Statistical Decision Making for Optimal Budget Allocation in Crowd Labeling

Abstract

There is an increasing popularity in crowdsourcing data labeling tasks to non-expert workers or annotators recruited through commercial internet services such as Amazon Mechanical Turk. Those crowdsourcing workers need to be paid for each label they provide, while a task requester usually only has a limited amount of budget for data labeling. So it is desirable to have an optimal policy to wisely allocate the budget among workers and data instances which need to label by considering worker reliability and task difficulty such that the quality of the finally aggregated labels can be maximized. We formulate such a budget allocation problem as a Bayesian Markov decision process (MDP) which simultaneously conducts learning and decision making. Under our framework, the optimal allocation policy can be obtained by applying dynamic programming (DP), but DP quickly becomes computationally intractable when the size of the problem increases. To solve this challenge, we propose a computationally efficient approximate policy called optimistic knowledge gradient policy. Experiments on both synthetic and real data show that at the same budget level our policy results in higher quality labels than existing policies.

1 Introduction

In many machine learning applications, data are usually collected without labels. For example, a digital camera does not automatically tag a picture as a portrait or a landscape. A traditional way for data labeling is to hire a small group of experts to provide labels for the entire set of data. However, for large-scale data, such an approach becomes inefficient and very costly. Thanks to the advent of online crowdsourcing services such as Amazon Mechanical Turk, a much more efficient way is to post unlabeled data to a crowdsourcing marketplace, where a big crowd of low-paid workers can be hired instantaneously to perform labeling tasks.

Despite of its high efficiency and immediate availability, crowd labeling raises many new challenges. Since labeling tasks are tedious and workers are usually non-experts, labels generated by the crowd suffer from low quality. As a remedy, most crowdsourcing services resort to labeling redundancy to reduce the labeling noise, which is achieved by collecting multiple labels from different workers for each data instance. In particular, a crowd labeling process can be described as a two phase procedure:

-

1.

Assign unlabeled data to a crowd of workers and each data instance is asked to label multiple times;

-

2.

Aggregate the collected raw labels to infer the true labels.

In principle, more raw labels will lead to a higher chance of recovering the true label. However, each raw label comes with a cost: the requester has to pay workers pre-specified monetary reward for each label they provide, usually, regardless of the label’s correctness. For example, a worker typically earns 10 cents by categorizing a website as porn or not. In practice, the requester has only a limited amount of budget which essentially restricts the total number of raw labels that he/she can collect. This raises a challenging question central in crowd labeling: What is the best way to allocate the budget among data instances and workers so that the overall accuracy of aggregated labels is maximized ?

The most important factors that decide how to allocate the budget are the intrinsic characteristics of data instances and workers: labeling difficulty/ambiguity for each data instance and reliability/quality of each worker. In particular, an instance is less ambiguous if its label can be decided based on the common knowledge and a vast majority of reliable workers will provide the same label for it. In principle, we should avoid spending too much budget on those easy instances since excessive raw labels will not bring much additional information. In contrast, for an ambiguous instance which falls near the boundary of categories, even those reliable workers will still disagree with each other and generate inconsistent labels. For those ambiguous instances, we are facing a challenging decision problem on how much budget that we should spend on them. On one hand, it is worth to collect more labels to boost the accuracy of the aggregate label. On the other hand, since our goal is to maximize the overall labeling accuracy, when the budget is limited, we should simply put those few highly ambiguous instances aside to save budget for labeling less difficult instances. In addition to the ambiguity of data instances, the other important factor is the reliability of each worker and, undoubtedly, it is desirable to assign more instances to those reliable workers. Despite of their importance in deciding how to allocate the budget, both the data ambiguity and workers’ reliability are unknown parameters at the beginning and need to be updated based on the stream of collected raw labels in an online fashion. This further suggests that the budget allocation policy should be dynamic and simultaneously conduct parameter estimation and decision making.

To search for an optimal budget allocation policy, we model the data ambiguity and workers’ reliability using two sets of random variables drawn from known prior distributions. Then, we formulate the problem into a finite-horizon Bayesian Markov Decision Process (MDP) [29], whose state variables are the posterior distributions of these variables, which are updated by each new label. Here, the Bayesian setting is necessary. We will show that an optimal policy only exists in the Bayesian setting. Using the MDP formulation, the optimal budget allocation policy for any finite budget level can be readily obtained via the dynamic programming (DP). However, DP is computationally intractable for large-scale problems since the size of the state space grows exponentially in budget level. The existing widely-used approximate policies, such as approximate Gittins index rule [12] or knowledge gradient (KG) [13, 9], either has a high computational cost or poor performance in our problem. In this paper, we propose a new policy, called optimistic knowledge gradient (Opt-KG). In particular, the Opt-KG policy dynamically chooses the next instance-worker pair based on the optimistic outcome of the marginal improvement on the accuracy, which is a function of state variables. We further propose a more general Opt-KG policy using the conditional value-at-risk measure [32]. The Opt-KG is computationally efficient, achieves superior empirical performance and has some asymptotic theoretical guarantees.

To better present the main idea of our MDP formulation and the Opt-KG policy, we start from the binary labeling task (i.e., providing the category, either positive or negative, for each instance). We first consider the pull marketplace (e.g., Amazon Mechanical Turk or Galaxy Zoo) , where the labeling requester can only post instances to the general worker pool with either anonymous or transient workers, but cannot assign to an identified worker. In a pull marketplace, workers are typically treated as homogeneous and one models the entire worker pool instead of each individual worker. We further assume that workers are fully reliable (or noiseless) such that the chance that they make an error only depend on instances’ own ambiguity. At a first glance, such an assumption may seem oversimplified. In fact, it turns out that the budget-optimal crowd labeling under such an assumption has been highly non-trivial. We formulate this problem into a Bayesian MDP and propose the computational efficient Opt-KG policy. We further prove that the Opt-KG policy in such a setting is asymptotically consistent, that is, when the budget goes to infinity, the accuracy converges to 100% almost surely.

Then, we extend the MDP formulation to deal with push marketplaces with heterogeneous workers. In a push marketplace (e.g., data annotation team in Microsoft Bing group), once an instance is allocated to an identified worker, the worker is required to finish the instance in a short period of time. Based on the previous model for fully reliable workers, we further introduce another set of parameters to characterize workers’ reliability. Then our decision process simultaneously selects the next instance to label and the next worker for labeling the instance according to the optimistic knowledge gradient policy. In fact, the proposed MDP framework is so flexible that we can further extend it to incorporate contextual information of instances whenever they are available (e.g., as in many web search and advertising applications [21]) and to handle multi-class labeling.

In summary, the main contribution of the paper consists of the three folds: (1) we formulate the budget allocation in crowd labeling into a MDP and characterize the optimal policy using DP; (2) computationally, we propose an efficient approximate policy, optimistic knowledge gradient; (3) the proposed MDP framework can be used as a general framework to address various budget allocation problems in crowdsourcing (e.g., rating and ranking tasks).

The rest of this paper is organized as follows. In Section 2, we first present the modeling of budget allocation process for binary labeling tasks with fully reliable workers and motivate our Bayesian modeling. In Section 3, we present the Bayesian MDP and the optimal policy via DP. In Section 4, we propose a computationally efficient approximate policy, Opt-KG. In Section 5, we extend our MDP to model heterogeneous workers with different reliability. In Section 6, we present other important extensions, including incorporating contextual information and multi-class labeling. In Section 7, we discuss the related works. In Section 8, we present numerical results on both simulated and real datasets, followed by conclusions in Section 9.

2 Binary Labeling with Homogeneous Noiseless Workers

We first consider the budget allocation problem in a pull marketplace with homogeneous noiseless workers for binary labeling tasks. We note that such a simplification is important for investigating this problem, since the incorporation of workers’ reliability and extensions to multiple categories become rather straightforward once this problem is correctly modeled (see Section 5 and 6).

Suppose that there are instances and each one is associated with a latent true label for . Our goal is to infer the set of positive instances, denoted by . Here, we assume that the homogeneous worker pool is fully reliable or noiseless. We note that it does not mean that each worker knows the true label . Instead, it means that fully reliable workers will do their best to make judgements but their labels may be still incorrect due to the instance’s ambiguity. Further, we model the labeling difficulty/ambiguity of each instance by a latent soft-label , which can be interpreted as the percentage of workers in the homogeneous noiseless crowd who will label the -th instance as positive. In other words, if we randomly choose a worker from a large crowd of fully reliable workers, we will receive a positive label for the -th instance with probability and a negative label with probability . In general, we assume the crowd is large enough so that the value of can be any value in . To see how characterizes the labeling difficulty of the -th instance, we consider a concrete example where a worker is asked to label a person as adult (positive) or not (negative) based on the photo of that person. If the person is more than 25 years old, most likely, the corresponding will be close to 1, generating positive labels consistently. On the other hand, if the person is younger than 15, she may be labeled as negative by almost all the reliable workers since is close to 0. In both of this cases, we regard the instance (person) easy to label since can be inferred with a high accuracy based on only a few raw labels. On the contrary, for a person is one or two years below or above 18, the is near 0.5 and the numbers of positive and negative labels become relatively comparable so that the corresponding labeling task is very difficult. Given the definition of soft labels, we further make the following assumption:

Assumption 2.1

We assume that the soft-label is consistent with the true label in the sense that if and only if , i.e., the majority of the crowd are correct, and hence .

Given the total budget, denoted by , we suppose that each label costs one unit of budget. As discussed in the introduction, the crowd labeling has two phases. The first phase is the budget allocation phase, which is a dynamic decision process with stages. In each stage , an instance is selected based on the historical labeling results. Once is selected, it will be labeled by a random worker from the homogeneous noiseless worker pool. According to the definition of , the label received, denoted by , will follow the Bernoulli distribution with the parameter :

| (1) |

We note that, at this moment, all workers are assumed to be homogeneous and noiseless so that only depends on but not on which worker provides the label. Therefore, it is suffice for the decision maker (e.g., requester or crowdsourcing service) to select the instance in each stage instead of an instance-worker pair.

The second phase is the label aggregation phase. When the budget is exhausted, the decision maker needs to infer true labels by aggregating all the collected labels. According to Assumption 2.1, it is equivalent to infer the set of positive instances whose . Let be the estimated positive set. The final overall accuracy is measured by , the size of the mutual overlap between and .

Our goal is to determine the optimal allocation policy, , so that overall accuracy is maximized. Here, a natural question to ask is whether the optimal allocation policy exists and what assumptions do we need for the existence of the optimal policy. To answer this question, we provide a concrete example, which motivates our Bayesian modeling.

2.1 Why we need a Bayesian modeling

| Instance 1 () | 1 | 1 | label? |

| Instance 2 () | 1 | label? | |

| Instance 3 () | 1 | label? |

| Current Accuracy | Expected Accuracy | Improvement | |||

|---|---|---|---|---|---|

| 1 | 1 | 1 | 1 | 0 | |

| 0 | 0 | 0 | 0 | 0 | |

| 0.5 | 1 | 0 | |||

| 0.5 | 0 | 1 | |||

| 1 | 1 | 0.5 | |||

| 0 | 0 | 0.5 |

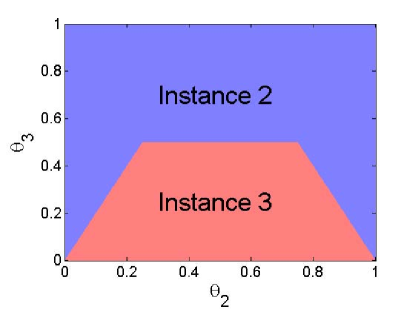

Let us check a toy example with 3 instances and 5 collected labels (see Table 1). We assume that the workers are homogenous noiseless and the label aggregation is performed by the majority vote rule. Now if we only have the budget to get one more label, which instance should be chosen to label? It is obvious that we should not put the remaining budget on the first instance since we are relatively more confident on what its true label should be. Thus, the problem becomes how to choose between the second and third instances. In what follows, we shall show that there is no optimal policy under the frequentist setting. To be more explicit, the optimal policy leads to the expected accuracy which is at least as good as that of all other policies for any values of .

Let us compute the expected improvement in accuracy in terms of the frequentist risk in Table 2. We assume that and if the number of 1 and labels are the same for an instance, the accuracy is 0.5 based on a random guess. From Table 2, we should not label the first instance since the improvement is always 0. This coincides with our intuition. When or , which corresponds to the blue region in Figure 1, we should choose to label the second instance. Otherwise, we should ask the label for the third one. Since the true value of and are unknown, a optimal policy does not exist under the frequentist paradigm. Further, it will be difficult to estimate and accurately when the budget is very limited.

In contrast, in a Bayesian setting with prior distribution on each , the optimal policy is defined as the policy which leads to the highest expected accuracy under the given prior instead of for any possible values of . Therefore, we can optimally determine the next instance to label by taking another expectation over the distribution of . In this paper, we adopt the Bayesian modeling to formulate the budget allocation problem in crowd labeling.

3 Bayesian MDP and Optimal Policy

In this section, we introduce a Bayesian MDP framework and discuss its optimal policy.

3.1 Bayesian Modeling

We assume that each is drawn from a known Beta prior . Beta is a rich family of distributions in the sense that it exhibits a fairly wide variety of shapes on the domain of , i.e., the unit interval . For presentation simplicity, instead of considering a full Bayesian model with hyperpriors on and , we fix and at the beginning. In practice, if the budget is sufficient, one can first label each instance equally many times to pre-estimate before the dynamic labeling procedure is invoked. Otherwise, when there is no prior knowledge, we can simply assume so that the prior is a uniform distribution. According to our simulated experimental results in Section 8.1.2, uniform prior works reasonably well unless the data is highly skewed in terms of class distribution. Other commonly used uninformative priors such as Jeffreys prior or reference prior () or Haldane prior () can also be adopted (see [31] for more on uninformative priors). Choices of prior distributions are discussed in more details in Section 4.2.

At each stage with as the current posterior distribution for , we make a decision by choosing an instance and acquire its label . Here denotes the action set. By the fact that Beta is the conjugate prior of the Bernoulli, the posterior of in the stage will be updated as:

We put into a matrix , called a state matrix, and let be the -th row of . The update of the state matrix can be written in a more compact form:

| (2) |

where is a vector with at the -th entry and 0 at all other entries. As we can see, is a Markovian process because is completely determined by the current state , the action and the obtained label . It is easy to calculate the state transition probability , which is the posterior probability that we are in the next state if we choose to be label in the current state :

| (3) |

Given this labeling process, the budget allocation policy is defined as a sequence of decisions: . Here, we require decisions depend only upon the previous information. To make this more formal, we define a filtration , where is the information collected until the stage . More precisely, is the the -algebra generated by the sample path . We require the action is determined based on the historical labeling results up to the stage , i.e., is -measurable.

3.2 Inference about the True Labels

As described in Section 2, the budget allocation process has two phases: the dynamic budget allocation phase and the label aggregation phase. Since the goal of the dynamic budget allocation in the first phase is to maximize the accuracy of aggregated labels in the second phase, we first present how to infer the true label via label aggregation in the second phase.

When the decision process terminates at the stage , we need to determine a positive set to maximize the conditional expected accuracy conditioning on , which corresponds to minimizing the posterior risk:

| (4) |

where is the indicator function111For example, if and 0 if .. The term inside expectation in (4) is the binary labeling accuracy which can also be written as .

We first observe that, for , the conditional distribution is exactly the posterior distribution , which depends on the historical sampling results only through . Hence, we define

| (5) | |||

| (6) |

As shown in [39], the optimal positive set can be determined by the Bayes decision rule as follows.

Proposition 3.1

solves (4).

The proof of Proposition 3.1 is given in the appendix for completeness.

With Proposition 3.1 in place, we plug the optimal positive set into the right hand side of (4) and the conditional expected accuracy given can be simplified as:

| (7) |

where . We also note that provides not only the estimated label for the -th instance but also how confident the estimated label is correct. According to the next corollary with the proof in the appendix, we show that the optimal is constructed based on a refined majority vote rule which incorporates the prior information.

Corollary 3.2

if and only if and if and only if . Therefore, solves (4).

By viewing and as pseudo-counts of 1s and s at the initial stage, the parameters and are the total counts of 1s and s. The estimated positive set consists of instances with more (or equal) counts of 1s than that of s. When , is constructed exactly according to the vanilla majority vote rule.

To find the optimal allocation policy which maximizes the expected accuracy, we need to solve the following optimization problem:

| (8) |

where represents the expectation taken over the sample paths generated by a policy . The second equality is due to Proposition 3.1 and is called value function at the initial state . The optimal policy is any policy that attains the supremum in (8).

3.3 Markov Decision Process

The optimization problem in (8) is essentially a Bayesian multi-armed bandit (MAB) problem, where each instance corresponds to an arm and the decision is which instance/arm to be sampled next. However, it is different from the classical MAB problem [1, 5], which assumes that each sample of an arm yields independent and identically distributed (i.i.d.) reward according to some unknown distribution associated with that arm. Given the total budget , the goal is to determine a sequential allocation policy so that the collected rewards can be maximized. We contrast this problem with our problem: instead of collecting intermediate independent rewards on the fly, our objective in (8) merely involves the final “reward”, i.e., overall labeling accuracy, which is only available at the final stage when the budget runs out. Although there is no intermediate reward in our problem, we can still decompose the final expected accuracy into sum of stage-wise rewards using the technique from [39], which further leads to our MDP formulation. Since these stage-wise rewards are artificially created, they are no longer i.i.d. for each instance. We also note that the problem in [39] is an infinite-horizon one which optimizes the stopping time while our problem is finite-horizon since the decision process must be stopped at the stage .

Proposition 3.3

Define the stage-wise expected reward as:

| (9) |

then the value function (8) becomes:

| (10) |

where and the optimal policy is any policy that attains the supremum.

The proof of Proposition 3.3 is presented in the appendix. In fact, the stage-wise reward in (9) has a straightforward interpretation. According to (8), the term is the expected accuracy at the -th stage. The stage-wise reward takes the form of the difference between the expected accuracy at the -stage and the -th stage, i.e., the expected gain in accuracy for collecting another label for the -th instance. The second equality in (9) holds simply because: only the -th instance receives the new label and the corresponding changes while all other remain the same. Since the expected reward (9) only depends on , we write

| (11) |

and use them interchangeably. The function with two parameters and has an analytical representation as follows. For any state of a single instance, the reward of getting a label 1 and a label are:

| (12) | ||||

| (13) |

The expected reward takes the following form:

| (14) |

where and are the transition probabilities in (3).

With Proposition 3.3, the maximization problem (8) is formulated as a -stage Markov Decision Process (MDP) as in (10), which is associated with a tuple:

Here, the state space at the stage , , is all possible states that can be reached at . Once we collect a label , one element in (either or ) will add one. Therefore, we have

| (15) |

The action space is the set of instances that could be labeled next: . The transition probability is defined in (3) and the expected reward at each stage is defined in (9).

-

Remark

We can also view Proposition 3.3 as a consequence of applying the reward shaping technique [24] to the original problem (8). In fact, we can add an artificial absorbing state, named , to the original state space (15) and assume that, when the budget allocation process finishes, the state must transit one more time to reach regardless of which action is taken. Hence, the original problem (8) becomes a MDP that generates a zero transition reward until the state enters where the transition reward is . Then, we define a potential-based shaping function [24] over this extended state space as for and . After this, (3.3) can be viewed as a new MDP whose transition reward equals that of (8) plus the shaping-reward function when the state transits from to . According to Theorem 1 in [24], (3.3) and (8) have the same optimal policy. This provides an alternative justification for Proposition 3.3.

3.4 Optimal Policy via DP

With the MDP in place, we can apply the dynamic programming (DP) algorithm (a.k.a. backward induction) [29] to compute the optimal policy:

-

1.

Set for all possible states . The optimal decision is the decision that achieves the maximum when the state is .

-

2.

Iterate for , compute the for all possible using the Bellman equation:

and is the that achieves the maximum.

The optimal policy . For an illustration purpose, we use DP to calculate the optimal instance to be labeled next in the toy example in Section 2.1 under the uniform prior for all . Since we assume that there is only one labeling chance remaining, which corresponds to the last stage of DP, we should choose the instance . According to the calculation in Table 3, there is a unique optimal instance for labeling, which is the second instance.

| Instance | ||||||

|---|---|---|---|---|---|---|

| 1 | (3,1) | |||||

| 2 | (2,2) | |||||

| 3 | (2,1) |

Although DP finds the optimal policy, its computation is intractable since the size of the state space grows exponentially in according to (15). Therefore, we need to develop a computationally efficient approximate policy, which is the goal of the next section.

4 Approximate Policies

Since DP is computationally intractable, approximate policies are needed for large-scale applications. The simplest policy is the uniform sampling (a.k.a, pure exploration), i.e., we choose the next instance uniformly and independently at random: . However, this policy does not explore any structure of the problem.

With the decomposed reward function, our problem is essentially a finite-horizon Bayesian MAB problem. Gittins [12] showed that Gittins index policy is optimal for infinite-horizon MAB with the discounted reward. It has been applied to the infinite-horizon version of problem (10) in [39]. Since our problem is finite-horizon, Gittins index is no longer optimal while it can still provide us a good heuristic index rule. However, the computational cost of Gittins index is very high: the state-of-art-method proposed by [25] requires time and space complexity.

A computationally more attractive policy is the knowledge gradient (KG) [13, 9]. It is essentially a single-step look-ahead policy, which greedily selects the next instance with the largest expected reward:

| (16) |

As we can see, this policy corresponds to the last stage in DP and hence KG policy is optimal if only one labeling chance is remaining.

When there is a tie, if we select the smallest index , the policy is referred to deterministic KG while if we randomly break the tie, the policy is referred to randomized KG. Although KG has been successfully applied to many MDP problems [28], it will fail in our problem as shown in the next proposition with the proof in the appendix.

Proposition 4.1

Assuming that and are positive integers and letting , then the deterministic KG policy will acquire one label for each instance in and then consistently obtain the label for the first instance even if the budget goes to infinity.

According to Proposition 4.1, the deterministic KG is not a consistent policy, where the consistent policy refers to the policy that will provide correct labels for all instances (i.e., ) almost surely when goes to infinity. We note that randomized KG policy can address this problem. However, from the proof of Proposition 4.1, randomized KG behaves similarly to the uniform sampling policy in many cases and its empirical performance is undesirable according to Section 8. In the next subsection, we will propose a new approximate allocation policy based on KG which is a consistent policy with superior empirical performance.

4.1 Optimistic Knowledge Gradient

| (17) |

The stage-wise reward can be viewed as a random variable with a two point distribution, i.e., with the probability of being and the probability of being . The KG policy selects the instance with the largest expected reward. However, it is not consistent.

In this section, we introduce a new index policy called “optimistic knowledge gradient” (Opt-KG) policy. The Opt-KG policy assumes that decision makers are optimistic in the sense that they select the next instance based on the optimistic outcome of the reward. As a simplest version of the Opt-KG policy, for any state , the optimistic outcome of the reward is defined as maximum over the reward of obtaining the label 1, , and the reward of obtaining the label , . Then the optimistic decision maker selects the next instance with the largest as in (17) in Algorithm 1. The overall decision process using the Opt-KG policy is highlighted in Algorithm 1.

In the next theorem, we prove that Opt-KG policy is consistent.

Theorem 4.2

Assuming that and are positive integers, the Opt-KG is a consistent policy, i.e, as goes to infinity, the accuracy will be (i.e., ) almost surely.

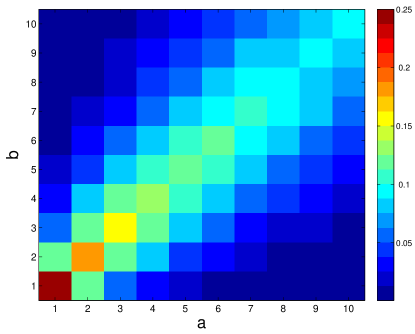

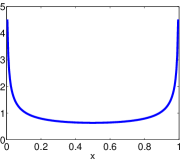

The key of proving the consistency is to show that when goes to infinity, each instance will be labeled infinitely many times. We prove this fact by showing that for any pair of positive integers , and when . As an illustration, the values of are plotted in Figure 2. Then, by strong law of large number, we obtain the consistency of the Opt-KG as stated in Theorem 4.2. The details are presented in the appendix. We have to note that asymptotic consistency is the minimum guarantee for a good policy. However, it does not necessarily guarantee the good empirical performance for the finite budget level. We will use experimental results to show the superior performance of the proposed policy.

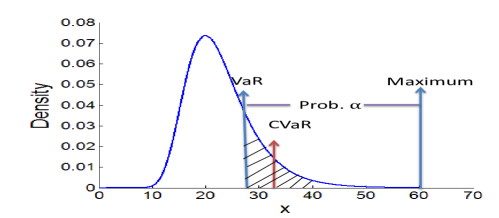

The proposed Opt-KG policy is a general framework for budget allocation in crowd labeling. We can extend the allocation policy based on the maximum over the two possible rewards (Algorithm 1) to a more general policy using the conditional value-at-risk (CVaR) [32]. We note that here, instead of adopting the CVaR as a risk measure, we apply it to the reward distribution. In particular, for a random variable with the support (e.g., the random reward with the two point distribution), let -quantile function be denoted as , where is the CDF of . The value-at-risk is the smallest value such that the probability that is less than (or equal to) it is greater than (or equal to) : . The conditional value-at-risk () is defined as the expected reward exceeding (or equal to) . An illustration of CVaR is shown in Figure 3.

For our problem, according to [32], can be expressed as a simple linear program:

As we can see, when , , which is the expected reward; when , , which is used as the selection criterion in (17) in Algorithm 1. In fact, a more general Opt-KG policy could be selecting the next instance with the largest with a tuning parameter . We can extend Theorem 4.2 to prove that the policy based on is consistent for any . According to our own experience, usually has a better performance in our problem especially when the budget is very limited. Therefore, for the sake of presentation simplicity, we introduce the Opt-KG using (i.e., in ) as the selection criterion.

Finally, we highlight that the Opt-KG policy is computationally very efficient. For instances with units of the budget, the overall time and space complexity are and respectively. It is much more efficient that the Gittins index policy which requires time and space complexity.

4.2 Discussions

It is interesting to see the connection between the idea of making the decision based on the optimistic outcome of the reward and the UCB (upper confidence bounds) policy [1] for the classical multi-armed bandit problem as described in Section 3.3. In particular, the UCB policy selects the next arm with the maximum upper confidence index, which is defined as the current average reward plus the one-sided confidence interval. As we can see, the upper confidence index can be viewed as an “optimistic” estimate of the reward. However, we note that since we are in a Bayesian setting and our stage-wise rewards are artificially created and thus not i.i.d. for each arm, the UCB policy [1] cannot be directly applied to our problem.

In fact, our Opt-KG follows a more general principle of “optimism in the face uncertainty” [35]. Essentially, the non-consistency of KG is due to its nature of pure exploitation while a consistent policy should typically utilizes exploration. One of the common techniques to handle the exploration-exploitation dilemma is to take an action based on an optimistic estimation of the rewards (see [35] and [8] ), which is the role plays in Opt-KG.

For our problem, it is also straightforward to design the “pessimistic knowledge gradient” policy which selects the next instance based on the pessimistic outcome of the reward, i.e.,

However, as shown in the next proposition with the proof in the appendix, the pessimistic KG policy is inconsistent under the uniform prior.

Proposition 4.3

When starting from the uniform prior (i.e., ) for all , the pessimistic KG policy will acquire one label for each instance and then consistently acquire the label for the first instance even if the budget goes to infinity.

Finally, we discuss some other possible choices of prior distributions. For presentation simplicity, we only consider the Beta prior for each with the fixed parameters and . In practice, more complicated priors can be easily incorporated into our framework. For example, in instead of using only one Beta prior, one can adopt a mixture of Beta distributions as the prior and the posterior will also follow a mixture of Beta distributions, which allows an easy inference about the posterior. As we show in the experiments (see Section 8.1.2), the uniform prior does not work well when the data is highly skewed in terms of class distribution. To address this problem, one possible choice is to adopt the prior where and are the weights and is a constant larger than 1 (e.g., ). In such a prior, corresponds to the data with more positive labels while to the data with more negative labels. In addition to the mixture Beta prior, one can adopt the hierarchical Bayesian approach which puts hyper-priors on the parameters in the Beta priors. The inference can be performed using empirical Bayes approach [11, 31]. In particular, one can periodically re-calculate the MAP estimate of the hyper-parameters based on the available data and update the model, but otherwise proceed with the given hyper-parameters. For common choices of hyper-priors of Beta, please refer to Section 5.3 in [11]. These approaches can also be applied to model the workers’ reliability as we introduced in the next Section. For example, one can use a mixture of Beta distributions as the prior for the workers’ reliability, where corresponds to reliable workers, to random workers and to malicious or poorly informed workers.

5 Incorporate Reliability of Heterogeneous Workers

In push crowdsourcing marketplaces, it is important to model workers’ reliability so that the decision maker could assign more instances to reliable workers. Assuming that there are workers in a push marketplace, we can capture the reliability of the -th worker by introducing an extra parameter as in [6, 30, 19], which is defined as the probability of getting the same label as the one from a random fully reliable worker. Recall that the soft-label is the -th instance’s probability of being labeled as positive by a fully reliable worker and let be the label provided by the -th worker for the -th instance. We model the distribution of for given and using the one-coin model [6, 19]222We can further extend it to a more complex two-coin model [6, 30] by introducing a pair of parameters to model the -th worker’s reliability. In particular, and are the probabilities of getting the positive and negative labels when a fully reliable worker provides the same label.:

| (18) | ||||

| (19) |

where denotes the label provided a random fully reliable worker for the -th instance. Here we make the following implicit assumption:

Assumption 5.1

We assume that different workers make independent judgements and, for each single worker, the labels provided by him/her to different instances are also independent.

As the parameter increases from to , the -th worker’s reliability also increases in the sense that gets more and more close to , which is the probability of getting a positive label from a random fully reliable worker. Different types of workers can be easily characterized by . When all , it recovers the previous model with fully reliable workers since , i.e, each worker provides the label only according to the underlying soft-label of the instance. When , we have , which indicates that the -th worker is a spammer, who randomly submits positive or negative labels. When , it indicates that the -th worker is poorly informed or misunderstands the instruction such that he/she always assigns wrong labels.

We assume that instances’ soft-label and workers’ reliability are drawn from known Beta prior distributions: and . At each stage, we need to make the decision on both the next instance to be labeled and the next worker to label the instance (we omit in here for notational simplicity). In other words, the action space . Once the decision is made, the distribution of the outcome is given by (18) and (19). Given the prior distributions and likelihood functions in (18) and (19), the Bayesian Markov Decision process can be formally defined as in Section 3. Similar to the homogeneous worker setting, the optimal inferred positive set takes the form of as in Proposition 3.1 with . The value function still takes the form of (8), which can be further decomposed into the sum of stage-wise rewards in (9) using Proposition 3.3. Unfortunately, in the heterogenous worker setting, the posterior distributions of and are highly correlated with a sophisticated joint distribution, which makes the computation of stage-wise rewards in (9) much more challenging. In particular, given the prior and , the posterior distribution of and given the label takes the following form:

| (20) |

where is the likelihood function defined in (18) and (19) and

As we can see, the posterior distribution no longer takes the form of the product of the distributions of and and the marginal posterior of is no longer a Beta distribution. As a result, does not have a simple representation as in (5), which makes the computation of the reward function much more difficult as the number of stages increases. Therefore, to apply our Opt-KG policy to large-scale applications, we need to use some approximate posterior inference techniques.

| (21) |

When applying Opt-KG, we need to perform inferences of the posterior distribution in total. Each approximate inference should be computed very efficiently, hopefully in a closed-form. For large-scale problems, most traditional approximate inference techniques such as Markov Chain Monte Carlo (MCMC) or variational Bayesian methods (e.g., [3, 27]) may lead to higher computational cost since each inference is an iterative procedure. To address the computational challenge, we apply the variational approximation with the moment matching technique so that each inference of the approximate posterior can be computed in a closed-form. In fact, any highly efficient approximate inference can be utilized to compute the reward function. Since the main focus of the paper is on the MDP model and Opt-KG policy, we omit the discussion for other possible approximate inference techniques. In particular, we first adopt the variational approximation by assuming the conditional independence of and :

We further approximate and by two Beta distributions:

where the parameters , , , are computed using moment matching with the analytical form presented in the appendix. After this approximation, the new posterior distributions of and still have the same structure as their prior distribution, i.e., the product of two Beta distributions, which allows a repeatable use of this approximation every time when a new label is collected. Moreover, due to the Beta distribution approximation of , the reward function takes a similar form as in the previous setting. In particular, assuming at a certain stage, has the posterior distribution and has the posterior distribution . The reward of getting positive and negative labels for the -th instance from the -th worker are presented in (22) and (23):

| (22) | ||||

| (23) |

With the reward in place, we present Opt-KG for budget allocation in the heterogeneous worker setting in Algorithm 2. We also note that due to the variational approximation of the posterior, establishing the consistency results of Opt-KG becomes very challenging in the heterogeneous worker setting.

6 Extensions

Our MDP formulation is a general framework to address many complex settings of dynamic budget allocation problems in crowd labeling. In this section, we briefly discuss two important extensions, where for both extensions, Opt-KG can be directly applied as an approximate policy. We note that for the sake of presentation simplicity, we only present these extensions in the noiseless homogeneous worker setting. Further extensions to the heterogeneous setting are rather straightforward using the technique from Section 5.

6.1 Utilizing Contextual Information

When the contextual information is available for instances, we could easily extend our model to incorporate such an important information. In particular, let the contextual information for the -th instance be represented by a -dimensional feature vector . We could utilize the feature information by assuming a logistic model for :

where is assumed to be drawn from a Gaussian prior . At the -th stage with the current state , the decision maker determines the instance and acquire its label . Then we update the posterior and using the Laplace method as in Bayesian logistic regression [4]. Variational methods can be applied to further accelerate the posterior update [16] . The details are provided in the appendix.

6.2 Multi-Class Categorization

Our MDP formulation can also be extended to deal with multi-class categorization problems, where each instance is a multiple choice question with several possible options (i.e., classes). More formally, in a multi-class setting with different classes, we assume that the -th instance is associated with a probability vector , where is the probability that the -th instance will be labeled as the class by a random fully reliable worker and . We assume that has a Dirichlet prior and the initial state is a matrix with as its -th row. At each stage with the current state , we determine the next instance to be labeled and collect its label , which follows the categorical distribution: . Since the Dirichlet is the conjugate prior of the categorical distribution, the next state induced by the posterior distribution is: and for all . Here is a row vector with one at the -th entry and zeros at all other entries. The transition probability is:

We denote the true set of instances in class by . By a similar argument as in Proposition 3.1, at the final stage , the estimated set of instances belonging to class is

where . We note that if the -th instance belongs to more than one , we only assign it to the one with the smallest index so that forms a partition of . Let and . The expected reward takes the form of:

With the reward function in place, we can formulate the problem into a MDP and use DP to obtain the optimal policy and Opt-KG to compute an approximate policy. The only computational challenge is how to calculate efficiently so that the reward can be evaluated. We present an efficient method in the appendix. We can further use Dirichlet distribution to model workers reliability as in [22]. Using multi-class Bayesian logistic regression, we can also incorporate contextual information into the multi-class setting in a straightforward manner.

7 Related Works

Categorical crowd labeling is one of the most popular tasks in crowdsourcing since it requires less effort of the workers to provide categorical labels than other tasks such as language translations. Most work in categorical crowd labeling are solving a static problem, i.e., inferring true labels and workers’ reliability based on a static labeled dataset [6, 30, 22, 37, 38, 41, 23, 10]. The first work that incorporates diversity of worker reliability is [6], which uses EM to perform the point estimation on both worker reliability and true class labels. Based on that, [30] extended [6] by introducing Beta prior for workers’ reliability and features of instances in the binary setting; and [22] further introduced Dirichlet prior for modeling workers’ reliability in the multi-class setting. Our work utilizes the modeling techniques in these two static models as basic building blocks but extends to dynamic budget allocation settings.

In recent years, there are several works that have been devoted into online learning or budget allocation in crowdsourcing [18, 19, 2, 14, 7, 40, 17, 15]. The method proposed in [19] is based on the one-coin model. In particular, it assigns instances to workers according to a random regular bipartite graph. Although the error rate is proved to achieve the minimax rate, its analysis is asymptotic and method is not optimal when the budget is limited. [18] further extended [19] to the multi-class setting. The new labeling uncertainty method in [15] is one of the state-of-the-art methods for repeated labeling. However, it does not model each worker’s reliability and incorporate it into the allocation process. [14] proposed an online primal dual method for adaptive task assignment and investigated the sample complexity to guarantee that the probability of making an error for each instance is less that a threshold. However, it requires gold samples to estimate workers’ reliability. [17] used MDP to address a different decision problem in crowd labeling, where the decision maker collects labels for each instance one after another and only decides whether to hire an additional worker or not. Basically, it is an optimal stopping problem since there is no pre-fixed amount of budget and one needs to balance the accuracy v.s. the amount of budget. Since the accuracy and the amount of budget are in different metrics, such a balance could be very subjective. Furthermore, the MDP framework in [17] cannot distinguish different workers. To the best of our knowledge, there is no existing method that characterizes the optimal allocation policy for finite . In this work, with the MDP formulation and DP algorithm, we characterize the optimal policy for budget allocation in crowd labeling under any budget level.

We also note that the budget allocation in crowd labeling is fundamentally different from noisy active learning [33, 26]. Active learning usually does not model the variability of labeling difficulties among instances and assumes a single (noisy) oracle; while in crowd labeling, we need to model both instances’ labeling difficulty and different workers’ reliability. Secondly, active learning requires the feature information of instances for the decision, which could be unavailable in crowd labeling. Finally, the goal of the active learning is to label as few instances as possible to learn a good classifier. In contrast, for budget allocation in crowd labeling, the goal is to infer the true labels for as many instances as possible.

In fact, our MDP formulation is essentially a finite-horizon Bayesian multi-armed bandit (MAB) problem. While the infinite-horizon Bayesian MAB has been well-studied and the optimal policy can be computed via Gittins index [12], for finite-horizon Bayesian MAB, the Gittins index rule is only an approximate policy with high computational cost. The proposed Opt-KG and a more general conditional value-at-risk based KG could be general policies for Bayesian MAB. Recently, a Bayesian UCB policy was proposed to address a different Bayesian MAB problem [20]. However, it is not clear how to directly apply the policy to our problem since we are not updating the posterior of the mean of rewards as in [20]. We note that our problem is also related to optimal stopping problem. The main difference is that the optimal stopping problem is infinite-horizon while our problem is finite-horizon and the decision process must stop when the budget is exhausted.

8 Experiments

In this section, we conduct empirical study to show some interesting properties of the proposed Opt-KG policy and compare its performance to other methods. We note that, first, we observe that several commonly used priors such as the uniform prior (), Jeffery prior () and Haldane prior () for instances’ soft-label lead to very similar performance. Therefore, we adopt the uniform prior () unless otherwise specified. Second, for each simulated experiment, we randomly generate 20 different sets of data and report the averaged accuracy. Here, the accuracy is defined as , which is normalized between . The deviations for different methods are similar and quite small and thus omitted for the purpose of better visualization and space-saving.

8.1 Simulated Study

8.1.1 Study on Labeling Frequency

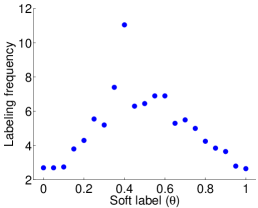

We first investigate that, in the homogeneous noiseless worker setting (i.e., workers are fully reliable), how the total budget is allocated among instances with different levels of ambiguity. In particular, we assume there are instances with soft-labels . We vary the total budget and report the number of times that each instance is labeled on average over 20 independent runs. The results are presented in Figure 4. It can be seen from Figure 4 that, more ambiguous instances with close to 0.5 in general receive more labels than those simple instances with close to 0 or 1. A more interesting observation is that when the budget level is low (e.g., in Figure 4(a)), the policy spends less budget on those very ambiguous instances (e.g., or ), but more budget on exploring less ambiguous instances (e.g., , or ). When the budget goes higher (e.g., in Figure 4(b)), those very ambiguous instances receive more labels but the most ambiguous instance () not necessarily receives the most labels. In fact, the instances with and receive more labels than that of the most ambiguous instance. When the total budget is sufficiently large (e.g., in Figure 4(c)), the most ambiguous instance receives the most labels since all the other instances have received enough labels to infer their true labels.

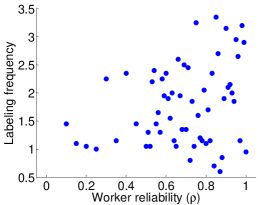

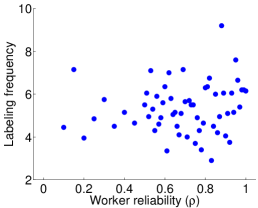

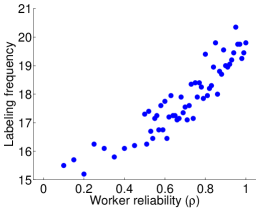

Next, we investigate that, in the heterogeneous worker setting, how many instances each worker is assigned. We simulate instances’ soft-labels as before and further simulate workers’ reliability for workers. Such a simulation ensures that there are more reliable workers, which is in line with actual situation. We vary the total budget and report the number of instances that each worker is assigned on average over 20 independent runs in Figure 5. As one can see, when the budget level goes up, there is clear trend that more reliable workers receive more instances.

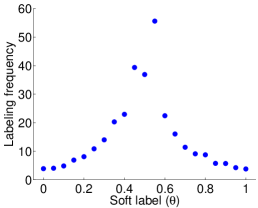

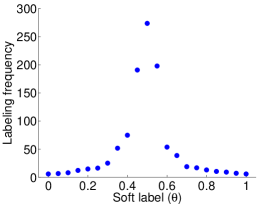

8.1.2 Prior for instances

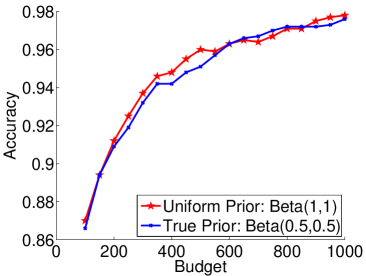

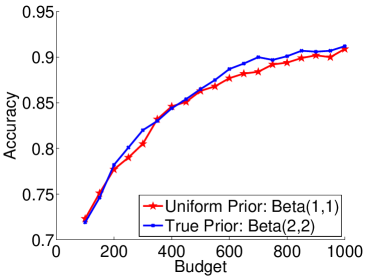

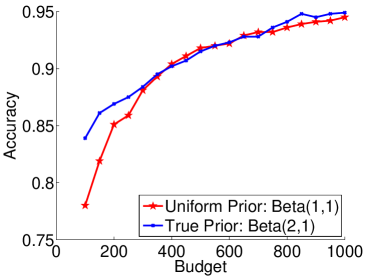

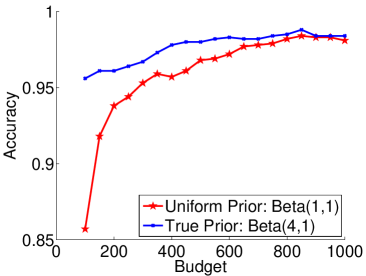

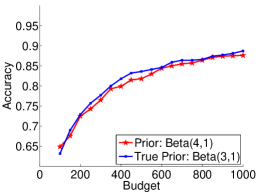

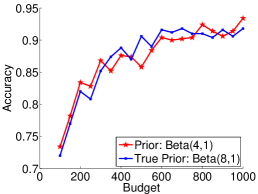

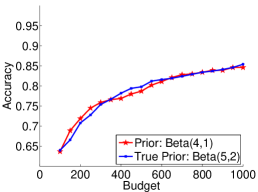

We investigate how robust Opt-KG is when using the uniform prior for each . We first simulate instances with each , , or . The density functions of these four different Beta distributions are plotted in Figure 6. For each generating distribution of , we compare Opt-KG using the uniform prior () (in red line) to Opt-KG with the true generating distribution as the prior (in blue line). The comparison in accuracy with different levels of budget () is shown in Figure 7. As we can see, the performance of Opt-KG using two different priors are quite similar for most generating distributions except for (i.e., the highly imbalanced class distribution). When , the Opt-KG with uniform prior needs at least units of budget to match the performance of Opt-KG with true generating distribution as the prior. This result indicates that for balanced class distributions, the uniform prior is a good choice and robust to the underlying distribution of . For highly imbalanced class distributions, if a uniform prior is adopted, one needs more budget to recover from the inaccurate prior belief.

8.1.3 Prior on workers

We investigate how sensitive the prior for the workers’ reliability is. In particular, we simulate instances with each and workers with , or . We ensure that there are more reliable workers than spammers or poorly informed workers, which is in line with the actual situation. We use the prior , which indicates that we have the prior belief that most workers preform reasonably well and the averaged accuracy is . In Figure 8, we show different density functions for generating and the prior that we use (in Figure 8 (d)). For each generating distribution of , we compare the Opt-KG policy using the prior () (in red line) to the Opt-KG with the true generating distribution as the prior (in blue line). The comparison in accuracy with different levels of budget () is shown in Figure 9. From Figure 9, we observe that the performance of Opt-KG using two different priors are quite similar in all different settings. Hence, we will use as the prior when the true prior of workers is unavailable.

8.1.4 Performance comparison under the homogeneous noiseless worker setting

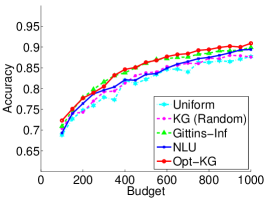

We compare the performance of Opt-KG under the homogeneous noiseless worker setting to several other competitors, including

-

1.

Uniform: Uniform sampling.

-

2.

KG(Random): Randomized knowledge gradient [9].

-

3.

Gittins-Inf: A Gittins-indexed based policy proposed in [39] for solving an infinite-horizon Bayesian MAB problem where the reward is discounted by . Although it solves a different problem, we apply it as a heuristic by choosing the discount factor such that .

-

4.

NLU: The “new labeling uncertainty” method proposed in [15].

We note that we do not compare to the finite-horizon Gittins index rule [25] since its computation is very expensive. On some small-scale problems, we observe that the finite-horizon Gittins index rule [25] has the similar performance as Gittins-Inf in [39].

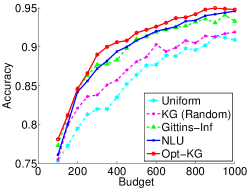

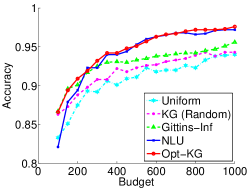

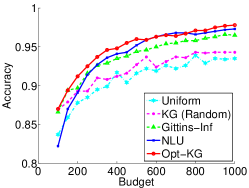

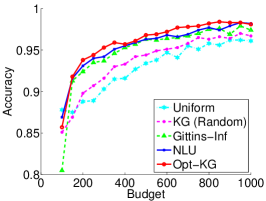

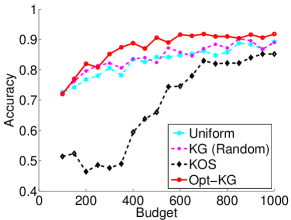

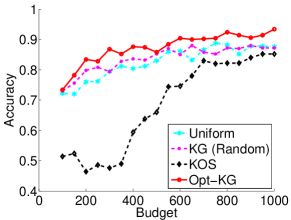

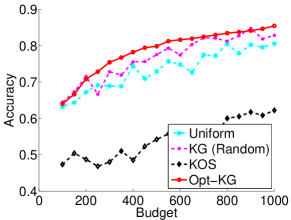

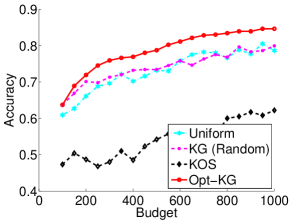

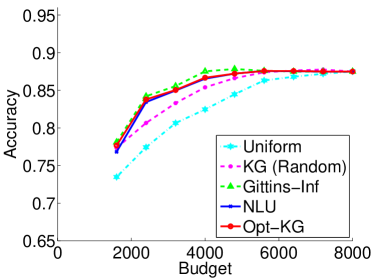

We simulate instances with each , , , or (see Figure 6). For each of the five settings, we vary the total budget and report the mean of accuracy for 20 independently generated sets of . For the last four settings, we report the comparison among different methods when either using the uniform prior (“uni prior” for short) or the true generating distribution as the prior. From Figure 10, the proposed Opt-KG outperforms all the other competitors in most settings regardless the choice of the prior. For , NLU matches the performance of Opt-KG; and for , Gittins-inf matches the performance of Opt-KG. We also observe that the performance of randomized KG only slightly improves that of uniform sampling.

8.1.5 Performance comparison under the heterogeneous worker setting

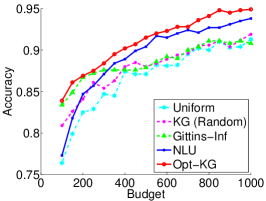

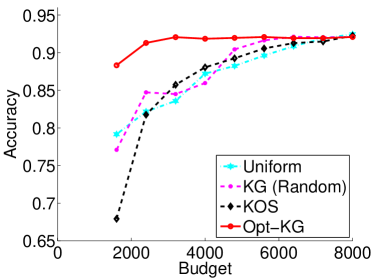

We compare the proposed Opt-KG under the heterogeneous worker setting to several other competitors:

We note that several competitors for the homogeneous worker setting (e.g., Gittins-inf and NLU) cannot be directly applied to the heterogeneous worker setting since they fail to model each worker’s reliability.

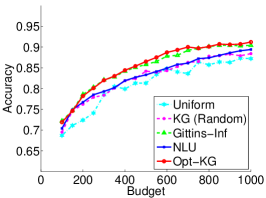

We simulate instances with each and workers with , , or (see Figure 8). For each of the four settings, we vary the total budget and report the mean of accuracy for 20 independently generated sets of parameters. For the last three settings, we report the comparison among different methods when either using prior or the true generating distribution for as the prior. From Figure 11, the proposed Opt-KG outperforms all the other competitors regardless the choice of the prior.

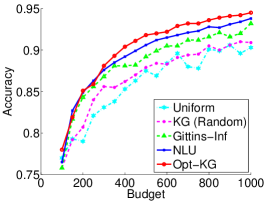

8.2 Real Data

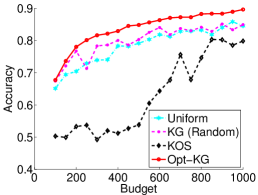

We compare different policies on a standard real dataset for recognizing textual entailment (RTE) (Section 4.3 in [34]). There are 800 instances and each instance is a sentence pair. Each sentence pair is presented to 10 different workers to acquire binary choices of whether the second hypothesis sentence can be inferred from the first one. There are in total 164 different workers. We first consider the homogeneous noiseless setting without incorporating the diversity of workers and use the uniform prior () for each . In such a setting, once we decide to label an instance, we randomly choose a worker (who provides the label in the full dataset) to acquire the label. Due to this randomness, we run each policy 20 times and report the mean of the accuracy in Figure 12(a). As we can see, Opt-KG, Gittins-inf and NLU all perform quite well. We also note that although Gittins-inf performs slightly better than our method on this data, it requires solving a linear system with variables at each stage, which could be too expensive for large-scale applications. While our Opt-KG policy has a time complexity linear in and space complexity linear in , which is much more efficient when a quick online decision is required. In particular, we present the comparison between Opt-KG and Gittins-inf on the averaged CPU time under different budget levels in Table 4. As one can see, Gittins-inf is computationally more expensive than Opt-KG.

| Budget | ||||

|---|---|---|---|---|

| Opt-KG | 1.09 | 2.19 | 3.29 | 5.48 |

| Gittins-inf | 25.87 | 35.70 | 45.59 | 130.68 |

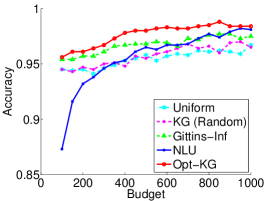

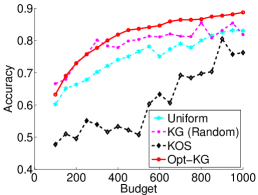

When the worker reliability is incorporated, we compare different policies in Figure 12(b). We put prior distribution for each which indicates that we have the prior belief that most workers perform reasonably well. Other priors in Figure 8 lead to similar results and thus omitted here. As one can see, the accuracy of Opt-KG is much higher than that of other policies when is small. It achieves the highest accuracy of only using 40% of the total budget (i.e., on average, each instance is labeled 4 times). One may also observe that when , the performance of Opt-KG does not improve and in fact, slightly downgrades a little bit. This is mainly due to the restrictiveness of the experimental setting. In particular, since the experiment is conducted on a fixed dataset with partially observed labels, the Opt-KG cannot freely choose instance-worker pairs especially when the budget goes up (i.e., the action set is greatly restricted). According to our experience, such a phenomenon will not happen on experiments when labels can be obtained from any instance-worker pair. Comparing Figure 12(b) to 12(a), we also observe that Opt-KG under the heterogeneous worker setting performs much better than Opt-KG under the homogeneous worker setting, which indicates that it is beneficial to incorporate workers’ reliability.

9 Conclusions and Future Works

In this paper, we propose to address the problem of budget allocation in crowd labeling. We model the problem using the Bayesian Markov decision process and characterize the optimal policy using the dynamic programming. We further propose a computationally more attractive approximate policy: optimistic knowledge gradient. Our MDP formulation is a general framework, which can be applied to binary or multi-class, contextual or non-contextual crowd labeling problems in either pull or push crowdsourcing marketplaces.

There are several possible future directions for this work. First, it is of great interest to show the consistency of Opt-KG in heterogonous worker setting and further provide the theoretical results on the performance of Opt-KG under finite budget. Second, in this work, we assume that both instances and workers are equally priced. Although this assumption is standard in many crowd labeling applications, a dynamic pricing strategy as the allocation process proceeds will better motivate those more reliable workers to label more challenge instances. A recent work in [36] provides some quality-based pricing algorithms for crowd workers and it will be interesting to incorporate their strategies into our dynamic allocation framework. Third, we assume that the labels provided by the same worker to different instances are independent. It is more interesting to consider that the workers’ reliability will be improved during the labeling process when some useful feedback can be provided. Further, since the proposed Opt-KG is a fairly general approximate policy for MDP, it is also interesting to apply it to other statistical decision problems.

10 Acknowledgement

We would like to thank Qiang Liu for sharing the code for KOS method; Jing Xie and Peter Frazier for sharing their code for computing infinite-horizon Gittins index; John Platt, Chris J.C. Burges and Kevin P. Murphy for helpful discussions; and anonymous reviewers and the associate editor for their constructive comments on improving the quality of the paper.

Appendix

Proof of Proposition 3.1

The final positive set is chosen to maximize the expected accuracy conditioned on :

| (24) |

| (25) |

To maximize (25) over , it easy to see that we should set if and only if . Therefore, we have the positive set

Proof of Corollary 3.2

Recall that

| (26) |

where is the beta function.

It is easy to see that . We re-write as follows

where the second equality is obtained by setting . Then we have:

Since , . When , and hence , i.e, . When , and . When , and .

Proof of Proposition 3.3

We use the proof technique in [39] to prove Proposition 3.3. According to (8), the value function takes the following form,

| (27) |

To decompose the final accuracy into the incremental reward at each stage, we define and . Then, can be decomposed as: . The value function can now be re-written as follows:

Here, the first inequality is true because is determinant and independent of ; the second inequality is due to the tower property of conditional expectation and the third one holds because , which is a function of and , depends on only through and . We define incremental expected reward gained by labeling the -th instance at the state as follows:

| (28) | |||||

The last equation is due to the fact that only will be changed if the -th instance is labeled next. With the expected reward function in place, the value function in (8) can be re-formulated as:

| (29) |

Proof of Proposition 4.1

To prove the failure of deterministic KG, we first show a key property for the expected reward function:

| (30) |

Lemma .1

When are positive integers, if , and if , .

To prove lemma .1, we first present several basic properties for and , which will be used in all the following theorems and proofs.

-

1.

Properties for :

(31) (32) (33) -

2.

Properties for :

(34) (35) (36) The properties for are derived from the basic property of regularized incomplete beta function 333http://dlmf.nist.gov/8.17.

- Proof of Lemma .1

When , by Corollary 3.2, we have , and . Therefore, the expected reward (30) takes the following form:

When , since are integers, we have and hence according to Corollary 3.2. The expected reward (30) now becomes:

When , we can prove in a similar way.

With Lemma .1 in place, the proof for Proposition 4.1 is straightforward. Recall that the deterministic KG policy chooses the next instance according to

and breaks the tie by selecting the one with the smallest index. Since if and only if , at the initial stage , for those instances . The policy will first select with the largest . After obtaining the label , either or will add one and hence and . The policy will select another instance with the “current” largest expected reward and the expected reward for after obtaining the label will then become zero. As a consequence, the KG policy will label each instance in for the first stages and for all . Then the deterministic policy will break the tie selecting the first instance to label. From now on, for any , if , then the expected reward . Since the expected reward for other instances are all zero, the policy will still label the first instance. On the other hand, if , and the first instance is the only one with the positive expected reward and the policy will label it. Thus Proposition 4.1 is proved.

-

Remark

For randomized KG, after getting one label for each instance in for the first stages, the expected reward for each instance has become zero. Then randomized KG will uniformly select one instance to label. At any stage , if there exists one instance (at most one instance) with , the KG policy will provide the next label for ; otherwise, it will randomly select an instance to label.

Proof of Theorem 4.2

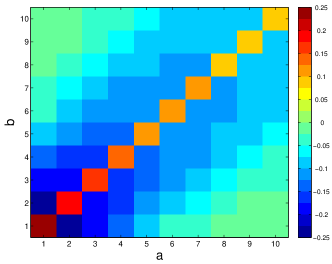

To prove the consistency of the Opt-KG policy, we first show the exact values for .

-

1.

When :

Therefore,

-

2.

When :

Therefore, we have and

-

3.

When :

Therefore

We note that the values of for different are plotted in Figure 2 in main text.

As we can see for any positive integers , we first prove that

| (37) |

in the following Lemma.

Lemma .2

Properties for :

-

1.

is symmetric, i.e., .

-

2.

.

-

3.

For any fixed , is monotonically decreasing in for .

-

4.

When , for any fixed , is monotonically decreasing in . By the symmetry of , when , for any fixed , is monotonically decreasing in .

By the above four properties, we have .

- Proof of Lemma .2

We first prove these four properties.

-

–

Property 1: By the fact that , the symmetry of is straightforward.

-

–

Property 2: For , and hence is monotonically decreasing in . Moreover,

Since and , .

-

–

Property 3: For any ,

-

–

Property 4: When , for any fixed :

According to the third property, when is an even number, we have . According to the fourth property, when is an odd number and , we have ; while when is an odd number and , we have . Therefore,

According to the second property such that , we obtain (37).

Using Lemma .2, we first show that, in any sample path, the Opt-KG will label each instance infinitely many times as goes to infinity. Let be a random variable representing the number of times that the -th instance has been labeled until the stage using Opt-KG. Given a sample path , let be the set of instances that has been labeled only finite number of times as goes to infinity in this sample path. We need to prove that is an empty set for any . We prove it by contradiction. Assuming that is not empty, then after a certain stage , instances in will never be labeled. By Lemma .2, for any , . Therefore, there will exist such that:

Then according to the Opt-KG policy, the next instance to be labeled must be in , which leads to the contradiction. Therefore, will be an empty set for any .

Let be the random variable which takes the value if the -th label of the -th instance is 1 and the value if the -th label is 0. It is easy to see that . Hence, , are independent and identically distributed random variables. By the fact that in all sample paths and using the strong law of large number, we conclude that, conditioning on , , the conditional probability of

for all , is one. According to Proposition 3.1, we have and . The accuracy is We have:

whenever for all . The last inequality is due to the fact that, as long as is not in any , any sample path that gives the event also gives the event , which further implies .

Finally, we have:

where the second equality is because is a zero measure set.

Proof of Proposition 4.3

Recall that our random reward is a two-point distribution with the probability of being and of being . The pessimistic KG selects the next instance which maximizes . To show that the policy is inconsistent, we first compute the exact values for for positive integers .

Utilizing Corollary 3.2 and the basic properties of in (34), (35), (36), we have:

-

1.

When :

Therefore,

-

2.

When :

Therefore, we have and

-

3.

When :

Therefore

We summarize the properties of in the next Lemma.

Lemma .3

Properties for :

-

1.

if and only if .

-

2.

is symmetric, i.e.,

-

3.

When , then is monotonically increasing in . By the symmetry of , when , is monotonically increasing in .

-

4.

When , for any fixed , is monotonically increasing in . By the symmetry of , when , for any fixed , is monotonically increasing in .

For better visualization, we plot values of for different in Figure 13. All the properties in Lemma .3 can be seen clearly from Figure 13. The proof of these properties are based on simple algebra and thus omitted here.

From Lemma .3, we can conclude that for any positive integers with :

| (38) |

Recall that the pessimistic KG selects:

When starting from the uniform prior with for all , the corresponding . After obtaining a label for any instance , the Beta parameters for will become either or with . Therefore, for the first stages, the pessimistic KG policy will acquire the label for each instance once. For any instance , we have either or at the stage . Then the pessimistic KG policy will select the first instance to label. According to (38), for any , . Therefore, the pessimistic KG policy will consistently acquire the label for the first instance. Since the tie will only appear at the stage , the randomized pessimistic KG will also consistently select a single instance to label after stages.

Incorporate Reliability of Heterogeneous Workers

As we discussed in Section 5 in main text, we approximate the posterior so that at any stage for all , and will follow Beta distributions. In particular, assuming at the current state and , the posterior distribution conditioned on takes the following form:

where the likelihood for is defined in (18) and (19), i.e.,

Also,

The posterior distributions no longer takes the form of the product of Beta distributions on and . Therefore, we use variational approximation by first assuming the conditional independence of and :

In fact, the exact form of marginal distributions can be calculated as follows:

To approximate the marginal distribution as Beta distribution, we use the moment matching technique. In particular, we approximate such that

| (39) | ||||

| (40) |

where and are the first and second order moment of . To make (39) and (40) hold, we have:

| (41) | ||||

| (42) |

Similarly, we approximate , such that

| (43) | ||||

| (44) |

where and are the first and second order moment of . To make (39) and (40) hold, we have:

| (45) | ||||

| (46) |

Furthermore, we can compute the exact values for , , and as follows.

Assuming that at a certain stage, follows a Beta posterior and follows a Beta posterior , the reward of getting positive and negative labels for the -th instance from the -th worker are:

| (47) | ||||

| (48) |

where and are defined in (41) and (42), which further depend on and through and . With the reward in place, we can directly apply the Opt-KG policy in the heterogeneous worker setting.

Extensions

Utilizing Contextual Information

When each instance is associated with a -dimensional feature vector , we incorporate the feature information in our budget allocation problem by assuming:

| (49) |

where is the sigmoid function and is assumed to be drawn from a Gaussian prior . At the -th stage with the state and , the decision maker chooses the -th instance to be labeled and observes the label . The posterior distribution has the following log-likelihood:

where is the precision matrix. To approximate by a Gaussian distribution , we use the Laplace method (see Chapter 4.4 in [4]). In particular, the mean of the posterior Gaussian is the MAP (maximum a posteriori) estimator of :

| (50) |

which can be computed by any numerical optimization method (e.g., Newton’s method). The precision matrix takes the following form,

By Sherman-Morrison formula, the covariance matrix can be computed as,

We also calculate the transition probability of and using the technique from Bayesian logistic regression (see Chapter 4.5 in [4]):

where and and .

To calculate the reward function, in addition to the transition probability, we also need to compute:

where is the Dirac delta function. Let

Since the marginal of a Gaussian distribution is still a Gaussian, is a univariate-Gaussian distribution with the mean and variance:

Therefore, we have:

| (51) |

where is the CDF of the standard Gaussian distribution.

With and transition probability in place, the expected reward in value function takes the following form :

| (52) |

We note that since will affect all , the summation from 1 to in (52) can not be omitted and hence (52) cannot be written as in (28). In this problem, KG or Opt-KG need to solve optimization problems to compute the mean of the posterior as in (50), which could be computationally quite expensive. One possibility to address this problem is to use the variational Bayesian logistic regression [16], which could lead to a faster optimization procedure.

Multi-Class Categorization

Given the model and notations introduced in Section 6.2, at the final stage when all budget is used up, we construct the set for each class to maximize the conditional expected classification accuracy:

| (53) |

Here, is the true set of instances in the class . The set consists of instances that belong to class . Therefore, should form a partition of all instances . Let

| (54) |

To maximize the right hand side of (53), we have

| (55) |

If there is belongs to more than one , we only assign it to the one with the smallest index . The maximum conditional expected accuracy takes the form:

Then the value function can be defined as:

where and Following Proposition 3.3, let and , we define incremental reward function at each stage:

The value function can be re-written as:

where . Since the reward function only depends on , we can define the reward function in a more explicit way by defining:

Here be a row vector of length with one at the -th entry and zeros at all other entries; and where

| (56) |

Therefore, we have .

To evaluate the reward , the major bottleneck is how to compute efficiently. Directly taking the -dimensional integration on the region will be computationally very expensive, where denotes the -dimensional simplex. Therefore, we propose a method to convert the computation of into a one-dimensional integration. It is known that to generate , it is equivalent to generate with and let . Then will follow . Therefore, we have:

| (57) |

It is easy to see that

| (58) | ||||

where is the density function of Gamma distribution with the parameter and is the CDF of Gamma distribution at with the parameter . In many softwares, can be calculated very efficiently without an explicit integration. Therefore, we can evaluate by performing only a one-dimensional numerical integration as in (58). We could also use Monte-Carlo approximation to further accelerate the computation in (58).

References

- [1] P. Auer, N. Cesa-Bianchi, and P. Fischer. Finite-time analysis of the multiarmed bandit problem. Machine Learning, 47:235–256, 2002.

- [2] Y. Bachrach, T. Minka, J. Guiver, and T. Graepel. How to grade a test without knowing the answers - a Bayesian graphical model for adaptive crowdsourcing and aptitude testing. In ICML, 2012.

- [3] M. J. Beal. Variational Algorithms for Approximate Bayesian Inference. PhD thesis, Gatsby Computational Neuroscience Unit, University College London, 2003.

- [4] C. M. Bishop. Pattern Recognition and Machine Learning. Springer, 2007.

- [5] S. Bubeck and N. Cesa-Bianchi. Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Foundations and Trends in Machine Learning, 5(1):1–122, 2012.

- [6] A. P. Dawid and A. M. Skene. Maximum likelihood estimation of observer error-rates using the EM algorithm. Journal of the Royal Statistical Society Series C, 28:20–28, 1979.

- [7] S. Ertekin, H. Hirsh, and C. Rudin. Wisely using a budget for crowdsourcing. Technical report, MIT, 2012.

- [8] E. Even-Dar and Y. Mansour. Convergence of optimistic and incremental Q-learning. In NIPS, 2001.

- [9] P. Frazier, W. B. Powell, and S. Dayanik. A knowledge-gradient policy for sequential information collection. SIAM J. Control Optim., 47(5):2410–2439, 2008.

- [10] C. Gao and D. Zhou. Minimax optimal convergence rates for estimating ground truth from crowdsourced labels. arXiv:1310.5764, 2013.

- [11] A. Gelman, J. B. Carlin, H. S. Stern, D. B. Dunson, A. Vehtari, and D. B. Rubin. Bayesian Data Analysis. Chapman and Hall, 3rd edition, 2013.

- [12] J. C. Gittins. Multi-armed Bandit Allocation Indices. John Wiley & Sons, 1989.

- [13] S. S. Gupta and K. J. Miescke. Bayesian look ahead one stage sampling allocations for selection the largest normal mean. J. of Stat. Planning and Inference, 54(2):229–244, 1996.

- [14] C. Ho, S. Jabbari, and J. W. Vaughan. Adaptive task assignment for crowdsourced classification. In ICML, 2013.

- [15] P. G. Ipeirotis, F. Provost, V. S. Sheng, and J. Wang. Repeated labeling using multiple noisy label. Data Mining and Knowledge Discovery, 2013.