On the Computation of Multivariate Scenario Sets for the Skew- and Generalized Hyperbolic Families

Abstract

We examine the problem of computing multivariate scenarios

sets for skewed distributions. Our interest is motivated by the

potential use of such sets in the ‘stress testing’ of insurance

companies and banks whose solvency is dependent on changes in a set of

financial ‘risk factors’. We define multivariate scenario sets based

on the notion of half-space depth (HD) and also introduce the notion

of expectile depth (ED) where half-spaces are defined by expectiles

rather than quantiles. We then use the HD and ED functions to define

convex scenario sets that generalize the concepts of quantile and

expectile to higher dimensions. In the case of elliptical

distributions these sets coincide with the regions encompassed by the

contours of the density function. In the context of multivariate

skewed distributions, the equivalence of depth contours and density

contours does not hold in general. We consider two parametric families

that account for skewness and heavy tails: the generalized hyperbolic

and the skew- distributions. By making use of a canonical form

representation, where skewness is completely absorbed by one

component, we show that the HD contours of these distributions are

‘near-elliptical’ and, in the case of the skew-Cauchy distribution, we

prove that the HD contours are exactly elliptical. We propose a

measure of multivariate skewness as a deviation from angular

symmetry and show that it can explain the quality of the elliptical

approximation for the HD contours.

Keywords: angular symmetry; expectile depth; generalized hyperbolic distribution; half-space depth; multivariate scenario sets; skew- distribution.

1. Lancaster Medical School, Lancaster University, Lancaster, UK

2. Institute of Infection and Global Health, University of Liverpool, Liverpool, UK

3. Department of Actuarial Mathematics and Statistics, Heriot-Watt University, Edinburgh, UK

4. Maxwell Institute for Mathematical Sciences, Edinburgh, UK

1 Introduction

While the topic of this paper is of independent computational statistical interest, the original motivation for studying these issues comes from applications in financial risk management.

Let be a random vector representing changes in a set of so-called financial risk factors, such as equity indexes, interest rates, foreign exchange rates, etc. These risk factors impact the value of a financial portfolio and lead to a random loss given by . The portfolio might be a derivatives desk at a bank or a product book (e.g. annuity book) of an insurer.

We will assume that: (1) we have data that permit the statistical estimation of a model for ; (2) the function is known to us. That is, for any value we are able to compute the resulting loss . The function contains information about the size of the positions in the portfolio and encapsulates the valuation formulas necessary to quantify the effect of changes in the risk factors on the values of the positions.

A first question of possible interest is: how do we construct a scenario set based on the probability distribution of that includes plausible scenarios?

In our opinion there are advantages to using scenario sets that are based on the idea of half-space depth rather than sets that are based on density. In the presence of multivariate skewness, density sets tend to be dragged towards the shorter tails of the distribution and exclude too many extreme scenarios in the outer tail.

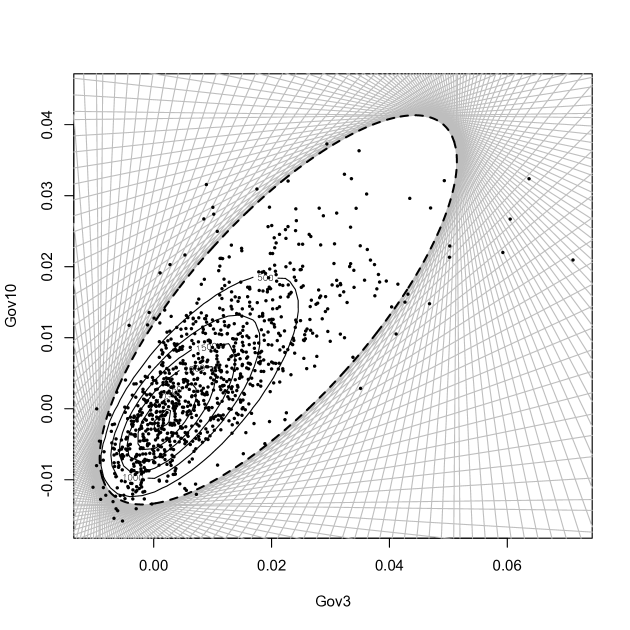

An example is given in Figure 1. We have plotted typical one-year changes in yield for a 3-year government bond and a 10-year government bond. These are the kinds of risk factors that would be considered in quantifying, for example, the change in the value of a portfolio of government bonds, or a portfolio of annuity liabilities. A bivariate normal inverse Gaussian () distribution has been fitted to the data (see Example 4.12) and, on the basis of the fitted model, density contours have been plotted and lines are shown that divide the plane into two half-spaces with probabilities and . The set formed by the intersection of closed half-spaces with probability is denoted . Points on the boundary are said to have depth so that is the set of points with depth at least .

If we construct a scenario set based on depth we want to be able to say whether for some arbitrary point . It is often the case that a regulator or manager asks the risk modeller to consider a particular extreme scenario and work out how costly it might be. In order to weigh the importance or plausibility of this scenario we would like to know its depth , i.e. the largest value of for which .

Suppose we are given a whole series of scenarios to consider and for each scenario we calculate the associated loss. Let for some denote a ruin set, i.e. a set of scenarios that lead to an unacceptably large loss. We would like to identify the ruin scenario that is most plausible, in the sense that it has the maximum depth . This is known as the reverse stress testing problem.

In this paper we will consider the properties of and related scenario sets when the distribution of is in either the skew- () or generalised hyperbolic () family. These are flexible families of skewed and potentially heavy-tailed distributions that are useful for modelling financial risk-factor changes. The NIG distribution fitted to the data in Figure 1 belongs to the latter family and we see that, in this case, the set is very close to (but not exactly) an ellipse. This “near ellipsoidal” behaviour is true of other distributions in these families.

The paper is structured as follows. In Section 2, we define multivariate scenario sets based on half-space depth () and briefly describe some important properties of the half-space median that are relevant for the purposes of this paper. In Section 3 we introduce the related notion of expectile depth () which generalizes the univariate concept of expectile to higher dimensions.

In Section 4 we examine the problem of computing depth sets based on and for the (Section 4.1) and (Section 4.2) families of distributions. We show that the computation of depth sets can be simplified by making use of a canonical form representation, where skewness is completely absorbed by one component. We also prove that the contours for the skew-Cauchy () distribution are elliptical, giving a further simplification in the computation.

We provide an algorithm for the construction of approximating ellipsoids to depth sets based on and investigate the quality of such an approximation. In Section 4.3 we examine the relationship between ellipsoidal depth sets and angular symmetry. We propose a multivariate measure of skewness as a deviation from angular symmetry and show that this measure can explain the quality of the ellipsoidal approximation. Numerical results, in Section 4.4, show its concordance with the probability of misclassification. Although the probability of misclassification is a direct and more interpretable measure of the error we incur when using ellipsoidal approximations, it is much more difficult to compute. We conclude with a discussion in Section 5.

2 Half-Space Depth

2.1 Half-Space Depth and its Relation to Quantiles

Let be a probability space and be a given random vector. For any and any directional vector , let

denote the closed half-space bounded by the hyperplane through . We write the probability that lies in the half-space as

The half-space depth of the point with respect to the probability distribution of is given by

| (1) |

where is the Euclidean norm. We note that is an affine invariant measure, meaning that if is a non-singular matrix and is a vector, then .

Let be a probability value. The main definition of a scenario set that we use is

| (2) |

which is the intersection of all closed half-spaces with probability at least . Sets of this kind are considered by many authors including Massé & Theodorescu (1994), Rousseeuw & Ruts (1999) and McNeil & Smith (2012). The construction is sometimes referred to as half-space trimming.

For we also define a -quantile function on by writing for the -quantile of . Then, (2) can be expressed in terms of by

We will make the assumption that has a strictly positive probability density on . This assumption is satisfied by the distributions that interest us in this paper and allows us to pass easily between the concepts of quantiles and depth. Under this assumption, we have

from which it can be easily deduced that

| (3) |

We thus refer to as a depth set and we refer to , the boundary of , as the depth contour; the contour consists of the points with depth exactly equal to .

In Figure 1 we show an example of the half-space trimming construction for (the mesh of grey straight lines) as well as the depth contour (the dashed curve).

2.2 The half-space median and angular symmetry

The function can be used to define an affine equivariant median known as the half-space median (or Tukey median) of . This is the set of maximal given by

| (4) |

By affine equivariant we mean that, if is a non-singular matrix and is a vector, then .

The half-space median is, in general, not unique unless is symmetric according to some notion of multivariate symmetry; see Serfling (2006) for a survey of multivariate concepts of symmetry. More general conditions for uniqueness are given in Small (1987) who shows that a sufficient condition for uniqueness in the bivariate case is the strict positivity of the density function. The least restrictive definition of multivariate symmetry, under which the half-space median is unique, is angular symmetry. The random variable is angularly symmetric about a point if

| (5) |

where “” indicates equality in distribution. Dutta, Ghosh & Chaudhuri (2011) show that if and only if is the center of angular symmetry. Thus, if is the centre of angular symmetry, then . This property is used in Section 4.3 to define two different measures of multivariate skewness as deviations from angular symmetry.

Note that if is the center of angular symmetry, then also corresponds to the component-wise median. This is clear, since if then

If we set , the th unit vector, we can infer that the th element of is the univariate median of the marginal distribution of the th component of .

3 Expectile Depth

3.1 Definitions

The notion of an expectile was introduced by Newey & Powell (1987) as the solution of an asymmetric least squares regression problem, analagous to quantile regression. Given an integrable random variable in and , the -expectile of the distribution function of is the unique solution of the equation

| (6) |

where , and is the expectation with respect to the distribution of .

It was shown by Jones (1994) that the -expectile of can be expressed as the -quantile of the related distribution function

where is the lower partial moment of . For any random variable the distribution function is continuous and strictly increasing on its support, implying that the -expectile is uniquely defined for all in .

In our application, for a fixed random vector , we define the -expectile function to be the -expectile of the distribution for and, for we consider a scenario set of the form

Let

denote the smallest probability of a half-space when probabilities are calculated according to . We refer to as the expectile depth of with respect to the distribution of and note that it is also an affine invariant measure. The scenario set may also be expressed as

With obvious notation, we use to indicate the boundary of , and refer to this as the -expectile depth contour.

3.2 Properties of expectile depth

There are both practical and theoretical reasons for considering expectile depth as an alternative to standard (quantile) depth. On the one hand the expectile can simply be viewed as a kind of generalized quantile; see Bellini et al. (2013). Using the techniques of McNeil & Smith (2012) it is straightforward to show that, when has an elliptical distribution, the set is an ellipsoidal set like , with axis lengths in identical proportions. However, for general distributions expectile depth sets will have different shapes to (quantile) depth sets.

At a more theoretical level, both the quantile function and the expectile function are positive-homogeneous functions on , meaning that they are functions satisfying for .

A fundamental result in convex analysis can be used to show that a positive-homogeneous function has a representation as the so-called support function

| (7) |

of the convex set

| (8) |

if and only if the function is also subadditive on ; see Rockafellar (1970) or McNeil & Smith (2012) for technical details and recall that a subadditive function satisfies for all and in .

The set in (8) is when and it is when . However, the quantile function is not subadditive in general, but only for certain underlying random vectors and certain values of . For example, for elliptically distributed random vectors is subadditive for . But when is a vector comprising two independent standard exponential random variables, McNeil & Smith (2012) show that is not subadditive for . In contrast, the expectile function is subadditive for any random vector with finite mean and .

Let satisfy and assume that and are non-empty. The implication of (7) is that for any there exists a scenario , i.e. a scenario on the boundary of the expectile depth set, such that . However, there may exist values such that for all . In this sense is more satisfactory as a multivariate analogue of the expectile than is as a multivariate analogue of the quantile.

4 Depth Sets for Skewed Distributions

We now consider two families of multivariate skewed distributions, both of which have a canonical form, obtained by an affine transformation, in which all of the skewness is absorbed by one of the marginal distributions. In view of the affine invariance of and , it suffices to be able to calculate these quantities for random vectors in their canonical form.

4.1 Skew- distribution

The skew- () distribution is a flexible model for skewed and heavy-tailed multivariate data (Azzalini & Capitanio, 2003; Azzalini & Genton, 2008). Let and denote the parameters of location, skewness and the degrees of freedom; let be a symmetric, positive-definite dispersion matrix. A random variable in is distributed according to a distribution if it has density function

where

and denotes the univariate Student distribution function with degrees of freedom. For later use, we also define the following correlation matrix

Skewness and tails heaviness are regulated by the parameters and , respectively; these two parameters jointly characterize the shape of the distribution. If the Student distribution is recovered; if we obtain the skew-normal () distribution (Azzalini, 2005; Azzalini & Capitanio, 1999); if and we obtain the multivariate normal distribution.

The next result, which follows from the linear transformation result given in Appendix A.1, introduces the canonical form of the distribution (). The importance of the canonical form in summarizing important features related to the location, skewness and kurtosis of the family is discussed in an unpublished paper by Capitanio (2012).

Theorem 4.1.

Let where and . Let and define , where is an orthonormal matrix with first column equal to . Then .

If is in canonical form, we simply write , where is the scalar parameter of skewness; if , the case of the skew-Cauchy () distribution, then ; if , then .

Without loss of generality we have assumed that for a random vector in canonical form all of the asymmetry is absorbed in the first component and we have for . We now show that the and contours of the distribution are symmetric with respect to the axis of the unique asymmetric component. This property is useful in the construction of scenario sets based on either or of any distribution, as shown later in some examples.

Theorem 4.2.

Let and denote two points in whose first elements are equal and the others differ in sign at most. If , then and .

Proof.

For a given normalized vector , consider the half-space .

Let be a set of indices indicating the elements of that have opposite sign with respect to the corresponding elements of . Define the random vector so that if and if , where is the complement of ; similarly define so that if and if . Since it follows that

and hence that

We obtain and when we take the infimum over all . ∎

In the special case of the distribution, the computation of contours is further simplified. As shown in the next theorem, the contours of the distribution are circular, and hence ellipsoidal for the general distribution; we use and to indicate the secant and tangent functions, respectively.

Theorem 4.3.

If , then

| (9) |

where

Proof.

From the expression of the univariate quantile function of the distribution (Behboodian, Jamalizadeh & Balakrishnan, 2006), for any directional vector , we can write

where is the first element of . It follows that

By observing that the Euclidean unit ball can be written as , we conclude that for , the vectors describe the unit ball and therefore

∎

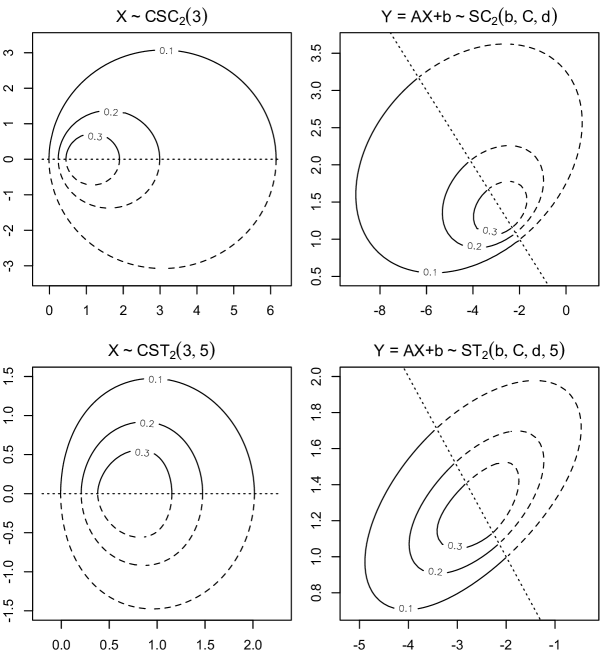

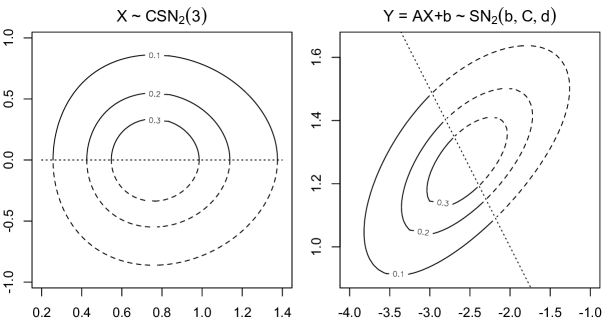

We now give some examples to illustrate the depth contours and expectile depth contours of certain special cases of the ST distribution. While the skew-Cauchy has elliptical depth contours, other cases have contours that are near-elliptical; the quality of an elliptical approximation will be investigated further in Section 4.4. Algorithm 1 is used to calculate half-space depth and a similar approach can be used for expectile depth, as indicated in Example 4.5.

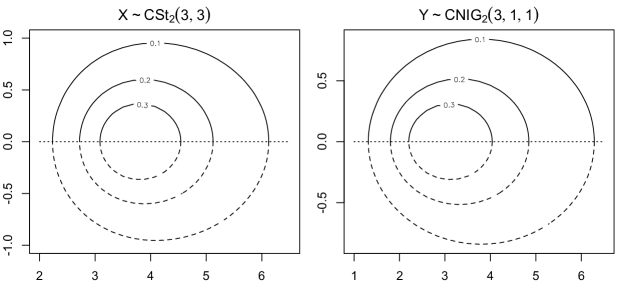

Example 4.4.

Let and define

and . The linear transformation has distribution , where

and . Figure 2 shows the construction of , for , for the random variables and , letting vary over the values . An efficient computation of the depth contours for is given by applying an affine transformation to the depth contours computed for , where skewness is completely absorbed by the first component. Note that from Theorem 4.2, we only need to compute half of the depth contour and obtain the other half by symmetry. In the case of the computation is further simplified by the circular shape of the depth contours of the canonical form.

Example 4.5.

4.2 Generalized hyperbolic distribution

A class of multivariate skewed distributions that has received a lot of attention in the financial literature is the class of generalized hyperbolic () distributions; see McNeil, Frey & Embrechts (2005) and Eberlein (2010). Let , denote the parameters of location and skewness, let be a symmetric, positive-definite dispersion matrix and l et , , be scalars. has a generalized hyperbolic distribution, written , if it has density

where

and where denotes the modified Bessel function of third kind. This class of distributions can be stochastically represented as mean-variance mixtures of normal distributions using the representation

| (10) |

where

-

;

-

is a matrix such that ;

-

has a generalized inverse Gaussian (GIG), denoted by , with density function (17) in the Appendix.

Note that and are equal in distribution for , which causes an identifiability problem. This problem can be solved by imposing a constraint on the model parameters; see the NIG case below.

An important feature of the distribution is its flexibility. It also contains several special cases and, in particular, we consider the following.

-

Normal-inverse-Gaussian () distribution: and (our choice of identifiability constraint).

-

Skewed- () distribution: , and .

Other special cases and a more detailed discussion of the family of distributions are given in McNeil, Frey & Embrechts (2005).

We now introduce the canonical form of the distribution. The following result follows from the general result on linear transformations in Appendix A.2.

Theorem 4.6.

Let where for . Let and define where is an orthonormal matrix having the first column equal to . Then .

If is in canonical form, then we write where is the scalar skewness parameter; in the case of the distribution, we write ; and in the case of the distribution, .

Theorem 4.2 in Section 4.1 can be easily extended to the family using a similar argument that makes use of the canonical form, thus we omit it.

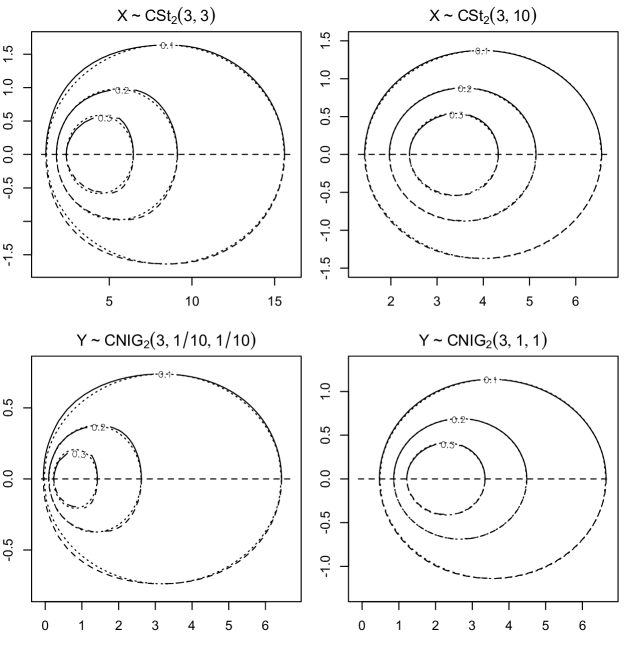

In the following example we calculate half-space depth contours for special cases of the GH distribution. A similar approach to Algorithm 1 is used to compute half-space depth at points . Since the family is closed under linear operations, the probabilities of half spaces are simply computed from the distribution function of univariate distributions. The example suggests that the depth contours are particularly close to elliptical for many distributions and, in view of this, we also calculate an approximating ellipsoid using Algorithm 2. Expectile depth is also straightforward to compute, as we illustrate.

Example 4.7.

Let and . Figure 4 shows some contours for (top panels), letting vary over the set , and (lower panels), with . Dotted lines correspond to approximating ellipsoids obtained from Algorithm 2. As shown in Figure 4 larger values of for and larger values of for result in a better ellipsoidal approximation of the depth contours (see Section 4.3). Figure 5 shows contours for with (left panel) and with (right panel).

Let :

-

1.

Compute .

-

2.

Compute where and are given in Theorem 4.6.

-

3.

For each component of compute the -quantile , the -quantile , and set and , for .

-

4.

Approximate with the ellipsoid

where .

4.3 Relationship between angular symmetry and ellipsoidal depth sets

A natural measure of skewness that quantifies the deviation of a random variable in from angular symmetry is

| (11) |

where is the half-space median. The affine equivariance of the median implies that is an affine invariant measure of skewness. This can be seen by letting denote the affine transformation that puts into its canonical form and observing that

For the and distributions we also define an alternative measure of skewness by

| (12) |

where denotes the component-wise median of ; this measure is simpler to calculate. Note that since and if is angularly symmetric then . Alternative measures of multivariate skewness are discussed in a non-parametric context in Liu, Prelius & Singh (1999).

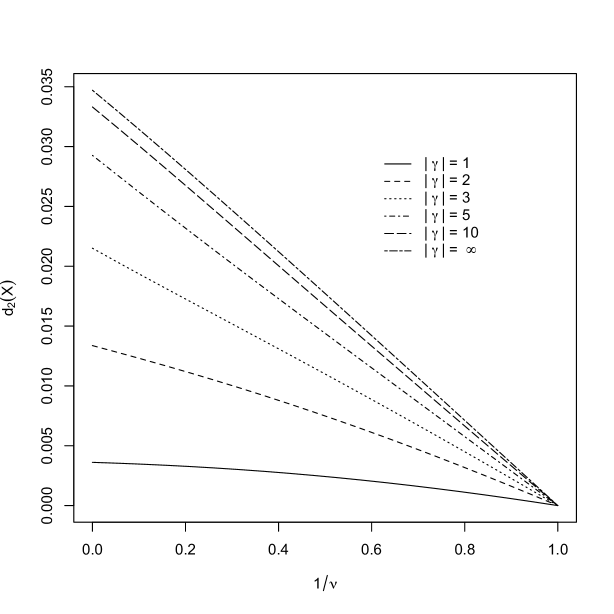

Figure 6 shows some curves of for different distributions against and letting vary over the set . Here, we only focused on in order to highlight the different values taken by in this interval; however, for , the different curves monotonically increase towards 1/2. Deviation from angular symmetry appears to reach its maximum at about , that corresponds to the case of the independent pair of variables , where is a standard normal variable and is a half-normal variable. However, closeness of the distribution to angular symmetry is indicated for values of close to 1. Indeed, the following results prove that in the case of the distribution, angular symmetry holds exactly.

Theorem 4.8.

If , then for any the median of is

| (13) |

Corollary 4.9.

If , then is angularly symmetric about where is given by (13).

Proof.

It follows from Theorem 4.8 that the component-wise median of is where is given by (13). For any directional vector , we can write

| (14) |

If the above equation equals ; let and set . Using Appendix A.1 it may be easily shown that , where is defined in Theorem 4.8. It follows that (14) can be expressed as

Since is arbitrary we conclude that and hence that is the half-space median, as well as the center of angular symmetry of . ∎

Corollary 4.10.

If , then is angularly symmetric about where , and

Proof.

Figure 7 is an analogous plot to Figure 6 for the case of the distribution. In this case the degrees of freedom play an opposite role with respect to the case: as . This can be explained as follows. Using the stochastic representation in (10), as , tends to a degenerate distribution which is constant in 1. From (10), we have that tends in distribution to which is elliptically (hence also angularly) symmetric.

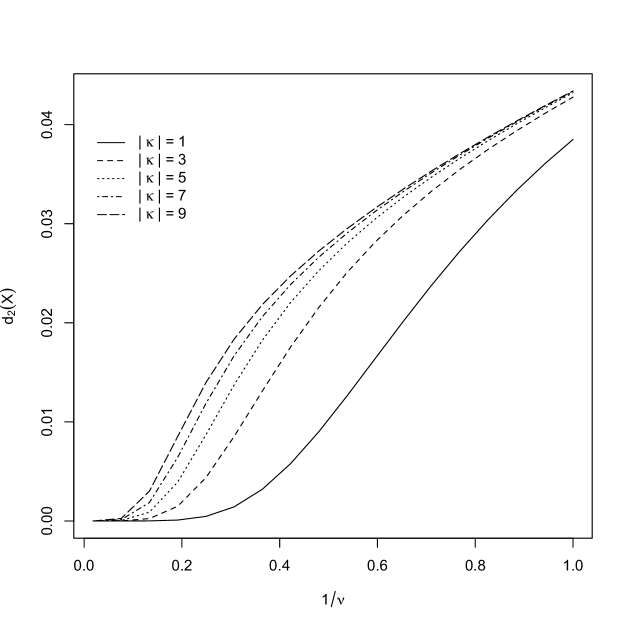

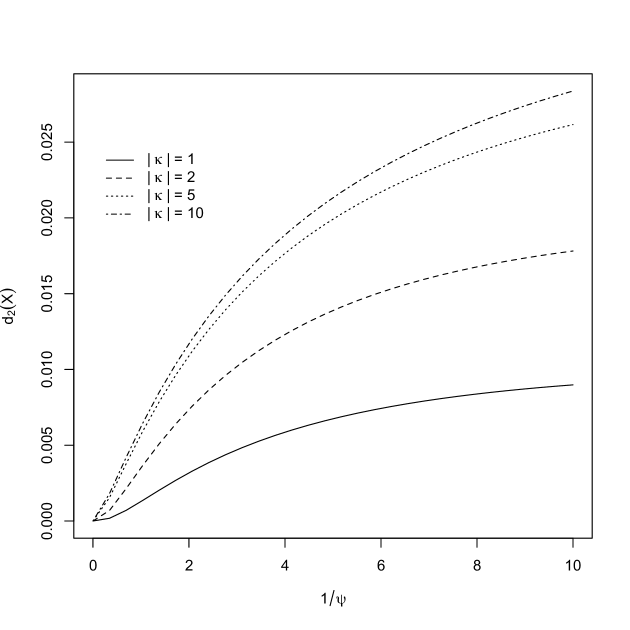

A similar argument applies to the distribution. As , tends in distribution to the constant 1 and the same conclusions are drawn as in the previous case. This is reflected in Figure 8, where for decreasing values of . Hence large values of results in a better ellipsoidal approximation.

4.4 Probability of misclassification using ellipsoidal approximations

Let denote a random variable in , belonging either to the or family. If is the approximating ellipsoid of then the misclassification set is given by

where is the set of false negatives and is the set of false positives. The probability of misclassification is

| (15) |

where is the density function of . The above integral is intractable, in general, so we use numerical quadrature to approximate the integral as a sum over a fine grid. Letting be a regular grid covering with cell area , we have

For small values of (for example ) we find that, in general, the misclassification probability is relatively low with values exceeding only in very extreme cases with very strong asymmetry. Additionally, we find that the main component in the misclassification probability is generally given by while is often negligible. The next example illustrate these observations.

Example 4.11.

Let , and . In this example, we consider the approximation of with the ellipse . In Tables 3-3 the probability mass of the sets and , and the index are reported for each of the three random random vectors while the skewness parameters and are allowed to vary. In all three cases, the misclassification probability increases for increasing values of the skewness parameter. The random variable appears to have the highest misclassification probability of about for , a case of extremely high asymmetry.

| 1 | 0.008 | 0.000 | 0.009 |

|---|---|---|---|

| 2 | 0.028 | 0.000 | 0.018 |

| 5 | 0.069 | 0.000 | 0.026 |

| 15 | 0.089 | 0.000 | 0.029 |

| 30 | 0.095 | 0.000 | 0.029 |

| 1 | 0.002 | 0.002 | 0.004 |

|---|---|---|---|

| 2 | 0.008 | 0.005 | 0.013 |

| 5 | 0.025 | 0.009 | 0.029 |

| 10 | 0.035 | 0.010 | 0.033 |

| 50 | 0.036 | 0.010 | 0.035 |

| 1 | 0.001 | 0.000 | 0.005 |

|---|---|---|---|

| 3 | 0.002 | 0.001 | 0.013 |

| 5 | 0.003 | 0.001 | 0.015 |

| 10 | 0.003 | 0.001 | 0.017 |

| 20 | 0.003 | 0.001 | 0.017 |

Only in the case of is the probability mass on not negligible, with a maximum value of about . The random variable has the lowest misclassification probability even for very high values of , reaching a maximum value of about . Note that the measure of skewness is also a good indicator of the quality of the ellipsoidal approximation, although it is not comparable between different families of distributions.

Example 4.12.

We now consider the yield data for 3-year and 10-year government bonds, plotted in Figure 1. We fitted a bivariate and obtained the following maximum likelihood estimates

The resulting index of skewness is which indicates a low level of skewness (as deviation from angular symmetry) of the estimated distribution. Indeed, the misclassification probability of the ellipsoidal approximation is extremely low as is also evident in Figure 1.

5 Discussion

In this paper we have shown how multivariate scenario sets based on and can be efficiently computed in the case of the and distributions. Computation can be simplified by making use of a canonical form representation where only one component is asymmetric at most. Additionally, in the case of multivariate sets based on , ellipsoids represents a good approximation with a probability of misclassification exceeding only in cases of extremely high skewness. We have demonstrated that the quality of the ellipsoidal approximations can be explained in terms of the closeness of the and distributions to angular symmetry. We proposed a measure of the departure from angular symmetry which is easy to compute and concordant with the misclassification probability.

In our examples of ellipsoidal approximations, we only considered bivariate cases. However, the affine invariance property and the availability of a canonical form, with all the asymmetry absorbed in the marginal distribution of the first component, means that this is sufficient to gain an understanding of the quality of the approximation. Indeed, the skewness index , introduced in Section 4.3, and the curves shown in Figures 6, 7 and 8, are independent of the dimension of the underlying vector. Although the probability of misclassification will change with dimension, the geometry of these distributions means that the changes will remain modest.

The near-elliptical shape of the depth sets for and distributions, and the availability of a simple method of constructing an elliptical approximation, makes these distributions attractive for modelling the behaviour of financial risk factors in the stress testing applications metioned in the Introduction.

Although we only considered the and distributions, we believe that some of the results can be easily extended to other multivariate skewed distributions which are closed under affine transformations and which admit a canonical form representation. An example is given by skew scale mixtures of normal variates (Branco & Dey, 2001) of which the multivariate skew-slash distribution (Wang & Genton, 2006) is one of the many special cases.

Finally, some of the presented material might also be useful to address the related problem of defining multivariate measures of skewed distributions that do not depend on the existence of the moments of the distribution. For example, Theorem 4.3 and Algorithm 2 also allow for an exact and approximate computation, respectively, of a multivariate measure of kurtosis proposed by Wang & Serfling (2005), who only considered elliptical distributions as parametric examples. Additionally, Corollary 4.10 provides a measure of location for the distribution, namely its center of angular symmetry, that should be preferred to the location parameter which usually lies in regions far from the “center” of the distribution. It would also be interesting to investigate whether the half-space median of the and distributions is unique or whether a specific point of maximum depth can be identified by making use of the canonical form.

Acknowledgements

Some of the work was done while Emanuele Giorgi was a student at the Department of Statistical Sciences in the University of Padua, Italy, under the supervision of Adelchi Azzalini.

References

- Azzalini (2005) Azzalini, A. (2005). The skew-normal distribution and related multivariate families. Scandinavian Journal of Statistics 32, 159–188.

- Azzalini & Capitanio (1999) Azzalini, A. & Capitanio, A. (1999). Statistical applications of the multivariate skew-normal distribution. Journal of Royal Statistics. Series B 61, 579–602. The full article is available at arXiv.org:0911.2093v1.

- Azzalini & Capitanio (2003) Azzalini, A. & Capitanio, A. (2003). Distributions generated by perturbation of symmetry with emphasis on a multivariate skew distribution. Journal of Royal Statistical Society. Series B 65, 367–389. The full article is available at arXiv.org:0911.2342v1.

- Azzalini & Genton (2008) Azzalini, A. & Genton, M. G. (2008). Robust likelihood methods based on the skew- and related distributions. International Statistical Review 76, 106–129.

- Behboodian et al. (2006) Behboodian, J., Jamalizadeh, A. & Balakrishnan, N. (2006). A new class of skew-Cauchy distributions. Statistics and Probability Letters 76, 1488–1493.

- Bellini et al. (2013) Bellini, F., Klar, B., Müller, A. & Gianin, M. (2013). Generalized quantiles as risk measures. Preprint.

- Branco & Dey (2001) Branco, M. D. & Dey, D. K. (2001). A general class of multivariate skew-elliptical distributions. Journal of Multivariate Analysis 79, 99 – 113.

- Capitanio (2012) Capitanio, A. (2012). On the canonical form of scale mixtures of skew-normal distributions. Available at arXiv.org:1207.0797v1.

- Dutta et al. (2011) Dutta, S., Ghosh, A. K. & Chaudhuri, P. (2011). Some intriguing properties of Tukey’s half-space depth. Bernoulli 17, 1420–1434.

- Eberlein (2010) Eberlein, E. (2010). Generalized hyperbolic models. In Encyclopedia of Quantitative Finance, R. Cont, ed. Wiley, New York, pp. 833–836.

- Jones (1994) Jones, M. C. (1994). Expectiles and M-quantiles are quantiles. Statistics and Probability Letters 20, 149–153.

- Liu et al. (1999) Liu, R. Y., Prelius, J. M. & Singh, K. (1999). Multivariate analysis by data depth: descriptive statistics, graphics and inference. The Annals of Statistics 27, 783–858.

- Massé & Theodorescu (1994) Massé & Theodorescu (1994). Halfplane trimming for bivariate distributions. Journal of Multivariate Analysis 48, 188–202.

- McNeil & Smith (2012) McNeil, A. & Smith, A. (2012). Multivariate stress scenarios and solvency. Insurance: Mathematics and Economics 50, 299–308.

- McNeil et al. (2005) McNeil, A. J., Frey, R. & Embrechts, P. (2005). Quantitative Risk Management: Concepts, Techniques and Tools. Princeton University Press, Princeton.

- Newey & Powell (1987) Newey, W. K. & Powell, J. L. (1987). Asymmetric least squares estimation and testing. Econometrica 55, 819–847.

- Rockafellar (1970) Rockafellar, R. (1970). Convex Analysis. Princeton University Press, Princeton.

- Rousseeuw & Ruts (1999) Rousseeuw, P. & Ruts, I. (1999). The depth function of a population distribution. Metrika 49, 213–244.

- Serfling (2006) Serfling, R. (2006). Multivariate symmetry and asymmetry. In Encyclopedia of statistical sciences, vol. 8. S. Kotz, N. Balakrishnan, C. B. Read and B. Vidakovic, Wiley, New York, 2nd ed., pp. 5538–5345.

- Small (1987) Small, C. G. (1987). Measures of centrality of multivariate and directional distribution. The Canadian Journal of Statistics 15, 31–39.

- Wang & Genton (2006) Wang, J. & Genton, M. G. (2006). The multivariate skew-slash distribution. Journal of Statistical Planning and Inference 136, 209 – 220.

- Wang & Serfling (2005) Wang, J. & Serfling, R. (2005). Nonparametric multivariate kurtosis and tailweight measures. Journal of Nonparametric Statistics 17, 441–456.

Appendix A Linear forms

Let be a non-singular matrix with rank and let .

A.1 Skew- distribution

If , then , where

with .

If and is a directional vector in , then , where

| (16) |

A.2 Generalized hyperbolic distribution

If , then , where

If and is a directional vector in , then .

Appendix B Generalized Inverse Gaussian distritbuion

If has a generalized inverse Gaussian () distribution, written as , then its density is

| (17) |

where is the modified Bessel function of the third kind of order and with the following constraints on the other parameters: , if ; , if ; , if .