Majorization and a Schur–Horn Theorem

for positive compact operators,

the nonzero kernel case

Abstract

Schur–Horn theorems focus on determining the diagonal sequences obtainable for an operator under all possible basis changes, formally described as the range of the canonical conditional expectation of its unitary orbit.

Following a brief background survey, we prove an infinite dimensional Schur–Horn theorem for positive compact operators with infinite dimensional kernel, one of the two open cases posed recently by Kaftal–Weiss. There, they characterized the diagonals of operators in the unitary orbits for finite rank or zero kernel positive compact operators. Here we show how the characterization problem depends on the dimension of the kernel when it is finite or infinite dimensional.

We obtain exact majorization characterizations of the range of the canonical conditional expectation of the unitary orbits of positive compact operators with infinite dimensional kernel, unlike the approximate characterizations of Arveson–Kadison, but extending the exact characterizations of Gohberg–Markus and Kaftal–Weiss.

Recent advances in this subject and related subjects like traces on ideals show the relevance of new kinds of sequence majorization as in the work of Kaftal–Weiss (e.g., strong majorization and another majorization similar to what here we call -majorization), and of Kalton–Sukochev (e.g., uniform Hardy–Littlewood majorization), and of Bownik–Jasper (e.g., Riemann and Lebesgue majorization). Likewise key tools here are new kinds of majorization, which we call - and approximate -majorization ().

keywords:

Schur–Horn Theorem , majorization , diagonals , stochastic matricesMSC:

[2010] Primary 26D15 , 47B07 , 47B65 , 15B51 , Secondary 47A10 , 47A12 , 47L071 Introduction

The Schur–Horn Theorem in finite matrix theory characterizes the diagonals of a self-adjoint matrix in terms of its eigenvalues. In particular, if are the eigenvalues of a self-adjoint matrix counting multiplicity, then its diagonal sequence has the following relationship with its eigenvalues:

where are any monotone decreasing rearrangements of . This relationship between the sequences is called majorization and is historically denoted by . Schur proved this diagonal-eigenvalue relationship in [1] and Horn [2] proved the converse. That is, Horn proved that given , there exists a self-adjoint matrix with eigenvalue sequence and diagonal sequence .

To modernize this perspective, let denote a Hilbert space (finite or separable infinite dimensional) and fix an orthonormal basis for (). Denote by the abelian algebra of diagonal operators (the canonical atomic masa of ) corresponding to the basis and the self-adjoint operators in . Given an operator , we denote by the diagonal operator having as its diagonal the main diagonal of (i.e., is the canonical faithful normal trace-preserving conditional expectation). Let be the full unitary group of , and given an operator let denote the orbit of under acting by conjugation . With this notation we can state the classical Schur–Horn Theorem ([2, 1]) in a form which translates naturally to the infinite dimensional case (see for instance Theorems 1.8, 1.9 and Corollary 3.5).

Theorem 1.1 (Classical Schur–Horn Theorem [1, 2]).

Let be a finite dimensional complex Hilbert space and a masa of relative to a fixed basis corresponding to with conditional expectation . Then for any self-adjoint operator ,

where denote the eigenvalue sequences of counting multiplicity.

Since the advent of the Schur–Horn theorem, there has been significant progress towards developing infinite dimensional analogues. This was perhaps started by the work of Markus [3] and Gohberg and Markus [4], but more recently the topic was revived by A. Neumann in [5]. However, Neumann studied an approximate Schur–Horn phenomenon, i.e., the operator-norm closure of the diagonals of bounded self-adjoint operators (equivalently, the -norm closure of the diagonal sequences), which Arveson and Kadison deemed too coarse a closure [6, Introduction paragraph 3]. Instead, they studied the expectation of the trace-norm closure of the unitary orbit of a trace-class operator and then proved Schur–Horn analogues for trace-class operators in (type I∞ factor). They also formulated a Schur–Horn conjecture for type II1 factors, but discussion of this topic is outside the scope of this paper. For work on II1 and II∞ factors, see the work of Argerami and Massey [7, 8, 9], Bhat and Ravichandran [10] and a recent unpublished work Ravichandran [11].

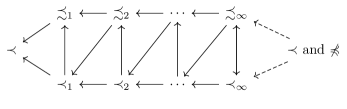

Majorization plays an essential role in Schur–Horn phenomena, but also has given rise to new kinds of majorization inside and outside this arena. The Riemann and Lebesgue majorizations of Bownik–Jasper are applied to Schur–Horn phenomena in [12, 13, 14]. And the uniform Hardy–Littlewood majorization of Kalton–Sukochev [15] is used ubiquitously in Lord–Sukochev–Zanin [16] as an essential tool to study traces and commutators for symmetrically normed ideals. In this paper we also develop new kinds of majorization essential for our work (see introduction Figs. 1 and 2 and accompanying description).

Basic notation for this paper.

For a set , let denote its cardinality. Let denote the cone of nonnegative sequences converging to zero and the cone of nonnegative decreasing sequences converging to zero. For a sequence , let denote the monotonization of , or rather the monotonization of when is not finitely supported. That is, denotes the -th largest element of . Notice that if is finitely supported, then ends in zeros. However, if has infinite support, then has no zeros, and in this case the monotonization reflects neither the zeros of nor their multiplicity.

The following Definition 1.2 agrees with most of the literature, but it is a departure from that of [17] which did not include this equality condition. When they needed an equality-like condition, they used instead the more restrictive Definition 1.3 of strong majorization.

Definition 1.2.

Let . One says that is majorized by , denoted , if for all ,

Definition 1.3 ([17, Definition 1.2]).

Let . One says that is strongly majorized by , denoted , if for all ,

Note that when , so is , and in this -summable case, majorization as defined above in Definition 1.2 is equivalent to strong majorization in Definition 1.3. However, in the nonsummable case, the latter is clearly a stronger constraint than the former. Strong majorization is not an essential tool in the main theorems of this paper, but we thought it important to emphasize the distinction between our definition of majorization and those of Kaftal–Weiss just described above.

The reason for our Definition 1.2 departure from that of Kaftal–Weiss is for convenience, efficiency of notation and unification of cases. This notation allows us to state in a more unified way the results for both trace-class and non trace-class operators simultaneously without splitting the conclusions into cases (compare Theorem 1.7 to the two cases in [17, Corollary 5.4]).

Recent History.

In [17], Kaftal and Weiss provided an exact extension of the Schur–Horn Theorem to positive compact operators, i.e., precise characterizations without taking closures of any kind. That is, in terms of majorization they characterize precisely the expectation of the unitary orbit of strictly positive compact operators and the expectation of the partial isometry orbit for all positive compact operators. And they ask for but leave as an open question a characterization of the expectation of the unitary orbit of positive compact operators with nonzero kernel.

To describe this subject requires some traditional preliminaries. The range projection for operators is the orthogonal projection onto . Thus for a self-adjoint operator , is the projection onto and hence , and in general . Throughout this paper we opt for using and instead of and .

Definition 1.4.

Given an operator , the partial isometry orbit of is the set

Notice this extends to partial isometries the standard notation of unitary orbits .

Stochastic matrices play a central role in this subject due to the following definition and lemma.

Definition 1.5.

A matrix with positive entries is called

-

•

substochastic if its row and column sums are bounded by 1;

-

•

column-stochastic if it is substochastic and its column sums equal 1;

-

•

row-stochastic if it is substochastic and its row sums equal 1;

-

•

doubly stochastic if it is row- and column-stochastic;

-

•

unistochastic if it is the Schur-product of a unitary matrix with its complex conjugate

(the Schur-product of two matrices and is the matrix , that is, it is the entrywise product of ); -

•

orthostochastic if it is the Schur-square of an orthogonal matrix, i.e., unitary with real entries.

And the connection between expectations of orbits and stochastic matrices is:

Lemma 1.6 ([17, Lemmas 2.3, 2.4]).

Let and for any contraction , let for all . Then

| if and only if . |

Furthermore,

-

(i)

is substochastic;

-

(ii)

is an isometry if and only if is column-stochastic;

-

(iii)

is a co-isometry (isometry adjoint) if and only if is row-stochastic;

-

(iv)

is unitary if and only if is unistochastic;

-

(v)

is orthogonal if and only if is orthostochastic.

For completeness we repeat the straightforward short proof.

Proof.

Given , notice that for any ,

Notice now that

| (1.1) |

and similarly

| (1.2) |

Many of the results in [17] are stated and proved in terms of these stochastic matrices. We state here some of their theorems more relevant to this study.

Theorem 1.7 ([17, Corollary 5.4]).

If , then

As an integration of the summable and nonsummable cases, above Theorem 1.7 as stated is an example of the convenience afforded by our definition of majorization in contrast with that of [17, Corollary 5.4], where the summable and nonsummable cases are combined here under the new notation.

Using these tools, Kaftal and Weiss go on to prove an infinite dimensional analogue of the Schur–Horn Theorem for partial isometry orbits. This includes the unitary orbits for strictly positive compact operators (see the next two theorems).

Theorem 1.8 ([17, Proposition 6.4]).

Let . Then

Again, comparing this statement of the theorem with [17, Proposition 6.4], one sees the convenience of defining majorization as in Definition 1.2 as opposed to [17, Definition 1.2].

Focusing on the partial isometry orbit as opposed to the unitary orbit in the above theorem sidesteps the effects of the dimension of the kernel of the operator . In this way, this theorem avoids the difficulties that lie therein. A similar situation appeared in [6] when they studied for positive trace-class operators , which does not involve kernel dimension considerations. In addition, they showed that . More generally, for positive compact, it is elementary to show . Since none of these three objects encodes the dimension of the kernel of and because they coincide for trace-class operators, is a natural substitute for for positive compact operators (outside the trace class) in the context of Schur–Horn theorems.

However, the question of precisely what is for all was only partially answered in [17]. In particular, it was answered when has finite rank or when (that is, when is strictly positive). When has finite rank, (see Theorem 2.4, proof case 1), and so is covered by Theorem 1.8. For the case when , they have

Theorem 1.9 ([17, Proposition 6.6]).

Let with . Then

Our main contribution.

Theorem 1.9 left open the case when has infinite rank and nonzero kernel. We attempt here to close this gap. In particular, we characterize when has infinite dimensional kernel. When has finite dimensional kernel, we give a necessary condition for membership in (which we conjecture is also sufficient), and we give a sufficient condition for membership in (which we know not to be necessary when , see Example 2.6 below which also appears in [17, Proposition 6.10, Example 6.11]). These main results are embodied in Theorems 2.4, 3.4 and Corollary 3.5. Both of these membership conditions involve new kinds of majorization, which here we call -majorization and herein we introduce approximate -majorization (for , Definitions 2.2 and 3.1 below). There is a natural hierarchy of these new types of majorization which the diagram in Figure 1 describes succinctly. All of these implications are natural (see the discussions following Definitions 2.2 and 3.1) except the two corresponding to the dashed arrows, which are handled in Proposition 2.7 and are only applicable when both sequences in question are in . A linear interpretation of the diagram in Figure 1 is presented in Figure 2.

2 -majorization (sufficiency)

A result which was known to Kaftal and Weiss, and almost certainly to others, is a necessary condition for membership in the expectation of the unitary orbit of a positive operator (see [17, Proof of Lemma 6.9]). Namely, the dimensions of the kernels of operators in the range of the expectation of the unitary orbit of a positive operator cannot increase from the dimension of the kernel of the operator itself.

Proposition 2.1.

If and , then for some , and hence also .

Vector proof.

Since , for some unitary , and since , the required trace inequality follows from the inclusion , which itself follows from and

Projection proof.

Since , is the largest projection so that . Since , there is some unitary so that . Notice also that since . Therefore,

Then since is faithful and is positive, it is zero, and thus conjugating by shows . By the maximality of , and therefore

Before we proceed with our analysis, we need to introduce next a concept similar to [17, Definition 6.8(ii)] which here we call -majorization. Roughly speaking, it is majorization along with eventual -expanded majorization. And this led us to the definition below of -majorization which is both new and fruitful.

Definition 2.2.

Given and , we say that is -majorized by , denoted , if and there exists an such that for all , we have the inequality

And -majorization, denoted , means for all .

Note that is precisely the statement that (recall Definition 1.2, which includes equality of the sums). One also observes that if and , then (we use often the special case that -majorization implies -majorization, i.e., majorization). For this reason, for infinitely many is equivalent to for all , in which case we say that is -majorized by and we write .

One should also take note that -majorization is actually strictly stronger than -majorization when . That is, there exist sequences for which but . From the remarks of the previous paragraph, it suffices to exhibit when . To produce such sequences, start with any and define

Even though is not necessarily monotone, it is not difficult to verify that but .

Remark 2.3.

Because , Theorem 1.8 for implies that is a necessary condition for ; Proposition 2.1 shows is another necessary condition for membership in and with majorization is equivalent to membership in when by Theorem 1.9. It was natural in [17] to ask how the role of majorization is impacted by the dimension of these kernels. In particular here we enhance this program by asking, what role, if any, plays in relating membership in to majorization. And when this difference is undefined, is the minimal for which . This is the strategy that guided our program.

The result below appears in [17] as Lemma 6.9 for , the proof of which utilizes orthostochastic matrices. We provide a different proof which instead utilizes expectations of unitary orbits because it leads to a straightforward extension to the case. See Remark 2.5 for when an orthostochastic matrix can be produced to implement the construction. But we do not have a complete characterization for this orthostochasticity case.

Theorem 2.4.

Let , and .

If for some , and ,

then .

Proof.

Without loss of generality we may assume that (i.e., are simultaneously diagonalized) because for every . We may further reduce to the case when via a splitting argument. Because , without loss of generality we can assume . Then with respect to , one has , , , and has zero kernel. Thus once we find a unitary on for which , then satisfies .

Case 1: has finite rank.

In this case , even if is not necessarily self-adjoint. Indeed, the elements of , by Definition 1.4, have the form for some partial isometry for which , so . Then and is also a partial isometry with . But this partial isometry is finite rank since and and hence also are finite rank, and so can be extended to a unitary for which . This shows , and hence equality. That the conclusion of Theorem 2.4 holds in this case is then covered by Theorem 1.8, since , , and since implies .

In the proof of Case 1, we only used the facts that had finite rank and . Although not needed in this case, the other hypotheses hold automatically and for edification we explain why. Even though for some implies , one has the stronger converse: when has finite support, implies for every , i.e., . Indeed, let be the largest index for which has a nonzero value. Then for all , we have

and therefore . Since is arbitrary, . This shows that the second inequality in the hypotheses is satisfied for since its right-hand side is infinite. The first inequality is satisfied since because is finite rank.

Case 2: has infinite rank and (the case).

With the earlier reduction that and using , Case 2 is a direct consequence of Theorem 1.9.

Case 3: has infinite rank and (the most complicated case).

Since , if necessary, by passing to a smaller we may assume , even if (in which case ). Since , one has , and since , one has .

We now employ another splitting. First let denote the basis that diagonalizes , and then assign them different names, that is, let be the collection of ’s such that . Since is diagonalized with respect to the basis the collection forms an orthonormal basis for . Let consist of the remainder of the set , which means is a basis for . Then , where and . Let and then define by

| (2.1) |

Then because of the way in which we chose and and because , if we let and then are

where is the zero sequence and by hypothesis .

The heuristic idea of the proof is the following in descriptive informal language. First construct a sequence which is a sparsely compressed version of but sufficient to retain majorization by , i.e., . Next apply Case 2 to obtain a special unitary for which . Finally, apply another unitary to decompress the diagonal to the diagonal .

Now inductively choose sequences of nonnegative integers and with the following properties:

-

(i)

if ,

(or if ). -

(ii)

For each , whenever , one has

-

(iii)

for each .

For transparency and brevity, we only loosely describe the construction of the pair of sequences and . The construction proceeds in pairs, . We may choose to satisfy property (ii) since and hence because . For this we use the fact that property (ii) is an eventual property in the sense that if it holds for some it holds for any larger . Moreover, because and , has infinitely many strictly decreasing jumps, i.e., for infinitely many one has . If necessary, increase so that it satisfies this condition. Then since , we may choose to satisfy property (iii). To construct the entire pair of sequences, simply iterate this process while simultaneously ensuring , which we can guarantee because property (ii) is an eventual property.

Next since for all , one has for

When , if we set for convenience of notation, then regardless of whether or these inequalities partition

with each and .

Next define the sequence which shifts and alters at one point in each : for each (or for each if , in which case the last interval is ), set

This partition of ensures that is well-defined. Property (iii) guarantees that is monotone decreasing. And property (ii) allows us to conclude that which will follow from equations (2.2)–(2.4). We omit their straightforward natural proofs for the sake of clarity of exposition. Equations (2.2)-(2.3) have natural proofs by induction and (2.4) is merely one case for when .

For all ,

| (2.2) |

and

| (2.3) |

When , the last interval requires separate consideration. That is, if and one has and so

| (2.4) |

It is now simple to prove that using condition (ii) and equations (2.2)–(2.4). Indeed, notice that for , if and since also and , and considering separately the cases and , one has

| (2.5) |

And for , if , one has

| (2.6) |

Finally, if and , one has

| (2.7) |

Recalling that is the disjoint union of for , (2.2–2.4) and (2.5–2.7) imply that for all

Passing to the limit as yields since . Hence .

By Case 2 and our earlier reduction (first paragraph of proof) applied to and , we obtain a unitary of the form for which

Since has this form, for all and one has

Then for all define on given by the unitary matrix

| (2.8) |

where

Then is the compression of to and if one interprets as canonically acting on this same subspace, one computes

| (2.9) |

because

Next let and let be the unitary defined by

From the above computations, one can see that the diagonal operator

for an appropriate permutation of the basis . But conjugation by operators which permute the basis corresponding to , in particular , commutes with , and is unitary, so . ∎

Remark 2.5 (Orthostochasticity).

In the above proof, if was already diagonalized with respect to the basis , then all the unitary operators either are orthogonal with respect to this basis, or can be chosen as such. Indeed, and are orthogonal, and where , coming from Theorem 1.9, can be chosen to be orthogonal by [17, Corollary 6.1, NS(ii′) and S(ii′)]. A consequence of this combined with Lemma 1.6 is that if , and if

then there exists an orthostochastic matrix for which .

Example 2.6 ([17, Proposition 6.10, Example 6.11]).

The following example, in conjunction with Lemma 1.6, will show that the condition is not necessary for and . In particular, the converse of Theorem 2.4 fails for this case, but is true when is either infinite or undefined as proved by Corollary 3.5.

A counterexample is the following. Let where . Let be an orthostochastic matrix with the property that if and only if (so that otherwise and rows and columns sum to one), e.g., [17, Example 6.11]. Then choosing we claim that . One can see this from the calculation

| (2.10) |

where the latter inequality follows since .

This example can be easily extended to create similar orthostochastic examples (e.g., ) for when and , but for with zeros. Then since is orthostochastic, by Lemma 1.6 one has that for some orthogonal matrix with . Therefore -majorization for any is not necessary to characterize .

To verify observe that for sufficiently large , one has

Discussion on majorizations.

The Figures 1–2 at the end of the introduction show the interconnections between various types of majorization. Here through Proposition 2.9 we begin a discussion of some of these interconnections. Next we exhibit a relationship between strong majorization (recall Definition 1.3) and -majorization. As stated, it may seem to apply to summable sequences, but in fact the hypotheses, majorization and not strong majorization, negate that possibility as addressed just after the proof of Proposition 2.7.

Proposition 2.7.

If and , then

Proof.

It suffices to show that if , then the condition implies for every . Indeed, suppose that

Then since one can choose for which for all . Then for all sufficiently large for which both and one has that

Note that Proposition 2.7 applies only to , since if either or is summable, majorization implies both are summable, and in this case majorization and strong majorization are equivalent (see Definition 1.3, succeeding comment). Furthermore, the converse of Proposition 2.7 fails because there exist sequences for which hence also , and yet , as exhibited in the following example.

Example 2.8.

In this exposition so far we have not considered any hands-on examples of -majorization. In refuting this possible converse of Proposition 2.7 we provide one, but first we explain our natural motivation for it.

Motivation. Suppose has . Then there is some basis with respect to which . It is a natural question to ask if there exists some with . The answer is yes by Theorem 2.4, but there is a more straightforward way to see this in this case. Indeed, if we let denote the rotation by acting on the subspace , and , then , where denotes the -ampliation of , i.e., .

Example. Fix any and choose , where -majorization is easily verified (hint: ). Then

From this it follows that

| (2.11) |

From the second inequality in (2.11) it follows that if , then (e.g. for , ). However, the first inequality of (2.11) shows the inverse, that if , then (e.g. for , ). The first example provides the failure of the converse of Proposition 2.7. Moreover one has, for , if and only if .

The previous example shows that for appropriate , there exist which are counterexamples to the converse of Proposition 2.7. However, with more work one can show for every sequence , there is some with and , as the next proposition shows. Though it will not be used later in this paper, we present it here for completeness.

Proposition 2.9.

For every there exists some with and .

Proof.

Without loss of generality, we may assume since the definitions of -majorization and strong majorization depend only on its monotonization .

If , set . By the example preceding this proposition, we have and .

It therefore suffices to assume . For this we adopt the following conventions. Let juxtaposition of finite sequences denote the concatenation of those sequences. Let denote the length of a finite sequence . Let be an abbreviation of and an abbreviation for . Finally, if is a sequence (not necessarily finite) and with , let denote the finite subsequence .

If and , then . To construct we proceed inductively. Let be any positive sequence converging to zero and let . Then let be the smallest positive integer for which . Let be the largest positive integer for which , i.e., and . Then setting

this choice of guarantees that

| (2.12) |

Denote the difference between the lengths of and by

and then exploiting , choose for which . Then one has

| (2.13) |

because, noting that the length of is greater by than , one has

| (2.14) | ||||

Continuing with the induction, suppose that for some as in the previous case we are given a finite decreasing sequence and , with and with the last term of being equal to and satisfying

| (2.15) |

As in the previous case, by an argument identical to that of (2.14), together these (2.15) inequalities imply

| (2.16) |

We then construct an extension of and with satisfying all of the properties in the preceding paragraph for replacing in all instances. The procedure mimics the base case as follows. Let be the smallest integer greater than for which . Along with (2.15) this inequality implies that

Hence letting be the largest positive integer for which

| (2.17) |

one has . And by the maximality of one also has

| (2.18) |

Adding to both sides of (2.17) and (2.18) the -terms from to excluding , one defines as denoted and obtains

| (2.19) |

and

| (2.20) |

So from (2.19)–(2.20) the difference of the (2.20) sums is nonnegative and less than . This shows that , as defined in (2.19), satisfies the first inequalities of (2.15). Note further that is decreasing since and are decreasing and because the last term of is .

As for , and recalling that , set

and hence . Next, since we may choose some satisfying the last inequality of (2.15), for replacing . These facts again imply (2.16) for replacing by an argument identical to (2.14).

By induction, we have constructed with the desired properties (i.e., paragraph containing inequalities (2.15) and (2.16)). Furthermore, by construction each is an extension of the preceding ones. Thus, the infinite sequence given by when is well-defined. Finally it suffices to show that and .

In order to prove it suffices to observe the following two facts. Firstly, if then

| (2.21) |

Secondly, for each , if then

| (2.22) |

because

Indeed, since , these inequalities (2.21) and (2.22) imply for infinitely many , i.e., .

Finally, (2.16) implies since

Operator consequences

The following corollary of Theorem 2.4 and Proposition 2.7 gives a method of ensuring membership in , for . The purpose of this corollary is to provide a more easily computable way to make this determination in special cases. For if one is given sequences , establishing or its negation seems more difficult than verifying , which requires only and the strict positivity of the associated condition.

Corollary 2.10.

Suppose , , , and but , then .

3 Approximate -majorization (necessity)

Theorem 2.4 of the last section shows that if or when undefined we set , then -majorization () is a sufficient condition for membership in , but Example 2.6 shows it is not necessary for . In our quest to characterize in terms of sequence majorization, we introduce a new type of majorization called approximate -majorization, which is a necessary condition for membership in .

Definition 3.1.

Given and , we say that is approximately -majorized by , denoted , if and for every , there exists an such that for all ,

Furthermore, if for infinitely many (equivalently obviously, for all ), this we call approximate -majorization and denote it by .

Remark 3.2.

Notice from the above definition that if is -majorized by , then is trivially approximately -majorized by . However, there is a partial converse with a small loss in that approximate -majorization implies -majorization. That is, if and is approximately -majorized by , then by choosing , from the above display is -majorized by . Combining these two facts yields that if and only if , which is a fact we will exploit later. Furthermore, as we saw in the proof of Theorem 2.4 Case 1, if has only finitely many nonzero terms, then any which is majorized by is -majorized by and so also approximately -majorized by .

Example 3.3.

It is important to note that -majorization is distinct from approximate -majorization. That is, for each we exhibit sequences with but . When , it suffices to consider the sequences and . Elementary calculations verify that (that is, and ), and but . To produce analogous sequences for any , define

Then but , which proves that -majorization and approximate -majorization are distinct. However, it should be noted that these examples were not nearly as easy for us to come by as those for -majorization. In particular the examples immediately preceding Remark 2.3 came naturally, but the single example above took some effort. For further discussion on pairs of sequences but see unifying Remark 3.7.

Our main theorem on necessity for membership in depends on approximate -majorization:

Theorem 3.4.

Suppose and . If

then .

Proof.

Suppose and are as in the hypotheses of this theorem. We may assume that has infinite rank for otherwise the conclusion holds because of Remark 3.2 and Theorem 2.4 proof of Case 1.

We may also assume that . Otherwise, by Proposition 2.1 and therefore . Thus we would need to prove which is equivalent to , and this holds by Theorem 1.8.

Note that since , satisfies . It suffices to show for all with . Because , without loss of generality via unitary equivalence for and permutations for , and the fact that conjugation by a permutation commutes with the expectation , we may assume that

where is interspersed with zeros. (To aid intuition, in case we may choose and hence also .) Since by Lemma 1.6(iv), there exists a unistochastic matrix for which . However, only double stochasticity of is used here. For all one has

| (3.1) |

For a doubly-stochastic matrix , denote the last quantity in equation (3.1) as . It is clear that for fixed , depends solely on the columns of .

Now fix any , and choose for which

| (3.2) |

The existence of follows from column-stochasticity, which yields

Certainly inequality (3.2) holds with replaced by any , since is a doubly stochastic matrix and so its entries are nonnegative.

Consider a permutation matrix which fixes the first coordinates and has the property that

where are the remaining -terms. (To aid intuition, when and we choose and , is already in this form without need of the permutation .) Then notice that is both doubly stochastic and satisfies inequality (3.2) if and only if does the same. Notice also that inequality (3.2) depends only on the first columns of . Then direct computations show

| (3.3) |

Denote the entries of by . From the definition of above it is clear that whenever . This yields an upper bound for when

The inequalities above along with equation (3.3) yield

Since is arbitrary, , and since the positive integer is arbitrary, . ∎

One of our main results is Corollary 3.5 which, in the rather general setting where has infinite rank and infinite dimensional kernel, we obtain a precise characterization of in terms of majorization and -majorization.

Corollary 3.5.

Suppose has infinite rank and infinite dimensional kernel . Then

the members of with finite dimensional kernel and infinite dimensional kernel, respectively, are characterized by

and

Proof.

Corollary 3.5 can be expressed as

This motivates the following conjectured characterization for , which remains an open problem. And if this conjecture should prove false, is there a proper majorization characterization of ?

Conjecture 3.6.

Let . Then

The following remark provides a method for producing pairs of sequences and for which but .

Remark 3.7.

Recall that Example 2.6 provided an orthostochastic matrix such that for every , setting , where , yields . Using Lemma 1.6 one has . By Theorem 3.4,

hence . In general, given two finite sequences, say , of lengths and (where is arbitrary) and having the same sum (i.e., ), one can prepend to and to , clearly obtaining new sequences with but .

Although we did not mention it earlier, in Example 2.6 there is a substantial amount of freedom in choosing . In particular, examination of [17, Example 6.11] ensures that each sum-1 strictly positive column vector followed by a Gram–Schmidt process produces a distinct orthostochastic matrix that can be used in Example 2.6. Perhaps these orthostochastic can be exploited or modified to prove Conjecture 3.6.

4 convexity

Historically, convexity played a central role and is ubiquitous in majorization theory. For example, Horn [2, Theorem 1] integrates theorems of Hardy, Littlewood and Pólya [18] and Birkhoff [19] to prove

where is the set of permutation matrices. For operators, in [2], using [1], Horn proved that is convex whenever by establishing the characterization

where is the eigenvalue sequence of (Theorem 1.1). However, the verification that is convex is immediate from its majorization characterization even without the theorem of Horn integrating Hardy, Littlewood, Pólya and Birkhoff mentioned above. Likewise it is straightforward to verify that if , then

is convex. In particular, this leads to the results of Kaftal and Weiss on the convexity of the expectation of the partial isometry orbit of a positive compact operator.

Theorem 4.1 ([17, Corollary 6.7]).

Let . Then

-

•

is convex.

-

•

If or has finite rank, then is convex.

Since we have a characterization of when has both infinite rank and infinite dimensional kernel, it seems natural to ask if is convex in this case. The answer is positive, however the verification is much less obvious to us (see below Corollary 4.3). But first, a lemma.

Lemma 4.2.

Suppose that , , such that , . If , then .

Proof.

Set . There are two cases: either has finite support, or not. If the former, then since and , one easily has by the comment immediately preceding Theorem 4.1. Then since has finite support, we can improve this to (see Remark 3.2 or proof of Theorem 2.4 Case 1), which is equivalent to . Thus .

The second case: has infinite support. For now, suppose both are finite. Let be a bijection monotonizing : . Since , one has

| (4.1) |

which immediately yields the disjoint union

for each . Therefore , and each term increases to the cardinality of its corresponding set from equation (4.1). From this cardinality equation, it is clear that and are both increasing sequences. However, we may further conclude that they increase without bound. Indeed,

which shows . Likewise . And are both infinitely supported since they are majorized by and is infinitely supported (as shown simply in the proof of Theorem 2.4 Case 2, first paragraph). Thus we have verified . Therefore, given , once is sufficiently large so that and , one has

where . The above computation proves that . But since , either , or eventually . In either case .

Finally, to remove the restriction that be finite, observe that the above proof actually showed that for any , with , one has , where . The proof now splits into several subcases.

If , and , then if one chooses both and , one has for sufficiently large so that .

If , and , then for and any , eventually reaches since . Therefore , which means since was arbitrary.

The cases where and hold by symmetric arguments.

If , then for , one has and so , hence . ∎

Examination of the proof of Lemma 4.2 actually shows that we may replace approximate -majorization with -majorization everywhere in the statement of the lemma and the result remains valid. Indeed, the only difference in the proof is that the terms involving disappear when -majorization is used.

An operator consequence of this is:

Corollary 4.3.

If and , then is convex.

Proof.

Take and . Let and also let be their corresponding diagonal sequences in . If , that follows immediately from Corollary 3.5 and from the fact that convex combinations of elements majorized by are themselves majorized by . However, if , we use the dichotomy of Corollary 3.5 for . Observing that and similarly for , simply notice that either or (so ), in which case by Corollary 3.5. Likewise, or . Thus by Lemma 4.2 one has . And so by Corollary 3.5, . ∎

References

- [1] I. Schur, Über eine klasse von mittelbildungen mit anwendungen auf der determinantentheorie, Sitzungsber. Berliner Mat. Ges. 22 (1923) 9–29.

- [2] A. Horn, Doubly stochastic matrices and the diagonal of a rotation matrix, American Journal of Mathematics 76 (1954) 620–630.

- [3] A. Markus, Eigenvalues and singular values of the sum and product of linear operators, Uspehi Mat. Nauk 19 (4 (118)) (1964) 93–123.

- [4] I. C. Gohberg, A. Markus, Some relations between eigenvalues and matrix elements of linear operators, Mat. Sb. (N.S.) 64 (106) (1964) 481–496.

-

[5]

A. Neumann,

An

infinite dimensional version of the Schur-Horn convexity theorem,

Journal of Functional Analysis 161 (2) (1999) 418–451.

doi:10.1006/jfan.1998.3348.

URL http://www.sciencedirect.com/science/article/pii/S0022123698933481 - [6] W. Arveson, R. V. Kadison, Diagonals of self-adjoint operators, Operator Theory, Operator Algebras, and Applications 414 (2006) 247–263.

- [7] M. Argerami, P. Massey, A Schur-Horn theorem in factors, Indiana Univ. Math. J. 56 (5) (2007) 2051–2059. doi:10.1512/iumj.2007.56.3113.

- [8] M. Argerami, P. Massey, A contractive version of a Schur-Horn theorem in factors, J. Math. Anal. Appl. 337 (1) (2008) 231–238. doi:10.1016/j.jmaa.2007.03.095.

- [9] M. Argerami, P. Massey, Schur-Horn theorems in -factors, Pacific J. Math. 261 (2) (2013) 283–310. doi:10.2140/pjm.2013.261.283.

- [10] B. Bhat, M. Ravichandran, The Schur-Horn theorem for operators with finite spectrum., Proc. Am. Math. Soc. 142 (10) (2014) 3441–3453. doi:10.1090/S0002-9939-2014-12114-9.

- [11] M. Ravichandran, The Schur-Horn Theorem in von Neumann algebras, preprint, arXiv:1209.0909 [math.OA] (September 2012).

- [12] M. Bownik, J. Jasper, The Schur-Horn Theorem for operators with finite spectrum, preprint, arXiv:1302.4757 [math.FA] (February 2013).

- [13] M. Bownik, J. Jasper, The Schur-Horn Theorem for operators with finite spectrum., Trans. Amer. Math. Soc.(to appear).

- [14] J. Jasper, The Schur-Horn theorem for operators with three point spectrum, Journal of Functional Analysis 265 (8) (2013) 1494–1521. doi:10.1016/j.jfa.2013.06.024.

- [15] N. J. Kalton, F. Sukochev, Symmetric norms and spaces of operators., Journal für die Reine und Angewandte Mathematik 621 (2008) 81–121. doi:10.1515/CRELLE.2008.059.

- [16] S. Lord, F. Sukochev, D. Zanin, Singular traces. Theory and applications., Berlin: de Gruyter, 2013.

-

[17]

V. Kaftal, G. Weiss,

An

infinite dimensional Schur-Horn Theorem and majorization theory,

Journal of Functional Analysis 259 (12) (2010) 3115–3162.

doi:10.1016/j.jfa.2010.08.018.

URL http://www.sciencedirect.com/science/article/pii/S0022123610003563 - [18] G. H. Hardy, J. E. Littlewood, G. Pólya, Inequalities. 2nd ed., 1st. paperback ed., 2nd Edition, Cambridge (UK) etc.: Cambridge University Press, 1988.

- [19] G. Birkhoff, Three observations on linear algebra, Univ. Nac. Tucumán. Revista A. 5 (1946) 147–151.