Testing for independence between functional time series

Abstract.

Frequently econometricians are interested in verifying a relationship between two or more time series. Such analysis is typically carried out by causality and/or independence tests which have been well studied when the data is univariate or multivariate. Modern data though is increasingly of a high dimensional or functional nature for which finite dimensional methods are not suitable. In the present paper we develop methodology to check the assumption that data obtained from two functional time series are independent. Our procedure is based on the norms of empirical cross covariance operators and is asymptotically validated when the underlying populations are assumed to be in a class of weakly dependent random functions which include the functional ARMA, ARCH and GARCH processes.

Key words and phrases:

functional observations, tests for independence, weak dependence, long run covariance function, central limit theoremResearch supported by NSF grant DMS 1305858

1. Introduction and results

A common goal of data analysis in econometrics is to determine whether or not a relationship exists between two variables which

are measured over time. A determination in either way may be useful. On one hand, if a relationship is confirmed to exist between two variables

then further investigation into the strength and nature of the

relationship may lead to interesting insights or effective predictive models. Conversely if there is no

relationship between the two variables then an entire toolbox of

statistical techniques developed to analyze two samples which are

independent may be used. The problem of testing for correlation between

two univariate or multivariate time series has been well treated, and we

discuss the relevant literature below. However, as a by product of

seemingly insatiable modern data storage technology, many data of interest

exhibit such large dimension that traditional multivariate techniques are not

suitable. For example, tick by tick stock return data is stored hundreds

of times per second, leading to thousands of observations during a single

day. In such cases a pragmatic approach is to treat the data as densely

observed measurements from an underlying curve, and, after using the

measurements to approximate the curve, apply statistical techniques to the

curves themselves. This approach is fundamental in functional data

analysis, and in recent years much effort has been put forth to adapt

currently available procedures in multivariate analysis to functional

data. The goal of the present paper is to develop a test for independence

between two functional time series.

In the context of checking for independence between two second order

stationary univariate time series, Haugh (1976) proposed a testing

procedure based on sample cross–correlation estimators. His test may be

considered as an adaptation of the popular Box–Ljung–Pierce portmanteau

test (cf. Ljung and Box (1978)) to two samples. In a similar progression

the multivariate portmanteau test of Li and Mcleod (1981) was extended

to test for correlation between two multivariate ARMA time series by El Himdi

and Roy (1997) whose test statistic was based on cross–correlation

matrices. The literature on such tests has also grown over the years to

include adaptations for robustness as well as several other

considerations, see Koch and Yang (1986), Li and Hui (1996) and El Himdi et

al (2003) for details. Many of these results are summarized in Li (2004).

A separate approach for multivariate data based on the distance correlation measure is developed in Székely and Rizzo (2013).

The analysis of functional time series has seen increased attention in

statistics, economics and in other applications over the last decade, see Horváth and Kokoszka

(2012) for a summary of recent advances. To test for independence within a

single functional time series, Gabrys and Kokoszka (2007) proposed a

method where the functional observations are projected onto finitely many

basis elements, and a multivariate portmanteau test is applied to the

vectors of scores which define the projections. Horváth et al (2013)

developed a portmanteau test for functional data in which the inference is

performed using the operator norm of the empirical covariance operators at

lags , , which could be considered as a direct

functional analog of the Box–Ljung–Pierce test. Due to the infinite

dimension of functional data, a normal limit is established for the test

statistic rather than the classical limit with degrees of freedom

depending on the data dimension.

The method that we propose for testing noncorrelation between two

functional time series follows the example of Horváth et al (2013).

Suppose that we have observed and

which are samples from jointly stationary sequences

of square integrable random functions on [0,1]. Formally we are interested

in testing

against the alternative

| for some integer , , | |||

| where . |

We use the notation to mean . Assuming jointly Gaussian distributions for the underlying observations, independence reduces to zero cross–correlations at all lags, and hence is equivalent to the complement of in that case. To derive the test statistic, we note that under , the sample cross–covariance functions

should be close to the zero function for all choices of , where

Under a cross covariance function is different from the zero function for at least one . The test statistic is then based on

with the hope that it includes the covariance estimator corresponding to

a non zero function if it exists. We then reject for large values of

. Our main result is the asymptotic distribution of under .

In order to cover a large class of functional time series processes, we assume that and are approximable Bernoulli shifts.

We say that is an absolutely

approximable Bernoulli shift in if

| (1.1) | ||||

| (1.2) |

and

| (1.3) | ||||

In assumption (1.1) we take to be an arbitrary measurable space, however in most applications is itself a function space and the evaluation of is a functional of . In this case assumption (1.2) follows from the joint measurability of the ’s.

Assumption (1.3) is stronger than the requirement used by Hörmann and Kokoszka (2010), Berkes et al (2013) and Jirak (2013) to establish the central limit theorem for sums of Bernoulli shifts. Since we need the central limit theorem for sample correlations, higher moment conditions and a faster rate in the approximability with –dependent sequences are needed.

We assume that the sequences and satisfy the following conditions:

Assumption 1.1.

and with some ,

Assumption 1.2.

is an absolutely approximable Bernoulli shift in ,

and

Assumption 1.3.

is an absolutely approximable Bernoulli shift in .

The functions defining the Bernoulli shift sequences and as in (1.1) will be denoted by and , respectively. The independence of the sequences and stated under is conveniently given by:

Assumption 1.4.

The sequences and are independent.

The parameter defines the number of lags used to define the test statistic. As increases it becomes possible to accurately estimate cross covariances for larger lags, and thus we allow to tend to infinity with the sample size. Namely,

Assumption 1.5.

and , as , with some , where is defined in Assumption 1.1.

To state the limit result for we first introduce the asymptotic expected value and variance. Let for all

and define

| (1.4) |

It is shown in Lemma B.1 that under Assumptions 1.2 and 1.3 the infinite sum in the definition of above is absolutely convergent. Let

and

| (1.5) |

Theorem 1.1.

Upon the estimation of and this result supplies an asymptotic test for .

The rest of the paper is organized as follows. In Section 2 we discuss the estimation of the parameters appearing in Theorem 1.1 as well as a simulation study of how the limit result is manifested in finite sample sizes. The statistical utility of Theorem 1.1 is then illustrated by an application to tick data from several stocks listed on the NYSE. The proof of the main result is given in Section 3. The paper concludes with two appendices which contain some technical results needed in Section 3.

2. Finite sample properties and an application

2.1. Parameter estimates

In order to use Theorem 1.1 for data analysis it is necessary to estimate and from the sample. Let

and

Since is an infinite sum of integrated correlations, it is natural to use a kernel estimator of the form

where is a kernel function with window . According to the definition in (1.5), is an infinite sum of integrals of squared correlations and so we can use again a kernel type estimator:

where is a kernel with window ,

We note that is essentially the long run variance of the integrals , and is the correlation of lag between these integrals. Hence can be considered as an estimated correlation and is a kernel long run variance estimator based on the estimated correlations. We assume that the kernels satisfy standard regularity conditions: (i) , (ii) is continuous and bounded (iii) there is such that if . It can be shown if as , then under Assumption 1.5. If , as , then one can show that in probability as . Hence Theorem 1.1 yields

| (2.1) |

where stands for a standard normal random variable.

2.2. Simulation study

We now turn to a small simulation study which compares the limit result in Theorem 1.1 to the finite sample behavior of . In order to describe the data generating processes (DGP’s) used below, let and be independent sequences of iid standard Brownian motions on . Two DGP’s were considered which each satisfy the conditions of Theorem 1.1:

and

The motivation behind using Brownian motions for the error sequences in each of the DGP’s is due to our application in Section 2.3 to cumulative intraday returns which often look like realizations of Brownian motions, see Figure 2.2 below. A precise but somewhat technical condition for the existence of a stationarity solution in the FARq(1) model is given in Bosq (2000), however it is sufficient to assume that the operator norm of is less than one. In our case we take so that , respectively. To simulate the stationary FARq(1) process we used a burn in sample of size 100 starting from an independent innovation. In order to compute the statistic of (2.1) we must select the kernels and as well as the windows and used to compute the estimates and . For our analysis we used Bartlett kernels

and windows . The simulations results below were repeated for several other common choices of kernel functions including the Parzen and flat–top kernels, as well as different choices for the window parameters. The changes in the results were negligible for different choices of the kernel functions. The results were also stable over window choices between to which constitute the usual range of acceptable windows. Each DGP was simulated 1000 times independently for various values of and , and the percentage of test statistics which exceeded the 10, 5, and 1 percent critical values of the standard normal distribution are reported in Table 2.1.

| DGP | IID | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| H | 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | |

| 50 | 2 | 13.8 | 8.0 | 2.7 | 9.7 | 6.1 | 2.8 | 15.2 | 10.7 | 4.8 | 24.3 | 17.4 | 8.0 |

| 5 | 14.6 | 7.8 | 3.1 | 11.4 | 6.3 | 2.9 | 16.4 | 11.1 | 4.1 | 26.0 | 20.7 | 11.8 | |

| 7 | 13.2 | 7.6 | 3.8 | 10.2 | 6.0 | 2.1 | 15.5 | 10.4 | 5.0 | 33.0 | 25.4 | 13.7 | |

| 100 | 3 | 11.5 | 7.0 | 2.7 | 9.5 | 6.0 | 2.4 | 12.4 | 7.0 | 3.1 | 26.8 | 20.1 | 13.3 |

| 5 | 10.3 | 5.1 | 2.1 | 8.5 | 4.7 | 0.8 | 12.8 | 7.2 | 3.8 | 26.4 | 22.5 | 15.8 | |

| 10 | 9.8 | 3.9 | 1.3 | 8.7 | 3.8 | 0.9 | 11.4 | 6.5 | 2.7 | 32.0 | 27.3 | 20.1 | |

| 200 | 4 | 10.0 | 6.6 | 2.5 | 10.2 | 5.8 | 2.1 | 10.9 | 6.4 | 3.0 | 16.5 | 12.8 | 7.2 |

| 7 | 8.7 | 4.8 | 1.2 | 11.0 | 7.1 | 2.5 | 10.5 | 6.0 | 1.9 | 21.4 | 17.7 | 12.6 | |

| 15 | 9.8 | 5.2 | 1.3 | 8.4 | 4.3 | 1.7 | 10.4 | 7.0 | 2.7 | 25.5 | 20.6 | 14.7 | |

| 300 | 5 | 10.3 | 5.4 | 1.2 | 9.7 | 6.0 | 2.1 | 9.7 | 5.5 | 2.2 | 15.3 | 10.5 | 6.8 |

| 10 | 10.5 | 5.7 | 1.4 | 10.0 | 5.7 | 2.3 | 10.4 | 5.3 | 1.9 | 21.0 | 18.1 | 12.7 | |

| 17 | 9.8 | 4.7 | 1.1 | 10.1 | 5.1 | 1.2 | 10.9 | 5.7 | 2.4 | 26.4 | 22.5 | 16.4 | |

Based on this data we have the following remarks:

-

(i)

When the level of dependence within the processes is not too strong the tail of the distribution of appears to be approaching that of the standard normal as .

-

(ii)

There appears to be little effect in the results due to the choice of when the dependence is weak. Even for values of close to we still observe finite sample distributions which are close to the limit.

-

(iii)

When the dependence is strong , i.e. , the tail of the distribution of becomes significantly heavier than that of the standard normal. This effect is worsened by increasing .

-

(iv)

In the context of hypothesis testing, achieves good size even when the temporal dependence is weak to moderate as long as the sample size is large. If strong dependence is suspected in the data then the distribution of may be skewed to the right.

2.3. Application to cumulative intraday stock returns

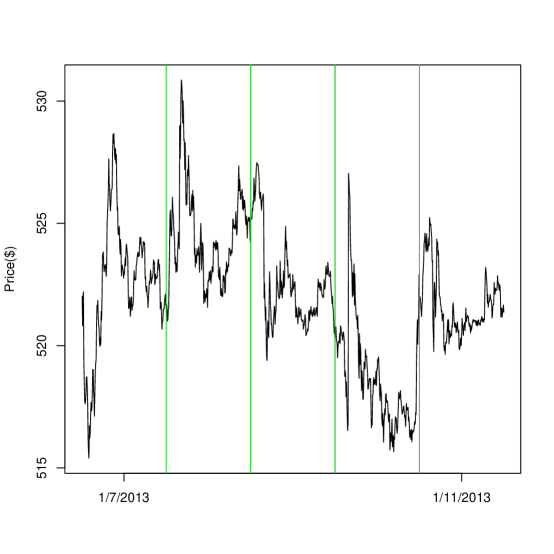

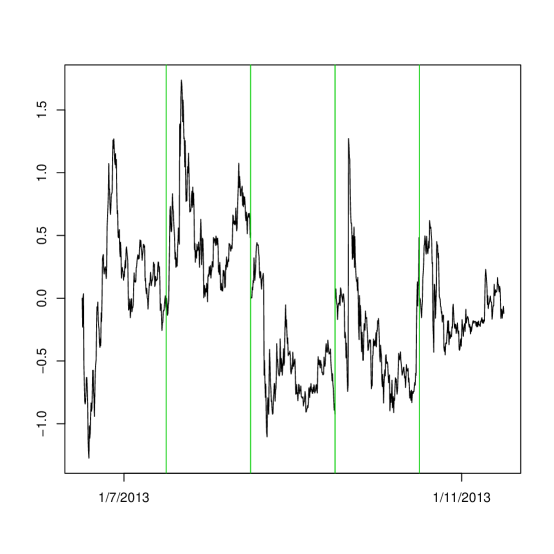

A natural example of functional data are intraday price curves constructed from densely observed price records of an asset. Five of such curves constructed from the 1 minute average stock price of Apple are shown in Figure 2.1. Several authors have studied the analysis of the shapes of price curves, see Müller et al (2011) and Kokoszka et al (2013) for a small sample of such work. In our application we use (2.1) to test for correlation between samples of curves constructed from pairs of 20 of the highest trade volume stocks listed on the New York Stock Exchange. The data we consider was obtained from www.nasdaq.com and www.finam.com and consists of the 1 minute average stock prices of the stocks listed in Table 2.2 from January 1st, 2013 to December 11, 2013, which comprise 254 daily records per stocks. Since the test statistic is based on integrals of the sampled curves its value changes little due to the way the curves are constructed from the original observations, and thus we simply used linear interpolation. It is argued in Horváth et al (2014) that price curves themselves are typically not stationary and thus must be suitably transformed before analysis assuming stationarity may be performed. Scaler price data is typically transformed to appear closer to stationary by taking the log differences, and in our example we employ a similar technique for functional data which was proposed in Gabrys et al (2010):

Definition 2.1.

Suppose , is the price of a financial asset at time on day . The functions

are called the cumulative intraday returns (CIDR’s).

| Company Name | Ticker Symbol | Company Name | Ticker Symbol |

|---|---|---|---|

| Apple | AAPL | AT&T | ATT |

| Bank of America | BAC | Boeing | BA |

| Chevron | CVX | Cisco Systems | CSCO |

| Citigroup | C | Coca Cola | KO |

| DuPont | DD | Exxon Mobil | XOM |

| GOOG | HP | HPQ | |

| IBM | IBM | Intel | INTC |

| McDonalds | MCD | Microsoft | MSFT |

| Verizon | VZ | Walmart | WMT |

| Disney | DIS | Yahoo | YHOO |

The CIDR’s of the five curves in Figure 2.1 are shown in Figure 2.2. It is apparent that the overall shapes of the price curves are retained by the CIDR’s and, since the CIDR’s always start from zero, level stationarity is enforced. A more rigorous argument for the stationarity of the CIDR’s is given in Horváth et al (2014).

Based on the 20 stocks we used there are 190 pairs of CIDR samples for comparison. For each pair the test statistic was computed as outlined in Section 2.2 using and . An approximate –value of the test was then calculated by taking , where is the standard normal distribution function. Of the 190 –values computed 70% were less than .05 indicating that there is strong correlation between the CIDR’s of most pair of stocks listed on the NYSE. More insight can be achieved by looking at individual comparisons. Table 2.3 contains the –values of all comparisons of a subset of 9 of the stocks. Some clusters are apparent, like the technology companies (AAPL,IBM,GOOG), energy companies (CVX,XOM) and service companies (WMT,DIS,MCD) for which all of the within group comparisons give effectively zero -values. Also many of the comparisons between the tech companies and energy companies yielded large –values, indicating that these groups of CIDR’s exhibit little cross correlation. Similar clusters became apparent among the rest of the sample of 20 stocks, and using cluster analysis methods based on the values of could lead to further insights. For example, one could say that stocks A and B are similar if the value of computed between the CIDR’s from A and B exceeds a certain threshold, i.e. stocks A and B are highly correlated. This will not lead to perfect clustering, however, using correlation clustering algorithms as in Kriegel et al (2009), the number of similarities across clusters or dissimilarities within clusters can be minimized.

| IBM | .000 | |||||||

|---|---|---|---|---|---|---|---|---|

| GOOG | .001 | .000 | ||||||

| XOM | .541 | .612 | .051 | |||||

| CVX | .531 | .521 | .003 | .000 | ||||

| C | .329 | .007 | .006 | .008 | .001 | |||

| WMT | .602 | .358 | .000 | .001 | .000 | .000 | ||

| DIS | .221 | .002 | .000 | .014 | .000 | .000 | .001 | |

| MCD | .000 | .018 | .457 | .185 | .000 | .133 | .000 | .043 |

| AAPL | IBM | GOOG | XOM | CVX | C | WMT | DIS |

3. Proof of Theorem 1.1

The proof of Theorem 1.1 requires several steps. First we claim that it is enough to prove Theorem 1.1 for the square integrals of the correlations without centering by the sample means. In the second step we argue that can be approximated with the sum of integrated squared correlations of –dependent random functions if and are both large enough. The last step is the proof of the central limit theorem for the sum of integrated squared correlations of –dependent functions for every fixed , when This is established using a blocking argument.

It is easy to see that does not depend on the means of the observations, and so we can assume without loss of generality that

| (3.1) |

In order to simplify the calculations we define

and

Proof.

This claim can be proven by standard arguments so the details are omitted. ∎

For every we define according to Assumption 1.2

| (3.2) |

with where the ’ are independent copies of and independent of The random function is defined analogously by

| (3.3) |

with where the ’ are independent copies of and independent of It follows from the definition that both and are stationary –dependent sequences, independent of each other. Also, for every and we have that and in distribution. Next we introduce

and

We also use the notation

and similarly

in the rest of the proofs.

Proof.

By the stationarity of and we have

It follows from Assumptions 1.2–1.4 that for every fixed

| (3.4) |

For any we write

It follows from (3.4) that for all

| (3.5) |

We prove in Appendix A that there is a constant depending only on and such that for all

| (3.6) |

Hence we get that

| (3.7) |

and therefore by Assumptions 1.2, 1.3 and 1.5

| (3.8) |

Following the proof of Lemma A.1 one can verify that

| (3.9) |

and

| (3.10) |

with the the same as in (3.6). We wish to note that the proofs of (3.9) and (3.10) are simpler than that of (3.6) due to the –dependence of and . Using (3.9) and (3.10) we get that

Lemma 3.3.

Proof.

First we define , and the sets , where is defined as the largest integer satisfying , i.e. . Let

and define

Since the random variables are constructed from –dependent random functions we can assume by letting , that are independent and identically distributed. Using Petrov (1995, p. 58) we get that

Using the stationarity and the –dependence of the ’s and the ’s we obtain that

where only depends on , and . Also, it follows from Appendix B that there is such that

since . Thus by Assumption 1.5 we get that

and so by Lyapunov’s theorem (cf. Petrov (1995, p. 126)) we conclude

where denotes a standard normal random variable.

Next we define the small blocks which do not contribute to the limit. Let . Using Petrov (1995, p. 58) and stationarity we conclude that

| (3.11) |

with some constants and . Since , by independence we obtain that

| (3.12) | ||||

on account of . Let . We can divide into blocks of size and one additional smaller block. The sums of over these blocks give 2 dependent variables so by (3.11) we get that

Thus we have

| (3.13) | ||||

on account of . The same arguments give

where Let . Repeating the proofs of (3.12) and (3.13) one can verify that

completing the proof of Lemma 3.3. ∎

Summary: The problem of testing for independence between two finite dimensional time series has been studied extensively in the literature and most available methods are based on cross covariance estimators. In this paper we established the asymptotic normality of a test statistic constructed from the operator norms of empirical cross covariance operators using functional data. This asymptotic result supplies a test of the null hypothesis that two functional time series are independent. The rate at which the asymptotic result is achieved as the sample size increases was investigated using a Monte Carlo simulation study and the results showed that the limit approximation was accurate for moderate to large sample sizes. Finally we illustrated an application of our limit result to testing for independence between cumulative intraday return curves constructed from the closing prices of stocks.

Acknowledgements: We are grateful to two anonymous referees for their careful reading of our paper and for their helpful insights and remarks.

References

- [1] Berkes, I., Horváth, L. and Rice, G.: Weak invariance principles for sums of dependent random functions. Stochastic Processes and their Applications 123(2013), 385–403.

- [2] Bosq, D.: Linear Processes in Function Spaces. Springer, New York, 2010.

- [3] El Himdi, K. and Roy, R.: Tests for noncorrelation of two multivariate ARMA time series. The Canadian Journal of Statistics, 25(197), 233–256.

- [4] El Himdi, K., Roy, R. and Duchesne, P.: Tests for non–correlation of two multivariate time series: a nonparametric approach. Mathematical Statistics and Applications: Festschrift for Constance van Eeden, 397 -416, IMS Lecture Notes Monogr. Ser., 42, Inst. Math. Statist., Beachwood, OH, 2003.

- [5] Gabrys, R., Hörmann, S. and Kokoszka, P.: Monitoring the intraday volatility pattern. Journal of Time Series Econometrics 5(2013), 87–116.

- [6] Gabrys, R. and Kokoszka, P.: Portmanteau test of independence for functional observations. Journal of the American Statistical Association 102(2007), 1338–1348.

- [7] Haugh, L.D.: Checking the independence of two covariance-stationary time series: a univariate residual cross-correlation approach. Journal of the American Statistical Association, 7(1976), 378 -385.

- [8] Hörmann, S. and Kokoszka, P.: Weakly dependent functional data. Annals of Statistics 38(2010), 1845–1884.

- [9] Horváth, L., Hušková, M. and Rice, G.: Test of independence for functional data. Journal of Multivariate Analysis, 117(2013), 100 -119.

- [10] Horváth, L. and Kokoszka, P.: Inference for Functional Data with Applications. Springer, New York, 2012.

- [11] Horváth, L, Kokoszka, P. and Rice, G.: Testing stationarity of functional time series. Journal of Econometrics (forthcoming), 2014.

- [12] Jirak, M.: On weak invariance principles for sums of dependent random functionals. Statistics & Probability Letters 83(2013), 2291–2296

- [13] Koch, P.D. and Yang, S.: A method for testing the independence of two time series that accounts for a potential pattern in the cross-correlation function. Journal of the American Statistical Association, 81(1986), 533 -544.

- [14] Kokoszka, P., Miao, H. and Zhang, X.: 2013. Functional multifactor regression for intraday price curves. Technical report. Colorado State University, 2013.

- [15] Kriegel, H.–S., Kröger, P. and Zimek, A.: Clustering high–dimensional data: a survey on subspace clustering, and correlation clustering. ACT Transactions on Knowledge Discovery from Data 3(2009), 1.1–1.58.

- [16] Li, W.K.: Diagnostic Checks in Time Series. Chapman and Hall/CRC, New York, 2004.

- [17] Li, W.K. and Hui, Y.Y.: Robust residual cross correlation tests for lagged relations in time series. Journal of Statistical Computations and Simulations. 49(1994), 103–109.

- [18] Li, W.K. and McLeod, A.I.: Distribution of the residual autocorrelations in multivariate ARMA time series models. J. Royal Statistical Society, Ser. B 43(1981), 231–239.

- [19] Ljung, G. and Box, G.: On a measure of lack of fit in time series models. Biometrika 66(1978), 67–72.

- [20] Müller, H–G., Sen, R. and Stadtmüller, U.: 2011. Functional data analysis for volatility. Journal of Econometrics 165(2011), 233 245.

- [21] Petrov, V.V.: Limit Theorems of Probability Theory. Clarendon Press, Oxford, 1995.

- [22] Székely, G. and Rizzo, M.: The distance correlation t–test of independence in high dimension. Journal of Multivariate Analysis, 117(2013), 193–213.

Appendix A Bound for covariances

Proof.

It is easy to see that by Assumptions 1.2–1.4 we have

We proceed by bounding the sums in over several subsets of the indices whose union covers all possible combinations.

Case I. Let , and . Using Assumption 1.2 and the Cauchy–Schwarz inequality we get for all

| (A.1) | ||||

since by construction and are independent with zero mean. Similarly, for all we have

| (A.2) |

By bounds in (A.1) and (A.2) we conclude

| (A.3) |

Assumption 1.2 implies

The Cauchy–Schwarz inequality and the stationarity of the ’s gives as in (A.1) that

and similarly

Thus we get

| (A.4) |

Repeating the arguments above, one can easily verify that

| (A.5) |

Combining (A.4) and (A.5) we get

| (A.6) |

Minor modifications of the proofs of (A.3) and (A.6) lead to

| (A.7) |

and

| (A.8) |

Next we develop bounds for the sum when the indices are in . We define the random functions and , where are iid copies of , independent of . It is clear that and have the same distribution and are independent of . (Note that and are defined by using the same ’s, making them different from and of (3.2)). By Assumption 1.2 and the Cauchy–Schwarz inequality we have

| (A.9) | ||||

and similarly

Clearly,

with

Applying (A.2) and (A.9) we get that

Using the definition of we conclude

It follows similarly

implying

Using nearly identical arguments we obtain that

and

Case II. Let and For we write with the help of Assumption 1.2

and similarly

Thus we get

For similar arguments yield

If , then we get

and

resulting in

since due to the restriction on , there are only choices for for any . Next we consider the sum of the expected values assuming that . Using (A.1) and (A.2) we conclude

and

by Abel’s summation formula. Finally we consider the case when the summation is over . Let and If we have

| (A.10) | ||||

and similarly

resulting in

In case of the upper bound in (A.10) still holds but for the ’s we have

Since for all we have that we conclude

Furthermore, by (A.1) and (A.2) we get

This completes the proof of the lemma. ∎

Appendix B Asymptotics for means and variances of and

We recall that is determined by the –dependent random functions and defined in (3.2) and (3.3), respectively.

Lemma B.1.

Proof.

First we note that by the stationarity of and we have

proving B.1. Similarly,

and therefore by Assumptions 1.2 and 1.3 we have (B.2).

To prove (B.3) we note that by stationarity we have

since by the arguments used in Section A

Next we show that

| (B.5) |

Using the definition of we have

where ,

and

Let and Using stationarity we get

By the –dependence of and we obtain that

| (B.6) |

Also, it is easy to check that

| (B.7) |

and therefore we need to study only. We decompose as , where

Furthermore, let and . Using again –dependence we get that

Furthermore,

and

Elementary algebra and give

and therefore

where

and

Thus we have

In a similar fashion it can be shown that

where

Since , the proof of (B.5) is complete.

Observing that , if , and , (B.3) is established.

The series in the definitions of are absolutely convergent and Assumptions 1.2 and 1.3 imply that , as , proving (B.4).

∎