On efficient dimension reduction with respect to a statistical functional of interest

Abstract

We introduce a new sufficient dimension reduction framework that targets a statistical functional of interest, and propose an efficient estimator for the semiparametric estimation problems of this type. The statistical functional covers a wide range of applications, such as conditional mean, conditional variance and conditional quantile. We derive the general forms of the efficient score and efficient information as well as their specific forms for three important statistical functionals: the linear functional, the composite linear functional and the implicit functional. In conjunction with our theoretical analysis, we also propose a class of one-step Newton–Raphson estimators and show by simulations that they substantially outperform existing methods. Finally, we apply the new method to construct the central mean and central variance subspaces for a data set involving the physical measurements and age of abalones, which exhibits a strong pattern of heteroscedasticity.

doi:

10.1214/13-AOS1195keywords:

[class=AMS]keywords:

On efficient dimension reduction with respect to a statistical functional of interest

, and t1Supported in part by a NSF Grant DMS-11-06815. t2Supported in part by a NSF Grant DMS-12-05546.

62-09, 62G99, 62H99, Central subspace, conditional mean, variance and quantile, efficient information, efficient score, Frechet derivative and its representation, projection, tangent space

1 Introduction

The purpose of this paper is twofold: to introduce a new framework for sufficient dimension reduction that targets a statistical functional of interest, and to develop semiparametrically efficient estimators for problems of this type.

Let be a -dimensional random vector and be a random variable. In classical sufficient dimension reduction (SDR), we are interested in a lower dimensional linear predictor , where is a matrix with , such that is independent of given . That is, the conditional distribution of given is the same as that of given . In this problem, the identifiable parameter is , the subspace of spanned by the columns of . Under mild conditions, there exists a unique smallest subspace that satisfies this condition, and it is called the central subspace; see Li (1991, 1992), Cook and Weisberg (1991), Cook (1994, 1996, 1998). For a general discussion of the sufficient conditions for the central subspace to exist, see Yin, Li and Cook (2008). The SDR provides us a mechanism to reduce the dimension of the predictor while preserving the conditional distribution of given .

In many applications, our interests are in some specific aspects of the conditional distribution . For example, in nonparametric regression, we are interested in the conditional mean ; in median regression, we are interested in the conditional median , and in volatility analysis we are interested in the conditional variance and in supervised classification we are interested in the class label of given its covariates . To illuminate this point further, let us consider the model

| (1) |

where and are unknown functions. In this case, the central subspace, which is the two-dimensional subspace of spanned by and , only tells us the sufficient predictors can be any linear combination of and , but it does not tell us that the conditional mean is a function of , and the conditional variance is a function of . Thus, the information provided by the central subspace is clearly inadequate if we want to build a model like (1).

Under these circumstances, it makes sense to reformulate sufficient dimension reduction to target a specific functional, so as to provide a more nuanced picture of the relation between and than offered by the central subspace. Several such efforts have been made over the past decade or so. For example, Cook and Li (2002) introduced the central mean subspace, which is defined by the relation , where is minimal in the same sense as it is in the central subspace. Yin and Cook (2002) introduced the th central moment subspace through the relation . Zhu and Zhu (2009) introduced the central variance subspace by requiring that is a function of . Zhu, Dong and Li (2013) introduced a general class of estimating equations for single-index conditional variance. The Minimum Average Variance Estimator (MAVE) by Xia et al. (2002) also targets the central mean subspace. Kong and Xia (2012) introduced an adaptive quantile estimator for single-index quantile regression, which targets the conditional quantile. It turns out the space spanned by the columns of in the above relations are all subspaces of the central subspace. They provide refined structures for the central subspace. As a consequence, can be written as , and we can refine central subspace based on the sufficient predictor . For convenience, we reset as , and use to represent the original predictor throughout the rest of the paper.

The first goal of this paper is to unify these problems by introducing a general dimension reduction paradigm with respect to statistical functional of the conditional density of given , say , through the following statement:

| (2) |

Note that sufficient dimension reduction for conditional mean, conditional moments and conditional variance discussed in the last paragraph are all special cases of relation (2). The minimal subspace of that satisfies this relation is called the -central subspace.

The second, and the main goal of this paper is to develop semiparametrically efficient estimators for the -central subspace. In a series of recent papers, Ma and Zhu (2012, 2013a, 2013b) use semiparametric theory to study sufficient dimension reduction and develop semiparametrically efficient estimators of the central subspace. These are related to the earlier developments by Li and Dong (2009) and Dong and Li (2010), which use estimating equations to relax the elliptical distribution assumption for sufficient dimension reduction. We extend Ma and Zhu’s approach to find semiparametrically efficient estimator for the -central subspace. We derive the general formulas for the efficient score and efficient information for the semiparametric family specified by the relation (2), and further deduce their specific forms for three important statistical functionals: the linear functionals (L-functionals), the composite linear functionals (C-functionals) and implicit functionals (I-functionals). These functionals cover a wide range of applications. For example, all conditional moments are L-functionals, all conditional cumulants [see, e.g., McCullagh (1987)] are C-functionals and quantities such as conditional median, conditional quantile and conditional support vector machine Li, Artemiou and Li (2011) are I-functionals.

Using the formulas for efficient score and efficient information, we propose a one-step Newton–Raphson alorithm to implement semiparametrically efficient estimation. Compared with the semiparametric estimators of Ma and Zhu (2013a), our algorithm has two distinct and attractive features. First, since our algorithm relies on the MAVE-type procedure for minimization, it can be implemented by iterations of a least squares problem without resorting to high-dimensional search-based optimization. Second, unlike Ma and Zhu (2013a), our method does not require any specific parameterization of that potentially restricts the generality of their method.

The rest of the paper is organized as follows. In Section 2, we give a general formulation of sufficient dimension reduction with respect to a statistical functional of interest. To set the stage for further development, we lay out the semiparametric structure of our problem in Section 3. In Section 4, we derive the efficient score and efficient information for a general statistical functional. In Sections 5, 6 and 7, we further deduce the specific forms of the efficient score and efficient information for the L-, C- and I-functionals. In Section 8, we discuss the effect of estimating the central subspace on the efficient score. In Section 9, we develop the one-step Newton–Raphson estimation procedure for semiparametrically efficient estimation. In Section 10, we conduct simulation studies to compare our method with other methods, and in Section 11 we apply our method to a data set. Some concluding remarks are made in Section 12. The proofs of some technical results are given in the supplementary material [Luo, Li and Yin (2014)].

The following notation will be consistently used throughout the rest of the paper. The symbol denotes the dimensional identity matrix; denotes a vector whose th entry is 1 and other entries are 0; indicates independence or conditional independence between two random elements—that is, means and are independent, and means and are independent given . For integers and , denotes the dimensional Euclidean space, and denotes the set of dimensional matrices. For a function with multiple arguments, say , we use the dot notation to represent mappings of a subset of the arguments. For example, represents the mapping where and are fixed, and represents the mapping where is fixed. We use superscripts of to index components and subscripts of to index subjects. Thus, means the th component of the th observation in a sample . However, represents power when is not .

2 Dimension reduction for conditional statistical functional

Let and be -finite measure spaces, where and and and are -fields of Borel sets in and . Let be a pair of random elements that takes values in . Let be a family of densities of with respect to . We assume that is a semiparametric family; that is, there exist and a family of functions such that

Furthermore, we assume that each can be factorized into where is the marginal density of , is the conditional density of given . The real assumption in this factorization is that appears only in the conditional density.

As an illustration, consider the single index model where

and is an unknown function. Since is unknown, is identified up to a proportional constant. To avoid the trivial case, let us assume it has at least one nonzero component, and further assume this is the first component for convenience. We can then assume without loss of generality where . Then

where is the matrix . In this case, is the p.d.f. of and is the p.d.f. of for a given .

Now let denote the family , and

We assume that contains the true density of . That is, there exist , , and such that is the true density of . For convenience, we abbreviate , , and as , and .

Let be a class of densities of with respect to that contains all for , and . Let be a mapping from to . Such mappings are called statistical functionals. The functional induces the random variable

on , which we write as . Following the convention of the conditional expectation, we write as . This random variable can be used to characterize a wide variety of features of a conditional density that might interest us, as detailed by the following example.

Example 1.

Let be the functional . Then each uniquely defines the mapping

That is, is the conditional expectation under .

Let be the mapping

Then is the conditional variance under the conditional density .

Let be the functional defined by the equation in

| (3) |

where is the sign function that takes the value 1 if and takes the value if . The solution to (3) is the median of . Each uniquely defines the mapping , which is the conditional median of given under the conditional density .

We now give a rigorous definition of the -central subspace.

Definition 1.

If there is a matrix , with , such that is measurable with respect to , then we call a sufficient dimension reduction subspace for . The intersection of all such spaces is called the central subspace for conditional functional , or the -central subspace.

We denote the -central subspace by . For example, if is the conditional mean functional, then becomes the central mean subspace, which we write as ; if is the conditional median functional, then becomes the central median subspace, which we write as ; if is the conditional variance functional, then becomes the central variance subspace, which we write as . It is easy to see that : this is because implies

In the following, we denote the dimension of the by and any basis matrix of (of dimension ) as .

3 Formulation of the semiparametric problem

To set the stage for further development, we first outline the basic semiparametric structure of our problem. Let . Let and denote the inner product and norm in . For a technical reason, it is easier to work with an embedding of into , defined as

Let . This transformation ensures that ; whereas additional assumptions are needed to ensure . Also note that is the 0 element in .

A curve in that passes through is any mapping from that is Fréchet differentiable at . That is, there is a member of such that

The tangent space of at is the closure of the subspace of spanned by along all curves.

Let be the score with respect to ; that is,

Let be the componentwise projection of the random vector on to the orthogonal complement of the tangent space . This projection is called the efficient score, and we denote it by . The matrix

is called the efficient information. Now let be an i.i.d. sample of . For a function of , let denote the sample average of . Under some conditions, if is the solution to the estimating equation

| (4) |

then . Moreover, for any estimate of that is regular with respect to , can be decomposed as where two terms are asymptotically independent. This result, well known in the semiparametric literature as the Hájek–LeCam convolution theorem, implies has the smallest asymptotic variance among all regular estimators with respect to . That is, is semiparametrically efficient. For a comprehensive exposition of this theory, see Bickel et al. [(1993), Chapter 3] or van der Vaart [(1998), Chapter 25].

We now investigate how the sufficient dimension reduction in Definition 1 specifies the semiparametric family , and what is the meaning of the parameter in this context. Since our goal is to estimate , we need fewer parameters than . In fact, the set is a Grassmann manifold, which has dimension [see, e.g., Edelman, Arias, and Smith (1999)]. There always exists a smooth parameterization , where , because is determined if a certain submatrix of is fixed as and the complementary block has free varying entries. The specific form of the parameterization is not important to us.

Let be the -field generated by . Because is measurable with respect to if and only if

the semiparametric family for our purpose is , where

Here, for a sub--field of and a function , denotes the evaluation of the conditional expectation at .

In this paper, we will focus on the development of the efficient score, the efficient information and an accompanying estimation procedure, but will not give a rigorous proof of the asymptotic results [including the asymptotic distribution of and the convolution theorem], because it would far exceed the scope of the paper and because we do not expect the proof will fundamentally deviate from that given in Ma and Zhu (2013a). In addition, as mentioned earlier, by design, our method is applied to the sufficient predictor corresponding to the central subspace, whose dimension is relatively low. Consequently, we expect no surprises as regards the validity of -rate of convergence of our estimator. In the meantime, our simulation studies provide strong evidence that the our efficient estimator does approach the theoretical semiparametric variance bound for modestly large sample sizes.

4 Efficient score and efficient information

In this section, we derive the efficient score and efficient information for the semiparametric problem set up in Section 3. To this end, we first derive the tangent space for a fixed . Let be the tangent space of at , and be the tangent space of at .

Proposition 1

The following relations hold: {longlist}

;

in terms of the inner product in ;

.

This proposition was verified and used in Ma and Zhu (2012, 2013a). Since the family has no constraint, its tangent space is straightforward, as given in the next proposition, which is taken from Bickel et al. [(1993), page 52].

Proposition 2

consists of all functions in with.

To compute , we introduce a new functional for each fixed . Let be the class of densities . Let denote the mapping

| (5) | |||

This mapping is different from , which is from to . Nevertheless, note that . Let

| (6) |

The Fréchet derivative of at is denoted by . This is a bounded linear functional from to .

Theorem 1.

Suppose, for each , the functional is Fréchet differentiable at 0. Let be the Riesz representation of and assume . Then

Moreover, if, for each , the function is continuously Fréchet differentiable in a neighborhood of , then .

The proof of this theorem is technical and is presented in the supplementary material [Luo, Li and Yin (2014)] (Section I). From Theorem 1 and Propositions 1 and 2, we can easily derive the form of , as follows.

Corollary 1

Under the assumptions of Theorem 1,

We now compute the efficient score, which is the projection of the true score with respect to on to . Let

The true score for the parameter of interest is the Fréchet derivative

To differentiate from , we denote the above derivative by . This is an -dimensional vector. Since the mapping and also depend on , we now write them as and . We use to denote the mapping . Following Bickel et al. [(1993), Chapter 3], we use to represent the projection of a function on to a subspace of .

Theorem 2.

Suppose the following conditions hold: {longlist}[1.]

For each and in a neighborhood of , the mapping

is continuously Fréchet differentiable in a neighborhood of . Let be the Riesz representation of and be its centered version .

The function is Fréchet differentiable at with Fréchet derivative .

If

where is the reciprocal of , then . Then

| (8) |

Let . By the projection theorem, it suffices to show: {longlist}[(a)]

;

for any ,

| (9) |

By condition 3, . Moreover, by the definition of in condition 3 it is easy to verify that . Hence, assertion (a) holds.

Because , it has the form for some satisfying . Hence, the right-hand side of (9) is

Substitute the definition of into the right-hand side, and it becomes

However, because , the equation above reduces to

which is the left-hand side of (9).

The next corollary, which follows directly from Theorem 2, gives the general form for the efficient information estimating .

Corollary 2

Under the assumptions of Theorem 2, the efficient information for estimating is given by

| (10) |

In the next three sections, we apply the general result in Theorem 2 to derive the explicit forms of the efficient scores for three types of commonly used statistical functionals: the linear functionals, the composite linear functionals and the implicit functionals. The common thread that runs through these developments is the calculation of the Riesz representation of the Fréchet derivative .

5 Linear statistical functionals

Dimension reduction of this type is the direct generalizations of the central mean subspace [Cook and Li (2002)] and the central moment subspace [Yin and Cook (2002)]. It can also be viewed as a generalization of the single- and multiple-index models [see, e.g., Härdle, Hall and Ichimura (1993)]. Let be a square-integrable function. Let be the functional

The corresponding conditional statistical functional is

The -central subspace is defined by the relation

| (11) |

Theorem 3.

Because is Fréchet differentiable at , its Fréchet derivative is the same as the Gâteaux derivative [Bickel et al. (1993), page 455], which is defined by

However, because

the Riesz representation of is . Hence, by Theorem 2,

Also, for each ,

Take Fréchet derivative with respect to on both sides to obtain

as desired.

Example 2.

The central mean subspace introduced by Cook and Li (2002) is a special case of the -central subspace with . The efficient score and efficient information are given by (8) and (10) where

| (12) | |||||

For example, if the central mean subspace has dimension 1 and is spanned by for some and , as described in the second paragraph of Section 2, then

Therefore, the efficient score is

The efficient information is

where denotes for a matrix .

Alternatively, the efficient score and information can be written in the original parameterization . See the supplementary material [Luo, Li and Yin (2014)] (Section II) for their explicit forms in the -parameterization.

6 Composite linear statistical functionals

We now consider a nonlinear function of several linear functionals, which is motivated by dimension reduction for conditional variance considered in Zhu and Zhu (2009) and the single-index conditional heteroscedasticity model in Zhu, Dong and Li (2013). See also Xia, Tong and Li (2002). In fact, all cumulants are functionals of this type. Let be bounded linear functionals from to . That is,

where are square-integrable with respect to any density . Let be a differentiable function. Then defines a statistical functional on to . We call such functionals composite linear functionals, or C-functionals. For example, if

then is the variance functional. The corresponding conditional statistical functional is defined by

where denotes . We will use the following notation:

| (13) | |||||

Also note that, in our case, . Again, we use symbols such as and to indicate and .

Theorem 4.

As shown in Section 5, the Riesz representation of is simply . By the chain rule of Fréchet differentiation and definition (6), we have

Hence, the Riesz representation of is

In the meantime for each , we have

Differentiate both sides of this equation with respect to , to obtain

Hence,

Now take conditional expectation on both sides to prove the second relation in (4).

It is easy to see that an alternative expression of in Theorem 4 is

This expression is useful because is a function of , and its derivative with respect to can be estimated by local linear regression, as we will see in Section 9.

Example 3.

For the central variance subspace, we have

Hence, , and

The Riesz representation of and its centered version are

Hence,

In this case, the subspace consists of functions of the form

where is an arbitrary member of . Interestingly, the estimating equation proposed by Zhu, Dong and Li (2013) is a special member of with taken to be the components of .

7 Implicit statistical functionals

In this section, we study statistical functionals defined implicitly through estimating equations. Many robust estimators, such as conditional medians and quantiles, are of this type. Let , and be a function of the parameter and the variable . Such functions are called estimating functions [see, e.g., Godambe (1960), Li and McCullagh (1994)]. If the equation

| (15) |

has a unique solution for each , then it defines a functional that assigns each the solution to (15). We call such functionals implicit functionals, or I-functionals. If we replace by a conditional density function , then (15) becomes

The corresponding conditional statistical functional is . The -central subspace is defined by the statement

Naturally, we write the function as .

To simplify the presentation, we use the notion of generalized functions. Let be the class of functions defined on a bounded set in that have derivatives of all orders, whose topology is defined by the uniform convergence of all derivatives. Any continuous linear functional with respect to this topology is called a generalized function. For example, let . Then it can be shown that the linear functional

is continuous with respect to this topology. This continuous linear functional is called the Dirac delta function. We identify the functional with an imagined function on and write formally as the integral

A consequence of this convention is that if we pretend to be the derivative of the indicator function then we get correct answers at the integral level. For example, for any constant and small number , we have

Thus, the pretended linearization has caused no inconsistency. We use this device to simplify our presentation of quantiles.

Theorem 5.

Differentiating both sides of the equation

with respect to at , and using the relation

we find

Hence, the Riesz representation of the Fréchet derivative is

where the last equality holds because, by definition, . By (7) and the definition of in Theorem 2,

| (19) |

To further simplify the numerator of the right-hand side, differentiate both sides of the equation to obtain

where denotes . Hence,

Substitute this into (19) to prove the first relation in (5). Substitute (7) into the definition of in Theorem 2 to prove the second relation in (5).

In the next example, we derive the efficient score for a particular type of I-functional—the quantile functional.

Example 4.

If we assume all densities in are continuous, then the th quantile is the solution to the equation . Equivalently, is the solution to the equation

Because the generalized derivative of is , we have . Hence

Because is a binary random variable that takes the value with probability and with probability , we have

Hence, in the efficient score,

and is as given in (5) with being the conditional th quantile of given .

8 Effect of estimating the central subspace

Throughout the previous sections, we have treated as the true predictor from the central subspace; that is, where is the original predictor and is a basis matrix of the central subspace based for . However, in practice, itself needs to be estimated and, in theory at least, should affect the form of the efficient score about . While our simulation studies in Section 10 indicate that this effect is very small, for theoretical rigor we present here the efficient score treating the central subspace as an additional (finite-dimensional) nuisance parameter. For convenience, we use to denote both a matrix and the corresponding -dimensional Grassmann manifold.

Let denote the efficient score in Theorem 2 with replaced by . Let denote the efficient score for with treated as an additional nuisance parameter. Let denote the score with respect to . In the supplementary material [Luo, Li and Yin (2014)] (Section III) it is shown that

| (20) |

where is the function

in which indicates the Moore–Penrose inverse, and

In theory, the asymptotic variance bound based on is lower than or equal to that based on . However, in the simulation studies (Table 2 in Section 10) we see that the theoretical lower bound based on is nearly reached, which indicates that effect of estimating the central subspace on the efficient score for is very small.

9 Estimation

In this section, we introduce semiparametrically efficient estimators using the theory developed in the previous sections. For the L-functionals, we develop the estimator in full generality, but for the C- and I-functionals we focus on the conditional variance functional and the conditional quantile functional. Procedures for other C- or I-functionals can be developed by analogy.

We first clarify two points related to the algorithm we will propose. First, since we will rely heavily on the MAVE-type algorithms, it is more convenient to use the -parameterization rather than the -parameterization, and avoid redundancy in by taking the generalized matrix inverse. We will justify the -parameterization after introducing the algorithm. Second, the MAVE algorithm actually has two variants: the outer product gradient (OPG) and a refined version of MAVE (RMAVE). Typically, OPG, MAVE and RMAVE are progressively more accurate and require more computation. In the following, the MAVE-type algorithm can be replaced either by RMAVE for greater accuracy or by OPG for less computation.

Our estimation procedure is divided into four steps. In step 1, we estimate the central subspace and project on to this subspace to obtain . In step 2, we estimate using a -dimensional kernel estimate. These estimates are used as the proxy response, and we denote them by . In step 3, we apply MAVE to to estimate an initial value for . In step 4, we use one-step Newton–Raphson algorithm based on the efficient score and efficient information to approximate the semiparametrically efficient estimate. We call our estimator SEE, which stands for semiparametrically efficient estimator.

Preparation step: A MAVE code. Let be a random sample from , and be a kernel with bandwith . That is, for some symmetric function that integrates to 1 and . Compute the objective function

| (21) |

where , , and on the left denote and , respectively, and . We will use this objective function in several ways. It is well known that minimization of (21) can be solved by iterations of least squares, and in each iteration there is an explicit solution. Thus, purely search-based numerical optimization (such as the simplex method) is avoided. See, for example, Li, Li and Zhu (2010) and Yin and Li (2011).

Step 1: Estimation of central subspace. We use the MAVE-ensemble in Yin and Li (2011) to estimate the central subspace. In this procedure, in (21) is taken to be a set of functions randomly sampled from a dense family in . In this paper, take this set to be , where are i.i.d. . The sample of responses are standardized so that the range of the uniform distribution represents a reasonably rich class of functions relative to the range of . The basis matrix of is then estimated by the MAVE-ensemble. The projected predictor is taken as the predictor in steps 2–4. Since our goal is to estimate , the choice of the working dimension of is not crucial.

As was shown in Yin and Li (2011), at the population level, the MAVE ensemble is guaranteed to recover central subspace exhaustively as long as the functions of form a characterizing family. In practice, it is true any information lost in the initial step will be inherited by SEE. However, our experiences indicate that this problem can be mitigated by using a sufficiently rich ensemble family—for example, by increasing the range of the uniform distribution and the number of ’s.

Several other methods are available for exhaustive estimation of the central subspace, such as the semiparametrically efficient estimator of Ma and Zhu (2013a), the DMAVE by Xia (2007) and the Sliced Regression by Wang and Xia (2008). Here, we have chosen the MAVE-ensemble for its computational simplicity.

Step 2: Estimation of proxy response. This step is unnecessary for the L-functionals: because for some function , we can use itself as the proxy response . For the conditional variance functionals, this step needs not be fully performed: we can use as the proxy response , where is the kernel estimator of . If simplification of this type is not applicable, then we need to perform nonparametric estimation of . For example, for the I-functionals, we use the minimizer of the function as the proxy response .

Step 3: Initial estimate of . Apply MAVE to to obtain an initial estimate of by minimizing over all . Denote this initial estimate as .

Step 4: The one-step Newton–Raphson algorithm. Rather than attempting to solve the score equation (4), we propose a one-step Newton–Raphson procedure. Let be the efficient score in , which is obtained by replacing by and by whenever applicable. Let . We estimate by

| (22) |

where is the initial value from step 3.

We now describe in detail how to compute for different functionals. For the L-functional, the efficient score involves the following functions:

For the C-functional, it involves the functions:

For the conditional quantile functional, it involves the functions:

These functions can be categorized into three types: (a), (b), (d), (f), (g) are conditional means of random variables; (c), (e), (h) are derivatives of functions of with respect to ; (i) is the conditional density evaluated at a quantile. The first two types can be solved by minimizing in (21) with specific and : Table 1 gives the details of these random variables and matrices, as well as which parts of the MAVE output are needed in SEE.

| Quantities | MAVE output | ||

|---|---|---|---|

| (a) | |||

| (b) | |||

| (c) | |||

| (d) | |||

| (e) | |||

| (f) | , | ||

| (g) | |||

| (h) |

Finally, we estimate for any by the kernel conditional density estimator:

where is a different bandwidth for the response variable.

Tuning of bandwidths. We need to determine the kernel bandwidths at various stages in the above algorithm. We use the Gaussian kernel with optimal bandwidth for nonparametric regression [see, e.g., Xia et al. (2002)], where is determined by five-fold cross validation. That is, we randomly divide the data into 5 subsets of roughly equal sizes. For each , we use the th subset as the testing set and the rest as the training set. For a given , we conduct dimension reduction on the training set, and use the sufficient predictor to evaluate a certain prediction criterion at each point on the testing set and average these evaluations over the testing set, and finally average the five averages of the criterion to obtain a single number. We then minimize the resulting criterion over by a grid search. Naturally, the prediction criterion depends on the object to be estimated using that kernel. Below is a list of the prediction criteria we propose for the four steps in the estimation procedure.

In step 1: We use the distance correlation introduced by Székely and Rizzo [(2009), Theorem 1, expression (2.11); and therein are taken to be 2].

In step 2: For the L-functionals, no tuning is needed. For the conditional variance functional, we need to estimate , and we use the prediction criterion , where is the kernel estimate of based on the training set using a tuning constant . For conditional median, we use the prediction criterion , where is the kernel estimate of the conditional median based on the training set using a specific tuning constant.

In step 3: We use the prediction criterion , where is the proxy response obtained from step 2, and is the MAVE output .

In step 4: There are three types of kernels in this step: the kernel for , the kernel for , and the kernel for (the last one is needed only for the conditional median functional). Corresponding to these types, we use bandwidths

We use cross validation to determine the common . Once again, we use different prediction criteria for different functionals. For the conditional mean functional, we use the criterion . For conditional variance functional, we use the criterion . For the conditional median functional, we use the criterion.

Justification of parameterization. We now justify the one-step iteration formula (22) as an equivalent form of

| (23) |

Since is a function of a dimensional parameter , the efficient information has rank . Let denote the matrix whose columns are eigenvectors of corresponding to its nonzero eigenvalues, and let , where is a free parameter in . In this parameterization,

Hence, (23) is equivalent to

Multiply both sides by from the left, we find

By construction, , , and is Moore–Penrose inverse of . Thus, the above iterative formula is the same as (22).

In concluding this section, we point out two attractive features of our algorithm, which were briefly touched on in the Introduction. First, since our algorithm is implemented by repeated applications of variations of MAVE, it essentially consists of sequence of least squares algorithms, thus avoiding any search-based numerical optimization, which can be infeasible when the dimension of is high. The second advantage is that, since our algorithm is based on the -parameterization, we do not need any subjectively chosen parameterization. In comparison, Ma and Zhu (2013a) used the parameterization , where is a matrix with free-varying entries. Note that this is not without loss of generality, because in reality the first rows of can be linearly dependent.

10 Simulation comparisons

In this section, we conduct simulation comparisons between SEE and other methods for estimating three types of -central subspaces: conditional mean, conditional variance and conditional quantile. We use the distance between two subspaces proposed by Li, Zha and Chiaromonte (2005) to measure estimation errors, which is defined as

| (24) |

where and are subspaces of , and is the norm in . For each of the following models, the sample size is taken to be or 500, or both; each sample is repeatedly drawn for times in the simulation. In all simulations, we fix the working dimension in step 1 at , even though is no greater than 2 in all examples.

The explicit forms of the efficient scores efficient information for Models I–VII used in the following comparisons are derived in the supplementary material [Luo, Li and Yin (2014)] (Section II).

(a) Comparison for the central mean subspace. In this case, the functional is the conditional mean . We compare SEE with RMAVE under the following models:

where , , and . These models represent a variety of scenarios one might encounter in practice. Specifically, the central mean subspace is a proper subspace of the central subspace in Model I, but coincides with the latter in the other models. The conditional variance is a constant in Model II, but depends on in the other models. Because of its additive error structure Model II is favorable to MAVE. Finally, Model IV has a discrete response and the error only enters implicitly. Model I and Model III will be used again for Comparison (b), where conditional variance is the target; Model II was also used in Li (1991) and Xia et al. (2002).

The results with sample sizes and are presented in Table 2, in the blocks indicated by . The entries are in the form , where is the mean, and the standard error, of the distance (24) between the true and estimated , based on simulated samples.

(b) Comparison for the central variance subspace. Let be the conditional variance . We compare SEE with the estimator proposed in Zhu and Zhu (2009) and Zhu, Dong, and Li (2013). In Model I, the central variance subspace is different from either the central mean subspace or the central subspace, while in Model III, the three spaces coincide. The results with and are reported in Table 2, in the blocks indicated by .

| Functionals | Models | Estimators | ||||

|---|---|---|---|---|---|---|

| 200 | RMAVE | SEE | ALB | |||

| I | ||||||

| II | ||||||

| III | ||||||

| IV | ||||||

| Zhu–Zhu | Zhu–Dong–Li | SEE | ALB | |||

| I | ||||||

| III | ||||||

| AQE | SEE | ALB | ||||

| V | ||||||

| VI | ||||||

| 500 | RMAVE | SEE | ALB | |||

| I | ||||||

| II | ||||||

| III | ||||||

| IV | ||||||

| Zhu–Zhu | Zhu–Dong–Li | SEE | ALB | |||

| I | ||||||

| III | ||||||

| AQE | SEE | ALB | ||||

| V | ||||||

| VI | ||||||

(c) Comparison for the central median subspace. Let be the conditional median . We compare SEE with the adaptive quantile estimator (AQE) introduced by Kong and Xia (2012), which can also be used to estimate the central median subspace. We use the following models:

where and . For Model V, has a skewed-Laplace distribution with p.d.f.

In this case,

It follows that

For Model VI, . Although for this model the central mean subspace coincides with the central median subspace, due to the heavy-tailed error distribution the conditional median is preferred to the conditional mean. Similar models can be found, for example, in Zou and Yuan (2008). The results for sample sizes are presented in Table 2, in the blocks indicated by .

(d) Comparison with theoretical lower bound. To see how closely the theoretical asymptotic lower bound (ALB) is approached by SEE for finite samples, we now compute the limit

| (25) |

where is the semiparametrically efficient estimate. This is the best we can do to estimate the -central subspace. The explicit form and the derivation of (25) is given in the supplementary material [Luo, Li and Yin (2014)] (Section IV). We present the numerical values of this limit in the last column (under the heading ALB) of Table 2 for different models and functionals.

(e) Conclusions for comparisons in (a)–(d). From Table 2, we see that SEE achieves substantially improved accuracy across all models and functionals considered. Stability of the estimates is also improved as can be seen from the decrease in standard errors. Our simulation studies (not presented here) indicate that the results are not significantly affected by the working dimension of the central subspace. For example, we repeated the analysis with and the patterns of the comparisons are not significantly altered.

Comparing the results for and , we see that the proportion of improvement is smaller for the large sample size, as to be expected.

We see that the actual errors of the SEE computed from simulations are very close to the theoretical lower bounds both sample sized and the differences become negligible for . Since in the estimator the central subspace is estimated from the sample and in the lower bounds, the central subspace is treated as known; the closeness of these errors to their corresponding ALB also indicates that the lower bound based on in Section 8 is close to the lower bound based on . In other words, the effect of estimating the central subspace on the efficient score is small.

(f) Comparison under dependent components of . We now repeat comparisons in (a) through (d) using an with dependent components. Rather than taking , we now take

| (26) |

The same covariance matrix was used in Ma and Zhu (2012). The results parallel to those in Table 2 are presented in Table 3. We see that the errors are larger than those for with independent components, but the degree by which SEE improves upon the other estimators, and to which it approaches theoretical asymptotic lower bound, are similar to those for the independent-component case.

| Functionals | Models | Estimators | |||

|---|---|---|---|---|---|

| RMAVE | SEE | ALB | |||

| I | |||||

| II | |||||

| III | |||||

| IV | |||||

| Zhu–Zhu | Zhu–Dong–Li | SEE | ALB | ||

| I | |||||

| III | |||||

| AQE | SEE | ALB | |||

| V | |||||

| VI | |||||

(g) Comparison for conditional upper quartile. We now apply SEE to estimating the central upper-quartile subspace in which the functional of interest is solution to the equation . We generate from with given by (26). We compare SEE with AQE for Models V and VI, and the additional model

where . In Model V, the central upper-quartile subspace has dimension 2, spanned by and ; in Models VI and VII, the central upper-quartile subspaces have dimension and are spanned by and , respectively, where is the c.d.f. of the standard normal distribution. The performance of the estimators is summarized in Table 4.

We see that SEE outperforms AQE both in average accuracy and estimation stability. It is also interesting to note that, for Model VI, the central median subspace coincides with the central upper-quartile subspace, and the SEE based on the conditional median (Table 3) performs better than the SEE based on the conditional upper quartile (Table 4).

| Models | AQE | SEE | ALB |

|---|---|---|---|

| V | |||

| VI | |||

| VII |

11 Application: Age of abalones

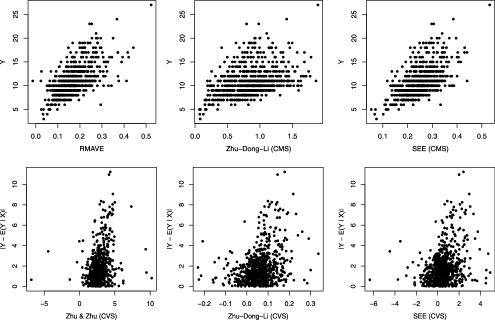

In this section, we evaluate the performance of SEE in an application, which is concerned with predicting the age of abalones using their physical measurements. The data can be found at the website http://archive.ics.uci.edu/ml/datasets.html, and consist of observations from 4177 abalones, of which 1528 are male, 1307 are female and 1342 are infant. The observations on each subject contain 7 physical measurements and the age of the subject, as measured by the number of rings in its shell. We only use the subset of male abalones. The 532th subject in this subset is an outlier, and is deleted. Thus, we have a sample of size with predictors and 1 response. For objective evaluation of the estimators, we further split the data into two subsets: the first 764 subjects are used as the training set to estimate the sufficient predictors and the rest 763 subjects are used as the testing set to plot the derived sufficient predictors versus the response.

We estimate both the central mean subspace (CMS) and the central variance subspace (CVS) of this data set. The CMS is estimated by RMAVE, SEE, and the method implicitly contained in Zhu, Dong and Li (2013). The CVS is estimated by the methods proposed by Zhu and Zhu (2009) and Zhu, Dong and Li (2013), and the SEE. The results are presented in Figure 1. The three upper panels are scatter plots of versus the sufficient predictor in the CMS as estimated by RMAVE, Zhu–Dong–Li and SEE in that order. The three lower panels are the scatter plots of the absolute residuals versus the sufficient predictor in the CVS as estimated by Zhu–Zhu, Zhu–Dong–Li and SEE.

To give an objective numerical comparison, we use a bootstrapped error measurement akin to that introduced by Ye and Weiss (2003), which is reasonable because all estimators involved are consistent. Since the predictors in the abalone data set are highly correlated, two estimates of that span substantially different linear spaces can correspond to nearly identical . For this reason, rather than measuring the error in , as we did in the simulations, here we directly measure the error in . Specifically, we generate bootstrap samples, and for each sample we compute the estimate . We also compute the full-sample estimate . For each bootstrap sample, we evaluate the sample correlation between

We denote sample correlations for the 500 bootstrap samples as . We then compute and call it the bootstrap error of the estimator. The result is summarized in the Table 5.

| Functionals | Estimators | ||

|---|---|---|---|

| RMAVE | Zhu–Dong–Li | SEE | |

| Zhu–Zhu | Zhu–Dong–Li | SEE | |

We see that SEE is the top performer for estimating both CMS and CVS, followed by the estimator of Zhu, Dong and Li (2013), and then by RMAVE. We also observe that the estimation of central variance subspace is in general less accurate than that of central mean subspace, as has been observed in many other cases, for example, in Zhu, Dong and Li (2013).

12 Discussions

In this paper, we introduce a general paradigm for sufficient dimension reduction with respect to a conditional statistical functional, along with semiparametrically efficient procedures to estimate the sufficient predictors of that functional. This method is particularly useful when we want to select sufficient predictors with some specific purposes in mind, such as estimating the conditional quantiles in a population. This work is a continuation, synthesis and refinement of previous works on nonparametric mean regression, nonparametric quantile regression and nonparametric estimation of heteroscedasticity, under the unifying framework of SDR. It provides us with tools to explore the detailed structures of the central subspace, making SDR more specific to our goals. Our work has also substantially broadened the scope of the semiparametric approach recently introduced to SDR by Ma and Zhu (2012, 2013a and 2013b).

In a wide range of simulation studies, the SEE is shown to outperform several previously proposed estimators for conditional mean, conditional quantile and conditional variance. Moreover, the theoretical semiparametric lower bound is approximately achieved by the actual error based on simulation. Finally, the algorithm we developed for SEE has a special advantage over that proposed in Ma and Zhu (2013a): it does not rely on any specific parameterization of the central subspace, which means we do not need to subjectively assign any element of to be nonzero from the outset.

Acknowledgments

The authors would like to thank two referees and an Associate Editor for their insightful and constructive comments and suggestions, which led to significant improvement of this work.

[id=suppA] \stitleExternal appendix to “On efficient dimension reduction with respect to a statistical functional of interest” \slink[doi]10.1214/13-AOS1195SUPP \sdatatype.pdf \sfilenameaos1195_supp.pdf \sdescriptionThe supplementary file provides the proof of Theorem 1, explicit formulas for the efficient scores in Section 10, the efficient score when the central subspace is unknown, and the explicit value of the limit in (25).

References

- Bickel et al. (1993) {bbook}[mr] \bauthor\bsnmBickel, \bfnmPeter J.\binitsP. J., \bauthor\bsnmKlaassen, \bfnmChris A. J.\binitsC. A. J., \bauthor\bsnmRitov, \bfnmYa’acov\binitsY. and \bauthor\bsnmWellner, \bfnmJon A.\binitsJ. A. (\byear1993). \btitleEfficient and Adaptive Estimation for Semiparametric Models. \bpublisherJohns Hopkins Univ. Press, \blocationBaltimore, MD. \bidmr=1245941 \bptokimsref\endbibitem

- Cook (1994) {bincollection}[auto:STB—2014/01/06—10:16:28] \bauthor\bsnmCook, \bfnmR. D.\binitsR. D. (\byear1994). \btitleUsing dimension-reduction subspaces to identify important inputs in models of physical systems. In \bbooktitle1994 Proceedings of the Section on Physical and Engineering Sciences \bpages18–25. \bpublisherAmerican Statistical Association, \blocationAlexandria, VA. \bptokimsref\endbibitem

- Cook (1996) {barticle}[mr] \bauthor\bsnmCook, \bfnmR. Dennis\binitsR. D. (\byear1996). \btitleGraphics for regressions with a binary response. \bjournalJ. Amer. Statist. Assoc. \bvolume91 \bpages983–992. \biddoi=10.2307/2291717, issn=0162-1459, mr=1424601 \bptokimsref\endbibitem

- Cook (1998) {bbook}[mr] \bauthor\bsnmCook, \bfnmR. Dennis\binitsR. D. (\byear1998). \btitleRegression Graphics: Ideas for Studying Regressions Through Graphics. \bpublisherWiley, \blocationNew York. \biddoi=10.1002/9780470316931, mr=1645673 \bptokimsref\endbibitem

- Cook and Li (2002) {barticle}[mr] \bauthor\bsnmCook, \bfnmR. Dennis\binitsR. D. and \bauthor\bsnmLi, \bfnmBing\binitsB. (\byear2002). \btitleDimension reduction for conditional mean in regression. \bjournalAnn. Statist. \bvolume30 \bpages455–474. \biddoi=10.1214/aos/1021379861, issn=0090-5364, mr=1902895 \bptokimsref\endbibitem

- Cook and Weisberg (1991) {barticle}[auto] \bauthor\bsnmCook, \bfnmR. D.\binitsR. D. and \bauthor\bsnmWeisberg, \bfnmS.\binitsS. (\byear1991). \btitleDiscussion of “Sliced inverse regression for dimension reduction.” \bjournalJ. Amer. Statist. Assoc. \bvolume86 \bpages316–342. \bptokimsref\endbibitem

- Dong and Li (2010) {barticle}[mr] \bauthor\bsnmDong, \bfnmYuexiao\binitsY. and \bauthor\bsnmLi, \bfnmBing\binitsB. (\byear2010). \btitleDimension reduction for non-elliptically distributed predictors: Second-order methods. \bjournalBiometrika \bvolume97 \bpages279–294. \biddoi=10.1093/biomet/asq016, issn=0006-3444, mr=2650738 \bptokimsref\endbibitem

- Edelman, Arias and Smith (1999) {barticle}[mr] \bauthor\bsnmEdelman, \bfnmAlan\binitsA., \bauthor\bsnmArias, \bfnmTomás A.\binitsT. A. and \bauthor\bsnmSmith, \bfnmSteven T.\binitsS. T. (\byear1999). \btitleThe geometry of algorithms with orthogonality constraints. \bjournalSIAM J. Matrix Anal. Appl. \bvolume20 \bpages303–353. \biddoi=10.1137/S0895479895290954, issn=0895-4798, mr=1646856 \bptnotecheck year \bptokimsref\endbibitem

- Godambe (1960) {barticle}[mr] \bauthor\bsnmGodambe, \bfnmV. P.\binitsV. P. (\byear1960). \btitleAn optimum property of regular maximum likelihood estimation. \bjournalAnn. Math. Statist. \bvolume31 \bpages1208–1211. \bidissn=0003-4851, mr=0123385 \bptokimsref\endbibitem

- Härdle, Hall and Ichimura (1993) {barticle}[mr] \bauthor\bsnmHärdle, \bfnmWolfgang\binitsW., \bauthor\bsnmHall, \bfnmPeter\binitsP. and \bauthor\bsnmIchimura, \bfnmHidehiko\binitsH. (\byear1993). \btitleOptimal smoothing in single-index models. \bjournalAnn. Statist. \bvolume21 \bpages157–178. \biddoi=10.1214/aos/1176349020, issn=0090-5364, mr=1212171 \bptokimsref\endbibitem

- Kong and Xia (2012) {barticle}[mr] \bauthor\bsnmKong, \bfnmEfang\binitsE. and \bauthor\bsnmXia, \bfnmYingcun\binitsY. (\byear2012). \btitleA single-index quantile regression model and its estimation. \bjournalEconometric Theory \bvolume28 \bpages730–768. \biddoi=10.1017/S0266466611000788, issn=0266-4666, mr=2959124 \bptokimsref\endbibitem

- Li (1991) {barticle}[mr] \bauthor\bsnmLi, \bfnmKer-Chau\binitsK.-C. (\byear1991). \btitleSliced inverse regression for dimension reduction. \bjournalJ. Amer. Statist. Assoc. \bvolume86 \bpages316–342. \bidissn=0162-1459, mr=1137117 \bptokimsref\endbibitem

- Li (1992) {barticle}[mr] \bauthor\bsnmLi, \bfnmKer-Chau\binitsK.-C. (\byear1992). \btitleOn principal Hessian directions for data visualization and dimension reduction: Another application of Stein’s lemma. \bjournalJ. Amer. Statist. Assoc. \bvolume87 \bpages1025–1039. \bidissn=0162-1459, mr=1209564 \bptokimsref\endbibitem

- Li, Artemiou and Li (2011) {barticle}[mr] \bauthor\bsnmLi, \bfnmBing\binitsB., \bauthor\bsnmArtemiou, \bfnmAndreas\binitsA. and \bauthor\bsnmLi, \bfnmLexin\binitsL. (\byear2011). \btitlePrincipal support vector machines for linear and nonlinear sufficient dimension reduction. \bjournalAnn. Statist. \bvolume39 \bpages3182–3210. \biddoi=10.1214/11-AOS932, issn=0090-5364, mr=3012405 \bptokimsref\endbibitem

- Li and Dong (2009) {barticle}[mr] \bauthor\bsnmLi, \bfnmBing\binitsB. and \bauthor\bsnmDong, \bfnmYuexiao\binitsY. (\byear2009). \btitleDimension reduction for nonelliptically distributed predictors. \bjournalAnn. Statist. \bvolume37 \bpages1272–1298. \biddoi=10.1214/08-AOS598, issn=0090-5364, mr=2509074 \bptokimsref\endbibitem

- Li, Li and Zhu (2010) {barticle}[mr] \bauthor\bsnmLi, \bfnmLexin\binitsL., \bauthor\bsnmLi, \bfnmBing\binitsB. and \bauthor\bsnmZhu, \bfnmLi-Xing\binitsL.-X. (\byear2010). \btitleGroupwise dimension reduction. \bjournalJ. Amer. Statist. Assoc. \bvolume105 \bpages1188–1201. \biddoi=10.1198/jasa.2010.tm09643, issn=0162-1459, mr=2752614 \bptokimsref\endbibitem

- Li and McCullagh (1994) {barticle}[mr] \bauthor\bsnmLi, \bfnmBing\binitsB. and \bauthor\bsnmMcCullagh, \bfnmPeter\binitsP. (\byear1994). \btitlePotential functions and conservative estimating functions. \bjournalAnn. Statist. \bvolume22 \bpages340–356. \biddoi=10.1214/aos/1176325372, issn=0090-5364, mr=1272087 \bptokimsref\endbibitem

- Li, Zha and Chiaromonte (2005) {barticle}[mr] \bauthor\bsnmLi, \bfnmBing\binitsB., \bauthor\bsnmZha, \bfnmHongyuan\binitsH. and \bauthor\bsnmChiaromonte, \bfnmFrancesca\binitsF. (\byear2005). \btitleContour regression: A general approach to dimension reduction. \bjournalAnn. Statist. \bvolume33 \bpages1580–1616. \biddoi=10.1214/009053605000000192, issn=0090-5364, mr=2166556 \bptokimsref\endbibitem

- Luo, Li and Yin (2014) {bmisc}[auto] \bauthor\bsnmLuo, \bfnmW.\binitsW., \bauthor\bsnmLi, \bfnmB.\binitsB. and \bauthor\bsnmYin, \bfnmX.\binitsX. (\byear2014). \bhowpublishedSupplement to “On efficient dimension reduction with respect to a statistical functional of interest.” DOI:\doiurl10.1214/13-AOS1195SUPP. \bptokimsref\endbibitem

- Ma and Zhu (2012) {barticle}[mr] \bauthor\bsnmMa, \bfnmYanyuan\binitsY. and \bauthor\bsnmZhu, \bfnmLiping\binitsL. (\byear2012). \btitleA semiparametric approach to dimension reduction. \bjournalJ. Amer. Statist. Assoc. \bvolume107 \bpages168–179. \biddoi=10.1080/01621459.2011.646925, issn=0162-1459, mr=2949349 \bptokimsref\endbibitem

- Ma and Zhu (2013a) {barticle}[mr] \bauthor\bsnmMa, \bfnmYanyuan\binitsY. and \bauthor\bsnmZhu, \bfnmLiping\binitsL. (\byear2013a). \btitleEfficient estimation in sufficient dimension reduction. \bjournalAnn. Statist. \bvolume41 \bpages250–268. \biddoi=10.1214/12-AOS1072, issn=0090-5364, mr=3059417 \bptokimsref\endbibitem

- Ma and Zhu (2013b) {barticle}[mr] \bauthor\bsnmMa, \bfnmYanyuan\binitsY. and \bauthor\bsnmZhu, \bfnmLiping\binitsL. (\byear2013b). \btitleEfficiency loss and the linearity condition in dimension reduction. \bjournalBiometrika \bvolume100 \bpages371–383. \biddoi=10.1093/biomet/ass075, issn=0006-3444, mr=3068440 \bptokimsref\endbibitem

- McCullagh (1987) {bbook}[mr] \bauthor\bsnmMcCullagh, \bfnmPeter\binitsP. (\byear1987). \btitleTensor Methods in Statistics. \bpublisherChapman & Hall, \blocationLondon. \bidmr=0907286 \bptokimsref\endbibitem

- Székely and Rizzo (2009) {barticle}[mr] \bauthor\bsnmSzékely, \bfnmGábor J.\binitsG. J. and \bauthor\bsnmRizzo, \bfnmMaria L.\binitsM. L. (\byear2009). \btitleBrownian distance covariance. \bjournalAnn. Appl. Stat. \bvolume3 \bpages1236–1265. \biddoi=10.1214/09-AOAS312, issn=1932-6157, mr=2752127 \bptokimsref\endbibitem

- van der Vaart (1998) {bbook}[mr] \bauthor\bsnmvan der Vaart, \bfnmA. W.\binitsA. W. (\byear1998). \btitleAsymptotic Statistics. \bseriesCambridge Series in Statistical and Probabilistic Mathematics \bvolume3. \bpublisherCambridge Univ. Press, \blocationCambridge. \bidmr=1652247 \bptokimsref\endbibitem

- Wang and Xia (2008) {barticle}[mr] \bauthor\bsnmWang, \bfnmHansheng\binitsH. and \bauthor\bsnmXia, \bfnmYingcun\binitsY. (\byear2008). \btitleSliced regression for dimension reduction. \bjournalJ. Amer. Statist. Assoc. \bvolume103 \bpages811–821. \biddoi=10.1198/016214508000000418, issn=0162-1459, mr=2524332 \bptokimsref\endbibitem

- Xia (2007) {barticle}[mr] \bauthor\bsnmXia, \bfnmYingcun\binitsY. (\byear2007). \btitleA constructive approach to the estimation of dimension reduction directions. \bjournalAnn. Statist. \bvolume35 \bpages2654–2690. \biddoi=10.1214/009053607000000352, issn=0090-5364, mr=2382662 \bptokimsref\endbibitem

- Xia, Tong and Li (2002) {barticle}[mr] \bauthor\bsnmXia, \bfnmYingcun\binitsY., \bauthor\bsnmTong, \bfnmHowell\binitsH. and \bauthor\bsnmLi, \bfnmW. K.\binitsW. K. (\byear2002). \btitleSingle-index volatility models and estimation. \bjournalStatist. Sinica \bvolume12 \bpages785–799. \bidissn=1017-0405, mr=1929964 \bptokimsref\endbibitem

- Xia et al. (2002) {barticle}[mr] \bauthor\bsnmXia, \bfnmYingcun\binitsY., \bauthor\bsnmTong, \bfnmHowell\binitsH., \bauthor\bsnmLi, \bfnmW. K.\binitsW. K. and \bauthor\bsnmZhu, \bfnmLi-Xing\binitsL.-X. (\byear2002). \btitleAn adaptive estimation of dimension reduction space. \bjournalJ. R. Stat. Soc. Ser. B Stat. Methodol. \bvolume64 \bpages363–410. \biddoi=10.1111/1467-9868.03411, issn=1369-7412, mr=1924297 \bptnotecheck related \bptokimsref\endbibitem

- Ye and Weiss (2003) {barticle}[mr] \bauthor\bsnmYe, \bfnmZhishen\binitsZ. and \bauthor\bsnmWeiss, \bfnmRobert E.\binitsR. E. (\byear2003). \btitleUsing the bootstrap to select one of a new class of dimension reduction methods. \bjournalJ. Amer. Statist. Assoc. \bvolume98 \bpages968–979. \biddoi=10.1198/016214503000000927, issn=0162-1459, mr=2041485 \bptokimsref\endbibitem

- Yin and Cook (2002) {barticle}[mr] \bauthor\bsnmYin, \bfnmXiangrong\binitsX. and \bauthor\bsnmCook, \bfnmR. Dennis\binitsR. D. (\byear2002). \btitleDimension reduction for the conditional th moment in regression. \bjournalJ. R. Stat. Soc. Ser. B Stat. Methodol. \bvolume64 \bpages159–175. \biddoi=10.1111/1467-9868.00330, issn=1369-7412, mr=1904698 \bptokimsref\endbibitem

- Yin and Li (2011) {barticle}[mr] \bauthor\bsnmYin, \bfnmXiangrong\binitsX. and \bauthor\bsnmLi, \bfnmBing\binitsB. (\byear2011). \btitleSufficient dimension reduction based on an ensemble of minimum average variance estimators. \bjournalAnn. Statist. \bvolume39 \bpages3392–3416. \biddoi=10.1214/11-AOS950, issn=0090-5364, mr=3012413 \bptokimsref\endbibitem

- Yin, Li and Cook (2008) {barticle}[mr] \bauthor\bsnmYin, \bfnmXiangrong\binitsX., \bauthor\bsnmLi, \bfnmBing\binitsB. and \bauthor\bsnmCook, \bfnmR. Dennis\binitsR. D. (\byear2008). \btitleSuccessive direction extraction for estimating the central subspace in a multiple-index regression. \bjournalJ. Multivariate Anal. \bvolume99 \bpages1733–1757. \biddoi=10.1016/j.jmva.2008.01.006, issn=0047-259X, mr=2444817 \bptokimsref\endbibitem

- Zhu, Dong and Li (2013) {barticle}[mr] \bauthor\bsnmZhu, \bfnmLiping\binitsL., \bauthor\bsnmDong, \bfnmYuexiao\binitsY. and \bauthor\bsnmLi, \bfnmRunze\binitsR. (\byear2013). \btitleSemiparametric estimation of conditional heteroscedasticity via single-index modeling. \bjournalStatist. Sinica \bvolume23 \bpages1235–1255. \bidissn=1017-0405, mr=3114712 \bptnotecheck year \bptokimsref\endbibitem

- Zhu and Zeng (2006) {barticle}[mr] \bauthor\bsnmZhu, \bfnmYu\binitsY. and \bauthor\bsnmZeng, \bfnmPeng\binitsP. (\byear2006). \btitleFourier methods for estimating the central subspace and the central mean subspace in regression. \bjournalJ. Amer. Statist. Assoc. \bvolume101 \bpages1638–1651. \biddoi=10.1198/016214506000000140, issn=0162-1459, mr=2279485 \bptokimsref\endbibitem

- Zhu and Zhu (2009) {barticle}[mr] \bauthor\bsnmZhu, \bfnmLi-Ping\binitsL.-P. and \bauthor\bsnmZhu, \bfnmLi-Xing\binitsL.-X. (\byear2009). \btitleDimension reduction for conditional variance in regressions. \bjournalStatist. Sinica \bvolume19 \bpages869–883. \bidissn=1017-0405, mr=2514192 \bptokimsref\endbibitem

- Zou and Yuan (2008) {barticle}[mr] \bauthor\bsnmZou, \bfnmHui\binitsH. and \bauthor\bsnmYuan, \bfnmMing\binitsM. (\byear2008). \btitleComposite quantile regression and the oracle model selection theory. \bjournalAnn. Statist. \bvolume36 \bpages1108–1126. \biddoi=10.1214/07-AOS507, issn=0090-5364, mr=2418651 \bptokimsref\endbibitem