∎

22email: mike.giles@maths.ox.ac.uk 33institutetext: Yuan Xia44institutetext: Mathematical Institute and Oxford-Man Institute of Quantitative Finance, Oxford University

44email: yuan.xia.cn@gmail.com

Multilevel Monte Carlo For Exponential Lévy Models

Abstract

We apply the multilevel Monte Carlo method for option pricing problems using exponential Lévy models with a uniform timestep discretisation. For lookback and barrier options, we derive estimates of the convergence rate of the error introduced by the discrete monitoring of the running supremum of a broad class of Lévy processes. We then use these to obtain upper bounds on the multilevel Monte Carlo variance convergence rate for the Variance Gamma, NIG and -stable processes. We also provide analysis of a trapezoidal approximation for Asian options. Our method is illustrated by numerical experiments.

JEL Classification C15 C63

Keywords:

multilevel Monte Carlo exponential Lévy models Asian options lookback options barrier optionsMSC:

65C05 91G601 Introduction

Exponential Lévy models are based on the assumption that asset returns follow a Lévy process schoutens03 ; ct04 . The asset price follows

| (1) |

where is an -Lévy process

where is a constant, is a Brownian Motion, is the jump measure and is the Lévy measure(c.f. Theorem 42 in protter04 ).

Models with jumps give an intuitive explanation of implied volatility skew and smile in the index option market and foreign exchange market(Chapter 11 in ct04 ). The jump fear is mainly on the downside in the equity market which produces a premium for low-strike options; the jump risk is symmetric in the foreign exchange market so the implied volatility has a smile shape. Chapter 7 in ct04 shows that models building on pure jump processes can reproduce the stylized facts of asset returns, like heavy tails and the asymmetric distribution of increments. Since pure jump processes of finite activity without a diffusion component cannot generate a realistic path, it is natural to allow the jump activity to be infinite. In this work we deal with infinite-activity pure jump exponential Lévy models, in particular models driven by Variance Gamma (VG), Normal Inverse Gaussian (NIG) and -stable processes which allow direct simulation of increments.

We are interested in estimating the expected payoff value in option pricing problems. In the case of European options, it is possible to directly sample the final value of the underlying Lévy process, but in the case of Asian, lookback and barrier options the option value depends on functionals of the Lévy process and so it is necessary to approximate those. In the case of a VG model with a lookback option, the convergence results in dl11 show that to achieve an root mean square (RMS) error using a standard Monte Carlo method with a uniform timestep discretisation requires paths, each with timesteps, leading to a computational complexity of .

In the case of simple Brownian diffusion, Giles giles07b ; giles08b introduced a multilevel Monte Carlo (MLMC) method, reducing the computational complexity from to for a variety of payoffs. The objective of this paper is to investigate whether similar benefits can be obtained for exponential Lévy processes.

Various researchers have investigated simulation methods for the running maximum of Lévy processes. Reference ft12 develops an adaptive Monte Carlo method for functionals of killed Lévy processes with a controlled bias. Small-time asymptotic expansions of the exit probability are given with computable error bounds. For evaluating the exit probability when the barrier is close to the starting point of the process, this algorithm outperforms a uniform discretisation significantly. Reference kkpv12 develops a novel Wiener-Hopf Monte-Carlo method to generate the joint distribution of which is further extended to MLMC in fkss12 , obtaining an RMS error with a computational complexity of for Lévy processes with bounded variation and for processes with infinite variation. The method currently cannot be directly applied to VG, NIG and stable processes. References dh10 ; dereich11 adapt MLMC to Lévy-driven SDEs with payoffs which are Lipschitz w.r.t. the supremum norm. If the Lévy process does not incorporate a Brownian process, reference dereich11 obtains an upper bound on the worst case computational complexity, where is the BG index which will be defined later.

In contrast to those advanced techniques, we take the discretely monitored maximum based on a uniform timestep discretisation of the Lévy process as the approximation. The outline of the work is as follows. First we review the Multilevel Monte Carlo method and present the three Lévy processes we will consider in our numerical experiments. To prepare for the analysis of the multilevel variance of lookback and barrier, we bound the convergence rate of the discretely monitored running maximum for a large class of Lévy processes whose Lévy measures have a power law behavior for small jumps, and have exponential tails. Based on this, we conclude by bounding the variance of the multilevel estimators. Numerical results are then presented for the multilevel Monte Carlo applied to Asian, lookback and barrier options using the three different exponential Lévy models.

2 Multilevel Monte Carlo (MLMC) method

For a path-dependent payoff based on an exponential Lévy model on the time interval , let denote its approximation using a discretisation with uniform timesteps of size on level ; in the numerical results reported later, we use . Due to the linearity of the expectation operator, we have the following identity:

| (2) |

Let denote the standard Monte Carlo estimate for using paths, and for , we use independent paths to estimate using

| (3) |

For a given path generated for , we can calculate using the same underlying Lévy path. The multilevel method exploits the fact that decreases with , and adaptively chooses to minimise the computational cost to achieve a desired RMS error. This is summarized in the following theorem in giles12 ; giles15 :

Theorem 2.1

Let denote a functional of , and let denote the corresponding approximation using a discretisation with uniform timestep . If there exist independent estimators based on Monte Carlo samples, each with complexity , and positive constants such that and

-

i)

-

ii)

-

iii)

-

iv)

,

then there exists a positive constant such that for any there are values and for which the multilevel estimator

has a mean-square-error with bound

with a computational complexity with bound

We will focus on the multilevel variance convergence rate in the following numerical results and analysis since it is crucial in determining the computational complexity.

3 Lévy models

The numerical results to be presented later use the following three models.

3.1 Variance Gamma (VG)

The VG process with parameter set is the Lévy process with characteristic function The Lévy measure of the VG process is (Table 4.5 in ct04)

One advantage of the VG process is that its additional parameters make it possible to fit the skewness and kurtosis of the stock returns (section 7.3 in ct04 ). Another is that it is easily simulated as we have a subordinator representation in which is a Brownian process and the subordinator is a Gamma process with parameters ().

For the ease of computation, we follow the mean-correcting pricing measure in section 6.2.2 in schoutens03 , with risk-free interest rate . Let be a martingale. This results in the drift being

After transforming the parameter representation to the definition we use, the calibration in table 6.3 in schoutens03 gives .

3.2 Normal Inverse Gaussian (NIG)

The NIG process with parameter set is the Lévy process with characteristic function and Lévy measure

is the modified Bessel function of the second kind (section 4.4.3 in ct04 ). As , while as ,

In terms of simulation, the NIG process can be represented as , where the subordinator is an Inverse Gaussian process with parameters . Algorithm 6.9 in ct04 can be used to generate Inverse Gaussian samples.

Using the mean-correcting pricing measure leads to

Following the calibration in schoutens03 we use the parameters , and again use risk-free interest rate .

3.3 Spectrally negative -stable process

The scalar spectrally negative -stable process has a Lévy measure of the form; see section 1.2.6 in kyprianou06 :

for and some non-negative . We follow the reference to discuss another parameterisation of -stable process with characteristic function

| (4) |

where sgn if and sgn.There are no positive jumps for the spectrally negative process, which has a finite exponential moment cw03 .

4 Key numerical analysis results

The variance of the multilevel correction, depends on the behavior of the difference between the continuously and discretely monitored suprema of , defined for a unit time interval as

To derive the order of weak convergence for lookback-type payoffs, we are concerned with , which is extensively studied in the literature. For example, dl11 , chen11 and cfs11 derive asymptotic expansions for jump-diffusion, VG, NIG processes, as well as estimates for general Lévy processes, by using Spitzer’s identity spitzer56 .

A key result due to Chen chen11 is the following:

Theorem 4.1

Suppose is a scalar Lévy process with triple with finite first moment, i.e.

Then satisfies

-

1.

If

-

2.

If and is of finite variation, i.e.

-

3.

If and is of infinite variation, then

where

is the Blumenthal-Getoor index of , and is an arbitrarily small strictly positive constant.

The VG process has finite variation with Blumenthal-Getoor index ; the NIG process has infinite variation with Blumenthal-Getoor index . They correspond to the second and third cases of Theorem 4.1 respectively.

For the multilevel variance analysis we require higher moments of . In the pure Brownian case, Asmussen et al (agp1995 ) obtain the asymptotic distribution of , which in turn gives the asymptotic behavior of . dl11 extends theresult to finite activity jump processes with non-zero diffusion.

However, in this paper we are looking at infinite activity jump processes. Our main new result is therefore concerned with the convergence rate of for pure jump Lévy processes. This will be used later to bound the variance of the Multilevel Monte Carlo correction term for both lookback and barrier options.

Theorem 4.2

Let be a scalar pure jump Lévy process, and suppose its Lévy measure satisfies

| (5) |

where are constants. Then for

satisfies

If, in addition, is spectrally negative, i.e. for , then

for any .

We will give the proof of this result later in Section 7.6. Note that for , the general bound in Theorem 4.2 is slightly sharper than Chen’s result for , is the same for , and is not as tight as Chen’s result for ; the spectrally negative bound is slightly sharper than Chen’s result for , and the bound is the same for .

5 MLMC analysis

5.1 Asian options

We consider the analysis for a Lipschitz arithmetic Asian payoff where

and is Lipschitz such that .

We approximate the integral using a trapezoidal approximation:

| (6) |

and the approximated payoff is then .

Proposition 1

Let be a scalar Lévy process underlying an exponential Lévy model. If are as defined above, and , then

The proof will be given later in Section 7.1. Using the Lipschitz property, the weak convergence for the numerical approximation is given by

while the convergence of the MLMC variance follows from

5.2 Lookback options

In exponential Lévy models, the moment generating function can be infinite for large value of . To avoid problems due to this, we consider a lookback put option which has a bounded payoff

| (7) |

where Note that is a Lipschitz function of , since we have . Without loss of generality, we assume in the following.

Because of the Lipschitz property, we have where . Therefore we obtain weak convergence for the processes covered by Theorem 4.1, with the convergence rate given by the Theorem.

To analyse the variance, , we first note that

where . Hence, we have

Theorem 4.2 then provides the following bounds on the variance for the VG, NIG and spectrally negative -stable processes.

Proposition 2

Let be a scalar Lévy process underlying an exponential Lévy model. For the Lipschitz lookback put payoff (7), we have the following multilevel variance convergence rate results:

-

1.

If is a Variance Gamma (VG) process, then ;

-

2.

If is a Normal Inverse Gaussian (NIG) process, then ;

-

3.

If is a spectrally negative -stable process with , then , for any small

5.3 Barrier options

We consider a bounded up-and-out barrier option with discounted payoff

| (8) |

where again , and is bounded. On level , the numerical approximation is

| (9) |

where .

Our analysis for NIG and the spectrally negative -stable processes requires the following quite general result.

Proposition 3

If is a random variable with a locally bounded density in a neighbourhood of , and is a numerical approximation to , then for any there exists a constant such that

Proof

This result was first proved by Avikainen (Lemma 3.4 in avikainen09 ), but we give here a simpler proof. If, for some fixed , we have and , then . Hence,

with the first term being due to the local bound of ’s density and the second term due to the Markov inequality. Differentiating the upper bound w.r.t. , we find that it is minimised by choosing and we then get the desired bound.

Our analysis for the Variance Gamma process requires a sharper result customised to the properties of Lévy processes.

Proposition 4

If is a scalar pure jump Lévy process satisfying the conditions of Theorem 4.2 with , and and are the continuously and discretely monitored suprema of and has a locally bounded density in a neighbourhood of , then

for any .

The proof is given later in Section 7.7.

Both of the above propositions require the condition that the supremum has a locally bounded density for all strictly positive values. There is considerable current research on the supremum of Lévy processes chaumont13 ; cm15 ; kuznetsov11 ; kmr13 . In particular, the comments following Proposition 2 in cm15 indicate that the condition is satisfied by stable processes, and by a wide class of symmetric subordinated Brownian motions. Unfortunately, the VG and NIG processes in the current paper are not symmetric, so at present they lie outside the range of current theory, but new theory under development blanchet15 will extend the property to a larger class of Lévy processes including both VG and NIG.

We now bound the weak convergence of the estimator and the multilevel variance convergence.

Proposition 5

Let be a scalar Lévy process underlying an exponential Lévy model. For the up-and-out barrier option payoff (8), with the numerical approximation (9), we have the following rates of convergence for the multilevel correction variance and the weak error, assuming that has a bounded density:

-

•

If is a Variance Gamma (VG) process, then

where is an arbitrary positive number.

-

•

If is a NIG process, then

where is an arbitrary positive number.

-

•

If is a spectrally negative -stable process with , then

where is an arbitrary positive number.

Proof

The variance of the multilevel correction term is bounded by

For an up-and-out Barrier option, since the payoff is bounded we have

where .

6 Numerical results

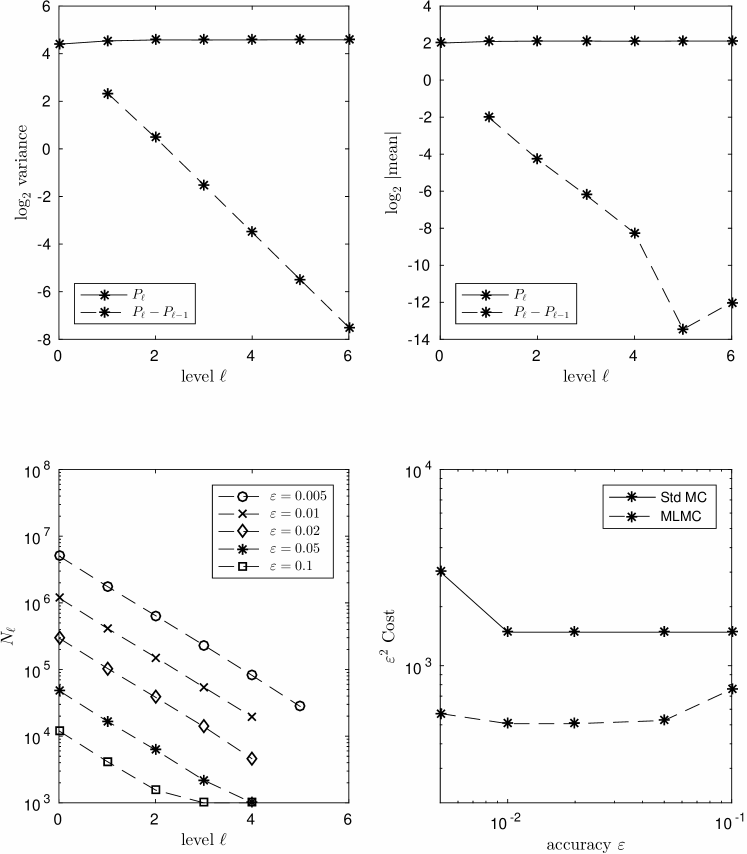

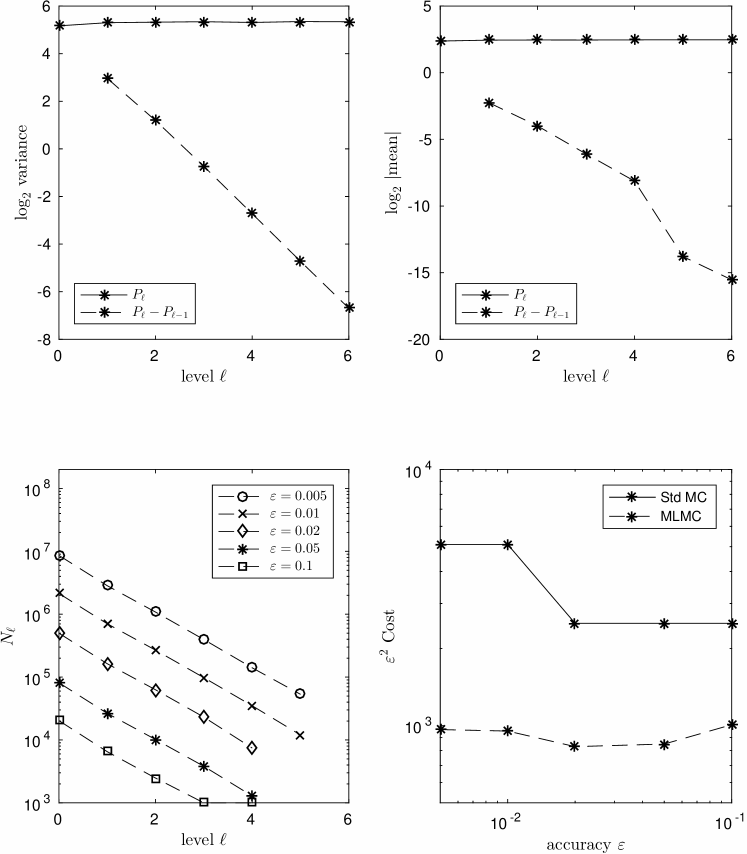

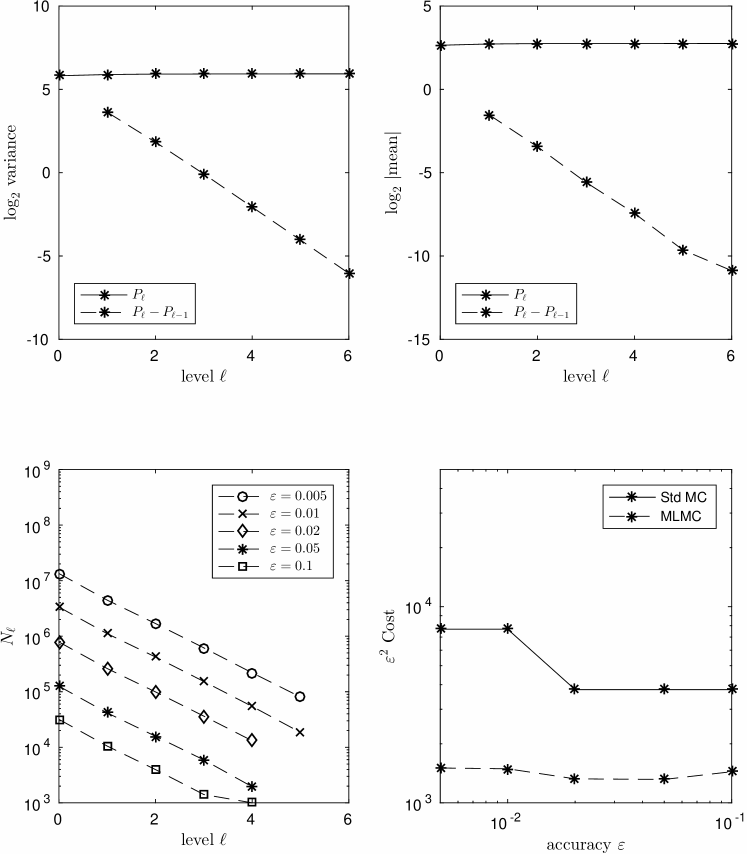

We have numerical results for three different Lévy models: Variance Gamma, Normal Inverse Gaussian and -stable processes, and three different options: Asian, lookback and barrier.

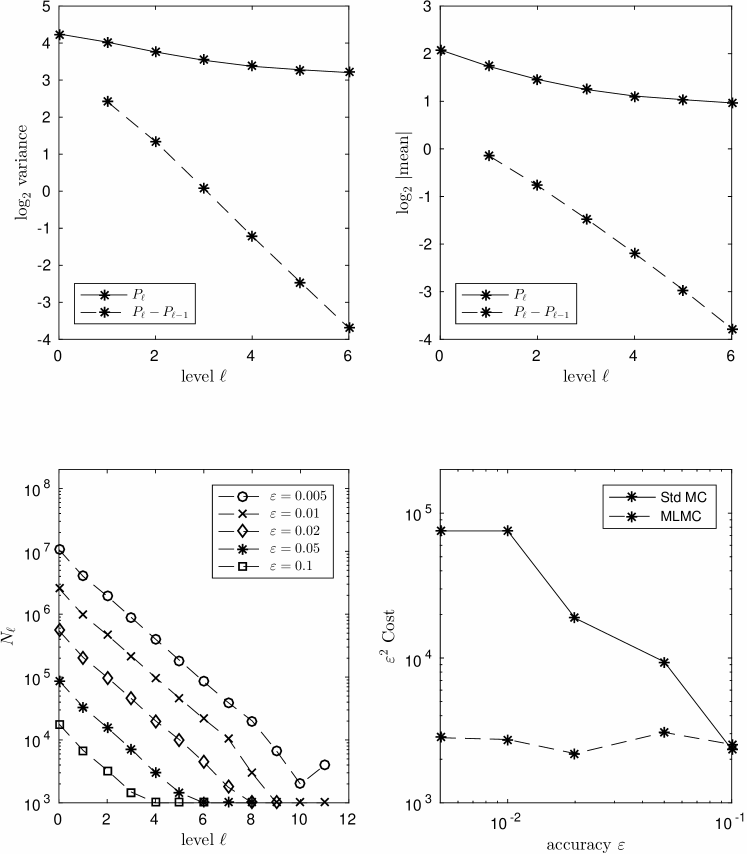

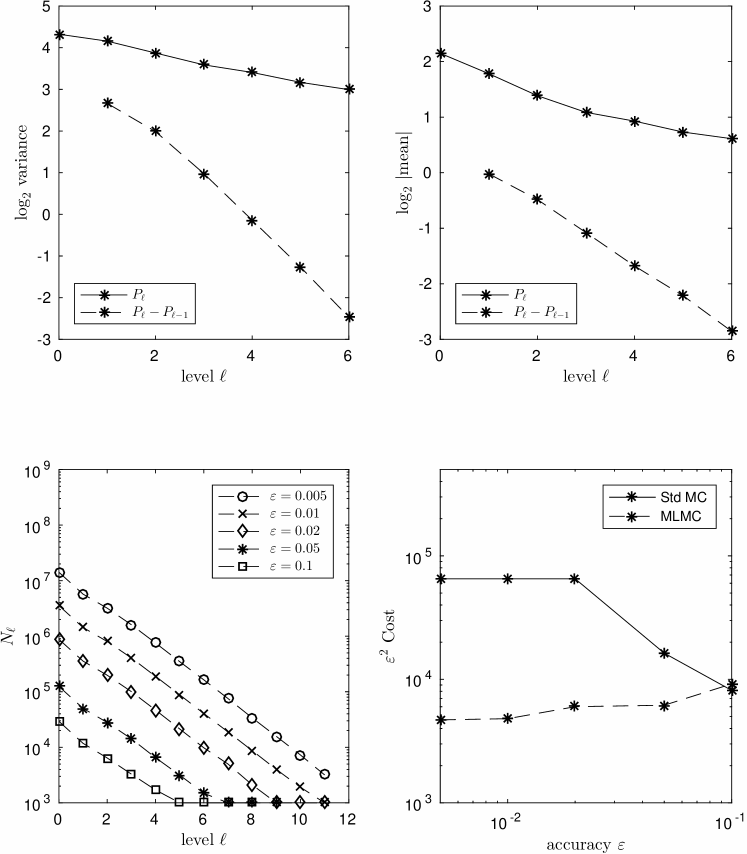

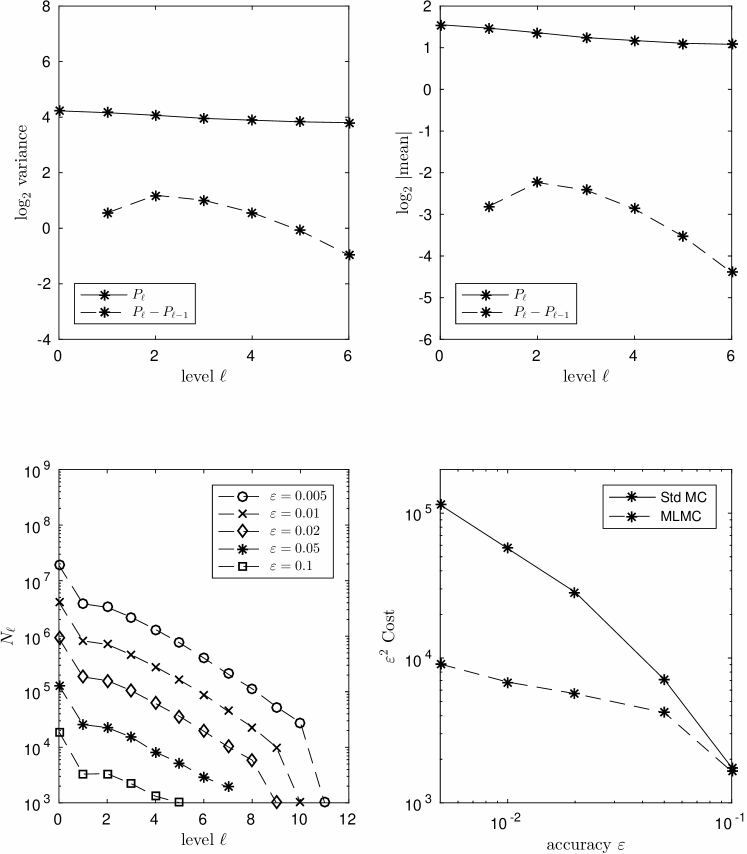

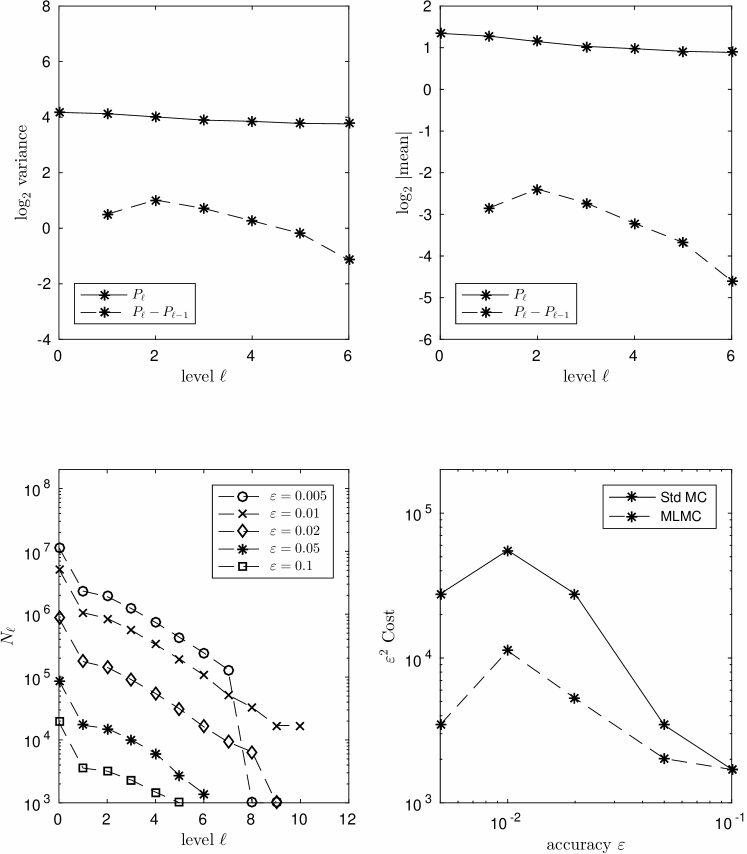

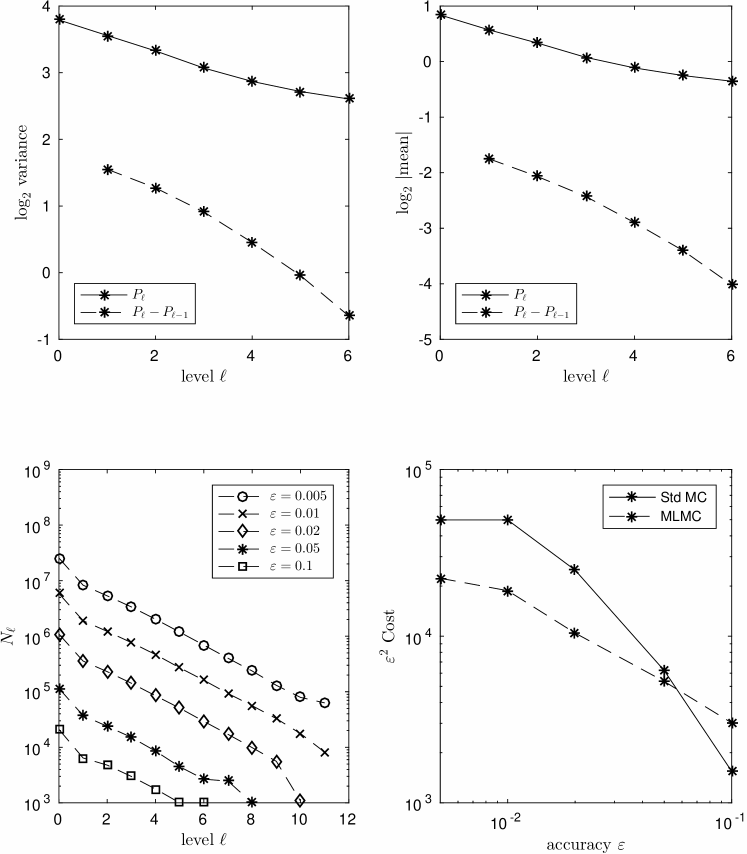

The current code is based on Giles’ MATLAB code giles08b , using which we generate standardised numerical results and a set of four figures. The top two plots correspond to a set of experiments to investigate how the variance and mean for both and vary with level . The top left plot shows the values for , so that the absolute value of the slope of the line for indicates the convergence rate of in condition i) of Thereom 2.1. Similarly, the absolute value of the slope of the line for in the top right plot indicates the weak convergence rate in the condition i) of Thereom 2.1.

The bottom two plots correspond to a set of MLMC calculations for different values of the desired accuracy . Each line in the bottom left plot corresponds to one multilevel calculation and displays the number of samples on each level. Note that as is varied, the MLMC algorithm automatically decides how many levels are required to reduce the weak error appropriately. The optimal number of samples on each level is based on an empirical estimation of the multilevel correction variance , together with the use of a Lagrange multiplier to determine how best to minimise the overall computational cost for a given target accuracy. A complete description of the algorithm is given in giles15 . The bottom right plots show the variation of the computational complexity with the desired accuracy . In the best cases, the MLMC complexity is , and therefore the plot is of versus so that we can see whether this is achieved, and compare the complexity to that of the standard Monte Carlo method.

6.1 Asian option

The Asian option we consider is an arithmetic Asian call option with discounted payoff

where , , , and

For a general Lévy process it is not easy to directly sample the integral process. We use the trapezoidal approximation

where is the number of timesteps. The payoff approximation is then

In the multilevel estimator, the approximation on level is obtained using timesteps.

Figures 1, 2, 3 are for the VG, NIG and -stable models respectively. The numerical results in the top right plots indicate approximately second order weak convergence. With the standard Monte Carlo method, the top left plots show that the variance is approximately independent, and therefore, the standard Monte Carlo calculation has computational cost . Multiplying this cost by to create the bottom right complexity plots, the scaled cost is and therefore goes up in steps as is reduced, when decreasing requires an increase in the value of the finest level . On the other hand, the convergence rate of the variance of the MLMC estimator is approximately for VG, for NIG and for the -stable model. Since in all three cases we have , the MLMC theorem gives a complexity which is which is consistent with the results in the bottom right plots which show little variation in for the MLMC estimator.

For this Asian option, MLMC is 3-8 times more efficient than standard MC. The gains are modest because the high rate of weak convergence means that only 4 levels of refinement are required in most cases, so there is only a difference in cost between each MC path calculation on the finest level, and each of the MLMC path calculations on the coarsest level.

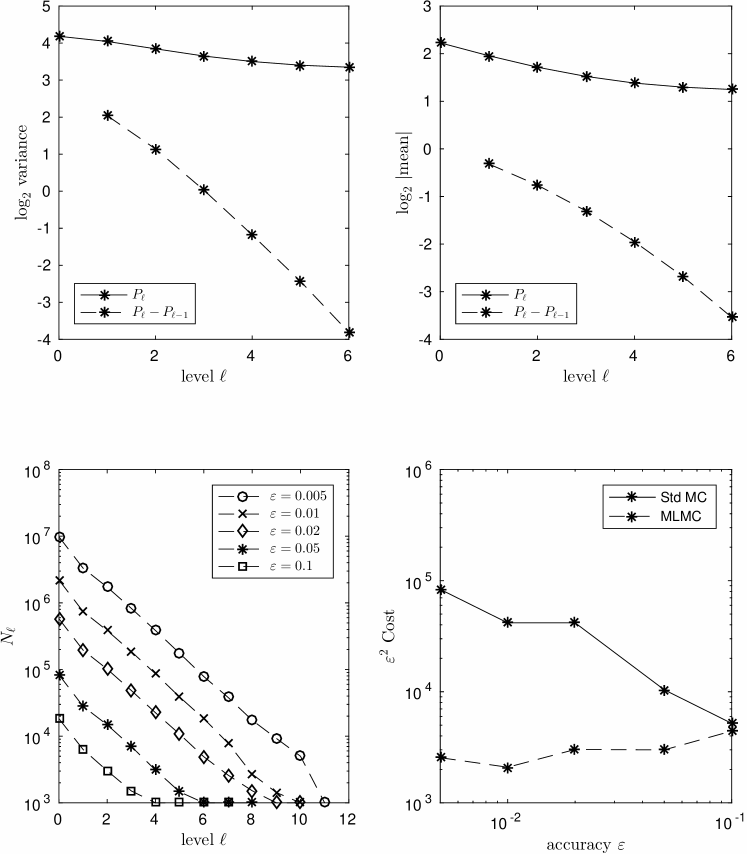

6.2

Lookback option

The lookback option we consider is a put option on the floating underlying,

where , with , , , . We use the discretely monitored maximum as the approximation, so that

Figures 4, 5, 6 show the numerical results for the VG, NIG and -stable models. The most obvious difference compared to the Asian option is a greatly reduced order of weak convergence, approximately , and in the respective cases. This reduced weak convergence leads to a big increase in the finest approximation level, which in turn greatly increases the standard MC cost but doesn’t significantly change the MLMC cost. Hence, the computational savings are much greater than for the Asian option, with savings of up to a factor of 30.

The small erratic fluctuation in on levels greater than is due to poor estimates of the variance due to a limited number of samples. This also appears later for the barrier option.

6.3 Barrier option

The barrier option is an up-and-out call with payoff

with , , , , . The discretely monitored approximation is

With the barrier option, the most noticeable change from the previous options is a reduction in the rate of convergence of the MLMC variance, with in the three cases. For , the MLMC theorem proves a complexity which is , with here being the rate of weak convergence. The fact that the MLMC complexity is not is clearly visible from the bottom right complexity plots, but there are still significant savings compared to the standard MC computations.

6.4 Summary and discussion

Table 1 summarizes the convergence rates for the weak error and the MLMC variance given by Propositions 1, 2, 5, and the empirical convergence rates observed in the numerical experiments.

In general, the agreement between the analysis and the numerical rates of convergence is quite good, suggesting that in most cases the analysis may be sharp. The most obvious gap between the two is with the weak order of convergence for the Asian option with all three models; the analysis proves an bound, whereas the numerical results suggest it is actually . The numerical results are perhaps not surprising as is the order of convergence of trapezoidal integration of a smooth function, and therefore it is the order one would expect if the payoff was simply a multiple of .

| VG | ||||

|---|---|---|---|---|

| numerical | analysis | |||

| option | weak | var | weak | var |

| Asian | ||||

| lookback | ||||

| barrier | ||||

| NIG | ||||

|---|---|---|---|---|

| numerical | analysis | |||

| option | weak | var | weak | var |

| Asian | ||||

| lookback | ||||

| barrier | ||||

| spectrally negative -stable with | ||||

|---|---|---|---|---|

| numerical for | analysis | |||

| option | weak | var | weak | var |

| Asian | ||||

| lookback | ||||

| barrier | ||||

7 Proofs

7.1 Proof of Proposition 1

Proof

We decompose the difference between the true value and approximation into parts which we can bound separately:

If we define

then

We have , and due to the independence of and we obtain

| (10) | |||||

Defining , we have . Furthermore, by the Cauchy-Schwarz inequality,

Note that for , and therefore for we have and hence

Now we calculate the second term in (10). Note that for is independent of , and is independent of so

Firstly, for ,

Moreover, we have and

Thus, for ,

Hence,

and we can therefore conclude that

7.2 Lévy process decomposition

The proofs rely on a decomposition of the Lévy process into a combination of a finite-activity pure jump part, a drift part, and a residual part consisting of very small jumps.

Let be an -Lévy process:

| (11) |

The finite activity jump part is defined by

to be the compound Poisson process truncating the jumps of smaller than which is assumed to satisfy . The intensity of and the c.d.f. of are

| (12) | |||||

The drift rate for the drift term is defined to be

| (13) |

so that the residual term is then a martingale:

| (14) |

We define

| (15) |

so that .

These three quantities, , and will all play a major role in the subsequent numerical analysis.

We bound by the difference between continuous maxima and 2-point maxima over all timesteps:

| (16) |

where the random variables

are independent and identically distributed. If we now define

then

| (17) | |||||

where we use with , in the first inequality, and , in the second inequality.

Let and . Then, for , Jensen’s inequality gives us

where in the final step we have used the fact that all of the have the same distribution as .

The task now is to bound the first and third terms in the final line of (7.2).

7.3 Bounding moments of

Theorem 7.1

Let be a scalar Lévy process with a triple , and let , , and be as defined in section 7.2.

Then provided , for any there exists a constant such that

| (19) |

where is a function depending on the Lévy measure .

Proof

Let

We will determine an upper bound on by analysing the jump behavior of the finite-activity process in a single interval .

Let be the number of jumps. If , then , while if , then . This can be seen from the behavior of in the different scenarios illustrated in Figure 10. More generally, if , then

Since

it follows that

| (20) | |||||

where . We then have

For there exists such that for any , , so

for some constant , where the last step uses the fact that

Therefore, we obtain the final result that

7.4 Bounding moments of

Proposition 6

Let be a scalar Lévy process with a triple and let , , and be as defined in section 7.2. Then satisfies

| (21) |

where is a constant depending on .

Proof

For any , by Jensen’s inequality and the Doob inequality (c.f. Theorem 19 and 20 in protter04 ),

For any , the Burkholder–Davis–Gundy inequality (c.f. Theorem 73 in protter04 ) gives

where is the quadratic variation of . We can use the method in the proof of Theorem 66inprotter04 to get

where is a constant depending on .

To extend this result to an arbitrary time interval we use a change of time coordinate, , with associated changed Lévy measure to obtain

7.5 Bounding moments of

Proposition 7

Let be a scalar pure jump Lévy process, with Lévy measure which satisfies

for constants and . If is as defined in section 7.2, and , then for and arbitrary there exists a constant , which does not depend on such that

In the particular case of , such a bound holds with .

Proof

Given , for any , Jensen’s inequality gives us

If , then the desired bound is obtained immediately. On the other hand, if , then

Since it implies that and thus is bounded. Hence there exists a constant such that

and by choosing large enough so that we obtain the desired bound.

7.6 Proof of Theorem 4.2

Proof

Provided , by (7.2) and (19) we have

| (22) |

where the notation means there exists constant independent of such that .

We can now bound each term, given the specification of the Lévy measure, and if we can choose appropriately how as so that the RHS of (22) is convergent, then the convergence rate of can be bounded.

For ,

| (25) | |||||

where are constants with , while for ,

If , then

| (29) | |||||

where are additional constants. If , it is easily verified that is bounded for , so (29) applies equally to this case.

Given we have

| (32) | |||||

Subject to the condition that , we now have

In the following we assume

-

1.

.

If we choose , then and the constant can be taken to be sufficiently small so that for sufficiently large .

Taking , we find that the dominant contribution to (22) comes from 3), giving the desired result that

-

2.

.

We can use Hölder’s inequality to give

For a spectrally negative process, , since doesn’t have positive jumps, and hence

We can take with the constant again chosen so that for sufficiently large . We then obtain

for any .

7.7 Proof of Proposition 4

We decompose the term we want to bound into parts and then balance their asymptotic orders to get desired result.

Note that only if either is close to the barrier or the difference between discretely and continuously monitored maximum is large. More precisely,

where and for an to be determined. Hence

Due to the locally bounded density for , .

If we denote

where is as defined previously in Section 7.2, then (17) gives

For , is bounded, so , for sufficiently large . Hence,

Now, requires that there are at least two jumps in one of the intervals. The probability of two jumps in one particular interval is

if , and hence

We use the Markov inequality for the remaining term. According to Proposition 6, and so

Combining these elements, provided , we have

Equating the first two terms on the right hand side gives .

If , then , so is satisfied. We also have and therefore for any we have

If , then , and hence . Balancing and , gives and

| (33) |

Since as , and , for any fixed value of it is possible to choose appropriate values of and to satisfy (33) and thereby conclude that

Acknowledgements.

This work was supported by the China Scholarship Council and the Oxford-Man Institute of Quantitative Finance. We would like to thank Ben Hambly, Andreas Kyprianou, Loic Chaumont, Jacek Malecki and Jose Blanchet for their helpful comments.References

- (1) Asmussen, S., Glynn, P., Pitman, J.: Discretization error in simulation of one-dimensional reflecting Brownian motion. The Annals of Applied Probability 5(4), 875–896 (1995)

- (2) Avikainen, R.: Convergence rates for approximations of functionals of SDEs. Finance and Stochastics 13(3), 381–401 (2009)

- (3) Blanchet, J.: personal communication (2015)

- (4) Carr, P., Wu, L.: The Finite Moment Log Stable Process and Option Pricing. The Journal of Finance 58(2), 753–778 (2003)

- (5) Chambers, J.M., Mallows, C.L., Stuck, B.: A method for simulating stable random variables. Journal of the American Statistical Association 71(354), 340–344 (1976)

- (6) Chaumont, L.: On the law of the supremum of Lévy processes. The Annals of Probability 41(3A), 1191–1217. (2013)

- (7) Chaumont, L., Malecki, J.: The asymptotic behavior of the density of the supremum of Lévy processes. Annales de l’Institut Henri Poincaré 52(3), 1178–1195 (2016)

- (8) Chen, A.: Sampling error of the supremum of a Lévy process. Ph.D. thesis, University of Illinois at Urbana-Champaign (2011). URL https://www.ideals.illinois.edu/handle/2142/26321

- (9) Chen, A., Feng, L., Song, R.: On the monitoring error of the supremum of a normal jump diffusion process. Journal of Applied Probability 48(4), 1021–1034 (2011)

- (10) Cont, R., Tankov, P.: Financial modelling with jump processes. Chapman & Hall/CRC, London (2004)

- (11) Dereich, S.: Multilevel Monte Carlo Algorithms for Lévy-driven SDEs with Gaussian correction. The Annals of Applied Probability 21(1), 283–311 (2011)

- (12) Dereich, S., Heidenreich, F.: A multilevel Monte Carlo algorithm for Lévy-driven stochastic differential equations. Stochastic Processes and their Applications 121(7), 1565–1587 (2011)

- (13) Dia, E., Lamberton, D.: Connecting discrete and continuous lookback or hindsight options in exponential Lévy models. Advances in Applied Probability 43(4), 1136–1165 (2011)

- (14) Ferreiro-Castilla, A., Kyprianou, A.E., Scheichl, R., Suryanarayana, G.: Multilevel Monte Carlo simulation for Lévy processes based on the Wiener–Hopf factorisation. Stochastic Processes and their Applications 124(2), 985–1010 (2014)

- (15) Figueroa-López, J., Tankov, P.: Small-time asymptotics of stopped Lévy bridges and simulation schemes with controlled bias. Bernoulli, 20(3), 1126–1164 (2014)

- (16) Giles, M.: Improved multilevel Monte Carlo convergence using the Milstein scheme. In: A. Keller, S. Heinrich, H. Niederreiter (eds.) Monte Carlo and Quasi-Monte Carlo Methods 2006, pp. 343–358. Springer-Verlag, Berlin Heidelberg New York (2007)

- (17) Giles, M.: Multilevel Monte Carlo path simulation. Operations Research 56(3), 607–617 (2008)

- (18) Giles, M.B.: Multilevel Monte Carlo methods. In: Monte Carlo and Quasi-Monte Carlo Methods 2012. Springer-Verlag (2012)

- (19) Giles, M.B.: Multilevel Monte Carlo methods. Acta Numerica 24, 259–328 (2015)

- (20) Kuznetsov, A., Kyprianou, A., Pardo, J., Van Schaik, K.: A Wiener–Hopf Monte Carlo simulation technique for Lévy processes. The Annals of Applied Probability 21(6), 2171–2190 (2011)

- (21) Kuznetsov, A.: On extrema of stable processes. The Annals of Probability 39(3), 1027–1060 (2011)

- (22) Kwasnicki, M., Malecki, J., Ryznar, M.: Suprema of Lévy processes. The Annals of Probability 41(3B), 2047–2065 (2013)

- (23) Kyprianou, A.: Introductory lectures on fluctuations of Lévy processes with applications. Springer Verlag, Berlin Heidelberg New York (2006)

- (24) Protter, P.: Stochastic integration and differential equations. Springer Verlag, Berlin Heidelberg New York (2004)

- (25) Schoutens, W.: Lévy processes in finance: pricing financial derivatives. Wiley-Blackwell, New Jersey (2003)

- (26) Spitzer, F.: A combinatorial lemma and its application to probability theory. Trans. Amer. Math. Soc 82(2), 323–339 (1956)