=0

Systemic Risk and Default Clustering for Large Financial Systems

Abstract.

As it is known in the finance risk and macroeconomics literature, risk-sharing in large portfolios may increase the probability of creation of default clusters and of systemic risk. We review recent developments on mathematical and computational tools for the quantification of such phenomena. Limiting analysis such as law of large numbers and central limit theorems allow to approximate the distribution in large systems and study quantities such as the loss distribution in large portfolios. Large deviations analysis allow us to study the tail of the loss distribution and to identify pathways to default clustering. Sensitivity analysis allows to understand the most likely ways in which different effects, such as contagion and systematic risks, combine to lead to large default rates. Such results could give useful insights into how to optimally safeguard against such events.

Keywords. Systemic risk, default clustering, large portfolios, loss distribution, asymptotic methods, rare events

1. Introduction

The past several years have made clear the need to better understand the behaviour in large interconnected financial systems. Almost all areas of modern life are touched by a financial crisis. The recent financial crisis of brought into focus the networked structure of the financial world. It challenged the mathematical finance community to understand connectedness in financial systems. The understanding of systemic risk, i.e., the risk that a large numbers of components of an interconnected financial system fails within a short time leading to the failure of the system itself, becomes an important issue to investigate.

Interconnections often make a system robust, but they can also act as conduits for risk. Even things that may seemingly be unrelated, may become related as risk restrictions, may for example, force a sale of one type of a well-performing asset to compensate for the poor behavior of another asset. Thus, appropriate mathematical models need to be developed, in order to help in the understanding of how risk can propagate between financial objects.

It is possible that initial shocks could trigger contagion effects (e.g., [Mei12]). Examples of such shocks include: changes in interest rate values, in currencies values, changes of commodities prices, or reduction in global economic growth. Then, there may be a transmission mechanism which causes other institutions in the system to be affected by the initial shock. An example of such a mechanism is financial linkages among economies. Another reason could simply be investor irrationality. In either case, systemic risk causes the perceived risk-return trade-off in the economy to change. Uncertainty becomes an issue and market participants fear subsequent losses in asset prices with a large dispersion in regards to the magnitude of the crisis. Reduce-form point process models of correlated default are many times used (a): to assess portfolio credit risk and (b): to value securities exposed to correlated default risk. The workhorses of these models are counting processes. In this work we focus on using dynamic portfolio credit risk models to study large portfolio asymptotics and default clustering.

Large portfolio asymptotic were first studied in [Vas91]. The model in [Vas91] is a static model of a homogeneous pool and firms default independently of one another conditional on a normally distributed random variable representing a systematic risk factor. Alternative distributions of the systematic factor were examined in [SO05], [LKSS01] and the case of heterogeneous portfolios was studied in [Gor03]. In [BHH+11], the authors extend the model of [Vas91] dynamically and the systematic risk factor follows a Brownian motion. In [BHH+11], the authors study a structural model for distance to default process in a pool of names. A firm defaults when the default process hits zero. Exploiting conditional independence of defaults, [DDD04] and [GKS07] have studied the tail of the loss distribution in the static case. Large deviations arguments were also used in [SS11] to study stochastic recovery effects on large static pools of credit assets.

Reduced-form models of correlated default timing have appeared in the finance literature under different forms. [GW06] take the intensity of a name as a function of the state of the names in a specified neighborhood of that name. The authors in [DPRST09] and [DPT09] take the intensity to be a function of the portfolio loss and each name can be either in a good or in a distressed financial state. These papers prove law of large numbers for the portfolio loss distribution and develop Gaussian approximations to the portfolio loss distribution based on central limit theorems. [CMZ12] consider the typical behavior of a mean field system with permanent default impact.

[SZ10] study large portfolio asymptotics for utility indifference valuation of securities exposed to the losses in the pool. In [GPY12], the authors study systematic risk via a mean field model of interacting agents. Using a model of a two well potential, agents can move freely from a healthy state to a failed state. The authors study probabilities of transition from the healthy to the failed state using large deviations ideas. In [FI13] the authors propose and study a model for inter-bank lending and study its stochastic stability.

The authors in [ASCDL10] employ jump-diffusion models driven by Hawkes processes to empirically study default clustering and the time dimension of systemic risk. [Dua94] proposes a hierarchical model with individual shocks and group specific shocks. The work of [BCH11] reviews intensity models that are governed by exogenous and endogenous Markov Chains. In [GSS13], the authors proposed a dynamic point process model of correlated default timing in a portfolio of firms (“names”). The model incorporates different sources of default clustering identified in recent empirical research, including idiosyncratic risks, exposure to systematic risk factors and contagion in financial markets, see [DSW06], [AGS10]. Based on the weak convergence ideas of [GSS13], the authors in [BC13] obtain and study formulas for the bilateral counterparty valuation adjustment of a credit default swaps portfolio referencing an asymptotically large number of entities.

The model in [GSS13] can be naturally understood as an interacting particle system that is influenced by an exogenous source of randomness. There is a central source of interconnections and failure of any of the components stresses the central ’bus’, which in turn can cause the failure of other components (a contagion effect). Computing the distribution of the loss from default in such models tends to be a difficult task and while Monte-Carlo simulation methods are broadly applicable, they can be slow for large portfolios or large time horizons as it is commonly the interest in practice. Mathematical and computational tools for the approximation to the distribution of the loss from default in large heterogeneous portfolios were then developed in [GSSS12], Gaussian correction theory was developed in [SSG13b] and analysis of tail events and most likely paths to failure via the lens of large deviations theory was then developed in [SS13]. We remark here that to a large extend systemic risk refers to the tail of the distribution. The authors in [SSG13a] combine the large pool asymptotic results of [GSSS12]-[SSG13b] with maximum likelihood ideas to construct tractable statistical inference procedures for parameter estimation in large financial systems.

Such mathematical results lead to new computational tools for the measurement and prediction of risk in high-dimensional financial networks. These tools mainly include approximations of the distribution of losses from defaults and of portfolio risk measures, and efficient computational tools for the analysis of extreme default events. The mathematical results also yield important insights into the behavior of systemic risk as a function of the characteristics of the names in the system, and in particular their interaction.

Financial institutions (banks, pension funds, etc) often hold large portfolios in order to diversify away a number of idiosyncratic effects of individual assets. Deposit insurance premia depend upon meaningful models and assessment of the macroeconomic effect of the various phenomena that drive defaults. Development of related mathematical and computational tools can help inform the design of regulatory policy, improve the pricing of federal deposit insurance, and lead to more accurate risk measurement at financial institutions.

In this paper, we focus on dynamic default timing models for large financial systems that fall into the category of intensity models in portfolio credit risk. Based on the default timing model developed in [GSS13], we address several of the issues just mentioned and that are typically of interest. The mathematical and computational tools developed allow to reach to financial related conclusions for the behavior of such large financial systems.

Although the primary interest of this work is risk in financial systems, models of the type discussed in this paper are generic enough to allow for modifications that make them relevant in other domains, including systems reliability, insurance and epidemiology. In reliability, a large system of interacting components might have a central connection, and be influenced by an external environment (temperature, for example). The failure of an individual component (which could be governed by an intensity model appropriate for the particular application) increases the stress on the central connection and thus the other components, making the entire system more likely to fail. In insurance, the system could represent a pool of insurance policies. The effect of wildfires might, in that example, be modelled by a contagion term. Systematic risk in the form of environmental conditions has an impact on the whole pool.

The rest of the article is structured as follows. In Section 2 we describe the correlated default timing proposed in [GSS13]. Section 3 studies the typical behavior of the loss distribution in such portfolios as the number of names (agents) in the pool grow to infinity. Section 4 focuses on developing the Gaussian correction theory. As we shall see there, Gaussian corrections are very useful because they make the approximations accurate even for portfolios of relatively small sizes. In Section 5, we study the tail of the loss distribution using arguments from the large deviations theory. We also study the most likely path to systemic failure and to the development of default clusters. An understanding of the preferred paths to large default rates and the most likely path to the creation of default clusters can give useful insights into how to optimally safeguard against such events. Importance sampling techniques can then be used to construct asymptotically efficient estimators for tail event probabilities, see Section 6. Conclusions are in Section 7. A large part of the material presented in this work, but not all, is related to recent work of the author described in [GSS13], [GSSS12], [SSG13b] and [SS13].

2. A dynamic correlated default timing model

One of the issues of fundamental importance in financial markets is systemic risk, which may be understood as the likelihood of failure of a substantial fraction of firms in the economy. There are a number of ways of interpreting this, but our focus will be the behavior of actual defaults. Defaults are discrete events, so one can frame the interest within the language of point processes. Empirically, defaults tend to happen in groups; feedback and exposure to market forces (along the lines of “regimes”) tend to produce correlation among defaults.

Let us fix a probability space where all random variables will be defined. Denote by the stopping time at which the -th component (or particle) in our system fails. Then, as , a failure time has intensity process , which satisfies

| (1) |

where is the sigma-algebra generated by the entire system up to time . Hence, we essentially have that the process defined by is a martingale.

Motivated by the empirical studies in [DSW06] and [AGS10], we may model the intensity in such a way that it depends on three factors: a mean reverting idiosyncratic source of risk, the portfolio loss rate and a systematic risk factor. Heterogeneity can be addressed by allowing the intensity parameters of each name to be different. The mean reverting character of the idiosyncratic source of risk is there to guarantee that the effect of a default in the pool has a transient effect on the default intensities of the surviving names. The dependence on the portfolio loss rate, denoted by is the term that is responsible for the contagious effects, whereas the systematic risk factor, denoted by is an exogenous source of risk. To be precise, the default intensities, ’s, are governed by the following interacting system of stochastic differential equations (SDEs)

| (2) |

where, be a countable collection of independent standard Brownian motions.

The process represents the empirical failure rate in the system, i.e.,

| (3) |

where by letting to be an i.i.d. collection of standard exponential random variables we have

| (4) |

The process represents the systematic risk, which can be modeled to be the solution to some SDE

| (5) |

where is a standard Brownian motion which is independent of the ’s and ’s. Plausible models for could be an Ornstein-Uhlenbeck process or a Cox-Ingersoll-Ross (CIR) process.

In the case for all , one recovers the classical CIR process model in credit risk, e.g., [DPS00]. Namely, the intensity SDE (1) extends the widely-used CIR process by including two additional terms that generate correlation between failure times. The term induces correlated diffusive movements of the component intensities; the process represents the state of the macro-economy, which affects all assets in the pool. The term introduces a feedback (contagion) effect. The standard term is a mean reverting term allowing the component to “heal” after a shock (i.e., a failure). This parsimonious formulation allows us to take advantage of the wealth of knowledge about CIR-type processes. The parameter allows us to later on focus on rare events.

The process of (3), which simply gives us the fraction of components which have already failed by time , affects each of the remaining components in a natural way. Each failure corresponds to a Dirac function in the measure ; the term thus leads to upward impulses in ’s, which leads (via (4)) to sooner failure of the remaining functioning components. We might think of a central “bus” in a system of components. Each of the components depends on this bus, which in turn sensitive to failures in the various components. In the financial application that was considered in [GSS13], this feedback mechanism is empirically observed to be an important channel for the clustering of defaults in the U.S. (see [AGS10]).

In order to allow for heterogeneity, the parameters in (2) depend on the index . Define the “type”

| (6) |

for each and . The ’s take value in . The parameters are assumed to be bounded uniformly in .

We can capture the heterogeneity of the system by defining and assuming that this empirical type frequency has a (weak) limit. In particular we make the following assumption

Assumption 2.1.

We assume that exists (in ).

Proposition 3.3 in [GSS13] guarantees that under the assumption of an existence of a unique strong solution for the SDE for process, the system (2)–(5) has a unique strong solution such that for every , and . The model (2)–(5) is a mean-field type model; the feedback occurs through the empirical average of the pool of names. It is somewhat similar to certain genetic models (most notably the Fleming-Viot process; see [DH82], [EK86, Chapter 10], and [FV79]). However, as it is also demonstrated in [GSS13] and in [GSSS12], the structure of the system (2)–(5) presents several difficulties that bring the analysis of such systems outside the scope of the standard setup.

3. Typical behavior: Law of large numbers

The system (2)–(5) can naturally be understood as an interacting particle system. This suggests how to understand its large-scale behavior. The structure of the feedback (the empirical average ) is of mean-field type (roughly within the class of McKean-Vlasov models; see [Gar88], [KK10]). An understanding of “typical” behavior of a system as is fundamental in identifying “atypical” or “rare” events.

To formulate the law of large numbers result, we define the empirical distribution of the ’s corresponding to the names that have survived up to time , as follows:

This captures the entire dynamics of the model (including the effect of the heterogeneities). We can directly calculate the failure rate from the ’s:

| (7) |

Let us then identify the limit of as . This is a law of large numbers (LLN) result and it identifies the baseline “typical” behavior of the system. For , let

| (8) |

for . The generator corresponds to the diffusive part of the intensity with killing rate , and is the macroscopic effect of contagion on the surviving intensities at any given time. The operators and capture the dynamics due to the exogenous systematic risk . Then tends in distribution (in the natural topology of subprobability measures on ) to a measure-valued process . Letting

for all , the limit satisfies the stochastic evolution equation

| (9) |

With sufficient regularity, this is equivalent to the stochastic integro-partial differential equation (SIPDE)

| (10) |

where ∗ denotes adjoint in the appropriate sense (for notational simplicity, we have written (10) to include the types as one of the coordinates; in a heterogeneous collection in practice we would often use only in solving (10)). We recall the rigorous statement in Theorem 3.1.

The SIPDE (10) gives us a “large system approximation” of the failure rate:

| (11) |

The computation of the first-order approximation (11) suggested by the LLN requires solving the SIPDE (10) governing the density of the limiting measure. In [GSSS12] a numerical method for this purpose is proposed. The method is based on an infinite system of SDE’s for certain moments of the limiting measure. These SDEs are driven by the systematic risk process and a truncated system can be solved using a discretization or random ODE scheme. The solution to the SDE system leads to the solution to the SIPDE via an inverse moment problem.

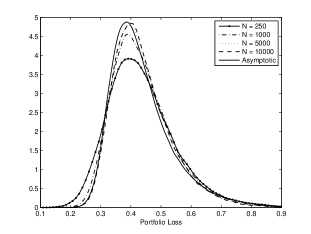

The approximation (11) has significant computational advantages over a naive Monte Carlo simulation of the high-dimensional original stochastic system (2)–(5) and its accuracy is demonstrated in the left of Figure 1 for a specific choice of parameters. It also provides information about catastrophic failure.

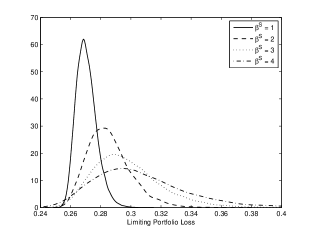

The tail represents extreme default scenarios, and these are at the center of risk measurement and management applications in practice. The analysis of the limiting distribution generates important insights into the behavior of the tails as a function of the characteristics of the system (2)–(5). For example, we see that the tail is heavily influenced by the sensitivity of a name to the variations of the systematic risk . The bigger the sensitivity the fatter the tail, and the larger the likelihood of large losses in the system (see the right of Figure 1). Insights of this type can help understand the role of contagion and systematic risk, and how they interact to produce atypically large failure rates. This, in turn, leads to ways to minimize or “manage” catastrophic failures.

Let us next present the statement of the mathematical result. We denote by the collection of sub-probability measures (i.e., defective probability measures) on ; i.e., consists of those Borel measures on such that .

Theorem 3.1 (Theorem 3.1 in [GSSS12]).

We have that converges in distribution to in . The evolution of is given by the measure evolution equation

Suppose there is a solution of the nonlinear SPDE

| (12) |

where denote adjoint operators, with initial condition

Then

We close this section, by briefly describing the method of moments that leads to the numerical computation of the loss from default. We focus our discussion on the homogeneous case and we refer the reader to [GSSS12] for the general case.

Firstly, we remark that the SPDE (12) can be supplied with appropriate boundary conditions, which as it is mentioned in [GSSS12], are

Secondly, it turns out that for , the moments exist almost surely. By (11) is is clear that we want to compute . In particular, note that the limiting loss .

By an integration by parts and using the boundary conditions at and at , we can prove that they follow the following system of stochastic differential equations

| (13) | ||||

where .

The system (13) is a non-closed system since to determine , one needs to know . So, in practice one must perform a truncation at some level where we let (that is, we use the first moments). As it is shown in [GSSS12] one needs relatively small numbers of moments in order to compute the zero-th moment with good accuracy. Then, by solving backwards, one computes and from this one gets the limiting loss distribution

4. Central limit theorem correction

The asymptotics of (10) give via (11) the limiting behavior of the system as the number of components becomes large. Starting with that result, the results in [SSG13b] develop Gaussian fluctuation theory analogous to the central limit theory (see for example [DPRST09], [DPT09], [FM97], [KX04] for some related literature). This result provides the leading order asymptotics correction to the law of large numbers approximation developed in Section 3. In practical terms, the usefulness of such of a result is twofold: (a) the approximation is accurate even for portfolios of moderate size, see [SSG13b], and (b): one can make use of the approximation to develop tractable statistical inference procedures for the statistical calibration of such models, see [SSG13a].

To be more precise, let us define the signed measure

as . Conditional on the exogenous systematic risk process , a central limit theorem applies and exists in an appropriate space of distributions and is Gaussian. Unconditionally, it may not be Gaussian but is of mean zero (since we have removed the bias from ).

The usefulness of the fluctuation analysis is that it leads to a second-order approximation to the distribution of the portfolio loss in large pools. The fluctuations analysis yields an approximation which improves the first-order approximation (11) suggested by the LLN, especially for smaller system sizes .

In particular, Theorem 4.1 implies that

for large . This motivates the approximation

which then implies the following second-order approximation for the portfolio loss.

| (14) |

The numerical computation of the second-order approximation (14) suggested by the fluctuation analysis is amenable to a moment method similar to that used for computing the first-order approximation (11). In addition to solving the LLN SIPDE, we would also need to solve for the fluctuation limit. This limit is governed by a stochastic evolution equation, which gives rise to an additional system of “fluctuation moments.” This system is driven by the exogenous systematic risk process and the martingale in Theorem 4.1 that is conditionally Gaussian given .

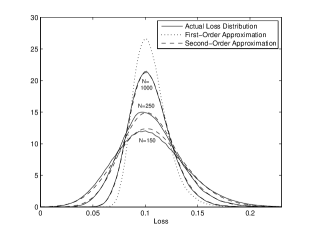

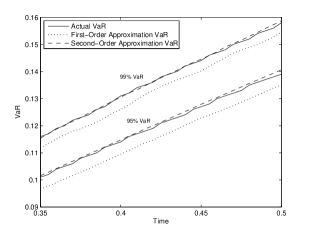

Left of Figure 2 compares the approximate loss distribution with the actual loss distribution for specific parameter choices. It is evident from the numerical comparisons that the second-order approximation has increased accuracy, especially for smaller portfolios and in the tail of the distribution. The right of Figure 2 compares for the and percent value at risk (VaR) between the actual loss, LLN approximation (11), and approximation (14) for a pool of names. It is also evident from the figure that the approximation for the VaR based on (14) is much more accurate than the law of large numbers approximation.

Let us close this section, with a few words on the actual mathematical result. It turns out that the convergence happens in an appropriate weighted Hilbert space, which we denote by , with and the appropriate weight functions, and will be its dual. Such weighted Sobolev spaces were introduced in [Pur84] and further generalized in [GK90] to study stochastic partial differential equations with unbounded coefficients. These weighted spaces turn out to be convenient for the present situation, see [SSG13b].

In order to state the convergence result, we introduce some operators. Let and for , define

Then, we have the following theorem related to the fluctuations analysis.

Theorem 4.1.

[Theorem 4.1 in [SSG13b]] For large enough and for appropriate weight functions , the sequence is relatively compact in . For any , the limit accumulation point of , denoted by , is unique in and satisfies the stochastic evolution equation

| (15) |

for any , where is a distribution-valued martingale with predictable variation process

Conditional on the -algebra that is generated by the Brownian motion, is centered Gaussian with covariance function, for , given by

| (16) |

It is clear that if for all , then the limiting distribution-valued martingale is centered Gaussian with covariance operator given by the (now deterministic) term within the expectation in (16).

The main idea for the derivation of (15) comes from the proof of the convergence to the solution of (9). Define

for . Let’s also assume for the moment that for every , i.e, let’s neglect exposure to the exogenous risk and focus on contagion. Then we can write the evolution of as

where is a martingale which may change from line to line. This leads to (9), when for every , see [GSS13].

5. Analysis of tail events: Large deviations

Once we have identified what is typical, we can study the structure of atypically large failure rates. Large deviations outlines a circle of ideas and calculations for understanding the origination and transformation of rare events (see [FW84], [Var84]). Large deviation arguments allow us to identify the “dominant” way that rare events will occur in complex systems. This is the feature that is being exploited in [SS13], i.e., how different sources of stochasticity can lead to system collapse.

By the discussion in Section 3, we have that the pool has a default rate at time . Let’s fix . Then ; it is a rare event that the default rate in the pool exceeds . We want to understand as much as possible about .

Using, the theory of large deviations, we can understand both how rare this event is, and what the “most likely” way is for this rare event to occur. Events far from equilibrium crucially depend on how rare events propagate through the system. Large deviations gives rigorous ways to understand these effects, and we want to use this machinery to understand the structure of atypically large default clusters in the portfolio. A reference for large deviations is [DZ88].

If we have that

for some appropriate functional , then by the contraction principle we should have that

| (17) |

where

| (18) |

(in other words, is the large deviations rate function for ). This gives us the rate at which the tail of the default rate decays as the diversification parameter grows. More importantly, though, the variational problem (18) gives us the preferred way which atypically large default rates occur. Namely, if there is a such that

then for any , the Gibbs conditioning principle suggests that

Insights into large deviations of (2)–(5) have been developed in [SS13] when and when as . We note here that in the case , the large deviations principle is conditional on the systematic risk . Such results allow us to study the comparative effect of the systematic risk process and of the contagion feedback on the tails of the loss distribution.

Before presenting the result, let us first investigate numerically a test case, which is indicative of the kind of results that large deviations theory can give us. Apart from approximating the tail of the distribution, large deviations can give quantitative insights into the most likely path to failure of a system.

For presentation purposes and for the rest of this section, we assume that as . Consider a heterogeneous test portfolio composed initially of names. Let us assume that we can separate the names in the portfolio into three types: Type A is of the names, Type B is of the names and Type C is of the names. For presentation purposes, we assume that all parameters but the contagion parameter are the same among the different types. In particular, we have the following choice of parameters.

| Type A | 0.5 | 2 | 0.5 | 0.2 | 1 | 1 | 10 |

| Type B | 0.5 | 2 | 0.5 | 0.2 | 1 | 1 | 3 |

| Type C | 0.5 | 2 | 0.5 | 0.2 | 1 | 1 | 1 |

It is instructive to compare the different cases, based on whether there are contagion effects in the default intensities or not. In particular, we compare two different cases, (a) Systematic risk only: , and (b) Systematic risk and contagion: . In each case, the time horizon is .

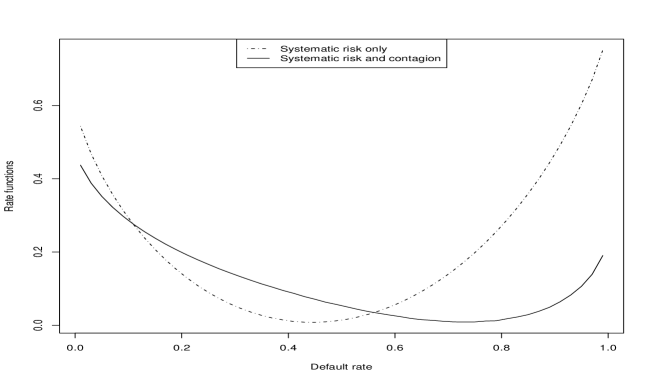

Using the methods of Section 3, one can compute that the typical loss in such a pool at time . If contagion effects are not present, i.e., if , then the typical loss in such a portfolio at time is . If on the other hand, contagion (feedback) effects are present and the parameters take the values of Table 1, then the typical loss in such a portfolio at time has been increased to . In Figure 3, we plot the large deviations rate functions for each of the two different cases. As we saw in the beginning of this section, the rate function governs the asymptotics of the tail of the loss distribution. Notice that in every case, the rate function is convex and it becomes zero at the corresponding law of large numbers.

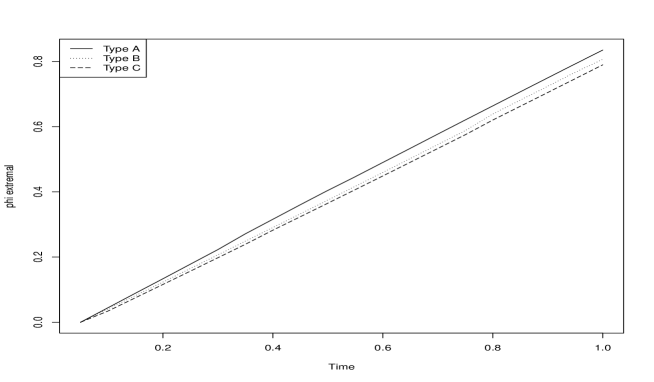

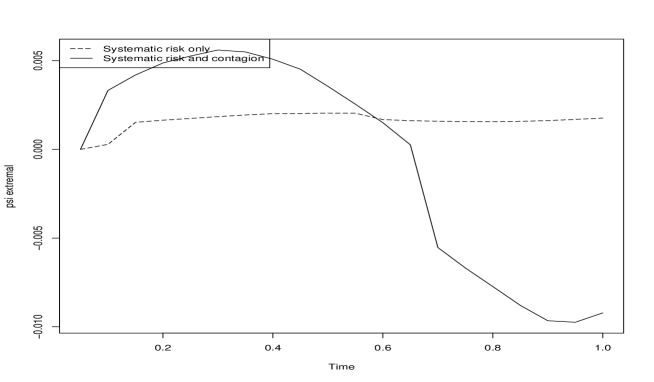

Moreover, since the contagion parameter of Type A is higher than the contagion parameter for Type B or C, one expects that names of Type A will be more prompt to the contagious impact of defaults. Indeed, after computing the rate function and the associated extremals, as defined by large deviations theory, one gets the most likely paths to failure as seen in Figures 4-5. The trajectories correspond to the contagion extremals for each of the three types, whereas the corresponds to the systematic risk extremal.

One can make two conclusions out of Figures 4-5. The first conclusion is related to the extremals (Figure 4). We notice that at any given time , the extremal for Type A is bigger than the extremal for Type B, which in turn is bigger than the extremal of Type C. This implies that unlikely large losses for components of Type A are more likely than unlikely large losses for components of Type B, which are more likely than large losses for components of Type C. Thus, components of Type A affect the pool more than components of Type B, which in turn affect the pool more than components of Type C even though Type A composes of the pool, whereas Type B, composes of the pool and Type C composes of the pool. The second conclusion is related to the extremals (Figure 5). We notice that the effect of the systematic risk is most profound in the beginning but then its significance decreases.

Namely, if a large cluster were to occur, the systematic risk factor is likely to play an important role in the beginning, but then the contagion effects become more important. Assets of Type A are likely to contribute to the default clustering effect more, followed by assets of Type B and the ones that will contribute the least to the default cluster are assets of Type C.

As it is also seen in the numerical experiments done in [SS13], the large deviations analysis help quantify the effect that the contagion and the systematic risk factor have on the behavior of the extremals (the most likely path to failure). An understanding of the role of the preferred paths to large default rates and the most likely ways in which contagion and systematic risk combine to lead to large default rates would give useful insights into how to optimally hedge against such events.

Let us next proceed by motivating the development of the large deviations principle for the default timing model (2)–(5) that is considered in this paper.

We denote scenarios, i.e., defaults, that are not in by an abstract point not in and define the Polish space

To motivate things, let’s first assume for simplicity that and that the system is homogeneous, i.e., that for all . Define

with . This Feller diffusion will represent the conditional intensity of a “randomly-selected” component of our (homogeneous and independent) system. Define the measure by setting

for all ; is the common law of the default times ’s.

In the independent case, i.e., when , standard Sanov’s theorem [DZ88], implies that has a large deviations principle with rate function

if and if (i.e., is the relative entropy of with respect to ). By the contraction principle, the rate function for is

In the independent case, we can actually compute both the extremal that achieves the infimum and the corresponding rate function in closed form.

Assume that and . Fix such that . Define

for all . Then and are in . We can write that

| (19) |

where is entropy on . We can minimize the term by setting , and we get that

This is in fact obvious; , and in this case the ’s are i.i.d. Bernoulli random variables with common bias . The rate function of (5) is the entropy of Bernoulli coin flips. Of more interest, however, is the optimal path. In setting in (19), we essentially identify the optimal path

where the last relation holds since we also require .

It turns out that one can extend this result to give a generalized Sanov’s theorem for the case , where feeds back into the dynamics of the ’s. The case can be treated using a conditioning argument and the well developed theory of large deviations for small noise diffusions. For the heterogeneous case, one needs an additional variational step which minimizes over all the possible ways that losses are distributed among systems of different types. Even though an explicit closed form expression for the extremals and for the corresponding rate function is no longer possible, one can still rely on numerically computing them. Let us make this discussion precise.

To fix the discussion, let us assume (see [SS13] for the general case) that the exogenous risk is of Ornstein-Uhlenbeck type, i.e.,

Let be a reference Brownian motion. Fix a name in the pool and time horizon .

The Freidlin-Wentzell theory of large deviations for SDE’s gives us a natural starting point. In the Freidlin-Wentzell analysis, a dominant ODE is subjected to a small diffusive perturbation; informally, the Freidlin-Wentzell theory tells us that if we want to find the probability that the randomly-perturbed path is close to a reference trajectory, we should use that reference trajectory in the dynamics. This leads to the correct LDP rate function for the original SDE. If we want to find the asymptotics of the probability that for some absolutely continuous functions and , i.e., , we should consider the stochastic hazard functions

This will represent the conditional intensity of a “randomly-selected” name in our pool. Define next

where, we have used the superscript to denote the dependence on the particular type. Then for every we have that

where is an exponential(1) random variable which is independent of . In other words, is the density (up to time ) of a default time whose conditional intensity is . In fact, due to the affine structure of the model, we have an explicit expression for (see Lemma 4.1 in [SS13]).

For given trajectories and in , define as

for all .

At a heuristic level one can derive the large deviations principle as follows. Let us assume that we can establish that

and that also has large deviations principle in with action functional ; i.e.,

as . Then, we should have that

In fact, the previous heuristics can be carried out rigorously and in the end one derives the following rigorous large deviations result.

Theorem 5.1 (Theorem 3.8 in [SS13]).

Consider the system defined in (2)-(5) with such that and let . Under the appropriate assumptions the family satisfies the large deviation principle, with rate function

where if , then

and otherwise. Here, is the rate function for the process . Namely, for with we have

and otherwise. has compact level sets.

If the heterogeneous portfolio is composed by different types of assets with homogeneity within each type, then Theorem 5.1 simplifies to the following expression.

For let us define the functional

Due to the affine structure of the model, we have an explicit expression for (see Lemma 4.1 in [SS13]).

Assume that of the names are of type with and . Setting , we get the following simplified expression for the rate function

An optimization algorithm can then be employed to solve the minimization problem associated with and compute the extremals for and . This is the formula that the numerical example presented in Figures 4-5 was based on. In the numerical example that was considered there we had three types, i.e., .

The large deviations results have a number of important applications. Firstly, they lead to an analytical approximation of the tail of the distribution of the failure rate for large systems. These approximations complement the first- and second- order approximations suggested by the law of large numbers and fluctuations analysis of Sections 3 and 4 respectively and facilitates the estimation of the likelihood of systemic collapse. Secondly, the large deviations results provide an understanding of the “preferred” ways of collapse, which can also be used to design “stress tests” for the system. In particular, this understanding can guide the selection of meaningful stress scenarios to be analyzed. Thirdly, they can motivate the design of asymptotically efficient importance sampling schemes for the tail of the portfolio loss. We discuss some of the related issues in Section 6.

6. Monte Carlo methods for estimation of tail events: Importance sampling

Suppose we want to computationally simulate , where again holds. Accurate estimates of such rare-event probabilities are important in many applications areas of our system (2)–(5), including credit risk management, insurance, communications and reliability. Monte Carlo methods are widely used to obtain such estimates in large complex systems such as ours; see, for example, [BJ06, BZ08, CC10, JPFV09, KGL12, GKMT10, Gla04, GL05, ZBGG11].

Standard Monte Carlo sampling techniques perform very poorly in estimating rare events (for which, by definition, most samples can be discarded). Importance sampling, which involves a change of measure, can be used to address this issue. In general, large deviations theory provides an optimal way to ‘tilt’ measures. The variational problems identified by large deviations usually lead to measure transformations under which pre-specified rare events become much more likely, but which give unbiased estimates of probabilities of interest; see for example [AG07, Buc04, DW04, DW07, DSW12, GW97, Sad96].

Let be any unbiased estimator of that is defined on some probability space with probability measure . In other words, is a random variable such that , where is the expectation operator associated with . In our setting, it takes the form

where is the associated Radon-Nikodym derivative.

Importance sampling involves the generation of independent copies of under ; the estimate is the sample mean. The specific number of samples required depends on the desired accuracy, which is measured by the variance of the sample mean. However, since the samples are independent it suffices to consider the variance of a single sample. Because of unbiasedness, minimizing the variance is equivalent to minimizing the second moment. An application of Jensen’s inequality, shows that if

then achieves this best decay rate, and is said to be asymptotically optimal. One wants to choose such that asymptotic optimality is attained.

To motivates things let us assume for the moment that and that the system is homogeneous, i.e., that for all . In the independent and homogeneous case, are i.i.d. random variables such that for every

For notational convenience, we shall define

It is easy to see that,

To minimize the variance, we need to increase the probability of defaults. Define

A simple computation shows that

Define

Clearly . Notice that the density of a with respect to a is

Therefore, for fixed, the suggestion is to simulate under a new change of measure, under which and to return the estimator

It is clear that this estimator is unbiased. We want to choose that minimizes the variance, or equivalently the second moment. For this purpose, we define the second moment

Notice that

Due to convexity of , we have that the maximizer over of the lower bound is at such that . In particular, (recall that ) we have

This construction means that under the new measure, we have

In fact, we have the following theorem.

Theorem 6.1.

Proof.

By Jensen’s inequality we clearly have the upper bound. Namely, for every

| (21) |

Now, we need to prove that the lower bound is achieved for , i.e., that

| (22) |

Recalling that and , we easily see that

This concludes the proof of the theorem. ∎

In the heterogeneous case, i.e. if can be different for each , then is no longer Binomial, but it is a sum of independent (but not identically distributed) Bernoulli random variables with success probability

indexed by . Due to independence, similar methods as the one described above can be used to construct asymptotically efficient importance sampling schemes in the heterogeneous case.

The scheme just presented essentially amounts to a twist in the intensity of the defaults. However, in contrast to the independent case, i.e., when , the situation in the general dependent case is more complicated. Notice also if at least one one of the ’s is not zero, then the model (2)–(5) does not fall into the category of the doubly-stochastic models, so techniques as the ones used in [BJ06] do not apply. Also, implementation of interacting particle schemes for Markov Chain models as the ones developed in [CC10, JPFV09] do not readily apply for such intensity models. The re-sampling schemes of [GKMT10] could apply in this setting, but one would need to construct an appropriate mimicking Markov Chain, something which is not clear how to do in the current setting.

We briefly present here an importance sampling scheme for the case that there exists at least one and also applies independently of whether the systematic effects are present in the model or not. The suggested measure change essentially mimics the principal idea behind the measure change for the independent case. To be more precise, one directly twists the intensity of .

Let be the arrival times of and notice that . Let and be some progressively measurable twisting process. Then, define the measure via the Radon-Nicodym derivative

It is known that if , then defined by is a probability measure and it can be shown that admits intensity on the interval .

This construction gives us some freedom into choosing appropriately the twisting process . Different choices of the twisting process are of course possible. For tractability purposes we restrict attention to a one-parameter family and set

For any and under the measure induced by , i.e. under , the process has intensity on , i.e. it amounts to an additive shift of the intensity. Thus, is a superimposed default rate and its role is to increase the default rate in the whole portfolio.

The purpose then is to optimize the limit as of the upper bound of the second moment of the resulting estimator over . This is the measure change that is investigated in [GS11], and it is shown there that there is a choice of for which asymptotic optimality can be established. Namely, there is a choice of that minimizes the second moment of the estimator in the limit as . We refer the interested reader to [GS11] for implementation details on this change of measure for related intensity models and for corresponding simulation results.

7. Conclusions

We presented an empirically motivated model of correlated default timing for large portfolios. Large portfolio analysis allows to approximate the distribution of the loss from default, whereas Gaussian corrections make the approximation valid even for portfolios of moderate size. The results can be used to compute the loss distribution and to approximate portfolio risk measures such as Value-at-Risk or Expected Shortfall. Then, large deviations analysis can help understand the tail of the loss distribution and find the most-likely paths to systemic failure and to the creation of default clusters. Such results give useful insights into the behavior of systemic risk as a function of the characteristics of the names in the portfolio and can be also potentially used to determine how to optimally safeguard against rare large losses. Importance sampling techniques can be used to construct asymptotically efficient estimators for tail event probabilities.

8. Acknowledgements

The author was partially supported by the National Science Foundation (DMS 1312124).

References

- [AG07] Søren Asmussen and W. Peter Glynn. Stochastic Simulation: Algorithms and Analysis. Grundlehren der Mathematischen Wissenschaften. Springer-Verlag, New York, 2007.

- [AGS10] Shahriar Azizpour, Kay Giesecke, and Gustavo Schwenkler. Exploring the sources of default clustering. Working Paper, Stanford University, 2010.

- [ASCDL10] Y. Ait-Sahalia, J. Cacho-Diaz, and R. Laeven. Modeling financial contagion using mutually exciting jump processes. Technical report, NBER, 2010.

- [BC13] Lijun Bo and Agostino Capponi. Bilateral credit valuation adjustment for large credit derivatives portfolios. Finance and Stochastics, forthcoming, 2013.

- [BCH11] T. Bielecki, S. Crépey, and A. Herbertsson. Markov chain models of portfolio credit risk. Oxford Handbook of Credit Derivatives, Oxford University Press, New York, pages 327–382, 2011.

- [BHH+11] Nick Bush, Ben Hambly, Helen Haworth, Lei Jin, and Christoph Reisinger. Stochastic evolution equations in portfolio credit modelling. SIAM Journal on Financial Mathematics, 2:627–664, 2011.

- [BJ06] Achal Bassamboo and Sachin Jain. Efficient importance sampling for reduced form models in credit risk. Proceedings of the 2006 Winter Simulation Conference, pages 741–748, 2006.

- [Buc04] James Bucklew. Introduction to Rare Event Simulation. Grundlehren der Mathematischen Wissenschaften. Springer-Verlag, New York, 2004.

- [BZ08] Sandeep Juneja Achal Bassamboo and Assaf Zeevi. Portfolio credit risk with extremal dependence: Asymptotic analysis and efficient simulation. Operations Research, 56(3):593–606, 2008.

- [CC10] René Carmona and Stéphane Crépey. Particle methods for the estimation of Markovian credit portfolio loss distributions. International Journal of Theoretical and Applied Finance, 13(4):577–602, 2010.

- [CMZ12] Jakša Cvitanić, Jin Ma, and Jianfeng Zhang. The law of large numbers for self-exciting correlated defaults. Stochastic Processes and Their Applications, 122(8):2781–2810, 2012.

- [DDD04] Amir Dembo, Jean-Dominique Deuschel, and Darrell Duffie. Large portfolio losses. Finance and Stochastics, 8:3–16, 2004.

- [DH82] Donald A. Dawson and Kenneth J. Hochberg. Wandering random measures in the fleming-viot model. Annals of Probability, 10(3):554–580, 1982.

- [DPRST09] Paolo Dai Pra, Wolfgang Runggaldier, Elena Sartori, and Marco Tolotti. Large portfolio losses: A dynamic contagion model. The Annals of Applied Probability, 19:347–394, 2009.

- [DPS00] Darrell Duffie, Jun Pan, and Kenneth Singleton. Transform analysis and asset pricing for affine jump-diffusions. Econometrica, 68:1343–1376, 2000.

- [DPT09] Paolo Dai Pra and Marco Tolotti. Heterogeneous credit portfolios and the dynamics of the aggregate losses. Stochastic Processes and their Applications, 119:2913–2944, 2009.

- [DSW06] Darrell Duffie, Leandro Saita, and Ke Wang. Multi-period corporate default prediction with stochastic covariates. Journal of Financial Economics, 83(3):635–665, 2006.

- [DSW12] Paul Dupuis, Konstantinos Spiliopoulos, and Hui Wang. Importance sampling for multiscale diffusions. Multiscale Modelling and Simulation, 12:1–27, 2012.

- [Dua94] Jin-Chuan Duan. Maximum likelihood estimation using price data of the derivative contract. Mathematical Finance, 4:155–167, 1994.

- [DW04] Paul Dupuis and Hui Wang. Importance sampling, large deviations and differential games. Stochastics and Stochastics Reports, 76:481–508, 2004.

- [DW07] Paul Dupuis and Hui Wang. Subsolutions of an isaacs equation and efficient schemes for importance sampling. Mathematics of Operations Research, 32:723–757, 2007.

- [DZ88] Amir Dembo and Ofer Zeitouni. Large deviations techniques and applications, second edition. Springer-Verlag, New York, 1988.

- [EK86] Stewart N. Ethier and Thomas G. Kurtz. Markov Processes: Characterization and Convergence. John Wiley & Sons Inc., New York, 1986.

- [FI13] Jean-Pierre Fouque and Tomoyuki Ichiba. Stability in a model of inter-bank lending. SIAM Journal on Financial Mathematics, 4:784–803, 2013.

- [FM97] Begoña Fernandez and Sylvie Mélèard. A hilbertian approach for fluctuations on the mckean-vlasov model. Stochastic Processes and their Applications, 71:33–53, 1997.

- [FV79] Wendell H. Fleming and Michel Viot. Some measure-valued markov processes in population genetics theory. Indiana University Mathematics Journal, 28(5):817–843, 1979.

- [FW84] Mark Freidlin and Alexander. Wentzell. Random perturbations of dynamical systems, second edition. Springer-Verlag, New York, 1984.

- [Gar88] Jurgen Gartner. On the mckean-vlasov limit for interacting diffusions. Mathematische Nachrichten, 137(1):197–248, 1988.

- [GK90] Imre Gyöngy and Nikolai Krylov. Stochastic partial differential equations with unbounded coefficients and applications, I. Stochastics and Stochastics Reports, 32:53–91, 1990.

- [GKMT10] Kay Giesecke, Hossein Kakavand, Mohammad Mousavi, and Hideyuki Takada. Exact and efficient simulation of correlated defaults. SIAM Journal on Financial Mathematics, 1:868–896, 2010.

- [GKS07] Paul Glasserman, Wanmo Kang, and Perwez Shahabuddin. Large deviations in multifactor portfolio credit risk. Mathematical Finance, 17(3):345–379, 2007.

- [GL05] Paul Glasserman and Jingyi Li. Importance sampling for portfolio credit risk. Management Science, 51(11):1643–1656, 2005.

- [Gla04] Paul Glasserman. Tail approximations for portfolio credit risk. Journal of Derivatives, 12(2):24–42, 2004.

- [Gor03] Michael B. Gordy. A risk-factor model foundation for ratings-based bank capital rules. Journal of Financial Intermediation, 12:199–232, 2003.

- [GPY12] Josselin Garnier, George Papanicolaou, and Tzu-Wei Yang. Large deviations for a mean field model of systemic risk. SIAM Journal on Financial Mathematics, 4:151–184, 2012.

- [GS11] Kay Giesecke and Alexander Shkolnik. Asymptotic optimal importance sampling of default times. working paper, Stanford University, 2011.

- [GSS13] Kay Giesecke, Konstantinos Spiliopoulos, and Richard Sowers. Default clustering in large portfolios: Typical events. The Annals of Applied Probability, 23(1):348–385, 2013.

- [GSSS12] Kay Giesecke, Konstantinos Spiliopoulos, Richard Sowers, and Justin A. Sirignano. Large portfolio asymptotics for loss from default. Mathematical Finance, forthcoming, 2012.

- [GW97] Paul Glasserman and Yashan Wang. Counterexamples in importance sampling for large deviations probabilities. Annals of Applied Probability, 7:731–746, 1997.

- [GW06] Kay Giesecke and Stefan Weber. Credit contagion and aggregate losses. Journal of Economic Dynamics and Control, 30:741–767, 2006.

- [JPFV09] René Carmona Jean-Pierre Fouque and Douglas Vestal. Interacting particle systems for the computation of rare credit portfolio losses. Finance and Stochastics, 13(4):613–633, 2009.

- [KGL12] Shaojie Deng Kay Giesecke and Tze Leung Lai. Sequential importance sampling and resampling for dynamic portfolio credit risk. Operations Research, 60(1):78–91, 2012.

- [KK10] Peter M. Kotelenez and Thomas G. Kurtz. Macroscopic limits for stochastic partial differential equations of mckean–vlasov type. Probability Theory and Related Fields, 146(1-2):189–222, 2010.

- [KX04] Thomas G. Kurtz and Jie Xiong. A stochastic evolution equation arising from the fluctuations of a class of interacting particle systems. Communications in Mathematical Sciences, 2(3):325–358, 2004.

- [LKSS01] Andre Lucas, Pieter Klaassen, Peter Spreij, and Stefan Straetmans. An analytic approach to credit risk of large corporate bond and loan portfolios. Journal of Banking and Finance, 25:1635–1664, 2001.

- [Mei12] C. Meinerding. Asset allocation and asset pricing in the face of systemic risk: a literature overview and assessment. International Journal of Theoretical and Applied Finance (IJTAF), 15(03):1250023–1–1250023–27, 2012.

- [Pur84] O.G. Purtukhia. On the equations of filtering of multi-dimensional diffusion processes (unbounded coefficients). Thesis, Moscow, Lomonosov University 1984 (in Russian), 1984.

- [Sad96] S. John Sadowsky. On monte carlo estimation of large deviations probabilities. Annals of Applied Probability, 6:399–722, 1996.

- [SO05] Lutz Schloegl and Dominic O’Kane. A note on the large homogeneous portfolio approximation with the student-t copula. Finance and Stochastics, 9(4):577–584, 2005.

- [SS11] Konstantinos Spiliopoulos and Richard Sowers. Recovery rates in investment-grade pools of credit assets: A large deviations analysis. Stochastic Processes and Their Applications, 121(12):2861–2898, 2011.

- [SS13] Konstantinos Spiliopoulos and Richard Sowers. Default clustering in large pools: Large deviations. arXiv: 1311.0498, submitted, 2013.

- [SSG13a] Justin A. Sirignano, Gustavo Schwenkler, and Kay Giesecke. Likelihood estimation for large financial systems. working paper, Stanford University, 2013.

- [SSG13b] Konstantinos Spiliopoulos, Justin A. Sirignano, and Kay Giesecke. Fluctuation analysis for the loss from default. Stochastic Processes and their Applications, 124(7), pp. 2322-2362, 2014.

- [SZ10] Ronnie Sircar and Thaleia Zariphopoulou. Utility valuation of credit derivatives and application to CDOs. Quantitative Finance, 10(2):195–208, 2010.

- [Var84] S. R. S. Varadhan. Large deviations and applications, volume 46 of CBMS-NSF Regional Conference Series in Applied Mathematics. Society for Industrial and Applied Mathematics (SIAM), Philadelphia. PA, 1984.

- [Vas91] Oldrich Vasicek. Limiting loan loss probability distribution. Technical Report, KMV Corporation, 1991.

- [ZBGG11] Xiaowei Zhang, Jose Blanchet, Kay Giesecke, and Peter Glynn. Affine point processes: Asymptotic analysis and efficient rare-event simulation. Working Paper, Stanford University, 2011.