Multi-period Trading Prediction Markets with Connections to Machine Learning

Abstract

We present a new model for prediction markets, in which we use risk measures to model agents and introduce a market maker to describe the trading process. This specific choice on modelling tools brings us mathematical convenience. The analysis shows that the whole market effectively approaches a global objective, despite that the market is designed such that each agent only cares about its own goal. Additionally, the market dynamics provides a sensible algorithm for optimising the global objective. An intimate connection between machine learning and our markets is thus established, such that we could 1) analyse a market by applying machine learning methods to the global objective, and 2) solve machine learning problems by setting up and running certain markets.

1 Introduction

Following the mainstream interest in “big data”, one valuable direction of machine learning is towards to building up distributed, scalable and self-incentivised systems which could organise for solving large scale problems. Recently, prediction markets (Wolfers and Zitzewitz,, 2004) show the promise of being the abstract framework for machine learners to design these systems. As one type of markets, prediction markets naturally introduce the concepts such as self-incentivised computation and distributed environment. Additionally, the close relationship between prediction markets and probabilities shed light on a new way of achieving probabilistic modelling (Storkey,, 2011).

Since Pennock and Wellman, (1996), researchers have spent decades on building connections between machine learning and prediction markets. However, this problem has still not been well solved. One reason is that the framework of prediction markets is somehow too flexible, and in order to analyse the markets for machine learning goals one has to first specify a market model to describe the prediction markets. The other reason is that given a market model, we may still not know what the market is doing, even if we understand agent behaviours and market mechanisms. As distinct from most machine learning methods which explicitly define and optimise certain objectives, markets only introduce local objectives to each individual agent. To interpret a market as a machine learning method, we have to find the global objective that the market aims to optimise. This idea motivates our work.

Instead of just focusing on market mechanisms (Chen and Vaughan,, 2010), we would like to incorporate the agents and analyse our market as a whole. This setting is similar to (Storkey,, 2011; Penna et al.,, 2012; Barbu and Lay,, 2012); but unlike Barbu and Lay, (2012), we will build a model on agent behaviours; and unlike Storkey, (2011) and Penna et al., (2012), we model agents using risk measures, which makes our markets analytical.

The novel results of this paper are:

-

•

establishing a new prediction market model which both inherits the strengths of prediction markets and has mathematical convenience;

-

•

giving explicitly the global objective that the market aims to optimise as a whole, and interpreting the market trading process as a sequential optimisation procedure of the global objective;

-

•

strengthening the intimate connections between machine learning and markets by showing that the market effectively solves the dual of certain machine learning problems.

2 A General Prediction Market Setup

Let be the space of all possible future states. We say a prediction market is built on if it trades securities associated with the future state . Specifically, securities are defined as a set of random variables . Each is a payment function, that is, one unit of this security will pay to the holder if turns out to be the future state. This definition is quite general, and securities defined in this way are also referred to as complex securities (Abernethy et al.,, 2013). We require that all securities (collected into the vector ) are linearly independent, that is, for , we have only if . If they are not, then we can always pick a subset of linearly independent securities from such that all the other securities in can be represented by the linear combination of (Kreyszig,, 2007). Therefore it is redundant to consider that are not linearly independent. As an example, the Arrow-Debreu security is a special case of complex securities. When the sample space is discrete and contains only finite number of states, Arrow-Debreu securities are a set of securities, in which the -th one pays one unit if the -th state is true: . Note that in general cases , e.g. when the value of is continuous, there will be infinite number of states but we always have a finite for practice.

Agents can only trade these predefined securities. The behaviour of an agent is characterised by its portfolio , where is the amount of money that the agent has, and is the amount of shares the agent holds in security . We collect all into vector . If an agent has a portfolio , the total payment of the securities is

| (2.1) |

where is in essence a random variable on . We call the risky asset because of its uncertainty and the risk-free asset. The gross payment is thus

| (2.2) |

which is also a random variable. We call the (gross) asset. Denote the set of all that are accessible for an agent, and similarly the set of all . Notice that since are linearly independent, there exists a unique map (bijection) between and via (2.1). Therefore a portfolio could also be represented by . In our setting , but it is possible to make more abstract, which is not a space spanned by a prefixed number of securities but allows new security types to be added on the fly. This discussion is beyond our scope.

A market consists of two processes, that 1) each agent chooses a portfolio it would like to hold, and 2) agents try to move to their preferred portfolio by trading. To describe the decision making process we need a model of portfolio selection, while to describe trading we need to specify a market mechanism. These two parts will be discussed in Section 3 and 4.

Later in this paper, when the context is clear we will omit parentheses and write a random variable in an uppercase letter, e.g. (except the securities, which are denoted by ), and use the lowercase of the same letter for the value of it, e.g. . We will also write functionals in letters without any parentheses.

3 Preferences on Assets

Agents select assets based on their preferences. An agent’s preference order of two assets is measured by a functional , such that the agent prefers one asset than the other asset if and only if , and that the agent is indifferent between and if and only if . There are plenty of theories on choosing and analysing a specific form of . These includes expected utility theory (EUT) (Von Neumann and Morgenstern,, 2007), dual utility theory (Yaari,, 1987), risk measures (Artzner et al.,, 1999), etc. EUT is perhaps the most popular theories in economics and game theory, while risk measures are commonly seen in finance literature. We choose to use risk measures to model agent behaviours. We introduce risk measures in this section, while putting the detailed justification of using risk measures and its relation to EUT in Section 6.

3.1 Risk measures

As is indicated by their name, risk measures assign higher scores to assets that are more “risky”. They can also be understood as measures of the potential loss of choosing certain asset. A (monetary) risk measure is defined as a functional such that is finite and satisfies the following conditions (Artzner et al.,, 1999):

- Translation invariance

-

If and , then

(3.1) - Monotonicity

-

If and , then

(3.2)

Here should be understood as , that is, with the probability of one that will generate a lower return than . Thus monotonicity indicates that an asset with a better return deserves a lower risk. Due to translation invariance, a risk measure maps any risk-free asset to itself, and is additive w.r.t. any risk-free asset. Therefore, the output of a risk measure has the same unit with a risk-free asset, and can be calculated like an asset.

The domains of risk measures and the preference functional are different, as risk measures are defined on while the space of assets that agent can hold is . Fortunately, we could easily extend the definition to the domain by applying translation invariance (3.1)

| (3.3) |

A corresponding can thus be obtained by .

Risk measures are very generic. In our discussion we will use both risk measures and a specific class of them, the convex risk measures (Föllmer and Schied,, 2002). A risk measure is convex if and

| (3.4) |

It says that the risk of a combination of two assets should not be higher than holding them separately. In other words, convex risk measures encourage diversification, which is a natural condition on risk measures.

3.1.1 Examples of risk measures

A famous non-convex risk measure is the Value at Risk (VaR) (Linsmeier and Pearson,, 2000), which outputs a threshold loss such that the probability of exceeding is smaller than a predefined level

| (3.5) |

A famous convex risk measure is the Entropic risk measure (Föllmer et al.,, 2004)

| (3.6) |

Here is the moment-generating function, and is the KL-divergence (and this is where “entropic” comes in). We mention that the second representation of holds for all convex risk measures, and this representation becomes the key to connecting the markets to machine learning (cf. Section 5).

3.2 Rational Choices

Recall that a portfolio that leads to a higher value of is preferred. Thus the favourite portfolio of an agent should be the one that maximises , which we denote by . The behaviour of choosing is called the rational choice, and an agent is rational if it always chooses as its trading goal. Since in our framework , a rational agent will choose will under the rule of

| (3.7) |

In a market an agent only cares about its own goal (3.7). It seems like this property prevents us from linking markets to machine learning methods, as the latter always aim to achieve certain global objectives. However, with a careful design, we can let our markets implicitly define global objectives and make an agent contributes to the global objective at the same time as it achieves its own goal.

4 Multi-period Trading Markets

In this section we will build our market, a multi-period trading market whose trades are driven by a market maker. “Multi-period” is used to indicate that the prices of the securities are allowed to vary at different time steps, and that agents can trade with the market maker in multiple times (Föllmer et al.,, 2004). The market maker is introduced to simplify the market mechanism and to make the market run efficiently.

It is difficult to characterise the trading process in the markets with unspecified mechanisms, and those markets may not run efficiently. For example, there may not exist a consistent agreement among agents on how much should be paid to buy/sell one share of a security. Moreover, one agent who wants to sell a certain amount of shares may not find any buyers (Chen and Pennock,, 2007). One way to simplify the trading process is by introducing a market maker (Hanson,, 2007). A market maker is a special agent. It is a price maker, who defines the price for trading each security. All agents are only allowed to trade with the market maker. They can, however, make a trade at any time as long as they agree to pay under the market maker’s pricing. The pricing rule of a market maker at time step is a functional . At different time steps the cost for purchasing an asset may be different, i.e. it may happen that when .

Suppose that an agent has a portfolio at time and it would like to buy from the market maker at . The agent cannot propose an arbitrary price for but has to accept the price provided by the market maker . The updated portfolio is thus restricted to , and the updated asset is restricted to . Now a rational agent only cares about choosing its optimal purchase amount such that is minimised:

| (4.1) |

This portfolio selection procedure leads to Algorithm 1.

We now consider a multi-period market which involves a set of agents and a market maker. Assume that at each round there is only one agent that trades with the market maker. This assumption indicates that each agent trades with the market maker separately, and they do not cooperate to make a joint purchase. is thus the trading queue of the market. Since there are multiple agents, we use an extra subscript to distinguish the portfolios of different agents. For example, an agent ’s portfolio at time is . The initial values are denoted with the subscript . We collect all into vectors and , respectively. We assume that agents do not bring in any risky asset at the beginning, which is a natural assumption since only the market maker can issue securities. This assumption means we have and so .

At time , only the agent updates its portfolio by trading with the market maker while all the other agents keep the same portfolios as at . Suppose the asset that the agent would like to purchase is , then for all

| (4.2a) | ||||

| (4.2b) | ||||

Algorithm 2 runs a multi-period trading market.

We can also split Algorithm 2 into two routines, in terms of the market maker and each agent, respectively (Algorithm 3 and 4). We say this to emphasise the fact that each agent in the market has its own objective (which is to achieve the optimal portfolio based on its unique preferences), plus a communication with the market maker.

4.1 Appropriate choice on the pricing rule

There has been plenty of work on studying the pricing rule of the market maker (Brahma et al.,, 2012; Pennock,, 2004). A popular class of mechanisms is Hanson’s market scoring rules (Hanson,, 2007). It is later formalised by Abernethy et al., (2013), who use a set of reasonable axioms to characterise the pricing mechanism. We apply their result to our framework.

Let be the trade with the market maker at time . Consider two situations: 1) a trade happens with the market maker in ; and 2) a trade happens with the market maker in and is immediately followed by another trade , where . A natural requirement is that the cost of purchasing should be equal to the total cost of purchasing and . If we accept this property, then we can always find a functional such that (Abernethy et al.,, 2013)

| (4.3) |

We say a pricing rule is path-independent if it has the form of (4.3), and reload the notation to represent .

5 The Machine Learning Objective of the Multi-period Trading Markets

Remember that the primary goal of this paper is to establish an intimate connection between machine learning and our new prediction markets model. Before we start to analyse the multi-period trading markets, we introduce the machine learning context for which we want our markets to be utilised. Many machine learning tasks could be interpreted under the following generic framework: given a set of data sampled from a space and a hypothesis space which contains a class of accessible probabilities on , we would like to find a probability from that can best describe the data. Usually we use a functional to characterise the “best” performance, such that the best probability is the one that minimises . Formally, this involves an optimisation problem

| (5.1) |

For specific problems in which the information comes from different parts of the data or the models, has a form of , the sum of a set of functionals which share the same domain (see examples in Section 7 for details). We will show that a multi-period market effectively defines and optimises a machine learning task whose .

The connection is established in two steps: first we show that the market does have a global objective, and then show that under mild conditions the market optimises the dual of a machine learning problem .

5.1 The global objective of a market

We show that a multi-period trading market minimises a global objective. The optimisation is done sequentially via the market trading dynamics, that is, an agent will contribute to minimising this global objective as long as it makes a trade with the market maker. This argument is formalised in the following

Proposition 1 (The global objective of a market).

A multi-period market (Algorithm 2) with a path-independent pricing rule market maker aims to minimise the global objective

| (5.2) |

by performing a sequential optimisation algorithm, which is implemented by the market trading process (cf. (4.1) and (4.2)):

| (5.3a) | ||||

| (5.3b) | ||||

| (5.3c) | ||||

| (5.3d) | ||||

If the algorithm converges at time , i.e. for all , then achieves a local minimum of the objective in (5.2).

Proof.

At time only agent will trade with the market maker, so . At time , for any agent all quantities calculated before can be treated as constants as they could no longer be modified. Therefore, the functional that is minimised in (5.3a) has the same optimal point with the following functional

| (5.4) |

Apply the property of translation invariance to , we have

| (5.5) |

Sum over all ’s and denote this summation by , which is a functional. Then

| (5.6) |

Here ’s are the optimal point obtained from (5.3a). Substitute (5.5) to (5.6)

| (5.7) |

Note that at time for any agent it makes no trade , and so

| (5.8) |

The first summation on RHS thus becomes

| (5.9) |

Since the pricing rule is path-independent, the second summation on RHS is

| (5.10) |

where and . Since and for any and , we have

| (5.11) |

Finally, substitute (5.1) (5.10) and (5.1) to (5.6) and merge the rest terms we can end up with

| (5.12) |

where . This is a sequential minimisation scheme for . Finally, if the market converges at time , we have and , leading to at a local minimum of . ∎

Proposition 1 is the key to understanding the market mechanism. Despite that the market is set up to let agents behave under their own preferences, the market mechanism ensures that a global objective is established, and that the agent will contribute to optimising the global objective at the same time as it optimise its own goal. The trading process thus provides a sensible algorithm for achieving this global objective.

5.2 A primal-dual representation via convex analysis

One concern is that (5.2) is not commonly seen in machine learning problems111However, to complete our discussion, we show one example that uses (5.2) in Section 7. A different view of this objective should somehow be introduced. In fact, under mild requirements on the form of risk measures and pricing rules, the global objective forms the dual of the optimisation problem . The requirement for the risk measures is convexity (3.4). The requirement for the pricing rules is that it is duality-based (Abernethy et al.,, 2013).

5.2.1 More on convex risk measures

Artzner et al., (1999) and Föllmer and Schied, (2002) show that a convex risk measure has a form

| (5.13) |

where is a set of probabilities on such that is absolutely continuous w.r.t. and is well defined. The risk measure decreases as increases but this effect is penalised by a functional . (5.13) is in essence a Legendre-Fenchel transform with a slight change on signs (Boyd and Vandenberghe,, 2004).

5.2.2 Duality-based pricing rules

We keep following the idea of Abernethy et al., (2013) and apply their duality-based pricing rules to our problem. The authors point out that duality-based pricing rules are well motivated as they meet some natural conditions such as no-arbitrage. A duality-based pricing rule is path-independent and has a form222Abernethy et al., (2013) represent markets in securities and shares . To be consistent with our framework we change the representation to assets (cf. Section 2).

| (5.14) |

where denotes the Legendre-Fenchel transform of . Note that in their work is required to be convex, but this condition could be relaxed since for any we could define to replace , as is always convex (as it is a conjugate dual) and .

5.2.3 The primal problem

Now we are ready to show

Proposition 2 (The primal problem).

For a multi-period market which involves agents who use convex risk measures in (5.13)and a duality-based pricing rule market maker in (5.14), its global objective is the dual of

| (5.15) |

where and are functionals that share the same domain . Specifically, in (5.14), and where is the penalty functional of agent .

Proof.

We use the generalised Fenchel’s duality (Shalev-Shwartz and Singer,, 2007) to derive the Lagrange dual problem of (5.15). The generalised Fenchel’s duality states that the dual of problem (5.15) is

| (5.16) |

where denotes the Legendre-Fenchel transform.

We construct the convex risk measure for each agent . use (5.13) and choose

| (5.17) |

For the pricing rule (5.14) we choose and obtain . Substitute them back to the dual problem (5.16) and we end up with

| (5.18) |

This matches the global objective (cf. (5.2)) with a different sign. The negation sign is necessary because the Lagrange dual problem lower bounds the primal one

| (5.19) |

and become exact when the strong duality holds (Boyd and Vandenberghe,, 2004). ∎

Proposition 2 gives us two ways of building the connection between markets and machine learning: 1) If we model a market using our framework, we could then figure out the global objective of the market and then the primal problem, which can be solved using machine learning methods. 2) More interestingly, given a machine learning problem of form (5.15), we could transform it to a market and solve the problem by running the market, during which we could take the advantage of some market properties, such as distributed environment and privacy, to gain extra benefits.

6 Related Work

The idea of building models for prediction markets and discussing their relation to optimisation is not novel, and a few significant progresses have been achieved in the past few years. We will discuss the work that is closely related to ours.

It is Chen and Vaughan, (2010) who first show that what scoring rule market makers do are effectively online no-regret learning. Their study focuses on the market makers while agents are not directly modelled, which motivates a framework for the whole market.

Storkey, (2011) defines and analyses a type of prediction markets based on definitions on the markets, securities, and agents. Agents are modelled by EUT, that is, an agent is rational by maximising its expected utility. By analysing the equilibrium status of the market the author shows that the market can aggregate beliefs from agents to output a probability distribution over the future events. The author does not discuss precise market mechanisms or give the global objective of the market, which makes it difficult to link these markets to optimisation procedures.

Another important progress is given by Penna et al., (2012), who apply the market scoring rules as the market mechanism to the framework of Storkey, (2011). The work shows that with a large population of agents whose portfolios are drawn from a demand distribution, the whole market implements stochastic mirror descent. One concern is that they suggest using EUT to model agents but they do not use it to solve the optimal portfolios for the agents. This problem is partially solved by Premachandra and Reid, (2013), who derives the solution for a certain type of expected utilities. A similar setting is also studied by Sethi and Vaughan, (2013). They focus more on the convergence of the market dynamics, and show how markets can aggregate beliefs by using numerical evidences.

6.1 Risk measures and EUT

Here we justify the choice of risk measures as the agent decision rules. First, the output value of a risk measure can be treated as a risk-free asset and standard linear operations are well defined for it. In comparison, an expected utility outputs a number that only has abstract meaning, i.e. to measure the degree of agent’s satisfaction. Additionally, risk measures force translation invariance by definition, but expected utility functions do not have this property in general. With the help of translation invariance, the wealth can always be separated from the risky asset , which implies that the optimal portfolio does not depend on . This saves us from the trouble of associating with the aggregation weights, as the relationship between them is highly inconsistent and varies dramatically under different utilities (Storkey et al.,, 2012). Finally, we could always derive convex a risk measure from any expected utility (Föllmer et al.,, 2004)

| (6.1) |

where is the personal belief of the agent. In fact, the output of this risk measure is the risk premium, the least amount of money that one would like to borrow in order to accept this risky asset. Then a sensible decision rule should be to find an asset that minimise the premium, which leads to our decision rule.

As an example, consider the HARA utility

| (6.2) |

The resultant convex risk measure is the one who has the following penalty functional

| (6.3) |

where . A special case of HARA is given by and , which leads to the exponential utility function . It is easy to check that the risk measure associated with exponential utility is exactly the entropic risk measure in (3.6) with (Föllmer and Schied,, 2002).

7 Examples

In this section we use three examples to illustrate the connections between the multi-period trading markets and machine learning.

7.1 Opinion Pooling

The opinion pooling problem is a common setting for prediction market models (Barbu and Lay,, 2012; Storkey et al.,, 2012). Garg et al., (2004) show that the objective of an opinion pool is to minimise a weighted sum of a set of divergences. Particularly, for logarithmic opinion pool the objective is to

| (7.1) |

where is the KL-divergence and are weight parameters.

Now consider an log-opinion pool of a set of probabilities on a finite discrete sample space with states. To set up a market that matches the log-opinion pool, we first define a market on the same space and introduce Arrow-Debreu securities. We introduce agents, and assign a unique probability to agent as its personal belief. According to (3.6), agent ’s risk measure has the form

| (7.2) |

where we let match the weight by . For the sake of simplicity, we choose a logarithmic market scoring rule market maker (Hanson,, 2007)

| (7.3) |

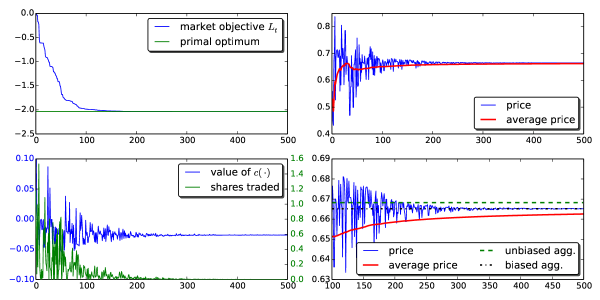

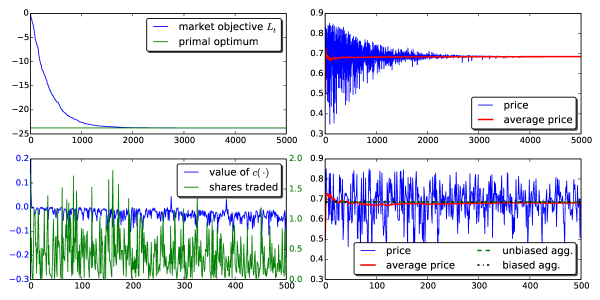

The market can be run by using Algorithm 2. Two typical simulation results are shown in Figure 1 and 2. The primal problem of this market is (applying Proposition 1 and 2)

| (7.4) |

where the domain is the probability simplex in dimensions and is the discrete uniform distribution in . In this case the optimal can be analytically solved. Recall that and we have

| (7.5) |

Since we introduce the market maker, the aggregated belief is not a pure weighted product of agents’ beliefs, but with a bias towards . However, when the population is sufficiently large such that , the effect of the market maker could be ignored and we will end up with a pure aggregation of agent beliefs (Penna et al.,, 2012).

7.2 Bayesian Update

We give our second example by first setting up a market and then match a machine learning problem to the market. Let’s build a market on a continuous sample space . We only define one security , and so the asset . We introduce only one agent. Again, the agent is characterised by an entropic risk measures, with coefficient and is the normal distribution. The moment-generating function in (3.6) is

| (7.6) |

and so the risk measure is . For the market maker we use the quadratic market scoring rule . Now we could run this market using Algorithm 2 with only one agent.

It could be shown that this market implements a Bayesian maximum a posteriori (MAP) update for the Gaussian, in which the prior is provided by the market maker and the likelihood information is provided by the agent.

Consider the setting of estimating a univariate Gaussian . All we need is the sufficient statistics calculated from a set of data points . For clarity of exposition let’s assume that we only care about the Bayesian updates of the mean parameter , and think is a prefixed constant. Introduce a Conjugate prior on the mean

| (7.7) |

where is so-called the pseudo count. The posterior is

| (7.8) |

where denotes the sample mean of the data set, and . If our goal is to calculate the MAP distribution then we have an optimisation problem

| (7.9) |

Let

| (7.10) |

and thus we have . Since and are convex, we could apply the Fenchel’s duality to the problem , which gives us the following dual problem

| (7.11) |

where is the Legendre-Fenchel transform of

| (7.12) |

and similarly . Choose the hyperparameter , and we finally have

| (7.13) |

This is exactly the agent’s objective. Since and are dual to each other, the market performs the Bayesian update (MAP estimate) in the dual space of the mean parameters.

7.3 Logistic Regression

In the third example we discuss a classic machine learning problem. Given a data set , we would like to build logistic regression model with -regularisation. The objective is

| (7.14) |

where is the norm.

To convert this problem to a market we use (5.2) and Proposition 1. Let the sample space be the space that generates the data and each future state is associated with a data in , . Define securities, each of which is . We introduce agents, such that the agent is only interested in trading in the -th security . Thus the shares of security held by agent is , and the asset is . The market inventory is . Let be the first term on the RHS of (7.14) and define the risk measure of agent as . We end up with

| (7.15) |

Now the market is ready to run under Algorithm 2. In order to show a slightly deeper connection to a specific learning method, we notice that the objective of agent at each round is . As the solution to this is not analytic, it is costly to solve for the exactly minimum of this objective at each time. To get rid of this problem, we could relax the condition that agents behaviour is rationally optimal, and let the agents accept a portfolio as long as it is better than its current position . Specifically agents can take steps towards the optimal solution. This can be achieved by the following portfolio updating rule

| (7.16) |

where is adjusted such that . In practice could be chosen by backtracking line search (Boyd and Vandenberghe,, 2004). The market we designed above effectively implements a coordinate descent algorithm (Luo and Tseng,, 1992).

Note that, instead of introducing agents, we can match the logistic regression problem by using only one agent and allowing it to trade all securities. This will result in a standard gradient descent method.

8 Conclusion

This paper establishes and discusses a new model for prediction markets. We use risk measures instead of expected utility to model agents, which results in an analytical market framework. We show that our market as a whole optimises certain global objective through its market dynamics. Based on this result, we make intimate connections between machine learning and markets.

One future work would be conducting a detailed analysis of this framework using the tools of convex optimisation (Boyd and Vandenberghe,, 2004). A particularly interesting topic is to find the conditions under which the market will converge. As we have observed, the stochasticity comes in when a large population of agents are involved, which is believed to be the nature of any real market (Penna et al.,, 2012).

Acknowledgement

This work was supported by Microsoft Research Cambridge through its PhD Scholarship Programme.

References

- Abernethy et al., (2013) Abernethy, J., Chen, Y., and Vaughan, J. W. (2013). Efficient market making via convex optimization, and a connection to online learning. ACM Trans. Econ. Comput., 1(2):12:1–12:39.

- Artzner et al., (1999) Artzner, P., Delbaen, F., Eber, J.-M., and Heath, D. (1999). Coherent measures of risk. Mathematical Finance, 9(3):203–228.

- Barbu and Lay, (2012) Barbu, A. and Lay, N. (2012). An introduction to artificial prediction markets for classification. Journal of Machine Learning Research, 13:2177–2204.

- Boyd and Vandenberghe, (2004) Boyd, S. P. and Vandenberghe, L. (2004). Convex optimization. Cambridge university press.

- Brahma et al., (2012) Brahma, A., Chakraborty, M., Das, S., Lavoie, A., and Magdon-Ismail, M. (2012). A bayesian market maker. In Proceedings of the 13th ACM Conference on Electronic Commerce, EC ’12, pages 215–232, New York, NY, USA. ACM.

- Chen and Pennock, (2007) Chen, Y. and Pennock, D. (2007). A utility framework for bounded-loss market makers. In Proceedings of the Twenty-Third Conference Annual Conference on Uncertainty in Artificial Intelligence (UAI-07), pages 49–56, Corvallis, Oregon. AUAI Press.

- Chen and Vaughan, (2010) Chen, Y. and Vaughan, J. W. (2010). A new understanding of prediction markets via no-regret learning. In Proceedings of the 11th ACM conference on Electronic commerce, EC ’10, pages 189–198, New York, NY, USA. ACM.

- Föllmer and Schied, (2002) Föllmer, H. and Schied, A. (2002). Convex measures of risk and trading constraints. Finance and Stochastics, 6(4):429–447.

- Föllmer et al., (2004) Föllmer, H., Schied, A., and Lyons, T. J. (2004). Stochastic finance: An introduction in discrete time. Springer, 2nd revised edition edition.

- Garg et al., (2004) Garg, A., Jayram, T., Vaithyanathan, S., and Zhu, H. (2004). Generalized opinion pooling. In AMAI.

- Hanson, (2007) Hanson, R. (2007). Logarithmic market scoring rules for modular combinatorial information aggregation. The Journal of Prediction Markets, 1(1):3–15.

- Kreyszig, (2007) Kreyszig, E. (2007). Introductory functional analysis with applications. Wiley. com.

- Linsmeier and Pearson, (2000) Linsmeier, T. J. and Pearson, N. D. (2000). Value at risk. Financial Analysts Journal, 56(2):pp. 47–67.

- Luo and Tseng, (1992) Luo, Z. and Tseng, P. (1992). On the convergence of the coordinate descent method for convex differentiable minimization. Journal of Optimization Theory and Applications, 72(1):7–35.

- Penna et al., (2012) Penna, N. D., Reid, M. D., and Frongillo, R. M. (2012). Interpreting prediction markets: a stochastic approach. In Pereira, F., Burges, C., Bottou, L., and Weinberger, K., editors, Advances in Neural Information Processing Systems 25, pages 3275–3283.

- Pennock, (2004) Pennock, D. M. (2004). A dynamic pari-mutuel market for hedging, wagering, and information aggregation. In Proceedings of the 5th ACM conference on Electronic commerce, EC ’04, pages 170–179, New York, NY, USA. ACM.

- Pennock and Wellman, (1996) Pennock, D. M. and Wellman, M. P. (1996). Toward a market model for bayesian inference. In Proceedings of the Twelfth international conference on Uncertainty in artificial intelligence, pages 405–413. Morgan Kaufmann Publishers Inc.

- Premachandra and Reid, (2013) Premachandra, M. and Reid, M. (2013). Aggregating predictions via sequential mini-trading. In the 5th Asian Conference on Machine Learning (ACML 2013).

- Sethi and Vaughan, (2013) Sethi, R. and Vaughan, J. W. (2013). Belief aggregation with automated market makers. Technical report, Microsoft Research New York.

- Shalev-Shwartz and Singer, (2007) Shalev-Shwartz, S. and Singer, Y. (2007). Convex repeated games and fenchel duality. In Schölkopf, B., Platt, J., and Hoffman, T., editors, Advances in Neural Information Processing Systems 19, pages 1265–1272, Cambridge, MA. MIT Press.

- Storkey, (2011) Storkey, A. (2011). Machine learning markets. In JMLR Workshop and Conference Proceedings, volume 15, pages 716–724.

- Storkey et al., (2012) Storkey, A., Millin, J., and Geras, K. (2012). Isoelastic agents and wealth updates in machine learning markets. In the 29th International Conference on Machine Learning (ICML 2012).

- Von Neumann and Morgenstern, (2007) Von Neumann, J. and Morgenstern, O. (2007). Theory of games and economic behavior (commemorative edition). Princeton university press.

- Wolfers and Zitzewitz, (2004) Wolfers, J. and Zitzewitz, E. (2004). Prediction markets. The Journal of Economic Perspectives, 18(2):107–126.

- Yaari, (1987) Yaari, M. E. (1987). The dual theory of choice under risk. Econometrica, 55(1):95–115.