If Archimedes would have known functions …

Abstract.

Could calculus on graphs have emerged by the time of Archimedes, if function, graph theory and matrix concepts were available 2300 years ago?

Key words and phrases:

Calculus, Graph theory, Calculus history1991 Mathematics Subject Classification:

Primary: 26A06, 97A30, 68R101. Single variable calculus

Calculus on integers deals with functions like . The difference as well as the sum with the understanding are functions again. We call the derivative and the integral. The identities and are the fundamental theorem of calculus. Linking sums and differences allows to compute sums (which is difficult in general) by studying differences (which is easy in general). Studying derivatives of basic functions like will allow to sum such functions. As operators, and where and are translations. We have . The derivative operator satisfies the Leibniz product rule . Since momentum satisfies the anti-commutation relation we have quantum calculus. The polynomials satisfy and . The exponential satisfies and . Define and as the real and imaginary part of . From , we deduce and . Since is monotone, its inverse is defined. Define the reciprocal by and . We check identities like from which follow. The Taylor formula is due to Newton and Gregory and can be shown by induction or by noting that satisfies the transport equation which is solved by . The Taylor expansion gives . We also get from that . The functions solve the harmonic oscillator equation . The equation is solved by the anti derivative . The wave equation can be written as which thus has the solution given as a linear combination of and . We replace now integers with a graph, the derivative with a matrix , functions by forms, anti-derivatives by , and Taylor with Feynman.

2. Multivariable calculus

Space is a finite simple graph . A subgraph of is a curve if every unit sphere of a vertex in consists of or disconnected points. A subgraph is a surface if every unit sphere is either an interval graph or a circular graph with . Let denote the set of subgraphs of so that and and is the set of triangles in . Intersection relations render each a graph too. The linear space of anti-symmetric functions on is the set of -forms. For , we have scalar functions. To fix a basis, equip simplices like edges and triangles with orientations. Let denote the exterior derivative . If be the boundary of , then for any . The boundary of a curve is empty or consists of two points. The boundary of a surface is a finite set of closed curves. A closed surface is a discretisation of a -dimensional classical surface as we can build an atlas from wheel subgraphs. An orientation of a choice of orientations on triangles in such that the boundary orientation of two intersecting triangles match. If is a -form and is an orientable surface, define . An orientation of a curve is a choice of orientations on edges in such that the boundary orientation of two adjacent edges correspond. If is a -form and is orientable, denote by the sum . For a -form, write and for a -form , write . If is a surface and is a -form, the theorem of Stokes tells that . It is proved by induction using that for a single simplex, it is the definition. If is a -dimensional graph, and is a function, then is the fundamental theorem of line integrals. A graph is a solid, if every unit sphere is either a triangularization of the -sphere or a triangularization of a disc. Points for which the sphere is a disc form the boundary. If is a -form and is a solid, then is Gauss theorem. The divergence is the adjoint . In school calculus, -forms and -forms are often identified as “vector fields” and -forms on the solid is treated as scalar functions. Gauss is now the divergence theorem. Define the Dirac matrix and the form Laplacian . Restricted to scalar functions, it is which is equal to , where is the adjacency matrix and the diagonal degree matrix of the graph. The Schrödinger equation is solved by . It is a multi-dimensional Taylor equation, because by matrix multiplication, the term is the sum over all possible paths of length where each step is multiplied with . The solution of the Schrödinger equation is now the average over all possible paths from to . This Feynman-Kac formula holds for general -forms. Given an initial form , it describes . The heat equation has the solution , the heat flow. Because leaves -forms invariant, the Feynman-Kac formula deals with paths which stay on the graph . As any linear differential equation, it can be solved using eigenfunctions of . If , it is a discrete Fourier basis. The wave equation can be written as which shows that with . Feynman-Kac for a -form expresses as the expectation on a probability space of finite paths in the simplex graph where is the length of .

3. Pecha-Kucha

Pecha-Kucha is a presentation form in which 20 slides are shown exactly 20 seconds each. Here are slides for a talk given on March 6, 2013. The bold text had been prepared to be spoken, the text after consists of remarks posted on March 2013.

-

1

![[Uncaptioned image]](/html/1403.5821/assets/x1.png)

What if Archimedes would have known the concept of a function? The following story borrows from classes taught to students in singular variable calculus and at the extension school. The mathematics is not new but illustrates part of what one calls “quantum calculus” or “calculus without limits”.

Quantum calculus comes in different flavors. A book with that title was written by Kac and Cheung [32]. The field has connections with numerical analysis, combinatorics and even number theory. The calculus of finite differences was formalized by George Boole but is much older. Even Archimedes and Euler thought about calculus that way. It also has connections with nonstandard analysis. In ”Math 1a, a single variable calculus course or Math E320, a Harvard extension school course, I spend 2 hours each semester with such material. Also, for the last 10 years, a small slide show at the end of the semester in multivariable calculus featured a presentation ”Beyond calculus”.

-

2

![[Uncaptioned image]](/html/1403.5821/assets/x2.png)

About 20 thousand years ago, mathematicians represented numbers as marks on bones. I want you to see this as the constant function 1. Summing up the function gives the concept of number. The number 4 for example is . Taking differences brings us back: .

The Ishango bone displayed in the slide is now believed to be about 20’000 years old. The number systems have appeared in the next couple of thousand years, independently in different places. They were definitely in place 4000 BC because we have Carbon dated Clay tablets featuring numbers. Its fun to make your own Clay tablets: either on clay or on chewing gum.

-

3

![[Uncaptioned image]](/html/1403.5821/assets/x3.png)

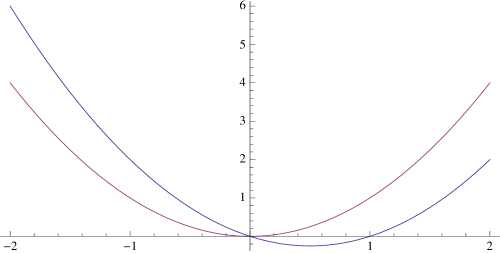

When summing up the previous function , we get triangular numbers. They represent the area of triangles. Gauss got a formula for them as a school kid. Summing them up gives tetrahedral numbers, which represent volumes. Integration is summation, differentiation is taking differences.

The numbers are examples of polytopic numbers, numbers which represent patterns. Examples are triangular, tetrahedral or pentatopic numbers. Since we use the forward difference and start summing from , our formulas are shifted. For example, the triangular numbers are traditionally labeled , while we write . We can think about the new functions as a new basis in the linear space of polynomials.

-

4

![[Uncaptioned image]](/html/1403.5821/assets/x4.png)

The polynomials appear as part of the Pascal triangle. We see that the summation process is the inverse of the difference process. We use the notation for the function in the nth row.

The “renaming idea” is part of quantum calculus. It is more natural when formulated in a non-commutative algebra, a crossed product of the commutative algebra we are familiar with. The commutative -algebra of all continuous real functions encodes the topology of the real numbers. If is translation, we can look at the algebra of operators on generated by and the translation operator s. With , the operators are the multiplication operators generated by the polynomials of the slide. The derivative be written as the commutator . In quantum mechanics, functions are treated as operators. The deformed algebra is no more commutative: with satisfying and the anti-commutation relations hold. Hence the name “quantum calculus”.

-

5

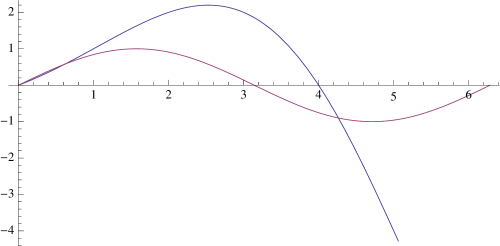

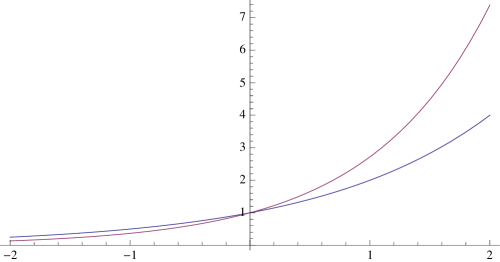

![[Uncaptioned image]](/html/1403.5821/assets/x5.png)

With the difference operation and the summation operation , we already get an important formula. It tells that the derivative of is times x to the . Lets also introduce the function to the power . This is the compound interest formula. We check that its derivative is a constant times the function itself.

The deformed exponential is just a rescaled exponential with base . Writing it as a compound interest formula allows to see the formula as the property that the bank pays you a multiple a to your fortune . The compound interest formula appears in the movie ”The bank”. We will below look at the more general exponential which is the exponential to the ”Planck constant” . If goes to zero, we are lead to the standard exponential function . One can establish the limit because .

-

6

![[Uncaptioned image]](/html/1403.5821/assets/x6.png)

The heart of calculus is the fundamental theorem of calculus. If we take the sum of the differences, we get the difference of f(x) minus f(0). If we take the difference of the sum, we get the function f(x). The pictures pretty much prove this without words. These formulas are true for any function. They do not even have to be continuous.

Even so the notation is simpler than and is simpler than the integral sign, it is the language with which makes the theorem look unfamiliar. Notation is very important in mathematics. Unfamiliar notation can lead to rejection. One of the main points to be made here is that we do not have to change the language. We can leave all calculus books as they are and just look at the content in new eyes. The talk is advertisement for the calculus we know, teach and cherish. It is a much richer theory than anticipated.

-

7

![[Uncaptioned image]](/html/1403.5821/assets/x7.png)

The proof of part I shows a telescopic sum. The cancellations are at the core of all fundamental theorems. They appear also in multivariable calculus in differential geometry and beyond.

It is refreshing that one can show the proof of the fundamental theorem of calculus early in a course. Traditionally, it takes much longer until one reaches the point. Students have here only been puzzled about the fact that the result holds only for x=nh and not in general. It would already here mathematically make more sense to talk about a result on a finite linear graph but that would increase mentally the distance to the traditional calculus in [10] on ”Historical Reflections on Teaching the fundamental Theorem of Integral Calculus”. Bressoud tells that ”there is a fundamental problem with the statement of the FTC and that only a few students understand it”. I hope this Pecha-Kucha can help to see this important theorem from a different perspective.

-

8

![[Uncaptioned image]](/html/1403.5821/assets/x8.png)

The proof of the second part is even simpler. The entire proof can be redone, when the step size h=1 is replaced by a positive h. The fundamental theorem allows us to solve a difficult problem: summation is global and hard, differences is local and easy. By combining the two we can make the hard stuff easy.

This is the main point of calculus. Integration is difficult, Differentiation is easy. Having them linked makes the hard things easy. At least part of it. It is the main reason why calculus is so effective. These ideas go over to the discrete. Seeing the fundamental idea first in a discrete setup can help to take the limit when h goes to zero.

-

9

![[Uncaptioned image]](/html/1403.5821/assets/x9.png)

We can adapt the step size h from 1 to become any positive number h. The traditional fundamental theorem of calculus is stated here also in the notation of Leibniz. In classical calculus we would take the limit h to 0, but we do not go that way in this talk.

When teaching this, students feel a slight unease with the additional variable h. For mathematicians it is natural to have free parameters, for students who have had little exposure to mathematics, it is difficult to distinguish between the variable x and h. This is the main reason why in this talk, I mostly stuck to the case h=1. In some sense, the limit h to 0 is an idealization. This is why the limit h going to 0 is so desirable. But we pay a prize: the class of function we can deal with, is much smaller. I myself like to see traditional calculus as a limiting case of a larger theory. The limit h to zero is elegant and clean. But it takes a considerable effort at first to learn what a limit is. Everybody who teaches the subject can confirm the principle that often things which were historically hard to find, are also harder to teach and master. Nature might have given up on it early on: seconds after the big bang: “Darn, lets just do it without limits …!”

-

10

![[Uncaptioned image]](/html/1403.5821/assets/x10.png)

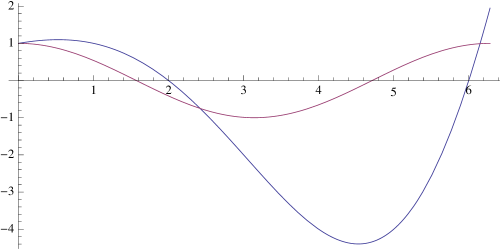

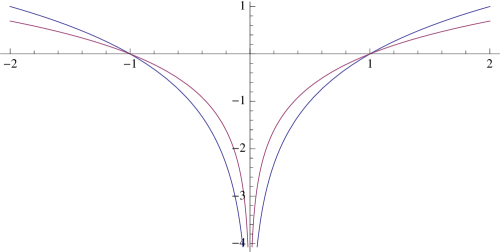

We can define cosine and sine by using the exponential, where the interest rate is the square root of -1. These deformed trigonometric functions have the property that the discrete derivatives satisfy the familiar formula as in the books. These functions are close to the trigonometric functions we know if h is small.

This is by far the most elegant way to introduce trigonometric functions also in the continuum. Unfortunately, due to lack of exposure to complex numbers, it is rarely done. The Planck constant is . The new functions are then very close to the traditional cos and sin functions. The functions are not periodic but a growth of amplitude is only seen if is of the order . It needs even for X-rays astronomical travel distances to see the differences.

-

11

![[Uncaptioned image]](/html/1403.5821/assets/x11.png)

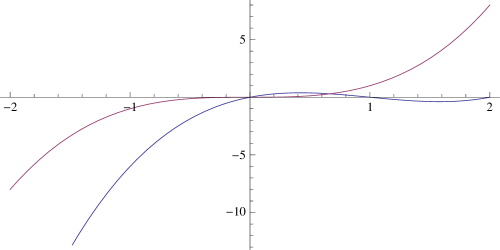

The fundamental theorem of calculus is fantastic because it allows us to sum things which we could not sum before. Here is an example: since we know how to sum up the deformed polynomials, we can find formulas for the sum of the old squares. We just have to write the old squares in terms of the new squares which we know how to integrate.

This leads to a bunch of interesting exercises. For example, because , we have we get a formula for the sum of the first n-1 squares. Again we have to recall that we sum from 0 to n-1 and not from 1 to n. By the way: this had been a ’back and forth’ in the early lesson planning. I had started summing from 1 to n and using the backwards difference . The main reason to stick to the forward difference and so to polynomials like was that we are more familiar with the difference quotient [f(x+h)-f(x)]/h and also with left Riemann sums. The transition to the traditional calculus becomes easier because difference quotients and Riemann sums are usually written that way.

-

12

![[Uncaptioned image]](/html/1403.5821/assets/x12.png)

We need rules of differentiation and integration. Reversing rules for differentiation leads to rules of integration. The Leibniz rule is true for any function, continuous or not.

The integration rule analogue to integration by parts is called Abel summation which is important when studying Dirichlet series. Abel summation is used in this project. The Leibniz formula has a slight asymmetry. The expansion of the rectangle has two main effects and , but there is an additional small part . This is why we have . The formula becomes more natural when working in the non-commutative algebra mentioned before: if , then because the translation operator now takes care of the additional shift: . The algebra picture also explains why is not because also the multiplication operation is deformed in that algebra. In the noncommutative algebra we have . While the algebra deformation is natural for mathematicians, it can not be used in calculus courses. This can be a reason why it appears strange at first, like quantum mechanics in general.

-

13

![[Uncaptioned image]](/html/1403.5821/assets/x13.png)

The chain rule also looks the same. The formula is exact and holds for all functions. Writing down this formula convinces you that the chain rule is correct. The only thing which needs to be done in a traditional course is to take the limit.

Most calculus textbooks prove the chain rule using linearization: first verify it for linear functions then argue that the linear part dominates in the limit. [Update of December 2013: The proof with the limit [64]]. Reversing the chain rule leads to the integration tool substitution. Substitution is more tricky here because as we see different step sizes h and H in the chain rule. This discretization issue looks more serious than it is. First of all, compositions of functions like are remarkably sparse in physics. Of course, we encounter functions like but they should be seen as fundamental functions and defined like . This is by the way different from .

-

14

![[Uncaptioned image]](/html/1403.5821/assets/x14.png)

Also the Taylor theorem remains true. The formula has been discovered by Newton and Gregory. Written like this, using the deformed functions, it is the familiar formula we know. We can expand any function, continuous or not, when knowing the derivatives at a point. It is a fantastic result. You see the start of the proof. It is a nice exercise to make the induction step.

James Gregory was a Scottish mathematician who was born in 1638 and died early in 1675. He has become immortal in the Newton-Gregory interpolation formula. Despite the fact that he gave the first proof of the fundamental theorem of calculus, he is largely unknown. As a contemporary of Newton, he was also in the shadow of Newton. It is interesting how our value system has changed. “Concepts” are now considered less important than proofs. Gregory would be a star mathematician today. The Taylor theorem can be proven by induction. As in the continuum, the discrete Taylor theorem can also be proven with PDE methods: solves the transport equation , where so that .

-

15

![[Uncaptioned image]](/html/1403.5821/assets/x15.png)

Here is an example, where we expand the exponential function and write it as as a sum of powers. Of course, all the functions are deformed functions. The exponential function as well as the polynomials were newly defined. We see what the formula means for .

It is interesting that Taylors theorem has such an arithmetic incarnation. Usually, in numerical analysis text, this Newton-Gregory result is treated with undeformed functions, which looks more complicated. The example on this slide is of course just a basic property of the Pascal triangle. The identity given in the second line can be rewritten as which in general tells that if we sum the n’th row of the Pascal triangle, we get . Combinatorially, this means that the set of all subsets can be counted by grouping sets of fixed cardinality. It is amusing to see this as a Taylor formula (or Feynman-Kac). But it is more than that: it illustrates again an important point I wanted to make: we can not truly appreciate combinatorics if we do not know calculus.

-

16

![[Uncaptioned image]](/html/1403.5821/assets/x16.png)

Taylor’s theorem is useful for data interpolation. We can avoid linear algebra and directly write down a polynomial which fits the data. I fitted here the Dow Jones data of the last 20 years with a Taylor polynomial. This is faster than data fitting using linear algebra.

When fitting the data, the interpolating function starts to oscillate a lot near the ends. But thats not the deficit of the method. If we fit n data points with a polynomial of degree n-1, then we get a unique solution. It is the same solution as the Taylor theorem gives. The proof of the theorem is a simple induction step, using a property of the Pascal triangle. Assume, we know . Now apply , to get . We can now get . Adding the terms requires a property of the Pascal triangle.

-

17

![[Uncaptioned image]](/html/1403.5821/assets/x17.png)

We can also solve differential equations. We can use the same formulas as you see in books. We deform the operators and functions so that everything stays the same. Difference equations can be solved with the same formulas as differential equations.

To make the theory stronger, we need also to deform the log, as well as rational functions. This is possible in a way so that all the formulas we know in classical calculus holds: first define the log as the inverse of exp. Then define and . Now holds for all integers. We can continue like that and define sqrt(x) as the inverse of and then the as . It is calculus which holds everything together.

-

18

![[Uncaptioned image]](/html/1403.5821/assets/x18.png)

In multivariable calculus, space takes the form of a graph. Scalar functions are functions on vertices, Vector fields are signed functions on oriented edges. The gradient of a function is a vector field which is the difference of function values. Integrating the gradient of a function along a closed path gives the difference between the potential values at the end points. This is the fundamental theorem of line integrals.

This result is is also in the continuum the easiest version of Stokes theorem. Technically, one should talk about -forms instead of vector fields. The one forms are anti-commutative functions on edges. [40] is an exhibit of three theorems (Green-Stokes, Gauss-Bonnet [37], Poincaré-Hopf [38]), where everything is defined and proven on two pages. See also the overview [42].

-

19

![[Uncaptioned image]](/html/1403.5821/assets/x19.png)

Stokes theorem holds for a graph for which the boundary is a graph too. Here is an example of a ”surface”, which is a union of triangles. The curl of a vector field F is a function on triangles is defined as the sum of vector fields along the boundary. Since the terms on edges in the intersection of triangles cancel, only the line integral along the boundary survives.

This result is old. It certainly seems have been known to Kirchhoff in 1850. Discrete versions of Stokes pop up again and again over time. It must have been Poincaré who first fully understood the Stokes theorem in all dimensions and in the discrete, when developing algebraic topology. He introduced chains because unlike graphs, chains are closed under boundary operation. This is a major reason, algebraic topologists use it even so graphs are more intuitive. One can for any graph define a discrete notion of differential form as well as an exterior derivative. The boundary of graph is in general only a chain. For geometric graphs like surfaces made up of triangles, the boundary is a union of closed paths and Stokes theorem looks like the Stokes theorem we teach.

-

20

![[Uncaptioned image]](/html/1403.5821/assets/x20.png)

Could Archimedes have discovered the fundamental theorem of calculus? His intellectual achievements surpass what we have seen here by far.

Yes, he could have done it. If he would not have been given the sword, but the concept of a function.Both the precise concept of limit as well as the concept of functions had been missing. While the concept of limit is more subtle, the concept of function is easier. The basic ideas of calculus can be explained without limits. Since the ideas of calculus go over so nicely to the discrete, I believe that calculus is an important subject to teach. It is not only a benchmark and a prototype theory, a computer scientist who has a solid understanding of calculus or even differential topology can also work much better in the discrete. To walk the talk: source code of a program in computer vision was written from scratch, takes a movie and finds and tracks features like corners [43]. There is a lot of calculus used inside.

This was a talk given on March 6 at a “Pecha-Kucha” event at the Harvard Mathematics department, organized by Sarah Koch and Curt McMullen. Thanks to both for running that interesting experiment.

4. Problems in single variable calculus

Teachers at the time of Archimedes could have assigned problems as follows.

Some of the following problems have been used in single variable and

extension school classes but most are not field tested. It should become obvious

however that one could build a calculus course sequence on discrete notions.

Since the topic is not in books, it would be perfect also for an “inquiry based

course”, where students develop and find theorems themselves.

-

1

Compute with and verify that with .

-

2

Find with . This was the task, which the seven year old Gauss was given by his school teacher Herr Büttner. Gauss computed because he saw that one can pair 50 numbers summing up to each and get . Legend tells that he wrote this number onto his tablet and threw it onto the desk of his teacher with the words “Hier ligget sie!” (=“Here it is!”). Now its your turn. You are given the task to sum up all the squares from to .

-

3

Find the next term in the sequence

by taking “derivatives” until you see a pattern, then “integrate” that pattern.

-

4

Lets compute some trig function values. We know for example. and . Compute and . (Answer: and .)

-

5

Find for the function . Your explicit formula should satisfy and lead to the sequence

-

6

Find for and evaluate it at . Answer: We have seen that so that . . We have . Indeed: and so that the result matches .

-

7

Verify that for and conclude that . For example, for we have .

-

8

The Fibonnacci sequence satisfies the rule . Verify that and use this fact to show that . For example, for we get or for we have .

-

9

Verify that the Taylor series sums up the ’th line in the Pascal triangle. For example, . To do so, check that is the Binomial coefficient and in particular that for so that the Taylor series is a finite sum.

-

10

Using the definition of trigonometric functions, check that and . Again, these are finite sums.

-

11

De Moivre is in the continuum the simplest way to derive the double angle formulas and . Check whether these double angle formulas work also with the new functions . Be careful that is not the same than .

-

12

Verify that has roots at with and has roots at with . To do so, note .

-

13

Find the solution of the harmonic oscillator which has the initial conditions . Solution: the solution is of the form , where are constants. Taking gives . Taking gives . Since and we have . The solution is .

-

14

If is a small positive number called Planck constant. Denote by the classical and functions. Verify that . Solution: . Remark. With , a Gamma ray of wave length traveling for one million light years meters, we start to see a difference between and . The amplitude of the former will grow and be seen as a gamma ray burst.

-

15

The functions and are not periodic on the integers. While we know for every integer , we have exploding exponentially (this is only since the Planck constant equal to ). Lets look at the tangent function . Verify that it is periodic on the integers.

-

16

Lets call be a discrete gradient critical point of if . Assume that is a continuous function from the real line to itself and that has a discrete gradient critical point . Verify that there is a classical local maximum or classical local minimum of in . Solution: this is a reformulation of the classical Bolzano extremal value theorem on the interval .

-

17

Injective functions on do not have discrete gradient critical points. Critical points must be defined therefore differently if one only looks at functions on a graph. A point is a critical point if the index is not zero. In other words, if either both or no neighbor of have smaller values than then is a critical point. Verify that if is an injective periodic function on , then is equal to . Hint: use induction. Assume it is true for , look at , then see what happens if the maximum of is taken away.

-

18

If is a classically differentiable function, then for any , there exists such that . Here is the classical derivative and the discrete derivative. Solution: this is a reformulation of the classical mean value theorem.

-

19

The Taylor expansion extends a function of compact support from the integers to the real line. It is an explicit interpolation formula which provides us with a function on the real line satisfying for integer arguments . Perform the Taylor expansion of the function .

-

20

Check that unlike the classical trigonometric function the function is not odd and the function is not even. Indeed, check that for while becomes unbounded for .

-

21

Compute the sum . Answer: . Now give an analytic expression for which can no more be evaluated by computing the sum directly.

-

22

Let us in this problem also write . Integrating the product rule gives leads to integration by parts formula

an expression which is in the discrete also called Abel summation. It is usually written as

Use integration by parts to sum up . Answer: the sum is .

-

23

We have defined as the derivative of . Verify that , where is the good old classical natural logarithm.

5. Problems in multi variable calculus

-

1

Bolzano’s extremal value theorem is obvious for finite graphs because a function on a finite set always has a global maximum and minimum. Verify that for a global minimum, the index is equal to . For every integer find a graph and a function for which a maximum is equal to . For example, for a star graph with rays and a function having the maximum in the center , we have .

-

2

A curve in is a subgraph with the property that every vertex has either or neighbors. The arc length of a path is the number of edges in . The boundary points are the vertices with one neighbor. A connected surface in is a subgraph for which every vertex has either a linear graph or circular graph as a unit sphere. The surface area of is the number of triangles in . The interior points are the points for which the unit sphere is a circular graph. A surface is called flat if every interior point has a unit sphere which is . Flat surfaces play the role of regions in the plane. The curvature of a boundary point of a flat surface is . Verify that the sum of the curvatures of boundary points is where is the number of holes. This is a discrete Hopf Umlaufsatz.

-

3

A graph is called simply connected if every simple and connected curve in can be deformed to a single edge using the following two deformation steps of a : replace two edges of within a triangle with the third edge of that triangle or replace an edge of in a triangle with the two other edges of the triangle. A deformation step is called valid if the curve remains a simple connected curve or degenerates to after the deformation. A -form is called a gradient field, if for some scalar function . Verify that on a simply connected surface, a -form is a gradient field if and only if the curl is zero on each triangle.

-

4

Stokes theorem for a flat orientable surface is what traditionally is called Greens theorem. It tells that the sum of the curls over the triangles is equal to the line integral along the boundary. Look at the wheel graph which is obtained by adding an other vertex to a circular graph and connecting all vertices of with . Define the -form , where each of the central edges is given the value and each edge is given the value . Find the curl on all the triangles and verify Green’s theorem in that case.

-

5

A graph is a surface if for every vertex , the unit sphere is a circular graph. The curvature at a point of a surface is defined as . Verify that an octahedron is a discrete surface and that the curvature is constant everywhere. See that the curvatures add up to . Verify also that the icosahedron is a discrete surface and that the curvature is constant adding up to . You have verified two special cases of Gauss-Bonnet. Play with other discrete surfaces but make sure that all “faces” are triangles.

-

6

We want to see an analogue of the second derivative test for functions of two variables on a discrete surface like an icosahedron. For an injective function on the vertices, call a critical point with nonzero index if has Euler characteristic different from . The number plays the role of the discriminant. Verify that if it is negative then we deal with a saddle point which is neither maximum nor minimum. Verify that if it is positive with empty , then it is a local minimum. Verify that if the discriminant is positive and is a circular graph, then it is a local maximum. As in the continuum, where the discriminant at critical points can be zero, this can happen also here but only in higher dimensions. Maybe you can find an example of a function on a three dimensional graph.

-

7

Given a surface and an injective function on , define the level curve of as the graph which has as vertices the edges of for which changes. Two such vertices are connected if they are contained in a common triangle. (Graph theorists call this a subgraph of the “line graph” of . Verify that for a two dimensional geometric graph, level curve of is a finite union of circular graphs and so a geometric one dimensional graph. The fact that the gradient is a function on changing sign on every original edge is the analogue of the classical fact that the gradient is perpendicular to the level curve.

-

8

An oriented edge of a graph is a ”direction” and plays the role of unit vectors in classical calculus. The value of is the analogue of a directional derivative. Start with a vertex of , then go into direction , where the directional derivative is maximal and stop if there is no direction in which the directional derivative is positive. This discrete gradient flow on the vertex set leads to a local maximum. Investigate how this notion of directional derivative corresponds to the notion in the continuum. Especially note that for an injective function, the directional derivative is never zero.

-

9

An injective function on a graph has no points for which . We therefore have to define critical points differently. We say is a critical point of if is not zero. Let be a discretisation of a disc. Check that for maxima, and is a circular graph. Check that for minima, and is empty. For Saddle points, where consists of two linear graphs. A vertex is called a monkey saddle if . Verify the ”island theorem”: the sum over all indices over the disc is equal to . A discrete Poincaré-Hopf theorem [38] assures that in general .

-

10

Let be two -forms, define the dot product of at a vertex as , where is the set of edges attached to . Define the length as . The angle between two -forms at is defined by the identity . Given two functions and an edge define the angle between two hyper surfaces at an edge as the angle between and . The hyper surface is part of the line graph of : it has as vertices the edges of the graph at which changes sign and as edges the pairs of new vertices which intersect when seen as old edges.

-

11

Let be two -forms. Define the cross product of at a vertex as the function on adjacent triangle as . It is a number which is the analogue of projecting the classical cross product onto a -dimensional direction in space. The cross product is anti-commutative. Unlike a two form, it is not a function on triangles because the order of the product plays a role. It can be made a -form by anti-symmetrization. Here is the problem: verify that for any two functions on the vertices of a triangle the cross product is up to a sign at all vertices.

-

12

Given three -forms , define the triple scalar product at a vertex as a function on an adjacent tetrahedron as . Verify that this triple scalar product has the same properties as the triple scalar product in classical multivariable calculus.

-

13

Let be the complete graph with two vertices and one edge. Verify that the Dirac operator and form Laplacian are given by

For an informal introduction to the Dirac operator on graphs and Mathematica code, see [41]. The Laplacian has the eigenvalues . Write down the solution of the wave equation where and are the values of on vertices and is the evolution of the -form.

-

14

The graph G= is the smallest possible four dimensional space. Given a -form , we have at each vertex triangles. The -form defines so a field with components. If one of the four edges emerging from is called ”time” and the triangles containing this edge define the electric field and the other triangles are the magnetic field . The equations are called Maxwell equations. Can we always get from the current ? Verify that if (Coulomb gauge), then the Poisson equation always allows to compute and so . The Coulomb gauge assumption is one of Kirchhoff’s conservation law: the sum over all in and outgoing currents at each node are zero.

-

15

Let denote the circular graph with vertices. Find a function on the vertex set, which has exactly two critical point, one minimum of index and one maximum of index . Now find a function with critical points and verify that there are no functions with an odd number of critical points. Hint: show first that the index of a critical point is either or and use then that the indices have to add up to .

-

16

Now look at the tetrahedron . Verify that every function on has exactly one critical point, the minimum.

-

17

Take a linear graph which consists of three vertices and two edges. There are 6 functions which take values on the vertices. In each case compute the index and verify that the average over all these indices gives the curvature of the graph, which is at the boundary and in the center. This is a special case of a result proven in [39].

Appendix A: Graph theory glossary

A graph consists of a vertex set and an edge set .

If and are finite, it is called a finite graph. If every

satisfies , elements and are identified and every appears

only once, the graph is called a finite simple graph. In other words, we

disregard loops , look at undirected graphs without

multiple connections. The cardinality of is called order and the

cardinality of is called size of the graph. When counting , we look at the

unordered pairs and not the ordered pairs . The later would be twice

as large.

Restricting to finite simple graphs is not much of a restriction

of generality. The notion of loops and multiple connections can be incorporated later by

introducing the algebraic notion of chains defined over the graph, directions using orientation.

Additional structure can come from divisors or difference operators defined over the graph.

When looking at geometry and calculus in particular, the notion of chains resembles more the

notion of fiber bundles, and directions are more like a choice of orientation.

Both enrichments of the geometry are important but can be popped upon a finite simple graph if

needed, similarly as bundle structures can be added to a manifold or variety.

As in differential geometry or algebraic geometry, the notions of fiber bundles or

divisors are important because they allow the use of algebra to study geometry. Examples are

cohomology classes of differential forms or divisor classes and both work very well in graph theory too.

Given a finite simple graph , the elements in are called vertices or nodes

while the elements in are called edges or links. A finite simple graph contains more

structure without further input. A graph is called a subgraph of if

and . A graph is called complete if the size is ,

where is the order. In other words, in a complete graph, all vertices are connected. The

dimension of a complete graph is if is the order. A single vertex is a complete graph

of dimension , an edge is a complete graph of dimension and a triangle is a complete graph

of dimension . Let denote the set of complete subgraphs of of dimension .

We have and the set of triangles in and the set of tetrahedra in .

Let be the number of elements in .

The number is called the

Euler characteristic of . For a graph without tetrahedra for example, we have

, where we wrote . For example, for an octahedron or

icosahedron, we have . More generally, any triangularization of a two dimensional sphere

has . The cube graph has no triangles so that illustrating that we see

it as a sphere with holes punched into. For a discretisation of a sphere with holes, we

have . If for example, where we have holes, we can identify the boundaries

of the holes without changing the Euler characteristic and get a torus.

Often, graphs are considered as ”curves”, one dimensional objects in which higher dimensional

structures are neglected. The most common point of view is to disregard even the two-dimensional

structures obtained from triangles and define the Euler characteristic of a graph as

, where is the number of vertices and the number of edges.

For a connected graph this is then often written as , where is called the genus.

It is a linear algebra computation to show that the Euler characteristic

is equal to the cohomological Euler characteristic , where is the

dimension of the cohomology group . For example, is the number of connected

components of the graph and is the ‘number of holes” the genus of the curve.

Ignoring higher dimensional structure also means to ignore higher dimensional cohomologies

which means that the Euler-Poincaré formula is or .

Given a subset of the vertex set, it generates a graph which has

as edge set all the pairs of with . A vertex is called

a neighbor of if .

If is a vertex of , denote by the unit sphere of of . It is

the graph generated by the set of neighbors of . Given a subgraph

of , we can build a new graph

called pyramid extension over . We can define a class of contractible graphs

as follows: the one point graph is contractible. Having defined contractibility for graphs

of order , a graph of order is contractible if there exists a contractible subgraph

of such that is a pyramid extension over .

Having a notion of contractibility allows to define critical point properly.

And critical points are one of the most important notions in calculus.

Given an injective function on the vertex set , a vertex is called a

critical point of if is

empty or not contractible. Because contractible graphs have Euler characteristic ,

vertices for which is nonzero are critical points. As in the continuum, there

are also critical points with zero index.

Lets look at examples of graphs: the complete graph is an dimensional simplex. They all have Euler characteristic . The circular graph is a one-dimensional geometric graph. The Euler characteristic is . Adding a central vertex to the circular graph and connecting them to all the vertices in produces the wheel graph . If the original edges at the boundary are removed, we get the star graph . All the and are contractible and have Euler characteristic . The linear graph consists of vertices connected with edges. Like the star graph it is also an example of a tree. A tree is a graph graph without triangles and subgraphs . Trees are contractible and have Euler characteristic . The octahedron and icosahedron are examples of two dimensional geometric graphs. Like the sphere, they have Euler characteristic .

Appendix B: Historical notes

For more on the history of calculus and functions and people,

see [11, 7, 9, 18, 8, 17, 33, 5, 58, 6, 62, 16].

Archimedes (287-212 BC) is often considered the father of integral calculus as he introduced

Riemann sums with equal spacing. Using comparison and

exhaustion methods developed earlier by Eudoxos (408-347 BC), he

was able to compute volumes of concrete objects

like the hoof, domes, spheres or areas of the circle or regions below

a parabola. Even so the concept of function is now very natural to us,

it took a long time until it entered the mathematical vocabulary.

[8] argues that tabulated function values used in ancient astronomy

as well as tables of cube roots and the like can be seen as evidence that

some idea of function was present already in antiquity. It was

Francois Viète (1540-1603) who introduced variables leading to

what is now called “elementary algebra” and

René Descartes (1596-1650) who introduced analytical geometry as well as

Pierre de Fermat (1601-1665) who studied also extremal problems and

Johannes Kepler (1571-1630) who acceleration as rate of change of

velocity and also optimized volumes of wine casks or computed what we would call today

elliptic integrals or trigonometric functions.

As pointed out for example in [15], new ideas are

rarely without predecessors. The notion of coordinate for example has been anticipated

already by Nicole Oresme (1323-1392) [9].

Dieudonné, who praises the idea of function as a “great

advance in the seventeenth century”, points out that first examples of plane curves

defined by equations can be traced back to the fourth century BC.

While ancient Greek mathematicians already had a notion

of tangents, the notion of derivative came only with Isaac Barrow (1630-1703)

who computed tangents with a method we would today called implicit differentiation.

Isaac Newton introduced derivatives on physical grounds using different terminology

like “fluxions”. Until the 18th century, functions were treated as an analytic expression

and only with the introduction of set theory due to Georg Cantor, the modern

function concept as a single-valued map from a set to a set appeared.

From [49]:

”The function concept is one of the most fundamental concepts of modern

mathematics. It did not arise suddenly. It arose more than two hundred years ago

out of the famous debate on the vibrating string”.

The word “function” as well as modern calculus notation came to us through

Gottfried Leibniz (1646-1716) in 1673. ([8] tells that

the term “function” appears the first time in print in 1692 and 1694).

Trig functions entered calculus with Newton in 1669 but were included in textbooks only in

1748 [33]. Peter Dirichlet (1805-1859) gave

the definition still used today stressing that for the definition

it is irrelevant on how the correspondence is established.

The notation as a value of evaluated at a point came even later through

Leonard Euler (1707-1783) and functions of several variables only appeared

at the beginning of the eighteenth century.

When Fourier series became available with Jean Baptiste Fourier (1768-1830) [22], one started to distinguish between “function” and “analytic expression” for the function. The concept has evolved ever since. One can see a function as a subset of the Cartesian product such that has exactly one point. A more algorithmic point of view emerged with the appearance of computer science pioneered by Fermat and Blaise Pascal (1623-1662). It is the concept of a function as a “rule” assigning to an “input” an “output” . A notion of Turing machine made precise what it means to “compute” . After the notion of analytic continuation has sunk in by Bernhard Riemann (1826-1866), it became clear that a function can be a world by itself with more information than anticipated. The zeta function for example, given as a sum can be extended beyond the domain , where the sum is defined to the entire complex plane except . We already know in school calculus that the geometric sum makes sense for if written as defining so even if the sum diverges. The theory of Riemann surfaces shows that functions often have an extended life as geometric objects. We have also learned that there are functions which are not computable. The function which assigns to a Turing machine the value if it halts and if not for example is not computable. The geometric point of view is how everything has started: functions were perceived as geometry very early on. The relation for example would have been seen by Pythagoras as a relation of areas of three squares built from a right angle triangles and mathematicians like Brahmagupta (598-670) or Al-Khwarizmi (780-850) saw the construction of roots of the quadratic equation as a geometric problem about the area of some region which when suitably completed becomes a square.

Appendix C: Mathematica code

Here are some of the basic functions:

Here is an illustration of the fundamental theorem of calculus:

And here is an example of a Taylor expansion leading to en interpolation.

The functions can also be defined using more general “Planck constant” :

Here are some graphs, already built into the computer algebra system:

6. Calculus flavors

Calculus exists in many different flavors. We have infinite-dimensional

versions of calculus like functional analysis and calculus of variations,

calculus has been extended to less regular geometries and functions using

the language of geometric measure theory, integral geometry or the theory of

distributions. Calculus in the complex in the form of complex analysis has

become its own field and calculus on more general spaces is known as

differential topology, Riemannian geometry or algebraic geometry, depending

on the nature of the objects and the choice of additional structures.

The term “quantum calculus” is used in many different contexts as mathematical objects can be

“quantized” in different ways. One can discretize, replace commutative algebras

with non-commutative algebras, or replace classical variational problems with path

integrals. “Quantized calculus” is part of a more general quantum calculus,

where a measure on the real line is chosen leading to the derivative

.

Quantized calculus is a special case, when is the Lebesgue measure and

quantum calculus is the case when is a Dirac measure so that .

The measure defining the derivative has a smoothing effect if it is applied to space of derivatives.

[12] defines quantized calculus as a derivative , where is a selfadjoint

operator on a Hilbert space satisfying . The Hilbert transform has this property.

Real variables are replaced by self-adjoint operator, infinitesimals

are compact operators , the integral is the Dixmier trace and integrable functions are replaced

by compact operators for which exists in a suitable sense,

where are the eigenvalues of the operator arranged in decreasing order.

The Dixmier trace neglects infinitesimals, compact operators for which .

A Fredholm module is a representation of an algebra as operators in the Hilbert space

such that is infinitesimal (=compact) for all . In the simplest case, for

single variable calculus, is the Hilbert transform.

It is evident that quantum calculus approaches like [12] (geared towards geometry) and

[32] (geared towards number theory) would need considerable

adaptations to be used in a standard calculus sequence for non-mathematicians. Quantum calculus flavors

already exist in the form of business calculus, where the concept of limit is discarded.

For a business person, calculus can be done on spreadsheets, integration is the process of adding

up rows or columns and differentiation is looking at trends, the goal of course being to integrate

up the changes and get trends for the future. Books like [30] (a “brief edition” with 800 pages)

however follow the standard calculus methodology.

I personally believe that the standard calculus we teach today is and will remain an important

benchmark theory which has a lot of advantages over discretized calculus flavors. From experience, I noticed

for example that having to carry around an additional discretization

parameter can be a turn-off for students. This is why in the talk,

was assumed. In the same way as classical mechanics is an elegant idealization of

quantum mechanics and Newtonian mechanics is a convenient limit of general relativity,

classical calculus is a teachable idealisation of a more general quantum calculus.

Still, a discrete approach to calculus could be an option for

a course introducing proofs or research ideas. Many of the current

calculus books have grown to huge volumes and resemble each other even to the point

that different textbooks label chapters in the same order and that problems resemble each other,

many of them appear generated by computer algebra systems.

But as many newcomers have seen, the transition from a standard textbook to a new textbook is hard.

If there are too many changes even if it only affects the order in which the material is taught,

then this can alienate the customer. Too fast innovation destroys its sales.

Innovative approaches are seldom successful commercially, especially because college

calculus systems have become complicated machineries, where larger courses with

different sections are coordinated and teams of teachers

and course assistants work together. When looking at the history of calculus

textbooks from the past, over decades or centuries, we can see that the development

today is still astonishingly fast today and that the variety has never been bigger.

A smaller inquiry based or proof based course aiming to have students

in a “state of research” can benefit from fresh approaches. The reason

is that asking to reprove standard material have become

almost impossible today. It is due to the fact that one can look up proofs so

easily today: just enter the theorem into a search engine and almost certainly a

proof can be found. It is no accident

that more inquiry based learning stiles have flourished in a time when point set topology

has been developed. Early point set topology for example was a perfect toy to

sharpen research skills. It has become almost impossible now to

make any progress in basic set topology because the topic has been cataloged

so well. When developing a new theorem, a contemporary student almost certainly

will recover a result which is a special case of something which has been

found 50-100 years ago. In calculus it is even more extreme because the theorems

taught have been found 200-300 years ago.

Learning old material in a new form is always exciting. I myself have learned calculus the standard way but then seen it again in a “nonstandard analysis course” given by Hans Läuchli. The course had been based on the article [52]. We were also recommended to read [57], a book which stresses in the introduction how Euler has worked already in a discrete setting. Euler would write , where is a number of infinite size (Euler: ”n numerus infinite magnus”) ([21] paragraph 155). Nelson also showed that probability theory on finite sets works well [53]. There are various textbooks which tried nonstandard analysis. One which is influenced by the Robinson approach to nonstandard analysis is [34]. But nonstandard analysis has never become the standard. It remains true to its name.

7. Calculus textbooks

The history of calculus textbooks is fascinating and would deserve to be written down

in detail. Here are some comments about some textbooks from my own calculus library.

The first textbook in calculus is L’Hôpital’s

“Analyse des Infiniment Petits pour l’Intelligence des Lignes Courbes” [14],

a book from 1696, which had less than 200 pages and still contains 156 figures.

Euler’s textbook [21] on calculus starts the text with a modern treatment of

functions but still emphasis ”analytic expressions”. Euler for example would hardly

considered the rule which assigns to an irrational numbers and on rational number,

to be a function. Euler uses already in that textbook already his formula

extensively but in material is closer of what we

consider “precalculus” today, even so it goes pretty far, especially with

series and continued fraction expansions. An other master piece is

the textbook of Lagrange [45].

[33] mentions textbooks of the 18th century with authors

C. Reyneau,G. Chayne,C. Hayes,H. Ditton,J. Craig,E. Stone,J. Hodgson, J. Muller or T. Simpson.

Hardy’s book [28], whose first edition came out in 1908 also contains a

substantial real analysis part and uses already the modern function approach. It no more

restricts to “analytic expressions” but also allows functions to be limiting

expressions of series of functions. It is otherwise a single variable text book.

From about the same time is [50], which is more than 100 years old but resembles

in style and size modern textbooks already, including lots of problems, also some of

applied nature.

The book [23] is a multivariable text which has many applications to

physics and also contains some differential geometry.

The book [46] is remarkable because it might be where we “stole” the first

slide of our talk from, mentioning sticks and pebbles to make the first steps in calculus.

This book weights only 150 pages but covers lots of ground.

[55] treats single variable on 200 pages with a decent amount of

exercises and [29] manages with the same size to cover a fair amount of multivariable

calculus and tensor analysis, differential geometry and calculus of variations

in three dimensions, uses illustrations however only sparingly. The structure of Hay’s book

is in parts close to modern calculus textbooks like [56, 61, 63, 27].

many of them started to grow fatter. The textbook [65] for example has already 420

pages but covers single and multivariable calculus,

real analysis and measure theory, Fourier series and partial differential equations. But it is

no match in size to books like [27] with 1318 pages or Stewart with about the same size.

Important in Europe was [13] which had been translated into other

language and which my own teachers still recommended. Its influence is clearly visible

in all major textbooks which are in use today. [47] made a big

impact as it is written with great clarity.

Since we looked at a discrete setting, we should mention that calculus books based

on differences have appeared already 60 years ago. The book [31] illustrates

the difficulty to find good notation. This is a common obstacle with discrete

approaches, especially also with numerical analysis books. Discrete calculus often suffers

from ugly notation using lots of indices. One of the reason why Leibnitz calculus has

prevailed is the use of intuitive notation. For a modern approach see [26].

Not all books exploded in size. [24] covers in 120 pages quite a bit of real analysis and multivariable calculus. But books would become heavier. [2] already counted 725 pages. It was intended for a three semester course and stated in the introduction: there is an element of truth in the old saying that the Euler textbook ’Introductio in Analysin Infinitorum, (Lausannae, 1748)’ was the first great calculus textbook and that all elementary calculus textbooks copied from books that were copied from Euler. The classic [35] had already close to 1000 pages and already included a huge collection of problems. Influential for the textbooks of our modern time are also Apostol [3, 4] which I had used myself to teach. It uses elements of linear algebra, probability theory, real analysis, complex numbers and differential equations. Its influence is also clearly imprinted on other textbooks. The book [19] was one of the first which dared to introduce calculus in arbitrary dimensions using differential forms. Since then, calculus books have diversified and exploded in general in size. There are also exceptions: original approaches include [59, 60, 51, 48, 54, 1, 44, 20, 25, 36].

8. Tweets

We live in an impatient twitter time. Here are two actually tweeted 140 character

statements which together cover the core of the fundamental theorem of calculus:

With and inverse , define . For example, , , , .

and

gives . With , the fundamental theorem holds.

References

- [1] C. Adams, A. Thompson, and J. Hass. How to Ace Calculus, The Streetwise guide. Henry Holt and Company, LLC, 1998.

- [2] R.P. Agnew. Calculus, Analytic Geometry and Calculus, with Vectors. McGraw-Hill Book Company, Inc, New York, 1962.

- [3] T.M. Apostol. One-variable calculus, introduction to linear algebra. John Wiley and Suns, New York, second edition edition, 1967.

- [4] T.M. Apostol. Calculus: Multivariable Calculus and Linear algebra with applications to differential equations and probability theory. John Wiley and Suns, New York, second edition edition, 1969.

- [5] V.I. Arnold. Huygens and Barrow, Newton and Hooke. Birkhäuser, 1990.

- [6] J.S. Bardi. The Calculus wars. Thunder’s Mouth Press, New York, 2006.

- [7] E.T. Bell. Men of Mathematics, the lives and achievements of the great mathematicians from Zeno to Poincare. Penguin Books, Melbourne, London, Baltimore, 1937-1953.

- [8] U. Bottazzini. The Higher Calculus, A History of Real and Complex Analysis from Euler to Weierstrass. Springer Verlag, 1986.

- [9] C.B. Boyer. The History of the Calculus and its Conceptual Development. Dover Publications, 2 edition, 1949.

- [10] D. M. Bressoud. Historical reflections on teaching the fundamental theorem of integral calculus. American Mathematical Monthly, 118:99–115, 2011.

- [11] F. Cajori. A history of Mathematics. MacMillan and Co, 1894.

- [12] A. Connes. Noncommutative geometry. Academic Press, 1994.

- [13] R. Courant. Differentrial and Integral Calculus, Volume I and II. Interscience Publishers, Inc, New York, 1934.

- [14] G. de L’Hôpital. Analyse des Infiniment Petits pour l’Intelligence des Lignes Courbes. Francois Montalant, Paris, second edition, 1716. first edition 1696.

- [15] J. A. Dieudonne. Mathematics - the music of reason. Springer Verlag, 1998.

- [16] W. Dunham. The Calculus Gallery, Masterpieces from Newton To Lebesgue. Princeton University Press, 2005.

- [17] W. Dunham. Touring the calculus gallery. Amer. Math. Monthly, 112(1):1–19, 2005.

- [18] C.H. Edwards. The historical Development of the Calculus. Springer Verlag, 1979.

- [19] H.M. Edwards. Advanced Calculus, A differential Forms Approach. Birkhäuser, 1969-1994.

- [20] I. Ekeland. Exterior differnential Calculus and Applications to Economic Theory. Sculoa Normale Superiore, Pisa, 1998.

- [21] L. Euler. Einleitung in die Analysis des Unendlichen. Julius Springer, Berlin, 1885.

- [22] J-B.J. Fourier. Théorie Analytique de la Chaleur. Cambridge University Press, 1822.

- [23] J.W. Gibbs and E.B. Wilson. Vector Analysis. Yale University Press, New Haven, 1901.

- [24] A. M. Gleason. Linear analysis and Calculus, Mathematics 21. Harvard University Lecture Notes, 1972-1973.

- [25] L. Gonick. The Cartoon Guide to Calculus. William Morrow, 2012.

- [26] L.J. Grady and J.R. Polimeni. Discrete Calculus, Applied Analysis on Graphs for Computational Science. Springer Verlag, 2010.

- [27] I.C. Bivens H. Anton and S. Davis. Calculus, 10th edition. Wiley, 2012.

- [28] G.H. Hardy. A course of pure mathematics. Cambridge at the University Press, third edition, 1921.

- [29] G.E. Hay. Vector and Tensor analysis. Dover Publications, 1953.

- [30] L.D. Hoffmann and G.L. Bradley. Calculus, for Business, Economics, and the social life sciences. McGraw Hill, brief edition, 2007.

- [31] C. Jordan. Calculus of finite differences. Chelsea publishing company, New York, 1950.

- [32] V. Kac and P. Cheung. Quantum calculus. Universitext. Springer-Verlag, New York, 2002.

- [33] V.J. Katz. The calculus of the trigonometric functions. Historia Math., 14(4):311–324, 1987.

- [34] H.J. Keisler. Elementary Calculus, An infinitesimal approach. Creative Commons, second edition, 2005.

- [35] M. Kline. Calculus. John Wiley and Sons, 1967-1998.

- [36] S. Klymchuk and S. Staples. Paradoxes and Sophisms in Calculus. MAA, 2013.

-

[37]

O. Knill.

A graph theoretical Gauss-Bonnet-Chern theorem.

http://arxiv.org/abs/1111.5395, 2011. -

[38]

O. Knill.

A graph theoretical Poincaré-Hopf theorem.

http://arxiv.org/abs/1201.1162, 2012. -

[39]

O. Knill.

On index expectation and curvature for networks.

http://arxiv.org/abs/1202.4514, 2012. -

[40]

O. Knill.

The theorems of Green-Stokes,Gauss-Bonnet and Poincare-Hopf in Graph

Theory.

http://arxiv.org/abs/1201.6049, 2012. -

[41]

O. Knill.

The Dirac operator of a graph.

http://http://arxiv.org/abs/1306.2166, 2013. -

[42]

O. Knill.

Classical mathematical structures within topological graph theory.

http://arxiv.org/abs/1402.2029, 2014. - [43] O. Knill and O. Ramirez-Herran. Space and camera path reconstruction for omni-directional vision. Retrieved February 2, 2009, from http://arxiv.org/abs/0708.2438, 2007.

- [44] H. Kojama. Manga Guide to Calculus. Ohmsha, 2009.

- [45] J.L. Lagrange. Lecons sur le calcul des fonctions. Courcier, Paris, 1806.

- [46] C.A. Laisant. Mathematics, Illustrated. Constable and Company Ltd, London, 1913.

- [47] S. Lang. A first course in Calculus. Springer, fifth edition, 1978-1986.

- [48] M. Levi. The Mathematical Mechanic. Princeton University Press, 2009.

- [49] N. Luzin. Function. I,II. Amer. Math. Monthly, 105(1):59–67, 263–270, 1998.

- [50] D.A. Murray. A first course in infinitesimal calculus. Longmans, Green and Co, New York, 1903.

- [51] Paul J. Nain. When least is best. Princeton University Press, 2004.

- [52] E. Nelson. Internal set theory: A new approach to nonstandard analysis. Bull. Amer. Math. Soc, 83:1165–1198, 1977.

- [53] E. Nelson. Radically elementary probability theory. Princeton university text, 1987.

- [54] I. Niven. Maxima and Minima without Calculus, volume 6 of Dolciani Mathematical Expositions. MAA, 1981.

- [55] W.F. Osgood. Elementary Calculus. MacMillan Company, 1921.

- [56] A. Ostebee and P. Zorn. Multivariable Claculus. Sounders College Publishing, 1998.

- [57] A. Robert. Analyse non standard. Presses polytechniques romandes, 1985.

- [58] A. Rosenthal. The history of calculus. Amer. Math. Monthly, 58:75–86, 1951.

- [59] H.M. Schey. div grad curl and all that. Norton and Company, New York, 1973-1997.

- [60] J.C. Sparks. Calculus without limits - Almost. Author House, third edition, 2007.

- [61] J. Stewart. Calculus, Concepts and contexts. Brooks/Cole, 4e edition, 2010.

- [62] M.B.W. Tent. Gottfried Wilhelm Leibniz, the polymath who brought us calculus. CRC Press, 2012.

- [63] G.B. Thomas, M.D. Weir, and J.R. Hass. Thomas’ Calculus, Single and Multivariable, 12th edition. Pearson, 2009.

- [64] J. Wästlund. A yet simpler proof of the chain rule. American Mathematical Monthly, 120:900, 2013.

- [65] D.V. Widder. Advanced Calculus. Prentice-Hall, Inc, New York, 1947.