study of the test for the null hypothesis of no relevant change in the distribution function, which was discussed in Section 5.5. For a given sample of independent random variables the test statistic for the null hypothesis (5.15) of no relevant change in the distribution function is defined as

where

| (6.3) |

Here denotes the order statistic of . The null hypothesis of no relevant change in the distribution function is rejected whenever (3.28) holds. For the definition of an estimator of the asymptotic variance we note that we assumed independent observations such that the formula for reduces to

where we use the notation . The estimator is now obtained by plugging in and replacing the unknown distribution functions by and by the empirical distribution functions calculated from the subsample before and after the estimated change-point.

In order to analyze size and power, we choose sample sizes with serially independent random variables, -distributed in the first half and -distributed with different degrees of freedom in the second half of the sample. The -distributed random variables are standardized such that they have mean and variance . The distance for is approximately equal to and this value was chosen as in the test (3.28). Table 1 shows the rejection probabilities of the test (3.28). Due to the different distance measure, they are somewhat difficult to compare to the other figures, but apparently, the test does work well. The power decreases in as the -distribution, standardized such that it has mean zero and variance one, converges to the -distribution for .

| / | 0.3730 | 0.3154 | 0.2764 | 0.2476 | 0.2254 | 0.2077 | 0.1932 |

|---|---|---|---|---|---|---|---|

| 200 | 0.995 | 0.784 | 0.404 | 0.174 | 0.078 | 0.042 | 0.021 |

| 500 | 1.000 | 0.978 | 0.614 | 0.221 | 0.069 | 0.023 | 0.006 |

| 1000 | 1.000 | 1.000 | 0.846 | 0.313 | 0.064 | 0.011 | 0.001 |

7 Empirical illustration

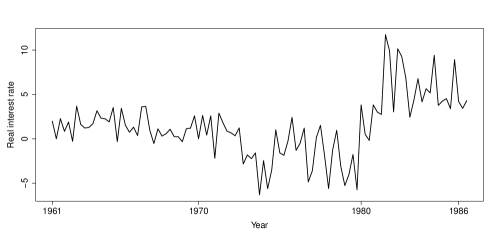

We illustrate the new method analyzing US ex post interest rates. This data set was also considered in Perron and Bai, (2003) and Garcia and Perron, (1996), among others, and is available on the website of the Journal of Applied Econometrics. The data consists of quarterly observations from 1961:1 to 1986:3 and is displayed in Figure 5.

We are interested in testing for relevant changes in the mean of these interest rates with the motivation that large shifts might be linked to a significant, long-ranging change in the economic or politic structure of the US, while this need not be true for small shifts. Indeed, both the figure and previous analysis in the literature indicate that there might be a large, statistically and economically significant break around 1980. However, there does not seem to be a consensus about the specific date of the break. Garcia and Perron, (1996) discuss monetary factors as a potential cause for this change, leading to a break point in the end of 1979. On the other hand, they argue that a change-point about one year later would have to be assumed if one argued that fiscal policies are a cause for the change. Based on formal change-point detection, Perron and Bai, (2003) identify 1980:3 as a break point.

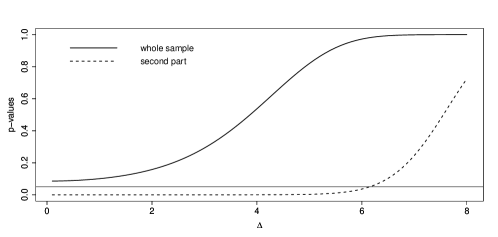

As there is no clear evidence for a distinguished point in time that can be considered as a break point, our new methods can provide new insight into the question if there exists a relevant break around 1980. Applied on the whole data set for , we can find no such that the p-value is smaller than , as Figure 6 shows. A reason for this might consist in the fact that there might exist mean jumps up- and downwards. In these cases, a CUSUM procedure is not optimal. So, we take a further look at a specific part of the data set, namely the values after 1972:3, a change-point that Perron and Bai, (2003) identify.222We take the point as given and do not consider potential size problems due to this pre-testing. In this situation which is well-suited for a CUSUM approach, our test rejects the null hypothesis for . We interpret this result as an evidence for a relevant change. The estimated break point is 1980:1, which lies in the middle between the dates mentioned above, and the empirical means before and after the break are equal to and , respectively.

Acknowledgements The authors thank Martina Stein, who typed numerous versions of this manuscript with considerable technical expertise, and Axel Bücher and Stanislav Volgushev for helpful discussions on an earlier version of this manuscript. This work has been supported in part by the Collaborative Research Center “Statistical modeling of nonlinear dynamic processes” (SFB 823, Teilprojekt A1 and C1) of the German Research Foundation (DFG). Parts of this paper were written while H. Dette was visiting the Isaac Newton Institute, Cambridge, UK, in 2014 (“Inference for change-point and related processes”) and the authors would like to thank the institute for its hospitality.

References

- Altman and Bland, (1995) Altman, D. G. and Bland, J. M. (1995). Statistics notes: Absence of evidence is not evidence of absence. British Medical Journal, 311(7003):485.

- Andrews, (1991) Andrews, D. (1991). Heteroskedasticity and autocorrelation consistent covariance matrix estimation. Econometrica, 59(3):817–858.

- Andrews, (1993) Andrews, D. W. K. (1993). Tests for parameter instability and structural change with unknown change point. Econometrica, 61(4):128–156.

- Andrews et al., (1996) Andrews, D. W. K., Lee, I., and Ploberg, W. (1996). Optimal change-point tests for normal linear regression. Journal of Econometrics, 70(1):9–36.

- (5) Aue, A., Hörmann, S., Horváth, L., and Reimherr, M. (2009a). Break detection in the covariance structure of multivariate time series models. Annals of Statistics, 37(6B):4046–4087.

- Aue and Horváth, (2013) Aue, A. and Horváth, L. (2013). Structural breaks in time series. Journal of Time Series Analysis, 34(1):1–16.

- (7) Aue, A., Horváth, L., Hušková, M., and Ling, S. (2009b). On distinguishing between random walk and change in the mean alternative. Econometric Theory, 25(2):411–441.

- Bai and Perron, (1998) Bai, J. and Perron, P. (1998). Estimating and testing linear models with multiple structural changes. Econometrica, 66(1):47–78.

- Berger and Delampady, (1987) Berger, J. O. and Delampady, M. (1987). Testing precise hypotheses. Statistical Science, 2(3):317–335.

- (10) Berkes, I., Gombay, E., and Horváth, L. (2009a). Testing for changes in the covariance structure of linear processes. Journal of Statistical Planning and Inference, 139(6):2044–2063.

- (11) Berkes, I., Hörmann, S., and Schauer, J. (2009b). Asymptotic results for the empirical process of stationary sequences. Stochastic Processes and their Applications, 119(4):1298–1324.

- Berkson, (1938) Berkson, J. (1938). Some difficulties of interpretation encountered in the application of the chi-square test. Journal of the American Statistical Association, 33(203):526–536.

- Brown et al., (1975) Brown, R., Durbin, J., and Evans, J. (1975). Techniques for testing the constancy of regression relationships over time. Journal of the Royal Statistical Society Series B, 37(2):149–163.

- Bücher, (2014) Bücher, A. (2014). A note on weak convergence of the sequential multivariate empirical process under strong mixing. Journal of Theoretical Probability, to appear.

- Carlstein, (1988) Carlstein, E. (1988). Nonparametric change-point estimation. Annals of Statistics, 16(1):188–197.

- Chen et al., (2013) Chen, C., Chan, J., Gerlach, R., and Hsieh, W. (2013). A comparison of estimators for regression models with change points. Statistics and Computing, 21(3):395–414.

- Chow, (1960) Chow, G. (1960). Tests of equality between sets of coefficients in two linear regressions. Econometrica, 28(3):591–605.

- Chow and Liu, (1992) Chow, S.-C. and Liu, P.-J. (1992). Design and Analysis of Bioavailability and Bioequivalence Studies. Marcel Dekker, New York.

- Csörgo and Horváth, (1997) Csörgo, M. and Horváth, L. (1997). Limit Theorems in Change-Point Analysis. Wiley, New York.

- Dehling et al., (2013) Dehling, H., Durieu, O., and Tusche, M. (2013). A sequential empirical central limit theorem for multiple mixing processes with application to B-geometrically ergodic Markov chains. arXiv:1303.4537.

- Deo, (1973) Deo, C. M. (1973). A note on empirical processes of strong-mixing sequences. The Annals of Probability, 1(5):870–875.

- Doukhan, (1994) Doukhan, P. (1994). Mixing: Properties and Examples (Lecture Notes in Statistics 85). Springer, Berlin.

- Garcia and Perron, (1996) Garcia, R. and Perron, P. (1996). An analysis of the real interest rate under regime shifts. The Review of Economics and Statistics, 78(1):111–125.

- Hansen, (1992) Hansen, B. E. (1992). Tests for parameter instablity in regression with I(1) processes. Journal of Business and Economic Statistics, 10(3):321–335.

- Horváth et al., (1999) Horváth, L., Kokoszka, P., and Steinebach, J. (1999). Testing for changes in multivariate dependent observations with an application to temperature changes. Journal of Multivariate Analysis, 68(1):96–119.

- Jandhyala et al., (2013) Jandhyala, V., Fotopoulos, S., MacNeill, I., and Liu, P. (2013). Inference for single and multiple change-points in time series. Journal of Time Series Analysis, forthcoming, doi: 10.1111/jtsa12035.

- Kim and Cai, (1993) Kim, H.-J. and Cai, L. (1993). Robustness of the likelihood ratio test for a change in simple linear regression. Journal of the American Statistical Association, 88(423):864–871.

- Kim and Siegmund, (1989) Kim, H.-J. and Siegmund, D. (1989). The likelihood ratio test for a change-point simple linear regression. Biometrika, 76(3):409–423.

- Krämer et al., (1988) Krämer, W., Ploberger, W., and Alt, R. (1988). Testing for structural change in dynamic models. Econometrica, 56(6):1355–1369.

- Liebscher, (1996) Liebscher, E. (1996). Central limit theorems for the sums of -mixing random variables. Stochastics and Stochastic Reports, 59(3-4):241–258.

- McBride, (1999) McBride, G. B. (1999). Equivalence tests can enhance environmental science and management. Australian New Zealand Journal of Statistics, 41(1):19–29.

- Nosek and Skzutnika, (2013) Nosek, K. and Skzutnika, Z. (2013). Change-point detection in a shape-restricted regression model. Statistics, forthcoming, doi: 10.1080/02331888.2012.760094.

- Page, (1954) Page, E. S. (1954). Continuous inspection schemes. Biometrika, 41(1-2):100–115.

- Page, (1955) Page, E. S. (1955). Control charts with warning lines. Biometrika, 42(1-2):243–257.

- Perron and Bai, (2003) Perron, P. and Bai, J. (2003). Computation and analysis of multiple structural change models. Journal of Applied Econometrics, 18(1):1–22.

- Preuss et al., (2014) Preuss, P., Puchstein, R., and Dette, H. (2014). Detection of multiple structural breaks in multivariate time series. arXiv:1309.1309v1.

- Roy, (1997) Roy, T. (1997). Calibrated nonparametric confidence sets. Journal of Mathematical Chemistry, 21(1):103–109.

- Székely and Rizzo, (2005) Székely, G. J. and Rizzo, M. L. (2005). A new test for multivariate normality. Journal of Multivariate Analysis, 93(1):58–80.

- van der Vaart and Wellner, (1996) van der Vaart, A. W. and Wellner, J. A. (1996). Weak Convergence and Empirical Processes. Springer Series in Statistics. Springer, New York.

- Wied, (2013) Wied, D. (2013). Cusum-type testing for changing parameters in a spatial autoregressive model for stock returns. Journal of Time Series Analysis, 34(1):221–229.

- Wied et al., (2012) Wied, D., Krämer, W., and Dehling, H. (2012). Testing for a change in correlation at an unknown point in time using an extended functional delta method. Econometric Theory, 28(3):570–589.

- Withers, (1975) Withers, C. S. (1975). Convergence of empirical processes of mixing rv’s on [0,1]. Annals of Statistics, 3(5):1101–1108.

- Xiao and Phillips, (2002) Xiao, Z. and Phillips, P. (2002). A cusum test for cointegration using regression residuals. Journal of Econometrics, 108(1):43–61.

- Zhou, (2013) Zhou, Z. (2013). Heteroscedasticity and autocorrelation robust structural change detection. Journal of the American Statistical Association, 108(502):726–740.