Pricing Currency Derivatives with Markov-modulated Lvy Dynamics

Abstract

Using a Lvy process we generalize formulas in Bo et al. (2010) for the Esscher transform parameters for the log-normal distribution which ensure the martingale condition holds for the discounted foreign exchange rate. Using these values of the parameters we find a risk-neural measure and provide new formulas for the distribution of jumps, the mean jump size, and the Poisson process intensity with respect to to this measure. The formulas for a European call foreign exchange option are also derived. We apply these formulas to the case of the log-double exponential distribution of jumps. We provide numerical simulations for the European call foreign exchange option prices with different parameters.

| 1 | Department of Mathematics and Statistics, University of Calgary, Canada |

| aswish@ucalgary.ca | |

| 2 | Department of Mathematics and Statistics, University of Calgary, Canada |

| mtertych@ucalgary.ca, maksym.tertychnyi@gmail.com | |

| 3 | Department of Mathematics and Statistics, University of Calgary, Canada |

| relliott@ucalgary.ca, robert.elliott@haskayne.ucalgary.ca |

Keywords : foreign exchange rate, Esscher transform, risk-neutral measure, European call option, Lvy processes, Markov processes.

Mathematics Subject Classification : 91B70, 60H10, 60F25.

1 Introduction

Until the early 1990s the existing academic literature on the pricing of foreign currency options could be divided into two categories. In the first, both domestic and foreign interest rates were assumed to be constant whereas the spot exchange rate is assumed to be stochastic. See, e.g., Jarrow et al (1981, [3]). The second class of models for pricing foreign currency options incorporated stochastic interest rates, and were based on Merton’s 1973, [30]) stochastic interest rate model for pricing equity options. See, e.g., Grabbe (1983, [23]), Adams et al (1987, [1]). Unfortunately, this pricing approach did not integrate a full term structure model into the valuation framework. To our knowledge, Amin et al. (1991, [3]) were the first to start discussing and building a general framework to price contingent claims on foreign currencies under stochastic interest rates using the Heath et al. (1987) model of term structure. Melino et al. (1991, [28]) examined the foreign exchange rate process, (under a deterministic interest rate), underlying observed option prices and Rumsey (1991, [37]) considered cross-currency options. Mikkelsen (2001, [32]) investigated by simulation cross-currency options using market models of interest rates and deterministic volatilities for spot exchange rates. Schlogl (2002, [38]) extended market models to a cross-currency framework. Piterbarg (2005, [34]) developed a model for cross-currency derivatives such as PRDC swaps with calibration for currency options; he used neither market models nor stochastic volatility models. In Garman et al. (1983, [10]) and Grabbe (1983, [23]), foreign exchange option valuation formulas were derived under the assumption that the exchange rate follows a diffusion process with continuous sample paths. Takahashi et al. (2006, [42]) proposed a new approximation formula for the valuation of currency options using jump-diffusion stochastic volatility processes for spot exchange rates in a stochastic interest rates environment. In particular, they applied the market models developed by Brace et al. (1998), Jamshidian (1997, [20]) and Miltersen et al. (1997, [31]) to model the term structure of interest rates. Also, Ahn et al. (2007, [2]) derived explicit formulas for European foreign exchange call and put options values when the exchange rate dynamics are governed by jump-diffusion processes. Hamilton (1988) was the first to investigate the term structure of interest rates by rational expectations econometric analysis of changes in regime. Goutte et al. (2011, [11]) studied foreign exchange rates using a modified Cox-Ingersoll-Ross model under a Hamilton Markov regime switching framework. Zhou et al. (2012, [43]) considered an accessible implementation of interest rate models with regime-switching. Siu et al (2008, [40]) considered pricing currency options under a two-factor Markov modulated stochastic volatility model. Swishchuk and Elliott applied hidden Markov models for pricing options in [41]. Bo et al. (2010, [8]) discussed a Markov-modulated jump-diffusion, (modeled by a compound Poisson process), for currency option pricing. We note that currency derivatives for domestic and foreign equity markets and for the exchange rate between the domestic currency and a fixed foreign currency with constant interest rates were discussed in Bjork (1998, [6]). We also mention that currency conversion for forward and swap prices with constant domestic and foreign interest rates were discussed in Benth et al. (2008, [5]).

In this article we generalize the results of [8] to a case when the dynamics of the FX rate are driven by a general Lvy process ([33]). The main results of our research are as follows:

1) In section 2 we generalize the formulas of [8] for Esscher transform parameters which ensure that the martingale condition for the discounted foreign exchange rate is a martingale for a general Lvy process (see (30)). Using these values of the parameters (see (39), (40)) we proceed to a risk-neural measure and provide new formulas for the distribution of jumps, (see (36)), the mean jump size (see (20)), and the Poisson process intensity with respect to the measure(see (19)). At the end of section 2 pricing formulas for European call foreign exchange options are given. (They are similar to those in [8], but the mean jump size and the Poisson process intensity with respect to the new risk-neutral measure are different).

2) In section 3 we apply formulas (19), (20), (39), (40) to the case of log double exponential processes, (see (51)), for jumps (see (58)-(63)).

3) In section 5 we provide numerical simulations of European call foreign exchange option prices for different parameters, (in the case of log-double exponential and exponential distributions of jumps): , where is the initial spot FX rate, is the strike FX rate for a maturity time and the parameters refer to the log-double exponential distribution.

In the Appendix codes for Matlab functions used in numerical simulations of option prices are provided.

2 Currency option pricing for general Lvy processes

Let be a complete probability space with a probability measure P. Consider a continuous-time, finite-state Markov chain on with a state space , the set of unit vectors with a rate matrix 111In our numerical simulations we consider three-state Markov chain and calculate elements in using Forex market EURO/USD currency pair. The dynamics of the chain are given by:

| (1) |

where is a -valued martingale with respect to , the P-augmentation of the natural filtration , generated by the Markov chain . Consider a Markov-modulated Merton jump-diffusion which models the dynamics of the spot FX rate, given by the following stochastic differential equation (in the sequel SDE, see [8]):

| (2) |

Here is drift parameter; is a Brownian motion, is the volatility; is a Poisson Process with intensity , is the amplitude of the jumps, given the jump arrival time. The distribution of has a density . The parameters , , are modeled using the finite state Markov chain:

| (3) |

The solution of (2) is , (where is the spot FX rate at time ). Here is given by the formula:

| (4) |

There is more than one equivalent martingale measure for this market driven by a Markov-modulated jump-diffusion model. We shall define the regime-switching generalized Esscher transform to determine a specific equivalent martingale measure.

Using Ito’s formula we can derive a stochastic differential equation for the discounted spot FX rate. To define the discounted spot FX rate we need to introduce domestic and foreign riskless interest rates for bonds in the domestic and foreign currency.

The domestic and foreign interest rates , are defined using the Markov chain (see [8]):

The discounted spot FX rate is:

| (5) |

Using (5), the differentiation formula, see Elliott et al. (1982, [12]) and the stochastic differential equation for the spot FX rate (2) we find the stochastic differential equation for the discounted discounted spot FX rate:

| (6) |

To derive the main results consider the log spot FX rate

Using the differentiation formula:

| (7) |

| (8) |

Let denote the P-augmentation of the natural filtration , generated by . For each set . Let us also define two families of regime switching parameters

, : , , .

Define a random Esscher transform on using these families of parameters , (see [8], [13], [15] for details):

| (9) |

The explicit formula for the density of the Esscher transform is given in the following Theorem. A similar statement is proven for the log-normal distribution in [8]. The formula below can be obtained by another approach, considered by Elliott and Osakwe ([14]).

In addition,the random Esscher transform density (see (9), (10)) is an exponential martingale and satisfies the following SDE:

| (11) |

Proof of Theorem 2.1. The compound Poisson Process, driving the jumps and the Brownian motion are independent processes. Consequently:

| (12) |

Let us calculate:

Write

Using the differentiation rule (see [12]) we obtain the following representation of :

| (13) |

where

is a martingale with respect to . Using this fact and (13) we obtain:

| (14) |

We have from the differentiation rule:

| (15) |

where is the volatility of a market.

| (17) |

If we represent in the form (see (17)) and apply differentiation rule we obtain (11). It follows from (11) that is a martingale.

We shall derive the following condition for the discounted spot FX rate ((5)) to be martingale. These conditions will be used to calculate the risk-neutral Esscher transform parameters , and give to the measure Q. Then we shall use these values to find the no-arbitrage price of European call currency derivatives.

Theorem 2.2. Let the random Esscher transform be defined by (9). Then the martingale condition(for , see (5)) holds if and only if the Markov modulated parameters () satisfy for all the condition:

| (18) |

Here the random Esscher transform intensity of the Poisson Process and the main percentage jump size are, respectively, given by

| (19) |

| (20) |

as long as , .

Proof of Theorem 2.2. The martingale condition for the discounted spot FX rate is

| (21) |

To derive this condition a Bayes’ formula is used:

| (22) |

taking into account that is a martingale with respect to , so:

| (23) |

Using formula (5) for the solution of the SDE for the spot FX rate, we obtain an expression for the discounted spot FX rate in the following form:

Using the expression for the characteristic function of Brownian motion (see (15)) we obtain:

| (27) |

| (29) |

From (29) we obtain the martingale condition for discounted spot FX rate:

| (30) |

We now prove, that under the Esscher transform the new Poisson process intensity and mean jump size are given by (19), (20).

Note that is the jump part of Lvy process in the formula (4) for the solution of SDE for spot FX rate. We have:

| (31) |

where P is the initial probability measure and Q is the new risk-neutral measure. Substituting the density of Esscher transform (10) into (31) we have (see also [14]):

| (32) |

Using (14) we obtain:

| (33) |

Substitute (33) into (32) and taking into account the characteristic function of Brownian motion (see (15)) we obtain:

| (34) |

Returning to the initial measure P, but with different ,we have:

| (35) |

Formula (19) for the new intensity of Poisson process follows directly from (34), (35). The new density of jumps is defined from (35) by the following formula:

| (36) |

We now calculate the new mean jump size given the jump arrival with respect to the new measure Q:

| (37) |

where the new measure is defined by the formula (36).

We can rewrite the martingale condition (30) for the discounted spot FX rate in the following form:

| (38) |

If we put , we obtain the following formulas for the regime switching Esscher transform parameters yielding the martingale condition (38):

| (39) |

| (40) |

In the next section we shall apply these formulas (39), (40) to the log-double exponential distribution of jumps.

We now proceed to the general formulas for European calls (see [8], [29]). For the European call currency options with a strike price and the time of expiration the price at time zero is given by:

| (41) |

Let denote the occupation time of in state over the period . We introduce several new quantities that will be used in future calculations:

| (42) |

where ;

| (43) |

| (44) |

| (45) |

| (46) |

where is the variance of the distribution of the jumps.

| (47) |

where is the number of jumps in the interval , is the number of states of the Markov chain .

Note, that in our considerations all these general formulas (42)-(47) mentioned above are simplified by the fact that: with respect to the new risk-neutral measure Q with Esscher transform parameters given by (39), (40). From the pricing formula in Merton (1976, [29]) let us define (see [8])

| (48) |

where is the standard Black-Scholes price formula (see [6]) with initial spot FX rate , strike price , risk-free rate , volatility square and time to maturity.

Then, the European style call option pricing formula takes the form (see [8]):

| (49) |

where is the joint probability distribution density for the occupation time, which is determined by the following characteristic function (See [14]):

| (50) |

where is a vector of ones, is a vector of transform variables, .

3 Currency option pricing for log-double exponential processes

The log-double exponential distribution for ( are the jumps in (2)), plays a fundamental role in mathematical finance, describing the spot FX rate movements over long period of time. It is defined by the following formula of the density function:

| (51) |

The mean value of this distribution is:

| (52) |

The variance of this distribution is:

| (53) |

The double-exponential distribution was first investigated by Kou in [24]. He also gave economic reasons to use such a type of distribution in Mathematical Finance. The double exponential distribution has two interesting properties: the leptokurtic feature (see [22],; [24] ) and the memoryless property(the probability distribution of X is memoryless if for any non-negative real numbers and , we have , see for example [45]). The last property is inherited from the exponential distribution.

A statistical distribution has the leptokurtic feature if there is a higher peak (higher kurtosis) than in a normal distribution. This high peak and the corresponding fat tails mean the distribution is more concentrated around the mean than a normal distribution, and it has a smaller standard deviation. See details for fat-tail distributions and their applications to Mathematical Finance in [44]. A leptokurtic distribution means that small changes have less probability because historical values are centered by the mean. However, this also means that large fluctuations have greater probabilities within the fat tails.

In [27] this distribution is applied to model asset pricing under fuzzy environments. Several advantages of models including log-double exponential distributed jumps over other models described by Lvy processes (see [24]) include:

1) The model describes properly some important empirical results from stock and foreign currency markets. The double exponential jump-diffusion model is able to reflect the leptokurtic feature of the return distribution. Moreover, the empirical tests performed in [36] suggest that the log-double exponential jump-diffusion model fits stock data better than the log-normal jump-diffusion model.

2) The model gives explicit solutions for convenience of computations.

3) The model has an economical interpretation.

4) It has been suggested from extensive empirical studies that markets tend to have both overreaction and underreaction to good or bad news.The jump part of the model can be considered as the market response to outside news. In the absence of outside news the asset price (or spot FX rate) changes in time as a geometric Brownian motion. Good or bad news(outer strikes for the FX market in our case) arrive according to a Poisson process, and the spot FX rate changes in response according to the jump size distribution. Since the double exponential distribution has both a high peak and heavy tails, it can be applied to model both the overreaction (describing the heavy tails) and underreaction (describing the high peak) to outside news.

5) The log double exponential model is self-consistent. In Mathematical Finance, it means that a model is arbitrage-free.

The family of regime switching Esscher transform parameters is defined by (39), (40). Let us define , (the first parameter has the same formula as in general case) by:

| (54) |

We require an additional restriction for the convergence of the integrals in (54):

| (55) |

Then (54) can be rewritten in the following form:

| (56) |

Solving (56) we arrive at the quadratic equation:

| (57) |

If we have two solutions and one of them satisfies restriction (55):

| (58) |

Then the Poisson process intensity (see (19)) is:

| (59) |

The new mean jump size (see (20)) is:

| (60) |

as in the general case.

When we proceed to a new risk-neutral measure we have a new density of jumps

| (61) |

The new probability can be calculated using (36):

| (62) |

From (62) we obtain an explicit formula for :

| (63) |

4 Currency option pricing for log-normal processes

Log-normal distribution of jumps with the mean, the deviation (see [46]), and its applications to currency option pricing was investigated in [8]. More details of these distributions and other distributions applicable for the Forex market can be found in [47]. We give here a sketch of results from [8] to compare them with the case of the log-double exponential distribution of jumps discussed in this article. The main goal of our paper is a generalization of this result for arbitrary Lvy processes. The results, provided in [8] are as follows:

Theorem 2.3. For the density of the Esscher transform defined in (9) is given by

| (64) |

where are the mean value and deviation of jumps, respectively. In addition, the random Esscher transform density , (see (9), (10)), is an exponential martingale and satisfies the following SDE

| (65) |

Theorem 2.4. Let the random Esscher transform be defined by (9). Then the martingale condition(for , see (5)) holds if and only if the Markov modulated parameters () satisfy for all the condition:

| (66) |

where the random Esscher transform intensity of the Poisson Process and the mean percentage jump size are respectively given by

| (67) |

| (68) |

The regime switching parameters satisfying the martingale condition (66) are given by the following formulas: is the same as in (39),

| (69) |

With such a value of a parameter :

| (70) |

Note, that these formulas (67)-(70) follow directly from our formulas for the case of general Lvy process, (see (19),(20), (40)). In particular, the fact that by substituting (40) into the expression for in (20). From (40) we derive:

| (71) |

As

| (72) |

we obtain from (71) the following equality:

| (73) |

The expression for the value of the Esscher transform parameter in (69) follows immediately from (73). Inserting this value of into the expression for in (19) we obtain the formula (70).

In the numerical simulations, we assume that the hidden Markov chain has three states: up, down, side-way, and the corresponding rate matrix is calculated using real Forex data for the thirteen-year period: from January 3, 2000 to November 2013. To calculate all probabilities we use the Matlab script (see the Appendix).

5 Numerical simulations

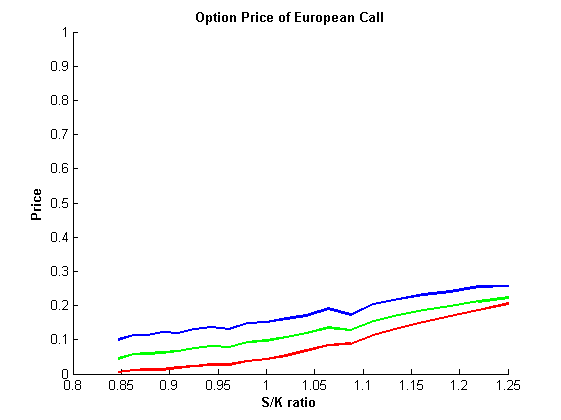

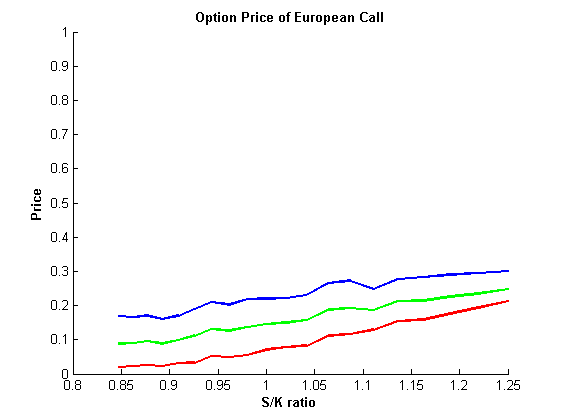

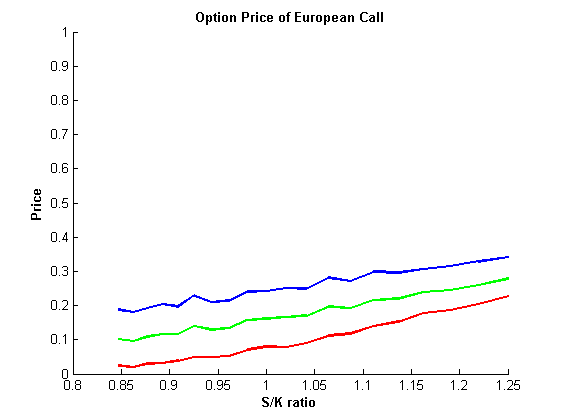

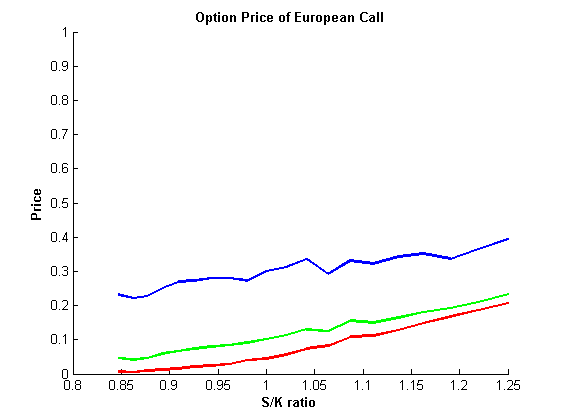

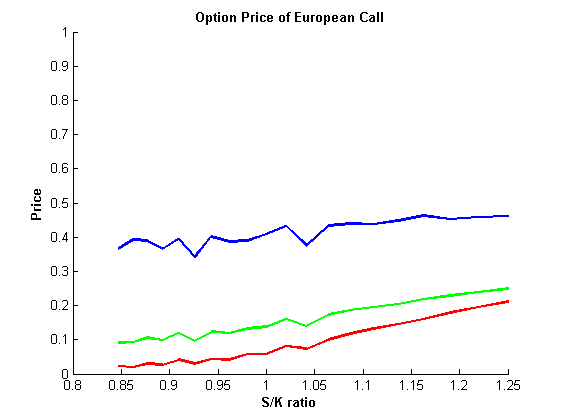

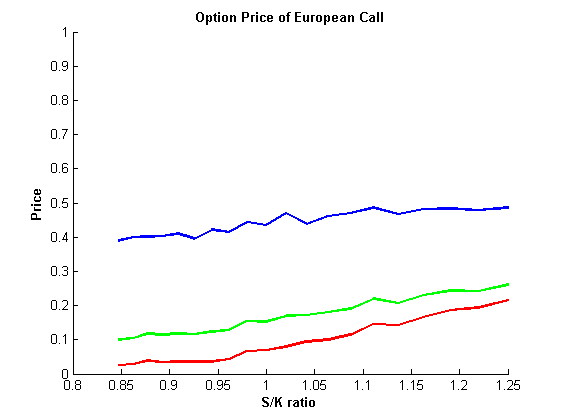

In the Figures 2-4 we shall provide numerical simulations for the case when the amplitude of jumps is described by a log-double exponential distribution. These three graphs show a dependence of the European-call option price against , where is the initial spot FX rate, is the strike FX rate for a different maturity time in years: 0.5, 1, 1.2. We use the following function in Matlab:

Draw( S_0,T,approx_num,steps_num, teta_1,teta_2,p,mean_normal,sigma_normal)

to draw these graphs222Matlab scripts for all plots are available upon request. The arguments of this function are: is the starting spot FX rate to define first point in ratio, is the maturity time, approx num describe the number of attempts to calculate the mean for the integral in the European call option pricing formula (see section 2, (49)), steps num denotes the number of time subintervals to calculate the integral in (49); teta 1, teta 2, p are parameters in the log-double-exponential distribution (see section 3, (51)). mean normal, sigma normal are the mean and deviation for the log-normal distribution (see section 4). In these three graphs: ; .

Blue line denotes the log-double exponential, green line denotes the log-normal, red-line denotes the plot without jumps. The ratio ranges from 0.8 to 1.25 with a step 0.05; the option price ranges from 0 to 1 with a step 0.1. The number of time intervals: num =10.

From these three plots we conclude that it is important to incorporate jump risk into the spot FX rate models. Described by Black-Scholes equations without jumps, red line on a plot is significantly below both blue and green lines which stand for the log-double exponential and the log-normal distributions of jumps, respectively.

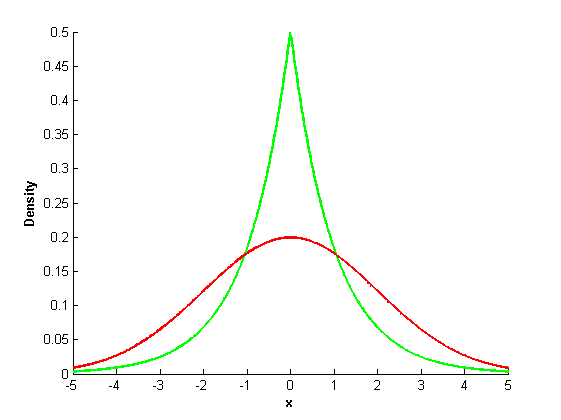

All three plots have the same mean value 0 and approximately equal deviations for both types of jumps: log-normal and log-double exponential. We investigate the case when it does not hold (see Figures 5-7).

As we can see, the log-double exponential curve moves up in comparison with the log-normal and without jumps option prices.

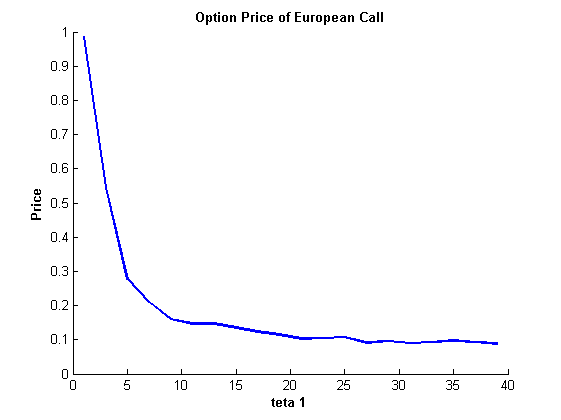

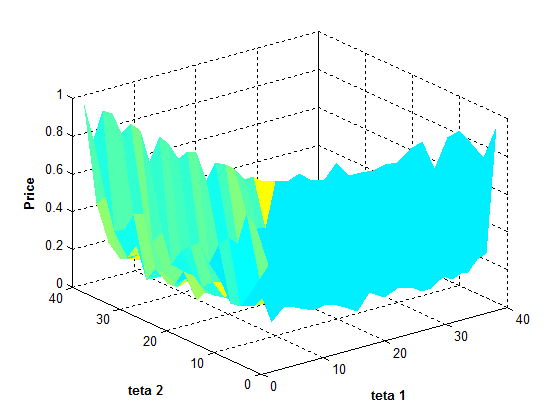

If we fix the value of the parameter in the log-double exponential distribution with the corresponding plot is given in Figure 8.

Figure 9 represents a plot of the dependence of the European-call option price against values of the parameters in a log-double exponential distribution, again .

6 Conclusion

In the conclusion, we generalized the results of [8] to the case when the dynamics of the FX rate is driven by a general Lvy process. The main results of our research are as follows: 1) We generalized the formulas of [8] for Esscher transform parameters which ensure that the martingale condition for the discounted foreign exchange rate is a martingale for a general Lvy process. Using the values of these parameters we proceeded to a risk-neural measure and provide new formulas for the distribution of jumps, the mean jump size, and the Poisson process intensity with respect to the measure. Pricing formulas for European call foreign exchange options have been given as well (They are similar to those in [8], but the mean jump size and the Poisson process intensity with respect to the new risk-neutral measure are different); 2) We applied obtained formulas to the case of log double exponential processes; 3) We also provided numerical simulations of European call foreign exchange option prices for different parameters. Codes for Matlab functions used in numerical simulations of option prices are also provided.

References

- [1] Adams P. and Wyatt S. (1987): Biases in option prices: Evidence from the foreign currency option market. J. Banking and Finance, December, 11, 549-562.

- [2] Ahn C., Cho D. and Park K. (2007): The pricing of foreign currency options under jump-diffusion processes. J. Futures Markets, 27, 7, 669-695.

- [3] Amin K. and Jarrow R. (1991): Pricing foreign currency options under stochastic interest rates. J. Intern. Money and Finance, 10, 310-329.

- [4] Bates, D.S., 1996. Jumps and stochastic volatility: exchange rate processes implicit in Deutsche mark options. Review of Financial Studies 9, 69-107.

- [5] Benth F., Benth J. and Koekebakker S. (2008): Stochastic Modeling of Electricity and Related Markets. World Scientific.

- [6] Bjork T. (1998): Arbitrage Theory in Continuous Time. 2nd ed. Oxford University Press.

- [7] Black, F. and M. Schotes. (1973): The pricing of options and corporate liabilities, Journal of Political Economy 81, 637-659. Clark, P.. 1973, A subordinated stochastic

- [8] Bo L., Wang Y. and Yang X. (2010): Markov-modulated jump-diffusion for currency option pricing. Insurance: Mathematics and Economics, 46, 461-469.

- [9] Brace A., Gatarek D. and Musiela M. (1998): A multifactor Gauss Markov implementation of Heath, Jarrow, and Morton. Mathematical Finance,7, 127-154.

- [10] Garman M. and Kohlhagern S. (1983): Foreign currency options values. J. Intern. Money and Finance. 2, 231-237.

- [11] Goutte S. and Zou B. (2011): Foreign exchange rates under Markov regime switching model. CREA Discussion paper series. University of Luxemburg.

- [12] Elliott, R. J. (1982): Stochastic Calculus and Applications. Springer.

- [13] Elliott, R.J., Chan, L., Siu, T.K. (2005): Option pricing and Esscher transform under regime switching. Annals of Finance 1, 423-432.

- [14] Elliott, R.J., Osakwe, Carlton-James U. (2006): Option Pricing for Pure Jump Processes with Markov Switching Compensators. Finance and Stochastics, Vol. 10, Issue 2, p 250-275.

- [15] Elliott, R.J., Siu, T.K., Chan, L., Lau, J.W. (2007): Pricing options under a generalized Markov-modulated jump-diffusion model. Stochastic Analysis and Applications 25, 821-843.

- [16] Hamilton J. (1988): Rational-expectations econometric analysis of changes in regime: an investigation of the term structure of interest rates. J. Econ. Dyna. Control, 12 (2-3), 385-423.

- [17] Heath D., Jarrow R. and Morton A. (1987): Bond pricing and term structureof interest rates: A new methodology for contingent claims valuation. Cornell University, October.

- [18] Heston, S.L. (1993): A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies 6, 327–343.

- [19] Hull, John C. Options, Futures and Other Derivatives. Pearson International Edition, 2006.

- [20] Jamshidian F. LIBOR and swap market models and measures. Finance and Stochastics, 1, 293-330.

- [21] Jarrow R. and Oldfield G. (1981): Forward contracts and futures contracts. J. Financial Economics, 9,373-382.

- [22] Johnson, N., S. Kotz, N. Balakrishnan. (1995): Continuous Univariate Distribution, Vol. 2, 2nd ed. Wiley, New York.

- [23] Grabbe O. (1983): The pricing of call and put options on foreign exchange. J. Intern. Money and Finance, December, 2, 239-253.

- [24] Kou S. G. (2002): A jump-diffusion model for option pricing. Management Science, 48(8), 1086–1101.

- [25] Lech A. Grzelak, Cornelis W. Oosterlee. (2010): On Cross-Currency Models with Stochastic Volatility and Correlated Interest Rates. Munich Personal RePEc Archive;

- [26] Luenberger, D. Investment Science. Oxford University Press, 1998.

- [27] Li-Hua Zhang, Wei-Guo Zhang, Wen-Jun Xu, Wei-Lin Xiao. (2012): The double-exponential jump-diffusion model for pricing European options under fuzzy envirionments. Economical Modelling, 29, 780-786.

- [28] MelinoA. And Turnbull S. (1991): The pricing of foreign-currency options. Canadian J. Economics, 24, 251-181.

- [29] Merton, R.C., 1976. Option pricing when underlying stock returns are discontinuous. Journal of Finance and Economics 3, 125-144.

- [30] Merton R. (1973): The theory of rational option pricing. Bell J. Econ. Manag. Sci., Spring, 4, 141-183.

- [31] Miltersen K., Sandmann K. and Sondermann D. (1997): Closed form solutions for term structure derivatives with long-normal interest rates. J. Finance, 52, 409-430.

- [32] Mikkelsen P. (2001): Cross-currency LIBOR market model. University of Aarhus.

- [33] Papapantoleon A. (2000): An introduction to Lvy processes with Applications to Mathematical Finance. Lecture notes.

- [34] Piterbarg V. (2005): A multi-currency model with FX volatility skew. Working paper.

- [35] Privault N. (2013): Notes on Stochastic Finance. Lecture Notes. Nicolas Privault Notes on Stochastic Finance http://www.ntu.edu.sg/home/nprivault/indext.html.

- [36] Ramezani, C. A., Y. Zeng. (1999): Maximum likelihood estimation of asymmetric jump-diffusion process: Application to security prices. Working paper, Department of Statistics, University of Wisconsin, Madison, WI.

- [37] Rumsey J. (1991): Pricing cross-currency options. J. Futures markets, 11, 89-93.

- [38] Scholgl E. (2002): A multicurrency extension of the lognormal interest rate market models. Finance and Stochastics, 6, 173-196.

- [39] Shreve S.E. (2000): Stichastic Calculus for Finance 2. 2nd ed. Springer.

- [40] Siu T.K., Yang H. and Lau J. (2008): Pricing currency options under two-factor Markov-modulated stochastic volatility model. Insurance: Mathematics and Economics, 43, 295-302.

- [41] Swishchuk A., Elliott R., Pricing options. Hidden Markov Models in Finance, Springer, 2007.

- [42] Takahashi A., Takehara K. and Yamazaki A. (2006): Pricing currency options with a market model of interest rates under jump-diffusion stochastic volatility processes of spot exchange rates. CIRJE-F- 451, working paper.

- [43] Zhou N. and Mamon R. S. (2012): An accessible implementation of interest rate models with regimeswitching. Expert Systems with Applications, 39(5), 4679-4689.DOI URL:10.1016/j.eswa.2011.09.053.

- [44] http://vudlab.com/fat-tails.html

- [45] http://www.mast.queensu.ca/ stat455/lecturenotes/set4.pdf

- [46] http://www.fordham.edu/economics/mcleod/LogNormalDistribution.pdf

- [47] http://www.mql5.com/en/articles/271

Appendix

The Matlab function used to calculate probability matrix for the Markov chain modeling cross rates of currency pairs in the Forex market.

We assume that the Markov chain has only three states: "trend up", "trend down", "trend sideway". Such a choice of states is justified by numerous articles for the FX market (See www.mql5.com). In a file MaxDataFile open.CSV there are open prices of EURO/ESD currency pairs of Japanese candles over a 13 year period. This file was generated in the platform MT5 using MQL5 programming language.

function [ Probab_matrix ] =Probab_matrix_calc1(candles_back_up, candles_back_down,

delta_back_up, delta_back_down, candles_up,candles_down, delta_up, delta_down )

Probab_matrix=zeros(3,3);

m_open=csvread(’MaxDataFile_open.CSV’);

[size_open temp]=size(m_open);

m_before=zeros(1,size_open);

upper_border=size_open-max(candles_up, candles_down);

delta_up=delta_up/10000;

delta_down=delta_down/10000;

count_up=0;

count_down=0;

count_sideway=0;

beforeborder=max(candles_back_up, candles_back_down)+1;

for i=beforeborder:size_open

if (m_open(i)-m_open(i-candles_back_up)>=delta_up)

m_before(i)=1;

end

if (m_open(i-candles_back_down)-m_open(i)>=delta_down)

m_before(i)=-1;

end

end;

for i=1:upper_border

if(m_before(i)==1)

if(m_open(i+candles_up)-m_open(i)>=delta_up)

Probab_matrix(1,1)= Probab_matrix(1,1)+1;

else

if(m_open(i)-m_open(i+candles_down)>=delta_down)

Probab_matrix(1,2)= Probab_matrix(1,2)+1;

else

Probab_matrix(1,3)= Probab_matrix(1,3)+1;

end

end

end

if(m_before(i)==-1)

if(m_open(i+candles_up)-m_open(i)>=delta_up)

Probab_matrix(2,1)= Probab_matrix(2,1)+1;

else

if(m_open(i)-m_open(i+candles_down)>=delta_down)

Probab_matrix(2,2)= Probab_matrix(2,2)+1;

else

Probab_matrix(2,3)= Probab_matrix(2,3)+1;

end

end

end

if(m_before(i)==0)

if(m_open(i+candles_up)-m_open(i)>=delta_up)

Probab_matrix(3,1)= Probab_matrix(3,1)+1;

else

if(m_open(i)-m_open(i+candles_down)>=delta_down)

Probab_matrix(3,2)= Probab_matrix(3,2)+1;

else

Probab_matrix(3,3)= Probab_matrix(3,3)+1;

end

end

end

end

count_up=sum(Probab_matrix(1,:));

count_down=sum(Probab_matrix(2,:));

count_sideway=sum(Probab_matrix(3,:));

for j=1:3

Probab_matrix(1,j)= Probab_matrix(1,j)/count_up;

Probab_matrix(2,j)= Probab_matrix(2,j)/count_down;

Probab_matrix(3,j)= Probab_matrix(3,j)/count_sideway

end

end

For example run in Matlab:

[ Probab_matrix ] = Probab_matrix_calc1(30, 30, 10, 10, 30, 30, 10, 10);

Probability matrix is as follows: