Degrees of freedom for nonlinear least squares estimation

Abstract.

We give a general result on the effective degrees of freedom for nonlinear least squares estimation. It relates the degrees of freedom to the divergence of the estimator. We show that in a general framework, the divergence of the least squares estimator is a well defined but potentially negatively biased estimate of the degrees of freedom, and we give an exact representation of the bias. This implies that if we use the divergence as a plug-in estimate of the degrees of freedom in Stein’s unbiased risk estimate (SURE), we generally underestimate the true risk. Our result applies, for instance, to model searching problems, yielding a finite sample characterization of how much the search contributes to the degrees of freedom. Motivated by the problem of fitting ODE models in systems biology, the general results are illustrated by the estimation of systems of linear ODEs. In this example the divergence turns out to be a useful estimate of degrees of freedom for -constrained models.

Key words and phrases:

degrees of freedom, metric projection, nonlinear least squares, SURE2010 Mathematics Subject Classification:

62J02, 62J071. Introduction

The concept of effective degrees of freedom for least squares estimation in a mean value model is a classical and well studied concept, which is intimately related to and useful for model assessment and selection, see e.g. Hastie & Tibshirani (1990), Ye (1998), Efron (2004). The more recent interest in the concept has focused on the computation and estimation of degrees of freedom for non-smoothly penalized or constrained mean value models. The case of -penalized least squares estimation in linear models has recieved considerable attention, and Tibshirani & Taylor (2012) provide the most complete results. Convexity has been pivotal for these recent theoretical developments. In the constrained formulation the mean value model itself must be convex, and in the penalized formulation the results rely on duality theory from convex optimization. As we argue below, there are important applications in systems biology where the mean value models are inherently nonlinear and non-convex. Realistic models are complex and multivariate, and the amount of data is limited, so asymptotic arguments are difficult to justify. Thus for the development of appropriate small sample methods for model assessment, a detailed understanding of the effective degrees of freedom is very useful. We give results on the effective degrees of freedom for the completely general case where the mean value model is a closed set and the mean is estimated by least squares. We show that the classical estimator of the degrees of freedom – the divergence of the mean value estimator – is always well defined but generally biased. The bias arise from the non-convex geometry of the mean value model, and we show how the non-convexity is encoded into a Radon measure, and how this measure gives an explicit formula for the bias.

Our main motivation for considering non-convex mean value models is for estimation of continuous time dynamical models from experimental data as is encountered in systems biology, see e.g. Wilkinson (2006), Montefusco et al. (2011) or Oates & Mukherjee (2012). Multivariate ODE models constitute an important model class in this area. Despite the many existing approaches in the literature, data driven estimation and selection of a multivariate continuous time dynamical model remains a non-trivial problem. The challenges include the development of methods that scale well with the dimension of the model, as well as feasible methods to honestly assess the statistical uncertainty and to avoid overfitting. Through several approximations within the continuous time dynamical models, Oates & Mukherjee (2012) managed to recast aspects of the estimation problem (estimation of the network) in a unifying framework relying on the linear model. Though this allowed for the use of a range of regularization or model selection methods for the linear model, the conclusion was that “biological network inference remains profoundly challenging”. In addition, they observed that experimental designs with uneven sampling intervals represented particular difficulties. We believe that one of the difficulties lies in the approximations within the continuous time models, which become particularly pronounced for large sampling intervals. To overcome this problem and avoid the approximations, we need to consider estimation of the continuous time models directly, which inevitably leads to nonlinear mean value models.

We suggest that the challenges in systems biology outlined above may be approached by non-smooth regularization methods for estimation of parameters in multivariate ODE models. For this reason we consider -constrained nonlinear least squares estimation as a main example in the present paper. Our theoretical results do, however, apply to the general class of least squares estimators that are given by a possibly non-convex constraint on the mean value. Notably, they apply to estimators obtained by model searching.

In the remaining part of this introduction we describe the general setup in more details, and we outline the contributions of the paper. The objective is the assessment of the risk of nonlinear least squares estimators using Stein’s unbiased risk estimate (SURE), as treated in e.g. Efron (2004). SURE provides a non-asymptotic and unbiased estimate of the risk for general mean value estimators, if we can estimate the effective degrees of freedom unbiasedly. This was considered in Meyer & Woodroofe (2000) and Kato (2009) for the projection onto a closed convex set, and in Efron et al. (2004), Zou et al. (2007) and Tibshirani & Taylor (2012) for -penalized least squares estimation. Unbiased estimation of the effective degrees of freedom relies on Stein’s lemma, which does not hold in general – as we will show – for nonlinear least squares estimation. Our main result, Theorem 2, is a generalization of Stein’s lemma.

We consider the setup where , and . The objective is to estimate . With a nonempty closed set, and

| (1) |

denoting a point that minimizes the Euclidean distance from to , we estimate by . We do not require that belongs to . The map defined by (1) is known as the metric projection onto . Though it may not be uniquely defined everywhere, it is, in fact, Lebesgue almost everywhere unique. For the purpose of this introduction we assume that a (Borel measurable) selection has been made on the Lebesgue null set where the metric projection is not unique.

We may think of as the image of a parametrization, that is, for a map and a closed set it holds that

| (2) |

The setup thus includes most linear and nonlinear regression models, and the estimator is the least squares estimator. Moreover, by taking parameter sets of the form

for and some function , the setup includes many regularization methods in their constrained formulation, see Figure 1. If is continuous and is bounded in addition to being closed, then is compact and thus automatically closed. The assumption that is closed is the only regularity assumption we require for the general results to hold. Note, in particular, that is not assumed convex as in Meyer & Woodroofe (2000) and Kato (2009). For convex , the metric projection is Lipschitz, which implies that Stein’s lemma holds. The novelty of our results is that they apply without a convexity assumption on .

With

denoting the risk of the estimator, it is well known that

| (3) |

where

| (4) |

See e.g. Tibshirani & Taylor (2012), Efron (2004) and Ye (1998).

It turns out that the metric projection is Lebesgue almost everywhere differentiable, see Section 2, and we can therefore introduce the Stein degrees of freedom as

with denoting the divergence of . As mentioned above, if is almost differentiable, Lemma 2 (Stein’s lemma) in Stein (1981) implies that

However, differentiability Lebesgue almost everywhere does not imply almost differentiability, and Theorem 2 in Section 2 gives that in general

| (5) |

Theorem 2 also gives a characterization of , whose size is closely related to the distance from to points where the metric projection is non-differentiable, and the “magnitude” of the non-differentiability – see also the discussion in Section 6. This “magnitude” is in turn related to the non-convexity of , and our result is to the best of our knowledge the first result that characterizes how non-convexity affects the degrees of freedom, and hence the risk of the least squares estimator. The non-convexity of is basically unavoidable when we consider parametrized models with a nonlinear parametrization , and it is also pivotal for dealing with model search problems. A typical model search problem falls within our setup by taking to be a finite union of closed sets (the union of the different models). The prime example is best subset selection in linear regression, which corresponds to being a union of subspaces. We give a more detailed treatment of a special case of best subset selection in Example 1 and make some remarks about the general case after this example.

It follows from (3) and (5) that the risk estimate

| (6) |

is negatively biased in general – systematically underestimating the true risk. Whether we can estimate or bound this bias is still an open problem, but our characterization of in Theorem 2 provides a way to attack this problem. In Section 4 we present the results of using (6) in the context of -constrained estimation and model searching for dynamical systems modeled using linear ODEs. To compute we need formulas for the computation of the divergence , and we give two such results in Section 3 when is given by (2) – with some additional regularity assumptions on the parametrization .

2. Degrees of freedom for the metric projection

In this section we present the main general results on differentiability of the metric projection, and how the divergence is related to the degrees of freedom. This gives a characterization of the bias of as an estimate of in cases where the metric projection does not satisfy a sufficiently strong differentiability condition. The proofs are given in Section 5.

Definition 1.

With we say that a function is differentiable in in the extended sense if there is a neighborhood of such that is a Lebesgue null set and

for and a matrix .

If is differentiable in in the extended sense the matrix , depending on , is necessarily unique by denseness of in . We define the partial derivatives – and thus the divergence – of in in terms of by

for . Note that the partial derivatives of in need not exist in the classical sense if is differentiable in in the extended sense, but if they do, they coincide with .

Theorem 1.

There exists a Borel measurable choice of the metric projection as a map with the property that

for all . Moreover, , is uniquely defined and differentiable in the extended sense for Lebesgue almost all with for .

As a consequence of Theorem 1, is uniquely defined with probability 1, and it follows from the triangle inequality that

This shows, in particular, that has finite second moment. Moreover, Theorem 1 gives that the divergence is well defined and positive with probability 1. These considerations ensure that the following definition is meaningful.

Definition 2.

The degrees of freedom for the metric projection as an estimator of is defined as

| (7) |

and the Stein degrees of freedom is defined as

| (8) |

Our next result gives the general relation between and . To this end, let

denote the density for the distribution of – the multivariate normal distribution with mean vector and covariance matrix .

Theorem 2.

There exists a Radon measure , singular w.r.t. the Lebesgue measure, such that

| (9) |

The complete proof is given in Section 5, but let us explain the main ideas. Introducing the convex function

| (10) |

the metric projection is a subgradient of . The proof of Theorem 2 amounts to a computation of the second order distributional derivative of . Convexity of implies that the second order distributional derivatives in the coordinate directions are represented by positive measures, whence the partial distributional derivative of in the ’th direction is represented by a positive measure. Partial integration based on the definition (7) gives a representation of in terms of these partial distributional derivatives. Furthermore, the ’th partial distributional derivative of has, as a measure, Lebesgue decomposition

where denotes the Lebesgue measure on and . The measure that appears in Theorem 2 is given as . Note that depends only on the closed set , and is, in particular, independent of and .

|

To illustrate the general Theorem 2 we give a detailed treatment of the case where is the union of two orthogonal one-dimensional subspaces.

Example 1.

We consider the case , , and

is the union of the two orthogonal subspaces formed by the first and second coordinate axis. If we introduce the sets

for , we can for write the metric projection as

When we find that

and . To compute the singular measure we find, using Fubini’s theorem and standard partial integration, that for ,

This shows that the singular part of the distributional partial derivative of w.r.t. is the measure determined by

The singular measure is determined likewise, and is given by

By choosing positive functions such that for , it follows that

We find that the degrees of freedom for the selection among the two one-dimensional orthogonal projections becomes

In this particular case it follows directly from the covariance definition (7) that

where and are independent -distributed random variables. This concurs with findings in Ye (1998) on generalized degrees of freedom. The numerical value could in this case also be computed by computing the density of , and use this to compute the expectation .

The example above corresponds to best subset selection in linear regression with two orthogonal predictors. If we consider the general problem of best subset selection among subsets with linearly independent predictors we may note that . Recently, Tibshirani (2014) derived in the context of best subset selection an expression for for orthogonal predictors, and developed some generalizations of Stein’s lemma as well. He coined the term “search degrees of freedom” for the difference , as this difference in the context of best subset selection explicitly accounts for the contribution to the degrees of freedom coming from the model search. A straightforward consequence of our Theorem 2 is that the search degrees of freedom is, in fact, always positive. A fact that is intuitively reasonable – and observable in applications and simulation studies – but it has to the best of our knowledge not been established rigorously before. Though it may not be trivial, we expect that the measure can be computed for best subset selection in general. This promises further insights into the costs that model searching has on the degrees of freedom and ultimately the risk of the estimator.

As noted in the introduction, the risk estimate, , given by (3) underestimates the true risk whenever . An explicit representation of the bias follows directly from Theorem 2:

We observe that is unbiased if and only if the measure is the null measure. To control the size of the bias it may be useful to be able to bound the support of the singular measure . To this end we introduce the set of points with a non-unique metric projection onto . We call it the exoskeleton of , following the terminology in Hug et al. (2004), and we write

This set is also called the skeleton of the open set in Fremlin (1997). Theorem 1 implies that is a Lebesgue null set, but more is known. Theorem 1G in Fremlin (1997) gives, for instance, that has Hausdorff dimension at most . It should be noted that there can be points in where is not differentiable. We can then show the following proposition.

Proposition 1.

If

is locally Lipschitz, and in particular if it is , then .

If is convex (in addition to being nonempty and closed) the metric projection is uniquely defined everywhere and Lipschitz continuous, see Lemma 1 in Tibshirani & Taylor (2012). Thus and by Proposition 1 the measure is the null measure. From this we get the unbiasedness of for convex .

Corollary 1.

The measure in Theorem 2 is the null measure if is convex, in which case the risk estimate is unbiased.

To illustrate the general results further we give two additional examples. In Example 2 we consider the projection onto a convex -ball, which amounts to a form of -shrinkage. In Example 3 we consider the projection onto the -sphere, which shows some interesting phenomena in the non-convex case. Example 3 shows, in particular, that need not be convex for to be the null measure, and thus that the support of can be a strict subset of .

Example 2.

Let be the closed -ball with center and radius . Then

and

Since is convex

If the expectation and probability can be expressed in terms of incomplete -integrals. The unbiased estimate of is

It is interesting to compare the constrained estimator, which for fixed projects onto the ball of radius , with the linear shrinkage estimator

for a fixed . The linear shrinkage estimator coincides with the metric projection onto the ball with radius

| (11) |

It follows directly from (7) that the linear shrinkage estimator has degrees of freedom . For the metric projection onto a ball with radius given by (11) the unbiased estimate of the degrees of freedom equals

This is an unbiased estimate of degrees of freedom for a ball with fixed radius . The degrees of freedom for the linear shrinkage estimator is for fixed . The two estimates of degrees of freedom differ because the relation is -dependent.

Example 3.

In this example we take to be the -sphere of radius in , and we take and . Then for . The metric projection is not uniquely defined for and . The computation of the divergence is as above with

for . Since

we find that . Moreover,

and it follows that . Since straightforward computations give that

together with

for . This shows that

for , and we conclude that is the null measure for . This is an example where the measure can be 0 in cases where the exoskeleton is nonempty.

For we have , whereas has derivative for , and thus . It follows from Proposition 1 that (with the Dirac measure in 0) for . Since

we conclude that . Note that is the distributional derivative of the sign function.

3. Divergence formulas for nonlinear least squares regression

In this section our focus changes from the abstract results concerning an arbitrary closed set in to sets that are given in terms of a -dimensional parametrization. The main purpose is to provide explicit formulas for the computation of the divergence for a given in terms of the parametrization in two different situations of practical interest. Both results follow by implicit differentiation. The complete proofs are given in Section 2 in the supplementary material.

We assume in this section that , that is a closed set, and that the image is closed. The observation is fixed, and we make the following local regularity assumptions about the parametrization .

-

•

The metric projection of onto is unique with for .

-

•

The map is in a neighborhood of .

-

•

The map is open in , that is, if is a neighborhood of in , there is a neighborhood of in such that

The inverse function theorem implies the last assumption if the derivative of has rank (forcing ) in .

We introduce the two matrices and by

| (12) |

and

| (13) |

Note that for a linear model where for an matrix , .

Theorem 3.

If and has full rank , then

Note that under sufficient regularity assumptions, standard asymptotic arguments, see Sections 2.3 and 2.5 in Claeskens & Hjort (2008), give for fixed the expansion

for , with , , ,

The parameter is defined by , that is, is the point in the model closest to . Defining as the effective number of parameters, the generalization of AIC to misspecified models, known as Takeuchi’s information criterion, becomes

We recognize and as plug-in estimates of and , and thus as an estimate of . Theorem 3 identifies this estimate as the unbiased estimate of the Stein degrees of freedom. From the asymptotic arguments it does not follow that is negatively biased for finite sample sizes, but our Theorem 2 reveals that generally needs a finite sample correction.

We then turn our attention to the case where the parameter set is an -constrained subset of . That is, we consider parameter sets of the form

for and a fixed vector of nonnegative weights. With for , then is typically on the boundary of , and the formula in Theorem 3 for the divergence does not apply. Instead we note that fulfills the Karush-Kuhn-Tucker conditions

for with

and the Lagrange multiplier. We introduce the active set of parameters as

and let and denote the submatrices of and , respectively, with indices in .

Definition 3.

A solution to the Karush-Kuhn-Tucker conditions is said to fulfill the sufficient second order conditions if , for and for all nonzero satisfying .

Note that the sufficient second order conditions imply that a solution to the Karush-Kuhn-Tucker conditions is a local minimizer of in .

Theorem 4.

If has full rank , if and if fulfills the sufficient second order conditions, then

First note that has full rank and if is positive definite. For the linear model, this is the case when has rank . Then observe that in the case where is locally linear around to second order, that is, , we get that . Previous results in Zou et al. (2007) and Tibshirani & Taylor (2012) for -penalized linear regression give that the unbiased estimate of degrees of freedom is . The difference arises because we consider the constrained estimator, and this phenomenon was first observed in Kato (2009). See also Example 2 for a similar difference for -regularization. It is possible to compute the divergence of the penalized estimator under conditions similar to those above. The result is as expected. However, we cannot in an obvious way relate this quantity to the degrees of freedom of the penalized nonlinear least squares estimator. Our results hinge crucially on the fact that the estimator can be expressed in terms of a metric projection onto a closed set. If the penalized estimator can be given such a representation, e.g. via dualization as outlined in Tibshirani & Taylor (2012) in the linear case, we might be able to transfer the results to the penalized estimator, but we expect this to be difficult without convexity.

4. Model selection for a -dimensional linear ODE

In this section we present simulation results on the use of the risk estimate based on the divergence in a nontrivial example of nonlinear regression. The example considered is estimation of the parameters in a system of linear ordinary differential equations using an -constrained estimator as well as a model search approach. The main conclusion is that the bias of was considerable for the model search, while it was negligible for the -constrained estimator. All computations were carried out using the R package smde, see http://www.math.ku.dk/~richard/smde/.

The observations are with and for , and denoting the matrix exponential. It is well known that is the solution of the linear -dimensional ODE

for with initial condition . The unknown parameter is . We collect the observations into , and we let likewise denote the collection of expectations. We will identify the matrices and with vectors in for , which we denote by and as well (formally, the identification is made by stacking the columns). Thus . We also identify with a vector in where , and the parametrization is given as

| (14) |

We note that the number of observations as well as the number of parameters scale with . For many applications it may be realistic to achieve a good model for a sparse . Sparse estimation of is generally useful for computational and statistical reasons, and it may also be useful for network inference and interpretations.

We will in this paper focus on the special case , which we will refer to as the isochronal model. For the isochronal model with , in which case it is natural to parametrize the model in terms of . With an estimator of we can estimate as where denotes the principal matrix logarithm. The least squares estimator of amounts to ordinary linear least squares regression. We are, however, interested in obtaining sparse estimates of . Since the principal matrix logarithm does not preserve sparseness in general, we will maintain the parametrization in terms of and consider the family of -constrained nonlinear least squares estimators

where for and is a given weight matrix (with ). For technical details on the computation of derivatives and the implementation of the optimization algorithm see the supplementary material.

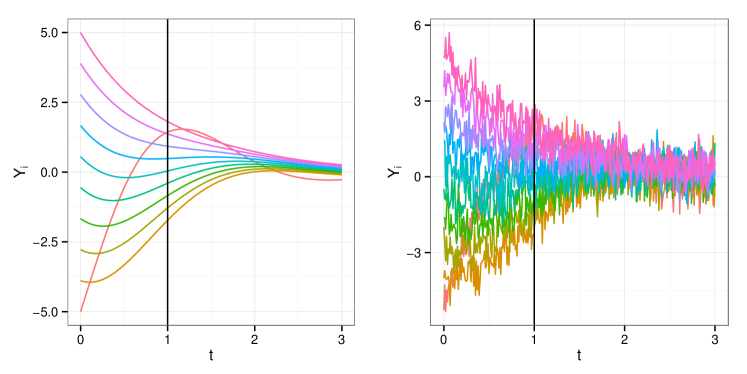

We did a simulation study with , , and . The matrix is given in the supplementary material, and contains 28 nonzero parameters out of 100. The matrix was chosen so that is dense and not well approximated by a sparse matrix. The matrix exponential is, in particular, not well approximated by the first order Taylor approximation . A single simulation of the sample paths is shown in Figure 3.

The initial conditions were sampled from the -dimensional normal distribution , and we used a total of replications. For the choice of weights (the ’s) we considered two situations; either , or adaptive weights, as introduced in Zou (2006), based on the MLE,

In this section we only report the results for the unit weights. See the supplementary material for the results using adaptive weights.

In the simulation study we computed the -constrained estimators for a range of values of and the corresponding estimates of the risk based on (6). The divergence was computed using Theorem 4 based on the formulas in Section 3 in the supplementary material.

With

denoting the data driven optimal estimate of , the resulting estimator of is . In addition, we computed the risk estimate

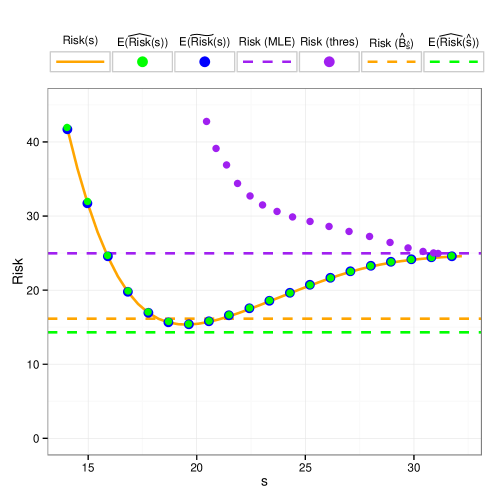

based on the approximation , see the discussion after Theorem 4. We also computed the MLE as well as a sequence of sparse(r) solutions obtained by hard thresholding the MLE. The results of the simulation study are summarized in Figure 4. The risk of the constrained estimator was minimal around . Both risk estimates, and , were, in this case, very close to being unbiased, and the estimated optimal constrained gave an estimator with close to minimal risk. The MLE and the sequence of thresholded MLEs all have larger risks than the constrained estimators for a substantial range of , and, more importantly, than the risk of . We should note, however, that did on average underestimate the actual risk of a little.

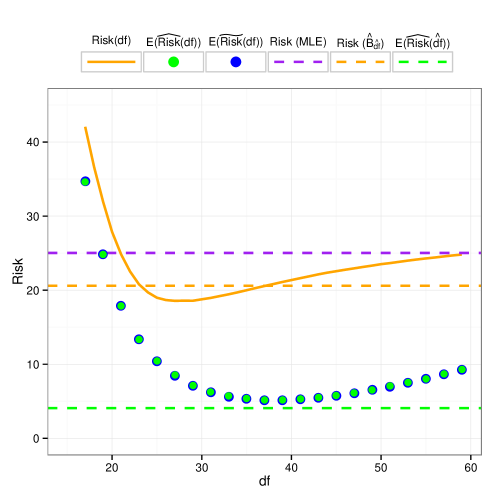

In addition to the -constrained estimator, we considered classical model searching. That is, we sought the best fitting model among all models with a given number of nonzero parameters. A complete search is computationally prohibitive, so we carried out a forward stepwise model search. The model search was initiated by a diagonal matrix, and in each step we added the parameter that decreased the squared error loss the most. The divergences were computed using either Theorem 3 or approximated by the number of nonzero parameters. The results are summarized in Figure 5. We found that the model with minimal risk had around 28 nonzero parameters. In this case, the risk estimates underestimated the true risk considerably. Moreover, they suggested that models with around 37 nonzero parameters had minimal risk. Consequently, the data driven choice of the number of nonzero parameters resulted in too large models with a correspondingly larger risk. In contrast to the -constrained case, the integral w.r.t. the singular measure in Theorem 2 can be detected as a bias for model searching. This bias cannot be ignored if we want to estimate the risk satisfactorily.

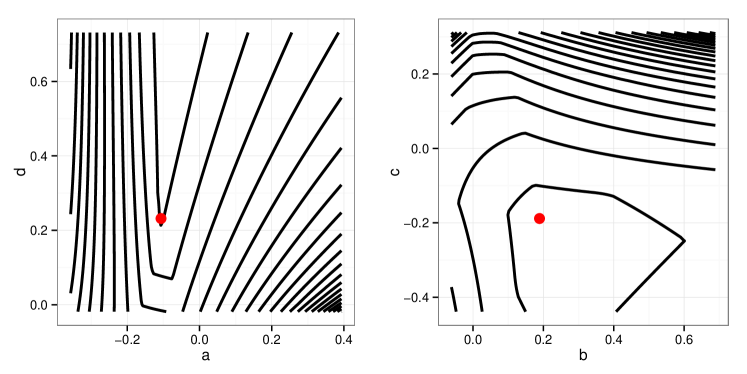

To understand better the results of the simulation study – and the nature of the nonlinear least squares problem – it would be desirable to be able visualize the image sets , or, in particular, the images of the boundaries of , for different choices of . These are the images under the matrix exponential of the boundaries of -balls. As these sets are subsets of a visualization is challenging. Figure 6 shows two selected slices of the sets by affine subspaces. The slices were constructed as follows. With

it holds that – the matrix that we used in the simulation. Fixing either or we get the two affine subspaces considered, which both include . The slices were computed as contour curves for and .

5. Proofs

In this section we give the proofs of the results stated in Sections 2. Doing so we will provide a brief account on the ideas and strategies used with some appropriate references to the literature. A further discussion of how our results and proofs are related to the literature is given in Section 6.

The proofs are based on the facts that the function defined by (10) is convex, that its subgradient in contains the points in closest to , and that if is differentiable in , its gradient equals the necessarily unique metric projection. That is, . This is all well known, see e.g. Theorem 3 in Asplund (1968) for a similar but abstract formulation, or Theorem 3.3 in Evans & Harris (1987) for an alternative formulation in . For completeness, Lemma 1 and its proof in the supplementary material give the details. Central to the proofs of Theorem 1 and Theorem 2 in Section 2 is a famous theorem of Alexandrov given first in Alexandrov (1939). It loosely states that a convex function is twice differentiable except perhaps on a Lebesgue null set. We state a version of Alexandrov’s theorem particularly useful for our purposes, which we will apply to the convex function .

Theorem 5.

Let be a convex function, and let denote the subset on which is differentiable. For Lebesgue almost all it holds that and there exists a matrix such that

| (15) |

for . The matrix is symmetric and positive semidefinite and as such uniquely determined by (15).

The theorem is a direct consequence of Theorem 2.3 and Theorem 2.8 in Rockafellar (2000). See, in addition, Chapter 13 – and Theorem 13.51 in particular – in Rockafellar & Wets (1998) for similar results. Theorem 5 also follows from Theorem 6.1 and Theorem 7.1 in Howard (1998), which is a nice self contained exposition of Rademacher’s and Alexandrov’s theorems.

In the light of Definition 1, Theorem 5 says that for a convex function , is defined Lebesgue almost everywhere, and is differentiable in the extended sense Lebesgue almost everywhere. Note, however, that the differentiability points of can be a strict subset of its maximal domain of definition.

Proof of Theorem 1.

The existence of a Borel measurable selection follows from general results in Rockafellar & Wets (1998). The set valued metric projection is defined as

As a set valued map, is outer semicontinuous by Example 5.23 in Rockafellar & Wets (1998), and combining Theorem 5.7 and Exercise 14.9 in Rockafellar & Wets (1998) it is, still as a set valued map, closed-valued and Borel measurable. Corollary 14.6 in Rockafellar & Wets (1998) implies that admits a Borel measurable selection, that is, there is a Borel measurable map with

for all .

Alexandrov’s Theorem can then be used to show that the selection of is unique and differentiable in the extended sense for Lebesgue almost all . Theorem 5 holds for the convex function . For those where (15) holds, the differentiability of in assures that is uniquely defined in as well as differentiable in in the sense of (15). The domain on which is uniquely defined thus satisfies that is a Lebesgue null set, and satisfies (15) for Lebesgue almost all . That is,

for , and is differentiable in the extended sense for Lebesgue almost all . By definition,

for those where is differentiable in the extended sense, and since is positive semidefinite, for . ∎

From hereon we assume, in accordance with Theorem 1, that a choice of has been made on the set where is not unique, such that is Borel measurable.

We turn to the proof of Theorem 2. The relation in Theorem 2 between the degrees of freedom, , and the Stein degrees of freedom, , will be established by partial integration. However, to handle metric projections in full generality we have to turn to distributional formulations of differentiation. Partial integration holds by definition for distributional differentiation. What we need is to identify the distributional partial derivatives of the coordinates of the metric projection. For this purpose, we define a signed Radon measure to be the difference of two (positive) Radon measures. In this sense a signed Radon measure need not have bounded total variation. Though we have to be careful with such a definition to avoid the undefined “", the difference of two Radon measures does give a well defined linear functional on .

Definition 4.

A function is of locally bounded variation if there exist signed Radon measures for on such that

for all .

Thus the functions of locally bounded variation are those -functions whose distributional partial derivatives are signed Radon measures. It is easily verified that Definition 4 is equivalent to other definitions in the literature, e.g. the definition in Chapter 5 in Evans & Gariepy (1992).

Lemma 1.

The functions for are of locally bounded variation. With denoting the ’th distributional partial derivative of it holds that

-

•

,

-

•

is a positive measure for all

-

•

and

for all with

(16) for all .

Proof.

First recall that

which proves that is in . A standard mollifier argument gives that for all

is a positive linear functional on due to convexity of . Riesz’s representation theorem gives the existence of a Radon measure such that

Taking and

for gives the existence of signed Radon measures , which by construction fulfill the two first bullet points. Since is convex, it is locally Lipschitz continuous, hence weakly differentiable with first weak partial derivatives coinciding with the pointwise partial derivatives, , for Lebesgue almost all . Hence

for all . We then prove that the partial integration formula generalizes to all that fulfill (16). To this end fix a positive function such that for . Define

then and

for . By monotone convergence

for . Moreover, and for , hence

for . Since

for some polynomial of degree independent of (for , say), and since the upper bound is integrable w.r.t. the -dimensional Lebesgue measure for large enough, it follows by dominated convergence that for large enough

The function is, in particular, -integrable. If fulfills (16) we let . Then , for , and

for . Moreover, for there is a constant such that

as well as

since fulfills (16). Again by Lebesgue as well as -integrability of the upper bound for large enough, it follows from dominated convergence that

∎

The first part of the proof of Lemma 1, where we establish the existence of the -measures, follows the proof of Theorem 6.3.2 in Evans & Gariepy (1992). In the remaining part we effectively prove that is a tempered distribution. This actually follows directly from the polynomial bound on by Example 7.12(c) in Rudin (1991). However, we need a little more than just the fact that the continuous linear functional

on the test functions extends to a continuous linear functional on the Schwartz space of rapidly decreasing functions. We also need the explicit form of the extension (the partial integration formula) as stated in Lemma 1.

To finally prove Theorem 2 we need to relate the distributional partial derivatives of to the pointwise partial derivatives defined Lebesgue almost everywhere. To this end we need the concept of approximate differentiability.

Definition 5.

Let denote the -dimensional Lebesgue measure and the -ball with center and radius . A function is approximately differentiable in if there is a matrix such that for all

for .

By Theorem 6.1.3 in Evans & Gariepy (1992) the matrix is unique if is approximately differentiable in . It is called the approximate derivative of in . Note that approximate differentiability of in is a local property, which only requires that is defined Lebesgue almost everywhere in a neighborhood of .

Lemma 2.

If is differentiable in in the extended sense then is approximately differentiable in with the same derivative.

Proof.

Assume that is differentiable in in the extended sense with derivative . We can then for fixed choose sufficiently small such that is a Lebesgue null set and

for . Choosing an arbitrary extension of to we find that

which implies that is approximately differentiable in with derivative . ∎

If has coordinates of locally bounded variation with corresponding distributional partial derivatives of denoted for we have by Lebesgue’s decomposition theorem that

with . We can now state (and subsequently use) a well known but rather deep result on approximate differentiability of functions of locally bounded variation. See Theorem 6.1.4 in Evans & Gariepy (1992).

Theorem 6.

If has coordinates of locally bounded variation then is approximately differentiable for Lebesgue almost all with derivative .

It is straightforward to see that if has coordinates of locally bounded variation then it is also, as a function from to , approximately differentiable for Lebesgue almost all with derivative .

Proof of Theorem 2.

From Lemma 1, is of locally bounded variation with distributional partial derivatives . Combining Theorem 1, Lemma 2 and Theorem 6 – and using that the approximate derivative is unique – we conclude that

with .

Proof of Proposition 1.

The set is open. If is locally Lipschitz on Theorem 4.2.5 in Evans & Gariepy (1992) gives that is weakly differentiable, and the weak partial derivative in the ’th direction coincides with the Lebesgue almost everywhere defined . That is,

for all . It follows that

and all the singular measures are null measures. ∎

6. Discussion

Our main result obtained in this paper is Theorem 2. It characterises the size of , which can be interpreted as how much the non-convexity of affects the degrees of freedom. From Theorem 2 we observe that , and its magnitude is determined by how large is on the Lebesgue null set where the singular measure is concentrated. This is, in turn, determined by the distance (scaled by ) from to points in in combination with the distribution of the mass of the measure on . The singular measure depends only on , and it represents global geometric properties of .

Previous results on degrees of freedom in Tibshirani & Taylor (2012), Kato (2009), Zou et al. (2007) and Meyer & Woodroofe (2000) all correspond to being convex, and the resulting Lipschitz continuity of the metric projection implies pointwise differentiability almost everywhere by Rademacher’s Theorem. To establish pointwise differentiability almost everywhere of the metric projection onto any closed set, we relied instead on the fact that it is the derivative of a convex function. We then used Alexandrov’s theorem for convex functions to establish almost everywhere differentiability of the metric projection. This is in principle well known in the mathematical literature, and Asplund provided, for instance, only a brief argument in Asplund (1973) for what is close to being Theorem 1. However, we needed to clarify in what sense the metric projection is differentiable, and the precise relationship between pointwise derivatives Lebesgue almost everywhere and distributional derivatives for which partial integration applies. The original formulation of Alexandrov’s theorem was, in particular, stated as the existence of a quadratic expansion of a convex funktion for Lebesgue almost all . This formulation does not require a definition of differentiability of in in cases where is not defined in a neighborhood of . Consequently, the conclusion cannot be formulated in terms of alone. The more recent formulation of Alexandrov’s theorem as in Theorem 5 was useful, since it allowed us to formulate Theorem 1 in terms of differentiability properties of the metric projection itself rather than as a quadratic expansion of .

We gave three simple examples where analytic computations could shed some light on the general results, and then we considered a more serious application in Section 4 on the estimation of parameters in a -dimensional linear ODE. This example served several purposes. First we used it to test our algorithms for computing the nonlinear -regularized least squares estimator, and we used it to test the divergence formula given in Theorem 4. For the chosen model and parameter set and the -constrained estimator we concluded that was, for all practical purposes, unbiased, that it was useful for selection of , and that the selected model had a lower risk than e.g. the MLE. The example also showed that in this case the approximation to the divergence was sufficiently accurate to be a computationally cheap alternative to the formula from Theorem 4. When we considered model searching instead, the risk estimate based on the divergence became biased, and tended to select too complex models. Our conclusion is that for the -constrained estimator, the set may be non-convex, but this presents no problem for the estimation of the degrees of freedom by the divergence. On the contrary, when is a union of models and we perform model searching, the non-convexity of implies that the divergence underestimates the degrees of freedom considerably.

For practical applications we are faced with three challenges: We need to compute the divergence to estimate ; we need to control, estimate or bound the difference ; and we need to know or estimate . For the latter, the typical solution is to estimate in an (approximately) unbiased way. In the ODE example an estimate of can be based on the MLE of . For the computation of the divergence we gave two formulas for parametrized models. We expect that similar formulas can be derived via implicit differentiation in cases where we have a parametrized model, but with different restrictions on the parameters than we considered. Alternatively, abstract results in Chapter 13 in Rockafellar & Wets (1998) can be considered. The greatest challenge is to control the difference . Our simulations showed an example where this difference was negligible as well as an example where it was not. In some simple cases we were also able to compute the measure , which can be used to compute the difference. We do not expect that it will be an easy task to compute in many cases of practical interest, but we do expect that it will be possible for best subset selection. We also expect that it will be possible to make analytic progress on the further characterization of and its support, e.g. when it has a density w.r.t. the -dimensional Hausdorff measure. It is, in addition, possible to show that under a so-called prox-regularity assumption on , the metric projection is Lipschitz in a neighborhood of , see Poliquin et al. (2000). Thus in this neighborhood is 0. This can be a path for bounding if is close to . Even if it appears to be a challenging path, our representation of in terms of the singular measure does provide us with a novel way to achieve further progress.

References

- (1)

- Alexandrov (1939) Alexandrov, A. D. (1939), ‘Almost everywhere existence of the second differential of a convex function and some properties of convex surfaces connected with it’, Leningrad Sate University Annals [Uchenye Zapiski] Mathematical Series 6, 3–35.

- Asplund (1968) Asplund, E. (1968), ‘Fréchet differentiability of convex functions’, Acta Math. 121, 31–47.

- Asplund (1973) Asplund, E. (1973), ‘Differentiability of the metric projection in finite-dimensional Euclidean space’, Proc. Amer. Math. Soc. 38, 218–219.

- Bühlmann & van de Geer (2011) Bühlmann, P. & van de Geer, S. (2011), Statistics for high-dimensional data, Springer Series in Statistics, Springer, Heidelberg. Methods, theory and applications.

-

Claeskens & Hjort (2008)

Claeskens, G. & Hjort, N. L. (2008), Model selection and model averaging, Cambridge Series in Statistical

and Probabilistic Mathematics, Cambridge University Press, Cambridge.

http://dx.doi.org/10.1017/CBO9780511790485 - Efron (2004) Efron, B. (2004), ‘The estimation of prediction error: Covariance penalties and cross-validation’, Journal of the American Statistical Association pp. 99–467.

-

Efron et al. (2004)

Efron, B., Hastie, T., Johnstone, I. & Tibshirani, R.

(2004), ‘Least angle regression’, Ann.

Statist. 32(2), 407–499.

With discussion, and a rejoinder by the authors.

http://dx.doi.org/10.1214/009053604000000067 - Evans & Gariepy (1992) Evans, L. C. & Gariepy, R. F. (1992), Measure theory and fine properties of functions, Studies in Advanced Mathematics, CRC Press, Boca Raton, FL.

-

Evans & Harris (1987)

Evans, W. D. & Harris, D. J. (1987), ‘Sobolev embeddings for generalized ridged domains’, Proc. London

Math. Soc. (3) 54(1), 141–175.

http://dx.doi.org/10.1112/plms/s3-54.1.141 -

Fremlin (1997)

Fremlin, D. H. (1997), ‘Skeletons and central

sets’, Proc. London Math. Soc. (3) 74(3), 701–720.

http://dx.doi.org/10.1112/S0024611597000233 - Hastie & Tibshirani (1990) Hastie, T. J. & Tibshirani, R. J. (1990), Generalized additive models, Vol. 43 of Monographs on Statistics and Applied Probability, Chapman and Hall, Ltd., London.

-

Hastie et al. (2009)

Hastie, T., Tibshirani, R. & Friedman, J. (2009), The Elements of Statistical Learning, Springer

Series in Statistics, second edn, Springer, New York.

Data mining, inference, and prediction.

http://dx.doi.org/10.1007/978-0-387-84858-7 - Howard (1998) Howard, R. (1998), Alexandrov’s theorem on the second derivatives of convex functions via Rademacher’s theorem on the first derivatives of Lipschitz functions. Unpublished lecture notes.

-

Hug et al. (2004)

Hug, D., Last, G. & Weil, W. (2004), ‘A local Steiner-type formula for general closed sets and applications’,

Math. Z. 246(1-2), 237–272.

http://dx.doi.org/10.1007/s00209-003-0597-9 -

Kato (2009)

Kato, K. (2009), ‘On the degrees of freedom

in shrinkage estimation’, Journal of Multivariate Analysis 100(7), 1338 – 1352.

http://www.sciencedirect.com/science/article/pii/S0047259X08002753 -

Meyer & Woodroofe (2000)

Meyer, M. & Woodroofe, M. (2000),

‘On the degrees of freedom in shape-restricted regression’, Ann.

Statist. 28(4), 1083–1104.

http://dx.doi.org/10.1214/aos/1015956708 - Montefusco et al. (2011) Montefusco, F., Cosentino, C. & Bates, D. G. (2011), Nonlinear dynamics: a brief introduction, in M. P. H. STUMPF, D. J. BALDING & M. GIROLAMI, eds, ‘Handbook of Statistical Systems Biology’, Wiley-Blackwell, pp. 83–111.

-

Oates & Mukherjee (2012)

Oates, C. J. & Mukherjee, S. (2012), ‘Network inference and biological dynamics’, The Annals of Applied

Statistics 6(3), 1209–1235.

http://dx.doi.org/10.1214/11-AOAS532 -

Poliquin et al. (2000)

Poliquin, R. A., Rockafellar, R. T. & Thibault, L. (2000), ‘Local differentiability of distance functions’, Trans. Amer. Math. Soc. 352(11), 5231–5249.

http://dx.doi.org/10.1090/S0002-9947-00-02550-2 - Rockafellar (2000) Rockafellar, R. T. (2000), ‘Second-order convex analysis’, J. Nonlinear Convex Anal. 1(1), 1–16.

-

Rockafellar & Wets (1998)

Rockafellar, R. T. & Wets, R. J.-B. (1998), Variational analysis, Vol. 317 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of

Mathematical Sciences], Springer-Verlag, Berlin.

http://dx.doi.org/10.1007/978-3-642-02431-3 - Rudin (1991) Rudin, W. (1991), Functional analysis, International Series in Pure and Applied Mathematics, second edn, McGraw-Hill Inc., New York.

- Stein (1981) Stein, C. M. (1981), ‘Estimation of the mean of a multivariate normal distribution’, Ann. Statist. 9(6), 1135–1151.

-

Tibshirani (2014)

Tibshirani, R. J. (2014), ‘Degrees of freedom

and model search’, arXiv pp. 1–21.

http://arxiv.org/abs/1402.1920 -

Tibshirani & Taylor (2012)

Tibshirani, R. J. & Taylor, J. (2012), ‘Degrees of freedom in lasso problems’, Ann.

Statist. 40(2), 1198–1232.

http://dx.doi.org/10.1214/12-AOS1003 - Wilkinson (2006) Wilkinson, D. J. (2006), Stochastic modelling for systems biology, Chapman & Hall/CRC Mathematical and Computational Biology Series, Chapman & Hall/CRC, Boca Raton, FL.

-

Ye (1998)

Ye, J. (1998), ‘On measuring and correcting

the effects of data mining and model selection’, J. Amer. Statist.

Assoc. 93(441), 120–131.

http://dx.doi.org/10.2307/2669609 -

Zou (2006)

Zou, H. (2006), ‘The adaptive lasso and its

oracle properties’, J. Amer. Statist. Assoc. 101(476), 1418–1429.

http://dx.doi.org/10.1198/016214506000000735 -

Zou et al. (2007)

Zou, H., Hastie, T. & Tibshirani, R. (2007), ‘On the “degrees of freedom” of the lasso’, Ann. Statist. 35(5), 2173–2192.

http://dx.doi.org/10.1214/009053607000000127