Sequential Quasi-Monte Carlo

Abstract

We derive and study SQMC (Sequential Quasi-Monte Carlo), a class of algorithms obtained by introducing QMC point sets in particle filtering. SQMC is related to, and may be seen as an extension of, the array-RQMC algorithm of L’Ecuyer et al., (2006). The complexity of SQMC is , where is the number of simulations at each iteration, and its error rate is smaller than the Monte Carlo rate . The only requirement to implement SQMC is the ability to write the simulation of particle given as a deterministic function of and a fixed number of uniform variates. We show that SQMC is amenable to the same extensions as standard SMC, such as forward smoothing, backward smoothing, unbiased likelihood evaluation, and so on. In particular, SQMC may replace SMC within a PMCMC (particle Markov chain Monte Carlo) algorithm. We establish several convergence results. We provide numerical evidence that SQMC may significantly outperform SMC in practical scenarios.

Key-words: Array-RQMC; Low discrepancy; Particle filtering; Quasi-Monte Carlo; Randomized Quasi-Monte Carlo; Sequential Monte Carlo

1 Introduction

Sequential Monte Carlo (SMC, also known as particle filtering) is a class of algorithms for computing recursively Monte Carlo approximations of a sequence of distributions , , . The initial motivation of SMC was the filtering of state-space models (also known as hidden Markov models); that is, given a latent Markov process , observed imperfectly as e.g. , recover at every time the distribution of given the data . SMC’s popularity stems from the fact it is the only realistic approach for filtering and related problems outside very specific cases (such as the linear Gaussian model). Recent research has further increased interest in SMC, especially in Statistics, in at least two directions. First, several papers (Neal,, 2001; Chopin,, 2002; Del Moral et al.,, 2006) have extended SMC to non-sequential problems; that is, to sample from distribution , one applies SMC to some artificial sequence that ends up at . In certain cases, such an approach outperforms MCMC (Markov chain Monte Carlo) significantly. Second, the seminal paper of Andrieu et al., (2010) established that SMC may be used as a proposal mechanism within MCMC, leading to so called PMCMC (particle MCMC) algorithms. While not restricted to such problems, PMCMC is the only possible approach for inference in state-space models such that the transition kernel of may be sampled from, but does not admit a tractable density. Excitement about PMCMC is evidenced by the 30 papers or so that have appeared in the last two years on possible applications and extensions.

Informally, the error rate of SMC at iteration is , where is some function of . There has been a lot of work on SMC error rates (e.g. Del Moral,, 2004), but it seems fair to say that most of it has focussed on the first factor ; that is, whether to establish that the error rate is bounded uniformly in time, , or to reduce through more efficient algorithmic designs, such as better proposal kernels or resampling schemes.

In this work, we focus on the second factor , i.e. we want the error rate to converge quicker relative to than the standard Monte Carlo rate . To do so, we adapt to the SMC context ideas borrowed from QMC (Quasi-Monte Carlo); that is, the idea of replacing random numbers by low discrepancy point sets.

The following subsections contain very brief introductions to SMC and QMC, with an exclusive focus on the concepts that are essential to follow this work. For a more extensive presentation of SMC, the reader is referred to the books of Doucet et al., (2001), Del Moral, (2004) and Cappé et al., (2005), while for QMC and RQMC, see Chapter 5 of Glasserman, (2004), Chapters 5 and 6 of Lemieux, (2009), and Dick and Pillichshammer, (2010).

1.1 Introduction to SMC

As already mentioned, the initial motivation of SMC is the sequential analysis of state-space models; that, is models for a Markov chain in ,

which is observed only indirectly through some , with density .

This kind of model arises in many areas of science: in tracking for instance, may be the position of a ship (in two dimensions) or a plane (in three dimensions), and may be a noisy angular observation (radar). In Ecology, would be the size of a population of bats in a cave, and would be plus noise. And so on.

The most standard inferential task for such models is that of filtering; that is, to recover iteratively in time , , the distribution of , given the data collected up time , . One may also be interested in smoothing, , or likelihood evaluation, , notably when the model depends on a fixed parameter which should be learnt from the data.

A simple Monte Carlo approach to filtering is sequential importance sampling: choose an initial distribution , a sequence of Markov kernels , , then simulate times iteratively from these ’s, , , and reweight ‘particle’ (simulation) as follows: , , where the weight functions are defined as

| (1) |

and in the denominator denotes the conditional probability density associated to kernel . Then it is easy to check that the weighted average is a consistent estimate of the filtering expectation , as . However, it is well known that, even for carefully chosen proposal densities , sequential importance sampling quickly degenerates: as time progresses, more and more particles get a negligible weight.

Surprisingly, there is a simple solution to this degeneracy problem: one may resample the particles; that is, draw times with replacement from the set of particles, with probabilities proportional to the weights . In this way, particles with low weight gets quickly discarded, while particles with large weight may get many children at the following iteration. Empirically, the impact of resampling is dramatic: the variance of filtering estimates typically remains stable over time, while without resampling it diverges exponentially fast.

The idea of using resampling may be traced back to Gordon et al., (1993), and has initiated the whole field of particle filtering. See Algorithm 1 for a summary of a basic PF (particle filter). The price to pay for introducing resampling is that it creates non-trivial dependencies between the particles, which complicates the formal study of such algorithms. In particular, establishing convergence (as ) is non-trivial, although the error rate of SMC is known to be ; see e.g. the central limit theorems of Del Moral and Guionnet, (1999), Chopin, (2004) and Künsch, (2005). We shall see that it is also the resampling step that makes the introduction of Quasi-Monte Carlo into SMC non-trivial.

At time ,

- (a)

-

Generate for all .

- (b)

-

Compute and for all .

From time to time ,

- (a)

-

Generate for all , the multinomial distribution that produces outcome with probability . See Algorithm 2.

- (b)

-

Generate for all .

- (c)

-

Compute , and for all .

The complexity of SMC is . In particular, to implement the resampling step in time (Step (a) at times in Algorithm 1), one proceeds as follows: (a) generate , where the are independent uniform variates (see p.214 of Devroye,, 1986, for a well-known algorithm to generate directly in time, without any sorting); and (b) use the inverse transform method for discrete distributions, recalled in Algorithm 2. We will re-use Algorithm 2 in SQMC.

1.2 Introduction to QMC

QMC (Quasi-Monte Carlo) is generally presented as a way to perform integration with respect to the (semi-closed) hypercube of dimension :

where the vectors must be chosen so as to have “low discrepancy”, that is, informally, to be spread evenly over . (We respect the standard convention in the QMC literature to work with space , rather than , as it turns out to be technically more convenient.)

Formally, the general notion of discrepancy is defined as

where is the volume (Lebesgue measure on ) of , and is a set of measurable sets. Two discrepancies are particularly useful in this work: the extreme discrepancy,

which is the discrepancy relative to the set of dimensional intervals , ; and the star discrepancy:

where again , . When , the star discrepancy is the Kolmogorov-Smirnov statistic for an uniformity test of the points .

These two discrepancies are related as follows (Niederreiter,, 1992, Proposition 2.4):

The importance of the concept of discrepancy, and in particular of the star discrepancy, is highlighted by the Koksma–Hlawka inequality (see e.g. Kuipers and Niederreiter,, 1974, Theorem 5.1):

which conveniently separates the effect of the smoothness of (as measured by , the total variation in the sense of Hardy and Krause, see Chapter 2 of Niederreiter,, 1992 for a definition), and the effect of the discrepancy of the points . The quantity is generally too difficult to compute in practice, and the Koksma–Hlawka inequality is used mainly to determine the asymptotic error rate (as ), through the quantity .

There are several methods to construct so that for any ; which is of course better than the Monte Carlo rate . The best known rates are for QMC point sets that are allowed to depend on (i.e. are not necessarily the first elements of ) and for QMC sequences (that is are the first elements of a sequence which may be generated iteratively). For simplicity, we will not distinguish further QMC point sets and QMC sequences, and will use the same notation in both cases (although our results will apply to both types of construction).

These asymptotic rates seem to indicate that the comparative performance of QMC over Monte Carlo should deteriorate with : for , only for . But since these rates correspond to an upper bound for the error size, it is hard to determine beforehand if and when QMC “breaks” with the dimension. For instance, Glasserman, (2004, p.327) exhibits a a numerical example where QMC remains competitive relative to Monte Carlo for and .

Describing the different strategies to construct low-discrepancy point sets is beyond the scope of this paper; see again the aforementioned books on QMC. Figure 1 illustrates the greater regularity of a QMC point set over a set of random points.

1.3 Introduction to RQMC

RQMC (randomized QMC) amounts to randomize the points in such a way that (a) they still have low discrepancy (with probability one); and (b) each marginally. The simplest construction of such RQMC point sets is the random shift method proposed by Cranley and Patterson, (1976) in which we take , where and is a low-discrepancy point set.

RQMC has two advantages over QMC. First, one then obtains an unbiased estimator of the integral of interest:

which makes it possible to evaluate the approximation error through independent replications. We will see that, in our context, this unbiasedness property will also be very convenient for another reason: namely to provide an unbiased estimate of the likelihood of the considered state-space model.

Second, Owen, 1997a ; Owen, 1997b ; Owen, (1998) established that randomization may lead to better rates, in the following sense: under appropriate conditions, and for a certain type of randomization scheme known as nested scrambling, the mean square error of a RQMC estimator is . The intuition behind this rather striking result is that randomization may lead to cancellation of certain error terms.

1.4 A note on array-RQMC

Consider the following problem: we have a Markov chain in , whose evolution may be formulated as

and we wish to compute the expectation of , for certain functions .

From the two previous sections, we see that a simple approach to this problem would be to generate a QMC (or RQMC) point set in , , to transform into , and finally to return the corresponding empirical average, . The problem with this direct approach is that the dimension of may be very large, and, as we have seen, equidistribution properties of QMC point sets (as measured by the star discrepancy) deteriorate with the dimension.

An elegant alternative to this approach is the array-RQMC algorithm of L’Ecuyer et al., (2006), see also Lécot and Ogawa, (2002), Lécot and Tuffin, (2004), and L’Ecuyer et al., (2009). The main idea of this method is to replace the QMC point set in by QMC points sets in . Then, is obtained as , where the ancestor of is chosen so as to be the -th “smallest” point among the ’s. Note that array-RQMC therefore requires to specify a total order for the state space ; for instance one may define a certain so that means that is “smaller” than .

Array-RQMC is shown to have excellent empirical performance in the aforementioned papers. On the other hand, it is currently lacking in terms of supporting theory (see however l2008randomized, for ); in particular, it is not clear how to choose the order , beside the obvious case where . The SQMC algorithm we develop in this paper may be seen as an extension of array-RQMC to particle filtering. In particular, it re-uses the essential idea to generate one QMC point set at each step of the simulation process. As an added benefit, the convergence results we obtain for SQMC also apply to array-RQMC, provided the state space is ordered through the Hilbert curve, as explained later.

1.5 Background, plan and notations

QMC is already very popular in Finance for e.g. derivative pricing (Glasserman,, 2004), and one may wonder why it has not received more attention in Statistics so far. The main reason seems to be the perceived difficulty to adapt QMC to non-independent simulation such as MCMC (Markov chain Monte Carlo); see however Chen et al., (2011) and references therein, in particular Tribble, (2007), for exciting numerical and theoretical results in this direction which ought to change this perception.

Regarding SMC, we are aware of two previous attempts to develop QMC versions of these algorithms: Lemieux et al., (2001) and Fearnhead, (2005); see also Guo and Wang, (2006) who essentially proposed the same algorithm as Fearnhead, (2005). The first paper casts SMC as a Monte Carlo algorithm in dimensions, where , and therefore requires to generate a low-discrepancy point set in . But, as we have already explained, such an approach may not work well when is too large.

Our approach is closer to, and partly inspired by, the RPF (regularized particle filter) of Fearnhead, (2005), who, in the same spirit as array-RQMC, casts SMC as a sequence of successive importance sampling steps of dimension . (The paper focus on the case.) The main limitation of the RPF is that it has complexity . This is because the importance sampling steps are defined with respect to a target which is a mixture of components, hence the evaluation of a single importance weight costs .

The SQMC algorithm we develop in this paper has complexity per time step. It is also based on a sequence of importance sampling steps, but of dimension ; the first component is used to determine which ancestor should be assigned to particle . For , this requires us to “project” the set of ancestors into , by means of a space-filling curve known as the Hilbert curve. The choice of this particular space-filling curve is not only for computational convenience, but also because of its nice properties regarding conversion of discrepancy, as we will explain in the paper. (One referee pointed out to us that the use of Hilbert curve in the context of array-RQMC has been suggested by Wächter and Keller, (2008), but not implemented.)

The paper is organised as follows. Section 2 derives the general SQMC algorithm, first for , then for any through the use of the Hilbert curve. Section 3 presents several convergence results; proofs of these results are in the Appendix. Section 4 shows how several standard extensions of SMC, such as forward smoothing, backward smoothing, and PMCMC, may be adapted to SQMC. Section 5 compares numerically SQMC with SMC. Section 6 concludes.

Most random variables in this work will be vectors in , and will be denoted in bold face, or . In particular, will be an open set of . The Lebesgue measure in dimension is denoted by . Let be the set of probability measures defined on dominated by (restricted to ), and be the expectation of function relative to . Let be the set of integers for . We also use this notation for collections of random variables, e.g. , and so on.

2 SQMC

The objective of this section is to construct the SQMC algorithm. To this aim, we discuss how to rewrite SMC as a deterministic function of independent uniform variates , , which then may be replaced by low-discrepancy point sets.

2.1 SMC formalisation

A closer inspection of our basic particle filter, Algorithm 1, reveals that this algorithm is entirely determined by (a) the sequence of proposal kernels (which determine how particles are simulated) and (b) the sequence of weight functions (which determine how particles are weighted). Our introduction to particle filtering focussed on the specific expression (1) for , but useful SMC algorithms may be obtained by considering other weight functions; see e.g. the auxiliary particle filter of Pitt and Shephard, (1999), as explained in Johansen and Doucet, (2008), or the SMC algorithms for non-sequential problems mentioned in the introduction.

The exact expression and meaning of and will not play a particular role in the rest of the paper, so it is best to think of SMC from now on as a generic algorithm, again based on a certain sequence , being an initial distribution, and being a Markov kernel for , and a certain sequence of functions, , , which produces the following consistent (as ) estimators:

where , and and are defined as follows:

| (2) | |||||

| (3) | |||||

| (4) |

with expectations taken with respect to the law of the non-homogeneous Markov chain , e.g.

and with the conventions that and empty products equal one; e.g. .

For instance, for the standard filtering problem covered in our introduction, where is set to (1), is the filtering expectation of , i.e. , and is the predictive distribution of , i.e. .

2.2 Towards SQMC: SMC as a sequence of importance sampling steps

QMC requires to write any simulation as an explicit function of uniform variates. We therefore make the following assumption for our generic SMC sampler: to generate , one computes , and to generate , one computes , where , and the functions are easy to evaluate.

Iteration of Algorithm 1 amounts to an importance sampling step, from to , which produces the following estimator

of ). To introduce QMC at this stage, we take where is a low-discrepancy point set in .

The key remark that underpins SQMC is that iteration of Algorithm 1 also amounts to an importance sampling step, but this time from

| (5) |

to

where and are two random probability measures defined over , a set of dimension . In particular, the generation of random variables and in Steps (a) and (b) of Algorithm 1 is equivalent to sampling times independently random variables from : i.e. (not to be mistaken with ), and .

Based on these remarks, the general idea behind SQMC is to replace at iteration the IID random numbers sampled from by a low-discrepancy point set relative to the same distribution.

When , this idea may be implemented as follows: generate a low-discrepancy point set in , let , then set , , where is the generalised inverse of the empirical CDF

It is easy to see that the most efficient way to compute for all is (a) to sort the ’s, i.e. to find permutation such that , (b) to sort the , call the corresponding result; (c) to obtain as the output of Algorithm 2, with inputs and ; and finally (d) set .

Algorithm 3 gives a pseudo-code version of SQMC for any , but note how Step (b) at times simplifies to what we have just described for .

When , the inverse transform method cannot be used to sample from the marginal distribution of relative to , at least unless the are “projected” to the real line in some sense. This is the point of the Hilbert curve presented in the next section.

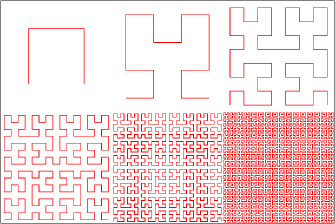

2.3 The Hilbert space-filling curve

The Hilbert curve is a continuous fractal map which “fills” entirely . is obtained as the limit of a sequence , , the first terms of which are depicted in Figure 2.

The function admits a pseudo-inverse , i.e. for all . is not a bijection because certain points have more than one pre-image through ; however the set of such points is of Lebesgue measure 0.

Informally, transforms into , while preserving “locality”: if , are close, then and are close as well. We will establish that also preserves discrepancy: a low-discrepancy point set in remains a low-discrepancy point set in when transformed through . It is these properties that give to the Hilbert curve its appeal in the SQMC context (as opposed to other space filling curves, such as Z-ordering). We refer to Sagan, (1994), Butz, (1969) and Hamilton and Rau-Chaplin, (2008) for how to compute in practice for any . For , we simply set for .

The following technical properties of and will be useful later (but may be skipped on first reading). For , let be the collection of consecutive closed intervals in of equal size and such that . For , belongs to , the set of the closed hypercubes of volume that covers , ; and are adjacent, i.e. have at least one edge in common (adjacency property). If we split into the successive closed intervals , and , then the ’s are simply the splitting of into closed hypercubes of volume (nesting property). Finally, the limit of has the bi-measure property: for any measurable set , and satisfies the Hölder condition for any .

2.4 SQMC for

Assume now , and consider the following change of variables at iteration :

where is the inverse of the Hilbert curve defined in the previous section, and is some user-chosen bijection between and . To preserve the low discrepancy property of it is important to choose for a mapping which is discrepancy preserving. This requires to select such that where the ’s are continuous and strictly monotone. But choosing such a is trivial in most applications; e.g. apply the logistic transformation component-wise when (see Section 5 for more details).

With this change of variables, we obtain particles that lie in , and (5) becomes

Sampling a low-discrepancy sequence from may then proceed exactly as for ; that is: use the inverse transform method to sample points from the marginal distribution , then sample conditionally on , with . The exact details of the corresponding operations are the same as for . We therefore obtain the general SQMC algorithm as described in Algorithm 3.

At time ,

- (a)

-

Generate a QMC or a RQMC point set in , and compute for each .

- (b)

-

Compute and for each .

Iteratively, from time to time ,

- (a)

-

Generate a QMC or a RQMC point set in ; let .

- (b)

-

Hilbert sort: find permutation such that if , or if .

- (c)

-

Find permutation such that , generate using Algorithm 2, with inputs and , and compute for each .

- (e)

-

Compute , and for each .

To fully define SQMC, one must choose a particular method to generate point sets at each iteration. If QMC point sets are generated, one obtains a deterministic algorithm, while if RQMC point sets are generated, one obtains a stochastic algorithm.

2.5 Complexity of SQMC

The complexity of both Steps (b) and (c) (for ) of the SQMC algorithm is , because they include a sort operation. The complexity of Step (a) depends on the chosen method for generating the point sets . For instance, Hong and Hickernell, (2003) propose a method that applies to most constructions of -sequences (such as the Faure, the Sobol’, the Niederreiter or the Niederreiter-Xing sequences). The cost to randomize a QMC point set is only if one chooses the simple random shift approach, while nested scrambling methods for -sequences, which are such that all the results below hold, may be implemented at cost (Owen,, 1995; Hong and Hickernell,, 2003).

To summarise, the overall complexity of SQMC is , provided the method to generate the point sets is chosen appropriately.

3 Convergence study

We concentrate on two types of asymptotic results (as ): consistency, and stochastic bounds, that is bounds on the mean square error for the randomized SQMC algorithm (i.e. SQMC based on randomized QMC point sets). We leave deterministic bounds of the error (for when deterministic QMC point sets are used) to future work. We find stochastic bounds more interesting, because (a) results from (Owen, 1997a, ; Owen, 1997b, ; Owen,, 1998) suggest one might obtain better convergence rates than for deterministic bounds; and (b) the randomized version of SQMC has more applications, as discussed in Section 4.

These results are specialised to the case where the simulation of at time is based on the inverse transform method, as explained in Section 3.1. Certain of our results require to be bounded, so for simplicity we take , and is set to the identity function. (Recall that, to deal with certain QMC technicalities, we follow the standard practice of taking rather than .) The fact that is bounded may not be such a strong restriction, as our results allow for unbounded test functions ; thus, one may accommodate for an unbounded state space (and expectations with respect to that space) through appropriate variable transforms.

We introduce the following extreme norm. For any signed measure over ,

which generalises the extreme discrepancy in the following sense:

for any point set in , where is the operator that associates to its empirical distribution:

Our consistency results will be stated with this norm. Note that implies for any continuous, bounded function , by portmanteau lemma (Van der Vaart,, 2007, Lemma 2.2).

The next subsection explains how the inverse method may be used to generate given . The two following subsections state preliminary results that should provide insights on the main ideas that underpin the proofs of our convergence results. Readers interested mostly in the main results may skip these subsections and go directly to Section 3.4 (consistency) and Section 3.5 (stochastic bounds).

This section will use the following standard notations: for the supremum norm for functions , for the set of square integrable functions and for the set of continuous, bounded functions .

3.1 Inverse transform method

We discuss here how to write the simulation of as , using the inverse transform method. Our convergence results are specialised to this particular .

For a generic distribution , , let be the Rosenblatt transformation (Rosenblatt,, 1952) of defined through the following chain rule decomposition:

where, recursively, being the CDF of the marginal distribution of the first component (relative to ), and for , , being the CDF of component , conditional on ), again relative to . Similarly, we define the multivariate GICDF (generalised inverse CDF) through the following chain rule decomposition:

where, recursively, being the GICDF of the marginal distribution of the first component (relative to ), and for , , being the GICDF of component , conditional on ), again relative to . Note that this function depends on the particular order of the components of . For some probability kernel , define similarly and as, respectively, the Rosenblatt transformation and the multivariate GICDF of distribution for a fixed .

It is well known that taking , and lead to valid simulations algorithms, i.e. if , resp. , then , resp. .

3.2 Preliminary results: importance sampling

Since SQMC is based on importance sampling (e.g. Iteration of Algorithm 3), we need to establish the validity of importance sampling based on low-discrepancy point sets; see Götz, (2002); Aistleitner and Dick, (2014) for other results on QMC-based importance sampling.

Theorem 1.

Let and be two probability measures on such that the Radon-Nikodym derivative is continuous and bounded. Let be a sequence of point sets in such that as , and define

Then, as .

See Section A.1.2 of the Appendix for a proof.

Recall that in our notations we drop the dependence of point sets on , i.e. we write rather than , although in full generality may not necessarily be the first points of a fixed sequence.

The next theorem gives the stochastic error rate when a RQMC point set is used.

Theorem 2.

Consider the set-up of Theorem 1. Let be a sequence of random point sets in such that marginally and, ,

where as . Let and assume that either one of the following two conditions is verified:

-

1.

is continuous and, for any , there exists a such that, almost surely, , ;

-

2.

for any there exists a such that, almost surely,

Then, for all ,

See Section A.1.2 of the Appendix for a proof.

To fix ideas, note that several RQMC strategies reach the Monte Carlo error rate and therefore fulfil the assumptions above with for any (see e.g. Owen, 1997a, ; Owen,, 1998). In addition, nested scrambling methods for -sequences in base (Owen,, 1995; Matoǔsek,, 1998; Hong and Hickernell,, 2003) are such that . This result is established for in Owen, 1997a ; Owen, (1998) and extended for an arbitrary in Gerber, (2014).

3.3 Preliminary results: Hilbert curve and discrepancy

We motivated the use of the Hilbert curve as a way to transform back and forth between and while preserving low discrepancy in some sense. This section formalises this idea.

For a probability measure on , we write the image by of . For a kernel , we write the image of by the mapping , where denotes the joint probability measure .

The following theorem is a technical result on the conversion of discrepancy through .

Theorem 3.

Let be a sequence of probability measure on such that, , where admits a bounded probability density . Then

See Section A.2.1 of the Appendix for a proof.

The following theorem is an extension of Hlawka and Mück, (1972, “Satz 2”), which establishes the validity, in the context of QMC, of the multivariate GICDF approach described in Section 3.1. More precisely, for a probability measure on , Hlawka and Mück, (1972, “Satz 2”) show that (under some conditions on , see below).

Theorem 4.

Let be a Markov kernel and assume that:

-

1.

For a fixed , the -th coordinate of is strictly increasing in , , and, viewed as a function of and , is Lipschitz;

-

2.

, , and .

-

3.

The sequence is such that as , where admits a strictly positive bounded density .

Let , , be a sequence of point sets in such that as , and define where

Then

See Section A.2.2 of the Appendix for a proof.

Assumption 1 regarding the regularity of the vector-valued function is the main assumption of the above theorem and comes from Hlawka and Mück, (1972, “Satz 2”). It is verified as soon as kernel admits a density that is continuously differentiable on (Hlawka and Mück,, 1972, p.232). Assumption 2 is a technical condition, which will always hold under the assumptions of our main results.

3.4 Consistency

We are now able to establish the consistency of SQMC; see Appendix A.3 for a proof of the following theorem. For convenience, let when .

Theorem 5.

Consider the set-up of Algorithm 3 where, for all , is a (non random) sequence of point sets in , with and for , such that as . Assume the following holds for all :

-

1.

The components of are pairwise distinct, for .

-

2.

is continuous and bounded;

- 3.

-

4.

where is a strictly positive bounded density.

Let . Then, under Assumptions 1-4, as ,

Assumption 1 is stronger than necessary because for the result to hold it is enough that the number of identical particles does not grow too quickly as . Note that this is a very weak restriction since Assumption 1 holds almost surely when RQMC point sets are used, since then the particles are generated from a continuous GICDF. The assumption that the weight functions are bounded is standard in SMC literature (see e.g. Del Moral,, 2004).

3.5 Stochastic bounds

Our second main result concerns stochastic bounds for the randomized version of SQMC, i.e. SQMC based on randomized point sets . See Section A.4 of the Appendix for a proof of the next result.

Theorem 6.

Consider the set-up of Algorithm 3 where , , are independent sequences of random point sets in , with and for , such that, for all , marginally and

-

1.

For any , there exists a such that, almost surely, , .

-

2.

For any function , where , and where both and do not depend on .

In addition, assume that the Assumptions of Theorem 5 are verified and that is continuous. Let for all . Then, ,

Note that the implicit constants in the line above may depend on . Assumptions 1 and 2 are verified for if is the first points of a nested scrambled -sequences in base . This result is established for in Owen, 1997a ; Owen, (1998) and can be extended to any pattern of using Hickernell and Yue, (2001, Lemma 1). Consequently, for this construction of RQMC point sets, Theorem 6 shows that the approximation error of SQMC goes to zero at least as fast as for SMC. However, contrary to the convergence rate of SMC, this rate for SQMC based on nested scrambled -sequences is not exact but results from a worst case analysis. We can therefore expect to reach faster convergence on a smaller class of functions. The following result shows that it is indeed the case on the class on continuous and bounded functions; see Section A.4.4 of the Appendix for a proof.

Theorem 7.

Consider the set-up of Algorithm 3 where , , are -sequences in base , with and for , independently scrambled such that results in Owen, 1997a ; Owen, (1998) hold. Let , , and assume the following holds:

-

1.

Assumptions of Theorem (6) are verified;

-

2.

For , is a continuous function of .

Let . Then, ,

4 Extensions

4.1 Unbiased estimation of evidence, PMCMC

Like SMC, the randomized version of SQMC (that is SQMC based on RQMC point sets) provides an unbiased estimator of the normalising constant of the Feynman-Kac model, see (2).

Lemma 8.

Provided that is a RQMC point set in for (i.e. marginally), with and for , the following quantity

is an unbiased estimator of , .

We omit the proof, as it follows the same steps as for SMC (Del Moral,, 1996).

In a state-space model parametrised by , is the marginal likelihood of the data up to time . One may want to implement a Metropolis-Hastings sampler with respect to posterior density for the full dataset and for a prior distribution , but is typically intractable.

Andrieu et al., (2010) established that, by substituting with an unbiased estimate of in a Metropolis sampler, one obtains an exact MCMC (Markov chain Monte Carlo) algorithm, in the sense that the corresponding MCMC kernel leaves invariant . The so obtained algorithm is called PMMH (Particle marginal Metropolis-Hastings). Andrieu et al., (2010) use SMC to obtain an unbiased estimate of ), that is, at each iteration a SMC sampler is run to obtain that estimate. We will call PMMH-SQMC the same algorithm, but with SQMC replacing SMC for the evaluation of an unbiased estimate of the likelihood.

The acceptance rate of PMMH depends directly on the variability of the estimates of . Since the point of (randomized) SQMC is to provide estimates with a lower variance than SMC (for a given ), one may expect that PMMH-SQMC may require a smaller number of particles than standard PMMH for satisfactory acceptance rates; see Section 5 for a numerical illustration of this.

4.2 Smoothing

Smoothing amounts to compute expectations of functions of the complete trajectory ; e.g. is the expectation of conditional on data for a state-space model with Markov process and observed process . See Briers et al., (2010) for a general overview on SMC smoothing algorithms. This section discusses how to adapt certain of these algorithms to SQMC.

4.2.1 Forward smoothing

Forward smoothing amounts to carry forward the complete trajectories of the particles, rather than simply keeping the last component (as in Algorithm 1). A simple way to formalise forward smoothing is to introduce a path Feynman-Kac model, corresponding to the inhomogeneous Markov process , and weight function (abusing notations) . Then forward smoothing amounts to Algorithm 1 applied to this path Feynman-Kac model (substituting with ).

One may use the same remark to define a SQMC version of forward smoothing: i.e. simply apply SQMC to the same path Feynman-Kac model. The only required modification is that the Hilbert sort of Step (b) at times must now operate on some transformation of the vectors , of dimension , rather than vectors of dimension as in the original version.

Forward smoothing is sometimes used to approximate the smoothing expectation of additive functions, , such as the score function of certain models (e.g. Poyiadjis et al.,, 2011). In that case, one may instead apply SQMC to the Feynman-Kac model corresponding to the inhomogeneous Markov process . This means that in practice, one may implement the Hilbert sort on a space of much lower dimension (i.e. the dimension of this new ), which is computationally more convenient.

4.2.2 Backward smoothing

Backward smoothing consists of two steps: (a) a forward pass, where SMC is run from time to time ; and (b) a backward pass, where one constructs a trajectory recursively backwards in time, by selecting randomly each component out of the particle values generated during the forward pass. An advantage of backward smoothing is that it is less prone to degenerate than forward smoothing. A drawback of backward smoothing is that generating a single trajectory costs , hence obtaining of them costs ).

Backward smoothing for SQMC may be implemented in a similar way to SMC: see Algorithm 4 for the backward pass that generates trajectories from the output of the SQMC algorithm. Note that backward smoothing requires that the Markov kernel admits a closed-form density with respect to an appropriate dominating measure. Then one may compute empirical averages over the so obtained trajectories to obtain smoothing estimates in the usual way.

5 Numerical study

The objective of this section is to compare the performance of SMC and SQMC. Our comparisons are either for the same number of particles , or for the same amount of CPU time to take into account the fact that SQMC has greater complexity than SMC. These comparisons will often summarised through gain factors, which we define as ratios of mean square errors (for a certain quantity) between SMC and SQMC.

In SQMC, we generate as a Owen, (1995) nested scrambled Sobol’ sequence using the C++ library of T. Kollig and A. Keller (http://www.uni-kl.de/AG-Heinrich/SamplePack.html). Note that both the generation and the randomization of -sequences in base 2 (such as the Sobol’ sequence) are very fast since logical operations can be used. In order to sort the particles according to their Hilbert index we use the C++ library of Chris Hamilton (http://web.cs.dal.ca/~chamilto/hilbert/index.html) to evaluate , . Again, Hilbert computations are very fast as they are based on logical operations (see Hamilton and Rau-Chaplin,, 2008, for more details). In addition, thanks to the nesting property of the Hilbert curve (see Section 2.3) we only need to take large enough such that different particles are mapped into different points of . Function is set to the inverse transform described in Section 3.1, and function to a component-wise (rescaled) logistic transform; that is, with

and where the constants and are used to solve numerical problems due to high values of . For instance, when is a stationary process we chose and where and are respectively the mean and the standard deviation of the stationary distribution of .

SMC is implemented using systematic resampling (Carpenter et al.,, 1999) and all the random variables are generated using standard methods (i.e. not using the multivariate GICDF). The C/C++ code implementing both SMC and SQMC is available on-line at https://bitbucket.org/mgerber/sqmc.

Even if Theorems 6 and 7 are valid for any pattern of , choosing for powers of 2 (with 2 the base of the Sobol’ sequence) is both natural and optimal for QMC methods based on (scrambled) -sequences (see e.g. Owen, 1997b, ; Hickernell and Yue,, 2001; and Chapter 5 of Dick and Pillichshammer,, 2010). Comparing the performance of SQMC for different patterns of is beyond the scope of this paper (see Gerber,, 2014, for a discussion of this point) and therefore we follow in this numerical study the standard approach in the QMC literature by considering values of that are powers of 2. We nevertheless do one exception to this rule for the PMMH estimation on real data (Section 5.3) because doubling the number of particles to reduce the variance of the likelihood estimate used in the Metropolis-Hastings ratio may be very inefficient from a computational point of view. As we will see, allowing to differ from powers of the Sobol’ base does not seem to alter the performance of SQMC.

One may expect the two following situations to be challenging for SQMC: (a) small (because our results are asymptotic); and (b) large (because of the usual deterioration of QMC with respect of the dimension, and also because of the Hilbert sort step). Thus we consider examples of varying dimensions (from 1 to 10), and we will also make vary within a large range (between and ).

5.1 Example 1: A non linear and non stationary univariate model

We consider the following popular toy example (Gordon et al.,, 1993; Kitagawa,, 1996):

| (6) |

and , where denotes the -dimensional Gaussian distribution with mean and covariance matrix . We generate observations from 100 time steps of the model, with the parameters set as in Gordon et al., (1993): , , , . Note that inference in this model is non trivial because the observation does not allow to identify the sign of , and because the weight function is bimodal if (with modes at ). In addition, we expect this model to be challenging for SQMC due to the high non linearity of the Markov transition .

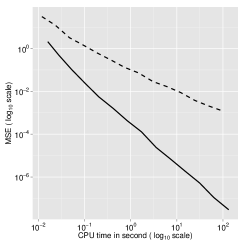

All the results presented below are based on 500 independent runs of SMC and SQMC. Figure LABEL:fig:UnivModel:Lik presents results concerning the estimation of the log-likelihood functions evaluated at the true value of the parameters. The two top graphs show that, compared to SMC, SQMC yields faster convergence of both the mean and the variance of the estimates.

These better consistency properties of SQMC are also illustrated on the bottom left graph of Figure LABEL:fig:UnivModel:Lik where we have reported for each the range in which lies the 500 estimates of the log-likelihood. From this plot we see that quickly the SQMC estimates stay in a very tiny interval while, on the contrary, the SMC estimates are much more dispersed, even for large values of .

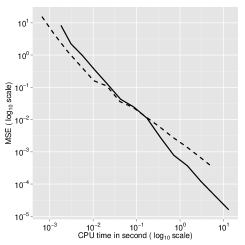

The bottom right panel of Figure LABEL:fig:UnivModel:Lik shows the MSE of SQMC and SMC as a function of CPU time. One sees that the gain of SQMC over SMC does not only increase with , as predicted by the theory, but also with the CPU time which is of more practical interest. On the other hand, in this particular case (log-likelihood evaluation for this univariate model), when is small the reduction in MSE brought by SQMC does not compensate its greater running time. Nevertheless, we observe that SQMC outperforms SMC very quickly, that is, as soon as the CPU time is larger or equal to seconds.

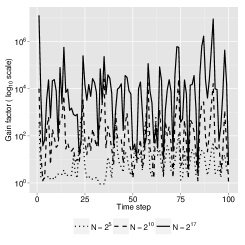

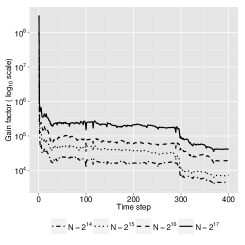

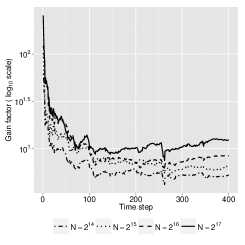

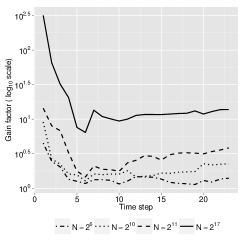

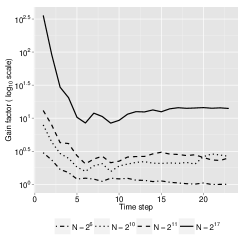

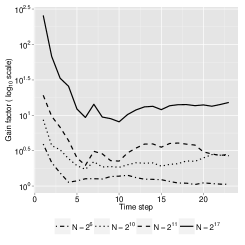

In the left graph of Figure 3 we have reported the gain factor for the estimation of as a function of and for different values of . From this plot we observe both significant and increasing gain of SQMC over SMC.

The right panel of Figure 3 compares SQMC and SMC backward smoothing for the estimation of as a function of and for . As for the filtering problem, SQMC significantly outperforms SMC with gain factors that increase with the number of particles.

5.2 Example 2: Multivariate stochastic volatility model

We consider the following multivariate stochastic volatility model (SV) proposed by Chan et al., (2006):

| (7) |

where , and are diagonal matrices and , with a correlation matrix and .

In order to study the relative performance of SQMC over SMC as the dimension of the hidden process increases we perform simulations for . The parameters we use for the simulations are the same as in Chan et al., (2006): , , for all and

where is the -dimensional identity matrix, and is the matrix having one in all its entries. Note that the errors terms and are correlated so that the weight function depends now both on and on . The prior distribution for is the stationary distribution of the process and we take .

|

|

|

|

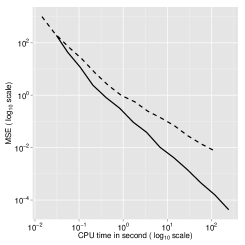

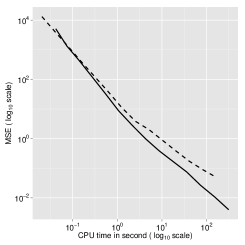

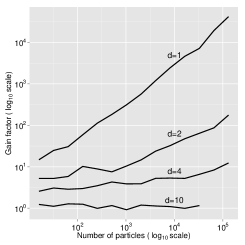

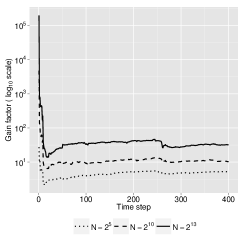

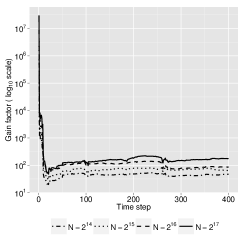

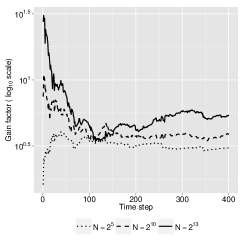

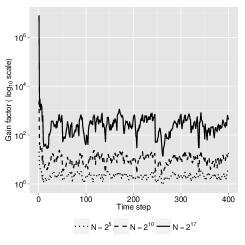

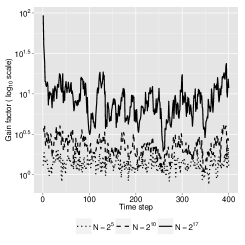

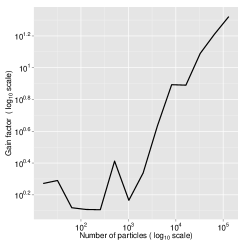

The three first panels of Figure 4 present results for the estimation of the log-likelihood (evaluated at the true value of the parameters and for the complete dataset ), for . One sees that the gain factor increases quickly with , and, more importantly, the MSE of SQMC converges faster than SMC even as a function of CPU time. In fact, except for a very small interval for the univariate model, SQMC always outperforms SMC in terms of MSE for the same CPU effort. We note the particularly impressive values of the gain factor we obtain for when is large: around for . The last panel of Figure 4 plots the gain factors as a function of , for same values of , plus . The improvement brought by SQMC decreases with the dimension, and in fact, for , the gain factor is essentially one for the considered values of ; yet for we still observe some notable improvement; e.g. a gain factor of 10 for . We now focus on , 2 and 4.

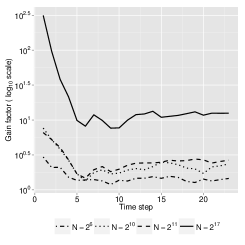

Figure 5 represents the evolution with respect to of the MSE for the partial log-likelihood of data up to time ; gain factors are reported for different values of . As we can see from these graphs, the performance of SQMC does not seem to depreciate with .

Finally, Figure 6 shows that SQMC also give impressive gain when concerning the estimation of the filtering expectation of the first component of .

| Univariate SV model | |

|

|

| Bivariate SV model | |

|

|

| Four dimensional SV model | |

|

|

| Bivariate SV model | Four dimensional SV model |

|---|---|

|

|

5.3 Application: Bayesian estimation of MSV using PMMH on real data

To compare SMC to SQMC when used as a way to approximate the likelihood within a PMMH algorithm, as described in Section 4.1, we turn our attention to the Bayesian estimation of the multivariate SV model (7), for . As in Chan et al., (2006), we take the following prior:

where and denotes respectively the diagonal elements of and , and a flat prior for . In addition, we assume that is uniformly distributed on the space of correlation matrices which are such that the errors terms and are independents (no leverage effects). To sample from the posterior distribution of the parameters we use a Gaussian random walk Metropolis-Hastings algorithm with covariance matrix calibrated so that the acceptance probability of the algorithm becomes, as , close to 25%. The matrix , as well as the starting point of the Markov chain, are calibrated using a pilot run of the algorithm with and starting at the value of the parameters we used above for the simulations. To compare PMMH-SQMC with PMMH-SMC, we run the two algorithms during iterations and for values of ranging from 10 to 200, where increases from 10 to 100 by increment of 10 and then by increment of 50.

We consider the following dataset: the two series are the mean-corrected daily return on the Nasdaq and S&P 500 indices for the period ranging from the January 2012 to the 21 October 2013 so that the data set contains observations.

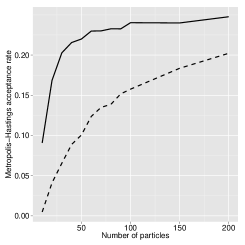

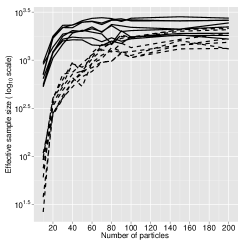

Figure 7 shows the Metropolis-Hastings acceptance rate and the effective sample sizes (see Robert and Casella,, 2004, Section 12.3.5, for a definition) for the PMMH-SQMC algorithm and for the standard PMMH algorithm. We first observe that the acceptance rate of PMMH-SQMC increases very quickly with . Indeed, it is already of 20% for only 30 particles while for the same number of particles the acceptance rate for the standard PMMH is approximatively 6.5%. As far as the acceptance rate is concerned, there is no significant gain to take for the PMMH-SQMC algorithm while for the plain Monte Carlo algorithm the acceptance rate is only about 20% for and therefore much smaller than the target of 25%. Looking at the results for the effective sample sizes (ESSs), we see that the same conclusions hold. More precisely, for the PMMH-SQMC algorithm, the ESSs increase with much faster than for PMMH-SMC. Indeed, for , the ESSs for the former is between 2.18 and 14.94 times larger than for PMMH-SMC.

5.4 Example 3: Neural decoding

Neural decoding models are used for brain-machine interface in order to make inference about an organism’s environment from its neural activity. More precisely, we consider the problem of decoding a set of environment variables , from the firing ensemble of neurons. The latent vector may be interpreted as two-dimensional hand kinetics for motor cortical decoding (see Koyama et al.,, 2010, and references therein for more details about neural decoding models). Noting the vector of velocities, the neural decoding model we consider is given by (Koyama et al.,, 2010)

| (8) |

and , where , the ’s are conditionally independent, denotes the Poisson distribution with parameter , is the duration of the interval over which spikes are counted at each time step, and

Realistic values for the parameters, see Koyama et al., (2010), that we will take in ours simulations, are , , , , , .

One important aspect of this model is that the dimension of the noise term is lower than the dimension of . As a result, two components of are deterministic functions of . Many tracking problems have a similar structure.

This requires us to slightly adapt SQMC as follows: one samples jointly the ancestor variables and the new velocities as in Steps (b) and (c) of Algorithm 3, then one obtains the new as , i.e. the deterministic linear transformation of and defined by the model. Note that in this case the dimension of the point set is 3 for ; we could say that in this case, even if the dimension of itself is .

Figures 8 and 9 present, respectively, results for the estimation of the log-likelihood (evaluated at the true value of the parameters) and for the estimation of the filtering expectation for . Concerning the log-likelihood estimation we observe fast increase of the gain factor after about particles with a maximum close to 21 when is very large. The gain of SQMC compensates its longer running time after only about seconds. Important and increasing (in ) gains are also observed for the estimation of the filtering expectations.

6 Conclusion and future work

The main message of the paper is that SMC users should be strongly encouraged to switch to SQMC, as SQMC is “typically” much more accurate (produces estimates with smaller errors) than SMC. We add the word “typically” to recall that our asymptotic analysis, by construction, proves only that the SQMC error is smaller than the SMC error for large enough. But our range of numerical examples, which are representative of real-world filtering problems, makes us optimistic than in most practical cases SQMC should outperform SMC even for moderate values of .

The main price to pay to switch to SQMC is that users should spend some time thinking on how to write the simulation of given as , where and is a deterministic function that is easy to evaluate. Fortunately, this is often straightforward. In fact, there are many models of interest where given is linear and Gaussian. Since this case is already implemented in our program, adapting it to such a model should be just a matter of changing a few lines of code (to evaluate the probability density of given ).

Regarding future work, the most pressing tasks seem (a) to refine the convergence rate of the SQMC error; and (b) to establish that it does not degenerate over time (in the spirit of time-uniform estimates for SMC, see p. 244 of Del Moral,, 2004). Regarding the former, He2014 make the interesting conjecture that the mean square error of SQMC converges at rate . This would explain why the relative performance of SQMC decreases with the dimension. Fortunately, a majority of the state space models of interest in signal processing, finance, or other fields are such that . A notable exception is geophysical data assimilation (in e.g. meteorology or oceanography) for which can be very large, but for such large-dimensional problems SMC seems to perform too poorly for practical use anyway (Bocquet et al.,, 2010).

Finally, it is also our hope that this paper will help QMC garner wider recognition in Bayesian computation and related fields. Granted, QMC is more technical than standard Monte Carlo, and there is perhaps something specific about particle filtering that makes the introduction of QMC so effective. Yet we cannot help but think that the full potential of QMC in Statistics remains under-explored.

Acknowledgements

We thank the referees, Christophe Andrieu, Simon Barthelmé, Arnaud Doucet, Paul Fearnhead, Simon Lacoste-Julien, and Art Owen for excellent remarks that helped us to greatly improve the paper. The second author is partially supported by a grant from the French National Research Agency (ANR) as part of the “Investissements d’Avenir” program (ANR-11-LABEX-0047).

References

- Aistleitner and Dick, (2014) Aistleitner, C. and Dick, J. (2014). Functions of bounded variation, signed measures, and a general Koksma-Hlawja inequality. arXiv:1406.0230.

- Andrieu et al., (2010) Andrieu, C., Doucet, A., and Holenstein, R. (2010). Particle Markov chain Monte Carlo methods. J. R. Statist. Soc. B, 72(3):269–342.

- Barvínek et al., (1991) Barvínek, E., Daler, I., and Francu, J. (1991). Convergence of sequences of inverse functions. Archivum Mathematicum, 27(3-4):2001–204.

- Bocquet et al., (2010) Bocquet, M., Pires, C. A., and Wu, L. (2010). Beyond Gaussian statistical modeling in geophysical data assimilation. Monthly Weather Review, 138(8):2997–3023.

- Briers et al., (2010) Briers, M., Doucet, A., and Maskell, S. (2010). Smoothing algorithms for state–space models. Ann. of the Inst. of Stat. Math., 62(1):61–89.

- Butz, (1969) Butz, A. R. (1969). Convergence with Hilbert’s space filling curve. Journal of Computer and System Science, 3(2):128–146.

- Cappé et al., (2005) Cappé, O., Moulines, E., and Rydén, T. (2005). Inference in Hidden Markov Models. Springer-Verlag, New York.

- Carpenter et al., (1999) Carpenter, J., Clifford, P., and Fearnhead, P. (1999). Improved particle filter for nonlinear problems. IEE Proc. Radar, Sonar Navigation, 146(1):2–7.

- Chan et al., (2006) Chan, D., Kohn, R., and Kirby, C. (2006). Multivariate stochastic volatility models with correlated errors. Econometric reviews, 25(2-3):245–274.

- Chen et al., (2011) Chen, S., Dick, J., and Owen, A. B. (2011). Consistency of Markov chain quasi-Monte Carlo on continuous state spaces. Ann. Stat., 39(2):673–701.

- Chopin, (2002) Chopin, N. (2002). A sequential particle filter for static models. Biometrika, 89:539–552.

- Chopin, (2004) Chopin, N. (2004). Central limit theorem for sequential Monte Carlo methods and its application to Bayesian inference. Ann. Stat., 32(6):2385–2411.

- Cranley and Patterson, (1976) Cranley, R. and Patterson, T. (1976). Randomization of number theoretic methods for multiple integration. SIAM Journal on Numerical Analysis, 13(6):904–914.

- Del Moral, (1996) Del Moral, P. (1996). Non-linear filtering: interacting particle resolution. Markov processes and related fields, 2(4):555–581.

- Del Moral, (2004) Del Moral, P. (2004). Feynman-Kac Formulae. Genealogical and Interacting Particle Systems with Applications. Probability and its Applications. Springer Verlag, New York.

- Del Moral et al., (2006) Del Moral, P., Doucet, A., and Jasra, A. (2006). Sequential Monte Carlo samplers. J. R. Statist. Soc. B, 68(3):411–436.

- Del Moral and Guionnet, (1999) Del Moral, P. and Guionnet, A. (1999). Central limit theorem for nonlinear filtering and interacting particle systems. Ann. Appl. Prob., 9:275–297.

- Devroye, (1986) Devroye, L. (1986). Non-Uniform Random Variate Generation. Springer-Verlag, New York.

- Dick and Pillichshammer, (2010) Dick, J. and Pillichshammer, F. (2010). Digital nets and sequences: discrepancy theory and quasi-Monte Carlo integration. Cambridge University Press.

- Doucet et al., (2001) Doucet, A., de Freitas, N., and Gordon, N. J. (2001). Sequential Monte Carlo Methods in Practice. Springer-Verlag, New York.

- Fearnhead, (2005) Fearnhead, P. (2005). Using random quasi-Monte Carlo within particle filters, with application to financial time series. J. Comput. Graph. Statist., 14(4):751–769.

- Gerber, (2014) Gerber, M. (2014). On integration methods based on scrambled nets of arbitrary size. ArXiv preprint.

- Glasserman, (2004) Glasserman, P. (2004). Monte Carlo Methods in Financial Engineering. Springer Verlag.

- Gordon et al., (1993) Gordon, N. J., Salmond, D. J., and Smith, A. F. M. (1993). Novel approach to nonlinear/non-Gaussian Bayesian state estimation. IEE Proc. F, Comm., Radar, Signal Proc., 140(2):107–113.

- Götz, (2002) Götz, M. (2002). Discrepancy and the error in integration. Monatsh. Math., 136(2):99–121.

- Guo and Wang, (2006) Guo, D. and Wang, X. (2006). Quasi-monte carlo filtering in nonlinear dynamic systems. Signal Processing, IEEE Transactions on, 54(6):2087–2098.

- Hamilton and Rau-Chaplin, (2008) Hamilton, C. H. and Rau-Chaplin, A. (2008). Compact Hilbert indices for multi-dimensional data. In Proceedings of the First International Conference on Complex, Intelligent and Software Intensive Systems.

- Hickernell and Yue, (2001) Hickernell, F. J. and Yue, R.-X. (2001). The mean square discrepancy of scrambled -sequences. SIAM Journal of Numerical Analysis, 38:1089–1112.

- Hlawka and Mück, (1972) Hlawka, E. and Mück, R. (1972). Über eine transformation von gleichverteilten folgen II. Computing, 9:127–138.

- Hong and Hickernell, (2003) Hong, H. S. and Hickernell, F. J. (2003). Algorithm 823: Implementing scrambled digital sequences. ACM Trans. Math. Softw., 29(2):95–109.

- Johansen and Doucet, (2008) Johansen, A. M. and Doucet, A. (2008). A note on auxiliary particle filters. Statist. Prob. Letters, 78(12):1498–1504.

- Kitagawa, (1996) Kitagawa, G. (1996). Monte Carlo filter and smoother for non-Gaussian nonlinear state space models. J. Comput. Graph. Statist., 5:1–25.

- Koyama et al., (2010) Koyama, S., Castellanos Pérez-Bolde, L., Shalizi, C. R., and Kass, R. E. (2010). Approximate methods for state-space models. J. Am. Statist. Assoc., 105(489):170–180.

- Kuipers and Niederreiter, (1974) Kuipers, L. and Niederreiter, H. (1974). Uniform distribution of sequences. Wiley-Interscience.

- Künsch, (2005) Künsch, H. R. (2005). Recursive Monte Carlo filters: Algorithms and theoretical analysis. Ann. Stat., 33:1983–2021.

- Lécot and Ogawa, (2002) Lécot, C. and Ogawa, S. (2002). Quasirandom walk methods. In Monte Carlo and Quasi-Monte Carlo Methods 2000, pages 63–85. Springer.

- Lécot and Tuffin, (2004) Lécot, C. and Tuffin, B. (2004). Quasi-monte carlo methods for estimating transient measures of discrete time markov chains. In Monte Carlo and Quasi-Monte Carlo Methods 2002, pages 329–343. Springer.

- L’Ecuyer et al., (2009) L’Ecuyer, P., Lécot, C., and L’Archevêque-Gaudet, A. (2009). On array-RQMC for Markov Chains: Mapping alternatives and convergence rates. In Monte Carlo and quasi-Monte Carlo methods 2008, pages 485–500. Springer Berlin Heidelberg.

- L’Ecuyer et al., (2006) L’Ecuyer, P., Lécot, C., and Tuffin, B. (2006). A randomized quasi-Monte Carlo simulation method for Markov chains. In Monte Carlo and quasi-Monte Carlo methods 2004, pages 331–342. Springer Berlin Heidelberg.

- Lemieux, (2009) Lemieux, C. (2009). Monte Carlo and Quasi-Monte Carlo Sampling (Springer Series in Statistics). Springer.

- Lemieux et al., (2001) Lemieux, C., Ormoneit, D., and Fleet, D. J. (2001). Lattice particle filters. Proceeding UAI’01 Proceedings of the Seventeenth conference on Uncertainty in artificial intelligence, pages 395–402.

- Matoǔsek, (1998) Matoǔsek, J. (1998). On the L2 -discrepancy for anchored boxes. Journal of Complexity, 14:527–556.

- Neal, (2001) Neal, R. M. (2001). Annealed importance sampling. Statist. Comput., 11:125–139.

- Niederreiter, (1992) Niederreiter, H. (1992). Random Number Generation and Quasi-Monte Carlo Methods. CBMS-NSF Regional conference series in applied mathematics.

- Owen, (1995) Owen, A. B. (1995). Randomly permuted -nets and (t, s)-sequences. In Monte Carlo and Quasi-Monte Carlo Methods in Scientific Computing. Lecture Notes in Statististics, volume 106, pages 299–317. Springer, New York.

- (46) Owen, A. B. (1997a). Monte Carlo variance of scrambled net quadrature. SIAM Journal on Numerical Analysis, 34(5):1884–1910.

- (47) Owen, A. B. (1997b). Scramble net variance for integrals of smooth functions. Ann. Stat., 25(4):1541–1562.

- Owen, (1998) Owen, A. B. (1998). Scrambling Sobol’ and Niederreiter-Xing points. Journal of complexity, 14(4):466–489.

- Pitt and Shephard, (1999) Pitt, M. K. and Shephard, N. (1999). Filtering via simulation: auxiliary particle filters. J. Am. Statist. Assoc., 94:590–599.

- Poyiadjis et al., (2011) Poyiadjis, G., Doucet, A., and Singh, S. S. (2011). Particle approximations of the score and observed information matrix in state space models with application to parameter estimation. Biometrika, 98:65–80.

- Robert and Casella, (2004) Robert, C. P. and Casella, G. (2004). Monte Carlo Statistical Methods, 2nd ed. Springer-Verlag, New York.

- Rosenblatt, (1952) Rosenblatt, M. (1952). Remarks on a multivariate transformation. Ann. Math. Stat., 23(3):470–472.

- Sagan, (1994) Sagan, H. (1994). Space-Filling curves. Springer-Verlag.

- Tribble, (2007) Tribble, S. D. (2007). Markov chain Monte Carlo algorithms using completely uniformly distributed driving sequences. PhD thesis, Stanford Univ. MR2710331.

- Van der Vaart, (2007) Van der Vaart, A. W. (2007). Asymptotic Statistics. Cambrige series in statistical and probabilistic mathematics.

- Wächter and Keller, (2008) Wächter, C. and Keller, A. (2008). Efficient simultaneous simulation of Markov chains. In Monte Carlo and Quasi-Monte Carlo Methods 2006, pages 669–684. Springer.

Appendix A Proofs

A.1 Importance sampling: Theorems 1 and 2

A.1.1 Preliminary calculation

Let , and, as a preliminary calculation, take and

| (9) |

We will use this inequality in the two following proofs.

A.1.2 Proof of Theorem 1

Take for in (9). Consider the first term above. The ratio is bounded by , and (since is bounded) by portmanteau lemma (Van der Vaart,, 2007, Lemma 2.2). Now consider the second term.

We follow essentially the same steps as in Van der Vaart, (2007, Lemma 2.2). Without loss of generality we assume that is a continuous probability measure (the same argument as in Van der Vaart,, 2007, is used for the general case).

Let and take such that . Since is compact, is uniformly continuous on . Let be such that , . Let be a split of into a finite collection of closed hyperrectangles with radius (at most) . Let and note that , . Thus

where for the first term we have

| (10) |

as converges to , and thus for large enough; and for the second term

| (11) |

Finally, for the third term:

| (12) |

Putting (10)-(12) together shows that, for all

| (13) |

for large enough (as ) which concludes the proof of Theorem 1.

A.1.3 Proof of Theorem 2

We prove first convergence (first part of Theorem 2). We start again from (9), but for any . For the second term, by Jensen’s inequality

by assumption. For the first term, using Cauchy-Schwartz, with

we have , and what remains to prove is that .

From (13), and under Assumption 2, one sees that there exists such that with probability one as soon as . Under Assumption 1, a bound similar to (13) is easily obtained by replacing with and observing that is continuous and bounded. Thus, for large enough

We now prove convergence (second part of Theorem 2):

with by assumption, and for the first term:

for large enough, using the same argument as above (as ). Then

where for the second term, , for the first term

and finally for the third term

with

which concludes the proof.

For subsequent uses (see the proof of Theorem 6), we note that these computations imply, for large enough,

| (14) | |||

| (15) |

A.2 Hilbert curve and discrepancy: Theorems 3 and 4

The proofs in this section rely on the properties of the Hilbert curved laid out in Section 2.3 and the corresponding notations.

A.2.1 Theorem 3

We first show that . Because is a continuous probability measure on , the result is obvious if is continuous as well. Let be such that is a discontinuity point of and let be small enough so that and . Then,

By the bi-measure property of the Hilbert curve, the set has Lebesgue measure in and therefore, where by assumption. Hence, for all small enough,

To prove the theorem note that the above computations imply that

To bound the right-hand side, let , , and (which may depend on ) and assume first that , so that . Take , where is the largest integer such that . Then

| (16) |

with . Since is the union of intervals in , is the union of hypercubes in , and therefore (using a similar argument as above and Niederreiter,, 1992, Proposition 2.4),

for a constant and where

For the second term of (16), by the properties of the Hilbert curve,

where the last inequality comes from the fact that is a bounded density.

In case , similar computations show that

To conclude, we choose so that , which gives

Finally, since replacing by changes nothing to the proof of the result above, one may conclude that .

A.2.2 Proof of Theorem 4

Preliminary computations

The proof of this result is based on Hlawka and Mück, (1972, “Satz 2”). Compared to this latter, the main technical difficulty comes from the fact that the Rosenblatt transformation is not continuous because is a weighted sum of Dirac measures. To control the “jumps” of the inverse Rosenblatt transformation introduced by the discontinuity of , we first prove the following Lemma.

Lemma 9.

To prove this Lemma, let where . Since contains at most two points, we have

where and ; note by Assumption 2 of Theorem 4 while by Assumption 3 of Theorem 4 and by Theorem 3. Therefore, as .

Assume now that . Then, this means that there exists a such that, for all there exists a for which . Assume first that . In that case, we have for a constant . Indeed, by the continuity of the Hilbert curve, the set is compact and therefore, , for a constant because the density is continuous and strictly positive. Therefore, if , we have

where the second equality uses the bi-measure property of the Hilbert curve.

Assume now that . Write and note that, since , we have and therefore

Thus, this shows that if , then there exists a such that . This contradicts the fact that as and the proof is complete.

Proof of Theorem 4

We use the shorthand for any set . One has

where

and where, for an arbitrary set with and with for all , we use the shorthand for the set

Let be a partition of in congruent hyperrectanges of size where is an arbitrary integer. Let , the set of the elements of that are strictly in , the set of elements such that , , , and so that

To bound , note that we can cover with sets in , hence

so that, by the definition of ,

We therefore have

The rest of the proof is dedicated to bounding , the number of hyperrectangles in required to cover . To that effect, first note that, using the continuity of and the fact that and are closed sets, we can easily show that . Let and be, respectively, the number of hyperrectangles in we need to cover and to cover . Hence, and we now bound , .

To bound we first cover with hyperrectangles belonging to a partition of the set . We construct as a partition of the set into hyperrectangles of size such that, for all points and in , we have

| (17) |

and

| (18) |

Let for an integer , so that and are in the same interval , and and belong to the same hypercube in . Let be the Lipschitz constant of , then

and Condition (17) is verified as soon as . Let us now look at Condition (18). We have:

where, as in the proof of Lemma 9, . Since and are in the same interval ,

as is bounded. To obtain both (17) and (18), we can take to be the smallest power of 2 such that where

which implies that we assume from now on that for large enough.

Let be a -dimensional face of and let be the set of hyperrectangles such that . Note that . For each , take a point and define

Let be the collection of hyperrectangles of size and having point , , as middle point.

For an arbitrary , let and . Since , is in one hyperrectangle . Hence, using (17) and (18),

where, as in the proof of Lemma 9, , and

Assume from now on that . Then, this shows that belongs to the hyperrectangle with center so that is covered by at most hyperrectangles . To go back to the initial partition of with hyperrectangles in , remark that every hyperrectangles in is covered by at most hyperrectangles in for a constant . Finally, since the set is made of the union of -dimensional faces of , we have

| (19) |

where .

We now consider the problem of bounding , the number of hyperrectangles in we need to cover the set . Note that contains the boundaries of the set that are due to the discontinuities of .

To that effect, we show that there exists a finite collection of sets in such that, for any , there exists a and a point which verifies and for a constant and where ; note that as by Lemma 9. Hence, by taking small enough (i.e. such that ), we have where is the number of hyperrectangles in we need to cover . Then, because the bound we derived above for the number of these hyperrectangles required to cover is uniform in , one can conclude using (19) that .

To construct the collection , let , that is, for a and with . By the definition of the boundary of a set, for any there exists a such that . Let and assume that the point verifies this condition, that is, , . (The case is treated in a similar way, just replace by in what follows.)

We now show that there exists a set and a point such that for a constant . We consider the set where . In order to construct , we write the -th coordinate of (with the natural convention when ).

Let be smallest index such that , . Then, for , set and , while, for , we set and .

To choose and we proceed as follows: if , we take and so that, noting the Hölder constant of ,

as required; if , we take and so that

as required.

Then, for , take and . Finally, to construct the right boundaries , , we define

Note that for all . Indeed, the continuity of and the fact that is compact imply that

Then, since and is strictly increasing with respect to its -th coordinate on , we indeed have for all .

The right boundaries , are then defined recursively as follows:

where

with the continuous extension of on . (Note that such an extension exists because is Lipschitz.) Because is continuous in and is compact, the function is continuous on with and . Therefore, as , we indeed have for all , as required.

To show that , note that, by the construction of we have, for all ,

Therefore, by the continuity of , for any there exists a such that . Hence, for , is selected recursively as the unique solution of . This concludes to show that there exists a such that and . Moreover, since , we have and therefore .

Finally, note that the set depends only on , the smallest index such that , . Defining , this shows that the collection of sets in satisfies the desired properties.

Finally, we may conclude the proof as follows:

where the optimal value of is such that . Let . Then, if , verifies all the conditions above and we have . Thus

Otherwise, if , let . Then and

Therefore , which concludes the proof.

A.3 Consistency: proof of Theorem 5

We first prove the following Lemma:

Lemma 10.

Let be a sequence of probability measures on . Assume that , and that is Hölder continuous with its -th component strictly increasing in , . Then, as ,

To prove this result, let , ,

The function is continuous and bounded and therefore we proceed as in the proof of Theorem 1. But since depends on and we want to take the supremum over , we need to make sure that, on a compact set , for any we can find which does not depend on such that, for , ,

To see that this is true, note that . Hence, for any point there exists a such that and therefore, by the Hölder property of , we have

where and are respectively the Hölder constant and the Hölder exponent of . Let be the continuous extension of on (which exists because is Hölder continuous on ). Let , and , . Then, define

and, noting the -th component of , ,

Let and be the mapping

Note that for a fix the function is continuous on (as is continuous). Therefore, for all and in such that , we have

with

Because is continuous and is compact, is continuous so that, for any , there exists a (that depends only on and therefore independent of ) such that . This concludes the proof of the Lemma.

We now prove Theorem 5. By the result of Hlawka and Mück, (1972, “Satz 2”) and Assumption 3, is such that . In addition, the importance weight function is continuous and bounded by Assumption 2. Therefore, by Theorem 1.

Assume that the result is true at time and let where . Then, the result is true at time if

| (20) |

To see that, let and be the Bolzmann-Gibbs transformation associated to (see Del Moral,, 2004, Definition 2.3.3). Then, the importance weight function

is continuous and bounded (by Assumption 2 and the continuity of the Hilbert curve) and therefore Theorem 1 implies that if (20) is verified.

To show (20), note that

By the inductive hypothesis, so that, by Theorem 3, Assumption 3, the Hölder property of the Hilbert curve and Lemma 10,

Finally, note that

because by the inductive hypothesis and the fact that is continuous and bounded (by Assumption 2 and the continuity of the Hilbert curve). Together with the inductive hypothesis and Assumptions 1, 3-4, this implies that all the assumptions of Theorem 4 are verified and therefore as required.

A.4 Stochastic bounds

A.4.1 Setup of the proof of Theorem 6

The result is proved by induction. By Assumption 2 of Theorem 5, the weight function is continuous and bounded. Therefore, the continuity of , the assumptions on (Assumptions 1 and 2) and Theorem 2 give the result at time .

Assume that the result is true at time and let where verifies the conditions of the theorem. As mentioned previously, iteration of SQMC is a QMC importance sampling step from the proposal distribution to the target where

with and as in the proof of Theorem 5. To bound and we therefore naturally want to use expression (14) and (15) derived in the proof of Theorem 2. To that effect, we need to show that, for large enough and almost surely, the assumptions given in Theorem 2 on the weight function and on the point set at hand (Assumption 2 of Theorem 2) are satisfied.

To see that the conditions on the weight function are fulfilled, note first that is continuous by Assumption 2 of Theorem 5 and by the continuity of the Hilbert curve. To show that is almost surely bounded for large enough, first note that, by Assumption 1, it is clear from the proofs of Theorem 3 and of Theorem 5 that, for all and for all , there exists a such that, almost surely,

In addition, under the assumptions of the theorem, is almost surely bounded above and below away from 0, for large enough. Indeed, by Lemma 10 (and using the Hölder property of the Hilbert curve), and, in particular, under the conditions of the theorem, for any , we have, almost surely,

| (21) |

for large enough (see the proof of Lemma 10 and the proof of Theorem 1). Writing , this observation, together with the fact that

where is continuous and bounded (by Assumption 2 of Theorem 5 and the continuity of the Hilbert curve), implies that, almost surely, for large enough (computations as in the proof of Theorem 1). Hence, almost surely, , for large enough.

Finally, to show that the point set (defined as in the proof of Theorem 5) verifies Assumption 2 of Theorem 2, note that, from Theorem 5 and under the assumptions of the theorem, for any there exists a such that, almost surely, for all . Together with (21), this shows that, as required, for any we have, almost surely and for large enough, .

A.4.2 Proof of Theorem 6: -convergence

We first bound . Let be the -algebra generated by the point set . Then, by Assumption 2,

with as in the statement of the theorem and almost surely and for large enough. Therefore, since , we have

| (23) |

Next, we need to bound . Note that

where the last factor is almost surely finite for all . Indeed, since , is finite for almost all and the integral with respect to is a finite sum. Hence, for all , almost surely so that, by Assumption 2, we have almost surely

where, with probability one and for large enough, . We now need to show that is bounded.

In order to establish this, we prove that for all and for large enough, we have, ,

| (24) |

for constant .

Equation (24) is true for . Indeed, let and note that, under the conditions of the theorem, almost surely and for large enough, for a constant . Hence, for large enough, we have

with . Assume that (24) is true for and note that, under the conditions of the theorem, almost surely and for large enough, for a constant . Then, for large enough (with the convention if ),