Partial correlation analysis:

Applications for financial markets

Abstract

The presence of significant cross-correlations between the synchronous time evolution of a pair of equity returns is a well-known empirical fact. The Pearson correlation is commonly used to indicate the level of similarity in the price changes for a given pair of stocks, but it does not measure whether other stocks influence the relationship between them. To explore the influence of a third stock on the relationship between two stocks, we use a partial correlation measurement to determine the underlying relationships between financial assets. Building on previous work, we present a statistically robust approach to extract the underlying relationships between stocks from four different financial markets: the United States, the United Kingdom, Japan, and India. This methodology provides new insights into financial market dynamics and uncovers implicit influences in play between stocks. To demonstrate the capabilities of this methodology, we (i) quantify the influence of different companies and, by studying market similarity across time, present new insights into market structure and market stability, and (ii) we present a practical application, which provides information on the how a company is influenced by different economic sectors, and how the sectors interact with each other. These examples demonstrate the effectiveness of this methodology in uncovering information valuable for a range of individuals, including not only investors and traders but also regulators and policy makers.

{classcode}G10, C10, D40

keywords:

Financial markets; Partial correlations; Influence; Risk1 Introduction

Understanding the complex nature of financial markets remains a great challenge, especially in light of the most recent crisis of 2008. Recent studies have investigated large data sets of financial markets, and have analyzed and modeled the static and dynamic behavior of this very complex system (Fama, 1965; Lo et al., 1997; Lo and Craig MacKinlay, 1990; Brock et al., 2009; Cont and Bouchaud, 2000; Eisler and Kertesz, 2006; Lux et al., 1999; Bouchaud and Potters, 2003; Voit, 2005; Sinha et al., 2010; Abergel et al., 2011; Takayasu, 2006; Sornette, 2004), suggesting that financial markets exhibit systemic shifts and display non-equilibrium properties.

One prominent feature in financial markets is the presence of an observed correlation (positive or negative) between the price movements of different financial assets. The presence of a high degree of cross-correlation between the synchronous time evolution of a set of equity returns is a well known empirical fact (Markowitz, 1952; Elton et al., 2009; Campbell et al., 1997). The Pearson correlation coefficient (Pearson, 1895) provides information about the similarity in the price change behavior of a given pair of stocks. Much effort has been devoted to extracting meaningful information from the observed correlations in order to gain insights into the underlying structure and dynamics of financial markets (Embrechts et al., 2002; Morck et al., 2000; Campbell et al., 2008; Krishan et al., 2009; Aste et al., 2010; Campbell et al., 2008; Cizeau et al., 2001; Laloux et al., 2000, 1999; Plerou et al., 1999; Podobnik et al., 2009; Pollet and Wilson, 2010; Tumminello et al., 2010; Huang et al., 2013; Forbes and Rigobon, 2002).

A large body of work has dealt with the systemic risks introduced into a financial system when there is a co-movement of financial assets. To understand how risks propagate through the entire system, many studies have focused on understanding the synchronization in financial markets that is especially pronounced during periods of crisis (Haldane and May, 2011; Bisias et al., 2012). Recent advancements include the CoVaR methodology (Adrian and Brunnermeier, 2011), and and Granger causality analysis (Granger, 1969; Billio et al., 2012). These measures focus on the relationship of one variable on a second variable, for a given time period. Finally, much work has been focused on the issue of conditional correlation (Engle, 2002) and event conditional correlation (Maugis, 2014), and its applications in financial markets. However, a missing dimension of these methodologies is the investigation of many-body interaction between financial assets.

Despite the meaningful information provided by investigating the correlation coefficient, it lacks the capacity to provide information about whether a different stock(s) eventually controls the observed relationship between other stocks. To overcome this issue we introduce the use of the partial correlation coefficient (Baba et al., 2004), and its applications.

A partial (or residual) correlation measures how much a a given variable, say , affects the correlations between another pair of variables, say and . Thus, in this pair, the partial correlation value indicates the correlation remaining between and after the correlation between and and between and have been subtracted. Defined in this way, the difference between the correlations and the partial correlations provides a measure of the influence of variable on the correlation . Therefore, we define the influence of variable on variable , or the dependency of variable on variable , as , to be the sum of the influence of variable on the correlations of variable with all other variables. This methodology has originally been introduced for the study of financial data (Kenett et al., 2010, 2012a, 2012b; Maugis, 2014), it has been extended and applied to other systems, such as the immune system (Madi et al., 2011), and semantic networks (Kenett et al., 2011). Causality, and more specifically the nature of the correlation relationships between different stocks, is a critical issue to unveil. The main goal of our study is to understand the underlying mechanisms of influence that are present in financial markets.

Previous work has focused on how variable affects variable , by averaging over all pairs, thus quantifying how variable affects the average correlation of with all other variables. Although this has provided important information that has been both investigated and statistically validated, our goal here is to present a more general and robust method to statistically pick the meaningful links without first averaging over all pairs. Unlike the previous work in which the average influence of on the correlation of with all others was calculated, and then statistically validated, here we first filter for validated links, and then average the influence. In order to achieve this we expand the original methodology and use statistical validation methods to filter the significant links. This statistically validated selection process reveals significant influence relationships between different financial assets. This new methodology allows us to quantify the influence different assets (e.g., economic sectors, other markets, or macro-economic factors) have on a given asset. The information generated by our methodology is applicable to such areas as risk management, portfolio optimization, and financial contagion, and is valuable to both policy makers and practitioners.

The rest of this paper is organized as follows: In Section 2 we introduce the partial correlation approach to quantify influence between financial assets. We present the new extensions of the methodology, which allows the selection of statistically significant influence links between different assets. We further discuss the empirical data analyzed in this study. In Section’s 3 and 4 we present two possible applications of the methodology. In Section 3 we focus on how the methodology provides new insights into market structure and its stability across time, while in Section 4 we present a practical application, which provides information on the how a company is influenced by different economic sectors, and how the sectors interact with each other. Finally, in Section 5 we discuss our results and provide additional insights into possible applications of this methodology.

2 Quantifying underlying relationships between financial assets

The aim of this paper is to present a new methodology that sheds new light on the underlying relationships between financial assets. Building on previous work (Kenett et al. (2010)), we present a robust and statistically significant approach to extracting the hidden underlying relationships. As such, the presented methodology provides new insights into the underlying mechanisms of financial markets.

2.1 Data

For the analysis reported in this paper we use daily adjusted closing stock price time series from four different markets, data provided by the Thomson Reuters Datastream. The markets investigated are the U.S., the U.K., Japan, and India, (see Table 1 for details, also Kenett et al. (2012b)). We only consider stocks that are active from January 2000 until December 2010. Volume data was used to identify and eliminate illiquid stocks from the sample. Table 1 presents the number of stocks remaining after filtering out the stocks that had no price movement for more than 6 percent of the 2700 trading days.

Summary of data sample Market Stocks used Index used # before # filtered U.S. S&P 500 S&P 500 500 403 U.K. FTSE 350 FTSE 350 356 116 Japan Nikkei 500 Nikkei 500 500 315 India BSE 200 BSE 100 193 126

2.2 Stock raw and partial correlation

To study the similarity between stock price changes, we calculate the time series of the daily log return, given by

| (1) |

where is the daily adjusted closing price of stock at day . The stock raw correlations are calculated using the Pearson correlation coefficient (Pearson, 1895)

| (2) |

where represents average over all days, and denotes the standard deviation.

However, in some cases, a strong correlation not necessarily means strong direct relation between two variables. For example, two stocks in the same market can be influenced by common macroeconomic factors and investor psychological factors. To study the direct correlation of the performance of these two stocks, we need to remove the common driving factors, which are represented by the market index. Partial correlation quantifies the correlation between two variables, e.g. stocks returns, when conditioned on one or several other variables (Baba et al., 2004; Shapira et al., 2009; Kenett et al., 2010). Specifically, let , be two stock return time series and be the index. The partial correlation, , between variables and conditioned on variable is the Pearson correlation coefficient between the residuals of and that are uncorrelated with . To obtain these residuals of and , they are both regressed on . The partial correlation coefficient can be expressed in terms of the Pearson correlation coefficients as

| (3) |

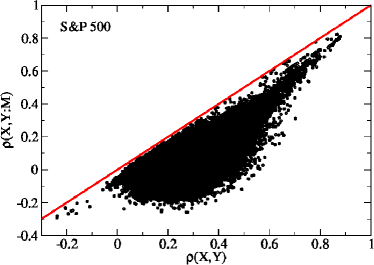

In figure 1 (a), we plot the correlation and partial correlation (using the index as the conditioning variable) between stocks that belong to the S&P 500 index. The figure shows that all points are below the diagonal straight line, which means the influence from the index to the correlation between any pair of stocks is always positive. Furthermore, when two stocks and both have business relation with a third common stock , their prices can be both affected by the performance of the third stock, thus showing similar price movements even after removing the index. By removing the influence from the third company, we can see the importance of the role that the third stock acts in the correlation of two stocks. Partial correlation coefficient between and conditioned on both and is

| (4) |

In order to quantify the influence of stock on the pair of and , we focus on the Influence quantity

| (5) |

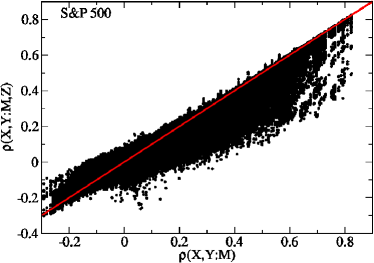

This quantity is large when a significant fraction of the partial correlation can be explained in terms of . In previous research, Kenett et al. defined this quantity by , which holds for general cases (Kenett et al., 2010). However, for the stock market case specifically, the fraction of that can be explained by contains two parts, index influence and stocks influence, because stock contains information of the index. Usually, the influence from the index is prevailing and overwhelms the influence from an individual stocks. For example, when and are competitor and cooperator respectively to stock , performances of and should have negative correlation because of . In this case, the influence from to the correlation between stocks and should be negative. However, because of the dominant correlation between these two stocks and the index, the is still positive. Thus, we suggest to remove the influence of the market before studying the influence of a stock on a pair of stocks. In the scatter plot of the partial correlation conditioned on index v.s. the partial correlation conditioned on both index and an individual stock (figure 1 (b)), the points distribute at both sides of the diagonal line, meaning a significant fraction of is negative.

The average influence of stock on the correlations between stock and all the other stocks in the system is defined as

| (6) |

It is important to note that approximates the net influence from stock to stock , excluding the influence from the index.

2.3 Test of statistical significance

In a system of size , there exists partial correlation interactions, , when all information is considered. To simplify the description of the system, the non-trivial interactions with certain significance level are selected. To decide the significance of partial correlation, we provide two methods: 1) Fisher’s transformation based approach; and 2) empirical based approach.

2.3.1 Fisher transformation statistical significance test

We first introduce the Fisher’s transformation method. According to ref. (Fisher, 1915), when and follow a bivariate normal distribution and , pairs to form the correlation are independent for , a transformation of the Pearson correlation

| (7) |

approximately follows normal distribution , where is the population correlation coefficient and is the sample size. The Fisher transformation holds when is not too large and is not too small. Furthermore, the Fisher’s z-transform of the partial correlation coefficients approximately follows (Fisher, 1924)

| (8) |

which leads to

| (9) |

When is significantly different from , is significantly different from zero. Thus the Student’s t-test is used to determine if and are different. Since is large, the degree of freedom is also large, where the t-test is approximately the same as the Z-test (Chou, 1975). In the next section, we propose a complementary empirical statistical significance test. The empirical approach overlaps with the Fisher transformation approach, and is faster and simpler to evaluate. For real finite size data the two are interchangeable, and the empirical approach is simpler to implement. Thus, after introducing the empirical approach below, we will make use of it throughout the remainder of the paper.

2.3.2 Empirical statistical significance test

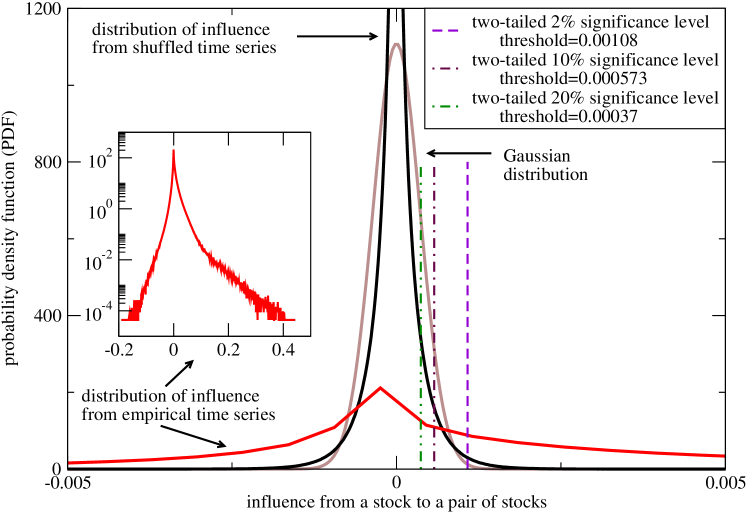

Next, we introduce the empirical time series shuffling statistical significance method. For each time series that we study, we shuffle the sequences of the returns, which destroys any correlations among these time series. The influences calculated from these time series should also be not different than zero. We shuffle the return time series of each stock by randomly rearranging the sequences of the returns. The shuffling process destroys correlations between each pairs of stocks returns, and between stock returns and benchmark return, i.e. and should be zero, which leads to equal to zero. By plotting the distribution of , we can find the thresholds of different significant levels for . In fig. 2, we shuffle the return time series of 403 S&P500 stocks, and the index, and plot the distribution of (solid black curve). As a comparison, we plot the Gaussian distribution with same average and standard deviation value in brown color. From the comparison, it is possible to observe that the empirical distribution of of has fat tails, and significantly deviates from the case of a gaussian distribution observed for random or shuffled data. The dashed lines represent the positions of one-tailed , and significance levels or two-tailed , and significance levels. We suggest to make use of the two-tailed test, due to the fact that the significant negative influence is also important. The red curve in fig. 2 presents the distribution of empirical . For the case of the S&P500 companies example presented in fig. 2, significance level of corresponds to a (Equation 9) ; confidence level of corresponds to ; and confidence level of corresponds to (see Table 2).

Summary of two-tail significance thresholds Significance level Threshold 1% 0.00152 2% 0.00108 5% 0.00081 10% 0.00057 20% 0.00037

As discussed above, while the two methods are interchangeable in respect to the resulting significance levels, there are additional benefits to using the empirical approach. The empirical shuffling method conserves the distribution of returns without requiring ad-hoc assumptions on the underlying distribution of the data. Furthermore, the empirical approach can also be expanded to meet stricter requirements. For example, if the short term time series structure is required to be conserved, the whole time series can be divided into segments with a given length and we can than shuffle the segments without changing the sequence of time series within the segments.

The empirical statistical significance test allows a selection of significant influence relationships between the investigated financial assets. In previous work (Kenett et al. (2010)), this was achieved by using different network based approaches, which than further allowed to investigate the nature of these relationships. Below we propose two new applications of this methodology, using the empirically statistically significant values of . The significance level used through out the paper is the , corresponding to two-tailed 2%.

3 Market structure and its stability

High correlation between two stocks at a given time do not necessarily guarantee high correlation in the future, because the behavior of stocks in financial markets evolve. In certain markets, companies change their strategies faster than in the other markets, which can be uncovered by the partial correlation analysis of the behavior of their stocks. If the companies tend to keep their past strategies, then the level of partial correlation between two companies’ stocks tends to be stable. While in markets where companies switch their strategies more quickly, two companies which had similar behavior in the previous year might have quite different behavior in the next year. In such markets, partial correlation between stocks should be more volatile.

We apply the partial correlation influence analysis to study the stability of the market structure. Specifically, we define the average influence of stock on all the other stocks in the market as

| (10) |

where is the average over all stocks. We rank the stocks by their values, which we consider as a representation of the structure of the market. By dividing the 11 year period into 44 quarterly periods, we can compare similarity of the market structures (ranking of stocks) in different years. Kendall rank correlation coefficient (Kendall, 1938) is applied to measure the similarity of the orderings for different periods. Let be a set of rankings of the variables for different periods and respectively. Any pair of observations and are said to be concordant if both and or if both and . Otherwise, they are said to be discordant. The Kendall coefficient is defined as

| (11) |

where if two rankings are the same, is one, if two rankings are independent, is zero, and if two rankings are discordant, equals minus one.

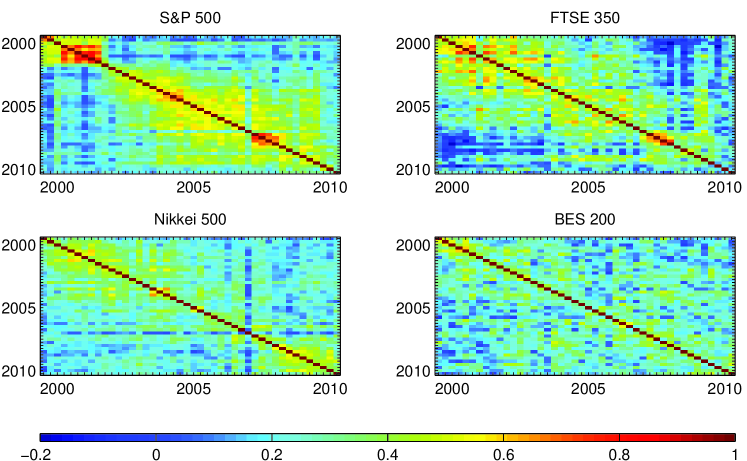

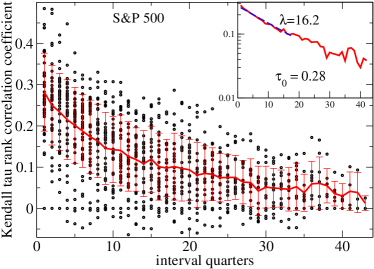

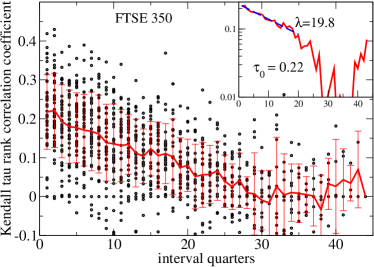

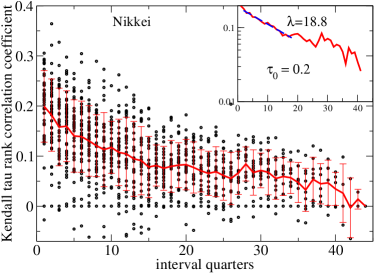

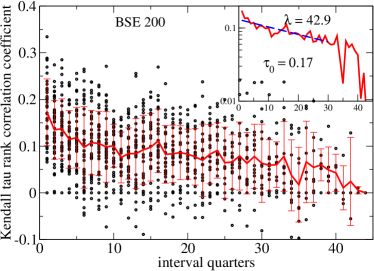

In figure 3, we present the Kendall coefficient for each different quarter pairs for the four investigated markets. Generally speaking, each market shows that the longer the time interval the smaller the rank correlation coefficient, meaning lower similarity between the market structures for the two quarters which are compared. Comparing the rank correlations for the four markets, we find that S&P 500, FTSE 350 and Nikkei 500 stocks show strong market stability patterns, while Indian BES 200 stocks almost do not demonstrate any stable patterns. This can be understood by considering that developed markets tend to keep their market structure longer than fast developing markets. Furthermore, it is possible to observe that for the US market there were structural changes in the market following the “dot com”crisis of 2000 and the “credit crunch”crisis of 2008. These can be identified in figure 3 by the red rectangle in the upper left corner for the former (Q4 of 2000 till Q4 of 2001), and the red rectangle in the bottom right corner for the latter (Q4 of 2007 till Q4 of 2008). These rectangles present a strong similarity in the structure during the two crises, followed by consecutive quarters with low values of thee rank correlation, representing the change in structure. Studying the other markets, it is also possible to observe the structural changes resulting from the 2008 financial crisis in the UK, but not in the structure of Japan or India.

To further quantitatively study the market stability, we plot the correlation coefficient of two rankings against the time interval of these two rankings (fig. 4). By averaging the correlation coefficients for each time interval, we can study how correlation coefficients decay as time evolves. We find the decay of the rank correlation coefficients follow an approximate exponential process, , as shown in the insets in fig. 4. Parameter describes the consistency of the rankings between two consecutive quarters. The larger is, the more consistent two consecutive ranking are. The parameter describes the characteristic time after which the correlation coefficient decays. Larger values mean longer persistence period, and thus describe the change in influence ranking across time. These two parameters together describes the stability of the markets. For the investigated markets, we obtain the following values: US - ; UK - ; Japan - ; and India - . As can also be observed in figure 3, has the largest value for the S&P500 case, and smalls value for the BES200 case; however, the persistence in India is largest (as represented by the values of ). We observe that the results for the Indian market differ from the other three markets. This is possibly related to the differences observed between developing and developed markets.

Put together, these analyses provide new insights into the dynamics of financial markets. Using the and parameters, can help in monitoring structural changes in the market, and their persistence. Thus, this methodology presents a unique tool for regulators and policy makers to monitor the stability and robustness of financial markets.

4 Quantifying the influence of economic sectors

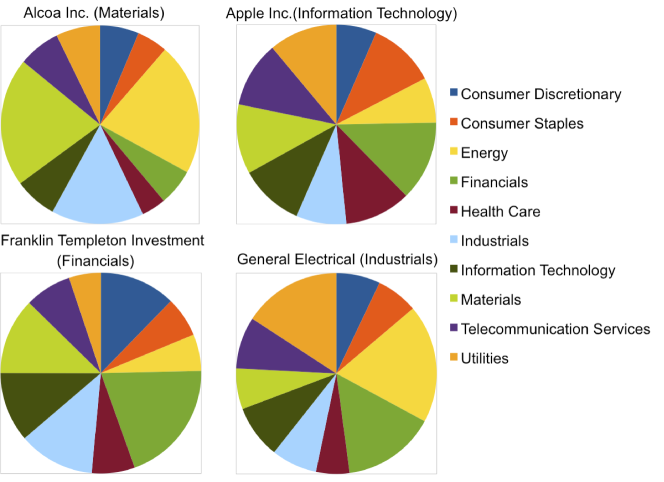

As our society becomes more and more integrated, production activities from different industries depend upon and influence each other. Categorizing a company into only one industrial sector can not reflect its whole performance and associated risk. Many listed companies in the stock market belong to conglomerates, conducting their business in different industry sectors, hence these companies’ performance will naturally be influenced by multiple industries. Even if a company only conducts its business in one sector, its performance can still be influence by other sectors because of the division of labor in modern society. For example, Alcoa Inc. as the world’s third largest producer of aluminum is listed in the materials sector in NYSE. However, the production of Alcoa Inc. requires dedicated supply of energy, e.g. Alcoa accounts for 15% of State of Victoria’s annual electricity consumption in Australia. Thus their performance is also heavily influenced by and contributes to the performance of the energy sector. In this section, we present an application of the partial correlation methodology to study the multiple-sector influence on stocks. We use the sector classification from the Global Industry Classification Standard (GICS).

To study the influence on a stock from different sectors, we first calculate the influence (eq. 6) from all other stocks . The analysis in this section is performed for the entire investigated time period. Next we calculate the average influence by sector, in which we use the sector categorization information of other stocks, as follows

| (12) |

where represents the investigated stock, represents a given sector, is the number of stocks in sector and represents the stocks in sector . The average influence reflects the level of influence that stock receives from sector . After we normalize the average influence, we can attribute stock ’s performance to sectors’ performances with coefficients

| (13) |

In figure 5, we present an example of four typical stocks to show the pie picture of . We can see from the figure that in the case of Alcoa Inc., we observe significant influence from the energy, materials and industrials sector. In the case of Franklin Templeton Investments, we find that the largest influence is from the financials sector. In the case of GE, we find that the main influence stems from the materials, utilities, and financial sector. Finally, studying the example of Apple, we find that there is a more homogeneous division of the influence between the different sectors. This could possibly indicate that out of these 4 companies, Apple is the most diverse in its activities, being influenced almost uniformly by different sectors of the economy.

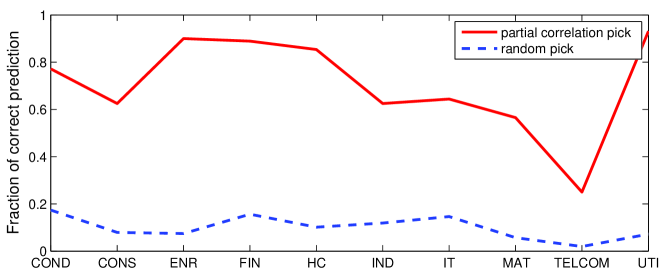

Finally, we perform a validation test on the the partial correlation analysis results, investigating whether the result of multi-sector influence on stocks is plausible. To this end, we first rank all the stocks in the S&P500 dataset by their fraction of influence () from the financials sector. We then investigate what are the economic sectors influencing these stocks, according to the rank. We find that the top stocks in the ranking according to our partial correlation analysis are dominantly classified into the financials sector. We repeat this analysis for all other economic sectors. Indeed, all other sectors show that our analysis is in agreement with the GICS sector classification. To quantitatively show this agreement, we calculate the correct prediction rate. According to the GICS, we find the total numbers of stocks () in all sectors. From the ranking of stocks according to the influence from a given sector, we select the top stocks. We then calculate the fraction of these top stocks that are classified by GICS into that certain sector as the correct prediction rate. If the partial correlation analysis prediction is in total agreement with the formal classification, then this correct prediction rate should be 1. If the prediction corresponds to the case of random picking, this correct prediction rate should be , where is the total number of stocks. In figure 6(c), we show that the partial correlation analysis of sector keeps a high correct prediction rate for all sectors, except the telecommunications sector, which could be related to the small number of telecommunication stocks that are part of the S&P500 index. An alternative interpretation to these results is that the financials and energy sectors are both highly cohesive sectors of economic activity. This means that the activity in these economic sectors is mainly contained inside each sector, with little influence of external economic sectors. Other sectors, such as Industrials and Materials, have stronger dependencies on other sectors, and are strongly influenced other sectors’ activities. Repeating this analysis for shorter periods of time, or combining the analysis with a moving window approach, could provide meaningful insights into the degree of interdependencies between the different economic sectors over time.

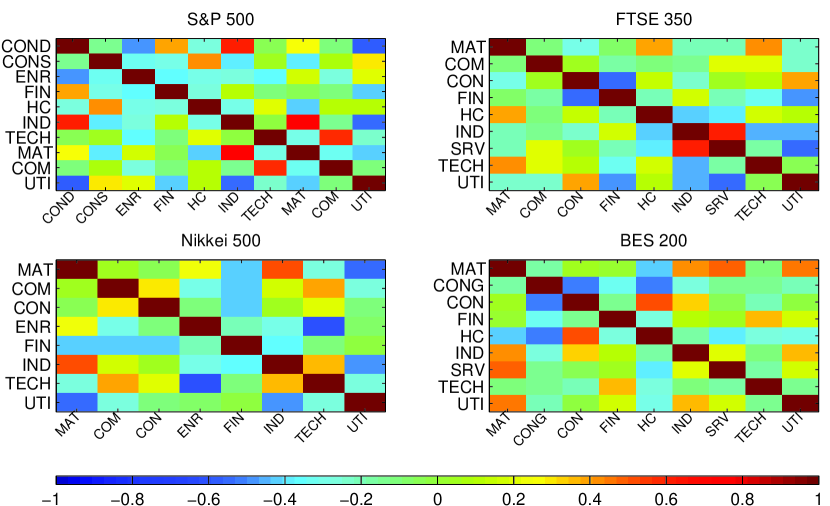

After studying the amount of influence that stocks receive from different sectors, we find that some sectors tend to influence the same stocks concurrently. We thus study the Pearson correlation of influences from two sectors to the same stocks, i.e. , where represents the vector variable of influence from sector to all stocks. Applying this definition of sector correlation to the S&P 500 data results in values that are presented in the first panel of figure 7. We find that in the S&P 500 index, the pairs of industrials sector and consumer discretionary sector, materials sector and industrials sector and the communications sector and the technology sector are very close to each other, in terms of their influence. Whenever a stock is highly influenced by one of these sectors, the other in the pair also tends to be influential to this stock. We also notice some dark blue area, e.g. the correlation between the utilities sector and the consumer discretionary sector, which means when a stocks is highly influence by one of the them, the other tends to be of little influence to the stock. We also study the UK FTSE 350 index, the Japanese Nikkei 500 index and the India BES 200 index. They all commonly show high correlation between materials sector and industrials sector.

5 Summary

This work presents a more general, statistically robust framework of the dependency network methodology introduced by Kenett et al. (2010). Using the dependency network methodology, we apply the partial correlation analysis to uncover dependency and influence relationship between the different companies in the investigated sample. Here we present a new statistically robust approach to filtering the extracted influence relationships, by either using a theoretical or an empirical approach. The influence method introduced in this study is generic and scalable, making it highly accessible to both policy makers and practitioners.

Here, we present two possible applications of this methodology. First, we study the stability of financial market structure and show that developed markets such as the US, UK, and Japan exhibit higher degree of market stability compared to developing countries such as India. Second, we show that one stock can be influenced by different sectors outside of its primary sector classification.

While financial analysts are usually specialized in one industry sector, a broader perspective of equity research is required to grasp the insights of stock performance expectations. The presented methodology provides new information on the interaction between different assets, and different economic sectors. Such information is valuable not only for investors and their practitioners, but also for regulators and policy makers.

Acknowledgements

We wish to thank ONR (Grant N00014-09-1-0380, Grant N00014-12-1-0548), DTRA (Grant HDTRA-1-10-1- 0014, Grant HDTRA-1-09-1-0035), NSF (Grant CMMI 1125290), the European MULTIPLEX (EU-FET project 317532), CONGAS (Grant FP7-ICT-2011-8-317672), FET Open Project FOC 255987 and FOC-INCO 297149, and LINC (no. 289447 funded by the EC s Marie- Curie ITN program) projects, DFG, the Next Generation Infrastructure (Bsik), Bi-national US-Israel Science Foundation (BSF), and the Israel Science Foundation for financial support.

References

- Abergel et al. (2011) Abergel, F., Chakrabarti, B., Chakraborti, A. and Mitra, M., Econophysics of order-driven markets, 2011, Springer.

- Adrian and Brunnermeier (2011) Adrian, T. and Brunnermeier, M.K., CoVaR. Technical report, National Bureau of Economic Research, 2011.

- Aste et al. (2010) Aste, T., Shaw, W. and Di Matteo, T., Correlation structure and dynamics in volatile markets. New Journal of Physics, 2010, 12, 085009.

- Baba et al. (2004) Baba, K., Shibata, R. and Sibuya, M., Partial correlation and conditional correlation as measures of conditional independence. Australian & New Zealand Journal of Statistics, 2004, 46, 657–664.

- Billio et al. (2012) Billio, M., Getmansky, M., Lo, A. and Pelizzon, L., Econometric measures of connectedness and systemic risk in the finance and insurance sectors. Journal of Financial Economics, 2012, 104, 535–559.

- Bisias et al. (2012) Bisias, D., Flood, M., Lo, A. and Valavanis, S., A survey of systemic risk analytics. US Department of Treasury, Office of Financial Research, 2012.

- Bouchaud and Potters (2003) Bouchaud, J. and Potters, M., Theory of financial risk and derivative pricing: from statistical physics to risk management, 2003, Cambridge Univ Pr.

- Brock et al. (2009) Brock, W., Hommes, C. and Wagener, F., More hedging instruments may destabilize markets. Journal of Economic Dynamics and Control, 2009, 33, 1912–1928.

- Campbell et al. (1997) Campbell, J., Lo, A. and MacKinlay, A., The econometrics of financial markets, Vol. 1, , 1997, princeton University press Princeton, NJ.

- Campbell et al. (2008) Campbell, R., Forbes, C., Koedijk, K. and Kofman, P., Increasing correlations or just fat tails?. Journal of Empirical Finance, 2008, 15, 287–309.

- Chou (1975) Chou, Y., Statistical analysis: with business and economic applications, 1975, Holt, Rinehart and Winston New York.

- Cizeau et al. (2001) Cizeau, P., Potters, M. and Bouchaud, J., Correlation structure of extreme stock returns. Quantitative Finance, 2001, 1, 217–222.

- Cont and Bouchaud (2000) Cont, R. and Bouchaud, J., Herd behavior and aggregate fluctuations in financial markets. Macroeconomic dynamics, 2000, 4, 170–196.

- Eisler and Kertesz (2006) Eisler, Z. and Kertesz, J., Scaling theory of temporal correlations and size-dependent fluctuations in the traded value of stocks. Physical Review E, 2006, 73, 046109.

- Elton et al. (2009) Elton, E.J., Gruber, M.J., Brown, S.J. and Goetzmann, W.N., Modern portfolio theory and investment analysis, 2009, John Wiley & Sons.

- Embrechts et al. (2002) Embrechts, P., McNeil, A. and Straumann, D., Correlation and dependence in risk management: properties and pitfalls. Risk management: value at risk and beyond, 2002, pp. 176–223.

- Engle (2002) Engle, R., Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics, 2002, 20, 339–350.

- Fama (1965) Fama, E.F., The behavior of stock-market prices. The journal of Business, 1965, 38, 34–105.

- Fisher (1915) Fisher, R., Frequency distribution of the values of the correlation coefficient in samples from an indefinitely large population. Biometrika, 1915, 10, 507–521.

- Fisher (1924) Fisher, R.A., The Distribution of the Partial Correlation Coefficient.. Metron, 1924, 3, 329–332.

- Forbes and Rigobon (2002) Forbes, K.J. and Rigobon, R., No contagion, only interdependence: measuring stock market comovements. The Journal of Finance, 2002, 57, 2223–2261.

- Granger (1969) Granger, C., Investigating causal relations by econometric models and cross-spectral methods. Econometrica: Journal of the Econometric Society, 1969, pp. 424–438.

- Haldane and May (2011) Haldane, A.G. and May, R.M., Systemic risk in banking ecosystems. Nature, 2011, 469, 351–355.

- Huang et al. (2013) Huang, X., Vodenska, I., Havlin, S. and Stanley, H.E., Cascading Failures in Bi-partite Graphs: Model for Systemic Risk Propagation. Scientific reports, 2013, 3.

- Kendall (1938) Kendall, M.G., A new measure of rank correlation. Biometrika, 1938, 30, 81–93.

- Kenett et al. (2012a) Kenett, D.Y., Preis, T., Gur-Gershgoren, G. and Ben-Jacob, E., Dependency network and node influence: Application to the study of Financial Markets. International Journal of Bifurcation and Chaos, 2012a, 22, 1250181.

- Kenett et al. (2012b) Kenett, D.Y., Raddant, M., Zatlavi, L., Lux, T. and Ben-Jacob, E., Correlations in the global financial village. International Journal of Modern Physics Conference Series, 2012b, 16, 13–28.

- Kenett et al. (2010) Kenett, D.Y., Tumminello, M., Madi, A., Gur-Gershgoren, G., Mantegna, R.N. and Ben-Jacob, E., Dominating clasp of the financial sector revealed by partial correlation analysis of the stock market. PLoS one, 2010, 5, e15032.

- Kenett et al. (2011) Kenett, Y.N., Kenett, D.Y., Ben-Jacob, E. and Faust, M., Global and Local Features of Semantic Networks: Evidence from the Hebrew Mental Lexicon. PloS one, 2011, 6, e23912.

- Krishan et al. (2009) Krishan, C.N.V., Petkova, R. and Ritchken, P., Correlation risk. Journal of Empirical Finance, 2009, 16, 353–367.

- Laloux et al. (1999) Laloux, L., Cizeau, P., Bouchaud, J. and Potters, M., Noise dressing of financial correlation matrices. Physical Review Letters, 1999, 83, 1467–1470.

- Laloux et al. (2000) Laloux, L., Cizeau, P., Potters, M. and Bouchaud, J., Random matrix theory and financial correlations. International Journal of Theoretical and Applied Finance, 2000, 3, 391–398.

- Lo et al. (1997) Lo, A.A.W.C., CRAIG, A. et al., The econometrics of financial markets, 1997, princeton University press.

- Lo and Craig MacKinlay (1990) Lo, A.W. and Craig MacKinlay, A., An econometric analysis of nonsynchronous trading. Journal of Econometrics, 1990, 45, 181–211.

- Lux et al. (1999) Lux, T., Marchesi, M. and Bonn, U., Scaling and criticality in a stochastic multi-agent model of a financial market. Nature, 1999, 397, 498–500.

- Madi et al. (2011) Madi, A., Kenett, D., Bransburg-Zabary, S., Merbl, Y., Quintana, F., Boccaletti, S., Tauber, A., Cohen, I. and Ben-Jacob, E., Analyses of antigen dependency networks unveil immune system reorganization between birth and adulthood. Chaos: An Interdisciplinary Journal of Nonlinear Science, 2011, 21, 016109–016109.

- Markowitz (1952) Markowitz, H., Portfolio selection. The journal of finance, 1952, 7, 77–91.

- Maugis (2014) Maugis, P., Event Conditional Correlation: Or How Non-Linear Linear Dependence Can Be. arXiv preprint arXiv:1401.1130, 2014.

- Morck et al. (2000) Morck, R., Yeung, B. and Yu, W., The information content of stock markets: why do emerging markets have synchronous stock price movements?. Journal of financial economics, 2000, 58, 215–260.

- Pearson (1895) Pearson, K., Contributions to the mathematical theory of evolution. II. Skew variation in homogeneous material. Philosophical Transactions of the Royal Society of London. A, 1895, 186, 343–414.

- Plerou et al. (1999) Plerou, V., Gopikrishnan, P., Rosenow, B., Nunes Amaral, L. and Stanley, H., Universal and nonuniversal properties of cross correlations in financial time series. Physical Review Letters, 1999, 83, 1471–1474.

- Podobnik et al. (2009) Podobnik, B., Horvatic, D., Petersen, A. and Stanley, H., Cross-correlations between volume change and price change. Proceedings of the National Academy of Sciences of the United States of America, 2009, 106, 22079–22084.

- Pollet and Wilson (2010) Pollet, J. and Wilson, M., Average correlation and stock market returns. Journal of Financial Economics, 2010, 96, 364–380.

- Shapira et al. (2009) Shapira, Y., Kenett, D. and Ben-Jacob, E., The index cohesive effect on stock market correlations. The European Physical Journal B, 2009, 72, 657–669.

- Sinha et al. (2010) Sinha, S., Chatterjee, A., Chakraborti, A. and Chakrabarti, B., Econophysics: an introduction, 2010, Wiley-VCH.

- Sornette (2004) Sornette, D., Why stock markets crash: critical events in complex financial systems, 2004, Princeton University Press.

- Takayasu (2006) Takayasu, H., Practical Fruits of Econophysics: Proceedings of the Third Nikkei Econophysics Symposium, 2006, Springer.

- Tumminello et al. (2010) Tumminello, M., Lillo, F. and Mantegna, R., Correlation, hierarchies, and networks in financial markets. Journal of Economic Behavior & Organization, 2010, 75, 40–58.

- Voit (2005) Voit, J., The statistical mechanics of financial markets, 2005, Springer.