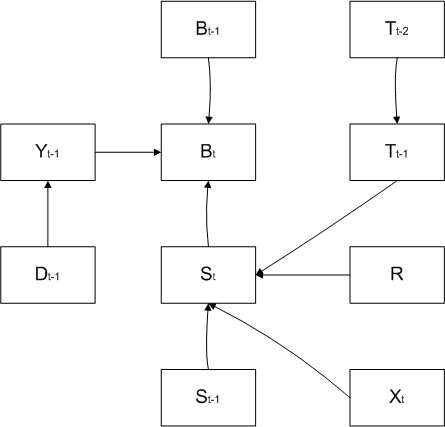

Figure 1: This diagram depicts the underlying causal structure of the model. See the text for the definitions of D,Y,B,T,S.

The model concerns the following random variables:

•

A discrete Markov process which records the behavioural state of the debtor during the time period - measured in months. The state is measured in the middle of each month.

•

A discrete-valued process which records the strongest debt management intervention that was applied to the debtor during the time period .

•

an entity-specific variable, gives the final result of the debtor’s most immediate previous debt case - NA, paid in full, liquidation/bankrupty, full write-off, partial write-off.

•

is the economic state at time period . This measure is obtained through clustering a pertinent collection of economic variables: change in CPI, change in unemployment, change in the average weekly wage, etc. The underlying variables for are varying quarterly, so will be constant in blocks of three months.

•

is a latent discrete Markov process which categorizes debtors in a time period into the behavioural scheme that governs the generation of . The model supposes that influences , and hence influences indirectly.

•

is a positive real-valued variable, given by

•

is a categorization of into - this is governed by a parameter that needs to be inferred. the notion is that as a debtor gets closer to being paid in full, its probability of making a large lump-sum payment to clear its debt may change.

We introduce a set of parameters as follows:

•

: defined by if and only if .

•

: a list of transition matrices, one for each combination of values of .

•

: a list of initial probabilities, one for each combination of values of .

•

: a list of transition matrices, one for each combination of values of and .

•

: a list of initial probabilities, one for each value of .

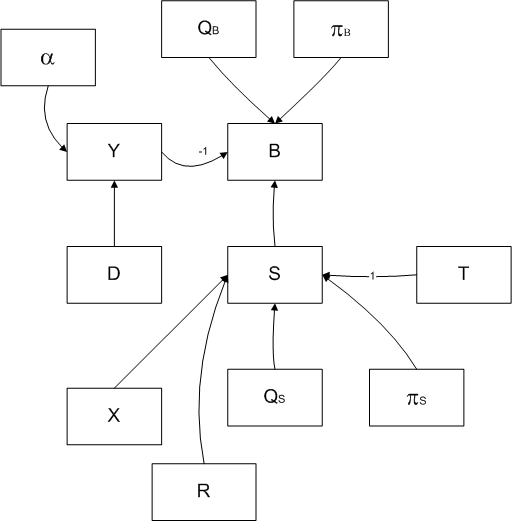

Figure 2 depicts the causal structure of the variables and the parameters - we have now expressed each of the variables as a vector of length as long as the number of observation periods.

Figure 2: This diagram depicts the underlying causal structure of the model, including the parameters. Refer to the text for definitions of the parameters

Every debt case begins at a time period and ends at a time period . If the debt case is indexed by , the the beginning is and the end is . There will be observations of , , , and from through to .

The log-likelihood of observing a single debt case is maximized when we maximize:

We apply the EM algorithm to , taking the expected value of conditional on and the -th iteration of the parameters , .

For this we define the responsibilities for each debt case, , and time , :

for ; and for ,

It is clear that , or if , - hence we need only compute .

This is done using the Forward-Backward algorithm:

1 Calculating

This calculation is standard, but we present it for completeness.

Define the following four sets of probabilities:

•

•

, .

•

,

•

,.

Then

and

with . The normalizing constants can be found by noting that and .

Having obtained (the forward matrices) we can calculate the backward matrices as follows:

Set .

For ,

2 Update equations for the M-step

The formulas that follow are the result of straightforward calculations.

Note that depends on an unknown value of . The approach will be to fit for a range of values of , and to choose the that gives the maximum value to: