Semi-Lagrangian schemes for linear and fully non-linear Hamilton-Jacobi-Bellman equations

Abstract.

We consider the numerical solution of Hamilton-Jacobi-Bellman equations arising in stochastic control theory. We introduce a class of monotone approximation schemes relying on monotone interpolation. These schemes converge under very weak assumptions, including the case of arbitrary degenerate diffusions. Besides providing a unifying framework that includes several known first order accurate schemes, stability and convergence results are given, along with two different robust error estimates. Finally, the method is applied to a super-replication problem from finance.

Key words and phrases:

Monotone approximation schemes, difference-interpolation methods, stability, convergence, error bound, degenerate parabolic equations, Hamilton-Jacobi-Bellman equations, viscosity solution.1991 Mathematics Subject Classification:

Primary: 65M12, 65M15, 65M06; Secondary: 35K10, 35K55, 35K65, 49L25, 49L20.Kristian Debrabant

University of Southern Denmark, Department of Mathematics and Computer Science

Campusvej 55

5230 Odense M, Denmark

Espen Robstad Jakobsen

Norwegian University of Science and Technology

NO–7491, Trondheim, Norway

(Communicated by the associate editor name)

1. Introduction

In this paper we consider the numerical solution of partial differential equations of Hamilton-Jacobi-Bellman type,

| (1) | |||||

| (2) |

where

, and is a complete metric space. The coefficients , , , and the initial data take values respectively in , the space of symmetric matrices, , , , and . We will only assume that is positive semi-definite, thus the equation is allowed to degenerate and hence not have smooth solutions in general. By solutions in this paper we will therefore always mean generalized solutions in the viscosity sense, see e. g. [6, 12]. Then the solution coincides with the value function of a finite horizon, optimal stochastic control problem [12].

To ensure comparison and well-posedness of (1)–(2) in the class of bounded -Lipschitz functions, we will use the following standard assumptions on its data:

-

(A1)

For any , for some matrix . Moreover, there is a constant independent of such that

where is a space-time Lipschitz/Hölder-norm.

The following result is standard.

2. Semi-Lagrangian schemes

Following [8] we propose a class of approximation schemes for (1)–(2) which we call Semi-Lagrangian or SL schemes. These schemes converge under very weak assumptions, including the case of arbitrary degenerate diffusions. In particular, these schemes are -stable and convergent for problems involving diffusion matrices that are not diagonally dominant. This class includes (parabolic versions of) the “control schemes” of Menaldi [11] and Camilli and Falcone [4] and some of the monotone schemes of Crandall and Lions [7]. It also includes SL schemes for first order Bellman equations [5, 9] and some new versions as discussed in the following section.

The schemes are defined on a possibly unstructured family of grids ,

for . Here satisfy

and is the set of vertices or nodes for a non-degenerate polyhedral subdivision of .

We consider the following general finite difference approximations of the differential operator in (1):

| (3) |

for and some . For this approximation we will assume

| (Y1) | ||||

| for all indicating components of the -vectors. |

Under assumption (Y1), a Taylor expansion shows that is a second order consistent approximation satisfying

| (4) |

for all smooth functions , where .

To relate this approximation to the spatial grid , we replace by its interpolant , yielding overall a semi-discrete approximation of (1),

We require the interpolation operator to fulfill the following two conditions:

-

(I1)

There are such that for all smooth functions

-

(I2)

There is a set of non-negative functions such that

and

for all .

(I1) implies together with (4) that is a consistent approximation of if . An interpolation satisfying (I2) is said to be positive and is monotone in the sense that implies that . Typically will be constant, linear, or multi-linear interpolation (i. e. in (I1)), because higher order interpolation is not monotone in general.

The final scheme can now be found by discretizing in time using a parameter ,

| (5) |

in , where , , for ,

As initial conditions we take

| (6) |

For the choices , and the time discretization corresponds to respectively explicit Euler, implicit Euler, and midpoint rule. For , the full scheme can be seen as generalized Crank-Nicolson type discretization.

3. Examples of approximations

- (1)

- (2)

- (3)

-

(4)

The new approximation obtained by combining approximations 1 and 2,

corresponds to our if for , and .

-

(5)

Yet another new approximation,

corresponds to our if for , and .

When does not depend on but does, approximations 4 and 5 are much more efficient than approximation 3.

4. Linear interpolation SL scheme (LISL)

To keep the scheme (5) monotone, linear or multi-linear interpolation is the most accurate interpolation one can use in general. In this typical case we call the full scheme (5)–(6) the LISL scheme. In the following, we denote by the positive part of . Then we have the following result by [8]:

Theorem 4.1.

(a) The LISL scheme is monotone if the following CFL conditions hold:

| (7) |

(b) The truncation error of the LISL scheme is ; it is first order accurate for , ( if ).

From this result it follows that the scheme is at most first order accurate, has wide and increasing stencil and a good CFL condition. From the truncation error and the definition of the stencil is wide since the scheme is consistent only if as and has stencil length proportional to

Here we have used that if (Y1) holds and , then typically . Note that if , then Finally, in the case the CFL condition for (5) is when , and it is much less restrictive than the usual parabolic CFL condition, .

Remark 1.

The LISL scheme is consistent and monotone for arbitrary degenerating diffusions, without requiring that is diagonally dominant or similar conditions. In comparison to other schemes applicable in this situation, like the ones of Bonnans-Zidani [3], it is much easier to analyze and to implement and faster in the sense that the computational cost for approximating the diffusion matrix is for fixed independent of the stencil size.

5. The error estimate of [8]

To simplify the presentation, in the following we restrict to a uniform time-grid, . Let . To apply the regularization method of Krylov [10] we need a regularity and continuous dependence result for the scheme that relies on the following additional (covariance-type) assumptions: Whenever two sets of data and are given, the corresponding approximations and in (3) satisfy

| (Y2) |

when are evaluated at and are evaluated at for all .

Then one can prove the following error estimate [8]:

Theorem 5.1 (Error Bound I).

This error bound holds also for unstructured grids. For more regular solutions it is possible to obtain better error estimates, but general and optimal results are not available. The best estimate in our case is which is achieved when and . Note that the CFL conditions (7) already imply that if . Also note that the above bound does not show convergence when is optimal for the LISL scheme ().

6. A new error estimate

In the above error estimate, the lower estimate on follows if you can prove regularity and continuous dependence results for the solution of the equation only. The proof of the upper estimate is symmetric and requires such results for the numerical solution. However, it is possible to avoid using such properties of the numerical solution by a clever approximation argument, see e. g. [1]. This allows for error estimates that show convergence for any such that the scheme is consistent. We need an extra assumption on the coefficients:

-

(A2)

The coefficients , , , are continuous in for all .

Theorem 6.1 (Error Bound II).

With optimal for the LISL scheme, and , we find that .

Proof.

By a direct computation the local truncation error of the method is bounded by

for smooth (cf. Lemma 4.1 in [8]). Moreover if also for any , then the truncation error is of order

Since the scheme is monotone (under the CFL condition) and condition (A1) holds, it now follows from Theorem 3.1 in [1] that

and we complete the proof optimizing over (as e. g. in [1, 8]). ∎

7. Convergence test for a super-replication problem

We consider a test problem from [2] which was used to test convergence rates for numerical approximations of a super-replication problem from finance. The corresponding PDE is

| (8) |

with , and . We take as exact solution as in [2], and then is forced to be

In [2] , while we take to prevent the LISL scheme from overstepping the boundaries. Note that changing does not change the solutions as long as in the interior of the domain, see [2], and hence the above equation is equivalent to the equation used in [2]. The initial values and Dirichlet boundary values at and are taken from the exact solution. As in [2], at and homogeneous Neumann boundary conditions are implemented. To approximate the values of , the Howard algorithm is used (see [2]), which requires an implicit time discretization, so we choose . We choose and a regular triangular grid. The numbers of time steps are chosen as .

The results at are given in Table 7. The numerical order of convergence is approximately one.

| rate | ||

|---|---|---|

| 1.50e-1 | 2.01e-1 | |

| 7.50e-2 | 9.49e-2 | 1.08 |

| 3.75e-2 | 4.29e-2 | 1.15 |

| 1.87e-2 | 1.94e-2 | 1.15 |

Results for the convergence test for the super-replication problem at

Remark 2.

Equation (8) can not be written in a form (1) satisfying the assumptions of this paper, so the results of this paper do not apply to this problem. However, it seems possible to extend them to cover this problem using comparison results from [2] along with -bounds on the numerical solution that follow from the maximum principle.

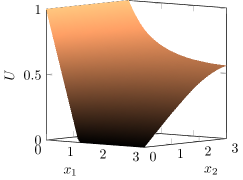

8. A super-replication problem

We apply our method to solve a problem from finance, the super-replication problem under gamma constraints considered in [2]. It consists of solving equation (8) with , Neumann boundary conditions and as in Subsection 7, and initial and Dirichlet conditions given by

The solution obtained with the LISL scheme is given in Figure 1 and coincides with the solution found in [2]. It gives the price of a put option of strike and maturity 1, and and are respectively the price of the underlying and the price of the forward variance swap on the underlying.

References

- [1] (MR2336272) [10.1090/S0025-5718-07-02000-5] Guy Barles and Espen Robstad Jakobsen, Error bounds for monotone approximation schemes for parabolic Hamilton-Jacobi-Bellman equations, Math. Comp., 76 (2007), 1861–1893.

- [2] (MR2519604) [10.1137/080725222] Olivier Bokanowski, Benjamin Bruder, Stefania Maroso and Hasnaa Zidani, Numerical approximation for a superreplication problem under gamma constraints, SIAM J. Numer. Anal., 47 (2009), 2289–2320.

- [3] (MR2087732) [10.1051/m2an:2004034] Joseph Frédéric Bonnans, Élisabeth Ottenwaelter and Hasnaa Zidani, A fast algorithm for the two dimensional HJB equation of stochastic control, M2AN Math. Model. Numer. Anal., 38 (2004), 723–735.

- [4] (MR1326802) Fabio Camilli and Maurizio Falcone, An approximation scheme for the optimal control of diffusion processes, RAIRO Modél. Math. Anal. Numér., 29 (1995), 97–122.

- [5] (MR713483) [10.1007/BF01448394] Italo Capuzzo Dolcetta, On a discrete approximation of the Hamilton-Jacobi equation of dynamic programming, Appl. Math. Optim., 10 (1983), 367–377.

- [6] (MR1118699) [10.1090/S0273-0979-1992-00266-5] Michael G. Crandall, Hitoshi Ishii and Pierre-Louis Lions, User’s guide to viscosity solutions of second order partial differential equations, Bull. Amer. Math. Soc. (N.S.), 27 (1992), 1–67.

- [7] (MR1417861) [10.1007/s002110050228] Michael G. Crandall and Pierre-Louis Lions, Convergent difference schemes for nonlinear parabolic equations and mean curvature motion, Numer. Math., 75 (1996), 17–41.

- [8] (MR3042570) [10.1090/S0025-5718-2012-02632-9] Kristian Debrabant and Espen Robstad Jakobsen, Semi-Lagrangian schemes for linear and fully non-linear diffusion equations, Math. Comp., 82 (2013), 1433–1462.

- [9] (MR866164) [10.1007/BF01442644] Maurizio Falcone, A numerical approach to the infinite horizon problem of deterministic control theory, Appl. Math. Optim., 15 (1987), 1–13.

- [10] (MR1759507) [10.1007/s004400050264] Nicolai V. Krylov, On the rate of convergence of finite-difference approximations for Bellman’s equations with variable coefficients, Probab. Theory Related Fields, 117 (2000), 1–16.

- [11] (MR993288) [10.1137/0327031] José-Luis Menaldi, Some estimates for finite difference approximations, SIAM J. Control Optim., 27 (1989), 579–607.

- [12] (MR1696772) Jiongmin Yong and Xun Yu Zhou, “Stochastic Controls”, vol. 43 of Applications of Mathematics, Springer-Verlag, New York, 1999.

Received xxxx 20xx; revised xxxx 20xx.