Joint densities of first hitting times of a

diffusion process through two time dependent boundaries

Abstract

Consider a one dimensional diffusion process on the diffusion interval originated in . Let and be two continuous functions of , with bounded derivatives and with and , . We study the joint distribution of the two random variables and , first hitting times of the diffusion process through the two boundaries and , respectively. We express the joint distribution of in terms of and and we determine a system of integral equations verified by these last probabilities. We propose a numerical algorithm to solve this system and we prove its convergence properties. Examples and modeling motivation for this study are also discussed.

keywords:

First-hitting time; diffusion process; Brownian motion; Ornstein Uhlenbeck process; copula.L. Sacerdote, O. Telve and C. Zucca

[Department of Mathematics “G. Peano”, University of Torino]

Laura Sacerdote

Ottavia Telve

Cristina Zucca \addressoneDepartment of Mathematics “G. Peano”, University of Torino, Via Carlo Alberto 10, 10123 Torino, Italy

60J60, 60G4060J70, 65R20.

1 Introduction

Exit times of diffusion processes from a strip play an important role in a variety of application ranging from computer science to engineering, from biology to metrology or finance (cf. [2, 13, 25, 28, 37]). According to the features of the model, constant or time dependent thresholds may bound the considered process. Typical examples are quality models with two tolerance bands. Some parameter may control exit times from the strip, with different effects on the exit time from the upper or the lower bound. The knowledge of the joint exit times pdf clarifies the role of these parameters. Another example is given by the survival probability of a population in a finite capacity environment or by tumor growth models (cf. [2]). Similar problems arise in metrology when we need to maintain the atomic clock error bounded by two tolerance bands. Moreover, avoiding an excessive increase of the error is of primary importance to improve GPS instruments (cf. [14]). In this setting the knowledge of the relationship between exit times from the upper and the lower boundary may suggest improvements to the clock reliability by acting on some parameters of the model involved in the joint distribution. Other possible applications can be found in finance where the interest focuses on the dependency between the times to sell or buy options when the level of gain or loss is preassigned. A large literature exists for the study of the first passage time of one dimensional diffusion processes through a boundary and analytical, numerical and simulation methods have been studied both for the direct (cf. [10, 7, 17, 18, 19, 29]) and the inverse problem (cf. [41]). However, most of these papers focuses on the one boundary problem, while for the two boundary case the few analytical results published rely either on the Brownian motion (cf. [27]) or particular time dependent boundaries, corresponding to special symmetries, for specific diffusions (cf. [9, 12]). The existing results generally focus on the first exit time from the strip, while our interest lies in the joint distribution of the times when the process first attains the upper and the lower boundary, respectively. This paper aims to cover this subject considering the joint distribution between these times. Some results, presented in a recent paper [15], are related with those on the Laplace transforms presented in this paper. However their focus is not the joint distribution of exit times from a strip.

The notation and the existing results that will be used in this paper are introduced in Section 2, while Sections 3 and 4 are devoted to the presentation of our results. In Section 3 we determine the expression of the joint distribution of the exit times from the upper and the lower boundary. The results are expressed in terms of first hitting time through a single boundary and of the probability of crossing the upper (lower) boundary for the first time at some instant preceding before crossing the lower (upper) boundary. Note that these probabilities are generally unknown. We prove then that they are the unique solution of a system of Volterra integral equations of the first kind. We also show that there exists an equivalent system of Volterra equations of the second type. When the boundaries are constant the Laplace transform method can be applied to solve the system, since the integrals of such system are of convolution type. Here we introduce three equivalent representations of the Laplace transform. In the case of the Brownian motion and constant boundaries a closed form expression for the joint distribution of the exit times from a strip is known (cf. [8]).

In Section 4 we propose a numerical scheme for the solution of the system of integral equations and we determine the order of convergence. This method works for both constant and time dependent boundaries. In the case of two constant boundaries the Laplace transforms (cf. [1]) of the probability of crossing the upper (lower) boundary for the first time at some instant preceding before crossing the lower (upper) boundary can be numerically inverted. Finally in Section 5, we present a set of examples.

2 Mathematical Background and Notations

Let be a one-dimensional regular time homogeneous diffusion process defined on a suitable probability space such that and with diffusion interval , where is an interval of the form , , or where and/or are admissible when the diffusion interval is open. If not specified, the diffusion interval is open and the endpoints and are natural boundaries. Let be the transition probability distribution function (pDf) of the process and let be the corresponding transition probability density function (pdf).

Let be a continuous functions with bounded derivatives. We denote as the first hitting time of the stochastic process across a boundary

| (1) |

Its pDf is

| (2) |

and is the corresponding pdf. In the case of two boundaries , , we indicate with and the first hitting times of the stochastic process across the boundaries and respectively. Aim of this paper is to study the dependency properties of , i.e. to determine

| (3) |

the joint pDf of and the corresponding joint pdf .

We define the following densities that distinguish the first boundary reached between the two ones delimiting the strip

| (4) |

and

| (5) |

For a standard Brownian motion the two densities and are known in closed form (cf. [8]) when the boundaries are constant and

| (6) | |||||

and the pdf and pDf of are

| (7) | |||||

| (8) |

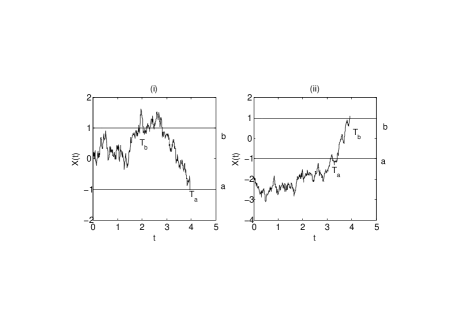

The quantities (4) and (5) are useful for the computation of the joint density function of and . Two different instances arise according to the location of the starting point with respect to the boundaries (cf. Figure 1).

It holds:

Theorem 2.1

Let be a diffusion process such that and let and be two continuous time dependent boundaries.

-

i)

If and for each or and for each , then

(9) -

ii)

If and for each , then

(10)

We omit the proof that is straightforward using the strong Markov property.

Remark 2.2

Note that the FPT pdf verifies the initial condition

| (11) |

Furthermore, due to the differentiability of the boundaries, it holds (cf. [34])

| (12) | |||||

| (13) |

3 System of integral equations

The computation of involves the transition pdfs and and the terms and . When the process is a linear regular diffusion, the transition pdf is available in closed form and, if the process is strictly linear, it is Gaussian. In the literature, transition pdf is also available for other regular diffusion processes, such as the Cox-Ingersoll-Ross model (also known as Feller process), the Bessel process or some instances of the Raleigh process (cf. [17, 16]). Further examples arise from space-time transformation of the Brownian motion (cf. [30]) or of the Cox-Ingersol-Ross process (cf. [11]). When closed form solutions are not available, the transition pdf is evaluated resorting to numerical methods, such as the numerical solution of the Kolmogorov equation [21, 36] or the numerical inversion of Fourier transforms [40]. Unfortunately closed form expressions for the densities and are known only for the Brownian motion with constant boundaries (cf. [8] formula 3.0.6) or for processes related to it through suitable transformations. Use of the following theorem helps to overcome this problem.

Theorem 3.1

Let be a diffusion process such that . Let and be two time dependent boundaries with bounded derivatives such that and for each . The pdf’s and are solution of the following system of Volterra first kind integral equations

| (14a) | ||||

| (14b) | ||||

Proof 3.2

Remark 3.3

It holds

Theorem 3.4

The system (14) has a unique continuous solution for .

Proof 3.5

The system of Volterra integral equations of the first kind (14) is equivalent to the system of Volterra integral equations of the second kind (16) that can be written in matricial form

| (17) |

where

| (18) |

| (19) |

| (20) |

Since the kernel is singular in , we introduce an equivalent system with continuous kernel. Mimicking the method presented in [10], we introduce two couple of functions and , , continuous in . Combining (14), (3.2) and (16), together with and we obtain

| (21) |

where

| (22) |

Remark 3.6

The functions and , can be determined. For example, for an Ornstein Uhlenbeck process characterized by the drift and infinitesimal variance , where , and are arbitrary real constants. The functions that regularize the kernels are , and , (cf. [10]).

When the boundaries are constant it holds:

Corollary 3.7

Let be a diffusion process such that and let and be two constant boundaries such that , then the following three expressions are equivalent for and :

| (24a) | ||||

| (24b) | ||||

| (25a) | ||||

| (25b) | ||||

| (26a) | ||||

| (26b) | ||||

where

and the functions , are fundamental solutions of (8.13b) in [35].

Proof 3.8

Generalizing the standard calculation of p. 30 in [20] for an arbitrary regular diffusion we obtain (24).

Applying Laplace transform to (14) and using the convolution theorem we get (25), a result recently published in [15].

Remark 3.9

The above results also hold for diffusion processes bounded by one or two reflecting boundaries when the diffusion interval is characterized by non natural boundaries, i.e. for Cox-Ingersoll-Ross whose diffusion interval is or for the reflected Brownian Motion.

4 Algorithms for and

In this section we describe two approaches to determine the density functions and .

When the boundaries are constant the densities and are obtained from the Laplace transforms (25) by inverting them numerically using, for example, Euler method [1].

Alternative methods become necessary when the boundaries and are time dependent or when the Laplace inversion presents numerical difficulties. For example in the case of the Ornstein Uhlenbeck process the expression of and involve parabolic cylinder function (cf. [18]). Their numerical inversion requests efforts specific for this instance. Furthermore there are processes for which and are not known in the literature. Their computation is possible however it requests the solution of specific second order differential equations (cf. [31]).

Here we propose the following numerical method that can be applied both for constant and time depending boundaries. Let us introduce a time discretization , where is a positive constant. To determine the two pdf’s and at the finite set of knots for , we use Euler method [23] to approximate the integrals on the r.h.s. of (14a) and (14b). Hence we get

| (30a) | ||||

| (30b) | ||||

The densities and can be evaluated in the knots for by means of the following algorithm.

Step 1

| (31a) | ||||

| (31b) | ||||

Step ,

| (32a) | ||||

| (32b) | ||||

Remark 4.1

The choice of equally spaced knots is motivated by the simplification of the notation but the method can be easily extended to non constant .

Theorem 4.2

If constants and exist, such that for all

| (33) | |||

| (34) |

then the absolute value of the errors and of the proposed algorithm at the discretization knots ,

are .

Proof 4.3

The Euler method applied to (14) gives

| (35a) | ||||

| (35b) | ||||

where and are the differences between the integrals on the r.h.s. of (14) and the finite sums on the r.h.s. of (35).

On subtracting (35a) from (30a) and (35b) from (30b)we get

| (36a) | ||||

| (36b) | ||||

Differencing (36) and recalling (12) and (13) we obtain

| (37a) | ||||

| (37b) | ||||

that can be rewritten as

| (38a) | ||||

| (38b) | ||||

Let us now consider the global error

| (39) |

When the hypotheses (33) and (34) are fulfilled

Observing that Euler method errors are and applying Theorem 7.1 of [23] we get and hence the thesis.

Remark 4.4

A better result on the errors can be obtained by improving the integral discretization rule, i.e. using the midpoint formula instead of Euler method. Other integration rules can improve the order of the error but strongly increase the computational complexity of the algorithm.

Remark 4.5

The two methods are equivalent in terms of computational time when the Laplace transform expression is a well behaved function. Nevertheless, the generalization of the method for a time dependent boundary is possible only for the numerical method.

5 Examples

In this section we discuss a set of examples of interest for the applications, i.e. standard Brownian motion, Geometric Brownian motion, Ornstein Uhlenbeck process. We apply the algorithms of Section 4 for numerical evaluations. When the joint densities are known in closed form, we use them to illustrate the reliability of the algorithms.

5.1 Standard Brownian motion

Let us consider a standard Brownian motion with constant boundaries. It is a time and space homogeneous diffusion process, hence we can rewrite its joint density functions (9) and (10) in closed form as

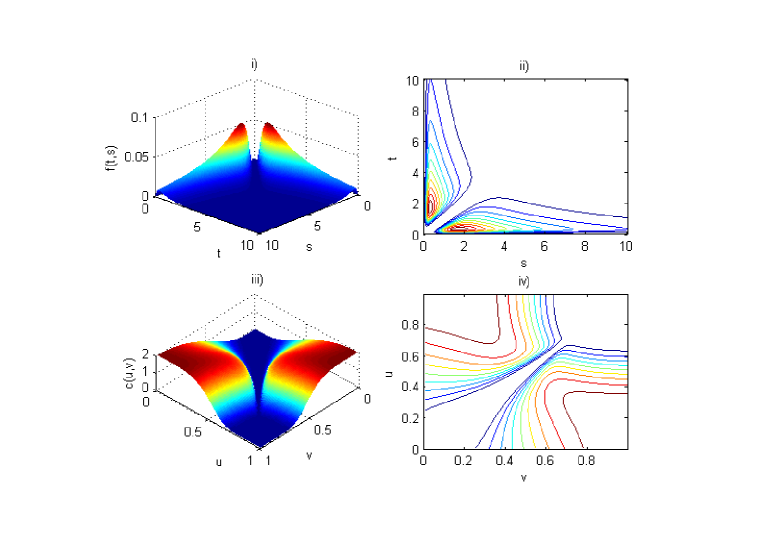

Figure 2 shows the joint pdf of the first hitting times of a standard Brownian motion through two constant boundaries and the corresponding copula together with the contour lines. Figures 3 illustrates the case of constant boundaries and asymmetric with respect to . The asymmetry of the boundaries location determines peaks of different height. Note that the maximum of the joint density have inverted height in the corresponding copula.

Remark 5.1

The stability of the algorithms introduced in Section 4, already proved by Theorem 4.2, is confirmed by the standard Brownian motion case where the pdf’s and are available in closed form. We apply the algorithms to the standard Brownian motion with constant boundaries and with discretization step and we compare the results with the closed form densities (6) with the series truncated to steps. The inversion of the Laplace transform with the Euler method gives a mean square deviation and . The numerical algorithm gives a mean square deviation and . It confirms the reliability of the new algorithm. The higher precision of the Laplace inversion with respect to the numerical method is determined by the simple expression of the involved Laplace transforms. However we cannot infer an analogous property for the other diffusions.

Remark 5.2

The extension of the above results to a Brownian motion with diffusion coefficient is straightforward. Indeed, a Brownian motion with diffusion coefficient can be transformed in a standard Brownian motion via the space transformation and the boundaries and becomes and respectively. When and one can determine . In this case the crossing of the boundary is not a sure event and the study of requests a suitable normalization. Similarly the case of and is analogous interchanging the role of the two boundaries.

Remark 5.3

Indicating with the copula of for a Brownian motion with diffusion coefficient and with the copula in the case , recalling the transformation , the relationship holds. Geometric Brownian motion can be obtained by a standard Brownian motion via the space transformation . The corresponding copula, , is related with the copula of the standard Brownian motion through .

The more general transformation is not interesting from the point of view of the exit times from a strip because it corresponds to transform the process into a Brownian motion with drift that has not a sure crossing, as stated in Remark 5.2.

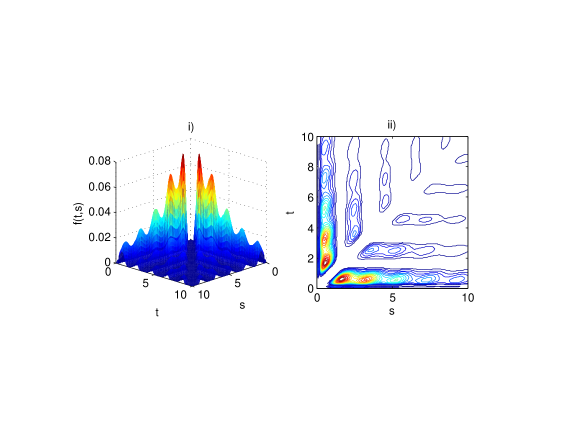

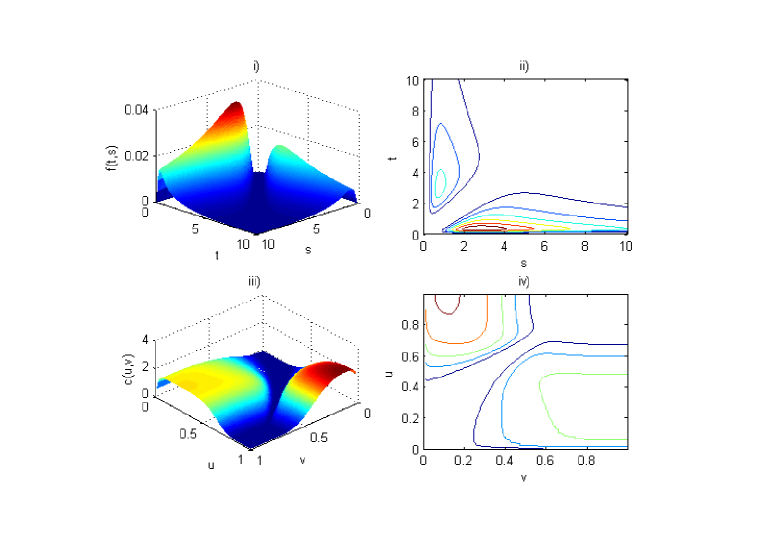

As a further example we consider a standard Brownian motion with the following boundaries and . Since the boundaries are time dependent, Laplace transform inversions cannot be applied. Figure 4 shows the joint pdf of the first hitting times and the corresponding contour lines obtained with the proposed numerical algorithm.

5.2 Ornstein Uhlenbeck Process

Consider as a further example the Ornstein Uhlenbeck process, described by the stochastic differential equation

| (43) | |||||

| (44) |

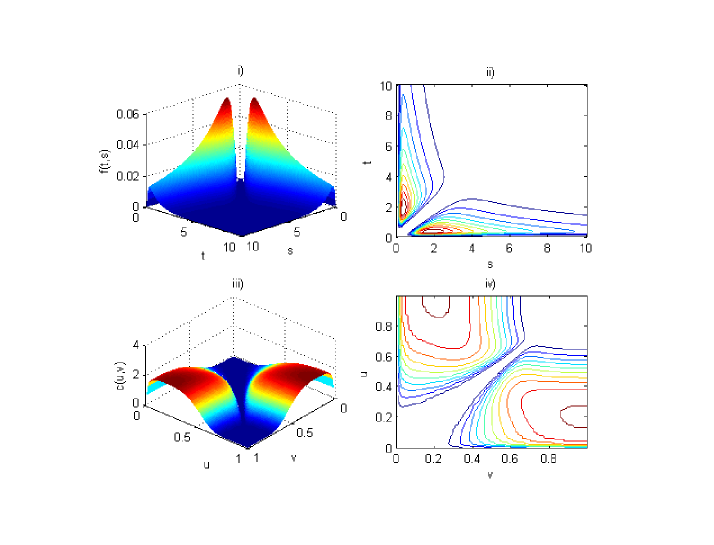

For this process representations and numerical methods are available and can be used to evaluate the first hitting time pdf [3, 10, 22]. On the other side, the density is not known in closed form. Here we have applied classical numerical algorithms (cf. [10]) to evaluate the first hitting time pdf and the algorithms of Section 4 to compute the second. Figure 5 shows the joint pdf and the corresponding copula of the first hitting times of an Ornstein Uhlenbeck process with parameter , , and through two constant boundaries . Figures 6 illustrates the case of asymmetric w.r.t. constant boundaries and . Note that represents the symmetry axis of the Ornstein Uhlenbeck process. The height of the peaks of the joint density and of the copula behaves as the Brownian motion case.

The Laplace transforms and for the OU process can be found in [8]. However the presence of the parabolic cylinder functions in their expression discourage their numerical inversion.

We are grateful to an anonymous referee for his interesting and constructive comments to improve the paper. Work supported in part by University of Torino Grant 2012 “Stochastic Processes and their Applications”and by project A.M.A.L.F.I. - Advanced Methodologies for the AnaLysis and management of the Future Internet (Università di Torino/Compagnia di San Paolo).

References

- [1] Abate, J. (1995) Numerical inversion of Laplace transforms of probability distributions. ORSA Journal on Computing 7, 36–43.

- [2] Albano, G. and Giorno V. (2006) A stochastic model in tumor growth. J Theor. Biol. 242, 329–336.

- [3] Alili, L., Patie P. and Pedersen, J.L. (2005) Representations of the First Hitting Time Density of an Ornstein-Uhlenbeck Process. Stoch. Model. 21, 967–980.

- [4] Arnold, L. (1974) Stochastic differential equations: Theory and Applications. Wiley-Interscience, New York.

- [5] Bassan, B. and Spizzichino, F. (2005) Relations among univariate aging, bivariate aging and dependence for exchangeable lifetimes. J. Multivariate Anal. 93 1, 313–339.

- [6] Bassan, B. and Spizzichino, F. (2005) Bivariate survival models with Clayton aging functions. Insurance Math. Econom. 37 1, 6–12.

- [7] Benedetto, E., Sacerdote, L. and Zucca, C. (2013) A first passage problem for a bivariate diffusion process: numerical solution with an application to neuroscience when the process is Gauss-Markov. J. Comput. Appl. Math. 242, 41–52.

- [8] Borodin, A.N. and Salminen, P. (2002) Handbook of Brownian Motion Facts and Formulae, 2nd edition. Birkh user, Basel.

- [9] Buonocore, A., Giorno V., Nobile, A.G. and Ricciardi, L.M. (1990) On the two-boundary first-crossing-time problem for diffusion processes. J. Appl. Probab. 27 1, 102–114.

- [10] Buonocore, A., Nobile, A.G. and Ricciardi, L.M. (1987) A new integral equation for the evaluation of first-passage-time probability densities. Adv. in Appl. Probab. 19 4, 784–800.

- [11] Capocelli, R.M., and Ricciardi L.M. (1976) On the transformation of diffusion processes into the Feller process. Math. Biosciences 29, 219-234.

- [12] Di Crescenzo A., Giorno V., Nobile A.G.and Ricciardi, L.M. (1995) On a symmetry-based constructive approach to probability densities for two-dimensional diffusion processes. J. Appl. Probab. 32 2, 316–336.

- [13] Davydov D., and Linetsky, V. (2003) Pricing Options on Scalar Diffusions: An Eigenfunction Expansion Approach. Oper. Res. 51 2, 185–209.

- [14] Galleani, L., Sacerdote, L., Tavella P. and Zucca, C. (2003) A mathematical model for the atomic clock error. Metrologia 40 4, S257–S264.

- [15] Giorno V., Nobile A.G. and Ricciardi, L.M. (2011) On the densities of certain bounded diffusion processes. Ricerche mat. 60, 89–124.

- [16] Giorno V., Nobile A.G., Ricciardi, L.M. and Sacerdote, L. (1986) Some remarks on the Rayleigh process. J. Appl. Prob. 23, 398–408.

- [17] Giraudo, M.T. and Sacerdote, L. (1999) An improved technique for the simulation of first passage times for diffusion processes. Commun. Statist. Simul. 28 4, 1135–1163.

- [18] Giraudo, M.T. and Sacerdote, L. (2013) Leaky Integrate and Fire models: a review on mathematicals methods and their applications. Lecture Notes in Mathematics 2058 4, 95–142.

- [19] Giraudo, M.T., Sacerdote, L. and Zucca, C. (2001) Evaluation of first passage times of diffusion processes through boundaries by means of a totally simulative algorithm. Meth.Comp. Appl. Prob. 3 2, 215–231.

- [20] Ito, K. and McKean, K.P. (1974). Diffusion Processes and Their Sample Paths. Springer.

- [21] Lapidus, L. and Pinder, G.F. (1999). Numerical Solution of Partial Differential Equations in Science and Engineering. Wiley.

- [22] Linetsky, V. (2004) Computing hitting time densities for CIR and OU diffusions: applications to mean-reverting models J. Comput. Finance 7 406, 1–22.

- [23] Linz, P. (1985). Analytical and numerical methods for Volterra equations. SIAM, Philadelphia.

- [24] Nelsen, R.B. (1999) An introduction to copulas, Lecture notes in Statistics 139, Springer, New York.

- [25] Novikov, A., Frishling, V. and Kordzakhia, N. (1999) Approximations of Boundary Crossing Probabilities for a Brownian Motion. J. Appl. Prob. 36, 1019–1030.

- [26] Oakes, D. (1989). Bivariate survival models induced by frailties. J. Amer. Statist. Assoc. 84 406, 487–493.

- [27] Orsingher, E. and Beghin, L. (2006) Probabilità e modelli aleatori. Aracne Editrice, Roma.

- [28] Panfilo, G., Tavella, P. and Zucca, C. (2004) How long does a clock error remain inside two threshold barriers? An evaluation by means of stochastic processes. Proc. European Frequency and Time Forum, Guilford.

- [29] Peskir, G. (2002). Limit at zero of the Brownian first-passage density. Probab. Theory Related Fields. 124, 100–111.

- [30] Ricciardi, L.M. (1976) On the transformation of diffusion processes into the Wiener process. J. Math. Analysis Appl. 54, 185-199.

- [31] Ricciardi, L.M. (1977) Diffusion Processes and Related Topics in Biology, Lecture Notes in Biomathematics, Vol. 14. Springer Verlag, Berlin.

- [32] Ricciardi, L.M., Di Crescenzo, A., Giorno V. and Nobile A.G. (1999) An outline of theoretical and algorithmic approaches to first passage time problems with applications to biological modeling. Math. Japonica 50 2, 247–322.

- [33] Ricciardi, L.M. and Sacerdote L. (1987) On the probability densities of an Ornstein-Uhlenbeck process with a reflecting boundary. J. Appl. Prob. 24, 355–369.

- [34] Ricciardi, L.M., Sacerdote L. and Sato, S. (1984) On an integral equation for first-passage-time probability densities. J. Appl. Prob. 21 2, 302–314.

- [35] Ricciardi, L.M. and Sato, S. (1990) Diffusion processes and first-passage-time problems. In: L.M. Ricciardi (Ed.), Lectures in Applied Mathematics and Informatics. Manchester Univ. Press., Manchester.

- [36] Smith G.D. (1978) Numerical Solution of Partial Differential Equations: Finite Difference Methods. Oxford Univ. Press.

- [37] Smith P.L. (2000) Stochastic dynamic models of response time and accuracy: A foundational primer. J. Math. Psychol. 44 3, 408–463.

- [38] Spizzichino, F. (2001) Subjective probability models for lifetimes. Chapman and Hall/CRC. Boca Raton, Fl.

- [39] Tricomi, F.G. (1957) Integral equations. Interscience, New York.

- [40] Van Loan C.F. (1992) Computational Frameworks for the Fast Fourier Transform. Siam, Philadelphia.

- [41] Zucca, C. and Sacerdote, L. (2009) On the inverse first-passage-time problem for a Wiener process. Ann. Appl. Probab. 19 4, 1319–1346.