The Geometry of relative arbitrage

Abstract.

Consider an equity market with stocks. The vector of proportions of the total market capitalizations that belong to each stock is called the market weight. The market weight defines the market portfolio which is a buy-and-hold portfolio representing the performance of the entire stock market. Consider a function that assigns a portfolio vector to each possible value of the market weight, and we perform self-financing trading using this portfolio function. We study the problem of characterizing functions such that the resulting portfolio will outperform the market portfolio in the long run under the conditions of diversity and sufficient volatility. No other assumption on the future behavior of stock prices is made. We prove that the only solutions are functionally generated portfolios in the sense of Fernholz. A second characterization is given as the optimal maps of a remarkable optimal transport problem. Both characterizations follow from a novel property of portfolios called multiplicative cyclical monotonicity.

Key words and phrases:

Stochastic portfolio theory, rebalancing, functionally generated portfolios, optimal transport, model-free finance2000 Mathematics Subject Classification:

Primary 00A30; Secondary 00A22, 03E201. Introduction

Consider investing in an equity market. At each point in time the investor allocates the current wealth among the stocks and form a portfolio. We will only consider self-financing portfolio strategies that are fully invested in the stock market, are long-only, and are never allowed to borrow or lend in the money market. Mathematically, consider the closed unit simplex in defined by

| (1) |

A portfolio at any point of time is represented by a vector in where is the number of stocks. The individual coordinates of this vector represent the proportions of wealth invested in each stock and are called portfolio weights. Over time this leads to a process with state space .

For example, a buy-and-hold portfolio is one where one buys a certain number of shares of each stock initially and holds them for all future time. Of special importance is the market portfolio defined as follows. Let be the market capitalization of stock at time . The market weight of stock is defined by

| (2) |

and the market portfolio is the portfolio with weights . The market weight takes values in the open unit simplex . The value of this portfolio reflects the growth of the entire equity market and is called a market index. For example, in the US equity market, a standard benchmark is the S&P500 index which is approximately the value process of a buy-and-hold portfolio.

Due to the special importance of the market portfolio as an investment benchmark and as an efficient portfolio according to some asset pricing models (such as CAPM), a lot of effort has been put into developing strategies that outperform it (referred colloquially as ‘beating the market’). Mainstream portfolio theory attempts to achieve this by building asset pricing models that explain and forecast stock returns using economic and technical variables (see [CK06] for an exposition for practitioners). Our approach is more closely aligned to Stochastic Portfolio Theory (SPT) introduced by Fernholz (see [Fer02, FK09]) who showed that it is possible to build explicit portfolios which beat the market under minimal and realistic assumptions on the behavior of equity markets. Working under a continuous time Itô process model, the theory identifies two fundamental sufficient conditions in terms of the market weight process : diversity and sufficient volatility. In the simplest setting, the market is diverse if for all , where for some (this means that the market is never too concentrated), and the market is sufficiently volatile if the eigenvalues of the diffusion matrix of are suitably bounded below. (Both notions will be generalized and explained in this work.) Call a portfolio function to be a map . Here, if is the current market weight, one chooses the portfolio . Under the conditions of diversity and sufficient volatility, Fernholz in [Fer99] showed that certain portfolio functions, that he called functionally generated, will outperform the market portfolio after a finite (but large) time, with probability one. These portfolios are called relative arbitrages with respect to the market. A remarkable fact is that these portfolios, being deterministic functions of the current market weights, are independent of the past or any future forecast. However, not all portfolio functions are functionally generated and it is far from clear from Fernholz’s proof whether any other portfolio function, that is not functionally-generated, can also beat the market under the conditions of diversity and sufficient volatility.

1.1. Statements of main results

One of the main contributions of our paper is to show essentially that no other portfolio functions, other than those that are functionally generated, can beat the market in the long run without additional assumptions. In contrast with the traditional continuous time set-up of SPT, in this paper time is taken to be discrete. We stress on discrete time since it allows complete absence of probabilistic assumptions. While traditionally the market weight is modeled as a continuous time semimartingale, here it is taken to be any deterministic sequence in . All relevant definitions in SPT are modified to this discrete time, pathwise set-up.

We first state some definitions which will be used througout the paper and in the statements of the main results. As noted above, the market is modeled by a sequence of market weights with values in . A portfolio function is a map . Every time the market weight is , the investor chooses the portfolio vector . Given a portfolio function , the value of the corresponding self-financing portfolio will be measured relative to the value of the market portfolio. Consider the quantity

and call it the relative value. It can be shown (see for example [PW13, Lemma 2.1]) that

| (3) |

and is strictly positive for all . In order to “beat the market”, we want to choose such that is large (at least when is sufficiently large).

In this context, the concept of relative arbitrage in SPT is extended to the notion of pseudo-arbitrage.

Definition 1 (Pseudo-arbitrage).

Let be a subset of . A portfolio function is called a pseudo-arbitrage on if the following properties hold.

-

(i)

There exists a constant such that for all sequences of market weight taking values in , we have for all .

-

(ii)

There exists some sequence along which .

Definition 1 formalizes some necessary requirements in order that a given portfolio function is guarenteed to outperform the market under diversity and sufficient volatility. First, under the (generalized) diversity condition , the portfolio is never allowed to lose more than a fixed amount (property (i)). That is, the downside risk is uniformly bounded below regardless of the market movements in a fixed region. Second, there is a possibility of unbounded gain (property (ii)). While these properties appear to be rather weak, they impose strong restrictions on the portfolio map. Given we give two characterizations of pseudo-arbitrage opportunities. First, we characterize pseudo-arbitrages as portfolios that are functionally generated in Fernholz’s sense (with a slightly extended definition).

Theorem 1.

A portfolio function is a pseudo-arbitrage on an open convex subset if and only if there exists a concave function satisfying the following properties:

-

(i)

the restriction of on is not affine,

-

(ii)

there exists such that , and

-

(iii)

for any , the vector of coordinatewise ratios defines a supergradient of the concave function at (see Proposition 5 for the precise definition).

If is continuous, then on it is necessarily given by the formula

| (4) |

Here is the one-sided directional derivative in the direction , where is the vector of all zeroes except one at the th coordinate.

In the above theorem we say that is generated by . It can be shown (see Proposition 5 below) that Theorem 1(iii) and (4) coincide with Fernholz’s definition of functionally generated portfolio under his more restrictive smoothness assumption.

Our second characterization establishes a geometric connection by describing pseudo-arbitrages via solutions to a Monge-Kantorovich optimal transport problem. To recall the general formulation (see [Vil03, Vil09] for details), let and be Polish (complete metric) spaces, and let be a measurable function called the cost function. Let and be (Borel) probability measures on and respectively. A coupling of is a probability measure on whose marginals are and respectively. Let be the collection of all such couplings. The Monge-Kantorovich optimal transport problem is the problem

| (5) |

Here the notation means that the random element has joint distribution . A solution of (5) is called an optimal coupling. We say that an optimal coupling of (5) solves the Monge problem if is a deterministic function of . The infinum in (5) is called the value of the problem.

Now we specialize to the case and together with the cost function

| (6) |

The interpretation is that represents the market weight and represents the deviation of the portfolio vector from the market weight. Given and , we may define a portfolio vector corresponding to via a change of measure:

| (7) |

where . Consider a probability measure on and on . Suppose the Monge-Kantorovich problem (5) with cost (6) has a solution and value of the problem is finite.

Theorem 2.

Let and suppose is a map such that belongs to the support of for all , i.e., is a selection of the support of . Define a portfolio on by (7) with . Then there exists a concave function such that part (iii) of Theorem 1 holds. Thus, is a pseudo-arbitrage on whenever is an open convex set and conditions (i) and (ii) in Theorem 1 hold.

For portfolio functions with strictly positive weights (this corresponds to the above formulation where takes values in ), there is an alternative formulation in terms of the exponential coordinate system of the unit simplex ; see [ANH07, Example 2.4]. We view as an -dimensional exponential family of probability distributions on atoms. For , we let be its exponential coordinates given by

| (8) |

The map defined by (8) is a global coordinate system of the manifold . We can now represent an arbitrary point of by

| (9) |

where

| (10) |

Now consider two Borel probability measures and on . Assume, for simplicity of exposition, that is supported on the entire . Consider the transport problem , where the infimum is taken over all couplings of . Suppose the problem has a solution and let be some selection from the support of the optimal coupling. Define a portfolio function by the recipe

| (11) |

We will show that this is an equivalent formulation of the transport construction of a portfolio as given in (7). The advantage of this formulation is that now the transport is on an Euclidean space with a strictly convex cost function. The function represents the negative shift, in exponential coordinates, to go from to .

The above results allow us to view functionally generated portfolios as maps that minimize the “total cost” of assigning portfolio weights to the market weights. This provides an elegant geometric approach and suggests a natural optimization problem for functionally generated portfolios. Namely, given prior beliefs regarding the possible market weights in the future (represented by or ) and a collection of portfolio weights to be chosen from (represented by or ), the investor can solve an optimal transport problem to obtain a functionally generated portfolio. The transport problem itself is apparently new and its solutions are characterized by Theorem 1 and Theorem 2. The transport problem can be solved explicitly for two stocks and in Section 4 we provide several examples using real data.

Both characterizations follow from a novel property of portfolios we call multiplicative cyclical monotonicity and will be developed in Section 2. Intuitively, this property requires that the portfolio does not underperform the market if the market weight goes over any discrete cycle in the unit simplex.

Apart from the references mentioned above, the following articles are closely related to our current work. The roles of diversity and sufficient volatility in relative arbitrage have been studied by authors such as Fernholz and Karatzas [FK05] and Fernholz, Karatzas, and Kardaras [FKK05]. Functionally generated portfolio is used by Banner and Fernholz [BF08] to prove that sufficient volatility of the smallest stock implies the existence of short term relative arbitrages. Generalizations of functionally generated portfolios to stochastic generating functions and application to statistical arbitrage is studied in Strong [Str12]. The discrete time set-up and the information-geometric flair is a continuation of Pal and Wong [PW13]. The case where the benchmark is a functionally generated portfolio (such as the equal-weighted portfolio) instead of the market is studied in [Won15]; a shape-constrained optimization problem for functionally generated portfolios is also formulated. A recent trend in mathematical finance is to study robust pricing and hedging of contingent claims under model uncertainty or model-free assumptions. For example, Fernholz and Karatzas [FK11] characterizes optimal relative arbitrage when the covariance matrix is uncertain. The theory of optimal transport also arises in this context, see, for example, Beiglböck et al. [BHLP13] and Beiglböck and Juillet [BJ14], although the motivation is quite different from this paper.

1.2. Notations

Let be the number of stocks of the market. The vector of market weights, as defined by (2), takes value in the open unit simplex in . All topological and measure-theoretic aspects will be relative to the unit simplex (with the Euclidean topology). Here and everywhere following, for any vectors and in , we let be their Euclidean inner product and be the Euclidean distance. If has nonzero components, we denote by the vector of the componentwise ratios . Also we let be the coordinate-wise product. A tangent vector of is a vector satisfying . We denote by the vector space of tangent vectors of .

Acknowledgment

We are grateful to Prof. Walter Schachermayer for a thorough reading of the manuscript and suggesting numerous comments for improvement. We also thank the anonymous reviewers for detailed comments about the presentation.

2. Multiplicative cyclical monotonicity

In this section we characterize pseudo-arbitrage portfolios using a property of multivariate functions we call multiplicative cyclical monotonicity. The main arguments are convex analytic and we begin by reviewing some basic notions. A standard reference of convex analysis is the book [Roc97] by Rockafellar.

2.1. Convex analysis on the unit simplex

A function is concave if for any and any , we have

Let be a concave function on . The superdifferential of is a multi-valued function from to , the set of tangent vectors of . For , a tangent vector belongs to if

| (12) |

for all . It is well known that is a non-empty compact convex set. The elements of are called supergradients (of at ). Intuitively, each supergradient defines via the left hand side of (12) a supporting hyperplane of at .

We will also consider differentiable functions on and their derivatives. Implicitly, we regard as an -dimensional manifold embedded in . A global coordinate system is the projection map . For example, a function on is of class ( times continuously differentiable) if the push forward is of class on the open set in . If a concave function is differentiable at , the superdifferential is a singleton containing the usual gradient.

For , let be the vertex of in the -th direction. If is a real or vector-valued function on , , and , we denote by the directional derivative of at in the direction whenever the limit exists. Explicitly, it is defined by

It is well known ([Roc97, Theorem 23.1]) that if is concave, then exists as a finite limit. If is vector-valued and differentiable, then is the differential map (push forward of tangent vectors).

2.2. Multiplicative cyclical monotonicity

By a cycle in the unit simplex we mean a finite sequence with .

Definition 2 (Multiplicative cyclical monotonicity (MCM)).

Let be a portfolio or more generally a multi-valued map from to . We say that satisfies multiplicative cyclical monotonicity (MCM) if over any cycle we have , i.e.,

| (13) |

For , we say that satisfies -MCM if the inequality (13) holds for all cyclces where the successive jump sizes are all less than .

From Definition 1 the minimum relative value of a pseudo-arbitrage is uniformly bounded below whenever takes value in the subset of . Since we are allowed to choose any path in , this is the case only if the portfolio does not underperform the market when the market weights goes through a cycle and return to an earlier position. Here is an immediate consequence of Definition 2.

Lemma 3.

Suppose is a portfolio which fails the MCM property. Then there exists a market weight sequence such that takes values in a finite subset of and as .

Proof.

Suppose that the MCM property breaks down for some cycle in . Then

| (14) |

where . Consider the market weight sequence defined by

In other words, the market cycles through the sequence . Clearly takes values in a finite set. By (14), we have which tends to zero as tends to infinity. It is easy to see that as well. ∎

The sequence in the proof of Lemma 3 is by all standards diverse and sufficiently volatile, yet the relative value of the portfolio goes to zero. It follows that the MCM property is necessary in order that a portfolio outperforms the market in all diverse and sufficiently volatile markets. In practice, it is of course unlikely that market weights travels along a cycle. The MCM property is a desirable theoretical property that a portfolio may or may not satisfy. It is clear that MCM implies -MCM for any . The definition above is a multiplicative form of the classical cyclical monotonicity property in convex analysis [Roc97, Section 24].

Our first result gives the connection between the MCM property and concave functions.

Proposition 4.

Let be a portfolio or more generally a multi-valued map from to .

-

(i)

satisfies MCM if and only if there exists a concave function such that

(15) -

(ii)

For any , if satisfies -MCM, then satisfies MCM.

Proof.

(i) The proof is an adaptation of the proof of [Roc97, Theorem 24.8]. For notational simplicity we assume that is single-valued. Suppose there exists a concave function such that (15) holds. Then over any discrete cycle with , we have

The final equality holds since . This shows that satisfies MCM.

Conversely, suppose that satisfies MCM. Fix a point and define a function on by

| (16) |

Here the infimum is taken over all and all choices of points such that . We claim that (15) holds.

Clearly , being the pointwise infimum of a family of affine functions in , is a concave function on . It is clear that is non-negative, and the MCM property implies that . It follows by concavity that must be everywhere positive on .

To show (15), let be given. Let . By definition of , there exists some and a sequence with such that

Setting , we have

The proof of (15) is completed by letting .

(ii) The idea is to repeat the proof of (i) with the additional restriction that the jumps have sizes less than . Consider the function defined by (16), where the infimum is taken over all and all choices of where . As before, is a positive concave function on , and (15) holds whenever . Thus

| (17) |

This shows that the component of parallel to (which is a tangent vector) is a superdifferential of the restricted concave function at , where is a convex neighborhood of . However, by [Roc97, Theorem 23.2], we have

Since the one-sided derivatives of depends only on the values of in a neighborhood of , we observe that for any convex neighborhood of . It follows that (17) holds for all . Thus by (i) satisfies MCM. ∎

Remark 1.

If is any subset of , we can define the MCM property on by requiring that (13) holds for all cycles in . A straightforward modification of the proof of Theorem 4 shows that there is a positive concave function defined on the entire simplex such that (15) holds for all . This observation will be useful in the proof of Theorem 8.

2.3. Functionally generated portfolios

In the set-up of Proposition 4 we say that is generated by and is a generating function of . Note that if is a positive concave function on , then is also concave and

Our next propositions show that MCM portfolios are functionally generated in the sense of Fernholz (see [Fer02, Theorem 3.1.5] for his formulation).

Proposition 5.

Remark 2.

Proof.

(i) Let . By (15), we have

for all . Note that is not a tangent vector of . The normalization (18) ‘projects’ to which is a tangent vector. Since is perpendicular to , the inner product does not change if is replaced by . Hence by (12) we have .

(ii) It is easy to verify that . To see that for each , let for in (12), and we have

Letting and dividing both sides by , we get the desired inequality .

That and are inverses of each other can be verified by a direct computation. ∎

Proposition 6.

Let be a portfolio on generated by a concave function .

-

(i)

The generating function is unique up to a positive multiplicative constant.

-

(ii)

For any and , we have

In particular, if is differentiable, the portfolio is given by the formula

(20) -

(iii)

If is continuous, then is continuously differentiable. More generally, if is of class , then is of class .

-

(iv)

If is concave and differentiable, and we define by (20), then is generated by . In particular, for all .

Proof.

(i) Suppose is generated by and which generate . Let and consider the line segment from to . Consider the restrictions of to , denoted by . They can be parametrized as one-dimensional concave functions. In particular, they are differentiable on except at most for countably many points on . By Proposition 5, the vector defines a supporting hyperplane of the log generating function. It follows that and have parallel supporting hyperplanes at all points of . In particular, the derivatives of and agree almost everywhere on . By the fundamental theorem of calculus for concave functions [Roc97, Corollary 24.2.1], we have

Since and are arbitrary, is a positive constant.

(ii) By definition of , for small enough such that , the superdifferential inequality (15) gives

| (21) |

Note that the inner product is given by

Taking log on both sides of (21), we have

Dividing by and taking the limits as and , we obtain the desired inequalities. Formula (20) is proved by noting that if (and hence ) is differentiable, for every tangent vector we have .

(iii) Suppose that is continuous. It follows that is a continuous selection of the superdifferential of . By [Rai88, Proposition 4] , and hence , is differentiable on . By [Roc97, Corollary 25.5.1], is actually continuously differentiable.

If is of class where , we already know is differentiable. In terms of the coordinate system , for we have

which is of class . Hence , and hence , is of class .

(iv) Suppose is differentiable and define by (20). To show , fix and , and consider the restriction of to the segment . The inequality is equivalent to and follows from concavity and positivity of . To verify that we only need to show that , or . This follows from the identity and linearity of the directional derivative for differentiable functions. Finally, is generated by by (ii). ∎

2.4. L-divergence

The concavity of the generating function has a financial meaning which will become clear in Lemma 7 below.

Definition 3 (L-divergence).

Let be a portfolio generated by a concave function . The L-divergence of the pair is defined by

| (22) |

We use this terminology because the expression (22) can be regarded as a logarithmic version of the widely used Bregman divergence (see [AC10]). It is clear from (15) that and is strictly positive unless is affine on the straight line joining and . When is strictly concave, only if . In general, is asymmetric and does not define a metric.

As an example, fix and consider the geometric mean . This is a concave function which generates the constant-weighted portfolio ([Fer02, Example 3.1.6]). We have

| (23) |

We call this the discrete excess growth rate , see [PW13, Definition 2.2].

Remark 3.

The L-divergence is defined for a pair because in general the portfolio generated by a given concave function is not unique. Whenever is not differentiable at any choice of supergradient defines a portfolio vector. Since a concave function is differentiable almost everywhere, the portfolios agree almost everywhere on .

The L-divergence features in the following decomposition formula which is a discrete time analogue of [Fer02, Theorem 3.1.5].

Lemma 7.

Let be generated by a positive concave function . Let be the L-divergence functional of the pair . Then the relative value process satisfies the decomposition

| (24) |

where is non-decreasing. Moreover, is affine if and only if for all market weight sequences.

Following Fernholz, we call the drift process.

Proof.

The decomposition formula (24) follows directly from the definitions. By (3) and (22), we have

Thus (24) follows by summing over and rearranging. Since , is non-decreasing.

It is clear that if is affine. Conversely, suppose for all market weight sequences. Then is affine on the line segment as . Since and are arbitrary, is affine on . ∎

Whenever is not affine on the line segment , the L-divergence is strictly positive. The drift process measures the cumulative amount of market volatility captured by the portfolio in the time interval . We say that the market is sufficient volatility for if as .

2.5. Characterization of pseudo-arbitrage

If is not MCM, Lemma 3 shows that there is a sequence of market weights along which the relative value goes to zero. This is a ‘global’ property in the sense that the faulty path might require big jumps. Our next result shows that failing to be MCM is also a ‘local’ property in the sense that the jumps could be as small as we wish. In fact, it could be completely localized around a single point.

Theorem 8.

Let be a portfolio map from to which fails the MCM property.

-

(i)

For any , there is a sequence of market weights such that for all and goes to zero as . Thus cannot be a pseudo-arbitrage over any set containing the path.

-

(ii)

For any , there exists such that the sequence in (i) can be chosen to lie entirely within the Euclidean ball of radius around .

Proof.

Part (i) has been proved in Lemma 3. That the sequence can be chosen with jump size less than follows from Proposition 4(ii).

To prove (ii), we will show that given , there is a point such that the MCM property fails inside the Euclidean ball of radius around . Then we may repeat the proof of (i) in this ball. This will be achieved by a method of contradiction using the following claim.

Claim. Suppose there exists such that for any , the MCM property holds over any choice of points selected within a ball of radius around . Then the MCM property holds on .

To prove the above claim let us recall the notions of line integrals and conservative vector fields. Let be a piecewise linear curve in indexed by a closed interval, say . The curve will be called a loop if . The line integral of the vector field over any will be denoted by

The line integral does not depend on parametrization, except for the orientation. By a slight abuse of notation, the line from any to any in , irrespective of parametrization, will be denoted by .

Let and let . Consider any loop whose range is contained in . Then we have

| (25) |

In other words, the vector field is locally conservative restricted to every . To see (25), we use the fact that satisfies MCM over . Therefore, by Theorem 4, there is a positive concave function on which generates on . Consider any line contained in . By [Roc97, Theorem 24.2], we have . Thus (25) holds for any piecewise linear loop in .

We now show that any locally bounded and conservative vector field over must be globally conservative. While this statement is well known for smooth vector fields, we only assume that is measurable and locally bounded, and the resulting potential is not necessarily differentiable. Since we are unable to find a reference for this result, we will give a sketch of proof and refer the reader to [PW14, Proof of Theorem 8] for more details.

Let be locally conservative in the sense of (25). Fix and consider two piecewise linear curves and from to . We will be done once we show

| (26) |

Without loss of generality, we may assume that .

In fact, we can assume that has exactly three corners and is a concatenation of and (we call such curves triangular). This is because once we establish (26) for such triangular curves, we can inductively eliminate corners in any other and establish (26) in general.

For the rest of the argument we assume that is triangular and is . Assume both and are indexed by .

We first suppose that . In this case, choose points in such that their images on are a sequence of equidistant points with successive distance less than . Now add lines between and . Now consider each loop which is formed by the oriented lines , , , and . See Figure 1.

By the triangle inequality for Euclidean distance it follows that the loop lies entirely inside . Hence, by our assumption on local conservation, the integrals of over these loops are zero. However, the sum of the integrals over all these loops is precisely the integral of over the concatenation of lines and . Therefore this integral is zero, proving (26).

It can be shown by means of a simple geometric argument that any other case can be reduced to Case 1 above (see [PW14] for details). Now that we have shown that is globally conservative, we can unambiguously define a function on by fixing some and defining

| (27) |

where the integral is over any piecewise linear curve from to . Over any , the function must coincide (up to a constant) with the concave function resulting from the local MCM property of the vector field . Thus, is locally concave on and hence it is concave (see [Hör07, page 58]) and generates . This shows that is MCM over and this completes the proof of the theorem. ∎

Proof of Theorem 1.

Sufficiency follows from the decomposition formula (24). By condition (ii), the first term on the right is bounded uniformly over all sequences (note that a positive concave function on is bounded above). Since is open, the L-divergence is identically zero on if and only if the function is affine. If is non-affine, one can clearly choose a sequence such that the accumulated L-divergence goes to infinity, and so along that sequence. Equation (4) is taken from Proposition 6(ii).

To prove necessity, we first note that cannot be a pseudo-arbitrage if there is a market cycle in over which the MCM property fails. By Remark 1, there exists a positive concave function on such that Theorem 1(iii) holds. Since is functionally generated, we may apply Lemma 7. If is affine over then the process is zero, and is bounded above if for all . This prevents from being a pseudo-arbitrage.

Finally, suppose zero is a limit point of the set . As a positive concave function on , can be extended continuously to . We can thus find a point in the closure such that . Fix a point and let be a strictly increasing sequence in converging to . Let be the sequence of market weights defined by

We choose such that is differentiable at for all . Since is differentiable, we have . It follows that

Using the elementary inequality for , we get

| (28) |

Comparing the right hand side of (28) with the line integral

it is not hard to see that by choosing the points properly the right side is . Thus, along this sequence the relative value process tends to zero as . This shows that cannot be a pseudo-arbitrage if zero is a limit point of . This completes the proof of Theorem 1. ∎

2.6. The differentiable case

In this subsection we derive differential inequalities satisfied by MCM portfolios. Let be a portfolio satisfying the MCM property. By Proposition 6, its generating function is . Recall that is the L-divergence functional defined by (22).

Definition 4 (Drift quadratic form).

Let be generated by a positive concave function on . The drift quadratic form of is the quadratic form satisfying

where and . Here is the Hessian of regarded as a quadratic form. By definition, it is given by

| (29) |

Direct differentiation shows that is the Taylor series approximation of . For small, we have

| (30) |

Of special importance is the case where is a constant-weighted portfolio. The corresponding drift quadratic form is called the excess growth quadratic form.

Definition 5 (Excess growth).

Let . The excess growth quadratic form of is defined by

| (31) |

where and .

Finally we need the concept of Fisher information metric from information geometry ([ANH07, Section 2.5]).

Definition 6 (Fisher information metric).

The Fisher information metric on defines an inner product of tangent vectors for each . If and are tangent vectors of , and , the inner product is defined by

Notice that if , then , so the excess growth quadratic form of the market portfolio is the Fisher information metric.

Theorem 9.

Let be a portfolio generated by a positive concave function on . Then:

-

(i)

The weight ratio satisfies

(32) for any and .

-

(ii)

For any and , we have

(33)

Recall that and are the push forwards of tangent vectors (images of the differential map). Intuitively, the inner product measures how much the portfolio weights move in the direction of the increment of market weights. By (33), in order that is a pseudo-arbitrage, the inner product cannot be more than the excess growth rate of the portfolio. This gives the meaning of concavity at the portfolio map level.

Proof.

(i) Let , and . By the MCM property with , we get

Expanding the above expression, we get

Dividing by and taking the limit as tends to zero, we get the desired inequality.

(ii) Without loss of generality, we may assume that is twice continuously differentiable on an open neighborhood of in . Using the product rule, we have

It follows that

∎

Remark 4.

In [PW13, Section 4], we showed that when , a functionally generated portfolio , where and , has a non-decreasing drift process if and only if

| (34) |

Using the identity , which follows from Itô’s formula, we can show that and . We get

Thus Theorem 9 generalizes (34) and provides a geometric interpretation.

Remark 5.

By Proposition 5 and Theorem 9, for a continuously differentiable portfolio the MCM property implies that the vector field is conservative (in the sense of (25) where is any curve in ) and satisfies the inequality (32). The converse is also true and here is a sketch of proof. If is conservative, the line integral defines via (27) a function on such that is given by (4). Moreover, (32) implies that is concave. Thus is generated by a concave function and is MCM.

When , all continuously differentiable vector fields on are conservative (also see [PW13, Lemma 4.6]) and thus (32) implies the MCM property. In general, a portfolio may satisfy (32) without being generated by a concave function. The following example is inspired by [Roc97, Section 24, page 240]. The construction works for any , but for concreteness we let . Consider the matrices

where is the transpose of . Let be a parameter to be chosen, and define , . Note that is non-symmetric and is (strictly) negative definite. Here we use matrix notation whenever convenient. The matrix defines a portfolio via the weight ratio, given by

| (35) |

where is some smooth function. Using the identity , we have

| (36) |

The portfolio is then given by

When , the entries of are greater than . It follows from (36) that , so the portfolio has positive weights.

If this portfolio is generated by a concave function, Proposition 6 implies that the generating function is smooth. By [Fer02, Proposition 3.1.11], there exists a continuously differentiable function on a neighborhood of in such that is an exact differential -form. It follows that for any and . Letting , we see by differentiating (35) that

So , while , which is clearly a contradiction. Thus the portfolio is not generated by a concave function.

It remains to check that (32) holds. From (35), we see that

| (37) |

For each , is a non-negative definite quadratic form in . By continuity, there exists a constant such that for all . Since is negative definite, by choosing sufficiently small, we can make the sum non-positive definite. Hence (32) holds on .

3. Optimal transport

In this section we study functionally generated portfolios from the point of view of optimal transport. The general optimal transport problem has been given in the Introduction. We begin by recalling the notion of -cyclical monotonicity which plays a crucial role in characterizing optimal solutions.

3.1. -cyclical monotonicity

Consider the Monge-Kantorovich optimal transport problem with state spaces and with cost function .

Definition 7 (-cyclical monotonicity).

Let be a subset of . We say that is -cyclical monotone if for any and any sequence in , we have

| (38) |

with the convention and .

It can be shown that -cyclical monotonicity is equivalent to the assertion that

| (39) |

where is any permutation of . The following is a basic result in optimal transport theory.

Theorem 10.

[Vil09, Theorem 5.10, part (ii)] Suppose that the cost function is continuous and bounded below. Let and be (Borel) probability measures on and respectively. Assume that the value of the transport problem (5) is finite. Then solves the optimal transport problem (5) if and only if the support of is -cyclically monotone.

3.2. MCM and -cylical monotonicity

We consider the cost function on defined by

| (40) |

The cost function is clearly continuous. Let be a function (thought of as a transport map). The map defines a portfolio function via (7):

| (41) |

The following proposition gives the link between the cost function (40) and the MCM property.

Proposition 11.

Let . The graph of is -cyclical monotone if and only if the portfolio defined by (41) has the MCM property.

Proof.

Let be a market cycle. By (41), we have

Multiplying the above terms along the market cycle and taking log on both sides, we have

| (42) |

Suppose is MCM. Then in (42) we have . So

Since the market cycle is arbitrary, this implies that the graph of is -cyclical monotone. The same reasoning shows that is MCM if the graph is -cyclical monotone. ∎

Proof of Theorem 2.

To show the first statement, suppose we can prove that the support of any optimal coupling is -cyclical monotone. Then the portfolio defined by (7) is MCM by Proposition 11. Thus is generated by a concave function by Proposition 4, and the rest follows from Theorem 1. It remains to prove that the support is -cyclical monotone.

Since the cost function (40) is unbounded below, we will use a little trick so that Theorem 10 can be applied. Let be an optimal coupling with finite cost. Consider the sets

Also let be the restriction of to , normalized to have mass . Since increases to , by the continuity of measure is well defined for sufficiently large. Let and be the marginals of . Consider the optimal transport problem

| (43) |

where . By the well known restriction property of optimal transport (see [Vil09, Theorem 4.6] whose proof does not rely on any topological assumptions), is optimal for (43). Now the cost function, when restricted to , is continuous and bounded below. So, by Theorem 10 we see that is -cyclical monotone. Since is arbitrary, is -cyclical monotone.

Now we argue the converse. Suppose the portfolio is a pseudo-arbitrage on . Let be any probability measure on , and let be the distribution of , where . We claim that the coupling is optimal for the optimal transport problem . Since is bounded below, is supported on for some . On the set , the cost function is continuous and bounded below. Thus the coupling is optimal by Theorem 10. ∎

3.3. MCM in exponential coordinates

Now we restrict to portfolio functions with strictly positive weights and give an alternative formulation of the transport problem using the exponential coordinates.

Recall that defined by (8) is the global coordinate system which gives the exponential coordinates. Given an arbitrary function , we can define a portfolio function by (11). Conversely, given a portfolio map , one can define by setting whenever . Rearranging gives

| (44) |

Fix a portfolio function . Now we express the evolution of in terms of the exponential coordinates. Given the market weight sequence , we define the exponential coordinate process by . Using (9), we have

Taking log on both sides, we have

Summing over time, we get

| (45) |

Now consider a discrete cycle where . Putting in (45), we have

Thus, if is MCM, then

| (46) |

which is the definition of -cyclical monotonicity. We summarize the above discussion by the following proposition. It allows us to pose the transport problem in terms of the exponential coordinates.

3.4. Relative entropy as a cost function

In this subsection we give another optimal transport problem giving rise to functionally generated portfolios. Now we take and consider the cost function on given by the negative relative entropy:

| (48) |

Here is interpreted as the market weight and is interpreted as the portfolio weight. Note that is non-positive and is if and only if .

Proposition 13.

Any -cyclical monotone subset of satisfies MCM. The converse is false.

Proof.

Let be a -cyclical monotone subset of , and let be a cycle in . Then -cyclical monotonicity implies that

Expanding, we have

Thus we get

Applying Jensen’s inequality to the sum inside the square bracket for each , we have

and the MCM property follows by exponentiating.

To see that the converse is false, let be the identity map on . This is the market portfolio, which is MCM. But , so the market portfolio maximizes the transportation cost. Any other rearrangement will increase relative entropy and decrease the transportation cost. ∎

Consider the transport problem with cost (48). Since any optimal coupling have -cyclical monotone support (argue as in the proof of Theorem 2), the support is MCM by Proposition 13 and thus is generated by a concave function. We give an alternative treatment which relates the problem with one with quadratic cost.

Theorem 14.

Let and . Let be supported on and let be supported on . Suppose that

| (49) |

Then the value of the problem (5) with cost function is finite. Moreover,

-

(i)

There exists a concave function such that any optimal coupling is concentrated on the set

-

(ii)

For any we have . Thus is bounded on .

The proof of the above theorem depends on the following lemma. Here, if is a vector with positive components, means applying log to each coordinate.

Lemma 15.

Let be a proper convex function on . Consider as a subset of . Assume that, for every point , there is a such that the following subdifferential inequality holds

| (50) |

That is, is a subdifferential of at . Then is a concave function on . Moreover, the portfolio function is generated by .

Proof.

Consider any two points . By (50) we get,

Proof of Theorem 14.

It is clear that the value of the problem is finite.

To prove (i) we will use the Knott-Smith optimality criterion ([Vil03, Theorem 2.12]) which is a fundamental result for optimal transport with quadratic cost. First we will reformulate problem (5). Let be the law of when . Then both and are probability measures on , and the optimization problem (5) becomes , where is the Shannon entropy of . Since , this term can be dropped. Completing the squares, we see that the transport problem is equivalent to

| (51) |

which is the usual optimal transport problem for the quadratic cost.

Let be an optimal solution to (51) (which exists by [Vil09, Theorem 4.1]). The Knott-Smith optimality criterion states that there is a lower semi-continuous convex function on such that the support of the optimal coupling is contained in the graph of . That is, for almost all we have . Consider the map and let . By Lemma 15, is a concave function which generates .

For (ii), let be in the support of as above. By convexity of and the fact that is a supergradient at , we have

Multiplying the above inequalities by the negative sign and then exponentiating prove our claim. ∎

3.5. Examples

Now we give some simple examples where optimality can be verified directly; a more realistic application will be given in Section 4. Let be the set of permutations of . For and , let denote the vector . Let be the set defined by

| (52) |

In other words, the rank of the th coordinate of a point in is . Let be the identity. Note that , by extending the action to sets.

Example 1.

In this example the cost function is (40). Let be a precompact subset of which is defined only by the ranked coordinates, i.e., for all . Let be an probability measure on which is invariant under relabelings of the coordinates. That is, is completely specified by the distribution of the ordered statistics and we say that is exchangeable. This will imply that the resulting portfolio functions are rank-based. We also assume that does not charge the boundaries of ’s.

Let (the is applied componentwise) and let be the uniform distribution on this finite set. Then the optimal coupling of can be described as follows. First, for every , we couple with . Next we extend by symmetry: for every , couple with . It can be checked that the resulting portfolio invests everything in the smallest stock. Similar examples can be worked out for . In this case the optimal portfolio will invest according to the rescaled market weights in the lowest two stocks. If is the set of the log of the sums of many distinct , the resulting portfolio invests according to the market in the smallest stocks. This is an example of portfolio selected by rank, see [Fer02, Example 4.3.2].

Example 2.

Now we consider the negative relative entropy cost . Let and be as in Example 1. Let and let be the uniform distribution on . It is then clear that the following coupling minimizes the cost: With every , couple with and extend by symmetry. Now the optimal coupling is again the portfolio that puts its entire holding on the smallest stock. However, if we take or the set of averages of many distinct ’s, the optimal portfolio will invest equally among the smallest stocks.

4. Empirical examples: two stocks case

In general, solving optimal transport problems (either analytically or numerically) is a difficult task; see for example [BFO14] and the references therein. Designing practical algorithms for solving the transport problem with cost (40) or (47) is an interesting open problem. In the case , the solution can be characterized explicitly due to the special structure of the real line and the convexity of the cost function (47). In this section we present the solution and give several empirical examples.

4.1. Monotone rearrangements

Throughout this section we assume . A typical point in is represented as

where is the exponential coordinate of . A portfolio vector with positive weights corresponding to can be expressed as

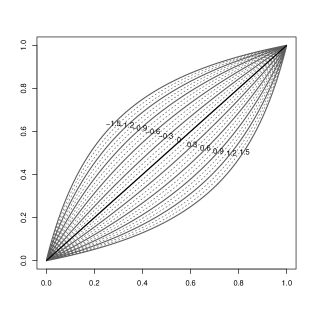

for some . So the exponential coordinate of is . We will choose as a function of . As increases, the portfolio underweights more and more stock 1 relative to the market weight. See Figure 3 for the dependence of the portfolio on at different points on the simplex. As an example, if is bounded by , the graph of the resulting portfolio will lie within the curves labeled and .

Consider the transport problem with cost (47). Let and be probability measures on . We assume that is absolutely continuous with respect to the Lebesgue measure. The cost is

Here

is a smooth and strictly convex function on . The transport problem is

| (53) |

where .

Let and be the distribution functions of and respectively.

Definition 8 (Monotone rearrangement).

The monotone transport map from to is the map defined by

| (54) |

In other words, is defined by matching the quantiles of to those of . It is clear from (54) that is non-decreasing. Moreover, it is easy to check that if , then . Thus is a coupling of . In fact, is the unique non-decreasing function (up to the null sets of ) which maps to .

The following theorem is a special case of a well-known fact (see for example [JS12, Theorem 3.1]). Indeed, the monotone transport map remains optimal if is replaced by any strictly convex function.

Theorem 16.

The coupling where and is the monotone transport map from to is the unique solution to the transport problem (53).

An explicit example is where and are normal. In this case, the monotone transport map is linear and the corresponding portfolio is essentially a diversity-weighted portfolio (see [Fer02, Section 3.4]).

Proposition 17.

Let and . Then the monotone transport map is given by

Moreover, the portfolio function corresponding to the transport map is given by

| (55) |

where and .

Proof.

Let and . The first statement follows from the fact that and have the same distribution.

Clearly the portfolio has the form (55) whenever the transport map is linear, so the normality assumption is not required. Nevertheless, it is instructive to see how the portfolio depends on the means and variances of and . In particular, the exponent in Proposition 17 depends on the ratio . If , then and is a constant-weighted portfolio. If , then and is essentially the diversity-weighted portfolio. If , then is negative and the corresponding portfolio is studied in the recent paper [VK15]. On the other hand, the mean of represents systematic overweight/underweight of stock 1 and interacts with other parameters to determine the constant .

4.2. Empirical examples

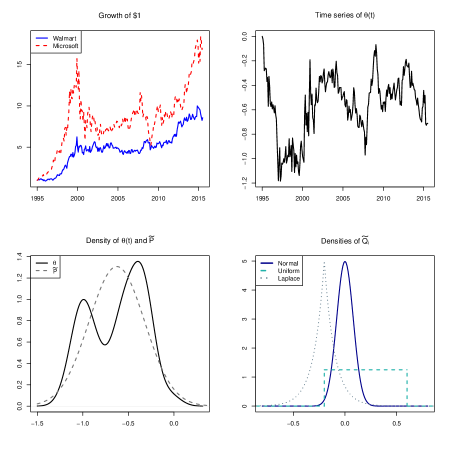

In this subsection we use a simple example to illustrate how our methodology of optimal transport might be applied in practice. Consider the monthly stock prices of Walmart (stock 1) and Microsoft (stock 2) from January 1995 to July 2015. The stock prices (normalized to be at January 1995) are plotted in Figure 4 (top left). The ‘market’ consists of the two stocks and the initial market weight is . We compute the exponential coordinate process (top right). Suppose we use the first 10 years of data (120 months) as training data. Our objective is to use the training data as well as choices of to construct portfolios that will be backtested using the next 10 years of data. To do this using optimal transport, we need to specify the probability distributions and on .

Choice of . The measure reflects our belief of the position of in the future. Figure 4 plots the density estimate of over the training period (bottom left). The distribution is bimodal (corresponding to the periods 1997-2000 and 2002-2004) and is mostly concentrated in the interval . Suppose our belief is that the market weight will most likely remain in this region in the next decade. For simplicity, we take to be the normal distribution whose mean and standard deviation match those of the density estimate. Explicitly, we have

A more diffuse distribution can be chosen if the investor is less certain.

Choice of . Recall that the portfolio has the representation

where is a function of and is the marginal distribution of , given that is distributed as .

To illustrate the effects of different distributions we consider three distributions given as follow:

Here we recall that the Laplace distribution with location parameter and scale parameter has density given by . The densities of these distributions are shown in Figure 4 (bottom right). We denote the resulting portfolios by , and .

Let us give some intuitions about these distributions. Overall, the distributions we choose concentrate in the interval . From Figure 3, they allow moderate deviations from the market weight but not too much (most of the time).

Note that has mean and has a rather small standard deviation (about a quarter of the standard deviation of ). This means that on average will not overweight or underweight stock 1 (Walmart) and the deviation is most of the time small. By Proposition 17, we know that is a diversity-weighted portfolio with . (From (55), the portfolio is constant-weighted if and buy-and-hold if .)

For , we expect that tends to underweight stock 1 (about of the time provided the future empirical distribution of is close to ). Since has bounded support, the weight ratios of are uniformly bounded on . However, the underweight can be significant on a certain region.

Finally, has a Laplace distribution which has fatter tails than the normal distribution. Thus we expect that deviates more (from the market portfolio) than a diversity-weighted portfolio with matching parameters near the boundary of the simplex. Also is chosen to have negative mean. Thus will tend to overweight stock 1. In practice, the location measure of should reflect the investor’s belief about the relative performances of the stocks in the future.

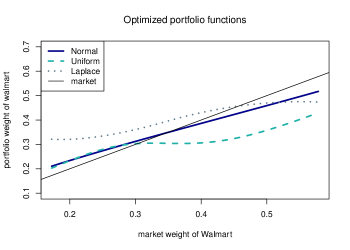

Results. For each choice of we solve the optimal transport problem using the method of monotone rearrangement (Theorem 16). The resulting portfolio functions are plotted in Figure 5. The range of shown contains more than of the mass of .

The features of the portfolios are consistent with our intuitions. As noted is a diversity-weighted portfolio which is quite close to the market portfolio by construction. Note that the curve intersects the market weight function around . This corresponds to the median of and is a consequence of the fact that is symmetric about . Thus if is close to reality, will overweight stock 1 half of the time and underweight stock 1 half of the time.

The portfolio consistently underweights stock 1 because is biased towards the right, and it has the largest deviation on the range shown. Nevertheless, if we draw the curves towards the boundary points and , the boundedness of the support of forces to be close to the market weight near the boundary of the simplex (in the sense that the weight ratios are bounded). This is not the case for and whose distributions have unbounded supports.

As for , we note that most of the curve is above the market because has negative mean. The portfolio deviates more and more towards the boundary because the Laplace distribution has fat tails. In this case, optimal transport couples large values of with the boundary values of which have small probability under .

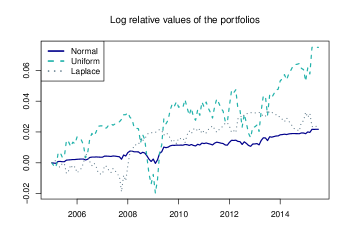

Backtesting. Finally we compute the relative values of the three portfolios with respect to the market portfolio during the testing period 2005-2015. The result is shown in Figure 6.

At the end of the period all three portfolios outperformed the market (by respectively , and , in log scale, over the 10 year period). The amounts are not large (except perhaps for ), and this is mostly because the portfolios deviate only moderately from the market portfolio. While detailed analysis of the performance is beyond the scope of the paper, we note that the relative riskiness of the portfolio (with respect to the market portfolio, also called the tracking error) depends on the deviation from the market weights and hence the location and dispersion of . The distribution deviates most from and thus is riskier; it also has the biggest reward at the end of the period. Note that the approach of optimal transport optimizes a portfolio function over a region of instead of picking portfolio weights period by period; it is simpler and perhaps more robust and prevents overfitting. See [Won15, Section 5] for another approach of optimizing functionally generated portfolios in terms of the concavity of the generating function.

References

- [AC10] S.-I. Amari and A. Cichocki, Information geometry of divergence functions, Bulletin of the Polish Academy of Sciences: Technical Sciences 58 (2010), no. 1, 183–195.

- [ANH07] S. Amari, H. Nagaoka, and D. Harada, Methods of information geometry, Translations of mathematical monographs, American Mathematical Society, 2007.

- [BF08] Adrian D. Banner and Daniel Fernholz, Short-term relative arbitrage in volatility-stabilized markets, Annals of Finance 4 (2008), no. 4, 445–454.

- [BFO14] Jean-David Benamou, Brittany D Froese, and Adam M Oberman, Numerical solution of the optimal transportation problem using the monge–ampere equation, Journal of Computational Physics 260 (2014), 107–126.

- [BHLP13] Mathias Beiglböck, Pierre Henry-Labordère, and Friedrich Penkner, Model-independent bounds for option prices: a mass transport approach, Finance and Stochastics (2013), 1–25.

- [BJ14] Mathias Beiglböck and Nicolas Juillet, On a problem of optimal transport under marginal martingale constraints., To appear in The Annals of Probability (2014).

- [BSS13] M. S. Bazaraa, H. D. Sherali, and C. M. Shetty, Nonlinear programming: Theory and algorithms, Wiley, 2013.

- [CK06] L. B. Chincarini and D. Kim, Quantitative equity portfolio management: An active approach to portfolio construction and management, McGraw-Hill Library of Investment and Finance, McGraw-Hill, 2006.

- [Fer99] Robert Fernholz, Portfolio generating functions, Quantitative Analysis in Financial Markets, River Edge, NJ. World Scientific (1999).

- [Fer02] E. R. Fernholz, Stochastic portfolio theory, Applications of Mathematics, Springer, 2002.

- [FK05] E. R. Fernholz and I. Karatzas, Relative arbitrage in volatility-stabilized markets, Annals of Finance 1 (2005), no. 2, 149–177.

- [FK09] by same author, Stochastic portfolio theory: an overview, Handbook of Numerical Analysis (P. G. Ciarlet, ed.), Handbook of Numerical Analysis, vol. 15, Elsevier, 2009, pp. 89 – 167.

- [FK11] Daniel Fernholz and Ioannis Karatzas, Optimal arbitrage under model uncertainty, The Annals of Applied Probability 21 (2011), no. 6, 2191–2225.

- [FKK05] E. R. Fernholz, I. Karatzas, and C. Kardaras, Diversity and relative arbitrage in equity markets, Finance and Stochastics 9 (2005), no. 1, 1–27.

- [Hör07] L. Hörmander, Notions of convexity, Modern Birkhäuser classics, Springer London, Limited, 2007.

- [JS12] Chloé Jimenez and Filippo Santambrogio, Optimal transportation for a quadratic cost with convex constraints and applications, Journal de mathématiques pures et appliquées 98 (2012), no. 1, 103–113.

- [PW13] S. Pal and T.-K. L. Wong, Energy, entropy, and arbitrage, ArXiv e-prints (2013), no. 1308.5376.

- [PW14] S. Pal and T.-K. L. Wong, The geometry of relative arbitrage, ArXiv e-prints (2014), no. 1402.3720v4.

- [Rai88] John Rainwater, Yet more on the differentiability of convex functions, Proceedings of the American Mathematical Society 103 (1988), no. 3, 773–778.

- [Roc97] R. T. Rockafellar, Convex analysis, Convex Analysis, Princeton University Press, 1997.

- [RW98] R Tyrrell Rockafellar and Roger J-B Wets, Variational analysis, vol. 317, 1998.

- [Str12] Winslow Strong, Generalizations of functionally generated portfolios with applications to statistical arbitrage, Arxiv e-prints (2012), no. 1212.1877.

- [Vil03] Cédric Villani, Topics in optimal transportation, Graduate studies in mathematics, American Mathematical Society, 2003.

- [Vil09] Cédric Villani, Optimal transport: old and new, vol. 338, Springer, 2009.

- [VK15] A. Vervuurt and I. Karatzas, Diversity-Weighted Portfolios with Negative Parameter, ArXiv e-prints (2015).

- [Won15] T.-K. L. Wong, Optimization of relative arbitrage, Annals of Finance (to appear) (2015).