MEAN-VARIANCE POLICY FOR DISCRETE-TIME CONE CONSTRAINED MARKETS: TIME CONSISTENCY IN EFFICIENCY AND MINIMUM-VARIANCE SIGNED SUPERMARTINGALE MEASURE††thanks: This research work was partially supported by Research Grants Council of Hong Kong under grants 414808, 414610 and 520412, National Natural Science Foundation of China under grant 71201094, and Shanghai Pujiang Program of China under grant 12PJC051. The second author is grateful to the support from the Patrick Huen Wing Ming Chair Professorship of Systems Engineering and Engineering Management.

Abstract

The discrete-time mean-variance portfolio selection formulation, a representative of general dynamic mean-risk portfolio selection problems, does not satisfy time consistency in efficiency (TCIE) in general, i.e., a truncated pre-committed efficient policy may become inefficient when considering the corresponding truncated problem, thus stimulating investors’ irrational investment behavior. We investigate analytically effects of portfolio constraints on time consistency of efficiency for convex cone constrained markets. More specifically, we derive the semi-analytical expressions for the pre-committed efficient mean-variance policy and the minimum-variance signed supermartingale measure (VSSM) and reveal their close relationship. Our analysis shows that the pre-committed discrete-time efficient mean-variance policy satisfies TCIE if and only if the conditional expectation of VSSM’s density (with respect to the original probability measure) is nonnegative, or once the conditional expectation becomes negative, it remains at the same negative value until the terminal time. Our findings indicate that the property of time consistency in efficiency only depends on the basic market setting, including portfolio constraints, and this fact motivates us to establish a general solution framework in constructing TCIE dynamic portfolio selection problem formulations by introducing suitable portfolio constraints.

Key Words: cone constrained market, discrete-time mean-variance policy, time consistency in efficiency, minimum-variance signed supermartingale measure

1 Introduction

In a dynamic decision problem, a decision maker may face a dilemma when the overall objective for the entire time horizon under consideration does not conform with a “local” objective for a tail part of the time horizon. In the language of dynamic programming, Bellman’s principle of optimality is not applicable in such situations, as the global and local interests derived from their respective objectives are not consistent. This phenomenon has been investigated extensively recently in the literature of finance and financial engineering under the term of time inconsistency. In the language of portfolio selection, when a problem is not time consistent, the (global) optimal portfolio policy for the entire investment horizon determined at initial time may not be optimal for a truncated investment problem at some intermediate time and for certain realized wealth level. Investors thus have incentives to deviate from the global optimal policy and to seek the (local) optimal portfolio policy, instead, for the truncated time horizon.

As time consistency (or dynamic consistency) is a basic requirement for dynamic risk measures (see Rosazza Gianin (2006), Boda and Filar (2006), Artzner et al. (2007) and Jobert and Rogers (2008)), all the appropriate dynamic risk measures should necessarily possess certain functional structure so that Bellman’s principle of optimality is satisfied. Unfortunately, almost all static risk measures which investors have been comfortably adopting in practice for decades, including the variance, VaR (Duffie and Pan (1997)) and CVaR (Uryasev (2000)), are not time consistent when being extended to dynamic situations (Boda and Filar (2006)). Researchers have proposed using the nonlinear expectation (“g-expectation”) (Peng (1997)) to construct time consistent dynamic risk measures.

When a dynamic risk measure is time consistent, it not only justifies the mathematical formulation for risk management, but also facilitates the solution process in finding the optimal decision, as the corresponding dynamic mean-risk portfolio selection problem satisfies Bellman’s principle of optimality, thus being solvable by dynamic programming (e.g., see Cherny (2010)). When a dynamic risk measure is time inconsistent, the corresponding dynamic mean-risk portfolio selection problem is nonseparable in the sense of dynamic programming, thus generating intractability, or even an insurmountable obstacle in deriving the solution. Consider the dynamic mean-variance portfolio selection problem as an example, as it is the focus of this paper. As the nonseparable structure of the variance term leads to a notoriety of the variance minimization problem, it took almost 50 years to figure out ways to extend the seminal Markowitz (1952)’s static mean-variance formulation to its dynamic counterpart (see Li and Ng (2000) for the discrete-time (multi-period) mean-variance formulation and Zhou and Li (2000) for the continuous-time mean-variance formulation). The derived dynamic optimal investment policy in Li and Ng (2000) and Zhou and Li (2000) is termed by Basak and Chabakauri (2010) as pre-committed dynamic optimal investment policy, as the (adaptive) optimal policy is fixed at time 0 to achieve overall optimality for the entire investment horizon. As the original dynamic mean-variance formulation is not time consistent, the derived pre-committed dynamic optimal investment policy does not satisfy the principle of optimality and investors have incentive to deviate from such a policy during the investment process in certain circumstances, as revealed in Zhu et al. (2003) and Basak and Chabakauri (2010).

There are two major research directions in the literature to alleviate the effects of the time inconsistency of the pre-committed optimal mean-variance policy. To remove the time inconsistency of the pre-committed optimal mean-variance policy, Basak and Chabakauri (2010) suggested the so-called time-consistent policy by backward induction in that the investor optimally chooses the (time consistent) policy at any time , on the premise that he has already decided his time consistent policies in the future. Björk et al. (2014) extended the formulation in Basak and Chabakauri (2010) by introducing state dependent risk aversion and used the backward time-inconsistent control method (see Björk and Murgoci (2010)) to derive the corresponding time-consistent policy. Czichowsky (2013) considered the time consistent policies for both discrete-time and continuous-time mean-variance models and revealed the connections between the two. Enforcing a time consistent policy in an inherent time-inconsistent problem undoubtedly incurs a cost, i.e., resulting in a worse mean-variance efficient frontier when compared with the one associated with the pre-committed mean-variance policy, as evidenced from some numerical experiments reported in Wang and Forsyth (2011). On the other hand, Cui et al. (2012) relaxed the concept of time consistency in the literature to “time consistency in efficiency” (TCIE) based on a multi-objective version of the principle of optimality: The principle of optimality holds if any tail part of an efficient policy is also efficient for any realizable state at any intermediate period (Li and Haimes (1987) and Li (1990)). Note that the essence of the ground breaking work of Markowitz (1952) is to attain an efficiency in portfolio selection by striking a balance between two conflicting objectives of maximizing the expected return and minimizing the investment risk. In this sense, TCIE is nothing but requiring efficiency for any truncated mean-variance portfolio selection problem at every time instant during the investment horizon. Cui et al. (2012) showed that the dynamic mean-variance problem does not satisfy time consistency in efficiency (TCIE) and developed a TCIE revised mean-variance policy by relaxing the self-financing restriction to allow withdrawal of money out of the market. While the revised policy achieves the same mean-variance pair of the terminal wealth as the the pre-committed dynamic optimal investment policy does, it also enables investors to receive a free cash flow stream during the investment process. The revised policy proposed in Cui et al. (2012) thus strictly dominates the pre-committed dynamic optimal investment policy.

It is interesting to note that the current literature on time inconsistency has been mainly confined to investigation of time consistent risk measures. While portfolio constraints serve as an important part of the market setting, the literature has been lacking of a study on the effects of portfolio constraints on the property of time consistency and TCIE. Let us consider an extreme situation where only one admissible investment policy is available over the entire investment horizon. In such a situation, no matter whether or not the adopted dynamic risk measure is time consistent, this policy is always optimal and time consistent, as it is the only choice available to investors. Another lesson we could learn is from Wang and Forsyth (2011) where they numerically compared the pre-committed optimal mean-variance policy and the time-consistent mean-variance policy (proposed by Björk et al. (2014)) in a continuous-time market with no constraint, with no-bankruptcy constraint or with no-shorting constraint, respectively. They found that with constraints, the efficient frontier generated by the time-consistent mean-variance policy gets closer to the efficient frontier generated by the pre-committed optimal mean-variance policy in the constrained market than in the unconstrained market, i.e., the presence of portfolio constraints may reduce the cost when enforcing a time consistent policy in an inherent time-inconsistent problem. Based on the above recognition, it is our purpose to study in this paper analytically the impact of convex cone-type portfolio constraints on TCIE in a discrete-time market. Our analysis reveals an “if and only if” relationship between TCIE and the conditional expectation of the density of the minimum-variance signed supermartingale measure (with respect to the original probability measure). As our finding indicates that the property of time consistency in efficiency only depends on the basic market setting, including portfolio constraints, we further establish a general solution framework in constructing TCIE dynamic portfolio selection problem formulations by introducing suitable portfolio constraints.

The main theme and the contribution of this paper is to address and answer the following question: Given a financial market with its return statistics known, what are the cone constraints on portfolio policies or what additional cone constraints are needed to be introduced such that the derived optimal portfolio policy is TCIE. The paper is thus organized to present this story line with the following key points in achieving this overall research goal. For a general class of discrete-time convex cone constrained markets, we derive analytically the pre-committed discrete-time efficient mean-variance policy using duality theory and dynamic programming (Section 2). Theorem 2.1 fully characterizes the distinct features of this policy and, in particular, reveals that the optimal policy is a two-piece linear function of the current wealth, while the time-varying breaking point of the two pieces is determined by a deterministic threshold wealth level. We then discuss the necessary and sufficient conditions for the pre-committed efficient policy to be TCIE (Section 3). Theorem 3.1 specifies the behavior pattern of TCIE policies for both cases below and above the threshold wealth level. We define and derive the minimum-variance signed supermartingale measure (VSSM) for cone constrained markets and reveal its close relationship with TCIE (Section 4). More specifically, we show in Theorem 4.3 that the pre-committed efficient mean-variance policy satisfies TCIE if and only if the conditional expectation of VSSM’s density (respect to the original probability measure) is nonnegative, or once the conditional expectation becomes negative, it remains at the same negative value until the terminal time. We finally answer the question how to completely eliminate time inconsistency in efficiency by introducing additional cone constraints to the market (Section 5). Theorem 5.1 can be viewed as the culmination of all the results in this paper, in which a constructive framework in achieving TCIE is established through identifying a convex cone for constraining portfolios such that its dual cone includes the given expected excess return vector of the market under consideration. In order to make our presentation clear, we have placed all the proofs in the appendix.

2 Optimal mean-variance policy in a discrete-time cone constrained market

The capital market of time periods under consideration consists of risky assets with random rates of returns and one riskless asset with a deterministic rate of return. An investor with an initial wealth joins the market at time and allocates his wealth among these assets. He can reallocate his wealth among the assets at the beginning of each of the following consecutive time periods. The deterministic rate of return of the riskless asset at time period is denoted by and the rates of return of the risky assets at time period are denoted by a vector , where is the random return of asset at time period and the notation ′ denotes the transpose operation. It is assumed in this paper that vectors , , are statistically independent with mean vector and positive definite covariance matrix,

Assume that all the random vectors, , , are defined in a filtrated probability space , where and is the trivial -algebra over . Therefore, is just the unconditional expectation . Let be the wealth of the investor at the beginning of the -th time period, and , , be the dollar amount invested in the th risky asset at the beginning of the -th time period. The dollar amount invested in the riskless asset at the beginning of the -th time period is then equal to . It is assumed that the admissible investment strategy is an -measurable Markov control, i.e., , and the realization of is restricted to a deterministic and non-random convex cone . Such cone type constraints are of wide application in practice to model regulatory restrictions, for example, restriction of no short selling and restriction for non-tradeable assets. Cone type constraints are also useful to represent portfolio restrictions, for example, the holding of the first asset must be no less than the second asset, which can be generally expressed by (see Cuoco (1997) and Napp (2003) for more details).

An investor of mean-variance type seeks the best admissible investment strategy, , such that the variance of the terminal wealth, , is minimized subject to that the expected terminal wealth, , is fixed at a preselected level ,

where

is the vector of the excess rates of returns. It is easy to see that and are independent, is an adapted Markovian process and .

Remark 2.1.

Varying parameter in from to yields the minimum variance set in the mean-variance space. Furthermore, as setting equal to in gives rise to the minimum variance point, the upper branch of the minimum variance set corresponding to the range of from to characterizes the efficient frontier in the mean-variance space which enables investors to recognize the trade-off between the expected return and the risk, thus helping them specify their preferred expected terminal wealth.

Note that condition implies the positive definiteness of the second moment of . The following is then true for :

which further implies

Constrained dynamic mean-variance portfolio selection problems with various constraints have been attracting increasing attention in the last decade, e.g., Li et al (2002), Zhu et al. (2004), Bielecki et al (2005), Sun and Wang (2006), Labbé and Heunis (2007) and Czichowsky and Schweizer (2010). Recently, Czichowsky and Schweizer (2013) further considered cone-constrained continuous-time mean-variance portfolio selection with price processes being semimartingales.

Remark 2.2.

In this section, we will use duality theory and dynamic programming to derive the discrete-time efficient mean-variance policy analytically in convex cone constrained markets. We will demonstrate that the optimal mean-variance policy is a two-piece linear function of the current wealth level, which represents an extension of the result in Cui et al. (2014) for discrete-time markets under the no-shorting constraint (a special convex cone) and a discrete-time counterpart of the policy in Czichowsky and Schweizer (2013).

We define the following two deterministic functions, and , on for ,

| (1) |

with terminal condition , and denote their deterministic minimizers and optimal values, respectively, as

| (2) | |||

| (3) |

As will be seen later in the paper, functions and appear in the optimal policy for problem . The following lemma is important in deriving our main result in this paper.

Lemma 2.1.

For , the following properties hold,

| (4) | |||

Furthermore, if and only if (Notation denotes the -dimensional zero vector).

Note that Lemma 2.1 reduces the piecewise quadratic form of in (3) to a piecewise linear one in (4). We can adopt Lagrangian duality and dynamic programming to solve problem .

Theorem 2.1.

Define (with being set to 1). When both and hold, or both and hold, problem does not have a feasible solution.

Under the assumption that problem is feasible, its optimal investment policy can be expressed by the following deterministic piecewise linear function of wealth level ,

| (5) | |||

where

| (6) |

Moreover, the minimum variance set is given as

and the mean-variance efficient frontier, which is the upper branch of the minimum variance set, is expressed as

| (7) |

Note that every point on the lower branch of the minimum variance set corresponding to is dominated by the minimum variance point with = and = 0. Although the cases with do not make sense from an economic point of view for the entire investment horizon, we do need this explicit expression for the lower branch of the minimum variance set for our later discussion in the paper. As we demonstrate later in the paper, the pre-committed investment policy is not time consistent in efficiency. Thus, applying the pre-committed mean-variance policy for a truncated time horizon could result in an inefficient mean-variance pair which falls onto the lower branch of the minimum variance set for the truncated time horizon. Time inconsistency in efficiency hides behind this kind of phenomena which is not economically sensible. The purpose of this paper is to devise a solution scheme to eliminate time inconsistency in efficiency, thus removing this kind of phenomena with no economic sense.

Remark 2.3.

Theorem 2.1 reveals that the optimal investment policy is a two-piece linear function with respect to the investor’s current wealth level and this finding represents the discrete-time counterpart of the result in Czichowsky and Schweizer (2013) for continuous-time. In Section 5, we will also demonstrate that the result in Theorem 2.1 is also an extension of the result in Cui et al. (2014) for multiperiod mean-variance formulation with no-shorting constraint.

When and hold, the optimal investment policy , , in (5) is efficient, which we term as a pre-committed efficient mean-variance policy following Basak and Chabakauri (2010). When , the optimal investment policy is achieved by , i.e., investor invests all his wealth in the riskless asset, which is exactly the minimum variance policy. When and hold, the optimal investment policy of , , , in (5) is inefficient.

Remark 2.4.

By setting , , the pre-committed discrete-time efficient mean-variance policy in (5) reduces to the one in the unconstrained market (Li and Ng (2000)),

where

The major differences between the pre-committed efficient mean-variance policies in a cone constrained market and in the unconstrained market lie in the following three aspects. First, in a cone constrained market, problem may become infeasible, while feasibility is never an issue for the mean-variance portfolio selection in unconstrained markets. Second, when , , are identically distributed, , , take the same value, which implies that investors hold a unique risky portfolio for any time period in an unconstrained market, which is also independent of the wealth level of the investor. In a cone constrained market, however, the investor may hold two different risky portfolios, and , while and are in general different for the same time . A key observation thus is that the investor may switch his risky position according to his current wealth level. Third, in a cone constrained market, although the excess rates of return of risky assets, , , are statistically independent, the future , , may influence the current risky portfolios, and , through parameters and , which implies that the independent structure of the optimal risky portfolio holding (rooted from the independent assumption of the random rate of return) is destroyed by the presence of constraints. Thus, in general, when , which implies further that the risky positions of the investor are not time-invariant anymore. In summary, we can conclude that, in a cone-constrained market, the risky positions are both state-dependent and time-dependent.

3 Conditions for Time Consistency in Efficiency of the Pre-committed Efficient Mean-Variance Policy

We check now the performance of the pre-committed optimal mean-variance policy derived for the entire investment time horizon given in (5) of the last section in truncated time periods. More specifically, we would like to examine the efficiency of in shorter time periods and develop conditions under which remains efficient all the time. Let us consider the following truncated mean-variance problem for any realized wealth in time period ,

where is a preselected level of the expected final wealth for the truncated mean-variance problem. As problem is of the same structure of problem , based on Theorem 2.1, the corresponding optimal policy of is given by

| (8) |

where

| (9) |

Evidenced from our discussion on , the solution to is mean-variance efficient at if and only if .

Now we consider the following inverse optimization problem of : For any , , find an expected final wealth level such that the truncated pre-committed optimal mean-variance policy , with = , specified in (5) solves . We call such a an induced expected final wealth level by the pre-committed policy at . It becomes evident now that if for some , , the induced is less than , then the truncated pre-committed optimal mean-variance policy , with = , is inefficient for the truncated mean-variance problem from stage to with given .

Definition 3.1.

An efficient solution of , , is time consistent in efficiency (TCIE) if for all wealth in time period , = 1, , , the induced expected final wealth level always satisfies , such that solves .

In plain language, a globally mean-variance efficient solution is TCIE if it is also locally mean-variance efficient for every intermediate stage and every possible realizable state (wealth level ).

Remark 3.1.

Note that the above definition of TCIE shares the same spirit as the one in Cui et al. (2012). However, the current one is defined in terms of the induced expected final wealth, while the one in Cui et al. (2012) is defined in terms of the induced trade off between the variance and the expectation of the terminal wealth.

Remark 3.2.

Note also that insisting time consistency of implies that solves for any realized wealth in every time period , = 1, , .

Remark 3.3.

Cui et al. (2012) showed that discrete-time mean-variance portfolio selection problem is not time consistent in efficiency (TCIE) in unconstrained markets. When the investor’s wealth level exceeds a deterministic level determined by the market setting, he may become irrational to minimize both the mean and the variance when continuing applying the pre-committed efficient policy. We will check in this section whether discrete-time mean-variance portfolio selection problem in cone constrained markets is also not TCIE.

Note that the truncated minimum variance policy is always the minimum variance policy of the corresponding truncated mean-variance problem. Therefore, we only need to check whether the truncated pre-committed efficient policy (expect for the minimum variance policy), , , is efficient or not with respect to the corresponding truncated mean-variance problem.

Theorem 3.1.

The truncated pre-committed efficient mean-variance policy (except for the minimum variance policy), , is also an efficient policy of the truncated problem , if and only if

Condition (i) in Theorem 3.1 for the efficiency of the truncated pre-committed efficient mean-variance policy at time can be interpreted as a threshold condition for ,

which is similar to the result of Proposition 3.1 in Cui et al. (2012). On the other hand, note from the last statement in Lemma 2.1, if becomes 1, then all with will remain 1, implying = 0, . Therefore, condition (ii) in Theorem 3.1 can be interpreted as follows: Once the wealth level at time exceeds the deterministic level, , investor switches to adopt the minimum variance policy (to invest all his wealth in the riskless asset). With the help of Eq. (5), under both conditions the investor either holds portfolio or only invests in riskless asset. Thus, we term as efficient risky portfolio. In contrast, when , , the truncated pre-committed efficient mean-variance policy is inefficient and the corresponding portfolio is thus termed as inefficient risky portfolio.

Based on Proposition 3.1 and the definition of time consistency in efficiency, the following lemma for TCIE of the pre-committed efficient mean-variance policy is apparent.

Lemma 3.1.

The pre-committed efficient mean-variance policy (except for the minimum variance policy) is TCIE if and only if condition (i) or condition (ii) holds for all possible achieved by pre-committed efficient mean-variance policy and for all .

Remark 3.4.

The following proposition betters our understanding further for investigating the possibility in achieving TCIE.

Proposition 3.1.

Adopting the pre-committed efficient mean-variance policy at time yields the following conditional probabilities,

We can conclude now that, for any pre-committed efficient mean-variance policy (except for the minimum variance policy), the probability that condition (i) or condition (ii) holds at time only depends on market parameters and , , where we assume the pre-committed mean-variance policy is efficient with (equivalent form of ). This finding motivates us to deepen our analysis by linking the time consistency in efficiency with a minimum-variance signed supermartingale measure introduced in the next section.

4 The variance-optimal signed supermartingale measure

It has been well known that the problems of mean-variance portfolio selection and mean-variance hedging have a strong connection (see Schweizer (2010)). Xia and Yan (2006) showed that in an unconstrained incomplete market, the optimal terminal wealth of an efficient dynamic mean-variance policy is related to the so-called variance-optimal signed martingale measure (VSMM) of the market, and the optimal terminal wealth has a nonnegative marginal utility if and only if VSMM is nonnegative. Note that VSMM is the particular signed measure with the minimum variance among all signed martingale measures, under which the discounted wealth process of any admissible policy is a martingale. In discrete-time unconstrained markets, the density of VSMM with respect to the objective probability measure takes a product form (see Schweizer (1996) and Černý and Kallsen (2009)). Actually, VSMM plays a central role in the mean-variance hedging and is the pricing kernel of the contingent claims (see Schweizer (1995) and Schweizer (1996)).

Motivated by Xia and Yan (2006), we will carry out our analysis forward in this section by deriving a similar “VSMM” in our constrained market. However, the situation is much more complicated in a constrained market than in an unconstrained one. Pham and Touzi (1999) and Föllmer and Schied (2004) showed that in a constrained market, no arbitrage opportunity is equivalent to the existence of a supermartingale measure, under which the discounted wealth process of any admissible policy is a supermartingale (see Carassus et al. (2001) for a situation with upper bounds on proportion positions). Therefore, we define in this paper the particular measure with the minimum variance among all signed supermartingale measures as the minimum-variance signed supermartingale measure (VSSM) and derive its semi-analytical form for discrete-time cone constrained markets. VSSM in our paper can be considered as an extension of VSMM in constrained markets and both take the product form. We will also show in this section that the VSSM is not only related to the optimal terminal wealth achieved by efficient mean-variance policies, but also associated with TCIE of efficient mean-variance policies. Our results explicitly assess the effect of portfolio constraints on TCIE.

We use to denote the set of all -measurable square integrable random variables. According to Pham and Touzi (1999) and Chapter 9 of Föllmer and Schied (2004), a cone constrained market does not have any arbitrage opportunity if and only if there exists an equivalent probability measure under which the discounted wealth process of any admissible policy is supermartingale. Therefore, we extend the definitions of the signed martingale measure and the variance-optimal signed martingale measure proposed in Schweizer (1996) to a signed supermartingale measure and minimum-variance signed supermartingale measure in this study.

Definition 4.1.

A signed measure on is called a signed supermartingale measure if , with and the discounted wealth process of any admissible policy is supermartingale under , i.e., for ,

| (10) |

where denotes the time- wealth level achieved by applying policy .

We denote by the set of all signed supermartingale measures. It is easy to see that inequality(10) is equivalent to either one of the following two inequalities,

| (11) | |||

| (12) |

where denotes the polar cone of , i.e.,

Definition 4.2.

A signed supermartingale measure is called minimum-variance signed supermartingale measure if minimizes

over all .

For , we define

Then we have

If , we can set , , equal to any value. It is easy to check that .

In the following, we will derive a semi-analytical form of the minimum-variance signed supermartingale measure in the cone constrained market. We first formulate the following pair of optimization problems for ,

and

Lemma 4.1.

The solutions of and are given respectively by

and the optimal objective values of and are and respectively.

Theorem 4.1.

The density of the minimum-variance signed supermartingale measure (with respect to objective probability measure ) is given by

where

Furthermore,

| (13) | |||

| (14) |

There is a strong connection between VSSM and the optimal terminal wealth achieved by the pre-committed efficient mean-variance policy. Substituting the pre-committed efficient mean-variance policy in (5) into the wealth dynamic equation yields

| (15) |

with . Set . From the wealth equation in (15) which satisfies, we deduce

| (16) |

Note that by virtue of the fact that and .

We can show

For , it is trivial. Assume that the statement holds true for , we now show that the statement also holds true for , as

Thus, the time optimal wealth achieved by the pre-committed efficient mean-variance policy is given by

| (17) |

which leads to the following theorem.

Theorem 4.2.

The optimal terminal wealth achieved by the pre-committed efficient mean-variance policy and the VSSM have the following duality relationship:

Remark 4.1.

Xia and Yan (2006) considered the mean-variance portfolio selection problem in an incomplete, albeit unconstrained, market and established the relationship between the mean-variance efficient portfolio and the variance-optimal signed martingale measure (VSMM) via analyzing the geometric property of the problem. Actually, the above Theorem 4.2 is an extension of Theorem 3.1 in Xia and Yan (2006) for the discrete-time cone constrained market. When the convex cone constraint is chosen as the whole space, our theorem reduces to the result in Xia and Yan (2006). On the other hand, different from Xia and Yan (2006), we prove the theorem by solving both the optimal terminal wealth and the VSSM directly.

Most prominently, we will demonstrate in the following that the VSSM is also related to the property of TCIE of the pre-committed efficient mean-variance policy.

Theorem 4.3.

The pre-committed efficient mean-variance policy (except for the minimum variance policy) in a cone constrained market is TCIE if and only if the variance-optimal signed supermartingale measure of this market satisfies:

| (18) |

or

| (19) |

where the stopping time is defined as

We can conclude from Theorem 4.3 that the pre-committed efficient mean-variance policy (except for the minimum variance policy) satisfies TCIE if and only if the conditional expectation of VSSM’s density (respect to the original probability measure) is nonnegative, or once the conditional expectation takes a negative value, it remains the same value until the terminal time.

It is also easy to see that condition (18) implies that and

In such a case, every mean-variance investor holds a long position of the effcieint risky portfolio , whose excess rate of return does not exceed 100% (), and achieves efficiency during the entire investment horizon.

The stopping time can be also expressed as

Then, condition (19) implies that for ,

and for ,

In this situation, every mean-variance investor starts from holding a long position of the efficient risky portfolio and switches all his wealth into the riskless asset once the excess rate of return of exceeds 100%, i.e., .

Theorem 4.3 shows that whether the pre-committed efficient mean-variance policy (except for the minimum variance policy) is TCIE only depends on the basic market setting (the distribution of excess rate of return and the portfolio constraint set ) and does not depend on the initial wealth level, , and the objective level which the investor aspires to achieve, . This clear recognition motivates us to consider active introduction of additional market constraints such that the phenomenon of time inconsistency in efficiency can be eliminated.

5 Elimination of time inconsistency in efficiency with portfolio constraints

From our discussion in the previous sections, it becomes clear that constraints on portfolio do have effects on TCIE. Suppose that a given discrete-time mean-variance problem is originally not TCIE. Are we able to eliminate the time inconsistency in efficiency by introducing suitable portfolio constraints into the market? We will demonstrate a positive answer to this question in this section.

Remark 5.1.

We proceed our investigation starting from an unconstrained market, then a market with no shorting, before dealing with a general cone constrained market.

i) Case of unconstrained markets:

If the market is constraint free, i.e., , we have

Therefore, the optimal mean-variance policy of is

where

| (20) |

which is exactly the result in Li and Ng (2000). We can assume here that . Otherwise, all efficient policies reduce to the one corresponding to investing only in the riskless asset.

Furthermore, the minimum-variance signed supermartingale measure in the unconstrained market is given by

which is exactly the variance-optimal signed martingale measure (VSMM) obtained in Schweizer (1995), Schweizer (1996) and Černý and Kallsen (2009).

Theorem 4.3 shows that the pre-committed efficient mean-variance policy (except for the minimum variance policy) in the unconstrained market satisfies time consistency in efficiency if and only if VSMM is a nonnegative measure for any , i.e.,

| (21) |

Actually, Cui et al. (2012) proved that condition (21) does not hold only if the market is an incomplete market and proposed a TCIE revised policy which i) achieves the same mean-variance pair as the pre-committed efficient policy does and ii) receives an additional positive free cash flow during the investment horizon.

ii) Case of markets without shorting:

Assume that shorting of risky assets is not allowed in the market, i.e., , and the expected excess rate of return of risky assets is nonnegative, i.e., . In this situation, we have

In addition, we also have

Therefore, the optimal policy of is

| (22) |

where

which is the result derived in Cui et al. (2014).

Furthermore, the variance-optimal signed supermartingale measure in such a market setting is given by

where

We can see that , . Therefore, according to Theorem 4.3, all pre-committed efficient policies are TCIE in a market with no shorting and with nonnegative expected excess rate of return.

We proceed now to a discussion for a general cone-constrained market setting.

Theorem 5.1.

If a convex cone is chosen to restrict portfolios such that the expected excess rate of return vector lies in the dual cone of , i.e.,

where , then the corresponding optimal discrete-time pre-committed efficient mean-variance policy is TCIE.

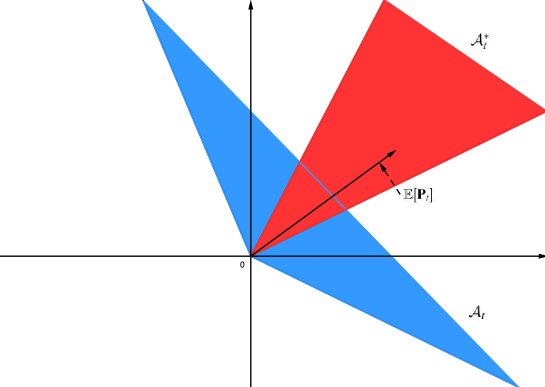

Figure 1 illustrates the above proposition graphically. Basically, this is an inverse process to find the convex cone . For a given market, is known. We first identify a cone such that . We then find another cone such that the selected becomes its dual cone. Apparently, the condition in Theorem 5.1 aims to enforce the inefficient risky portfolio equal to zero in order to achieve condition (19). Note that condition (18) is much harder to satisfy, as it is related to the distribution of excess rate of return which is uncontrollable in general.

Example 5.1.

We now consider an example of constructing a three-year pension fund consisting of S&P 500 (SP), the index of Emerging Market (EM), Small Stock (MS) of U.S market and a bank account. The annual rates of return of these three indices have the expected values, variances and correlations given in Table 1, based on the data provided in Elton et al. (2007).

| SP | EM | MS | |

| Expected Return | |||

| Variance | |||

| Correlation | |||

| SP | |||

| EM | |||

| MS | |||

We further assume that all annual rates of return are statistically independent and follow i) the identical multivariate normal distribution (with the statistics described above) or ii) the identical multivariate distribution with freedom 5 (and with the statistics described above) for all years, and the annual risk free rate is , i.e., , . We first compute , and as follows, for ,

| (23) |

In order to examine the phenomenon of time inconsistency in efficiency (by observing the number that the wealth level exceeds the threshold ), we simulate samples paths for each distribution assumption, with the setting of initial wealth equal to and the target expected return equal to .

Case 1: When the market is unconstrained, the optimal mean-variance policy of is

with (based on (20)) for both distribution assumptions. Apparently, under both the unbounded multivariate normal distribution and multivariate distribution, equation (21) does not hold, which implies that the time inconsistency in efficiency may occur. More specifically, recalling Theorem 3.1 and Lemma 3.1 and noticing with , the pre-committed efficient mean-variance policy does not satisfy TCIE if and only if the optimal wealth level exceeds the threshold

The simulation results show that the probabilities that exceeds the threshold are 0.055 for the multivariate normal distribution and 0.0558 for the multivariate distribution. This simulation outcome indicates that a distribution with a heavier tail tends to demonstrate a higher degree of time inconsistency in efficiency in an unconstrained market.

Case 2: To eliminate the time inconsistency in efficiency, we consider first to add the following cone constraint to the market,

which is a half-space with boundary that is a hyperplane orthogonal to . The dual cone of is

which is exactly the ray along (see Proposition 3.2.1 of Bertsekas (2003)). Notice that the constraint cone, , defined above is the largest cone (thus the loosest constraint) which we can identify to eliminate the time inconsistency in efficiency in this example.

Based on the proof of Theorem 5.1, we have for both distribution assumptions. By Lemma 2.1, we can compute numerically through penalty function method (see Appendix A of Cui et al. (2014)) with initial point as

| i) |

for the multivariate normal distribution and

| ii) |

for the multivariate distribution. The optimal investment policy is thus

| i) |

for the multivariate normal distribution and

| ii) |

for the multivariate distribution. The simulation shows that the probabilities that exceeds the threshold are 0.0559 for the multivariate distribution and 0.0533 for the multivariate distribution. Once exceeds the threshold , the investor puts all his wealth into the riskless asset, which eliminates the time inconsistency in efficiency in this example.

Case 3: In this case, we introduce into the market a more realistic convex cone constraint,

which implies that short selling is not allowed for the index of Emerging Market and the Small Stock of U.S market, and the negative position on S&P 500 cannot be too large. The dual cone of in this case is

Note that specifying at yields the ray along .

Based on the proof in Theorem 5.1, we have for both distribution assumptions. By Lemma 2.1, we can compute numerically through penalty function method (see Appendix A of Cui et al. (2014)) with initial point as

| i) |

for the multivariate normal distribution and

| ii) |

for the multivariate distribution. The optimal investment policy is thus

| i) |

for the multivariate normal distribution and

| ii) |

for the multivariate distribution. The simulation shows that the probabilities that exceeds the threshold are 0.0569 for the multivariate normal distribution and 0.0588 for the multivariate distribution and. Although, compared to the unconstrained case, both the probabilities increase, the investor puts all his wealth into the riskless asset immediately after exceeds the threshold .

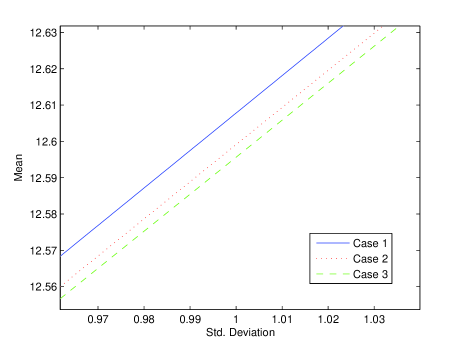

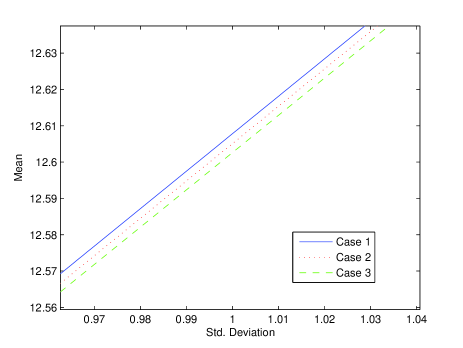

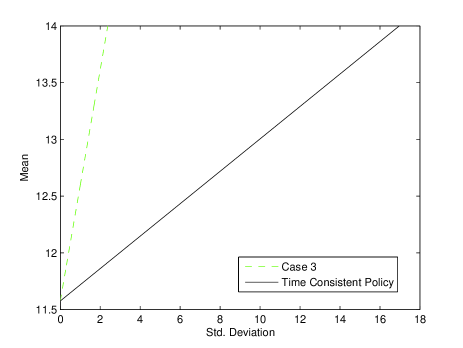

For the unconstrained market in Case 1, the expression of the efficient frontier achieved by the pre-committed policy is given in (76) in Li and Ng (2000). For cone constrained markets in Case 2 and Case 3, their efficient frontiers achieved by the pre-committed policy are given in Theorem 2.1 of this paper. For problem , we also derive in Appendix A9 of this paper its efficient frontier achieved by the time consistent policy proposed by Basak and Chabakauri (2010) and Björk et al. (2014), with its expression given in (40).

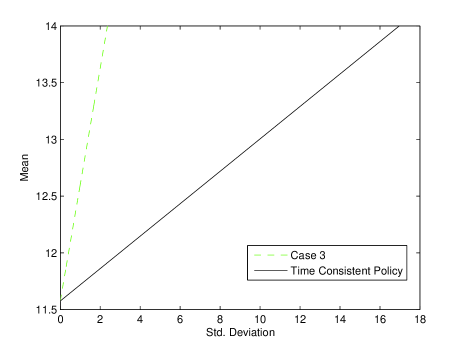

Figure 2 depicts the efficient frontiers in the mean-standard deviation space for Case 1, Case 2 and Case 3 and demonstrates a clear domination relationship among the three. Furthermore, Figure 3 illustrates a clear dominance relationship between Case 3 and the efficient frontier achieved by the time consistent policy. As both TCIE policies and the time consistent policy aim to align the inherently inconsistent global and local interests, they all sacrifice certain degrees of global performance, thus all being dominated by the pre-committed policy. Case 2 dominates Case 3 as Case 2 is associated with a looser constraint, while Case 3 is associated with a tighter constraint. It is interesting to note that both TCIE policies dominate the time consistent policy significantly, which indicates that insisting time consistency for an inherently time inconsistent problem may suffer a significant loss in its global performance. Expression (40) reveals that the time consistent policy achieves a good efficient frontier globally only if is large. In conclusion, by introducing appropriate constraints into the model, we can not only eliminate time inconsistency in efficiency, but also strick a good balance between the global and local mean-variance efficiency. Actually, relaxing the time consistency requirement to TCIE offers us a flexibility in deciding which level of a good global performance to maintain by introducing suitable portfolio constraints and deriving the corresponding pre-committed TCIE policy.

6 Conclusions

We have developed in this paper a complete answer to the following question: Given a financial market with its return statistics known, what are the cone constraints on portfolio policies or what additional cone constraints are needed to be introduced such that the derived optimal portfolio policy is time consistent in efficiency. There are three main contributions of the paper: i) analytical solution of the mean-variance formulation for discrete-time cone constrained markets; ii) complete characterization of time consistency in efficiency and its close relationship to the minimum-variance signed supermartingale measure; and iii) a systematic framework in guaranteeing time consistency in efficiency by enforcing suitable cone constraints on portfolios.

More specifically, we have investigated in this paper the discrete-time mean-variance portfolio selection problem formulation in a convex cone constrained market, have given the condition under which there exists an admissible policy, have derived analytically the pre-committed efficient mean-variance policy, and have identified the explicit conditions under which the pre-committed efficient mean-variance policy is TCIE. The derived optimal policy is of a two-piece linear form, and this fact reveals that in a cone constrained market, mean-variance investors may switch between one efficient risky portfolio and one inefficient risky portfolio depending on the individual’s current wealth level. Another prominent feature may also require our special attention: Market constraints make the current risky portfolios dependent not only on the current wealth level, but also on the future market conditions, even when the rates of return among different time periods are assumed to be independent.

Furthermore, we have extended the definition of variance-optimal signed martingale measure (VSMM) in unconstrained markets to minimum-variance signed supermartingale measure (VSSM) in constrained markets, and have derived the semi-analytical expression of VSSM’s density (respect to the original probability measure), which only depends on the basic market setting (including the distribution of the excess rate of return, , and the set of portfolio constraints, ). Our major finding demonstrates that the property of TCIE and VSSM are closely related, i.e., the pre-committed discrete-time efficient mean-variance policy (except for the minimum variance policy) satisfies TCIE if and only if the conditional expectation of VSSM’s density is nonnegative, or once the conditional expectation becomes negative, it remains the same negative value until the terminal time. This interesting finding is the first analytical result that explicitly assesses the impact of constraints on the property of time consistency in dynamic decision problems and motivates us to establish a general solution framework in constructing TCIE dynamic portfolio selection models by introducing suitable portfolio constraints. The semi-analytical expression of VSSM’s density may also benefit the research of mean-variance hedging in constrained markets.

An extension of our result to continuous-time cone constrained markets is straightforward, at least conceptually. On the other hand, if the rates of return among different periods are correlated, the problem will become more complicated and the idea of opportunity-neutral measure change in treating stochastic opportunity set in Černý and Kallsen (2009) may be helpful. The real challenge appears when considering general markets with convex portfolio constraints (may not be a cone type). In such a market, the pre-committed efficient mean-variance policy may depend on more than two risky portfolios, making the analysis much more complicated.

References

- Artzner et al. (2007) Artzner, P., F. Delbaen, J. M. Eber, D. Heath, and H. Ku (2007): Coherent multiperiod risk adjusted values and Bellman’s principle, Annals of Operations Research, 152, 5-22.

- Basak and Chabakauri (2010) Basak, S., and G. Chabakauri (2010): Dynamic mean-variance asset allocation, Review of Financial Studies, 23, 2970-3016.

- Bertsekas (2003) Bertsekas, D. P. (2003): Convex Analysis and Optimization, Athena Scientific.

- Bielecki et al (2005) Bielecki, T., H. Jin, S. Pliska, and X. Zhou (2005): Continuous-time mean–variance portfolio selection with bankruptcy prohibition, Mathematical Finance, 15, 213-244.

- Björk and Murgoci (2010) Björk, T., and A. Murgoci (2010): A general theory of Markovian time inconsistent stochasitc control problem, working paper. Available at SSRN: http://ssrn.com/abstract=1694759.

- Björk et al. (2014) Björk, T., A. Murgoci, and X. Y. Zhou (2014): Mean-variance portfolio optimization with state dependent risk aversion, Mathematical Finance, 24, 1-24.

- Boda and Filar (2006) Boda, K., and J. A. Filar (2006): Time consistent dynamic risk measures, Mathematical Methods of Operations Reseach, 63, 169-186.

- Carassus et al. (2001) Carassus, L., H. Pham, and N. Touzi (2001): No arbitrage in discrete time under portfolio constraints, Mathematical Finance, 11, 315-329.

- Černý and Kallsen (2009) Černý, A., and J. Kellsen (2009): Hedging by sequential regressions revisited, Mathematical Finance, 19, 591-617.

- Cherny (2010) Cherny, A. S. (2010): Risk-reward optimization with discrete-time conherent risk, Mathematical Finance, 20, 571-595.

- Cui et al. (2014) Cui, X. Y., J. J. Gao, X. Li, and D. Li (2014): Optimal multiperiod mean-variance policy under no-shorting constraint, European Journal of Operational Research, 234, 459-468.

- Cui et al. (2012) Cui, X. Y., D. Li, S. Y. Wang, and S. S. Zhu, (2012): Better than dynamic mean-variance: Time inconsistency and free cash flow stream, Mathematical Finance, 22, 346-378.

- Cuoco (1997) Cuoco, D. (1997): Optimal consumption and equilibrium prices with portfolio cone constraints and stochastic labor income, Journal of Economic Theory, 72, 33-73.

- Czichowsky (2013) Czichowsky, C. (2013): Time-consistent mean-variance portfolio selection in discrete and continuous time, Finance and Stochastics, 17, 227-271.

- Czichowsky and Schweizer (2010) Czichowsky, C., and M. Schweizer (2010): Convex duality in mean-variance hedging under convex trading constraints, NCCR FINRISK working paper No. 667, ETH Zurich.

- Czichowsky and Schweizer (2013) Czichowsky, C., and M. Schweizer (2013): Cone-constrained continuous-time Markowitz problems, Annals of Applied Probability, 23, 764-810.

- Duffie and Pan (1997) Duffie, D., and J. Pan, (1997): An overview of value at risk, The Journal of Derivatives, 4, 7-49.

- Elton et al. (2007) Elton, E. J., M. J. Gruber, S. J. Brown, and W. N. Goetzmann (2007): Modern Portfolio Thoery and Investment Analysis, John Wiley & Sons.

- Föllmer and Schied (2004) Föllmer, H., and A. Schied (2004): Stochastic Finance: An Introduction in Discrete Time, Berlin: de Gruyter.

- Jobert and Rogers (2008) Jobert, A., and L. C. Rogers (2008): Valuations and dynamic convex risk measures, Mathematical Finance, 18, 1-22.

- Labbé and Heunis (2007) Labbé, C., and A. J. Heunis (2007): Convex duality in constrained mean-variance portfolio optimization, Advances in Applied Probability , 39, 77-104.

- Li (1990) Li, D. (1990): Multiple objectives and nonseparability in stochastic dynamic programming, International Journal of Systems Science, 21, 933-950.

- Li and Haimes (1987) Li, D., and Y. Y. Haimes (1987): The envelope approach for multiobjective optimization problems, IEEE Transactions on Systems, Man, and Cybernetics, 17, 1026-1038.

- Li and Ng (2000) Li, D., and W. L. Ng (2000): Optimal dynamic portfolio selection: Multiperiod mean-variance formulation, Mathematical Finance, 10, 387-406.

- Li et al (2002) Li, X., X. Y. Zhou, and A.E.B. Lim (2002): Dynamic mean-variance portfolio selection with no-shorting constraints, SIAM Journal on Control and Optimization, 40, 1540-1555.

- Markowitz (1952) Markowitz, H. M. (1952): Portfolio selection, Journal of Finance, 7, 77-91.

- Napp (2003) Napp, C. (2003): The Dalang-Morton-Willinger theorem under cone constraints, Journal of Mathematical Economics, 39, 111 C126.

- Peng (1997) Peng, S. (1997): Backward SDE and related g-expectation. In N. El. Karoui, & L. Mazliak (Eds.), Backward stochastic differential equations, Pitman Research Notes Math. Ser. 364(pp. 141-159), Harlow: Longman Scientific and Technical.

- Pham and Touzi (1999) Pham, H., and N. Touzi (1999): The fundamental theorem of asset pricing with cone constraints, Journal of Mathematical Economics, 31, 265-279.

- Rockafellar (1970) Rockafellar, R. T. (1970): Convex Analysis, New Jersey: Princeton University Press.

- Rosazza Gianin (2006) Rosazza Gianin, E. (2006): Risk measures via g-expectations, Insurance: Mathematics and Economics, 39, 19-34.

- Schweizer (1995) Schweizer, M. (1995): Variance-optimal hedging in discrete time, Mathematics of Operations Research, 20, 1-32.

- Schweizer (1996) Schweizer, M. (1996): Approximation pricing and the variance-optimal martingale measure, Annuals of Probability, 24, 206-236.

- Schweizer (2010) Schweizer, M. (2010): Mean-variance hedging. In R. Cont (ed.) Encyclopedia of Quantitative Finance (pp. 1177-1181), Wiley.

- Sun and Wang (2006) Sun, W. G., and C. F. Wang (2006): The mean-variance investment problem in a constrained financial market, Journal of Mathematical Economics, 42, 885-895.

- Uryasev (2000) Uryasev, S. P. (2000): Probabilistic Constrained Optimization Methodology and Applications, Dordrecht: Kluwer Academic Publishers.

- Wang and Forsyth (2011) Wang, J., and P. A. Forsyth (2011): Continuous time mean variance asset allocation: A time-consistent strategy, European Journal of Operational Research, 209, 184-201.

- Xia and Yan (2006) Xia, J. M., and J. A. Yan (2006): Markowitz’s portfolio optimization in an incomplete market, Mathematical Finance, 16, 203-216.

- Zhou and Li (2000) Zhou, X. Y., and D. Li (2000): Continuous time mean-variance portfolio selection: A stochastic LQ framework, Applied Mathematics and Optimization, 42, 19-33.

- Zhu et al. (2003) Zhu, S. S., D. Li, and S. Y. Wang (2003): Myopic efficiency in multi-period portfolio selection with a mean-variance formulation. In S. Chen, S. Y. Wang, Q. F. Wu and L. Zhang (Eds.), Financial Systems Engineering, Lecture Notes on Decision Sciences, Vol. 2(pp. 53-74), Hong Kong: Global-Link Publisher.

- Zhu et al. (2004) Zhu, S. S., D. Li, and S. Y. Wang (2004): Risk control over bankruptcy in dynamic portfolio selection: A generalized mean-variance formulation, IEEE Transactions on Automatic Control, 49, 447-457.

Appendix:

A1: The proof of Lemma 2.1

Proof: From the definition in (3), it is easy to see that for all .

The first-order and second-order derivatives of with respect to are given, respectively, as follows,

Therefore, are strictly convex with respect to , which implies that are uniquely determined. Furthermore, are optimal if and only if

| (24) |

(see Theorem 27.4 in Rockafellar (1970)), which implies

| (25) |

due to the assumption that is a cone.

Then, we have

and

Therefore,

The equality holds in the above inequality if and only if . The situation for can be proved similarly.

A2: The proof of Theorem 2.1

Proof: Consider an auxiliary problem of by introducing Lagrangian multiplier ,

| (26) |

which is equivalent to the following formulation,

The above auxiliary problem can be further rewritten as

where

At time , we have

Thus, statement (27) holds true for time . Assume that statement (27) holds true for time . We now prove that the statement also remains true for time . Applying the recursive relationship between and yields

| (28) |

While , identifying optimal within the convex cone is equivalent to identifying optimal within the convex cone when we set . We thus have

From Lemma 1, the optimal control takes the following form,

Substituting back to the value function (28) leads to

When , identifying optimal within the convex cone is equivalent to identifying optimal within the convex cone when we set . We thus have

From Lemma 1, the optimal control takes the following form,

Substituting back to the value function (28) leads to

When , we can easily verify that is the minimizer. We can thus set

In summary, the optimal value for problem (26) is

| (31) |

which is a first-order continuously differentiable concave function. To obtain the optimal value and optimal strategy for problem , we maximize (31) over according to Lagrangian duality theorem. We derive our results for three different value ranges of .

i) .

The optimal Lagrangian multiplier takes zero value, i.e., . The optimal investment policy is thus , .

ii) .

When , i.e., , , we can take resulting . This means that does not have a feasible solution. When and , is a strictly concave function and is a decreasing linear function. The optimal Lagrangian multiplier satisfies

When and , are both strictly concave. The optimal Lagrangian multiplier satisfies

Therefore, the optimal mean-variance pair is presented by

iii) .

Similarly, when , does not have a feasible solution. When , the optimal Lagrangian multiplier satisfies

Then, the optimal mean-variance pair is presented by

Therefore, attains its maximum value at expressed in (6). Moreover, the optimal mean-variance pair of problem is presented by

Finally, the efficient frontier follows naturally from our above discussion.

A3: The proof of Theorem 3.1

Proof: Comparing Eq. (5) with Eq. (8), we can conclude that at time , the truncated pre-committed efficient mean-variance policy, , also solves when satisfies . Note from the discussion after Theorem 2.1 that the solution to is inefficient if and only if and (or equivalently, the solution to is efficient if i) , or ii) and ). When , we have

Therefore, when both and hold, the truncated pre-committed efficient mean-variance policy remains efficient for the truncated problem .

Similarly, when , we have

which implies that when both and hold, the truncated pre-committed efficient mean-variance policy switches to be inefficient for the truncated problem .

When , or , hold, we have , , i.e., the truncated pre-committed efficient mean-variance policy becomes the minimum variance policy for the truncated problem .

The proposition follows when combining the results for all the situations discussed above.

A4: The proof of Proposition 3.1

Proof: We only need to prove the first, the third and the fifth equalities.

Condition dictates the optimal policy at time as . The wealth level at time follows

which implies

Thus the first statement holds.

Condition dictates the optimal policy at time as . The wealth level at time is

which implies

Thus the third statement holds.

Condition dictates the optimal policy at time as . The wealth level at time is

which implies

Thus the fifth statement holds.

A5: The proof of Lemma 4.1

Proof: We solve both problems by duality theory. The dual problem of is

where the Lagrangian function is defined as

We also define

The first order condition of with respect to gives rise to

| (32) |

Note that if and only if .

Then we have

If , identifying optimal within the convex cone is equivalent to identifying optimal within the convex cone when we set . Then,

Therefore, attains its maximum at

| (33) | ||||

| (34) |

If , identifying optimal within the convex cone is equivalent to identifying optimal within the convex cone when we set . Then,

Now, attains its maximum when .

Substituting both (33) and (34) into (32) yields the expression of ,

and the optimal objective value of ,

Notice that if and only if .

Applying a similar approach to problem gives rise to the expression of and the corresponding optimal optimal value . Notice that if and only if .

A6: The proof of Theorem 4.1

Proof: The problem of finding the density of the minimum variance signed supermartingale measure is formulated as

| (35) |

We will prove by induction that the cost-to-go function of at time is given by

which implies (14).

At time , the statement holds true by recognizing . Assume that the statement holds true for time . We now prove that the statement also remains true for time .

At time , when , reduces to

On the other hand, when , reduces to

Then, the cost-to-go function becomes

Now the remaining part in our proof is to prove that

We will prove that

which implies the conditional expectation in (13).

When , the following is obvious,

Assume that at time our statement holds true, we prove now that the statement also holds for time , as

Therefore

A7: The proof of Theorem 4.3

Proof: Lemma 3.1 already states the necessary and sufficient condition under which the pre-committed efficient policy (except for the minimum variance policy) satisfies TCIE, which can be summarized as follows:

For ,

| or |

with .

If at time , , then

if and only if , (), .

Therefore, the necessary and sufficient condition can be reexpressed as

| or |

with .

A8: The proof of Theorem 5.1

Proof: Under the condition in the proposition, we have

which implies and for all .

A9: The time consistent policy of

In the solution framework proposed by Basak and Chabakauri (2010) and Björk et al. (2014), the so-called time consistent policy at time is derived by a backward induction, taking into account that optimal investment decisions have already been taken in the future. Thus, the time consistent policy is the collection of equilibrium strategies adopted by fictitious investors at different times in a sequential game. More specifically, the time investor considers the following problem,

| (36) |

We will prove by induction that the time consistent policy, the conditional mean and conditional variance of terminal wealth under time consistent policy are given as

| (37) | ||||

| (38) | ||||

| (39) |

where and

We start our proof from time where the investor faces the following optimization problem,

which can be solved by the Lagrangian method with its solution given as

Assume that at time , (37), (38) and (39) hold. Then at time , the investor faces the following optimization problem,

which is equivalent to

It is not difficult to verify the following optimal solutions for ,

Therefore, the efficient frontier of the time consistent policy is given as

| (40) |