Expert Opinions and Logarithmic Utility Maximization in a Market with Gaussian Drift

Abstract.

This paper investigates optimal portfolio strategies in a financial market where the drift of the stock returns is driven by an unobserved Gaussian mean reverting process. Information on this process is obtained from observing stock returns and expert opinions. The latter provide at discrete time points an unbiased estimate of the current state of the drift. Nevertheless, the drift can only be observed partially and the best estimate is given by the conditional expectation given the available information, i.e., by the filter. We provide the filter equations in the model with expert opinion and derive in detail properties of the conditional variance. For an investor who maximizes expected logarithmic utility of his portfolio, we derive the optimal strategy explicitly in different settings for the available information. The optimal expected utility, the value function of the control problem, depends on the conditional variance. The bounds and asymptotic results for the conditional variances are used to derive bounds and asymptotic properties for the value functions. The results are illustrated with numerical examples.

Key words and phrases:

Portfolio optimization, utility maximization, expert opinions, Kalman filter, partial information2010 Mathematics Subject Classification:

Primary 91G10; Secondary 93E11, 93E201. Introduction

We consider an investor who wants to maximize expected logarithmic utility of terminal wealth obtained by trading in a financial market consisting of one riskless asset and one stock. Stock returns satisfy

where is a Brownian motion, the volatility is constant, but the drift is some stochastic process independent of . Thus the drift is hidden and has to be estimated from the observed stock returns. The best estimate in a mean-square sense is the filter. While under suitable integrability assumptions we can get quite far in solving the utility maximization problem, see Björk, Davis and Landén [1] and Lakner [9], we need models which allow for finite dimensional filters to solve the problem completely including the computation of an optimal policy. Therefore, in the literature the drift process is either modeled as Ornstein-Uhlenbeck process (OUP) or as a continuous time Markov chain (CTMC). In both models finite-dimensional filters are well known, the Kalman and Wonham filters, respectively, see e.g. Elliott, Aggoun and Moore [5], Liptser and Shiryaev [11]. In these two models the utility maximization problem is solved, see Brendle [3], Lakner [10], Putschögl and Sass [13] and Honda [8], Rieder and Bäuerle [14], Sass and Haussmann [15], respectively.

However, to improve the estimate, an investor may rely on expert opinions. These provide a noisy estimate of the current state of the drift. For unbiased estimates, this reduces the variance of the filter. The better estimate then improves expected utility. This can be seen as a continuous time version of the static Black-Litterman approach which combines an estimate of the asset return vector with expert opinions on the performance of the assets, see Black and Litterman [2]. For a comparison with other Bayesian and robust Bayesian methods see Schöttle, Werner and Zagst [17].

Frey, Gabih and Wunderlich [6, 7] solve the case of an underlying CTMC. As an approximation, also expert opinions arriving continuously in time can be introduced. This allows for more explicit solutions for the portfolio optimization problem. Davis and LLeo [4] consider this approach for an underlying OUP, Sass, Seifried and Wunderlich [16] address the CTMC.

In this paper we look at the remaining case, an underlying OUP with time-discrete expert opinions. Due to the combination of continuous time-observations (stock returns) and discrete-time expert opinions, optimal portfolio policies are quite involved. We expect that for power utility they can be derived along the lines of [6, 7] using a stochastic control approach with an additional policy-dependent change of measure, cf. Nagai and Peng [12], and working with viscosity solutions. However, since our focus lies on explicit results and bounds on the improvement by expert opinions for different information regimes, we shall consider only logarithmic utility here. Explicit results for other utility functions are up to future research. On the other hand, an extension for logarithmic utility to the multivariate case, i.e., to markets with more than one risky asset, is straightforward. Filtering results and optimal policies can be derived analogously. But closed form solutions are no longer available for the conditional variances which then have to be computed numerically. Convergence results as in Section 4 would be more difficult to obtain.

The paper is organized as follows. In Section 2 we define the model for an OUP drift process and specify our concept of expert opinions. We introduce different settings for the available information which arises from observing the stock returns only (classical partial information), from expert opinions only and from the combination of stock returns and expert opinions. As reference we also consider full information. In Section 3 we state the classical Kalman filter for pure return observations and derive in the cases with expert opinion the filtering equations. In Section 4 we analyze the conditional variance in detail: In addition to staightforward bounds and monotonicity assumptions, Proposition 4.3 provides the limits for an increasing number of i.i.d. expert opinions for a finite time horizon and Proposition 4.6 provides tight asymptotic bounds for the conditional variance for regularly arriving expert opinions for an infinte time horizon. These properties and bounds are important since the optimal value is a function of the conditional variance. Our main result is Theorem 5.3 which provides for logarithmic utility explicit solutions in all four information settings. In the remainder of Section 5 we compare the optimal expected utilities (value functions) for the different cases. In Section 6 we provide extensive simulations and numerical computations to illustrate our theoretical results.

Summarizing, our contributions lie in (i) finding filtering equations in the settings with expert opinion, (ii) solving the -utility maximization problem with closed form solutions for optimal policies and values and (iii) deriving limits and bounds for the conditional variance and using these to compare different information settings.

2. Financial Market Model

For a fixed date representing the investment horizon, we work on a filtered probability space , with filtration satisfying the usual conditions. All processes are assumed to be -adapted.

Price dynamics

We consider a market model for one risk-free bond with prices and one risky security with prices given by

| (2.1) |

The volatility is assumed to be a positive constant and is an one-dimensional -adapted Brownian motion. The dynamics of the drift process are given by the stochastic differential equation (SDE)

| (2.2) |

where and are constants and is a Brownian motion independent of . Here, is the mean-reversion level, the mean-reversion speed and describes the volatility of . The initial value is assumed to be a normally distributed random variable independent of and with mean and variance . It is well-known that SDE (2.2) has the closed-form solution

| (2.3) |

This is a Gaussian process and known as Ornstein-Uhlenbeck process. It has moments

| (mean) | (2.4) | ||||

| (variance) | (2.5) | ||||

| (covariance function) |

for . It can be seen, that mean and variance approach exponentially fast the limits and , respectively, i.e. asymptotically for the drift has a distribution which is the stationary distribution. Starting with the stationary distribution leads to a (strict-sense) stationary drift process with mean and correlation function for .

We define the return process associated with the price process by . Note that satisfies and . So we have the equality This is useful, since it allows to work with instead of in the filtering part.

Investor information and expert opinions

An investor cannot observe the drift process directly. He has noisy observations of the hidden process at his disposal. More precisely we assume that the investor observes the return process and that he receives at discrete deterministic points in time with and noisy signals about the current state of . These signals or ”views” are interpreted as expert opinions and modelled by Gaussian random variables of the form with i.i.d. random variables independent of the Brownian motions and . So we assume that the expert’s views are unbiased, i.e., in expectation they coincide with the current (and unknown) value of the drift. The variance is a measure for the reliability of the expert: the larger the less reliable is the expert. Note that we always assume that an investor knows the model parameters, in particular the distribution of the initial value . Setting we can model a known (deterministic) initial value of the drift.

The information available to an investor can be described by the investor filtration for which we consider four cases , where

and where we assume that the -algebras , are augmented by the null sets of , e.g., . Note that . and correspond to an investor who observes only returns or expert opinions, respectively. describes the information arising from the combination of returns and expert opinions. Finally, describes an investor who has full information on the drift process . For stochastic drift full information is unrealistic, but we use results obtained for as reference points for the corresponding results in the other cases, e.g. when defining the efficiency in Section 6.

3. Partial Information and Filtering

The filter for the drift is the projection on the -measurable random variables. It is given by the conditional expectation and is optimal estimate in the mean-square sense. In the following we discuss the four cases , .

Return observations only ()

If the investor only observes the returns and has no access to the additional expert opinions, his information is given by . Then the drift process and return process are jointly Gaussian and hence the conditional distribution of given is completely described by the conditional mean and the conditional variance . The dynamics of and are given by the well-known Kalman filter, see e.g. Liptser and Shiryaev [11], which consists of the following SDE for

| (3.1) |

and a deterministic ODE for the conditional variance

| (3.2) |

hence is deterministic. The above ODE is known as Ricatti Equation and has for initial value the unique non-negative solution (see e.g. Lakner [10])

| (3.3) |

with , .

Only expert opinions ()

If the investor’s estimate on the drift is based only on expert opinions arriving at discrete points we have information . For the conditional mean and the conditional variance we have the following result.

Lemma 3.1.

-

(i)

Between two information dates and it holds for , that is Gaussian with

(3.4) (3.5) -

(ii)

At the information dates it holds that is Gaussian with

(3.6) (3.7) For we set and .

Proof.

Since the expert opinions arrive at discrete points in time it holds for . Then we have and . According to (2.3) we get

Therefore, and

where we used the martingale property of the stochastic integral and the Itô-Isometry. This yields the representations in (3.4) and (3.5).

The updating formulas (3.6) and (3.7) can be seen as an update of a degenerate discrete-time Kalman filter, see e.g. formulas (5.12) and (5.13) in Section 4.5 of Elliott, Aggoun and Moore [5]. It is degenerate here, since there is no evolution in time from to . Alternatively the updating formulas may be computed directly as a Bayesian update of given the -distributed expert opinion, cf. Theorem II.8.2 in Shiryaev [18].

Remark 3.2.

The updating formula (3.6) for the conditional mean shows that the filter after arrival of the -th expert opinion is a weighted mean of the filter before the arrival and the view of the expert’s view. The weight decreases with decreasing reliability (i.e increasing confidence) of the expert. So more weight is given to the view. For the limiting case (expert has full information) we have and . For we have and , i.e., there is no impact of the expert’s view since it carries no information on the unknown drift .

From updating formula (3.7) for the conditional variance it can be seen that , i.e. the extra information never increases the conditional variance. For the limiting case we have while for we have . Again there is no impact of the expert’s view.

Return observations and expert opinions ()

This combination of the settings and is the case we are mainly interested in. An investor typically uses all available information, stock returns and expert opinions.

Lemma 3.3.

-

(i)

Between two information dates and it holds for , that is Gaussian and satisfies

(3.8) (3.9) and initial values and , . The constant is given in (3.3) and for

(3.10) - (ii)

Proof.

Between two information dates and we are in the standard situation of the Kalman filter with Gaussian initial values , for signal and filter and deterministic value for the conditional variance. Since no additional expert opinions arrive in only the returns contribute to the investor filtration and we have for . So (3.8) and (3.9) follow immediately from the the corresponding Kalman filter equations (3.1) and (3.3).

Remark 3.4.

We obtain and from and given in the above Lemma for the limiting case . Then between the information dates is governed by the deterministic ODE while the conditional variance satisfies the linear ODE . Solving these equations yields the expressions given in Lemma 3.1. The interpretation of this limiting case is that the volatility is such high that no additional information can be retrieved from observing the stock returns and thus it is enough to consider the expert opinions.

Full information ()

For information it obviously holds , i.e. the conditional variance is zero. Below we will study the conditional variances and and show, that these values tend to zero if the number of information dates tends to , i.e. asymptotically the value for full information is obtained.

4. Properties of the Conditional Variance

As a special feature of the filters using , , which we considered in Section 3, we have a conditional variance which is deterministic as it is known for the standard Kalman filter (case ). This leads to the following result for the second-order moment of the filter which will play a crucial role in the proof of our main result in Theorem 5.3.

Lemma 4.1.

For the second-order moment of the filter , where , it holds for all

| (4.1) |

Proof.

The next proposition formally states an intuitive property of the filters namely that additional information on the unknown drift leads to an improvement of the drift estimate. This improvement can be measured by the conditional variance of the filter . We compare an investor observing both returns and expert opinions (H=C) with an investor who has access to only one of these sources of information (H=R,E).

Proposition 4.2.

It holds for all

Proof.

Between two information dates and the conditional variances for satisfy the ODE

with initial value where the r.h.s. of this ODE is given by (see Ricatti equation (3.2) and Lemma 3.3) and (see Remark 3.4). It is well-known that this ODE has a unique solution.

For the proof of we first note that . It holds . This implies that starting with coinciding initial values the solutions of the above ODE satisfy on . This inequality also holds after the update at since for and is increasing in . Iterating these arguments for yields for all .

For the proof of we observe that and . The uniqueness of the solution of the above ODE yields that the inequality for the initial values is inherited to the solutions on , i.e. it holds . Then also , the conditional variance after the update at time , satisfies

Iterating this argument for yields for all .

The next Proposition formalizes another intuitive property of the filters. If the number of expert opinions tends to infinity, i.e., the extra information arrives more and more frequent, then in the limit for we arrive at the case of full information about the unknown drift. This case is characterized by a vanishing conditional variance yielding in the limit a perfect estimate of , see Remark 4.4 below.

Proposition 4.3.

Asymptotics for

Let be a sequence of partitions of the interval into subintervals with mesh size

and such that information dates are retained, i.e., for . Moreover, let be a sequence of corresponding variances of the expert opinions at time . Assume that there is some constant such that for all and .

Then it holds for the conditional variances and , which correspond to these expert opinions, that for all

Proof.

Since , see Proposition 4.2, we can restrict to the proof of the assertion for . Moreover, we restrict to expert opinions with constant uncertainties . Then dominates the conditional variance in the case where expert variances are smaller than and the general assertion follows. We shall write for keeping the dependency on in mind.

For the dynamics of we have from Lemma 3.1 for and any

| (4.2) |

and

| (4.3) |

Since it follows from (4.2), (4.3)

| (4.4) |

Iterating this inequality and denoting yields for

| (4.5) |

for .

Now, let and . We have to show that we can choose such that . By we denote the index for which .

Suppose that for all there exists such that

| (4.6) |

Then we would get and thus by (4.5) with one iterations less

| (4.7) |

Since the bound for is strictly less than 1, independent of and is increasing in with for , the right hand side of (4.7) is decreasing and converges to for . In particular, we can choose such that . But this is a contradiction to the assumption in (4.6).

Therefore, there exists an such that for all there exists some index with

. For each we choose as the maximal index for which , i.e. is the last information time before (or equal) where the conditional variance before the update is smaller than .

If then (4.4) with implies that for large enough we have and the claim follows.

Otherwise, i.e. if then we have for that and thus as above.

We choose such that .

An iteration as in (4.5) starting with initial time and initial value (instead of and ) and using the upper bound for as in (4.7) yields finally for all

Remark 4.4.

Note that for full information we have for all . So Proposition 4.3 shows that and converge to for increasing the number of expert opinions. In particular this shows that we gain full information in the limit. More precisely, by increasing the number of expert opinions we get an arbitrarily sharp estimate of .

For Proposition 4.6 we need for the existence of the limits some monotonicity properties of the conditional variances.

Lemma 4.5.

Between the informations dates, i.e. for , we have

-

(i)

for that is decreasing, if , and increasing, if , where is given in (3.3),

-

(i)

and for that is decreasing, if , and increasing, if .

Proof.

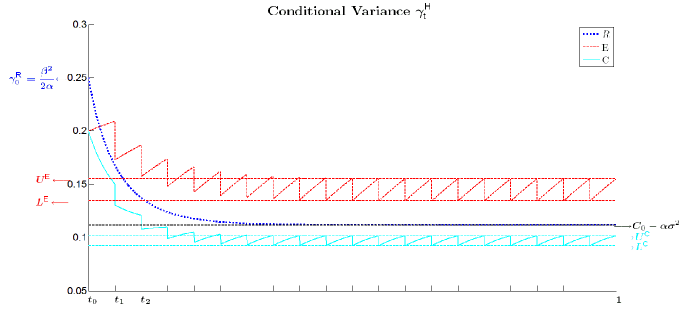

For the following proposition we consider an infinite time horizon . Note that the filtering equations in Lemma 3.1 and Lemma 3.3 up to each remain valid. It turns out that the asymptotic bounds, which we derive for the conditional variance for an infinite time horizon and with equidistant information times, give quite accurate approximations also for the finite horizon case, see e.g. Figure 1.

Parameters:

Proposition 4.6.

Asymptotics for

Consider the model as above but with an infinite time horizon and assume that the expert opinions arrive at equidistant information dates with some . First, without expert opinions () we have

| (4.8) |

where as in (3.3).

For let and for .

Then it holds for the conditional variances

| (4.9) |

Proof.

For the proof of assertion (4.9) we observe that there exists some index such that for the conditional variance is increasing between two information dates and . To prove this, note that

and

Since by Lemma 4.5 and are decreasing on as long as they lie above these boundaries and , respectively, iterating the updating formulas in Lemma 3.1 and Lemma 3.3 yields

Since , finally falls below the corresponding bound and with a similar argument as above then stays below this boundary. By Lemma 4.5, is increasing between the information dates below this boundary and thus a as stated above can be found in both cases.

Moreover, is bounded from below by , and hence for we have and . One can further show that the sequences and are either decreasing or increasing (the latter when starting with small ). Therefore, the limits exist and we have

For , Lemma 3.1 yields for the conditional variances before the update at the information dates , ,

where , and for Lemma 3.3 yields

Hence, can be expressed as

and . Since the limits and exist, we can substitute in the above equations for and in the updating formula , given in (3.7) and (3.11), first for and and second for to compute the limits. Therefore, and satisfy

Substituting the second into the first equation yields after some algebra the quadratic equation for with coefficients given in the proposition. Since it holds and and , hence there is one negative and one positive real solution. We are only interested in the positive solution which is given by yielding the expression in the proposition. The expression for follows from the updating formula.

A detailed look at the formulas for and in Proposition 4.6 reveals:

Corollary 4.7.

5. Portfolio Optimization Problem

Now that we have the filtering results at hand, it is quite straightforward to compute the optimal strategy and explicit representations for the value functions for our four cases of for logarithmic utility. This illustrates the influence of the expert opinions.

We describe the self-financing trading of an investor by the initial capital and the -adapted trading strategy where represents the proportion of wealth invested in stocks at time . It is well-known that in this setting the wealth process of the portfolio has the dynamics

| (5.1) |

We denote by

the class of admissible trading strategies, where .

We assume that the investor wants to maximize the expected logarithmic utility of terminal wealth. The optimization problem thus reads

| (5.2) |

where is called the value of the optimization problem for given initial capital . This is a maximization problem under partial information since we have required that the strategy is adapted to the investor filtration . In particular we are interested in an optimal strategy which attains the optimal value, i.e., .

Proposition 5.1.

The optimal strategy for problem (5.2) is

Proof.

From (5.1) it follows that

For we have , hence the latter integral is a martingale, in particular . Therefore, using a Fubini argument, the tower property of conditional expectations and that is -measurable, we get

| (5.3) | |||||

From (4.1) we have , where and are bounded, hence and the stated strategy is indeed admissible. Moreover, for all the quantity maximizes the integrand in (5.3) pointwise, which implies that is the maximizer of .

Remark 5.2.

If the drift is observable, then the optimal strategy is well-known: at time one has to invest the fractions of wealth in the risky stocks. So for logarithmic utility the so-called certainty equivalence principle holds, i.e. the optimal strategy under partial information is obtained by replacing the unknown drift by the filter estimate in the formula for the optimal strategy under full information. Note that this principle is no longer valid for other utility functions, e.g. for power utility, see Brendle [3], Lakner [10], Sass and Haussmann [15]).

Now we can state our main result which provides closed form expressions for the optimal values of the considered utility maximization problem under partial information.

Theorem 5.3.

Proof.

Substituting the optimal strategy given in Proposition 5.1 into the expression for in (5.3) yields

where we have used the expression for given in Lemma 4.1. Evaluating the integral using the expressions for the mean and variance of the drift given in (2.4) and (2.5) yields the expression (5.3) for . Finally, evaluating the integral using the expressions for given in (3.3), for and given in Lemma 3.1 and 3.3 and yields the formulas for in the theorem.

Remark 5.4.

-

(1)

Initializing the filter with the stationary distribution of the drift, i.e. , simplifies the expression for in Theorem 5.3 yielding

-

(2)

The well-known result for the classical Merton problem with constant drift can be obtained as special case by setting and . Then the optimal strategy is and the optimal value is simply .

Properties of the value function

We can now use Theorem 5.3 and the properties of derived in Section 4 to compare the value functions.

Corollary 5.5.

It holds

Proof.

From Theorem 5.3 we have the representation

The inequality given in Proposition 4.2 which holds for all yields the assertion.

Corollary 5.6.

Asymptotics for

Under the assumptions of Proposition 4.3 and denoting the value functions corresponding to expert opinions as specified in that proposition by and ,

we get

6. Numerical Results

In this section we illustrate the findings of the previous sections. The numerical experiments are based on a financial market model where the drift follows an Ornstein-Uhlenbeck process as given in (2.2) and (2.3), volatility is constant and the interest rate equals zero. For simulated drift process, stock prices and expert opinions we consider the maximization of expected logarithmic utility of terminal wealth. We assume that expert opinions with normally distributed views arrive at equidistant information dates and that their variances are constant, i.e. . If not stated otherwise we use the model parametes given in Table 1 in the subsequent simulations.

| Investment horizon | year | Drift: | Mean | |||

|---|---|---|---|---|---|---|

| Stock volatility | Mean reversion speed | |||||

| Expert’s variance | Volatility |

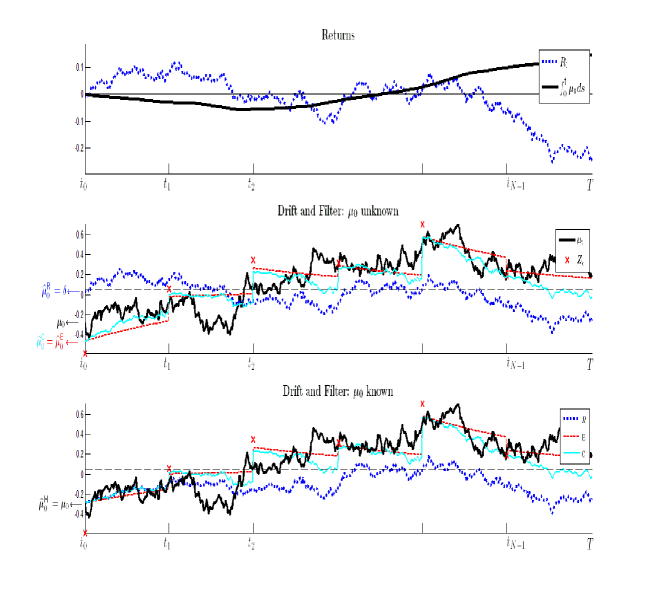

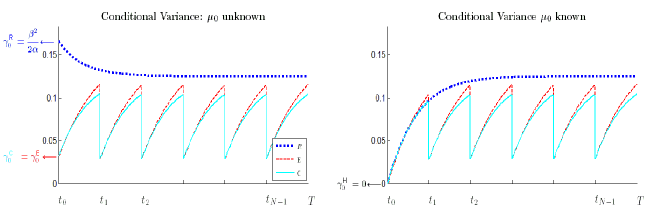

Filter

Figure 2.2 shows the filter and the conditional variance for . Note that for (full information) the filter coincides with the drift process while . The upper panel shows the simulated path of the return process from which the filter is computed. The plot also shows the path of which would be the return process for . In the second panel the initial value is assumed to be unknown and its distribution is the stationary distribution. Here the initial value of the filters is . The conditional variance, shown in the lower left panel, starts with the stationary variance, i.e. . Note that for the first update is at time and we have and . In the third panel we assume a known (deterministic) initial value . So at time also for we have full information on the drift and it holds and .

For emphasizing the effect of the filter updates due to the expert opinions we have chosen , which is quite small and corresponds to a very reliable expert. In the second and third panel the expert views are marked by red crosses. It can be seen that for the conditional variance jumps down in the information dates and the filter is quite close to the actual value of the drift . Between the information dates increases and the filter is driven back to its mean . While the conditional variances start for unknown resp. known initial value with different initial values the lower panel shows that quickly reaches the asymptotic value and also the asymptotic upper and lower bounds for and from Proposition 4.6 apply even for small times.

1. panel: return and (return for )

2. panel: drift and filters for unknown initial value

3. panel: drift and filters for known initial value

4. panel: conditional variances for unknown/known (left/right)

Parameters as in Table 1,

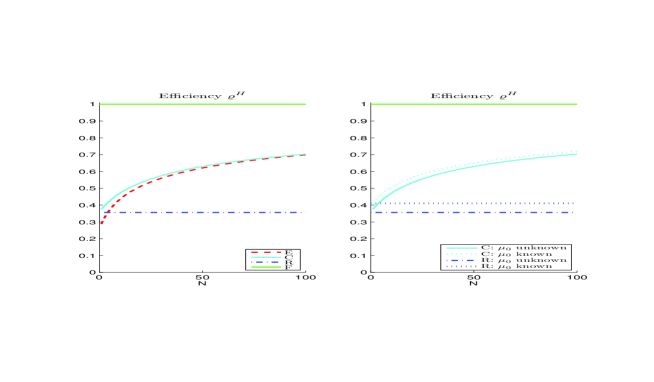

Efficiency

In order to quantify the monetary value of information contained in the observations of stock returns and expert opinions and in particular the value of the additional information due to the expert opinions, we compare four investors maximizing their expected log-utility from terminal wealth. First, the “fully informed” or –investor can observe the drift. Second, the –investor has only access to expert opinions while the –investor only observes stock returns. Finally the –investor has access to (the combination of) stock returns and expert opinions. Now we consider for the initial capital which the –investor needs to obtain the same maximized expected log-utility at time as the fully informed investor who started at time with unit wealth . The difference can be interpreted as loss of information for the (non fully informed) -investor while the ratio

is a measure for the efficiency of the -investor.

The initial capital required by the –investor is obtained as solution of the equation . From Theorem 5.3 it follows and since , hence

left: unknown initial value (stationary distribution)

right: unknown vs. known initial value, i.e.

vs.

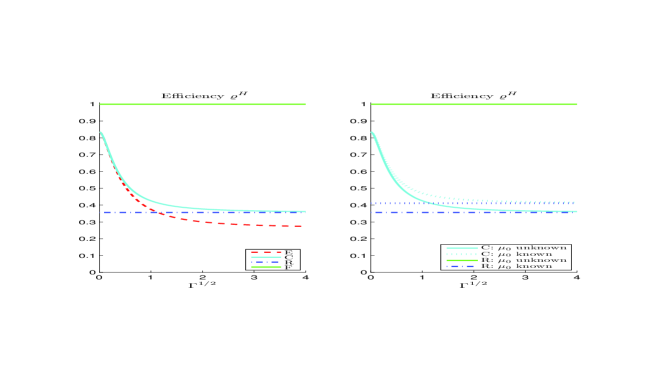

Figure 3 shows the efficiency as a function of the number of information dates. The left panel shows the results for the different investors assuming the initial value is unknown and its distribution is the stationary distribution. If an investor starts instead with a known initial value for the drift, i.e. , then this additional information increases the value and as a consequence the efficiency . This effect is shown for in the right panel. For the sake of better comparison we have set the known initial value equal to the mean of the drift . So at time the filters are initialized with , , for known as well as unknown .

Obviously, we have and the efficiency of the investor observing only returns and no expert opinions is not affected by while and increase with . As a consequence of Corollary 5.5 we always have and , since the investment decisions of the -investor are based on the observation of returns as well as expert opinions while the – and –investor have access to only one of these sources of information.

In order to illustrate the asymptotic results for given in Corollary 5.6 Table 2 gives for increasing numbers of information dates the values and efficiencies for and compares with the values and for . It can be observed that the result for the fully informed investor () is obtained for , i.e. and . For this study we assume that the initial value is unknown and its distribution is the stationary distribution. Then according to Theorem 5.3 the value is . For the interpretation of the values of given in Table 2 we note, that for year expert opinions arriving every month, week, day, hour, minute or second corresponds to or , respectively.

Finally, we study the dependence of the efficiency on the reliability of the expert opinions which is measured by the standard deviation of the views. The left panel of Figure 4 shows the results for an unknown initial value while the right panel compares the efficiencies and for known and unknown initial value. As in Figure 3, the efficiency is not affected by the expert opinions and does not depend on while and decrease with , i.e. with decreasing reliability of the expert opinions. As before we have . The figure also indicates that for the efficiency tends to the efficiency of the -investor since the expert opinions carry no additional information about the drift.

right: unknown vs. known initial value, i.e.

vs.

Parameters as in Table 1,

References

- [1] Björk, T., Davis, M.H.A. and Landén, C. (2010): Optimal investment with partial information. Mathematical Methods of Operations Research 71, 371–399.

- [2] Black, F. and Litterman, R. (1992): Global portfolio optimization. Financial Analysts Journal 48(5), 28–43.

- [3] Brendle, S. (2006): Portfolio selection under incomplete information. Stochastic Processes and Their Applications 116, 701–723.

- [4] Davis, M.H.A. and Lleo, S. (2013): Black–Litterman in continuous time: the case for filtering. Quantitative Finance Letters 1, 30–35.

- [5] Elliott, R.J., Aggoun, L. and Moore, J.B. (1994): Hidden Markov Models. Springer, New York.

- [6] Frey, R., Gabih, A. and Wunderlich, R. (2012): Portfolio optimization under partial information with expert opinions. International Journal of Theoretical and Applied Finance 15, No. 1.

- [7] Frey, R., Gabih, A. and Wunderlich, R. (2014): Portfolio optimization under partial information with expert opinions: a dynamic programming approach, arXiv1303.2513v2 [q-fin.PM].

- [8] Honda, T. (2003): Optimal portfolio choice for unobservable and regime-switching mean returns. Journal of Economic Dynamics and Control 28, 45- 78.

- [9] Lakner, P. (1995): Utility maximization with partial information, Stochastic Processes and their Applications 56, 247–273.

- [10] Lakner, P. (1998): Optimal trading strategy for an investor: the case of partial information. Stochastic Processes and their Applications 76, 77–97.

- [11] Liptser, R.S. and Shiryaev A.N. (2001): Statistics of Random Processes: General theory, 2nd edn, Springer, New York.

- [12] Nagai, H., Peng, S. (2002): Risk-sensitive dynamic portfolio optimization with partial information on infinite time horizon. Annals of Applied Probability 12, 173- 195

- [13] Putschögl, W. and Sass, J. (2008): Optimal consumption and investment under partial information. Decisions in Economics and Finance 31, 131–170.

- [14] Rieder, U. and Bäuerle, N. (2005): Portfolio optimization with unobservable Markov-modulated drift process. Journal of Applied Probability 43, 362–378.

- [15] Sass, J. and Haussmann, U.G (2004): Optimizing the terminal wealth under partial information: The drift process as a continuous time Markov chain. Finance and Stochastics 8, 553–577.

- [16] Sass, J., Seifried, F. and Wunderlich R. (2014): Continuous-time optimal investment and financial analysts’ research: Incorporating expert opinions into asset allocation, working paper.

- [17] Schöttle, K., Werner, R. and Zagst, R. (2010): Comparison and robustification of Bayes and Black-Litterman models. Mathematical Methods of Operations Research 71, 453–475.

- [18] Shiryaev, A.N. (1996): Probability. Springer, New York.