thmTheorem \newshadetheoremalgAlgorithm \newshadetheorempropProposition \newshadetheoremcorCorollary

On the solution of stochastic optimization and variational problems in imperfect information regimes

Abstract

We consider the solution of a stochastic convex optimization problem over a closed and convex set in a regime where is unavailable and is a suitably defined random variable. Instead, may be obtained through the solution of a learning problem that requires minimizing a metric in over a closed and convex set . Traditional approaches have been either sequential or direct variational approaches. In the case of the former, this entails the following steps: (i) a solution to the learning problem, namely , is obtained; and (ii) a solution is obtained to the associated computational problem which is parametrized by . Such avenues prove difficult to adopt particularly since the learning process has to be terminated finitely and consequently, in large-scale instances, sequential approaches may often be corrupted by error. On the other hand, a variational approach requires that the problem may be recast as a possibly non-monotone stochastic variational inequality problem in the space; but there are no known first-order stochastic approximation schemes are currently available for the solution of this problem. To resolve the absence of convergent efficient schemes, we present a coupled stochastic approximation scheme which simultaneously solves both the computational and the learning problems. The obtained schemes are shown to be equipped with almost sure convergence properties in regimes when the function is either strongly convex as well as merely convex. Importantly, the scheme displays the optimal rate for strongly convex problems while in merely convex regimes, through an averaging approach, we quantify the degradation associated with learning by noting that the error in function value after steps is , rather than when is available. Notably, when the averaging window is modified suitably, it can be see that the originakl rate of is recovered. Additionally, we consider an online counterpart of the misspecified optimization problem and provide a non-asymptotic bound on the average regret with respect to an offline counterpart. In the second part of the paper, we extend these statements to a class of stochastic variational inequality problems, an object that unifies stochastic convex optimization problems and a range of stochastic equilibrium problems. Analogous almost-sure convergence statements are provided in strongly monotone and merely monotone regimes, the latter facilitated by using an iterative Tikhonov regularization. In the merely monotone regime, under a weak-sharpness requirement, we quantify the degradation associated with learning and show that expected error associated with is . Preliminary numerics demonstrate the performance of the prescribed schemes.

keywords:

stochastic optimization, stochastic variational inequality, stochastic approximation, learningAMS:

1 Introduction

In the last two decades, robust optimization [7, 8] approaches have grown in relevance when decision-makers are faced with optimization problems with uncertain parameters. Succinctly, in such an approach, given an uncertainty set that captures the realizations assumed by such a parameter, the robust solution represents the worst-case over this set of realizations. Naturally, an appropriate choice of such an uncertainty set is crucial and as the availability of data reaches levels hitherto unseen, there is growing interest in data-driven approaches [9] for constructing such sets. Our interest is in closely related yet distinct settings driven by data in which the point estimate of a parameter may be obtained through a learning problem, suitably defined through the aggregation of data. We provide two instances of such problems:

(i) Portfolio optimization

Portfolio optimization problems prescribe the optimal constructions of portfolios over a set of assets, for which the mean and covariance of returns are not necessarily known. Traditional approaches have assumed that such returns are available while more recent robust optimization models have utilized factor-based models in constructing uncertainty sets [22, 11, 10]. An alternate, and possibly less conservative, data-driven model of such a problem that employs a point estimate of the mean and covariance matrix requires the solution of two coupled problems: (1) A portfolio optimization problem parametrized by representing the mean and covariance matrix of returns; and (2) A learning problem that utilizes data to obtain the best .

(ii) Power systems operation

The operation of power grids relies on the solution of hourly (or more frequent) commitment and dispatch problems, each of which is reliant on a range of parameters that are often uncertain. These parameters include supply-side information regarding capacity of wind-power as well as load forecasts. Recently robust optimization approaches have proved to be exceedingly popular [26, 49, 43]. An alternate formulation is given by the following two coupled problems: (1) An economic dispatch problem parametrized by , a vector that captures the unknown supply and demand side parameters; and (2) A learning problem that computes through the accumulation of data.

We believe that such coupled formulations have broad applicability beyond merely the settings mentioned above in (i) and (ii). They may also find application in inventory control problems with stochastic demand [36, 1, 44, 2], robust network design [33], robust routing in communication networks [23], amongst others. To recap the difference between the two problem frameworks, it can be seen that (R-Opt), a robust optimization framework, minimizes the worst-case of the optimal value over the uncertainty set while (L-Opt) considers the joint solution of an optimization problem in , parametrized by , where is a solution to a learning problem with a metric . The following formulations may provide a clearer comparison:

|

We consider regimes where the function is a convex expected-value function and the resulting problem is given by the following:

| () |

where is a closed and convex set, is a dimensional random variable defined on a probability space , is a real-valued function, and denotes an dimensional vector of parameters. Estimating such parameters often requires the resolution of a suitably defined learning problem, given by a stochastic optimization problem (), and defined next:

| () |

where is a closed and convex set, is a random variable defined on a probability space

, and is a real-valued function. When one considers the joint problem of learning and optimization, then

there are at least two obvious approaches that immediately emerge as

possibilities:

(a) Sequential approach: Consider an inherently serial process wherein the first stage

incorporates a model/parameter specification phase based on statistical

learning while the second stage leverages these findings in developing

and solving the actual optimization problem of interest. Such an

ordering relies on the learning problems being relatively small and

tractable compared to the optimization problems, ensuring that accurate

solutions are available within a reasonable time period. Strictly

speaking, if one terminates the learning process prematurely with

an estimator , the

resulting estimator is essentially corrupted by error in that . This error

propagates into the solution of the computational problem, denoted by

and the associated gap might be quite

significant. Note that unless the learning problem is solvable via a

finite termination algorithm, such a approach cannot provide asymptotic

statements but can, at best, provide approximate solutions.

Consequently, an inherently serial process reliant on a prematurely

truncated learning scheme often fails to provide accurate solutions to

the computational problem.

(b) Variational approach: Under suitable convexity

and differentiability requirements, the following holds:

if and only if is a solution to the (stochastic) variational inequality problem VI [15] where

Recall that is a

solution to VI if for all . Furthermore, if and denote solutions to

and (), respectively, then an

oft-used avenue in obtaining a solution

entails obtaining a solution to VI. However, unless

rather strong assumptions are imposed, the map is not

necessarily monotone, precluding the use of recently developed

stochastic approximation schemes for solving

monotone stochastic variational inequality

problems [25, 32, 47],

extragradient-based

variants [27, 48], and accelerated

approaches [13].

Simultaneous approach: This paper is motivated by the inadequacy of available approaches and,

more generally, the absence of asymptotically convergent schemes with

provable non-asymptotic rates. We present

a framework where the learning and the computational problems are

solved simultaneously via a joint set of stochastic approximation

schemes. Such an avenue has several advantages. First, under such an

approach, one can provide rigorous statements of asymptotic convergence

of the obtained estimators for both, the solution to the computational

problem and the associated learning problem. Second, error bounds on the

expected error can be provided for a fixed number of steps under a

regime with constant and diminishing steplengths. Third, the statements

may be extended to the variational regime in which the computational

problem is given by the variational counterpart of

, given by ; such a problem requires an such that

| () |

where is a closed and convex set, is a dimensional random variable defined on a probability space , is a real-valued continuous mapping. Note that when , this reduces to a convex optimization problem. Furthermore, the choice of using a variational problem, rather than merely an optimization problem, is founded on the need to model a variety of multiagent settings complicated by a breadth of strategic interactions, ranging from purely cooperative to distinctly noncooperative [16].

1.1 Related decision-making models

While unaware of the availability of general purpose

tools that can resolve precisely such problems, we describe

settings where such questions have assumed relevance:

Adaptive control [5]: In tracking

problems in adaptive

control [3], the authors consider a perturbation approach for

analyzing a adaptive tracking algorithm and consider three estimation

schemes, specifically least mean squares (LMS)

scheme, its recursive variant (RLMS), and the Kalman filter (which

requires some distributional assumptions on the noise). First, much of this treatment is in the unconstrained

regime with tractable (often quadratic estimation objectives),

allowing for deriving closed-form (and often linear) update rules.

Second, when the noise in the estimation process is

Gaussian, the Kalman filter provides a minimum variance estimator. If

on the other hand, the noise is non-Gaussian, then the Kalman filter

provides the optimal linear estimator (in the sense that no linear

filter provides smaller variance). In fact, these assumptions often form the basis of most adaptive

control algorithms (cf. [37] and [34] for a

discussion adaptive control and stochastic approximation.)

Our focus is on static stochastic problems with far less assumptions

on the nature of the problem and the associated distributions.

Specifically, we allow for more general stochastic convex objectives

(or monotone maps in the context of VIs) in either the optimization

or the learning problem, allow for convex feasibility sets for both

the optimization or the learning problems, and impose relatively

mild moment assumptions on the noise (unlike the Gaussian

assumptions that are necessary in some of the estimation

models).

Iterative learning control: A related avenue lies in iterative learning control (ILC) has its roots in the studies by Uchiyama [46] and Arimoto et al. [4]. ILC [39] is a form of tracking control employed for repetitive control problems, instances being chemical batch processes, robot arm manipulators, and reliability testing rigs. Our problem is more restrictive in its focus (static problems) but allow for more general settings in terms of nonlinearity and the underlying distributional requirements.

Multi-armed bandit problems: The multi-armed bandit (MAB) problem considers the question of how to play given a collection of slot machines faced by a gambler. Each machine provides a random reward from a distribution specific to that machine. The gambler aims to maximize the expected sum of rewards earned through a sequence of lever pulls. The total discounted reward is maximized by the index policy that pulls the bandit having greatest value of the Gittins index [21]. In effect, the reward function needs to be learnt while optimizing the system. There has been significant research on such problems over the last several decades, including on the question of computation [30] and finite-time analysis [6].

Finally, related questions also been studied in revenue management where [14] examined the devastating effect of learning with an incorrect model while maximizing revenue.

1.2 Outline and contributions

Broadly speaking, this paper focuses on the development of stochastic approximation schemes that generate iterates and and makes the following contributions. (i) In Section 2, we prove the a.s. convergence of the produced iterates to the prescribed solutions and derive error bounds in a standard and an averaging regime. In particular, we quantify the degradation in the convergence rate from introducing an additional learning phase; (ii) Section 2 concludes with a precise non-asymptotic bound on the average regret associated with employing the proposed scheme instead of an offline algorithm; (iii) In Section 3, we extend the a.s. convergence results to accommodate stochastic variational inequality problems, rather than merely convex optimization problems. Error analysis is carried out under a suitably defined growth property; (iv) In Section 4, we provide some supporting numerics and conclude in Section 5. Finally, throughout the paper, we use to denote the Euclidean norm of a vector , i.e., and to denote the Euclidean projection operator onto a set , i.e., .

2 Stochastic optimization problems with imperfect information

In this section, we focus on examining under various assumptions. We begin by stating the coupled stochastic approximation scheme and providing the necessary assumptions in Section 2.1. Convergence analysis of the presented scheme is provided in Section 2.2 while diminishing and constant steplength rate analysis is performed in Section 2.3. We conclude with a discussion of an online algorithm with the associated bounds on the decay of average regret in Section 2.4.

2.1 Algorithm statement and assumptions

As mentioned in the previous section, we propose a set of coupled stochastic approximation schemes for computing and .

Algorithm 1 (Coupled SA schemes for stochastic optimization problems).

Step 0. Given and sequences ,

Step 1.

| (Optk) | ||||

| (Learnk) |

where and .

Step 2. If , stop; else , go to Step. 1.

We begin by stating an assumption on the functions and .

Assumption 1 (Problem properties, A1-1).

Suppose the following hold:

-

(i)

For every , is strongly convex and continuously differentiable with Lipschitz continuous gradients in with convexity constant and Lipschitz constant , respectively.

-

(ii)

For every , the gradient is Lipschitz continuous in with constant .

-

(iii)

The function is strongly convex and continuously differentiable with Lipschitz continuous gradients in with convexity constant and Lipschitz constant , respectively.

Under Assumption (A1-1), the coupled problem admits a unique solution, as shown next.

Lemma 1 (Solvability).

Consider the problems and and suppose assumption (A1) holds. Then and collectively admit a unique solution.

Proof 2.1.

This follows from the strong convexity of over and the strong convexity of over .

Additionally, we make the following assumptions on the steplength sequences employed in the algorithm.

Assumption 2 (Steplength requirements, A2-1).

Let and be chosen such that:

-

(i)

,

-

(ii)

.

We define a new probability space , where , and . We use to denote the sigma-field generated by the initial points and errors for , i.e., and for We make the following assumptions on the filtration and errors.

Assumption 3 (A3).

Let the following hold:

-

(i)

and for all .

-

(ii)

and for all .

We conclude this subsection by stating three results (without proof) that will be subsequently employed in developing our convergence statements. The first two of these are relatively well-known super-martingale convergence results (cf. [41, Lemma 10, Pg. 49–50])

Lemma 2.

Let be a sequence of nonnegative random variables adapted to -algebra and such that

where , , and , and . Then,

Lemma 3.

Let , , and be non-negative random variables adapted to -algebra . If , and

Then, is convergent and almost surely.

Finally, we present a contraction result reliant on monotonicity and Lipschitz continuity requirements (cf. [17, Theorem 12.1.2, Pg. 1109]).

Lemma 4.

Let be a mapping that is strongly monotone over with constant , and Lipschitz continuous over with constant . If , then for any , we have that for any , we have

2.2 Almost-sure convergence

Our first convergence result shows that under the prescribed assumptions, Algorithm 1 generates a sequence of iterates that converges to the unique solution.

Proposition 5 (Almost-sure convergence under strong convexity of ).

Proof 2.2.

Note that Then, by the nonexpansivity of the Euclidean projector, may be bounded as follows:

By adding and subtracting , this expression can be further expanded as follows:

By leveraging the fact that , we have

| (1) |

where Terms 1 – 3 are defined as follows:

| Term 1 | |||

| Term 2 | |||

| and Term 3 |

By Lemma 4 and (A1-1), it follows that

| (2) |

Furthermore, the Lipschitz continuity of in (A1-1) allows for deriving the following bound:

| (3) |

Finally, Term 3 can be bounded by invoking the Cauchy-Schwarz inequality, Lemma 4, (A1-1) and the triangle inequality, we obtain

| (4) |

where the last inequality follows from Combining (1), (2), (3) and (LABEL:eq:stoch_strongly_optim_exp_term3), we get

| (5) |

Recall that satisfies the fixed point relationship which, together with non-expansivity of the Euclidean projector, allows for deriving the following bound on :

By taking conditional expectations and by recalling that , we obtain the following bound:

| (6) |

where . Next, by adding and (6) and by invoking (A2-1), we obtain the following bound.

where , and . From (A2-1), we have that and

Then, by invoking the super-martingale convergence theorem (Lemma 2), we have that as , which implies that and as .

Next we weaken the strong convexity requirement on the function through the following assumption.

Assumption 4 (A1-2).

Furthermore, we make the following assumptions on the steplength sequences employed in the algorithm.

Assumption 5 (A2-2).

Let , and some constant be chosen such that:

-

(i)

and ,

-

(iii)

and ,

-

(iii)

as .

Proceeding as in the previous result, we present a convergence result under these weakened conditions.

Theorem 6 (Almost-sure convergence under convexity of ).

Proof 2.3.

By the nonexpansivity of the Euclidean projector, we have for any that

By adding and subtracting , this expression can be further expanded as follows:

Noting that , we have

| (7) |

where Terms 1 – 3 are defined as follows:

| Term 1 | |||

| Term 2 | |||

| and Term 3 |

By invoking the convexity of in and the gradient inequality (see A1-2), we have that

| Term 1 | |||

where the last inequality follows from the identity From the Lipschitz continuity of in , the right hand side can be bounded as follows:

| (8) |

By the Lipschitz continuity of in (A1-2),

| (9) |

By adding and subtracting , and by invoking the Lipschitz continuity of in (A1-2) and the triangle inequality, we may derive a bound for Term 3 as follows:

| Term 3 | |||

By using the fact that , we have further that

| (10) |

where is chosen to satisfy (A2-2). Combining (7), (2.3), (9) and (10), we obtain the following bound on the conditional error.

| (11) |

From (6), we have that

| (12) |

where . Choose by (A2-2). Note that by assumption . By multiplying the left hand side of (12) by and adding to the left hand side of , we get

| (13) | ||||

Term 4 on the right hand side of (13) can be further expanded as

| (14) |

Combining (13) and (14), we get

We define the following:

Then, we have

By boundedness of and (A2-2), we have that and . So, by Lemma 3 we get that there exists a random variable such that in an almost sure sense as and

By (A2-2), Lemma 2 and (12), we can get that as . Thus, it follows that . Since , we get . Since the set is closed, all accumulation points of lie in . Furthermore, since along a subsequence , by continuity of it follows that has a subsequence converging to some point in , say , which satisfies . That means is some random point in . Moreover, since is convergent for any , the entire sequence converges to some random point in

2.3 Diminishing and constant steplength rate analysis

While the previous section focused on the almost sure convergence of the

prescribed learning and computational schemes, a natural question is

whether one can develop rate statements. We begin with an

examination of the global rate of convergence and show that

rate estimate is derived for an upper bound on the

mean-squared error in the solution when is strongly

convex in and represents the number of steps, consistent

with the result obtained for stochastic approximation

(cf. [40, 45]). In addition, it is seen that when the

function loses strong convexity, an analogous rate estimate is available by

using averaging, akin to an approach first employed in

[42], where longer stepsizes were suggested with

consequent averaging of the obtained iterates.

Proposition 7 (Rate estimates for strongly convex ).

Proof 2.4.

Suppose and . Then, may be bounded as follows by using the non-expansivity of the Euclidean projector:

| (15) |

Note that . By taking expectations on both sides of (15) and by invoking the bounds and , it follows that

| (16) |

But is strongly convex in with constant for every , leading to the following expression:

| (17) |

Combining (16) and (17), we get

| (18) |

Suppose . Since the function is strongly convex, we can use the standard rate estimate (cf. inequality (5.292) in [45]) to get the following

| (19) |

where with . Suppose , allowing us to claim the following:

where . By assuming that , the result follows by observing that

where .

Remark: Notice that here we assume that and are both smooth and strongly convex. A more general framework is that of composite objectives where the objective is a sume of nonsmooth and smooth stochastic components. Lan [35] proposed the accelerated stochastic approximation (AC-SA) algorithm for solving stochastic composite optimization (SCO) problems and proved that it achieves the optimal rate. In related work, Ghadimi and Lan [19, 20] propose a multi-stage AC-SA algorithm, which possesses an optimal rate of convergence for solving strongly convex SCO problems in terms of the dependence on different problem parameters. While this problem class is beyond the current scope, this approach may aid in refinement of the constants in the Proposition 7 in some regimes.

A shortcoming of the previous result is the need for strong convexity of in for every . In our next result, we weaken this requirement and allow for a merely convex , extending the optimal constant stepsize result in [45]. Specifically, given a prescribed number of iterations, say , the optimal “constant stepsize” derives the error minimizing steplength; in other words, for . This is in contrast with the constant stepsize result presented in Proposition 10, where for all . steps. The following Lipschitzian assumption is imposed on the function .

Assumption 6 (A6).

Suppose the following holds in addition to (A1-2).

-

(i)

For every , is Lipschitz continuous in with constant .

Theorem 8 (Rate estimates under convexity of ).

Proof 2.5.

By using the same notation in Proposition 7, we have from (16) that

| (20) |

Note that is convex in for every , allowing us to leverage the gradient inequality.

| (21) |

Combining (20) and (21), we obtain the following:

This allows for constructing the following bounds:

| (22) |

where the second inequality follows from the fact that , the third inequality follows from the boundedness of and Lipschitz continuity of in , and the last inequality follows from (19). As a result, for , we have the following:

| (23) |

Next, we define and . The following holds invoking these definitions:

| (24) |

Next, we consider points given by . By convexity of , we have that and by the convexity of in , we have . From (24) and by noting that and for , we obtain the following for

| (25) |

Suppose for . Then, it follows that

| (26) |

By minimizing the right hand side in , we obtain that

This implies the following bound:

where . Next, we can also claim that for ,

| (27) |

where . Thus, by employing (19), (27) and the Lipschitz continuity of in , we have the required result:

Remark: In effect, in the context of learning and optimization, the averaging approach leads to a complexity bound given loosely by

where are suitably defined. If is available, then , leading to the standard bound of . While it is not surprising that the requirement to learn imposes a degradation, it appears that this degradation is not severe. However, by changing the averaging window, this degradation disappears from a rate standpoint. Specifically, the next result is a corollary of Theorem 8 and uses a modified averaging window, as seen in [40].

Corollary 9 (Rate estimates under convexity of ).

Proof 2.6.

We now present a constant steplength error bound where the steplength is

fixed over the entire algorithm. As mentioned before, this differs from Theorem

8 in that the number of iterations is

not fixed. Constant steplength statements are particularly relevant in

networked regimes where the coordination of changing steplength

sequences across a collection of agents may prove complicated.

Proposition 10 (Constant steplength error bound).

2.4 Regret analysis

In this subsection, we consider the problem of online convex programming in a misspecified regime. In online convex programming problems, a decision-maker sees an infinite sequence of functions where each function is convex in its argument over a closed and convex set . An online convex programming algorithm [50] generates an iterate at each time epoch and a metric of performance is the regret associated with not using an offline algorithm that considers the following problem: If an online convex algorithm generates iterates then the regret is defined as

A desirable feature of an online convex programming algorithm is that it

is characterized by sublinear regret [50].

Often the model prescribed in an online optimization regime can be refined to a setting where the functions are related across time rather than being a sequence of unrelated functions. We consider one particular regime in which the decision-maker sees a sequence of functions given by , Furthermore, neither the values are known to the decision-maker nor is the fact that as . As earlier, we assume that the decision-maker has to furnish and we define the misspecified regret after steps associated with our generated sequence as follows:

Unlike the traditional definition, we consider the departure from and should be contrasted with the standard regret metric given by . For purposes of deriving analytical bounds, we define the following variant of regret as follows:

Next, we provide a rate

of decay of the upper bound of average regret.

Theorem 11 (Regret under convexity of ).

Proof 2.8.

By using the proof in Theorem 1 in [50] (cf. Theorem 21 in Appendix A), we obtain that is bounded as follows:

Next, if with , then we have the following bound on :

Therefore, we obtain the following bound on :

| (30) |

Recall that the difference between the real regret and misspecified regret is given by the following:

or

| (31) |

We proceed to derive bounds for Terms 1 and 2. Term 1 in (31) may be bounded as follows:

where the second and third inequalities follow from the Lipschitz continuity of in (A6) and (19). Through some analysis, the right hand side may be further bounded as follows:

| (32) |

This implies that in (31) converges to zero as . Next, we consider in (31). By the optimality condition for , we have the following expression:

| (33) |

Since is convex in for every , we may leverage the gradient inequality.

| (34) |

Combining (33) and (2.8), we get the following lower bound:

This allows for constructing the following bound on :

| (35) |

where with and the last inequality follows from (19). Note that

| (36) |

Combining (30), (31), (32), and (36), we have that can be bounded as follows:

Furthermore, this implies that the limit superior of the average regret is nonpositive.

Remark: In effect, in the context of learning and optimization, the averaging approach leads to a complexity bound given loosely by

where are suitably defined. If is available, then . Furthermore, by setting and , this leads to the bound of , which is a degradation as the result of learning .

3 Stochastic variational inequality problems with imperfect information

Several shortcomings exist in the optimization based formulation represented by . First, the misspecification arises entirely in the objectives while the constraints are known with certainty. Second, the underlying problem need not be an optimization problem, but could instead be captured by a variational inequality problem. Such problems [15] can capture a range of problems including economic equilibrium problems, traffic equilibrium problems, and convex Nash games. In fact, variational inequality problems can effectively capture optimization problems with misspecified constraints. This motivates the consideration of the misspecified stochastic variational inequality problem where can be learnt through the solution of the following problem:

| () |

where , and and abide by the previous specifications. In the majority of problem settings, but we employ the variational structure to introduce generality. In this section, we extend the results of the previous section to this regime. Specifically, we develop the convergence theory under settings where the variational map is both strongly monotone and merely monotone in for every in Section 3.1 and provide rate statements in Section 3.2.

3.1 Almost-sure convergence

As in Section 2, we propose a set of coupled stochastic approximation schemes for computing and . Given and , the coupled SA schemes are stated next:

Algorithm 2 (Coupled SA schemes for stochastic variational inequality problems).

Step 0. Given and sequences ,

Step 1.

| (Compk) | ||||

| (Learnk) |

where and .

Step 2. If , stop; else , go to Step. 1.

We begin by stating an assumption similar to (A1-1) on the mappings and .

Assumption 7 (A1-3).

Suppose the following hold:

-

(i)

For every , is both strongly monotone and Lipschitz continuous in with constants and , respectively.

-

(ii)

For every , is Lipschitz continuous in with constant .

-

(iii)

is strongly monotone and Lipschitz continuous in with constants and , respectively.

Now, we can leverage the results in Section 2.2 to examine the convergence properties for Algorithm 2.

Proposition 12 (Almost-sure convergence under strong monotonicity of ).

Proof 3.9.

Next, we weaken the rather stringent requirement of strong monotonicity of the map by using an iterative Tikhonov regularization, which can be stated as follows.

Algorithm 3 (Coupled regularized SA schemes for stochastic variational inequality problems).

Step 0. Given and sequences ,

Step 1.

| (Compk) | ||||

| (Learnk) |

where and .

Step 2. If , stop; else , go to Step. 1.

Unlike in standard Tikhonov regularization, such a scheme updates the regularization parameter after every step. Tikhonov regularization and its iterative counterpart has a long history [41] while iterative regularization schemes have seen relatively less study in the context of variational inequality problems (cf. [31, 29]). Of note is the extension to distributed schemes to accommodate monotone Cartesian stochastic variational inequality problems [32]. We employ such techniques in developing single-loop stochastic approximation schemes in the context of learning and optimization. The following assumptions will be made on both the decision variable and parameter.

Assumption 8 (A1-4).

Suppose the following holds in addition to (A1-3 (ii)) and (A1-3 (iii)).

-

(i)

For every , is monotone in and Lipschitz continuous in with constant .

In iterative Tikhonov regularization, one cannot independently choose and ; in fact, these sequences are related and satisfy some collectively imposed requirements.

Assumption 9 (A2-3).

Let , , and some constant be chosen such that:

-

(i)

and ,

-

(ii)

and ,

-

(iii)

as .

-

(iv)

.

Before providing a convergence result for Algorithm 3, we introduce the following results.

Lemma 13.

Let be a mapping that is monotone over , and Lipschitz continuous over with constant . Then, for any and , we have where .

Proof 3.10.

See proof of Theorem 1 in [28].

Lemma 14.

Let be a mapping that is monotone over . Given , let be a solution to VI. Then,

where and is a solution to VI(,).

Proof 3.11.

See Lemma 3 in [28].

The convergence result for Algorithm 3 can be stated as follows.

Theorem 15 (Almost-sure convergence under monotonicity of ).

Proof 3.12.

We have for any that Suppose is a solution to the following fixed-point problem

Then, by the triangle inequality may be bounded as follows:

Term 2 converges to zero by the convergence statement of Tikhonov regularization methods [15]. By using the non-expansivity of the Euclidean projector, can be bounded as follows:

By adding and subtracting , this expression can be further expanded as follows:

Noting that , we have

| (37) |

where

| Term 3 | |||

| Term 4 | |||

| Term 5 |

By Lemma 13 and (A1-4), Term 3 can be further bounded by

| (38) |

By the Lipschitz continuity of in (A1-4), Term 4 can be further bounded by

| (39) |

By the Cauchy-Schwarz inequality, Lemma 13, (A1-4) as well as the fact that , Term 5 can be further bounded by

| (40) |

where is chosen to satisfy (A2-3). Combining (37), (38), (39) and (LABEL:eq:VI_grad_grad_monotone_rand_exp_term3), we get

| (41) |

where .

On the other hand, we have that is the unique solution to VI and

Therefore, by the nonexpansivity of the Euclidean projector, may be bounded as follows:

By taking conditional expectations and by recalling that (A3), we obtain the following:

| (42) |

where , and the second inequality follows from Lemma 4, (A1-4) and (A3). Since by (A2-3) and , and

we have by Lemma 2 that . Choose by (A2-3). Note that by assumption . By multiplying the left hand side of (42) by and adding to the left hand side of , we get

| (43) |

Term 6 on the right hand side of (LABEL:eq:VI_grad_grad_monotone_rand_exp_theta) can be further expanded as

| (44) |

Combining (LABEL:eq:VI_grad_grad_monotone_rand_exp_theta) and (44), we get

Note that . We have

which can be further reduced to

By Lemma 14 and (A2-3), and Therefore, by boundedness of , (A2-3) and Lemma 3, we have that there exists a random variable such that

and Since , we get . This implies .

3.2 Diminishing and constant steplength error analysis

In this section, we estimate the convergence rate of the proposed schemes. Analogous to Section 2.3, we obtain the optimal rate estimate for the upper bound on the expected error in the solution when is strongly monotone in (). In addition, when is merely monotone and the variational inequality problem possesses the minimum principle sufficiency (MPS) property (See Lemma 17 for a definition of the MPS property), a rate estimate is still available by using averaging. If we replace and by and , respectively, in Theorem 7, then we obtain the following:

Theorem 16 (Rate estimate for strongly monotone ).

Next, we weaken the strong monotonicity of , but assume that () satisfies the MPS property, introduced in the following Lemma. Note that this property guarantees weak sharpness of the solution set; this is analogous to weak-sharpness of minima in optimization problems [12].

Lemma 17 (Theorem 4.3 in [38]).

Let be a mapping that is monotone over the compact polyhedral set . Let be the solution set of VI(). If the VI possesses the minimum principle sufficiency (MPS) property, then there exists a positive number such that where . We say that the VI() possesses the MPS property if for every in , where

By leveraging this property, we may estimate the convergence rate by using averaging as in Theorem 8.

Theorem 18 (Rate estimates under monotonicity of ).

Suppose (A1-4) and (A3) hold. Suppose , and for all and . Suppose is a compact polyhedral set, the solution set of VI is nonempty, and is a point in . Suppose VI possesses the MPS property. Let be computed via Algorithm 2. For , we define , and . Suppose for

where , and with . Then there exists a positive number such that for :

where and .

Proof 3.13.

By using the same notation in Theorem 8 except that we replace and by and , respectively, we have from (20) that

| (45) |

By Lemma 17, we have that there exists a positive number such that

| (46) |

where the last inequality follows from the monotonicity of in (). Combining (45) and (46),

| (47) |

Next, we follow the same proof method in Theorem 8. We define and . It follows from (24) and (47) that

| (48) |

Next, we consider points given by . Since is monotone in , we have that is convex, which implies that is convex in . So, we get . It follows from (25) and (48) that for

| (49) |

Suppose for . If we follow the same proof method in Theorem 8, then we can get from (27) and (49) that

Corollary 19 (Rate estimates under monotonicity of ).

Suppose (A1-4) and (A3) hold. Suppose , and for all and . Suppose is a compact polyhedral set, the solution set of VI is nonempty, and is a point in . Suppose VI possesses the MPS property. Let be computed via Algorithm 2. For , we define , and . Suppose for

where , and with . Then there exists a positive number such that

where .

Proof 3.14.

Next, we present a constant steplength error bound.

Proposition 20 (Constant steplength error bound).

Suppose (A3) holds. Suppose and . Suppose and for all . Suppose and . Suppose is a compact polyhedral set, the solution set of VI is nonempty, and is a point in . Suppose VI possesses the MPS property. Let be computed via Algorithm 1.

-

(i)

Suppose (A1-3) holds. Then, the following holds:

-

(ii)

Suppose (A1-4) holds. Then, there exists a positive number such that:

where .

4 Numerical results

In this section, we apply the developed algorithms on a class of misspecified economic dispatch problems described in Section 4.1. In Section 4.2, we apply the proposed schemes for purposes of learning optimal solutions and the misspecified parameters. Note that the simulations were carried out on Tomlab 7.4. The complementarity solver PATH [18] was utilized for obtaining solutions to these problems which subsequently formed the basis for comparison.

4.1 Problem description

We consider a setting where there are firms competing over a -node network. Firm may produce and sell its good at node , where and . We assume that for a given firm , the cost of generating units of power at node is random and is given by , where and are positive parameters, and is a random variable with mean zero for all and . Furthermore, the generation level associated with firm is bounded by its production capacity, which is denoted by . The aggregate sales of all firms at node has to satisfy the demand at node . A given firm can produce at any node and then sell at different nodes, provided that the aggregate production at all nodes matches the aggregate sales at all nodes for each firm. For simplicity, we assume that there is no limit of sales at any node. Then, the resulting problem faced by the grid operator can be stated as follows:

| (51) |

The resulting optimal solution is given by . Suppose firm generates units of power at node . We use to denote the cost associated with firm at node . The operator will solve the following (regularized) problem to estimate and :

| (52) |

The resulting optimal solution is given by . We assume that is distributed as per a uniform distribution and is specified by , while that the noise is distributed as per a uniform distribution and is specified by .

4.2 Results

In this subsection, we employ Algorithm 1 proposed in Section 2 for learning parameters and computing optimal solutions. We will examine the behavior and error bounds of the algorithm.

4.2.1 Behavior of the algorithm

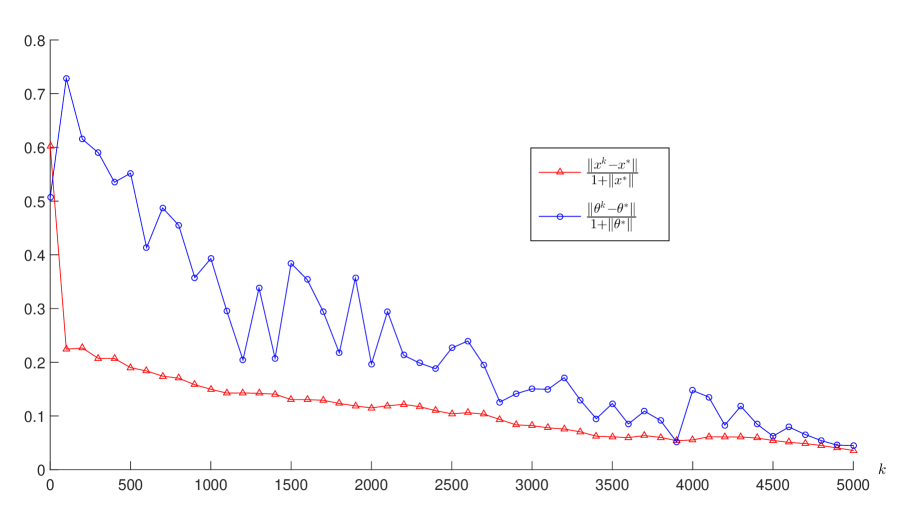

In this part, we consider a special case when and . Suppose, the noise is distributed as per a uniform distribution and is specified by . Suppose the steplength sequences and are chosen according to Proportion 7: and . Figure 1(a) illustrates the scaled error of the learning scheme when the number of steps increases.

4.2.2 Error bounds

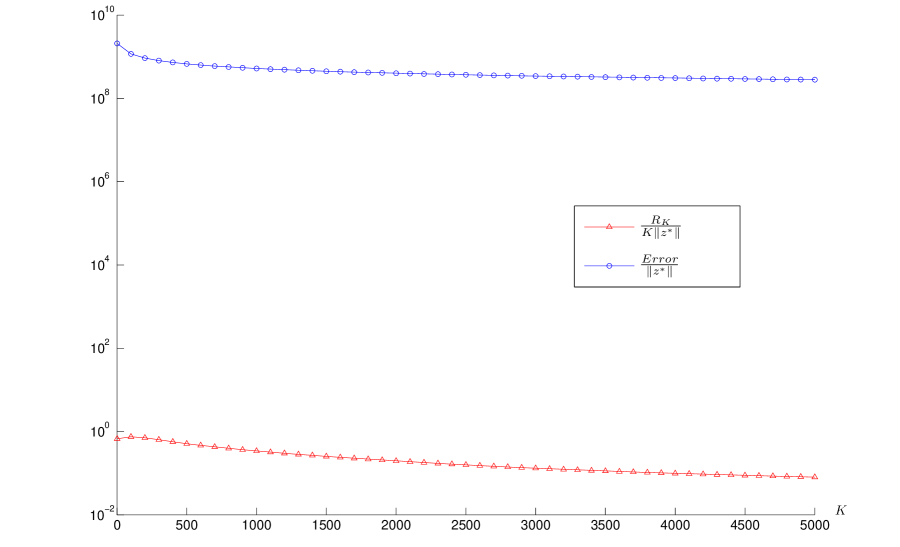

In this part, we examine the errors of the algorithm and compare them with the theoretical error bounds proposed in Section 2. Suppose, the noise is distributed as per a uniform distribution and is specified by .

- (a)

-

(b)

In the merely convex regime, suppose the steplength and the steplength sequence are chosen according to Theorem 8: is chosen by Table 1 (R) and . We use ERR to denote the theoretical error provided in Theorem 8 while denotes . The algorithm was terminated at and Table 1(R) shows the scaled errors of the learning scheme.

-

(c)

Suppose the steplength sequences and are chosen according to Theorem 11: and . We employ ERR to denote the theoretical error provided in Theorem 11 while denotes . The algorithm was terminated after iterations. Figure 1(b) illustrates the scaled regret and scaled theoretical error of the learning scheme when the number of steps increases (). Table 2 shows the scaled theoretical error of the learning scheme for different chosen with when . We see that when changes, error bounds change marginally primarily because the last term in Theorem 11 dominates the bound.

| N | W | ||||

|---|---|---|---|---|---|

| 10 | 2 | 7.3 | 9.2 | 4.8 | 3.7 |

| 10 | 4 | 3.7 | 2.1 | 4.9 | 3.1 |

| 10 | 6 | 3.8 | 7.8 | 4.7 | 8.3 |

| 10 | 8 | 1.7 | 9.1 | 4.8 | 8.5 |

| 10 | 10 | 2.4 | 1.2 | 4.3 | 8.6 |

| N | W | |||

|---|---|---|---|---|

| 10 | 2 | 1.9 | 2.5 | 72 |

| 10 | 4 | 6.5 | 1.1 | 93 |

| 10 | 6 | 2.7 | 2.6 | 127 |

| 10 | 8 | 1.3 | 1.7 | 131 |

| 10 | 10 | 1.4 | 2.6 | 133 |

| 0.5 | 4.8 | 3.1 |

| 0.6 | 3.3 | 3.1 |

| 0.7 | 2.3 | 3.1 |

| 0.8 | 1.8 | 3.1 |

| 0.9 | 1.5 | 3.1 |

5 Concluding remarks

Traditionally, much of the field of optimization has been defined by problems in which the functions and sets are known to the decision-maker. However, as problems grow in their reliance on data, such knowledge cannot be taken for granted. We consider one such instance of such problems where functions may be misspecified and the associated vector may be learnt through the parallel solution of a suitably defined problem. It is worth emphasizing the problem in the full space of learning and optimization variables is a challenging (non-monotone) stochastic variational problem for which no first-order methods are currently available. Yet, by leveraging the structure of the problem, we show that such problems can indeed be efficiently solved.

We consider a problem of solving a stochastic optimization problem in which the objective is parameterized by a vector that can be learnt by solving a suitably defined learning problem, captured by a stochastic optimization problem. In both strongly convex and merely convex regimes, we develop a set of coupled stochastic approximation schemes which produces a sequence of iterates that are shown to converge to the solution and unknown parameter in an almost sure sense. Additionally, we provide rate estimates for the prescribed schemes in both strongly convex and convex regimes. Through an analysis of the rate of convergence under a diminishing steplength setting, it is seen that the optimal rate of convergence is observed in strongly convex problems while in convex regimes, we see a degradation introduced by learning from to . This degradation is seen to disappear if the averaging window is modified appropriately. Similar rate statements are also provided in a constant steplength regime. In fact, we may also cast this problem as an online decision-making problem where a decision-maker sees a collection of misspecified functions. In a stochastic regime, we observe that an upper bound on the average regret can be shown to decay at a rate no worse than for a suitably chosen steplength.

Unfortunately, the optimization-based model cannot accommodate settings where there is misspecification in the constraints or, more generally, if the associated decision-making problem is an equilibrium problem. Motivated by this gap, we consider a misspecified stochastic variational inequality problem and propose analogous stochastic approximation schemes for computation and learning. To resolve the challenge associated with merely monotone maps, we employ (Tikhonov) regularized counterparts for which almost-sure convergence statements can be provided. Additionally, we provide rate statements for constant and diminishing steplength regimes, of which the latter requires imposing a suitable weak-sharpness assumption on the original problem. Again, it is seen that while the schemes display the optimal rate of convergence under strongly monotone regimes, a degradation in the rate is seen in the monotone regime.

References

- [1] E. Adida and G. Perakis, Dynamic pricing and inventory control: robust vs. stochastic uncertainty models—a computational study, Ann. Oper. Res., 181 (2010), pp. 125–157.

- [2] , Dynamic pricing and inventory control: uncertainty and competition, Oper. Res., 58 (2010), pp. 289–302.

- [3] R. Aguech, E. Moulines, and P. Priouret, On a perturbation approach for the analysis of stochastic tracking algorithms., SIAM J. Control and Optimization, 39 (2000), pp. 872–899.

- [4] S. Arimoto, S. Kawamura, and F. Miyazaki, Formation of high-speed motion pattern of a mechanical arm by trial, J. of Robot. Syst., 1 (1984), pp. 123–140.

- [5] K. J. Astrom and B. Wittenmark, Adaptive Control, Addison-Wesley Longman Publishing Co., Inc., Boston, MA, USA, 2nd ed., 1994.

- [6] P. Auer, N. Cesa-Bianchi, and P. Fischer, Finite-time analysis of the multiarmed bandit problem, Machine Learning, 47 (2002), pp. 235–256.

- [7] A. Ben-Tal, L. El Ghaoui, and A.S. Nemirovski, Robust Optimization, Princeton Series in Applied Mathematics, Princeton University Press, October 2009.

- [8] D. Bertsimas, D. B. Brown, and C. Caramanis, Theory and applications of robust optimization, SIAM Rev., 53 (2011), pp. 464–501.

- [9] D. Bertsimas, V. Gupta, and N. Kallus, Data-driven robust optimization, arXiv : 1401.0212.

- [10] D. Bertsimas and D. Pachamanova, Robust multiperiod portfolio management in the presence of transaction costs, Comput. Oper. Res., 35 (2008), pp. 3–17.

- [11] D. Bertsimas and M. Sim, The price of robustness, Oper. Res., 52 (2004), pp. 35–53.

- [12] J. V. Burke and M. C. Ferris, Weak sharp minima in mathematical programming, SIAM Journal on Control and Optimization, 31 (1993), pp. 1340–1359.

- [13] Y. Chen, G. Lan, and Y. Ouyang, Accelerated schemes for a class of variational inequalities, tech. report, Department of Industrial and Systems Engineering, University of Florida, initially drafted on March 17, 2014, submitted to Mathematical Programming, Series B, August 19, 2014, 2014.

- [14] W. L. Cooper, T. Homem-de Mello, and A. J. Kleywegt, Models of the spiral-down effect in revenue management, Oper. Res., 54 (2006), pp. 968–987.

- [15] F. Facchinei and J. S. Pang, Finite-dimensional variational inequalities and complementarity problems. Vol. I, Springer Series in Operations Research, Springer-Verlag, New York, 2003.

- [16] Francisco Facchinei and Jong-Shi Pang, Finite-dimensional variational inequalities and complementarity problems. Vol. I, Springer Series in Operations Research, Springer-Verlag, New York, 2003.

- [17] F. Facchinei and J. S. Pang, Finite-dimensional variational inequalities and complementarity problems. Vol. II, Springer Series in Operations Research, Springer-Verlag, New York, 2003.

- [18] M. C. Ferris and T. S. Munson, Complementarity problems in GAMS and the PATH solver, Journal of Economic Dynamics and Control, 24 (2000), pp. 165–188.

- [19] Saeed Ghadimi and Guanghui Lan, Optimal stochastic approximation algorithms for strongly convex stochastic composite optimization I: A generic algorithmic framework, SIAM Journal on Optimization, 22 (2012), pp. 1469–1492.

- [20] , Optimal stochastic approximation algorithms for strongly convex stochastic composite optimization, II: shrinking procedures and optimal algorithms, SIAM Journal on Optimization, 23 (2013), pp. 2061–2089.

- [21] J. C. Gittins, Multi-armed bandit allocation indices, Wiley-Interscience Series in Systems and Optimization, Chichester: John Wiley & Sons, Ltd., 1989.

- [22] D. Goldfarb and G. Iyengar, Robust portfolio selection problems, Math. Oper. Res., 28 (2003), pp. 1–38.

- [23] H. Hijazi, P. Bonami, and A. Ouorou, Robust delay-constrained routing in telecommunications, Ann. Oper. Res., 206 (2013), pp. 163–181.

- [24] H. Jiang and U. V. Shanbhag, On the solution of stochastic optimization problems in imperfect information regimes, in Winter Simulations Conference: Simulation Making Decisions in a Complex World, WSC 2013, Washington, DC, USA, December 8-11, 2013, IEEE, 2013, pp. 821–832.

- [25] H. Jiang and H. Xu, Stochastic approximation approaches to the stochastic variational inequality problem, IEEE Transactions on Automatic Control, 53 (2008), pp. 1462–1475.

- [26] R. Jiang, M. Zhang, G. Li, and Y. Guan, Two-stage network constrained robust unit commitment problem, European J. Oper. Res., 234 (2014), pp. 751–762.

- [27] A. Juditsky, A. Nemirovski, and C. Tauvel, Solving variational inequalities with stochastic mirror-prox algorithm, Stoch. Syst., 1 (2011), pp. 17–58.

- [28] A. Kannan and U. V. Shanbhag, Distributed iterative regularization algorithms for monotone Nash games, Proceedings of the IEEE Conference on Decision and Control (CDC), (2010), pp. 1963–1968.

- [29] , Distributed computation of equilibria in monotone Nash games via iterative regularization techniques, SIAM Journal of Optimization, 22 (2012), pp. 1177–1205.

- [30] M. N. Katehakis and Jr. A. F. Veinott, The multi-armed bandit problem: Decomposition and computation, Mathematics of Operations Research, 12 (1987), pp. 262–268.

- [31] I. V. Konnov, Equilibrium models and variational inequalities, vol. 210 of Mathematics in Science and Engineering, Elsevier B. V., Amsterdam, 2007.

- [32] J. Koshal, A. Nedic, and U. V. Shanbhag, Regularized iterative stochastic approximation methods for stochastic variational inequality problems, IEEE Trans. Automat. Contr., 58 (2013), pp. 594–609.

- [33] A. M. C. A. Koster, M. Kutschka, and C. Raack, Robust network design: formulations, valid inequalities, and computations, Networks, 61 (2013), pp. 128–149.

- [34] H. Kushner, Stochastic approximation: a survey, Wiley Interdisciplinary Reviews: Computational Statistics, 2 (2010), pp. 87–96.

- [35] Guanghui Lan, An optimal method for stochastic composite optimization, Math. Program., 133 (2012), pp. 365–397.

- [36] C. Li and S. Liu, A robust optimization approach to reduce the bullwhip effect of supply chains with vendor order placement lead time delays in an uncertain environment, Appl. Math. Model., 37 (2013), pp. 707–718.

- [37] L. Ljung and S. Gunnarsson, Adaptation and tracking in system identification - a survey, Automatica, 26 (1990), pp. 7–21.

- [38] P. Marcotte and D. Zhu, Weak sharp solutions of variational inequalities, SIAM J. Optim., 9 (1999), pp. 179–189.

- [39] K. L. Moore, Iterative Learning Control for Deterministic Systems, Springer-Verlag Series on Advances in Industrial Control, Springer-Verlag, London, 1993.

- [40] A. Nemirovski, A. Juditsky, G. Lan, and A. Shapiro, Robust stochastic approximation approach to stochastic programming, SIAM J. on Optimization, 19 (2009), pp. 1574–1609.

- [41] B. T. Polyak, Introduction to optimization, Optimization Software, Inc., New York, 1987.

- [42] B. T. Polyak and A. B. Juditsky, Acceleration of stochastic approximation by averaging, SIAM J. Control Optim., 30 (1992), pp. 838–855.

- [43] J. Wang R. Jiang and Y. Guan, Robust unit commitment with wind power and pumped storage hydro, IEEE Transactions on Power Systems (to appear).

- [44] C.-T See and M. Sim, Robust approximation to multiperiod inventory management, Oper. Res., 58 (2010), pp. 583–594. Supplementary data available online.

- [45] A. Shapiro, D. Dentcheva, and A. Ruszczyński, Lectures on stochastic programming, vol. 9 of MPS/SIAM Series on Optimization, SIAM, Philadelphia, PA, 2009. Modeling and theory.

- [46] M. Uchiyama, Formation of high-speed motion pattern of a mechanical arm by trial, Trans. Soc. Instrum. Control Engineering (Japan), 14 (1978), pp. 706–712.

- [47] F. Yousefian, A Nedić, and U.V. Shanbhag, A regularized smoothing stochastic approximation (RSSA) algorithm for stochastic variational inequality problems, in Proceedings of the Winter Simulation Conference (WSC), Dec 2013, pp. 933–944.

- [48] F. Yousefian, A Nedić, and U. V. Shanbhag, Optimal robust smoothing extragradient algorithms for stochastic variational inequality problems, 2014. Proceedings of the IEEE Conference on Decision and Control (CDC) (see http://arxiv.org/abs/1403.5591).

- [49] C. Zhao and Y. Guan, Unified stochastic and robust unit commitment, IEEE Transactions on Power Systems (to appear).

- [50] M. Zinkevich, Online convex programming and generalized infinitesimal gradient ascent, in ICML, Tom Fawcett and Nina Mishra, eds., AAAI Press, 2003, pp. 928–936.

Appendix A Theorem 1 in [50]

Definition 1.

Given an algorithm , a convex set and an infinite sequence where each is a convex function, if are the vectors selected by , then the cost of until time is defined as . The cost of a static feasible solution until time is defined as The regret of algorithm until time is defined as

The Greedy Projection algorithm proposed in [50] is as follows.

Algorithm 4 (Greedy Projection).

Select an arbitrary and a sequence of learning rates . In time step , after receiving a cost function, select the next vector according to:

Then, we have the following result.

Theorem 21 (Theorem 1 in [50]).

If , the regret of the Greedy Projection algorithm is:

where and .

Proof sketch: The regret of the Greedy Projection algorithm can be bounded as follows:

The result can be immediately obtained when .