Testing Composite Hypothesis based on the Density Power Divergence

Abstract

In any parametric inference problem, the robustness of the procedure is a real concern. A procedure which retains a high degree of efficiency under the model and simultaneously provides stable inference under data contamination is preferable in any practical situation over another procedure which achieves its efficiency at the cost of robustness or vice versa. The density power divergence family of Basu et al. (1998) provides a flexible class of divergences where the adjustment between efficiency and robustness is controlled by a single parameter . In this paper we consider general tests of parametric hypotheses based on the density power divergence. We establish the asymptotic null distribution of the test statistic and explore its asymptotic power function. Numerical results illustrate the performance of the theory developed.

AMS 2001 Subject Classification: 62F03, 62F35

keywords and phrases: density power divergence, linear combination of chi-squares, robustness, tests of hypotheses.

1 Introduction

Hypothesis testing is one of the fundamental paradigms of statistical inference. The likelihood ratio test is a key component of the classical theory of hypothesis testing; however, this test is known to be notoriously nonrobust under model misspecification and the presence of outliers. Many density based minimum distance procedures have been observed to have strong robustness properties in estimation and testing together with high efficiency, eg., Pardo (2006) and Basu et al. (2011). Among the available robust tests in the literature, those based on the class of disparities (Simpson, 1989 and Lindsay, 1994) are known to perform well in practical situations and have many theoretical advantages. However the effectiveness of these procedures in continuous models is tempered by the fact that it is necessary to construct a continuous density estimate of the data generating density as an intermediate step. The procedure thus becomes substantially more complicated and loses a part of its appeal. In contrast, none of the density power divergences require any density estimation to implement their minimization routines. Basu et al. (2013) considered parametric hypothesis testing based on the density power divergence for simple null hypotheses. In this paper we extend, in a nontrivial way, the problem for composite null hypotheses in general populations. To do that we have introduced the minimum density power divergence estimator restricted to a general null hypothesis, i.e. the restricted minimum density power divergence estimator. In order to derive the asymptotic distribution of the new family of test statistics proposed in this paper for testing composite null hypotheses, we need the asymptotic distribution of the restricted minimum density power divergence estimator. Thus the theoretical results presented in this paper require a fresh approach and represent a non-trivial generalization of the Basu et al. (2013) paper.

Let be some identifiable parametric family of probability measures on a measurable space , with an open parameter space Measures are assumed to be described by densities absolutely continuous with respect to a dominating -finite measure on . Let be a random sample from a density belonging to the family , where the support of the random variables is independent of the parameter . Consider a general null hypothesis of interest which restricts the parameter to a proper subset of , i.e.

| (1) |

In many practical hypothesis testing problems, the restricted parameter space is defined by a set of restrictions of the form

| (2) |

on , where is a vector-valued function such that the matrix

| (3) |

exists and is continuous in and rank. Here denotes the null vector of dimension , and the superscript in the above represents the transpose of the matrix.

In general, however, there are no uniformly most powerful tests for solving the class of problems formulated in (1). The canonical approaches for problems like these include the likelihood ratio test statistic, the Wald test statistic and the Rao test statistic; see, for instance, Silvey (1975). The tests based on disparities (or divergences), already mentioned earlier, also provide attractive theoretical alternatives for performing the above tests.

In this paper we will solve the hypothesis testing problem presented in (1) using the family of density power divergences. Let denote the set of all distributions having densities with respect to the dominating measure. Given any two densities and in , the density power divergence between them is defined, as the function of a nonnegative tuning parameter , as

| (4) |

The case corresponding to may be derived from the general case by taking the continuous limit as , and in this case is the classical Kullback-Leibler divergence. The quantities defined in equation (4) are genuine divergences in the sense for all and all , and is equal to zero if and only if the densities and are identically equal.

In Section 2 we introduce the restricted minimum density power divergence estimator (RMDPDE); we also study its asymptotic distribution and its relation with the minimum density power divergence estimator (MDPDE) in this section. The new family of test statistics and their asymptotic distributions are presented in Section 3. In Section 4 we describe the relation of the proposed test with the likelihood ratio test for the normal model, and in Section 5 we have considered testing hypotheses for the Weibull model. Numerical results including real data examples are presented in Section 6. The problem of tuning parameter selection is taken up in Section 7. Some concluding remarks are given in Section 8.

In the rest of the paper, we will frequently use the standard assumptions of asymptotic inference as given by Assumptions A, B, C and D of Lehmann (1983, p. 429). We will refer to them as the Lehmann conditions. Some of the proofs will also require the conditions D1–D5 of Basu et al. (2011, p. 304) which we will refer to as Basu et al. conditions. In order to avoid arresting the flow of the paper, these conditions have been presented in the Appendix.

2 Restricted Minimum Density Power Divergence Estimator

We consider the parametric model of densities ; suppose that we are interested in the estimation of . Let represent the distribution function corresponding to the density . The minimum density power divergence functional at is defined by the requirement . Clearly the term in (4) has no role in the minimization of over . Thus the essential objective function to be minimized in the computation of the minimum density power divergence functional reduces to

| (5) |

Notice that in the above objective function the density appears only as a linear term (unlike, say, the computation of the of the minimum Hellinger distance functional where the square root of the density is the relevant quantity). Thus given a random sample from the distribution we can approximate the above objective function by replacing with its empirical distribution function . For a given tuning parameter , therefore, the MDPDE of can be obtained by minimizing

| (6) |

over , where . In the special case , the objective function reduces to ; the corresponding minimizer turns out to be the maximum likelihood estimator (MLE) of . The minimization of the expression in (6) over does not require the use of a nonparametric density estimate of the true unknown distribution . Existing theory (e.g. De Angelis and Young, 1992) shows that in general there is little or no advantage in introducing smoothing for such functionals which may be empirically estimated using the empirical distribution function alone, except in very special cases. Using as a substitute for , if possible, is therefore a natural step.

Let be the likelihood score function of the model. Under differentiability of the model the minimization of the objective function in equation (6) leads to an estimating equation of the form

| (7) |

which is an unbiased estimating equation under the model. Since the corresponding estimating equation weights the score with the power of the density , the outlier resistant behavior of the estimator is intuitively apparent. See Basu et al. (1998) and Jones et al. (2001) for more details.

The functional is Fisher consistent; it takes the value when the true density is in the model. When it is not, represents the best fitting parameter. For brevity we will suppress the superscript in the notation for ; is the model element closest to the density in the density power divergence sense corresponding to tuning parameter .

Let be the true data generating density, and be the best fitting parameter. To set up the notation we define the quantities

| (8) | ||||

| (9) |

where , and is the so called information function of the model.

The following results, proved in Basu et al. (2011), form the basis of our subsequent developments.

Theorem 1

We assume that the Basu et al. conditions are true. Then

The above result is similar, in content and spirit, to those of White (1982). When the true distribution belongs to the model so that for some , the formula for , and simplify to

| (10) | ||||

| (11) | ||||

The restricted minimum density power divergence functional at , on the other hand, is the value in the parameter space which satisfies

provided such a minimizer exists. When a random sample is available from the distribution , the restricted minimum density power divergence estimator of minimizes (6) subject to . Under this set up we will determine, in the next theorem, the asymptotic distribution of the restricted minimum density power divergence estimator (RMDPDE) of .

Theorem 2

Assume that the Lehmann and Basu et al. conditions hold. Suppose that the true distribution belongs to the model, and is the true parameter. Then the minimum density power divergence estimator of obtained under the constraints of the null hypothesis has the distribution

where

| (12) |

| (13) |

and is as defined in (10), evaluated at .

Proof. See the Appendix.

3 Testing Parametric Composite Hypotheses using Density Power Divergence

Suppose is the unconstrained estimator of , whereas is the RMDPDE under the null hypothesis given in (1). In this section we will present the family of the density power divergence test statistics (DPDTS) for testing the composite null hypothesis in (1). This family of test statistics has the expression

| (14) |

where is given in (4). In the following theorem we present the asymptotic distribution of the family of DPDTS defined in (14).

Theorem 3

Assume that the Lehmann and Basu et al. conditions hold. The asymptotic distribution of defined in (14) coincides, under the null hypothesis given in (1), with the distribution of the random variable

where are independent standard normal variables, are the nonzero eigenvalues of and

| (15) |

The matrices and are defined by

| (16) |

and

| (17) |

In the above represents the true unknown value of .

Proof. See the Appendix.

Remark 4

The main point to note in the above proof is that it is by no means a trivial or simple extension of Theorem 1 of Basu et al. (2013). The proof of the latter theorem simply requires the results involving the unrestricted MDPD estimator which has been very well studied in the literature. In the present scenario, one has to deal with both the restricted and unrestricted MDPD estimators. The random nature of the second argument of the DPD makes the derivations substantially more complicated and entirely different techniques have to be applied to the proof of Theorem 3 in this paper. The restricted MDPD estimator which we have employed here only has a limited presence in the literature. In some sense Theorem 2 may also be considered to be a part of Theorem 3, but here we have presented them separately for pedagogical reasons as well as to keep a clear focus in our presentations.

Remark 5

We observe that the ranks of the matrices and are equal. Moreover, it can be easily shown that . So , i.e. there will be exactly non-zero eigenvalues.

Corollary 6

For the special case when we test the null hypothesis against under the model with unknown, the matrix has the form

so that the DPDTS has the same asymptotic distribution as that of , where is the only nonzero eigenvalue of the above matrix (equal to its th element). In particular when and , this eigenvalue becomes one, so that the DPDTS

| (18) |

has a simple asymptotic distribution. We will revisit this problem again in Section 4.

A simple approach to approximate the critical region of the DPDTS and perform the test could be the following. The eigenvalues described in Theorem 3 can be expressed as a function of the parameter . Under the null they can be consistently estimated by replacing in place of . Let represent the corresponding estimated eigenvalues. Generating independent observations from the distribution repeatedly, one can estimate the quantiles of the distribution of , where ’s are kept fixed during this exercise. The quantiles are then consistent approximations of the true quantiles of the asymptotic null distribution of the statistic in Theorem 3; the experimenter can then perform the test based on the critical values thus obtained. In particular when one can perform the test by comparing with the appropriate upper quantile of distribution. Tables of the cumulative distribution of are also available in Solomon (1960), Johnson and Kotz (1968), Eckler (1969) and Gupta (1963), which may be helpful in performing the test. Davies (1980) has proposed an algorithm to calculate the critical region corresponding to a linear combination of random variables. Several other conservative approximations of the critical value of the DPDTS are provided in Basu et al. (2013).

3.1 The Power Function

By Theorem 3 the null hypothesis should be rejected if where is the quantile of order of the asymptotic distribution of under . The following theorem can be used to approximate the power function.

Theorem 7

Suppose Lehmann and Basu et al. conditions are satisfied. Assume that is the true value of the parameter such that under . Suppose there exists such that the RMDPDE of satisfies . Further assume that

| (19) |

where and are appropriate matrices. Then, under , we have the following convergence

where

| (20) |

and

Proof. The result follows in a straightforward manner by considering a first order Taylor expansion of , which yields

Remark 8

On the basis of the previous theorem we get an approximation of the power function as

| (21) | |||||

where is the standard normal distribution function, is the quantile of order of the asymptotic distribution of under the null hypothesis, and is as defined in (20).

If some is the true parameter, then the probability of rejecting for a fixed size tends to one as . So the test statistic is consistent in the Fraser’s (1957) sense.

Obtaining the approximate sample size to guarantee a power of at a given alternative is an interesting application of formula (21). Let be the positive root of the equation

i.e.

where

and Then the required sample size is where is used to denote “integer part of”.

We may also find an alternative approximation of the power of at an alternative close to the null hypothesis. Let be a given sequence of alternatives, and let be the element in closest to in the Euclidean distance sense. One possibility to introduce contiguous alternative hypotheses is to consider a fixed and to permit to move towards as increases in the manner specified by the hypothesis

| (22) |

Theorem 9

Suppose that the model satisfies the Lehmann and Basu et al. conditions. Under the contiguous alternative hypotheses given in (22), the asymptotic distribution of coincides with the distribution of

where are independent standard normal variables, are the positive eigenvalues of , and the values of and are given by

Also is any square root of , and is the matrix of corresponding orthonormal eigenvectors.

Proof. See the Appendix.

From a practical point of view we will estimate the eigenvalues as well as and by their consistent estimators.

4 Normal Case: Connection with the Likelihood Ratio Test

Under the model, consider the problem of testing

| (23) |

where is an unknown nuisance parameter. In this case the unrestricted and null parameter spaces are given by and respectively. If we consider the function with , the null hypothesis can be written as

and we are in the situation considered in (23). We can observe that in our case Based on (6) and taking into account the fact that is the normal density with mean and variance , the estimator of is given by

where . Similarly, the estimator , when , will be obtained from

Simple calculations yield the expressions

and

Based on these matrices we get

On the other hand

and

| (24) |

which is identical to the matrix presented in Corollary 6. In order to apply the results of Theorem 3 in this connection, we need to get the expression of . As in Basu et al. (2013) we have

Using Corollary 6 and the single nonzero eigenvalue of the matrix given in (24), we then get

| (25) |

A special case of interest is the situation where and The likelihood ratio test for the problem under study is equivalent to the ordinary -test and one can determine the exact small sample critical values for this test. On the other hand the standard asymptotic formulation of the likelihood ratio test leads to the rejection of the null hypothesis when , where

is the likelihood ratio, and is the quantile of order for the distribution. The MLE of under the parameter space is

while the MLE under is

Straightforward calculations show that asymptotically we reject the null hypothesis when

| (26) |

This test may be looked upon as the asymptotic likelihood ratio test, as opposed to the usual -test which may be regarded as the exact version of the likelihood ratio test for the normal mean problem with unknown variance.

What is the relation of the test statistic given in (14) with the above test statistics? In the following we will demonstrate that for and , our test statistic coincides with the asymptotic likelihood ratio test described in (26). Note that the density power divergence for the case between the densities of two normal distributions with different means and variances is given by

Therefore for and , we get

A routine calculation shows that

so that

| (27) |

and by equations (26) and (27), the asymptotic likelihood ratio test statistic is exactly same as the DPDTS for and . Therefore when we are comparing the usual -test with the test statistic we are comparing an exact likelihood ratio test with an asymptotic likelihood ratio test.

5 Testing for the Weibull Distribution

While the normal model is the most important model where our methods are useful, it is also important to explore the applicability of the method in other models to demonstrate the general nature of the method. For this purpose we will include numerical results based on the Weibull distribution in our subsequent numerical study, together with the results on the normal model. Here we describe the statistic for the Weibull case. The probability density function of , a two parameter Weibull distribution, is given by

where , and the parameter space is given by . We are interested in testing

| (28) |

where is a nuisance parameter. Let us consider the function . Then, as in the normal case which was considered in Section 4, the null hypothesis can be written as

and

Let us define

and

It can be shown that

| (29) |

and

| (30) |

where denotes the gamma function. Note that . For the value of is calculated using numerical integration. Let us define

where , the score function of the Weibull distribution, is given by

Then it can be shown that

and

Now

| (31) |

| (32) |

and

| (33) |

Suppose we have two densities and from Weibull family, where and . If , then using (29) we get from equation (4)

| (34) |

where

The value of can also be calculated using numerical integration. For it can be shown that

| (35) |

Using equations (31)-(35) we calculate the test statistic as well as its asymptotic distribution.

Suppose and are the unconstrained estimators of and respectively, and is the RMDPDE of under the null hypothesis. For , the test statistic can be simplified as

where

6 Numerical Studies

In this section we provide some extensive numerical evidence of the performance of the proposed methods, demonstrating, in particular, their strong robustness properties. Notice that the test statistic depends on the data only through the value of the estimator (both unconstrained and constrained), so that the robustness of the test would appear to depend directly on the robustness of the estimator. However, it is still useful to develop actual theoretical robustness properties of the proposed tests. Fortunately there is a wealth of material available in this context which makes our work easy. Toma and Broniatowski (2011) and Toma and Leoni-Aubin (2010) have, in general, touched upon the issue of theoretical robustness properties of tests. They have considered several theoretical measures of robustness in this context. In a more limited, but a more focused setting Ghosh et al. (2015) have considered the robustness measures of test statistics based on the family of -divergences which include the DPD as a special case; in particular the influence functions of the tests and the so called level and power influence functions are derived. Taken together, the above references further reinforce the notion that the robustness of these tests are directly dependent on the robustness of the estimators as the influence function of the tests turn out to be directly related to the influence function of the estimators. The Ghosh et al. (2015) paper relates only to the case of the simple null hypothesis; however it is not difficult to intuitively see how the robustness of these tests extend to the case of the composite hypothesis. The theoretical robustness properties of some similar tests have been considered in the Ph.D. dissertation of Ghosh (2015). On the whole, there is substantial overall indication and evidence of the theoretical robustness properties of the tests under study. For the sake of brevity we do not repeat these results here, but concentrate instead on the performance of the tests as observed in simulations and actual real data examples.

6.1 Real Data Examples

6.1.1 Telephone-Fault Data

We consider the data on telephone line faults presented and analyzed by Welch (1987); the data were also analyzed by Simpson (1989). The data are given in Table 1, and consist of the ordered differences between the inverse test rates and the inverse control rates in 14 matched pairs of areas. A parametric approach to analyze this would be to model these data as a random sample from a normal distribution with mean and standard deviation . It is obvious that the first observation of this dataset is a huge outlier with respect to the normal model, while the remaining 13 observations appear to be reasonable with respect to the same.

Basu et al. (2013) provided a limited analysis of these data by testing simple null hypotheses under the normal model. They tested null hypothesis about the mean by assuming the variance to be known, and also tested null hypothesis about the variance by assuming the mean to be known. These are contrived situations, and are less meaningful than the more realistic situation where both parameters are unknown. In this paper we consider tests for the normal mean without assuming the scale parameter to be known.

For the full data, the -test for the null hypothesis against fails to reject the null due to the presence of the large outlier (two sided -value is 0.6584); however the robust Hellinger deviance test (Simpson, 1989) comfortably rejects the null (two sided -value based on the chi-square null distribution is 0.0061), as does the -test based on the cleaned data after the removal of the large outlier (two sided -value is 0.0076).

| Pair | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Difference | 3 | 59 | 83 | 93 | 110 | 189 | 197 | 204 | 229 | 289 | 310 |

|

|

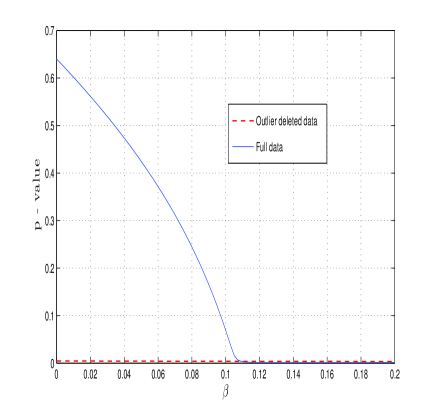

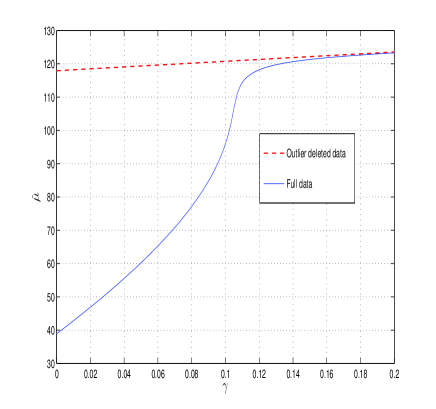

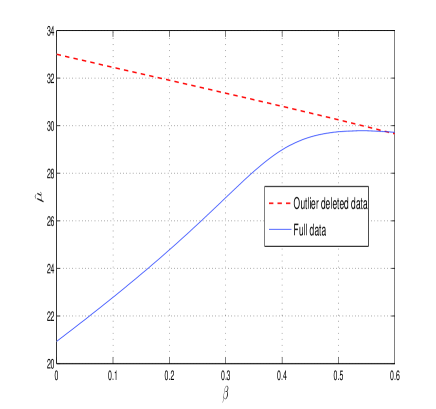

Under the normal model, the maximum likelihood estimates of (and ) are highly distorted due to the presence of the large outlier, and as a result the likelihood ratio test under the normal model fails to reject the null hypothesis. From the robustness perspective, this is precisely what we will like to avoid, and here we demonstrate that proper choices of the tuning parameter within the class of tests developed in this paper achieve this goal. Here we analyze the performance of the density power divergence tests with . Figure 1(a) represents the -values of the test versus for different values of in a region of interest. While it is clearly seen that the tests fail to reject the null hypothesis for these data at very small values of , the decision turns around sharply, as crosses and goes beyond 0.1. On the other hand, the -values of the same test based on the outlier deleted data remain stable, supporting rejection, at all values of (Figure 1(a)). The stable behavior of the test statistic based on the density power divergence for the full data approximately coincides with the stability of the density power divergence estimate of itself, obtained under a two-parameter normal model, which is presented in Figure 1(b). The minimum density power divergence estimators of for the full data and the outlier deleted data are practically identical for . At least in this example, the robustness of the test statistic is clearly linked to the robustness of the estimator.

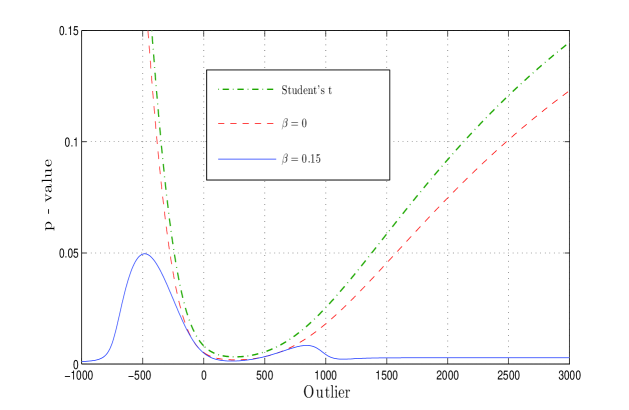

To further explore the robustness properties of the density power divergence tests we look at the two sided -values for different values of the outlier. For this purpose we vary the first outlying observation in the range from to 3000 by keeping the remaining 13 observations fixed. Figure 2 shows the corresponding -values of the density power divergence tests with as well as and the ordinary -test. It shows that initially the -value of the density power divergence test with increases as the first observation moves away from the center of the data set, but after a certain limit the test gradually nullifies the effect of the outlier. On the other hand, the -values of the -test and the density power divergence test with keep on increasing with the outlier on either tail. Indeed the -values of these two tests are remarkably close to each other.

6.1.2 Darwin’s Plant Fertilization Data

Charles Darwin had performed an experiment which may be used to determine whether self-fertilized plants and cross-fertilized plants have different growth rates. In this experiment pairs of Zea mays plants, one self and the other cross-fertilized, were planted in pots, and after a specific time period the height of each plant was measured. A particular sample of 15 such pairs of plants led to the paired differences (cross-fertilized minus self fertilized) presented in increasing order in Table 2 (see Darwin, 1878).

| Pair | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Difference | 6 | 8 | 14 | 16 | 23 | 24 | 28 | 29 | 41 | 49 | 56 | 60 | 75 |

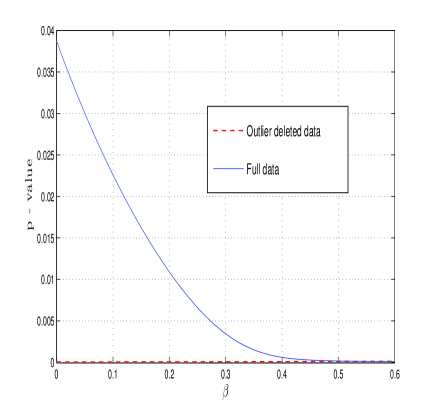

As in the previous example, we assume a normal model for the paired differences and test against , i.e. we test whether the mean of the paired differences is different from zero. The unconstrained minimum DPD estimates of under the normal model corresponding to different values of the tuning parameter are presented in Figure 3(b). The two negative paired differences appear to be geometrically well separated from the rest of the data, though they are perhaps not as huge outliers as the first observation in the telephone-fault data. These two observations do have a substantial impact on the parameter estimates and the test statistic for testing using density power divergence tests with very small values of , and it is instructive to compare to the case where these two outliers have been removed from the data. For small values of , the two sided -values of the test statistics are drastically different for the full data and outlier deleted cases (Figure 3(b)), but they get closer with increasing , and they essentially coincide for . Once again this seems to be directly linked to the robustness of the parameter estimates; Figure 3(b), which also depicts the progression of the parameter estimates for the outlier deleted data, clearly demonstrates that. For comparison we note that the two sided -values for the ordinary -test in this case are 0.0497 (for full data) and (for the cleaned data with the two outliers removed).

|

|

6.1.3 One Sided Tests

In general, the default alternative hypotheses considered in our proposed tests are of the two sided type. Depending on the nature of the problem and the dimension of the parameter, one sided alternatives may sometimes be of interest. For the telephone fault data the primary interest could be in determining whether the mean fault rate is higher than zero (rather than simply whether it is different from zero). It is presumable that Darwin’s interest in the fertilization problem was to determine whether cross fertilization leads to a higher growth rate compared to self fertilization; indeed the result of the test performed by R. A. Fisher (reported in Fisher, 1966) on the plant fertilization data relates to the one sided alternative. In this subsection we consider appropriate one sided tests for these two real data examples presented earlier in this section. For this purpose we consider the signed divergence statistic (the signed square root of the statistic presented in (25)) as was done in Simpson (1989). The relevant one sided -values are determined using the normal approximation, or that based on the -distribution. In the following we will describe the problem of testing against under the normal model with unknown scale.

The formal theory of constrained statistical inference (see Silvapulle and Sen, 2011) established the expression of the asymptotic likelihood ratio test for the hypotheses against to be

with asymptotic distribution equal to under , where a.s., is the indicator function and , are respectively the MDPDE and RMPDE for when the parameter spaces are the unrestricted and restricted ones of the two sided test (23). This test is almost the same as the one provided by the signed divergence likelihood ratio test statistic,

since the corresponding -values at are given by

where follows standard normal distribution. This means that if , both -values are equal, whereas for ,

Both tests are in practice equivalent, and such a difference for big -values comes from the fact that is formally more appropriate for against . We shall restrict ourselves, for simplicity, only to the signed divergence likelihood ratio test statistics and their DPD based analogues; the latter class of signed divergence DPDTS may be defined as

with asymptotic distribution equal to the standard normal under . In calculating the one sided -values based on the signed divergence Hellinger distance test in case of the telephone fault data, Simpson (1989) used an approximation based on the -distribution, as the sample size was only 14. In large samples, the distribution of the statistic is approximately normal. The problem for a normal distribution with dimension bigger than one with inequality restrictions is more complicated and requires a specific theory based on Silvapulle and Sen (2011). Martín and Balakrishnan (2013) illustrate the procedure of handing this problem when -divergence based test statistics and MLEs are applied.

Telephone-fault data The one sided -values for the signed divergence DPDTSs corresponding to and 0.3 are presented in Table 3 for the full as well as outlier deleted data, using both the standard normal () and (with suitable degrees of freedom) approximations. The result for the ordinary one-sided -test are also presented for comparison. The presence of the large outlier masks the significance in case of the -test, but the signed divergence DPDTSs provide consistent significant results with and without the outlier. Similar results were reported by Simpson (1989) with the signed divergence Hellinger distance test. The mean of the ordered differences between the inverse test rates and inverse control rates does appear to be greater than zero.

| Scenario | ||||||||

| cutoff | -test | DPD(0.15) | DPD(0.3) | |||||

| Full | Deleted | Full | Deleted | Full | Deleted | |||

| – | – | 0.0006 | 0.0019 | 0.0013 | 0.0017 | |||

| 0.3481 | 0.0037 | 0.0032 | 0.0068 | 0.0050 | 0.0064 | |||

Darwin’s plant fertilization data The results are presented in Table LABEL:tab:dar. The full data -value was reported by Fisher (1966). In this case the one sided -values for the -test lead to a shift from marginal significance to solid rejection due to the deletion of the (two) outliers. This also seems to be the case for signed divergence DPDTSs for very small values of . However, larger values of lead to a more consistent behavior of the tests. This dataset requires stronger downweighting compared to the telephone-fault data, as the outliers here are less extreme, and therefore more difficult to identify. Under a suitable robust test, it appears that the mean growth of cross fertilized plants would be declared to be significantly higher than self fertilized plants.

| Scenario | ||||||||

| cutoff | -test | DPD(0.15) | DPD(0.3) | |||||

| Full | Deleted | Full | Deleted | Full | Deleted | |||

| – | – | 0.0081 | 0.0017 | |||||

| 0.0252 | 0.0153 | 0.0008 | 0.0055 | 0.0009 | ||||

6.2 Simulation Results

6.2.1 Normal Case

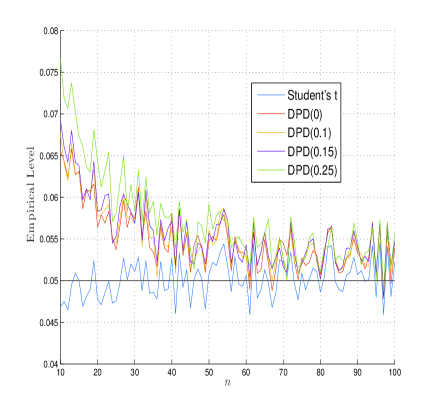

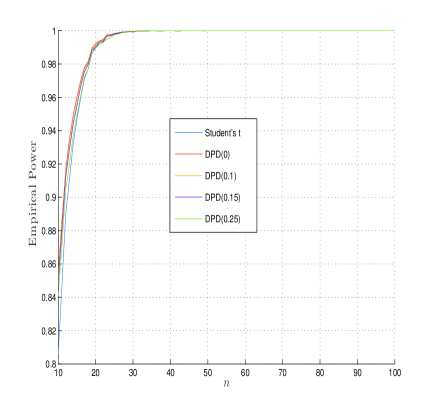

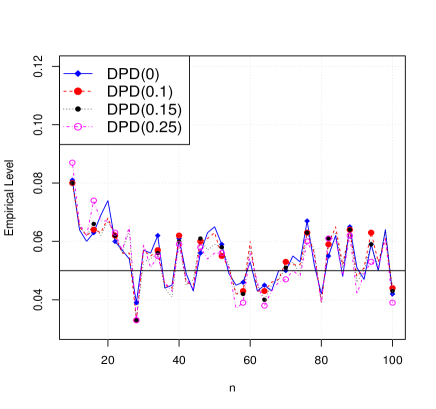

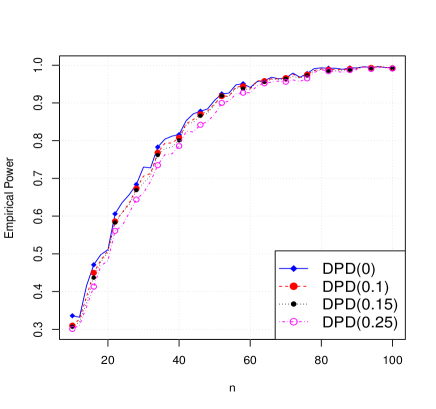

To further explore the performance of our proposed test statistic in case of the problem, we studied the behavior of the tests through simulation. We considered the hypothesis against the alternative with unknown when data were generated from the distribution. Subsequently, the same hypotheses were tested when the data were generated from the distribution. In the first case our interest was in studying the observed level (measured as the proportion of test statistics exceeding the chi-square critical value in a large number – here 10000 – of replications) of the test under the correct null hypothesis, and in the second case we were interested in the observed power (obtained in a similar manner as above) of the test under the incorrect null hypothesis. The results are given in Figures 4(a) and 4(b). In either case the nominal level was . We have used the ordinary -test together with several DPD test statistics, corresponding to and , in this particular study. The horizontal lines in Figure 4(a), and later in Figure 4(c), represent the nominal level of 0.05.

It may be noticed that all the tests excepting the exact likelihood ratio test (the -test) are slightly liberal for very small sample sizes and lead to somewhat inflated observed levels. However this discrepancy decreases rapidly, and by the time the sample size is 30 or more the observed levels have settled down reasonably around acceptable values. The observed powers of the tests as given in Figure 4(b) are, in fact, extremely close; in very small sample sizes the other tests have slightly higher power than the -test, but this must be a consequence of the observed levels of these tests being higher than the latter for such sample sizes. On the whole the proposed tests appear to be quite competitive to the ordinary -test for pure normal data.

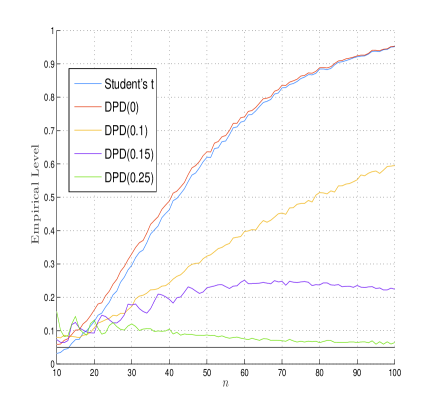

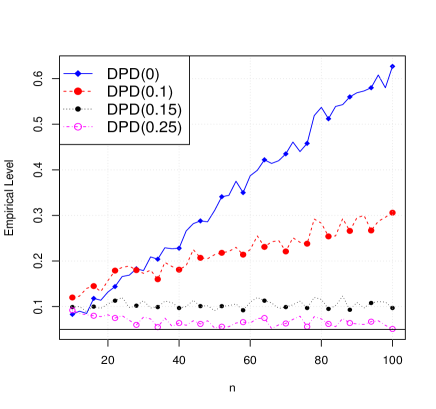

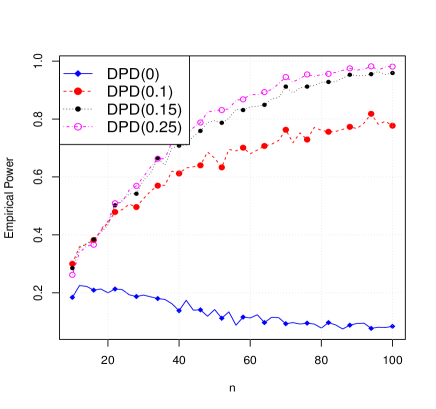

To evaluate the stability of the level of the tests under contamination, we repeated the tests for against under data generated from the mixture of and , where the mixing weight of the first component is 0.9. To illustrate the stability of power, the tests were performed with data generated under a mixture of and , where the mixing weight of the first component is again 0.9. The results are given in 4(c) and 4(d) respectively.

In this case there is a drastic and severe inflation in the observed level of the -test and that of the DPD(0) test. As increases, however, the resistant nature of the tests are clearly apparent. By the time , the levels have already been reduced to acceptable values. The opposite behavior is seen in case of power. There appears to be a complete breakdown in power for small values of , but the power remains quite stable for values of equal to 0.25 or greater.

On the whole it appears to be fair to claim that for sample sizes equal to or larger than 30 the efficiency of many of our DPDTSs are very close to the efficiency of the -test, but the robustness properties of our tests are often significantly better than the -test in terms of maintaining the stability of both the level and power.

|

|

| (a) | (b) |

|

|

| (c) | (d) |

|

|

| (a) | (b) |

|

|

| (c) | (d) |

6.2.2 Weibull Case

As we have mentioned before, it is important to demonstrate the properties of the proposed method in models other than the normal so that one has a better idea about the scope of the method. Accordingly we performed tests of composite hypotheses under the Weibull model in the spirit of Section 6.2.1. Let us consider the hypothesis defined in (28), where is taken to be 1.5. In the first study we have generated data from the distribution. The plot for the observed level for the hypothesis against the two sided alternative is given in Figure 5(a), where we have used 1,000 replications. Next the same hypotheses were tested when the data were generated from the distribution. The observed power function is plotted in Figure 5(b) for different values of . The powers are remarkably close. In all cases the nominal level was .

To evaluate the stability of the level and the power of the tests under contamination, we repeated the tests with data generated from the Weibull mixture consisting of 95% and 5% , and then from mixture of 95% and 5% . In either case the first larger component is our target. In Figures 5(c), the levels of the statistics under the contamination of first type are presented indicating the stability of levels for moderately large values of . Figure 5(d) demonstrates the stability of powers under contaminated data of the second type for the same values of .

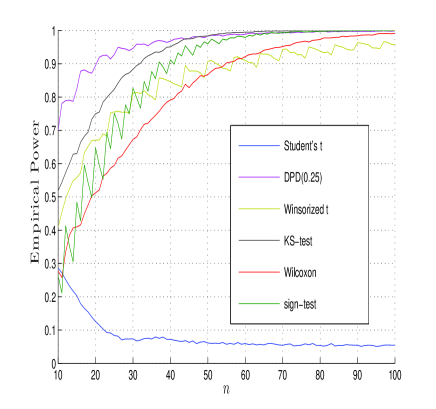

6.2.3 Comparison with Other Robust Tests

Here we provide a comparison of our proposed tests with some other popular resistant tests available in the literature. In particular we have used a parametric test – the Winsorized test of Dixon and Tukey (1968) together with three nonparametric tests – the one sample Kolmogorov-Smirnov (KS) test, the two sided Wilcoxon signed rank test and the two sided sign test. The model, the hypotheses, the parameters chosen, the level of significance and other details of the set up of this simulation are the same as those in Section 6.2.1.

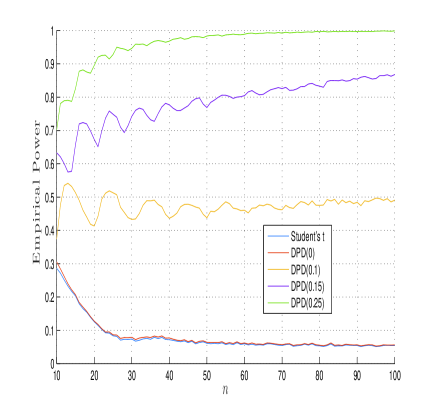

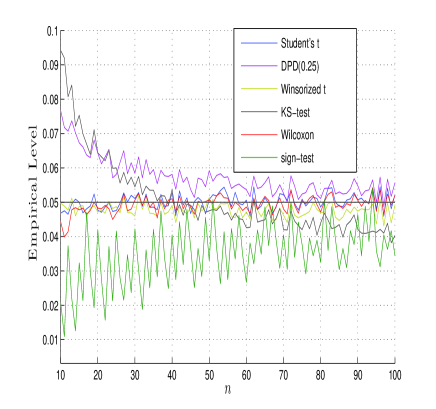

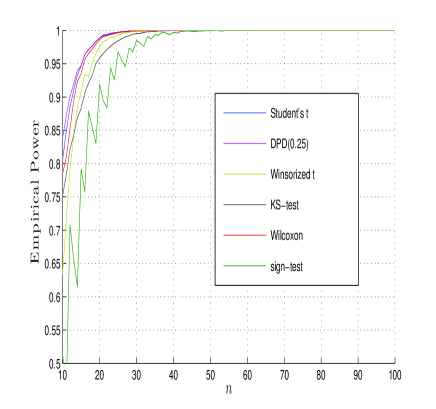

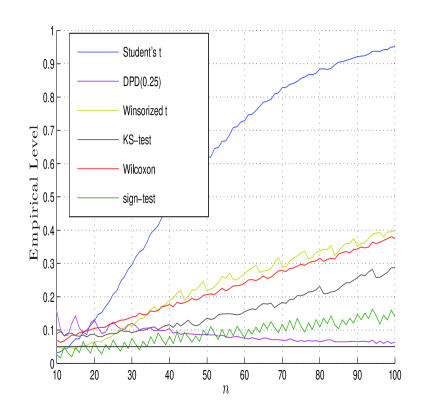

We have Winsorized the 15% extreme observations on each tail of the data distribution in case of the Winsorized -test. Note that the null hypotheses are slightly different for the nonparametric tests. For the KS-test we first standardize the data using robust statistics, and then test whether the corresponding distribution is a standard normal. The data are standardized using the transformation Here is the null value and is (median absolute deviation about the median). In case of the Wilcoxon test and the sign test we perform tests for the population median without making any parametric model assumptions. For comparison just one DPDTS is used in these simulations, that corresponding to the tuning parameter . To emphasize the robustness properties of these tests we have also included the Student’s -test in these investigations, so that the robust tests stand out in contrast. Our simulation results are presented in Figure 6.

From Figure 6(a) it may be observed that the empirical levels of the Winsorized -test, the KS-test and the Wilcoxon test are very close to the nominal level for pure normal data. For small sample sizes the DPDTS is slightly liberal; however even at a sample size of 30, it is off by only one percent compared to the nominal level. On the other hand the sign test is a bit conservative, even at fairly large samples. The observed powers of all the tests in Figure 6(b) rapidly approach unity in fairly small samples. The results in Figure 6(c) demonstrate that for contaminated data all tests except the DPDTS fail to maintain the nominal level. The observed level of the sign test is close to the nominal level for small sample sizes but eventually as the sample size increases it also breaks down. The powers of the tests for the contaminated data, plotted in Figure 6(d) show that all the robust tests exhibit stable power. For small sample sizes the DPDTS exhibits the highest power. The overall observation on the basis of all the above appears to be that the DPD based test is superior to the classical Wald test under contamination, and is also competitive or better than several other standard resistant tests in terms of robustness, at least to the extent this particular simulation study is concerned.

|

|

| (a) | (b) |

|

|

| (c) | (d) |

7 Choosing the Tuning Parameter

By construction, the test statistic in (14) employs two different tuning parameters and . These parameters have two different roles, in two different stages in the hypothesis testing process. The parameter is used to evaluate the robust unconstrained and constrained (under the null hypothesis) estimators. In the next stage a density power divergence with parameter is constructed to quantify the disparity between the fitted unrestricted and the restricted models. As seen in Theorem 3, the null distribution of the statistic can be derived for all values of the parameters , and in practice one can choose them independently of one another. As the robustness of the test statistic depends primarily on the robustness of the estimators, the choice of the parameter turns out to be more critical in our testing procedure. In repeated simulations (not presented here) our observation is that the parameter does not have a significant impact on the robustness of the procedure. Thus while the generality of the method allows us the choice of possibly different tuning parameters, for simplicity of implementation we will let , so that the selection problem reduces to that of a single parameter. Throughout the paper, we have used in our simulations and real data examples.

In a real situation, the experimenter will require some guidance on the choice of this single tuning parameter . Broniatowski et al. (2012) have reported that values of are often reasonable choices; we largely agree with this view, although tentative outliers and heavier contamination may require greater downweighting through a larger value of ; this is the case, for example, in Darwin’s plant fertilization data example. However, apart from fixed choices, other data driven and adaptive choices could also be useful, as one can then tune the parameter to make the procedure more robust as required. In this paper we follow the approach of Warwick and Jones (2005) for this purpose, which minimizes an empirical measure of the mean square error of the estimator to determine the “optimal” tuning parameter. This requires the use of a robust pilot estimator of the parameter. Warwick and Jones (2005) suggested the use of the MPDPDE corresponding to . The optimal parameter depends on the choice of the pilot estimator, however, and as larger values of lead to a loss in efficiency, Ghosh and Basu (2013) suggested the choice of the MDPDE with as the pilot estimator, which appears to be reasonable in most cases. Our subsequent analysis is based on the Warwick and Jones (2005) method, with the Ghosh and Basu (2013) modification.

We do acknowledge that the criterion to be considered for the choice of the optimal for the testing problem is not necessarily the same for the estimation problem. In hypothesis testing the appropriate criterion should involve a suitable linear combination of the inflation in the observed level under the null and the drop in power under contiguous alternatives in a contaminated scenario. However, an appropriate measure of this sort is not easy to construct. As it appears that the robustness of the proposed tests correspond almost exactly to the robustness of the MDPDEs, we feel that the optimal choice of as described in the previous paragraph would generally work reasonably well in case of the hypothesis testing problem also. As of now, we recommend the choice of according to the above recipe.

The above criterion leads to estimated optimal choices of to be 0.1919 for the telephone fault data, and 0.5657 for Darwin’s plant fertilization data respectively. As the first observation in the telephone fault data is a massive outlier, it is easily recognized by the testing procedures even at fairly small values of . However for Darwins’ plant fertilization data the outliers are more tentative, and therefore require stronger downweighting to eliminate their effect.

8 Concluding Remarks

This paper provides the appropriate theoretical machinery to perform general parametric tests of hypotheses based on the density power divergence. We demonstrate that one can construct a class of parametric tests of hypotheses based on the above measure which allows the experimenter to test for composite null hypotheses under the presence of nuisance parameters. The tests of this class have been shown to have excellent robustness properties in simulation studies and have a huge scope of application; for the purpose of numerical demonstration we have chosen the scenario of the usual -test and illustrated that for this situation the proposed test provides extremely satisfactory results. Similar improvements are also demonstrated outside the normal model, when data are generated from the Weibull distribution. When considered with the benefit of not requiring any intermediate smoothing technique as in the case of the Hellinger deviance test, our proposed techniques appear to prominently stand out among classes of robust tests for composite hypotheses. Our results also appropriately generalize the results of Basu et al. (2013).

Acknowledgments This work was partially supported by Grant MTM-2012-33740.

References

- Basu et al. (1998) A. Basu, I. R. Harris, N. L. Hjort, and M. C. Jones. Robust and efficient estimation by minimising a density power divergence. Biometrika, 85(3):549–559, 1998.

- Basu et al. (2011) A. Basu, H. Shioya, and C. Park. Statistical inference: The minimum distance approach. CRC Press, Boca Raton, FL, 2011.

- Basu et al. (2013) A. Basu, A. Mandal, N. Martin, and L. Pardo. Testing statistical hypotheses based on the density power divergence. Ann. Inst. Statist. Math., 65(2):319–348, 2013.

- Broniatowski et al. (2012) M. Broniatowski, A. Toma, and I. Vajda. Decomposable pseudodistances and applications in statistical estimation. J. Statist. Plann. Inference, 142(9):2574–2585, 2012.

- Darwin (1878) C. Darwin. The Effects of Cross and Self Fertilization in the Vegetable Kingdom. John Murray, London, 1878.

- Davies (1980) R. B. Davies. The distribution of a linear combination of random variables. Algorithm AS155. Appl. Statist., 29:323–333, 1980.

- De Angelis and Young (1992) D. De Angelis and G. A. Young. Smoothing the bootstrap. Internat. Statist. Rev., 60(1):45–56, 1992.

- Dik and de Gunst (1985) J. J. Dik and M. C. M. de Gunst. The distribution of general quadratic forms in normal variables. Statist. Neerlandica, 39(1):14–26, 1985.

- Dixon and Tukey (1968) W. J. Dixon and J. W. Tukey. Approximate behavior of the distribution of winsorized t (trimming/winsorization 2). Technometrics, 10(1):83–98, 1968.

- Eckler (1969) A. R. Eckler. A survey of coverage problems associated with point and area targets. Technometrics, 11(3):561–589, 1969.

- Fisher (1966) R. Fisher. The Design of Experiments. Hafner Press, New York, 1966.

- Fraser (1957) D. A. S. Fraser. Most powerful rank-type tests. Ann. Math. Statist, 28:1040–1043, 1957.

- Ghosh (2015) A. Ghosh. Robust Minimum Divergence Inference using Density Power Divergence and Its Extensions. PhD thesis, submitted to the Indian Statistical Institute, 2015.

- Ghosh and Basu (2013) A. Ghosh and A. Basu. Robust estimation for independent non-homogeneous observations using density power divergence with applications to linear regression. Electron. J. Stat., 7:2420–2456, 2013.

- Ghosh et al. (2015) A. Ghosh, A. Basu, and L. Pardo. On the robustness of a divergence based test of simple statistical hypotheses. J. Statist. Plann. Inference, 2015.

- Gupta (1963) S. S. Gupta. Bibliography on the multivariate normal integrals and related topics. Ann. Math. Statist., 34:829–838, 1963.

- Johnson and Kotz (1968) N. L. Johnson and S. Kotz. Tables of distributions of positive definite quadratic forms in central normal variables. Sankhyā, Series B, 30:303–314, 1968.

- Jones et al. (2001) M. C. Jones, N. L. Hjort, I. R. Harris, and A. Basu. A comparison of related density-based minimum divergence estimators. Biometrika, 88(3):865–873, 2001.

- Lehmann (1983) E. L. Lehmann. Theory of point estimation. Wiley Series in Probability and Mathematical Statistics. John Wiley & Sons Inc., New York, 1983.

- Lindsay (1994) B. G. Lindsay. Efficiency versus robustness: the case for minimum Hellinger distance and related methods. Ann. Statist., 22(2):1081–1114, 1994.

- Martín and Balakrishnan (2013) N. Martín and N. Balakrishnan. Hypothesis testing in a generic nesting framework for general distributions. J. Multivariate Anal., 118:1–23, 2013.

- Pardo (2006) L. Pardo. Statistical inference based on divergence measures. Chapman & Hall/CRC, Boca Raton, FL, 2006.

- Sen et al. (2010) P. K. Sen, J. M. Singer, and A. C. P. de Lima. From finite sample to asymptotic methods in statistics. Cambridge University Press, 2010.

- Silvapulle and Sen (2011) M. J. Silvapulle and P. K. Sen. Constrained statistical inference: Order, inequality, and shape constraints, volume 912. John Wiley & Sons, 2011.

- Silvey (1975) S. D. Silvey. Statistical inference. Chapman and Hall, London, 1975. Reprinting, Monographs on Statistical Subjects.

- Simpson (1989) D. G. Simpson. Hellinger deviance tests: efficiency, breakdown points, and examples. J. Amer. Statist. Assoc., 84(405):107–113, 1989.

- Solomon (1960) H. Solomon. Distribution of quadratic forms: tables and applications. Applied Mathematics and Statistics Laboratories, Stanford University Stanford, California, 1960.

- Toma and Broniatowski (2011) A. Toma and M. Broniatowski. Dual divergence estimators and tests: robustness results. J. Multivariate Anal., 102(1):20–36, 2011.

- Toma and Leoni-Aubin (2010) A. Toma and S. Leoni-Aubin. Robust tests based on dual divergence estimators and saddlepoint approximations. J. Multivariate Anal., 101(5):1143–1155, 2010.

- Warwick and Jones (2005) J. Warwick and M. Jones. Choosing a robustness tuning parameter. J. Stat. Comput. Simulation, 75(7):581–588, 2005.

- Welch (1987) W. J. Welch. Rerandomizing the median in matched-pairs designs. Biometrika, 74(3):609–614, 1987.

- White (1982) H. White. Maximum likelihood estimation of misspecified models. Econometrica, 50(1):1–25, 1982.

Appendix

There is some overlap between the Lehmann and Basu et al. conditions. In the following we present the consolidated set of conditions which are the useful ones in our context.

Lehmann and Basu et al. conditions

-

(LB1)

The model distributions of have common support, so that the set is independent of . The true distribution is also supported on , on which the corresponding density is greater than zero.

-

(LB2)

There is an open subset of of the parameter space , containing the best fitting parameter such that for almost all , and all , the density is three times differentiable with respect to and the third partial derivatives are continuous with respect to .

-

(LB3)

The integrals and can be differentiated three times with respect to , and the derivatives can be taken under the integral sign.

-

(LB4)

The matrix , defined in (8), is positive definite.

-

(LB5)

There exists a function such that for all , where for all , and , where is as defined in (6).

Proof of Theorem 2 This proof closely follows the approach of Sen et al. (2010). Let

| (36) |

be the function (6) divided by . By differentiating both sides of equation (36) with respect to we get

and differentiating again with respect to

Here and . We assume that the null hypothesis is true, and is the true value of the parameter. Since the model is correct converges in probability to

Notice that defined earlier in equation (10). Since represents the true distribution, some simple algebra establishes that

where is as defined in equation (11). Thus, asymptotically, has a distribution.

The restricted minimum density power divergence estimator of , i.e. , will satisfy

| (37) |

where is a vector of Lagrangian multipliers. Now we consider the Taylor expansion of about the point

| (38) |

where belongs to the line segment joining and . Now using the Khintchine’s weak law of large numbers we have

Therefore, from (38) we get

| (39) |

On the other hand, the Taylor expansion of about the point is

| (40) |

Combining equations (37) and (39) we have

| (41) |

The last expression also uses the fact that is an term. Similarly from (37) and (40) it follows that

| (42) |

Now we can express equations (41) and (42) in the matrix form as

Therefore

But

where and are as given in (12) and (13) respectively. The matrix is the quantity needed to make the right hand side of the above equation equal to the indicated inverse. Then

| (43) |

and we know

| (44) |

Proof of Theorem 3 Consider the expression . A Taylor expansion for an arbitrary , around leads to the relation

It is clear that , for each , and

Therefore,

Under

Using (43) and

we get

Therefore

| (45) |

On the other hand, . From equations (13) and (17) we have . Therefore it follows that

Now the asymptotic distribution of the random variables and

are the same because

Now we apply Corollary 2.1 in Dik and de Gunst (1985), which essentially states the following. Let be a -variate normal random variable with mean vector and variance-covariance matrix . Let be a real symmetric matrix of order . Let , and let be the nonzero eigenvalues of Then the distribution of the quadratic form coincides with the distribution of the random variable where are independent, each being a standard normal variable. In our case the asymptotic distribution of coincides with the distribution of the random variable where , are the nonzero eigenvalues of , where

Proof of Theorem 9 Notice that . From equation (45) we have

then

Under one has

and

We know that

Then, has the same asymptotic distribution as the quadratic form Now the result follows from Corollary 2.2 of Dik and de Gunst (1985): Let , a -variate normal distribution. Let be a real symmetric non-negative definite matrix of order . Let , , and let be the positive eigenvalues of . Then the quadratic form has the same distribution as the random variable

where are independent, each having a standard normal distribution. Values of and are given by

where is any square root of , and is the matrix of corresponding orthonormal eigenvectors. We therefore have the desired result.