Minsky financial instability, interscale feedback, percolation and Marshall-Walras disequilibrium

Abstract

We study analytically and numerically Minsky instability as a combination of top-down, bottom-up and peer-to-peer positive feedback loops. The peer-to-peer interactions are represented by the links of a network formed by the connections between firms; contagion leading to avalanches and percolation phase transitions propagating across these links. The global parameter in the top-bottom – bottom-up feedback loop is the interest rate. Before the Minsky Moment, in the ‘Minsky loans accelerator’ stage the relevant “bottom” parameter representing the individual firms’ micro-states, is the quantity of loans. After the Minsky Moment, in the ‘Minsky crisis accelerator’ stage, the relevant ‘bottom’ parameters are the number of ponzi units / quantity of failures / defaults. We represent the top-bottom, bottom-up interactions on a plot similar to the Marshall-Walras diagram for quantity-price market equilibrium (where the interest rate is the analog of the price). The Minsky instability is then simply emerging as a consequence of the fixed point (the intersection of the supply and demand curves) being unstable (repulsive). In the presence of network effects, one obtains more than one fixed point and a few dynamic regimes (phases). We describe them and their implications for understanding, predicting and steering economic instability.

1 Requisiteness of the agent based and network approach

1.1 Background on Minsky theory of instability

Minsky’s theory of instability has as a central element the procyclical self-reinforcing feedback loop between the individual behavior of economic players and the state of the economic system as a whole. This explains the fact that in spite of his brilliance and in spite of the personal admiration by many of his peers, for a long time, Minsky’s work could not be absorbed within the mainstream economic theory [Wray 2011a]. Indeed there are a series of crucial features in the Minsky instability theory which are incompatible with the neo-classical framework:

-

1.

the relationship between the individual and the macroscopic behavior cannot be expressed in a framework where both the system and the individuals are fused into a representative agent by simply ignoring aggregation concerns.

-

2.

the positive feedback loop between the system as such and the agents composing it, leads to a dynamics which instead of approaching equilibrium, as assumed by the neo-classical approach, runs away from it. Departures from the equilibrium, instead of being corrected by the forces within the economic system, are, in Minsky’s theory, exacerbated until a Minsky moment takes place and from then on, new divergence from equilibrium takes place in the opposite direction. Thus, as observed by Minsky [Minsky 1975], in a capitalist economy, stability is destabilizing and thus impossible.

-

3.

Minsky divided the companies into 3 classes:

-

-

Hedge - companies that are entitled to enough cash flow to completely pay their debts including their interest,

-

-

Speculative - companies that are only entitled to enough cash flow to serve their interest payments,

-

-

Ponzi - companies that do are not entitled to enough cash flow to pay interest on their loans.

This classification (see below for their formal definitions in Eqs. 1-4 and the associated text) requires an explicit representation of the companies and their dynamics in terms of a multi-agent system in which the processes take place by long chains of action and reaction between the various players. In fact the dynamic motion of companies forth and back between Hedge, Speculative, Ponzi and failed positions is at the very heart of the Minsky instability.

-

-

Thus Minsky had to construct his thinking on the basis of previous work that offered alternatives to the homogeneous, equilibrium, representative agent [Kirman 1992]:

-

a.

Keynes’ expectation dynamics under uncertainty .

-

b.

Hayek’s emphasis of the role of individuals in driving macroeconomic behavior.

-

c.

Schumpeter’s theory of innovation followed by creative destruction [Schumpeter 1936][Biondi 2008].

Minsky exposed his early views in a book entitled John Maynard Keynes [Minsky 1975]. Rather than attempting therein a scientific biography of Keynes, he used the Keynesian conceptual framework to emphasize the non-equilibrium, dynamical character of the economy and in particular the crucial role of uncertainty and individual subjective expectations in inducing fast changes in prices, values, production and employment. Following Keynes [Keynes 1937], Minsky endeavored to avoid in this way the difficulties that Hayek feared in deducing the dynamics of the economic system out of the behavior of individual agents. Hayek believed that in the absence of detailed information at the single agent and single transaction level, it would be impossible to deduce and even less to control, the emergence of market prices and dynamics. One critical issue in this debate has been coordination: Hayek renewed the classical wisdom that coordination of individual plans is impossible for a central planner, leaving coordination only to market(s), while Keynes and others argue against this received wisdom.

In Hayek, the only collective dimension is performed through the market, while Keynes introduced non-market coordination by governmental action among others. Keynes’ choice was to represent the macroscopic dynamics independently of an explicit microeconomic foundation. This was as a natural choice as the physicists’ choice (e.g. [Carnot 1890]) to use macroscopic thermodynamic concepts at a time when their atomic-molecular foundations were not yet available, neither empirically nor methodologically. Obviously, this comes at a price: the non-equilibrium aspects and the detailed description of the space and time transitions between various regimes are outside the reach of such a macro theory. Yet, as in the case of Carnot who devised thermal engines based only on macroscopic facts (e.g. that increasing temperature increases pressure) [Keynes 1937] was able to devise monetary and fiscal policies by which the economy regulators could steer the economic system out of depression and into full employment. He also described how these interventions can cause the growth or the transformation of the entire system. Thus, for crude macro-policy interventions in acute crisis conditions, Keynes’ attempts to circumvent the issue of micro-economic foundations was justified. Hayek’s despair of achieving a meaningful aggregation with the experimental and theoretical means of his time was justified as well.

Unfortunately this left the economic field largely at the mercy of naive aggregation in terms of representative agents which merely substituted the emergent complex collective dynamics by a copy of the mechanical behavior of a microeconomic ideal agent (additionally defaced by the assumptions of rationality, perfect knowledge or even perfect foreknowledge (cf. rational expectations theory [Lucas 1972])).

Minsky was left in the distinguished, but very limited, company of a minority that recognized bounded rationality [Simon 1997], non-equilibrium [Schumpeter 1928] and heterogeneity [Kirman 1992]. Most of the field continued to believe in Say’s wealth conservation, Walras equilibrium pricing, money neutrality and to ignore the role of debt financed investment. As recognized already by Minsky’s teacher [Schumpeter 1936], and by an increasing tide in the current literature (see e.g. [Biondi 2008]) the debt financed investment is a crucial factor in the capitalist economy. Unfortunately the mainstream economy had no place for Minsky’s disequilibrium ideas and no way to internalize this concepts: in the neoclassical frame of mind loans are just transfering the funds from individuals with less need for cash to individuals with more need for cash and are irrelevant at the macroeconomic level. One of the ambitions of the present paper is to express those Schumpeter-Minsky instability ideas in a format familiar from the study of equilibrium economic systems.

1.2 Role of solvable agent based models in the study of unstable economic systems

The novel capabilities to gather data at the resolution of individual agents and individual transactions as well as the statistical mechanics, field theory and complexity tools to extract non-trivial collective dynamics out of large sets of individual interactive agents, allow students at the present time to go beyond the positions that deny, in principle, the possibility for the regulators to steer the macroeconomic behavior. The original position expressed by Hayek, that there is no hope of reliably deducing from the myriads of microscopic acts a meaningful macroscopic collective dynamics, can be now re-evaluated. In the present paper we propose a way to re-address, from a positive perspective, the emergence of the macroeconomic collective phenomena from microeconomic individual interactions. We argue that the feature that can guide and give coherence and (to a degree) reproducibility to the connection between the micro and macro scales is autocatalyticity: the non-trivial structure of feedback loops that amplify the microeconomic individual events to systemic changes and reshape in turn individual behavior, according to the macroeconomic state.

In the last decade, the research bridging between the microeconomic basis and the emergent macroeconomic phenomena led to significant breakthroughs beyond the naive assumption that a collective of microscopic agents would behave as a single representative agent with properties similar to the typical individual. This has been discussed in the book “Microscopic Simulation of Financial Markets. From Investor Behavior to Market Phenomena” [LLS 2000]. However, initially the impression was created that the agent based models are tractable only by numerical methods, as can be seen from the comment of Harry Markowitz [Mark 2000]:

“Microscopic Simulation of Financial Markets points us towards the future of financial economics. If we restrict ourselves to models which can be solved analytically, we will be modelling for our mutual entertainment, not to maximize explanatory or predictive power.”

In fact the name “agent based modeling” became identified in the literature (mistakenly as we argue below) with computer simulations. The implicit hope in such a position was that using agent based models, which have all the necessary details at the microscopic level, the mechanisms and processes that govern the emergence of macroeconomic phenomena will reveal themselves in a direct and self-evident way. It might have been the case even that the mysterious invisible hand (as well as its trembling in market frictions and failures) would emerge from the multitude of individual actions and agents coordinated by market(s) and become visible in their simulations’ visualization and / or in their theoretical analysis. In particular, the access by modern electronic communication and information processing to the individual acts composing the global economic activity might have circumvented the difficulties that Hayek perceived at his time as forbidding the possibility to access and analyze the immense number of economic acts that compose the systemic economic dynamics. Those hopes were based on the success of similar scenarios played out during the last century in various other fields and notably in Physics. In the past it had been customary in many disciplines to formalize a collective of many similar objects in terms of a “mean field” or a “representative agent” characterized by the average of their individual properties and behavior. In reality such collectives may possess completely new properties and behavior than their components. In turn, they often constitute the elementary objects of a higher level of organization. The representative agent, mean field, continuum, linear way of thinking missed the higher level/order effects that are responsible for the emergence of life from chemistry, conscience from life, society from conscious individuals, etc [Holland 1992], [Lovelock 1979], [Gell-Mann 1994], [Prigogine 1997]. Understanding this connection between the elementary objects of one science and the collective phenomena overarching them allowed scientists to achieve many syntheses and insights and to overcome the obstacles that kept the classical sciences as isolated sub-cultures. Thus the possibility to go both empirically and theoretically to the individual economic agent level seemed a great opportunity to repeat in the economics field the great successes that physics achieved to understand the emergence of macroscopic phenomena and even to describe the conditions in which the macroscopic systems switch from one regime to another (e.g. phase transitions between solid and liquid or liquid and gas). A corresponding success in economics would be the understanding of the abrupt transition from the euphoria state to the panic state with a Minsky moment as the point of phase transition between the two.Richard Roll, former president of the American Finance Association and one of the leading research authorities in finance, gave a very optimistic evaluation of these prospects emerging from [Mark 2000]:

“This book contains the first fully comprehensive treatment of microscopic simulation in Finance. The authors make a compelling case that this technique originally used in physics to solve otherwise intractable problems, is destined to become a standard tool in finance.”

However it is not guaranteed that a method which worked well in the physical sciences applies with no change to the social, biological and human sciences. According to the Popperian paradigm, a scientific method has, on the one hand, to be able to make falsifiable statements: make nontrivial predictions that can be confronted with the empirical data. And on the other hand, according to Popper, “science is the art of systematic simplification”: scientific understanding means reducing the explanations of a phenomenon to a limited number of premises (Occam’s razor). The question is, whether this kind of oversimplification does not compromise the possibility to both understand phenomena of interest, and make reliable predictions. In the same way in which economists, witnessing a real life situation, might interpret it along very divergent narratives, the mere representation of a system in all its ‘micro’ details in the computer will not reveal automatically its salient features. In fact, a model with too many parameters to tune can predict anything – and thus nothing. If one has myriads of microscopic features it is very difficult to know which one is responsible for the macroscopic effects. By representing exactly in the computer a system, which one doesn’t understand, one ends up with two systems that one doesn’t understand: the original one and the computer model of it.

So, in order to validate complex, non-equilibrium theories such as Minsky’s, one has to look beyond computer simulations of agent based models. Minsky’s ideas suggest a generic way out of this dilemma: one should keep in the models only those individual features that are directly involved in the amplification of micro to macro. In the sequel, various models will be introduced; these will include only microscopic features involved in the process of amplification of microscopic individual events to macroscopic collective features. In this way, one still obtains the macroeconomic effects and the capability of making macroeconomic predictions applicable to policy recommendations, while not getting cluttered by the microscopic noise and the myriad of parameters related to it.

Thus the present paper, beyond the effort in describing in a precise way the Minsky’s financial instability scenario and its implications, has an additional methodological ambition: to emulate the success in the physics and the mathematics literature of treating multi-agent percolation processes by analytical methods [Stauffer 1985], [Grimmett 1999]. In fact our main tool will be the crucial relation Eq. 34 that relates analytically the density of susceptible agents in a network to the size of the contiguous clusters that they form.

However, the relation Eq. 34 by no means reduces the agent based network model to a continuous one: as in [Stauffer 1985], [Grimmett 1999], the discrete agent character will continue to show up in the large fluctuations in many aspects affecting the predictions and policy recommendations pertinent to steering the economic system. The discrete character of the agents is amplified in the phase transition parameter ranges to large variability in:

-

-

the fractal geometrical distribution of failures within the network of companies;

-

-

the intermittent fluctuation in the time sequence of failures;

-

-

the large non-self averaging variability between different realizations of the same or very similar systems.

In the following sections we will describe in detail the application of autocatalytic processes to economic systems.

2 Autocatalytic feedback mechanisms applied to economic systems

2.1 Background on Autocatalytic mechanisms

In modern terminology, Minsky’s proposal for understanding the instability and the crises of the complex capitalist economy is to identify and characterize the autocatalytic loops that destabilize it. In particular Minsky identified positive feedback loops that act between the global system level and its components at various scales. These autocatalytic loops are the filters that sort out the individual level events that may trigger a systemic catastrophe from those destined to drown in the noise of local, short lived perturbations. This implies that most of phenomena that make it to the macroscopic/systemic level do present, and are fuelled by, some kind of autocatalytic positive feedback loop. This fact was noticed in the past in many occasions and disciplines but in the absence of specific mechanisms that could explain it, it was often dismissed as incompatible with the ethos and ideology of scientific thinking. The ubiquity of such occurrences in so many fields (markets, economies, social organization, life, ecology, conscience, creativity) suggests an equally generic paradigm: in order to understand the emergence of collective behaviors in macroscopic systems, one has to find among the myriads of interactions and rules that govern their microscopic components, the ones that have the capability to generate autocatalytic feedback loops. It is only a behavior associated with such a positive feedback and autocatalytic loop that has the chance to be amplified to the macroscopic scale and to govern the system’s global dynamics.

In a series of models starting from heterogeneous interacting agents it has been found, using analytical, simulation and empirical methods, that indeed such positive feedback loops lead to the emergence of adaptive collective objects that change completely the dynamics of the system [Levy 1994], [LLS 2000], [Shnerb 2000], [Yaari 2009]. Thus, by generalizing the auto-catalysis concept one was able to explain how random microscopic elements may self-organize spontaneously into highly resilient localized collective objects and change dramatically the naively expected behavior of the system as a whole. Examples of such generalized autocatalytic mechanisms are: iterative contagion of neighbors (or business partners), proliferation (of successful entities under appropriate conditions), generation by such entities of the very conditions that produce them (or makes them grow), interactions between various aggregation levels within the system (individual events contributing to the general mood that encourage the further occurrence of such events) [Dover 2009], [Malcai 1999], [Yaari 2008].

One is led to the conclusion that the generic criterion that separates phenomena doomed to remain local and buried in the noise from phenomena destined to take over the system, is their positive feedback potential in its many guises and forms. In order to understand, predict and steer systemic changes one has to discover, identify and characterize the particular feedback loops that sustain and amplify them. These positive feedback mechanisms select just those sustainable emergent collective structures that possess such self-sustaining properties [Nowak 2010], [Cantono 2010]. The autocatalytic processes are responsible for many of the sudden changes that threaten the climate, the environment ecology, the social order, or the economic stability around the world. The emergence of new elements that trigger new autocatalytic loops in the system may highly and rapidly destabilize the current state of the system. The new elements may be attributed to external causes but often they are the unavoidable result of the intrinsic instability of the system [Biondi 2008].

Reflexivity

As mentioned above, the positive feedback / self-reinforcing loop – or the autocatalytic feedback loop as we will name it from now on – are not new concepts; one could write an entire monograph about their origins, history and the forms which they took at different times and places. One aspect, which became pre-eminent due to its relevance in the context of the latest global crises, is reflexivity. Reflexivity is a feedback loop between cause and effect in systems of self-conscious individuals. While the reflexivity concept has been known more recently in the context of evolutionary economics [Nelson 1982] and of rational expectations theory [Akerlof 2009], [Lodhia 2005] its roots are very old: The principle of reflexivity was perhaps first enunciated by William Thomas [Thomas 1923], [Thomas 1928]: “the situations that men define as true become true for them.” A particular aspect of reflexivity is the self-fulfilling prophecy – a prediction /prophecy that causes itself to become true, due to the positive feedback between belief and behavior. Karl Popper called the self-fulfilling prophecy the Oedipus effect [Popper 1976]:

“One of the ideas I had discussed in The Poverty of Historicism was the influence of a prediction upon the event predicted. I had called this the ‘Oedipus effect’, because the oracle played a most important role in the sequence of events which led to the fulfillment of its prophecy. …For a time I thought that the existence of the Oedipus effect distinguished the social from the natural sciences. But in biology, too — even in molecular biology — expectations often play a role in bringing about what has been expected.”

George Soros is an active promoter of the relevance of reflexivity to economics. For Soros [Soros 1987], if traders believe that prices will fall, they will sell – thus driving down prices, whereas if they believe prices will rise, they will buy – thereby driving prices up. As exposed in [Soros 2008], the central idea in his conceptual framework is

“that social events have a different structure from natural phenomena. In natural phenomena there is a causal chain that links one set of facts directly with the next. In human affairs the course of events is more complicated. Not only facts are involved but also the participants’ views and the interplay between them enters into the causal chain. There is a two-way connection between the facts and opinions prevailing at any moment in time: on the one hand participants seek to understand the situation (which includes both facts and opinions); on the other, they seek to influence the situation (which again includes both facts and opinions). The interplay between the cognitive and manipulative functions intrudes into the causal chain so that the chain does not lead directly from one set of facts to the next but reflects and affects the participants’ views. Since those views do not correspond to the facts, they introduce an element of [social] uncertainty into the course of events that is absent from natural phenomena. That element of uncertainty affects both the facts and the participants’ views.”

[Merton 1968] describes the emergence of a typical bank run: One day, a large number of customers come to the bank at once – the exact reason is never made clear, it could be a large statistical fluctuation. Customers, seeing so many others at the bank, begin to worry. False rumors spread that something is wrong with the bank and more customers rush to the bank to try to get some of their money out while they still can. The number of customers at the bank increases which in turn fuels the false rumors of the bank’s insolvency and upcoming failure, causing more customers to come and try to withdraw their money. The rumor of insolvency caused a sudden demand of withdrawal of too many customers, which could not be answered, causing the bank to become insolvent and declare bankruptcy. The rumoured prediction of a collapse led to its own fulfillment.

2.2 Minsky’s scenario and the role of ponzi units

Following Keynes, Minsky made an important point that the expectations and their dynamics are the strongest economic incentives and a driver for business cycles. Expectations play a central role in the precipitation of the crisis, as well as in the creation of the conditions which characterize financial fragility. According to Minsky’s theory of financial instability:

“Stability – even of an expansion – is destabilizing in that more adventuresome financing of investment pays off to the leaders, and others follow.” [Minsky 1975]

In other words, during a prolonged period of prosperity, the positive expectations which initially were resulting in a self-fulfilling prophecy (“success breeds daring”), at some point start (exogenously or endogenously) to be perceived – again in a self-fulfilling way (rationally justified or not) – as irrationally exuberant [Schiller 2006]. Expectations start then to diverge from the manipulative capabilities of individuals and therefore result in some initial occurrences of failures and bankruptcies. Such individual occurrences very rapidly lead to the change in expectations from positive to negative, triggering the precipitation of a crisis. The realization that the exuberance is irrational is not based on the microscopic experience of each of the individuals but rather on a global view of the system which is not available directly to the individuals. This explains the great delay and the unpredictable timing of the switch between the exuberant and panic moods and consequently the dramatic and sudden characteristics of the switch – the ‘Minsky moment’. In the year preceding the latest crisis, “the adventuresome financing of investment” led to unprecedented levels of leverage.

Following Minsky, [Biondi 2013] classifies economic entities into Hedge, Speculative or Ponzi finance positions using a cash-based financial analysis. He assumes that net cash flows from operations (cash earnings) fully cover both the interest charges and principal repayments in hedge positions, but only the interest charges in speculative positions, while they do not even fully cover the interest charges in ponzi positions. Accordingly, one can say that there was a multitude of companies (especially financial institutions) that, in search for increasing profits, became ‘speculative units’ before the crisis. Their financial solvability depended on the possibility to collateralise assets or refinance positions to cover principal repayments, because their net cash flows from operations did not enable such repayment. More seriously, those financial companies encounter, therefore, the risk of becoming ‘ponzi companies’: companies which cannot service the interest on their loans from their inflows from operations (cash earnings or earnings thereafter), being dependent on collateralisation, leveraging and market-dependent operations even to satisfy interest charges. Occasionally we shall call such companies in short ‘ponzi’ (we offer our apologies to the reader and to Mr. Ponzi [Ponzi 1935] for this crude short of hand).

Formally we define as ponzi a company which cannot pay the interest on its debt from its cash earnings (earnings, hereafter):

| (1) |

It would be useful in the next sections to use Eq. 1 to define the resilience of a company as the earnings to debt ratio.

| (2) |

With this definition, a company becomes a ‘ponzi unit’ at any moment if the interest rate increases to such an extent that it exceeds the company’s resilience:

| (3) |

Thus the difference between the value of the resilience of a company and the current interest rate (‘distance to ponzi status’),

| (4) |

is a crucial indicator of the failure susceptibility of a company to changes in the global mood and in particular in the interest rate.

The role of the Eqs. 3 and 4 is to connect the discrete qualitative conceptualization by the original Minsky classification with the real life quantitative continuous heterogeneous parameterization of companies in terms of their resilience. While the companies’ resiliences take naturally values in a continuous probability distribution, their comparison with the current interest rate, Eq. 3, provides a sharp criterion which separates in a discrete way the class of ponzi companies from the rest. Of course, this criterion is well defined at each given time. However, as described in detail in the next sections, the dynamics of the interest rate (depending in turn on the individual companies’ dynamics through Eq. 23) is continuously moving companies into and out of the ponzi status as part of the ‘Minsky accelerator’ dynamics.

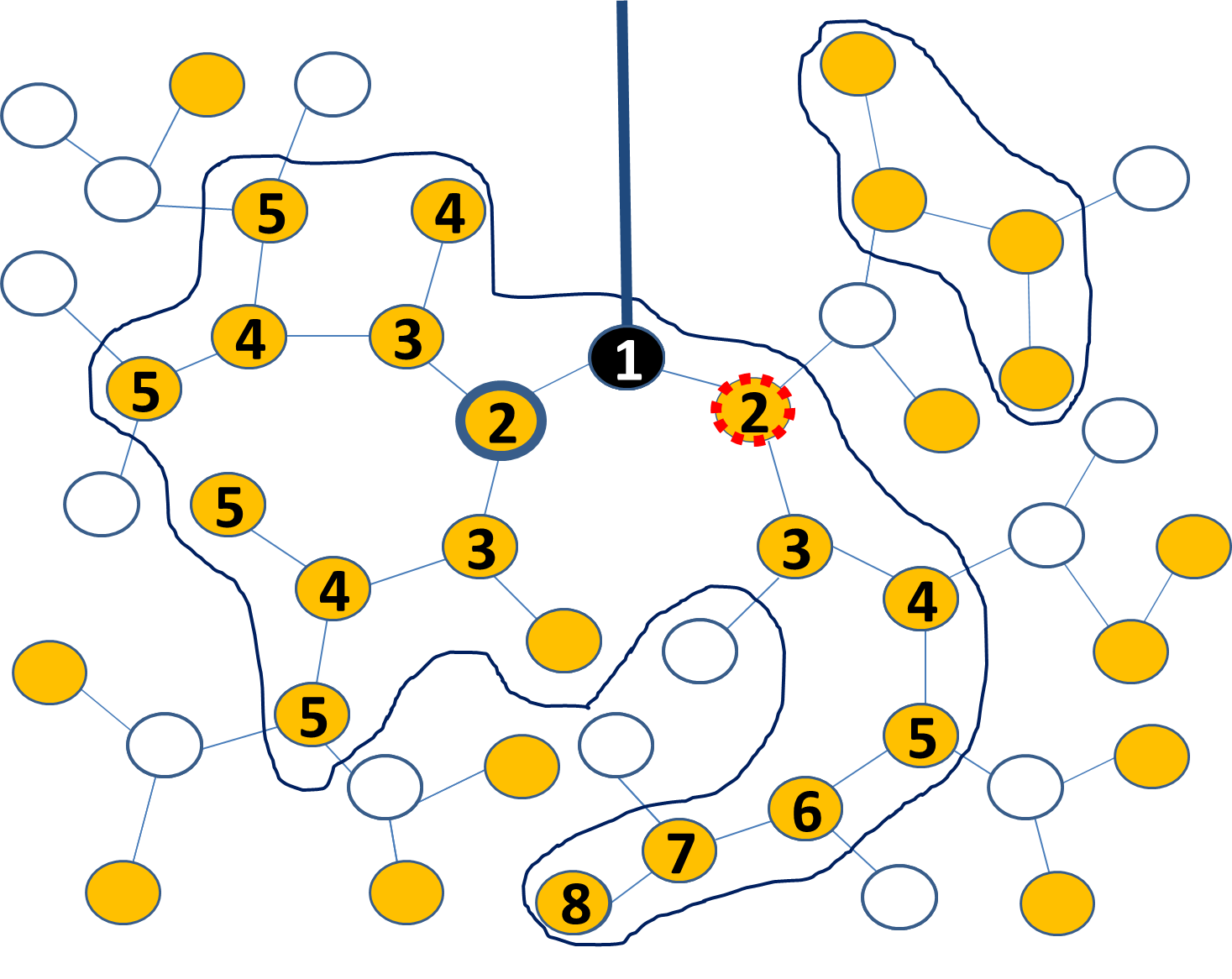

In the present paper we will occasionally distinguish between ponzi companies and failed companies. We will elaborate on this distinction as we progress in defining increasingly realistic models. The distinction is meant to reflect the empirical fact that many ponzi companies are not necessarily recognized as such by the other companies nor by the system as such. A well know example of this was the Madoff scheme where a ponzi unit acted for many years and it was treated as a perfectly healthy company. Only when external factors affected the company adversely, did its ponzi status become known, which influenced in turn the status of its creditors and the status of the system as such. Thus, in addition to the Minsky classification Hedge, Speculative and Ponzi, we introduce the ‘failed’, status which is a ponzi which is recognized and treated as such. In the same way as the ponzi status, the failed status may be reversible. Typically we will consider that a ponzi becomes a failed unit by contagion, when one of its partners has failed. Thus the differentiation between a simple ponzi and failed one is relevant in the network case when each company (node) has only a limited number of partners (nodes directly connected to it, as described in Sections 5 and 6).

In the case in which there are no network effects, as in Sections 3 and 4, one assumes that all companies are connected, and there will be no effective difference between the ponzi and failed statuses: a company will become failed as soon as it becomes ponzi. Thus in the non-network models of Sections 3 and 4, the debt-deflation phase is described in terms of a simple feedback loop: the increase in the interest rate causes many ponzi companies to fail which leads to an increase in the interest rate which in turn causes more speculative companies to become ponzi and fail, thus closing the feedback loop.

In the network based ‘Minsky accelerator percolation model’ described in Section 4, the ponzi status implies that the company is ‘susceptible”. More precisely, the company will fail iff any of its partners fails’. Thus in the percolation model one differentiates between the ‘susceptible’ or ponzi status of a company and the ‘contaminated’ or failed status, in which the company is recognized as ponzi by the system.

By ‘failure’ we do not necessarily mean bankruptcy, but rather serious distress and missed payments, i.e. a failure of a company to pay its debt obligations (default) which leads to sanctions by creditors and in particular to credit limitations by banks. The actions in the case of default could be the restructuring of the debt (extension of the due date and haircut for the debt repayment and the modification of the interest rate), or sometimes, the liquidation of all the assets. The mathematical relations connecting the interest rate to the number of ponzi and failed companies and quantifying thereby the Minsky accelerator will be introduced and discussed in Sections 4 and 5.

The ‘ponzi unit’ concept is crucial to Minsky’s theory of instability:

“An increase in the ratio of ponzi finance, so that it is no longer a rare event, is an indicator that the fragility of the financial structure is in danger zone for a debt-deflation.” Minsky (1986)

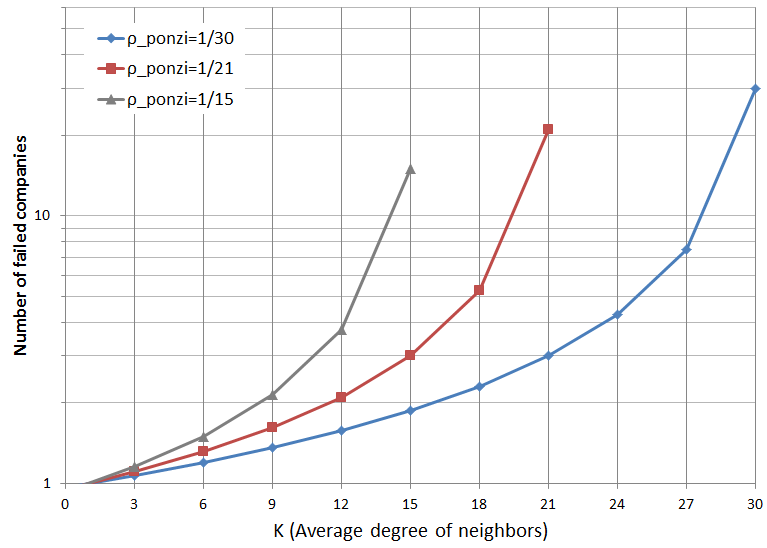

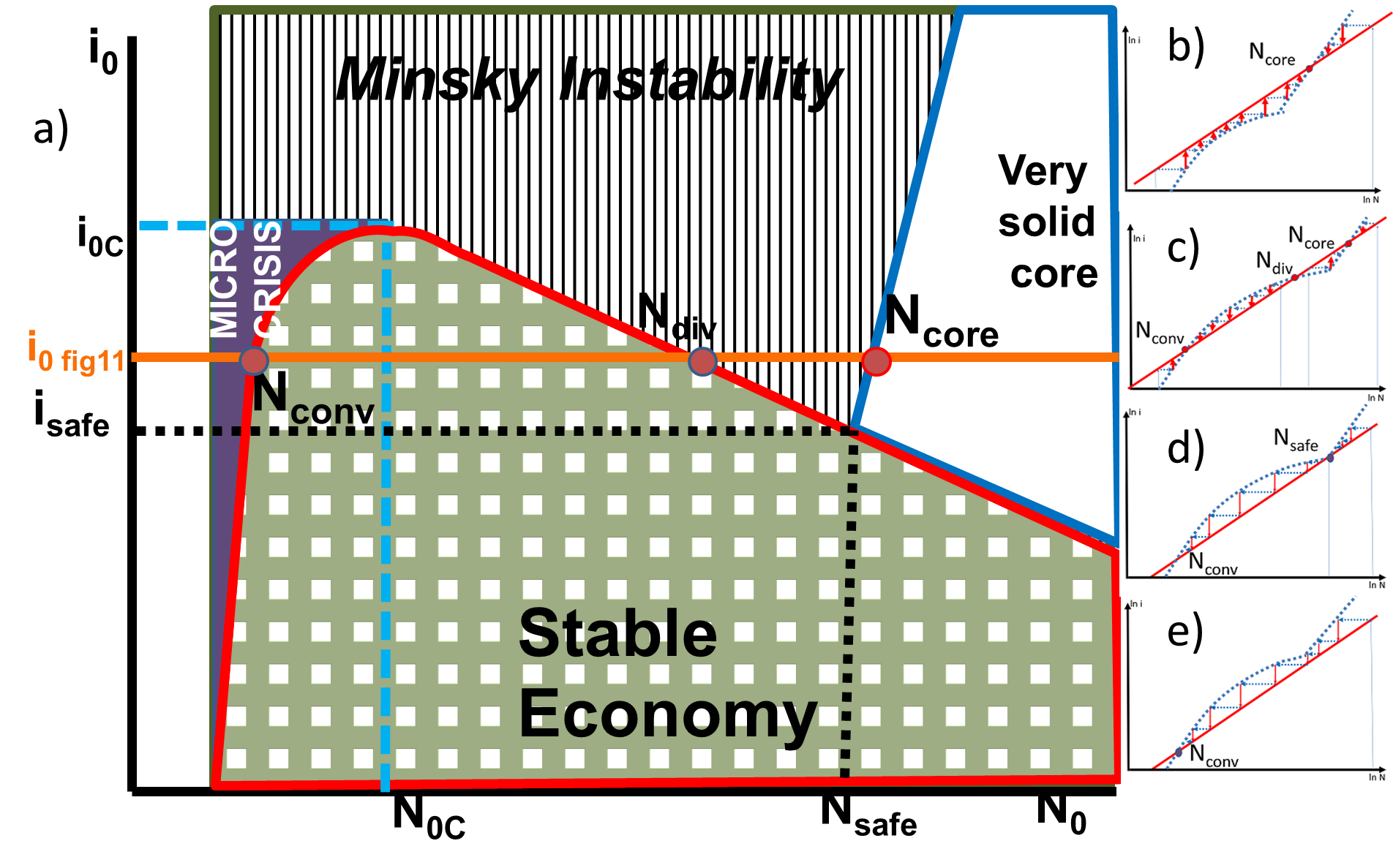

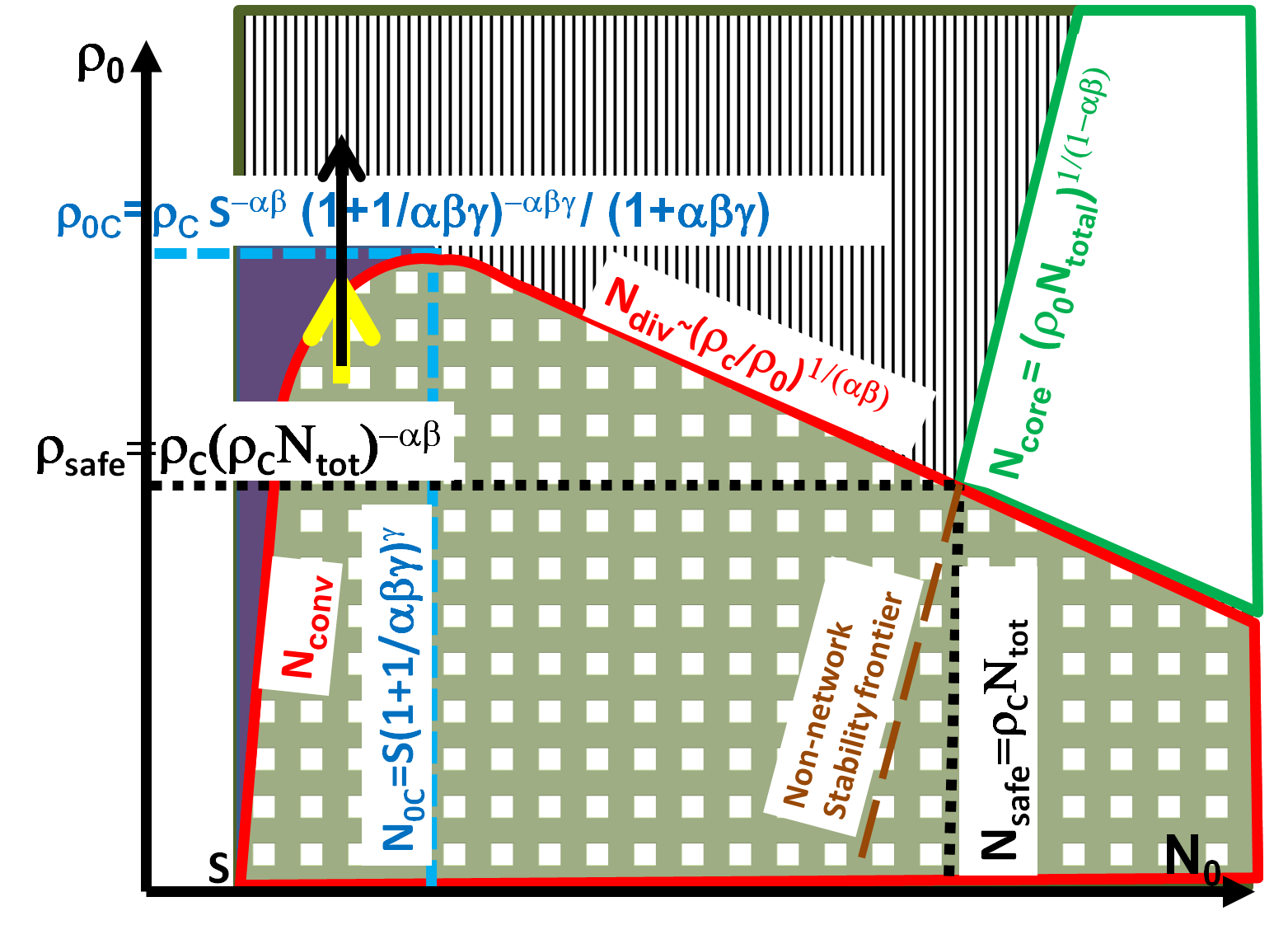

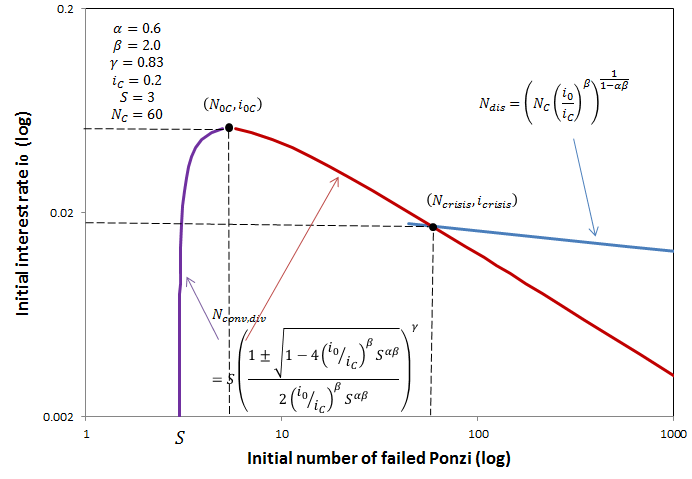

This Minsky vision came to happen during the great recession only too often: companies that increased their debt without increasing their earnings placed themselves in danger of becoming ponzi at the slightest increase in the interest rate. This has been central to the global financial crisis and its explanation (and suggested regulatory reforms) [Wray 2012], [Wray 2013]. Companies which incurred large leverage decreased their resilience and had difficulties to withstand the credit crunch. The interaction between the resilience in the macroeconomic context and the resilience of the microeconomic agent will be discussed in the subsequent sections. In particular in Figure 13 we cast our phase diagram describing the system susceptibility to a Minsky instability in terms of the density (fraction) of ponzi companies within the economy.

In addition to the usual Minsky crisis accelerator introduced in Section 4, we will discuss in the Section 3.3 the Minsky loans accelerator that characterizes the ‘exuberance phase’.

In the present paper we will formalize and study in detail the Minsky financial accelerator feedback loop by showing that there exists generically a critical fraction or density of ponzi companies above which the system becomes unstable. Congenial efforts to formalize the effect of over-leveraging on the global financial crisis and the network effects in the dynamics of systemic risk were offered in many recent works [Biondi 2005], [Stein 2011], [Adrian 2012]. In particular a model capturing these effects in a non-equilibrium context was presented in [Biondi 2012]. An agent-based model of socio-economic interaction-based phenomena and expectation formation (positive, negative or neutral) has been developed and studied in [Hohnisch 2005]. In that model, the swings between various market moods are explained in terms of the influence that the peer groups are exercising on each of their members. The approach of the collective as an entity has been advocated also in [Cantono 2010], [Cantono 2012], [Biondi 2005], [Biondi 2010].

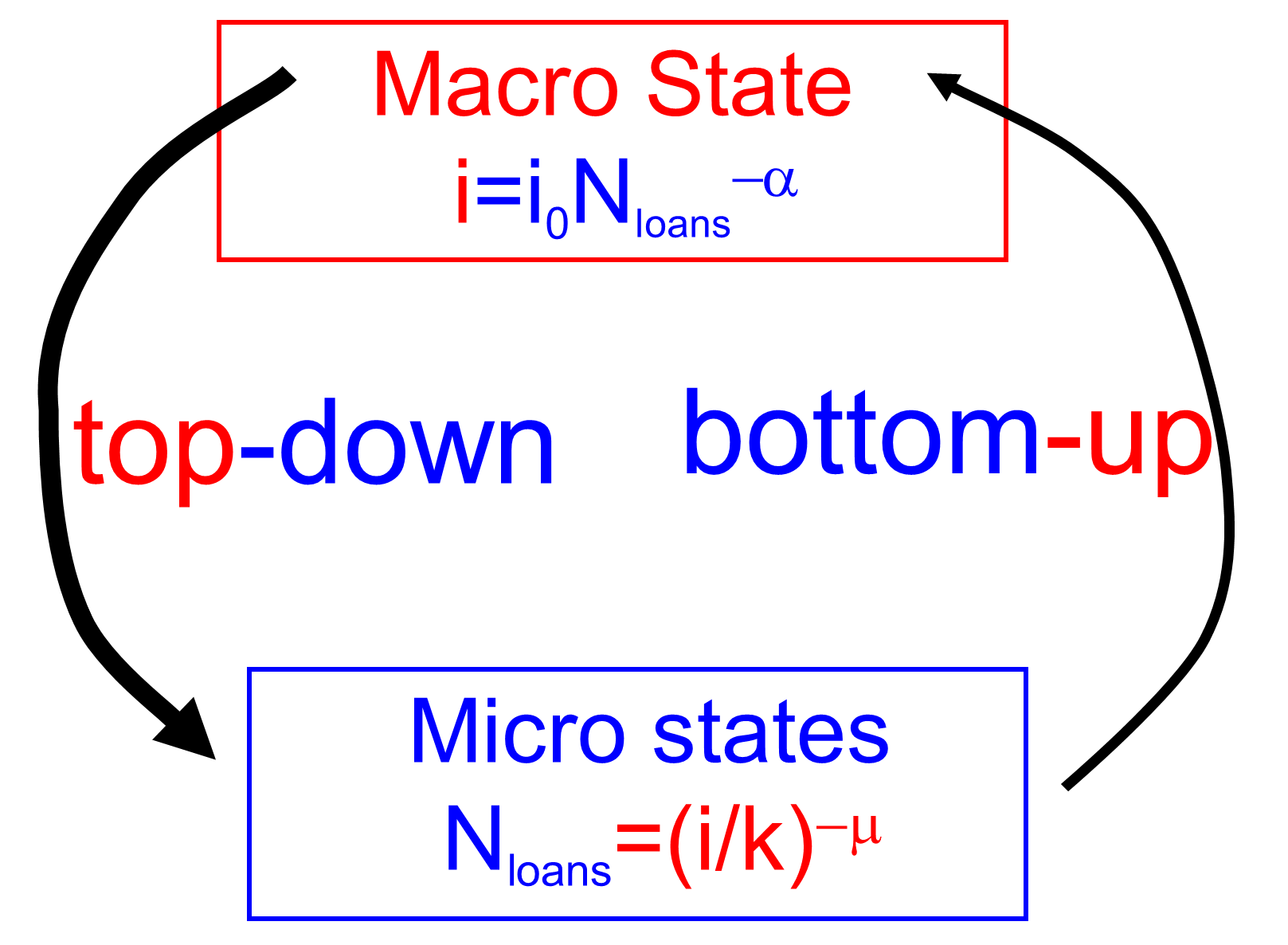

2.3 Connecting the Minsky Accelerator to the Marshall-Walras formalism

The price formation in neoclassical economics seems very distant or even contradictory to the kind of Minsky accelerator dynamics described in the previous section. Yet, in the following section, we will show that one can find formal connections which in turn might illuminate the kind of dynamics that precedes the Minsky moment and which takes, in the first place, the system away from equilibrium. We will treat the Minsky accelerator in a form that makes it quite similar to the Marshall-Walras formalism. More specifically, in the basic supply-demand diagram, on the y axis, instead of the price we will use the interest rate. The x axis will be different before and after the Minsky moment:

- -

- -

These formal parallels might seem artificial (especially the second) but they will emerge naturally from the mathematical processing of quite realistic assumptions.

This application of neoclassical concepts to Minsky’s ideas encounters two main obstacles that turn out to be more idiosyncratic than real:

-

-

using Marshall-Walras to describe run-away from equilibrium, rather then convergence to equilibrium;

-

-

treating, in the Marshall-Walras formalism, the amount of loans and the loan defaults as a production quantity.

Both items above seem at first sight to be in contradiction to the very basis of the neoclassical thinking:

-

-

the very motivation for Walras to invent the ‘tatonnement’ procedure and the quite similar market adjustments procedure by Marshall, was to substantiate Adam Smith’s insight that markets (prices and quantities) are brought to equilibrium by an ‘invisible hand’. Using it to demonstrate crisis and divergence from equilibrium seems the very opposite. It also seemingly goes against the ‘common sense’ view which suggests that the prices of the goods which are produced in excess will fall and the prices of the good for which demand is greater then supply, will rise.

-

-

in the neoclassical thinking, money is not production commodity (only exchanged: Say’s law) and even when new money is injected in an economy the reaction is (‘in the long term’) neutral (rational expectations).

However one should not get the impression that there are no precedents in the economic literature to the two ‘departures’ above:

-

-

for using the market mechanisms to obtain run-away from free-market equilibrium:

-

1.

the possibility, and in fact likelihood, that market equilibria can be unstable has been established by Sonnenschein-Mantel-Arrow-Debreu [Arrow 1954]. within the neoclassical framework;

-

2.

even the rational expectations idea has been introduced with the help of an example [Muth 1961]; of a divergence of the Walras procedure, which in fact happens for a very wide range of parameters;

-

3.

Veblen has introduced ideas in which the increase in the price increases demand, while

-

4.

the existence of economies with increasing returns (producing more costs less per product) has long been recognized (see for example [Arthur 1994]);

-

5.

the social positive feedbacks leading to herding and allowing demand to make large excursions out of equilibrium have been considered (see for example [Kirman 2010] [LLS 2000] [Solomon 2000]).

-

1.

-

-

For treating money or loans as a product, there was significant resistance because the conservation of money through the transactions within an economy has been one of the most efficient instruments to obtain useful theorems and models, starting with Say, through Hicks’ model and within the rational expectations theories. However, the use of Walras-like price-quantity diagram for interest rates and loans supply has been made in the past. For instance [Keen 2011] has emphasized that in addition to income earned by selling goods and services (which primarily finances consumption of goods and services and thus by and large conserves money), there exists the supply of money by banks in the context of entrepreneurial debt (which primarily finances investment) and in the context of rising ponzi debt (which primarily finances the purchase at increasing prices of existing assets).

A more significant departure from the neoclassical pattern is our analysis of the ‘Minsky crisis accelerator’ that takes place after the Minsky moment. The evolution of the ponzi density and the interest rate during this period occupies the bulk of the present paper. We will show that their dynamics mathematically parallels the Marshall-Walras feedback loop where, in order to find the equilibrium state, one equates:

-

-

the price per product offered by the suppliers as a function of the quantity of supplied products, with

-

-

the price per product for which the demand by the clients equals the same quantity of products.

The model based on the feedback loop between interest rate and ponzi failures will assume not only the autocatalytic loop between

-

-

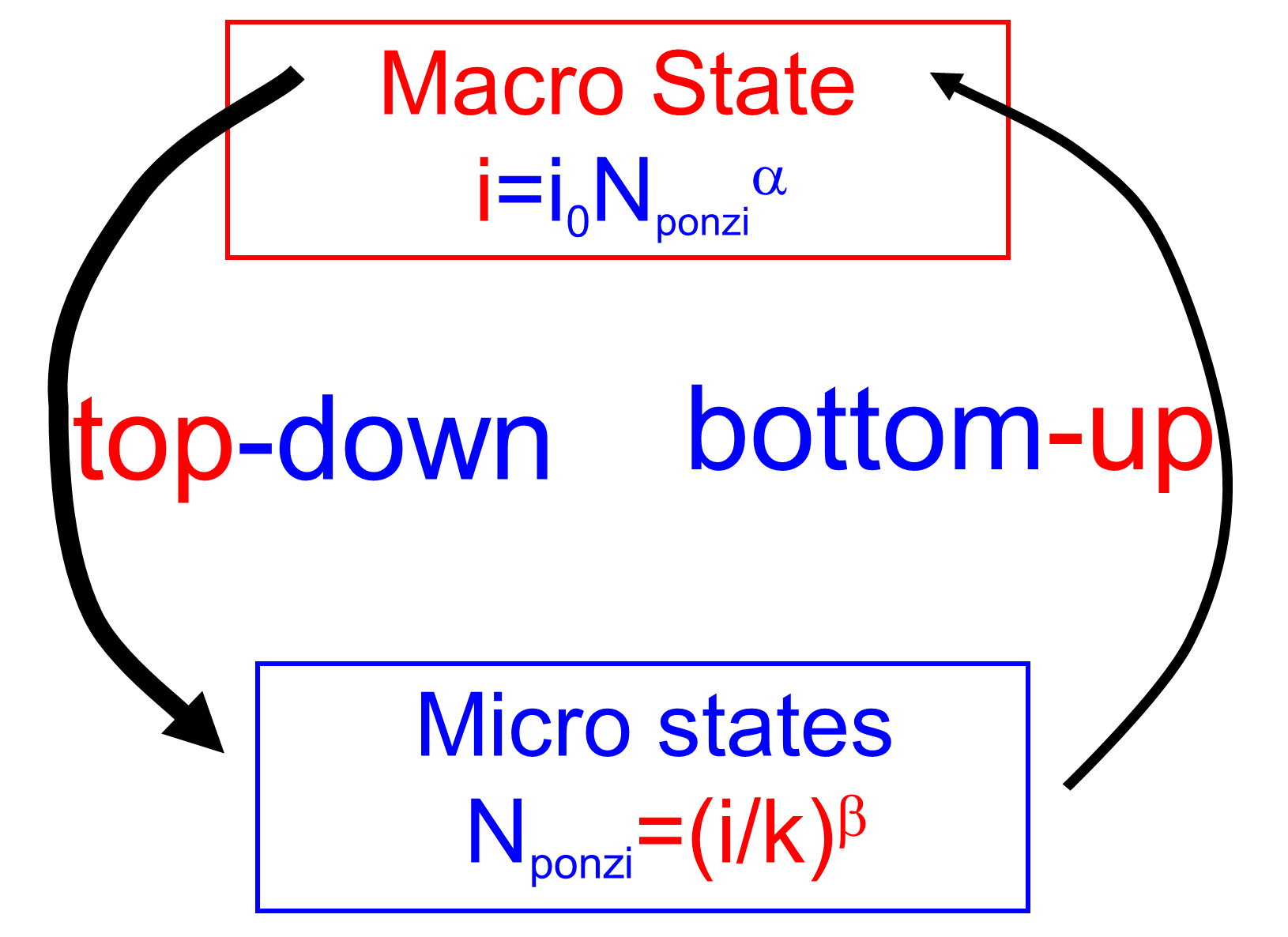

the bottom-up regulation (the influence of the quantity of ponzi companies on the interest rate offered by the lenders) and

-

-

the top-down feedback (the influence of the interest rate on the number of ponzi companies),

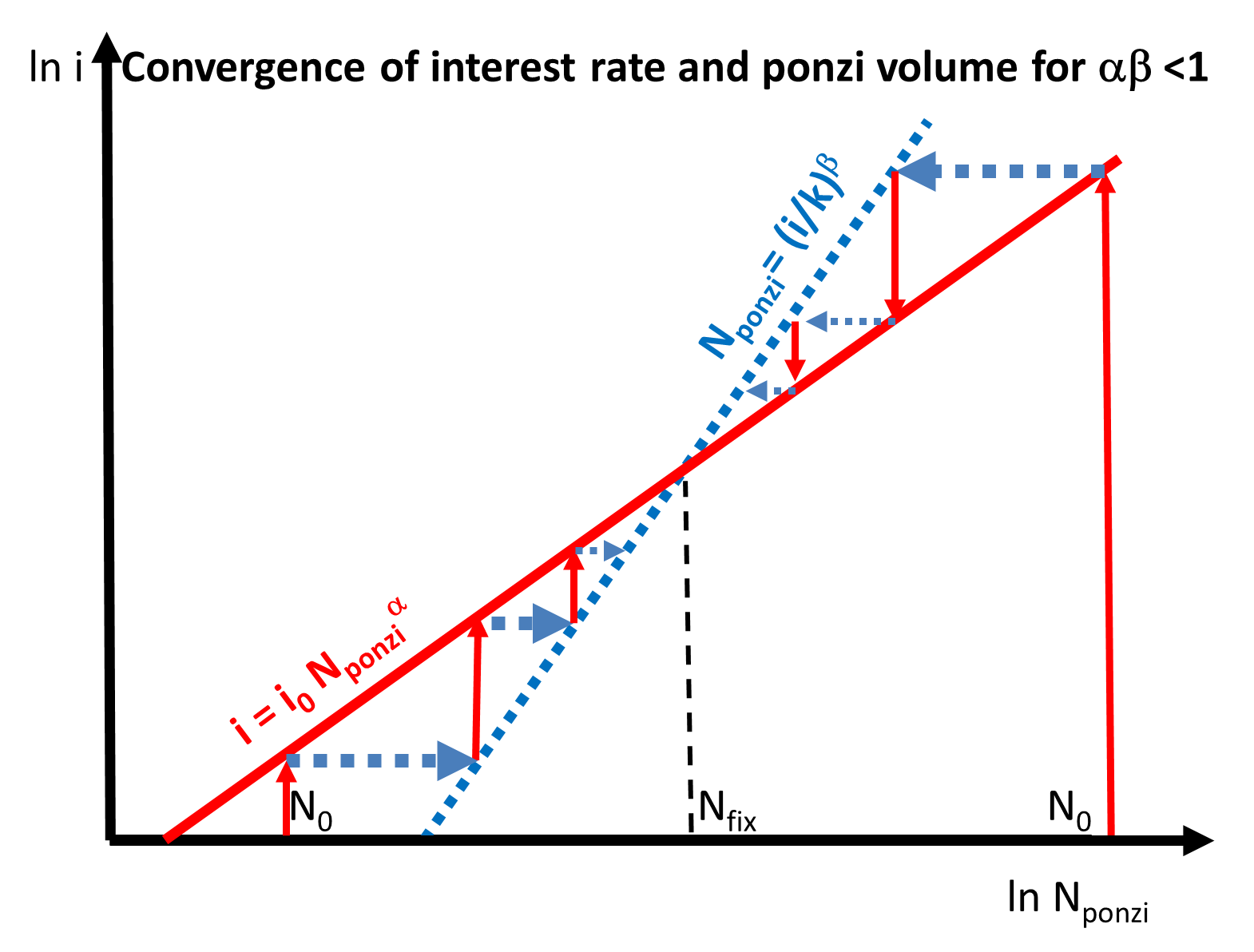

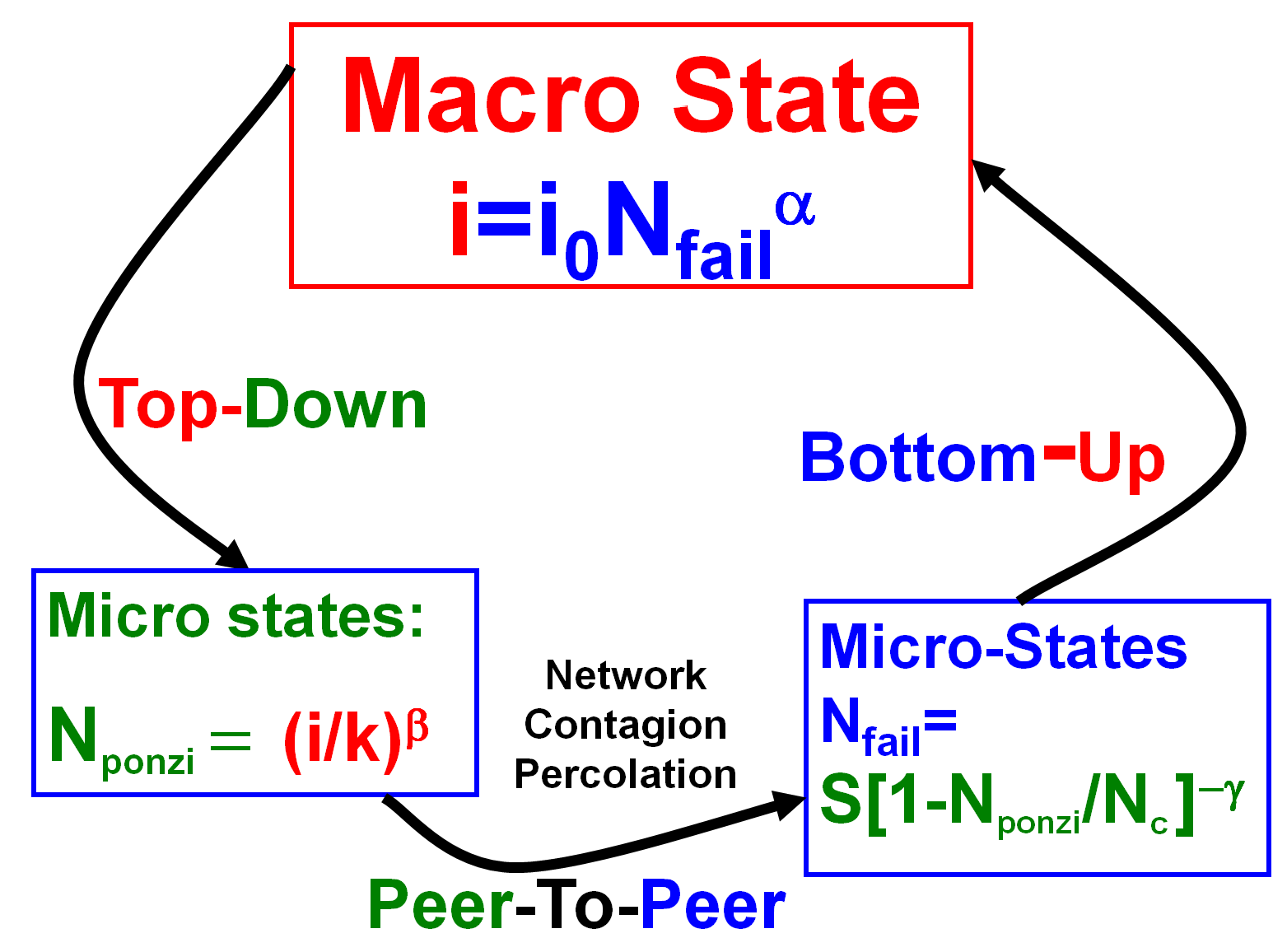

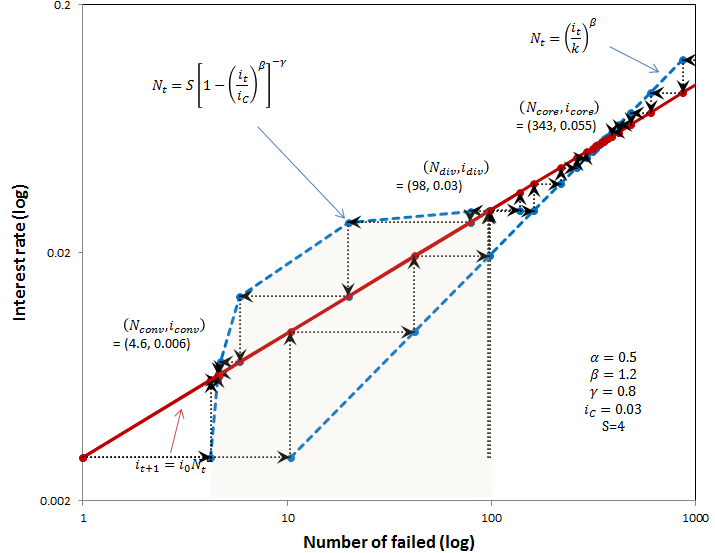

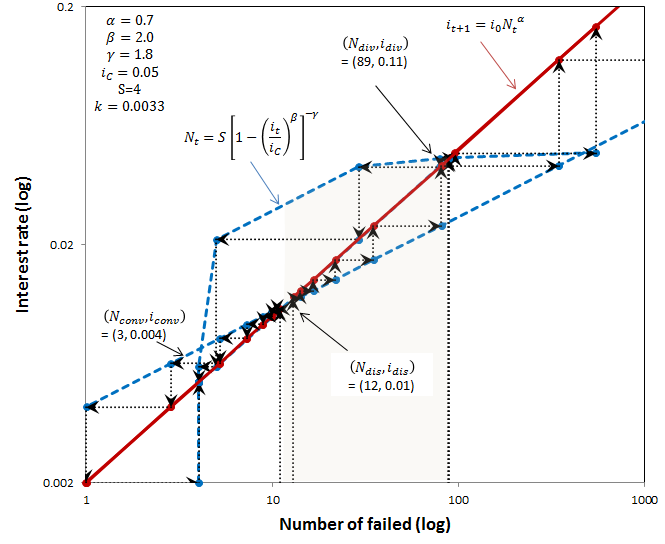

but it will also take into account the peer-to-peer interaction in terms of network effects. This will lead to a nontrivial configuration of stable and unstable fixed points Figure 11 and to a correspondingly complex phase diagrams as shown in Figures 12 and 13.

3 The Marshall-Walras price formation process applied to the interest rate and loans volume

3.1 The Marshall-Walras equilibrium in a loans market with decreasing returns

In neoclassical market equilibrium analysis, the formalism for finding fixed (equilibrium) states and establishing whether they are stable has been belabored for a long time, starting with Marshall and Walras and brought to mathematical perfection by Arrow-Debreu [Galor 2007]. In our case we are looking for equilibria (and the dynamics leading towards or away from them) which result from the dynamics of the interest rate. In the period preceding a Minsky moment, the relevant interaction is between the interest rate, , and the amount of loans outstanding, . In the period following the Minsky moment, the relevant interplay is between the number of ponzis, , and the interest rate, .

Let us first apply to the debt or loans market the Marshall-Walras method for price formation. We will discuss later its limitations and their important implications. The crucial assumptions are that:

-

-

The amount of loans demanded by the debtors, , is a decreasing function of the interest rate, , that they have to pay:

(5) where and are constants. This equation Eq. 5 implies that the number of loans increases as the interest rate decreases. This connection is also at the basis of the Hansen-Hicks IS-LM model of credit (money) supply. More precisely, the IS part of the model assumes that as the interest rate decreases, even investments with modest returns become lucrative because they can still give returns higher than the interest rate: one will do better by investing in a productive business than in keeping the money in the bank. Conversely, by borrowing money at very low interest one will gain even if one invests it in a modestly lucrative business. Thus the number of investments eligible for loans increases as the interest rate decreases. As the increase in investments leads to an increase in production (GDP) which establishes the neo-classical IS inverse connection between the interest rate and the GDP.

-

-

The interest rate, , that the banks are charging is an increasing function of the amount of loans, , they agree to supply. This is the famous law of decreasing returns. The argument is that the banks are charging an increasing price if their lending capacity is stretched up to or even beyond their limits, thus incurring a higher risk of default. We will discuss the realism of this assumption later. For the moment, we adopt this position and assume for definiteness that:

(6) where and are constants.

The power laws in Eqs. 5 and 6 have both empirical and theoretical justifications:

-

-

The square root rule of influence (corresponding to ) has been argued in social psychology by Wallacher and Nowak [Nowak 1998].

-

-

While the square root impact of orders on prices (corresponding to ) has been argued by Farmer at al, see [Farmer 2006].

-

-

A power law is the only functional form that is scale invariant. If the dynamics is not strongly influenced by other scales, it is natural to assume a power law behavior. In particular, the scale invariance can be connected in the context of pricing with the fact that the price behavior should be invariant to the monetary unit in which it is measured (a form of ‘money neutrality’).

However the results in the present paper are more general then the details of the power functional forms involved.

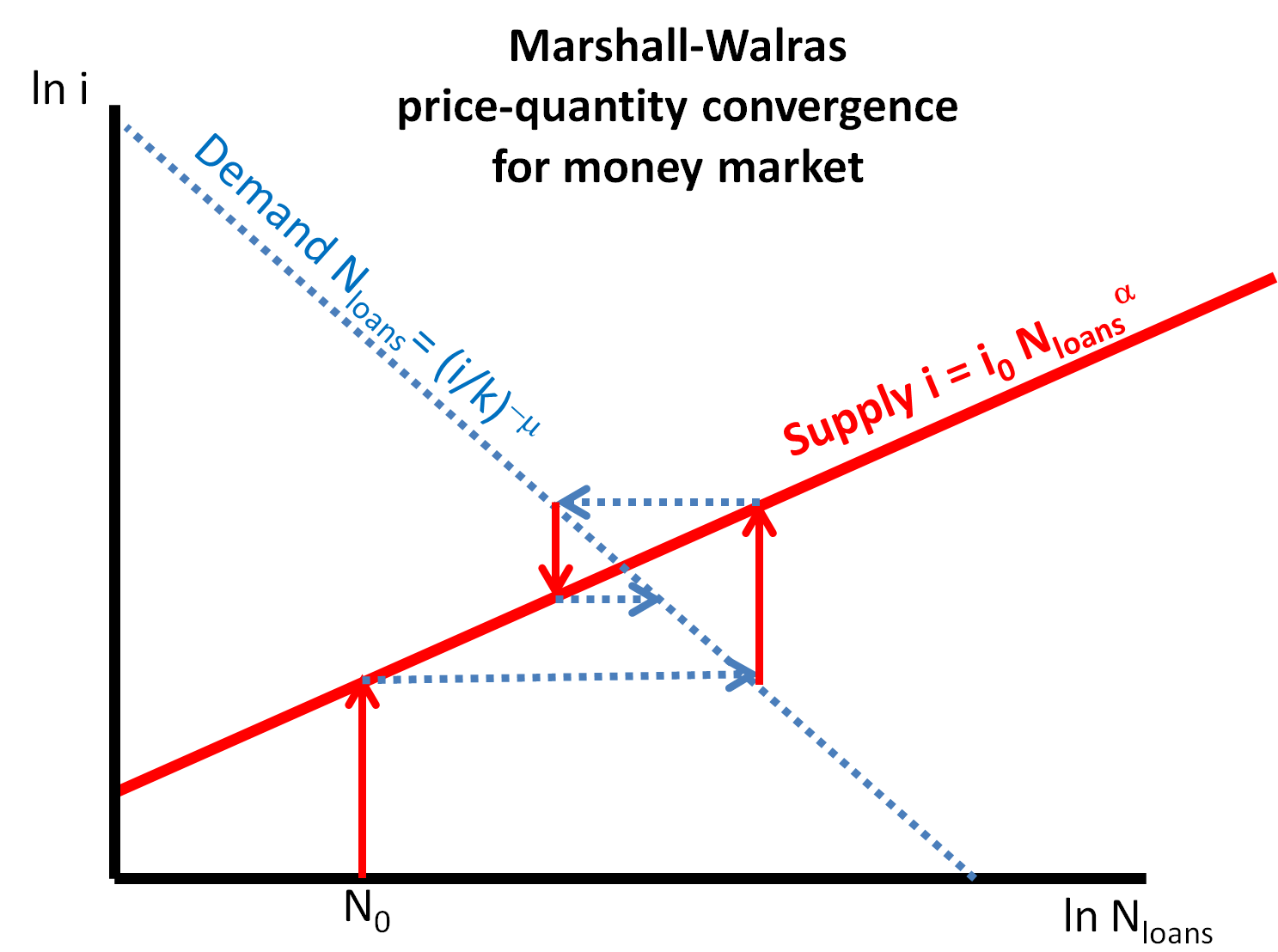

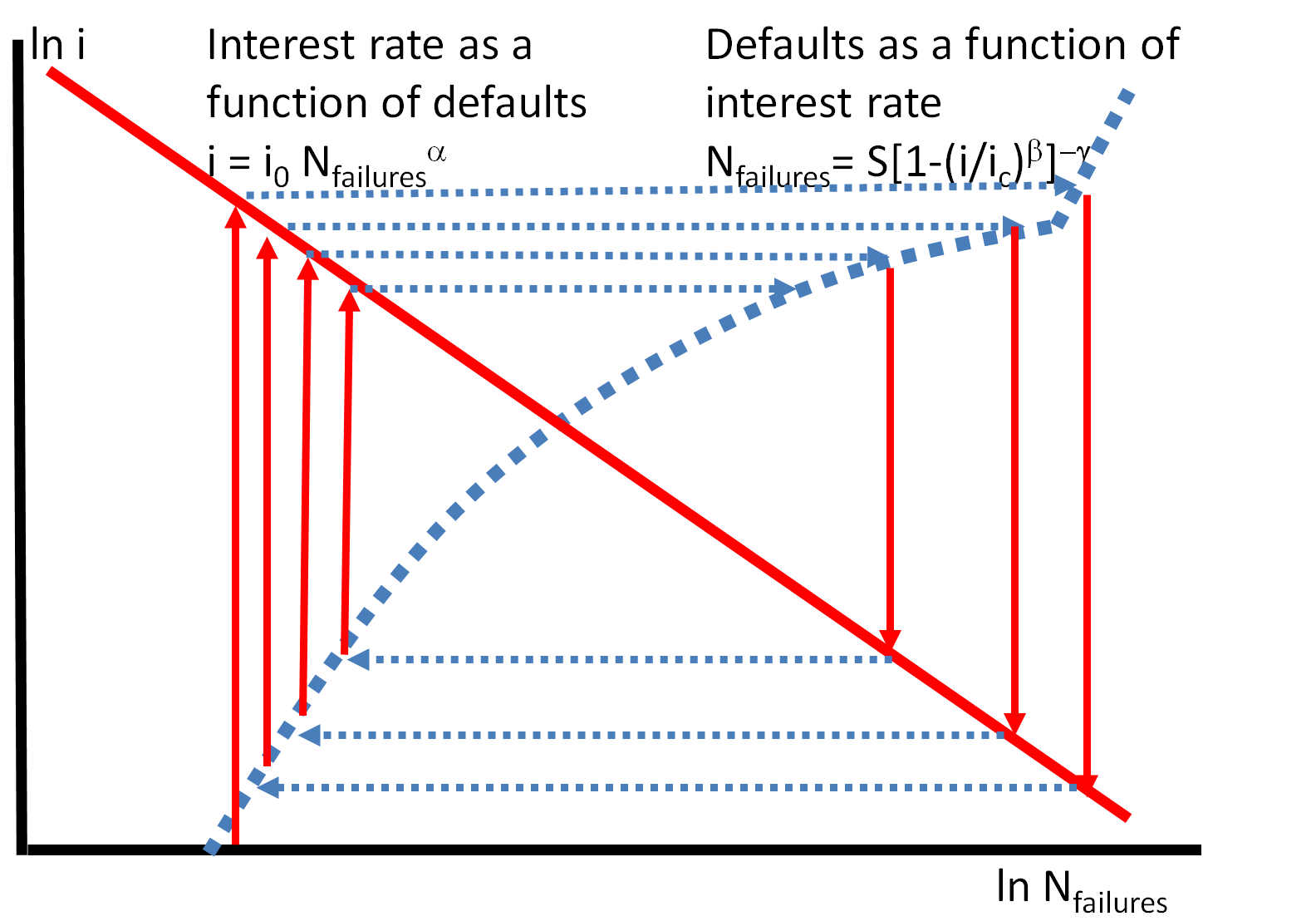

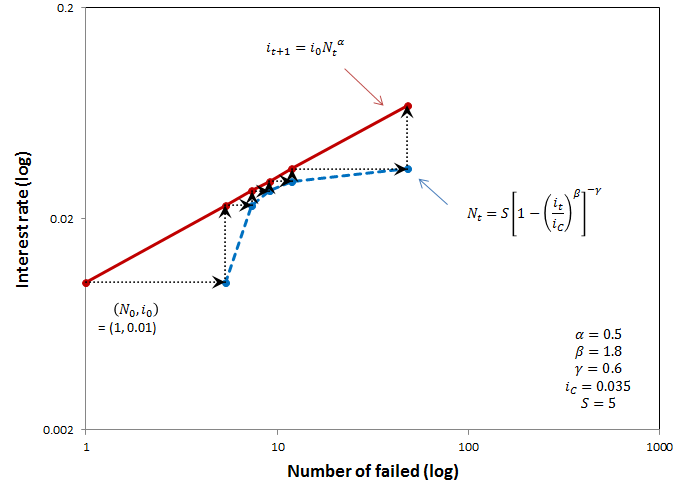

Marshall and Walras differed in the interpretation of the iterative procedure that may converge to the equilibrium point. While for Walras the iterative ‘tatonnement’ (‘tweaking’, ‘groping’) towards an equilibrium price, , and an equilibrium level of production, , took place in virtual time , Marshall considered the approach of the equilibrium as a genuine process in real time, , in which the supplier (in our case, the lender) reacted to the excess demand (in our case, of loans) by modifying the price (in our case, the interest rate) while the client (in our case, the debtor) reacted to the new price by modifying the quantity demanded:

| (7) |

| (8) |

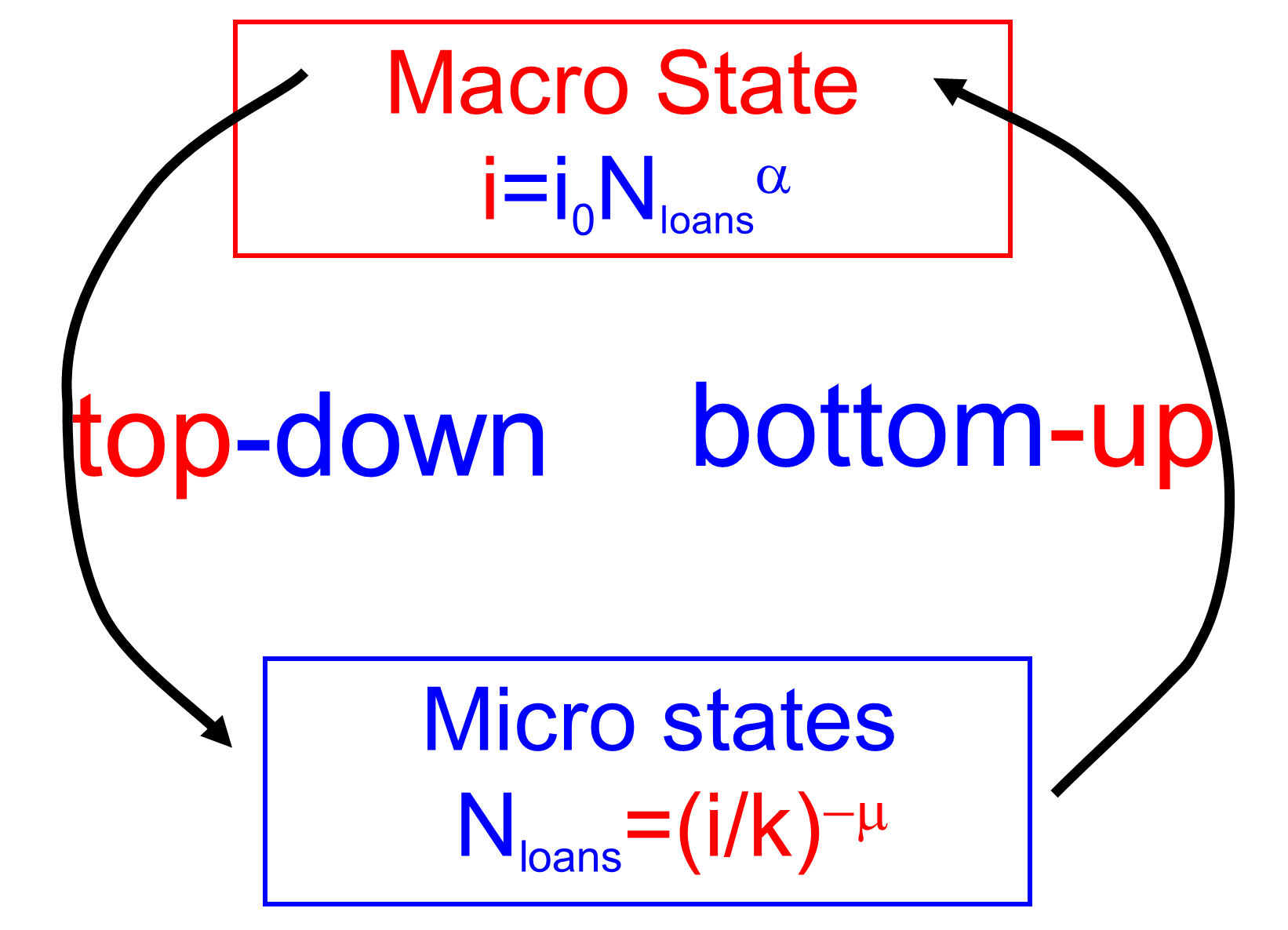

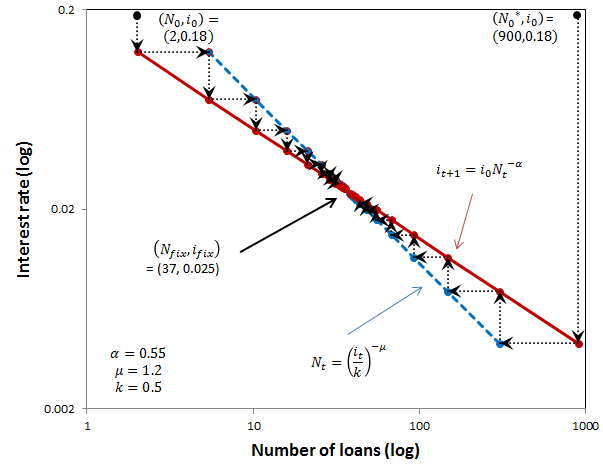

The equations 7 and 8 define a ‘top-down’ – ‘bottom-up’ feedback loop as shown in Figure 1(a).

Starting from a certain initial interest rate, , and an initial quantity of loans, , one triggers a ‘tatonnement’ chain reaction:

| (9) |

This iterative process is represented graphically in Figure 1(b):

-

-

each step is represented as a vertical arrow with coordinate equal to and ending on the curve given by Eq. 6;

-

-

each step is represented as a horizontal arrow with coordinate equal to and ending on the curve given by Eq. 5.

The equilibrium interest rate and loans quantity are then obtained as the common solution of the Eqs. 5 and 6, as seen in Figure 1(b):

| (10) | |||||

| (11) |

In the Appendix A the exact evolution of during this process is deduced:

| (12) |

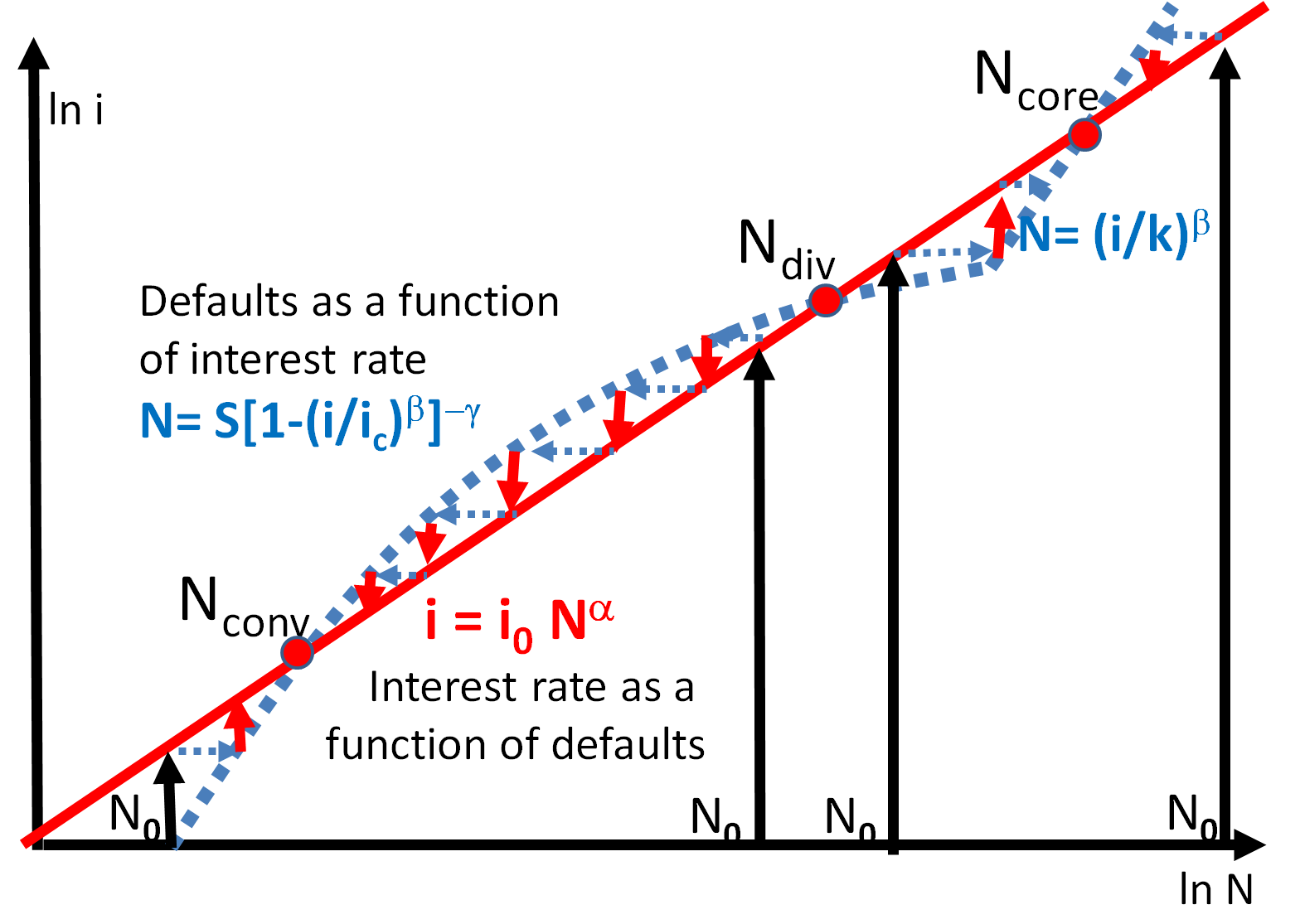

According to Eq. 12, for , since the exponent vanishes for , converges to . Thus, the Marshall-Walras process, Eq. 9, visualized in Figure 1(b), leads to the evolution of the number of loans, , given by Eq. 12, which converges to the stable fixed point, given in Eq. 11.

For , and both diverge to infinity, somewhat similar to the fears of the banks after the Lehman crash in September 2008. Yet, the convergence may still be achieved by modifying the details of the procedure. For instance, one could introduce smaller steps (say consisting of a fraction, ) instead of the full adjustment steps that overshoot the fixed point:

| (13) | |||||

| (14) |

Such solutions have been proposed in the past: [Kaldor 1934] (see especially pages 133-135) suggested that the adaptation of and takes place in small (individual transactions) steps (price/production stickiness) while [Muth 1961] assumed that the changes are performed by agents with foreknowledge or ‘rational expectations’. Another possibility could be:

| (15) |

The models Eqs. 13 - 15 are genuinely time-independent Markov processes, unlike Eq. 8 where the value of the interest rate at the beginning of the process, , is explicitly remembered throughout the process. However, this is not a problem for our models: they represent human reactions to specific events and moments, so singling out the initial value of the variables, , , is quite natural. E.g. the Minsky moment is definitely a memorable point of reference which the agents are quite naturally likely to remember throughout the crisis evolution. Thus, we will not pursue the models of the type Eqs. 13 - 15 here and will rather concentrate on models of the type Eqs. 7, 8.

The analysis in the present subsection is a paradigm which we will repeat in the next subsections and following sections, introducing increasingly realistic conditions. As envisaged in the general market equilibrium analysis of Sonnenschein-Mantel-Debreu, in the systems that we will consider, the generalization of the curves Eqs. 7 and 8 may have more (or less) than one intersection (common solution of Eqs. 5, 6) and neither a unique equilibrium interest rate, , nor even that the process stops at a given amount of loans, , will be guaranteed. A quite involved phase diagram will eventually emerge – Figure 12.

3.2 The Marshall-Walras equilibrium in loans market with increasing returns

In the previous section it was assumed that . This corresponds essentially the law of decreasing returns applied to the money market. It represents the assumption that the interest rate, , charged by the creditors increases with the quantity of loans, , that they supply. While the law of decreasing returns is often invoked in the neoclassical literature starting with Mills and Ricardo [Ricardo 1996], it applies less and less in the current economic conditions [Arthur 1994]. While it was more difficult to produce more apples from the same land area or to extract more coal from a mine that was already in use for some time, it is often easier to produce a computer or a copy of a program after one has already produced many units of it. However, the decreasing returns assumption is still often invoked in order to ensure market equilibrium, as indeed turned out to be the case in Figure 1(b).

As in many other cases, in the case of loans, modern conditions are conducive to a law of increasing returns: a bank that gave already many loans, has a lot of assets (the loans and their interest) which are also diversified over many debtors. Thus it is well insured against occasional creditor defaults. Therefore, it can afford to allocate more loans to more clients at lower interest rates. On the contrary, a bank with few loans has less assets and less diversification and has to charge a higher interest rate in order to protect itself against occasional defaults. Increasing returns has been recognized in the last decades both as a daily occurrence in the empirical economic reality and also as a significant factor determining the departures of the real life from neoclassical economic theory [Arthur 1994]. Moreover as detailed in [Biondi 2005] bank entities differ from markets in a way that makes the banking sector one of the sectors most likely to be affected by the factors leading to economies of scale because of its specific economic organization and specific features:

-

-

economies of knowledge (learning by doing, aggregating information from scale and variety of operations)

-

-

overheads split across various clients (leading to diminishing average and marginal costs)

-

-

implicit public guarantees for bigger entities (too big too fail), etc.

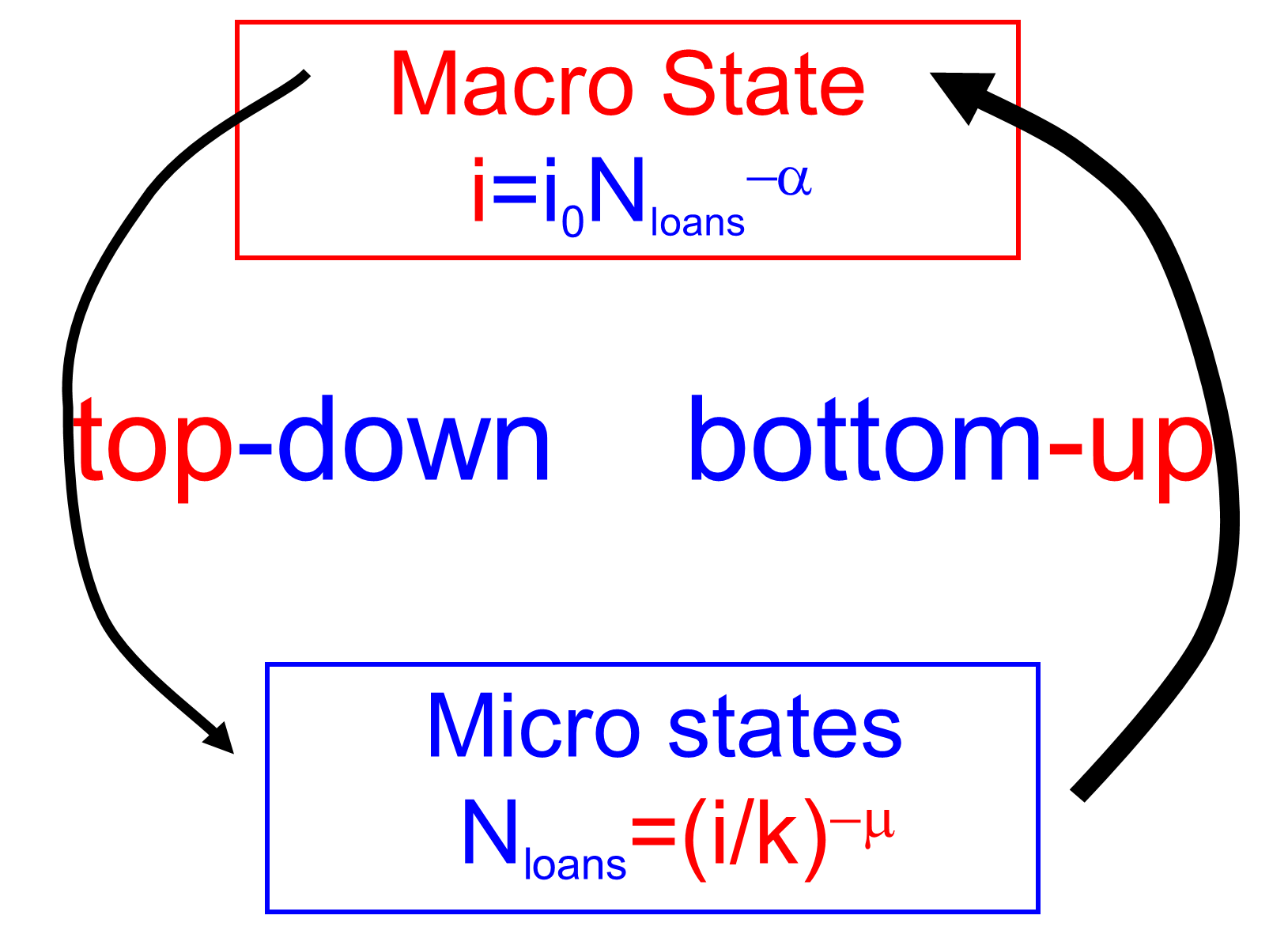

Thus, instead of Eq. 6 one is lead to study the case of a supply curve where the interest rate, , decreases with the quantity of loans, :

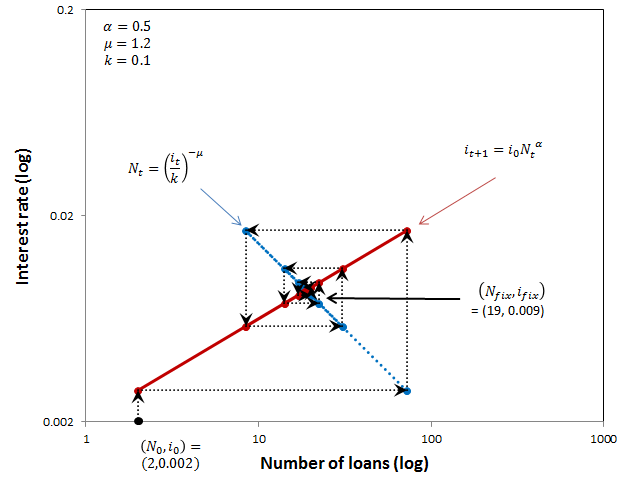

| (16) |

as exemplified in Figure 2(b). In the case of increasing returns, Eqs. 7 and 8 become:

The process of their coevolution, iteratively over time, is:

| (17) |

The amount of outstanding loans at any one time is (see Appendix B for the derivation):

| (18) |

where the fixed point is defined as the intersection between the two curves, Eqs. 16 and 5:

| (19) | |||||

| (20) |

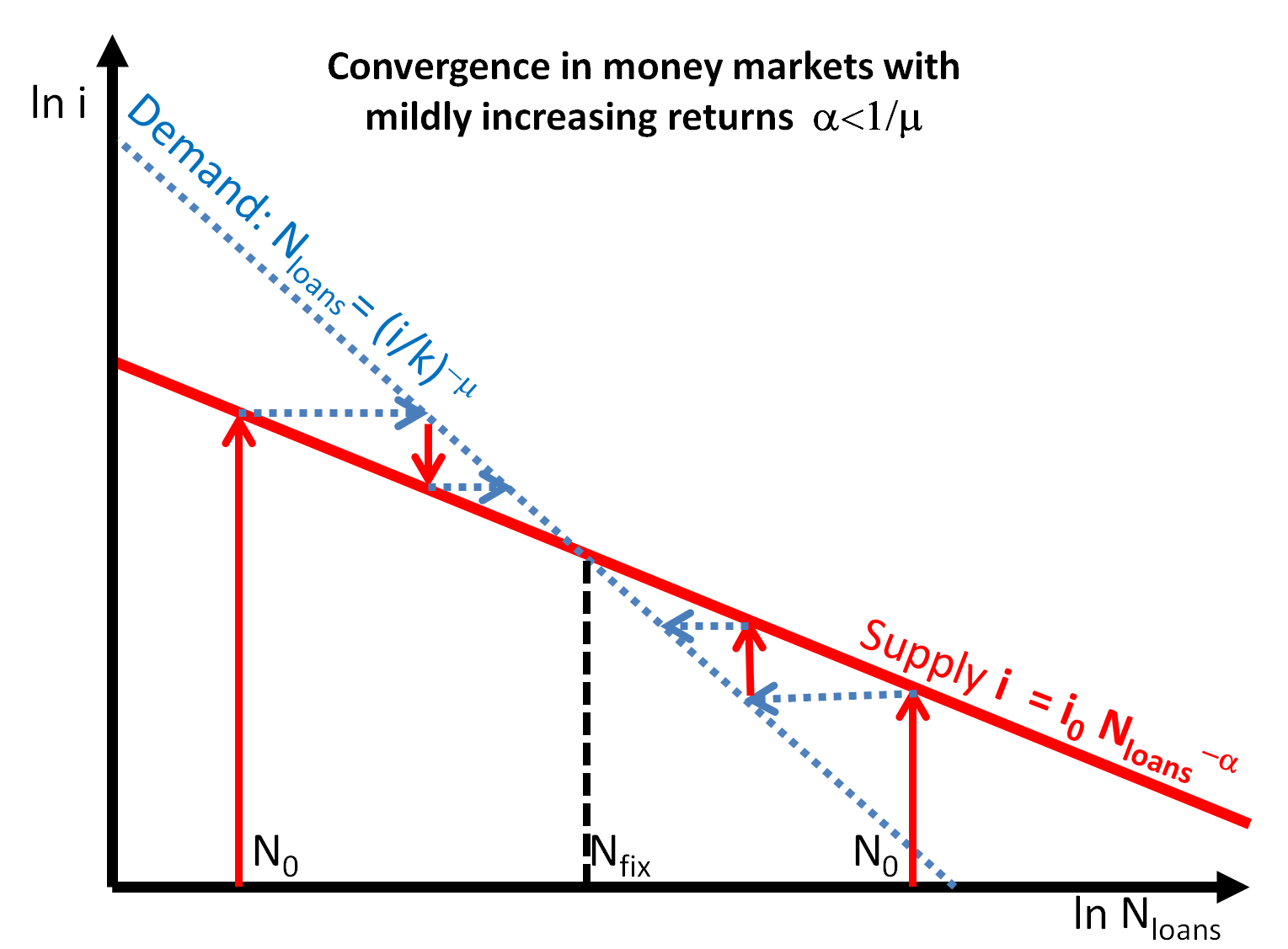

As opposed to the decreasing returns case (Eqs. 10, 11) the convergence condition cannot be circumvented by small step modifications of the type given in Eqs. 13, 14. Indeed, if the Eq. 18 converges in the limit to since the exponent . However for , instead of oscilating between and , as in the previous case Eq. 12 where the exponent oscillated between and , one has now a monotonic behavior because . Thus, if the initial point is less then , one has in Eq 18 a quantity less then at the power which converges to . On the contrary, if , then one has in Eq. 18 a quantity larger then at the power which diverges to .

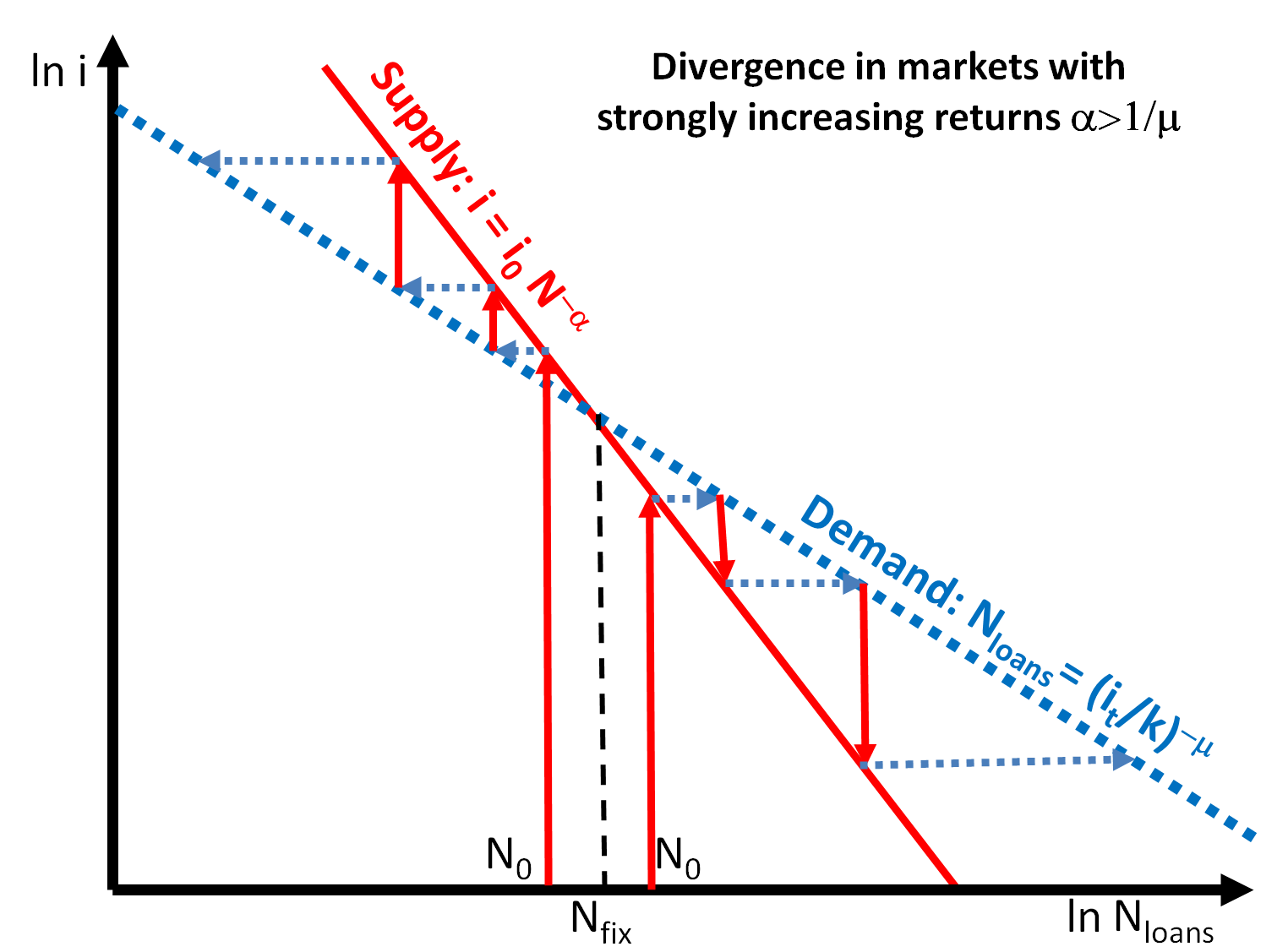

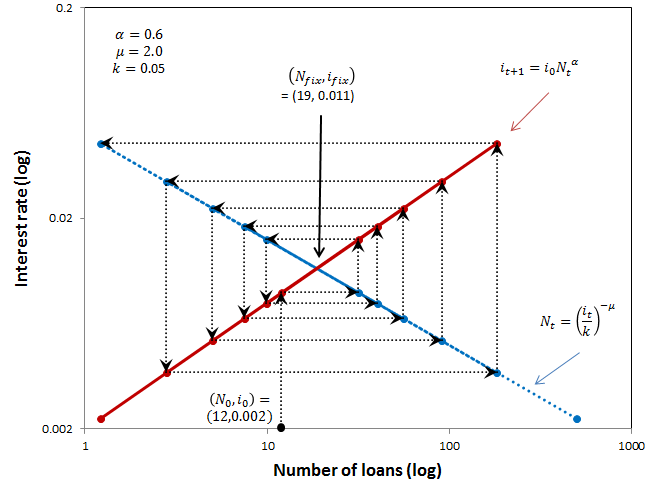

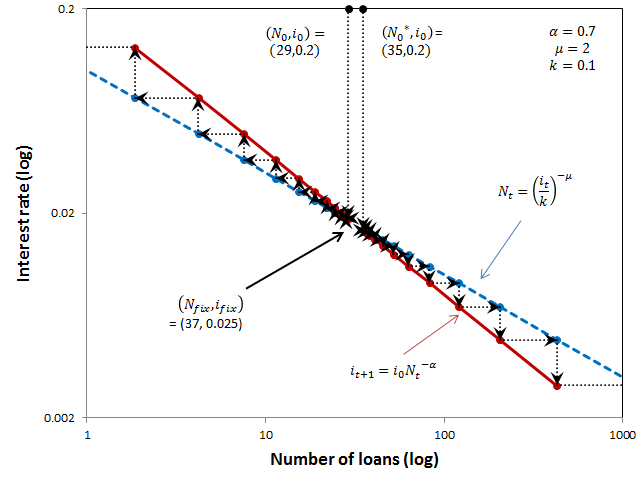

Thus we conclude that a genuine instability occurs at if the interest rate offered by the banks decreases with the volume of loans Eq. 3.2 faster than the decrease in the interest rate sufficient to insure an increase in the loans demand (), Eq. 7. This case is analyzed in the next subsection. The difference between the stable and unstable loan market with increasing returns can be best understood graphically by comparing Figures 2(b) and 3(b), where, on a double logarithmic scale graph:

-

-

the function is represented by a straight line of slope ;

-

-

while the function is represented by a straight line of slope because corresponds to the horizontal x axis while is measured on the vertical y axis.

The evolution of the iterative process , is represented by arrows. Following the arrows in Figures 2(b) and 3(b), one can see that:

-

-

if , i.e. the slope of is steeper then the slope of the process converges to the fixed point;

-

-

if, on the contrary, the slope of is steeper then the slope of , as in Figure 3(b), then the fixed point is unstable (repulsive).

The generic condition for the convergence and stability of a fix point of a discrete dynamical system is (cf. [Galor 2007]):

| (21) |

We will use this inequality in the rest of this paper and especially in obtaining the phase diagrams in the non-linear case with multiple fixed points given by Figs. 11, 12; not only does this criterion help establish the direction of the iterative process in the neighbourhood of the fixed points, but it also helps identify the character and the evolution of the process in the entire parameter intervals between the fixed points. In fact they correspond to the various phases (stable or unstable) of the system.

The formal convergence condition Eq. 21 is visually and more intuitively enforced in the various diagrams of the type shown in Figure 2(b), by just following the arrows that represent graphically the iterations of the process 17: horizontal arrows bring the process from to the corresponding while the vertical arrows advance the process from to .

More specifically, in Figure 2(b) the chains of arrows are pointing towards the stable fixed point, indicating that the process is converging towards it irrespective of on which side of it one starts. On the contrary, in Figure 3(b) the chains of arrows point away from unstable fixed point such that starting slightly above or below the fixed point, the distance to it increases as the process advances. Automatically this means that the entire interval between two fixed points (e.g. Figure 11) has a uniform behavior – it constitutes one phase of the system; irrespective of where one starts within that interval, the process will converge towards the stable fixed point and run away from the unstable fixed point.

3.3 The Rational of Irrational Exuberance

3.3.1 The Loans Accelerator

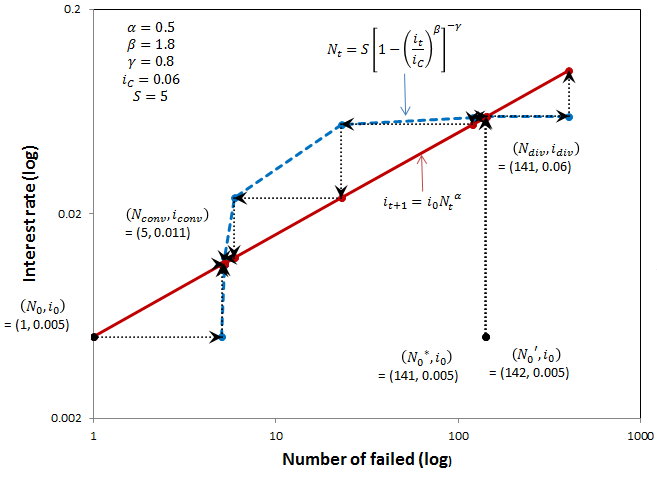

The Minsky vision of intrinsic instability has been perceived by both supporters and adversaries as incompatible with the mainstream neoclassical tradition. As in many other cases (Keynes, Schumpeter, etc.), the incompatibility is mainly in the minds of the researchers rather than in the actual mathematical hard core or the methodology. The instability is clearly singled out as the default rather then the outlier in the Sonnenschein-Mantel-Arrow-Debreu analyses. Concentrating on the convergent cases is only a particular choice which was (too) often made in the past. In the present sub-section we will use a Marshall-Walras neoclassical-like analysis to substantiate Minsky’s point that instability is a natural condition for a capitalist regime. In fact to obtain it, one only has to consider the case in the analysis of the previous sub-section.

In this case, the process Eq. 17 diverges because in Eq. 18 the exponent, , instead of vanishing for , diverges . Thus

-

-

for an initial , Eq. 18 implies . Of course for a finite number of agents , the process 17 will rather stop at 111As discussed below, the finiteness of may bring upon the Minsky moment: the Minsky loan accelerator is relying on the expectations that one may continue indefinitely to make loan-financed investments and pay the interests from the earnings. The finiteness of the economy means that at some stage the investments would exceed the capacity of the market to buy and will not give the returns necessary to pay the interest on the loans. This will push some of the most aggressive investors in a Ponzi position and trigger the Minsky moment..

-

-

for an initial , Eq. 18 implies .

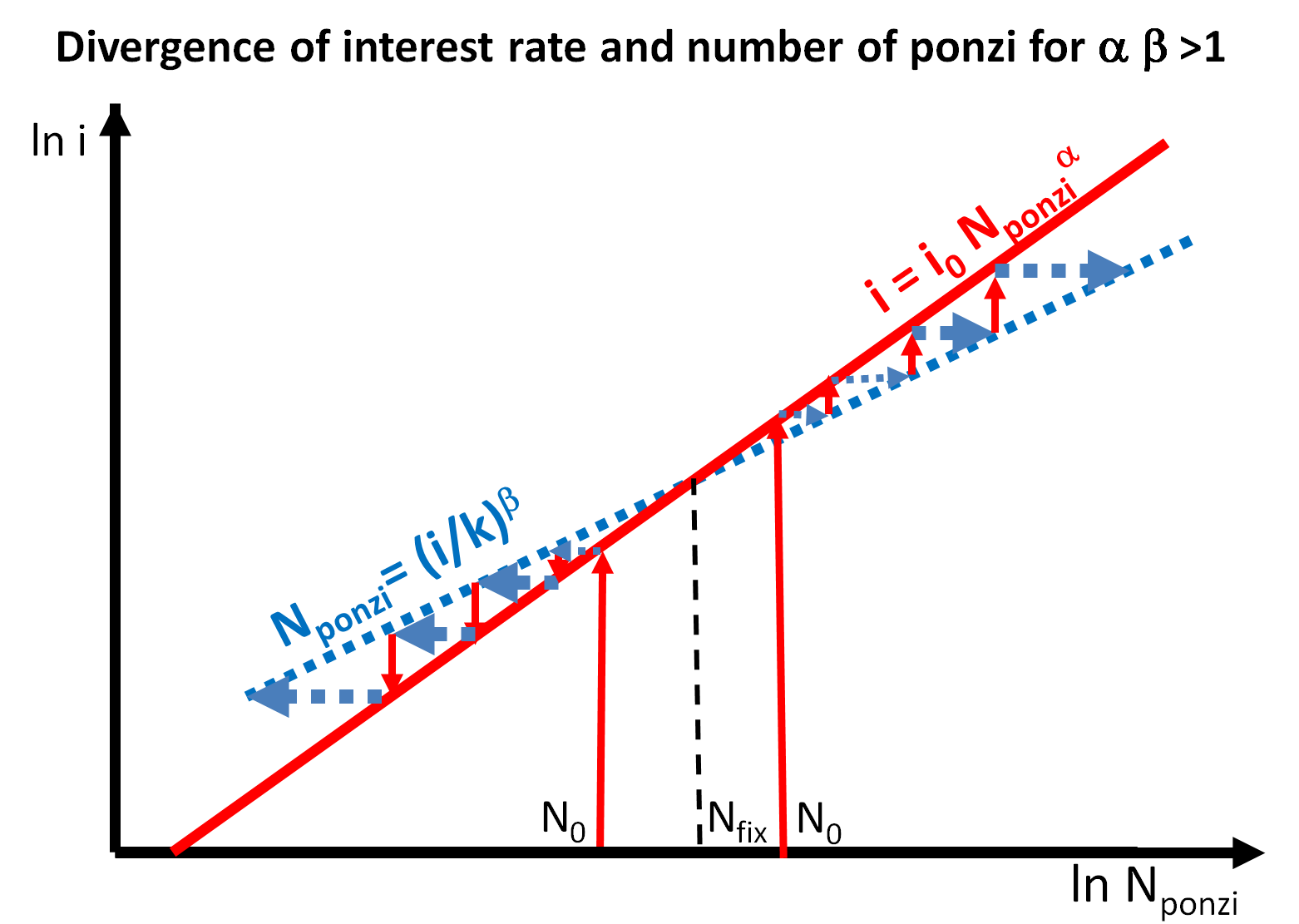

Thus, in the case , the fixed point becomes repulsive. Graphically this is seen in Figure 3(b), where, starting at points very close to (slightly above or slightly below) , leads to (and ) evolving in opposite directions, towards or , respectively. Figure 3(a) illustrates visually the autocatalytic feedback loop responsible for this instability in which the top-down feedback is dominant (fat top-down arrow).

The implications for the loans market are disastrous: banks that dare to lend in an aggressive way large quantities at low interest rate take over the market, while banks or financial sectors that take a more conservative position are squeezed out of the market. It becomes rational, and in fact unavoidable, for the creditors to have an as risky as possible policy just in order to avoid marginalization. In turn the debtors are encouraged to borrow larger and larger amounts at lower and lower interest rates.

However, as seen above and in the next sections, the formal expression of the run-away analysis has many common points with the neo-classical curve-crossing techniques used to find stable equilibria.

In the pre-crisis mode, the system is so successful that it slips into a state of exuberance which feeds back upon itself and increases exponentially the debt financed investment. [Greenspan 1996], [Schiller 2006] have called this exuberance ‘irrational’. However this is a matter of point of view: from the individual profit-seeking (capitalistic, in Minsky’s word) point of view this behavior is rational in as far as it maximizes one’s personal profits. However, for all-knowing agents who in particular would know the tragedy of the commons and the contents of the present paper, it should be clear that their behavior is likely to end in a collective loss.

Some commentators made Greenspan himself and the Federal Reserve Bank (Fed) responsible for the bubble by having kept interest rates too low and thereby encouraging the dangerous exuberance. Indeed, if loans with low interest are available, and the assets that can be bought with them have a high enough resilience: , which exceeds the interest rate: , the bottom line is that in this regime: . Thus borrowing in order to buy those assets looks from an myopic individual point of view (and in absence of understanding of the emergent collective dynamics) safe and profitable and thus rational!

This Minsky loans accelerator addresses a perennial puzzle faced by the mainstream neo-classical economics: the business cycle fluctuations. Not only the neo-classical models predict a crisis-free steady state but in fact they assume equilibrium as their main conceptual basis. The only way to admit some level of fluctuations is to attribute it to exogenous shocks that temporarily take the economy out of its stable equilibrium state [Kydland 1982]. According to those models, following such a shock, the invisible hand of the efficient market gently brings the system back to its equilibrium. On the opposite side, Minsky’s position is that crises are intrinsic to capitalism: the quite visible hand of debt financed investment is leading the capitalist system out of equilibrium. As seen below, the system eventually brings itself to a state in which the slightest noise is amplified to a systemic crisis. This ”Minsky moment” is described in the next subsection.

3.3.2 The Minsky Moment

As shown in the previous subsection, banks that would NOT lend with decreasing interest rates and debtors that would NOT take increasingly leveraged positions would in fact be the ones to be punished by lower profits, lower growth rates and market share loss. In order to give more loans, the banks will have to lend not only to solid highly promising companies (which at some stage become over-leveraged themselves), but also to units which are only riding on the positive-feedback expectations loop. Moreover, it is rational that the companies will adopt very large leverage positions that given the current interest rate are affordable at their current level of earnings. In fact this in itself leads to a version of the Minsky self-referential feedback loop: as the asset (stock market / real estate market) prices increase, so do the borrowing capabilities of the units holding them. This provides those units with more collateral for borrowing more on the same assets (which have now increased market value). The new loans received by those units may then go back reinvested in stock market / real estate, reinforcing the loop as long as the market price increases.

In fact, in order for the bank to continue the increase in its volume of lending, it has to find new borrowers. When all the good borrowers already have a loan, the bank has to lower its lending standards to capture new borrowers who were previously shut out of the credit market [Adrian 2010]. In an infinite economy and in the absence of noise this can be shown to be sustainable [LLS 1995]. However in the real world, one eventually rediscovers the ‘Herbert Stein’s Law’:

“If something cannot go on forever, it will stop.” [Krugman 2010].

In the present case the positive feedback loop is broken once there is even a small downward fluctuation of the rate of growth of the assets bought from the loan. This can in particular be brought upon by the finiteness of : the markets expand indefinitely to keep up with the ever increasing (loan financed) investments. Once the earnings from these investments cannot cover the interest payments on their debt , those units become ponzi and – when discovered – fail. This is the Minsky moment (Paul McCulley coined the term ‘Minsky moment’ to describe the 1998 Russian financial crisis). Following the Minsky moment, the previously lax credit policies are tightened, interest rates are increased (Eq. 23 below) which brings even mildly speculative (but until then viable, ) companies into ponzi positions () and eventual failure. In turn, this feeds back onto tightening further credit availability in the system and closing the feedback loop.

There is always some level of external noise that may cause the system to depart dramatically from that specified by these equations. As long as the leverage of companies is below a certain threshold, the noise is not sufficient to induce failures. However, as the leverage increases, the slightest fluctuation in the interest rate or the earnings may lead some of the borrowers into failure. This is the Minsky moment. The first wave of failures, induced by the noise, is then amplified systematically by the feedback between the number of failures and the interest rate; in order to avoid becoming ponzi, companies then have to deleverage. This increases the interest rate, which in turn forces more companies to deleverage or become ponzi.

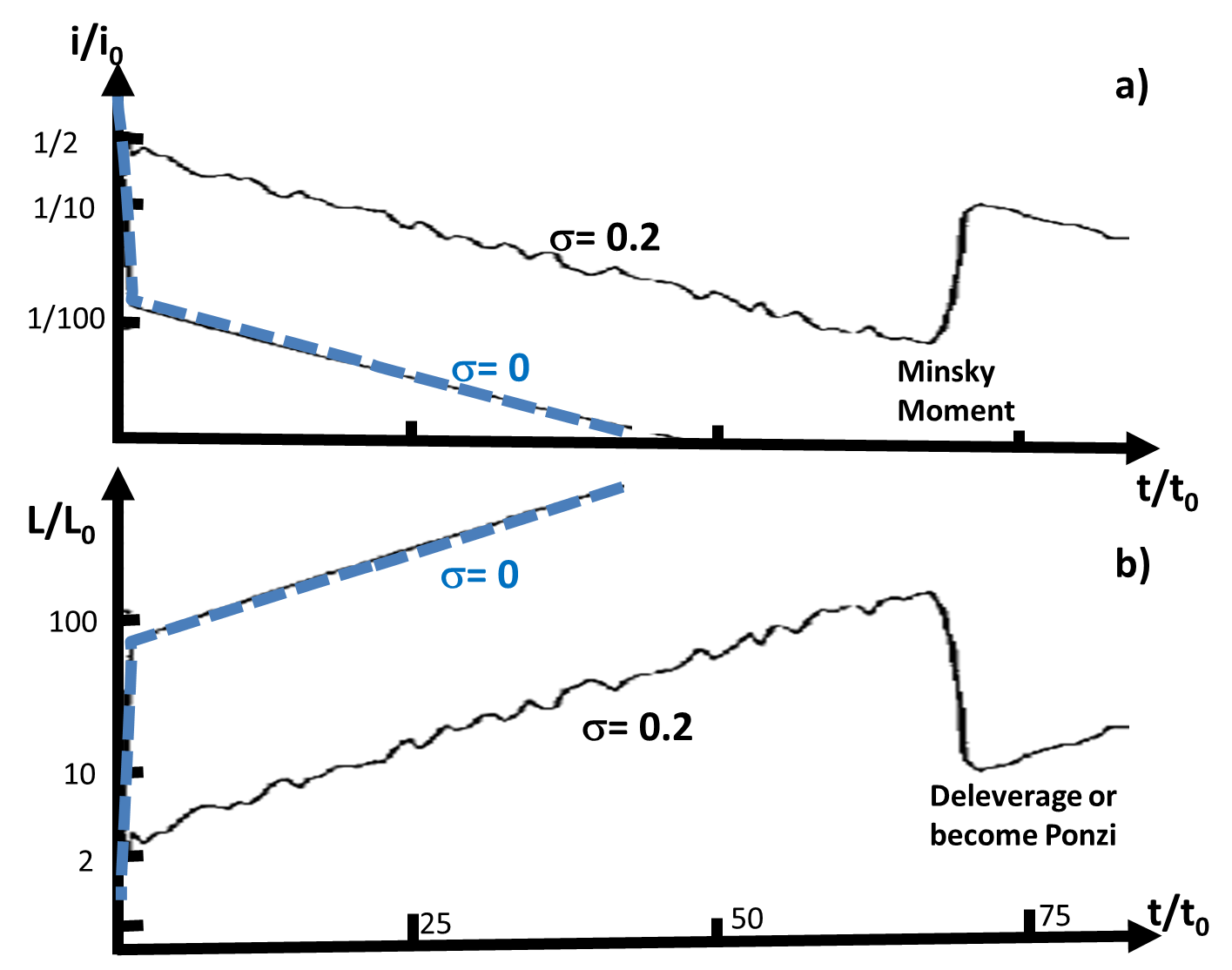

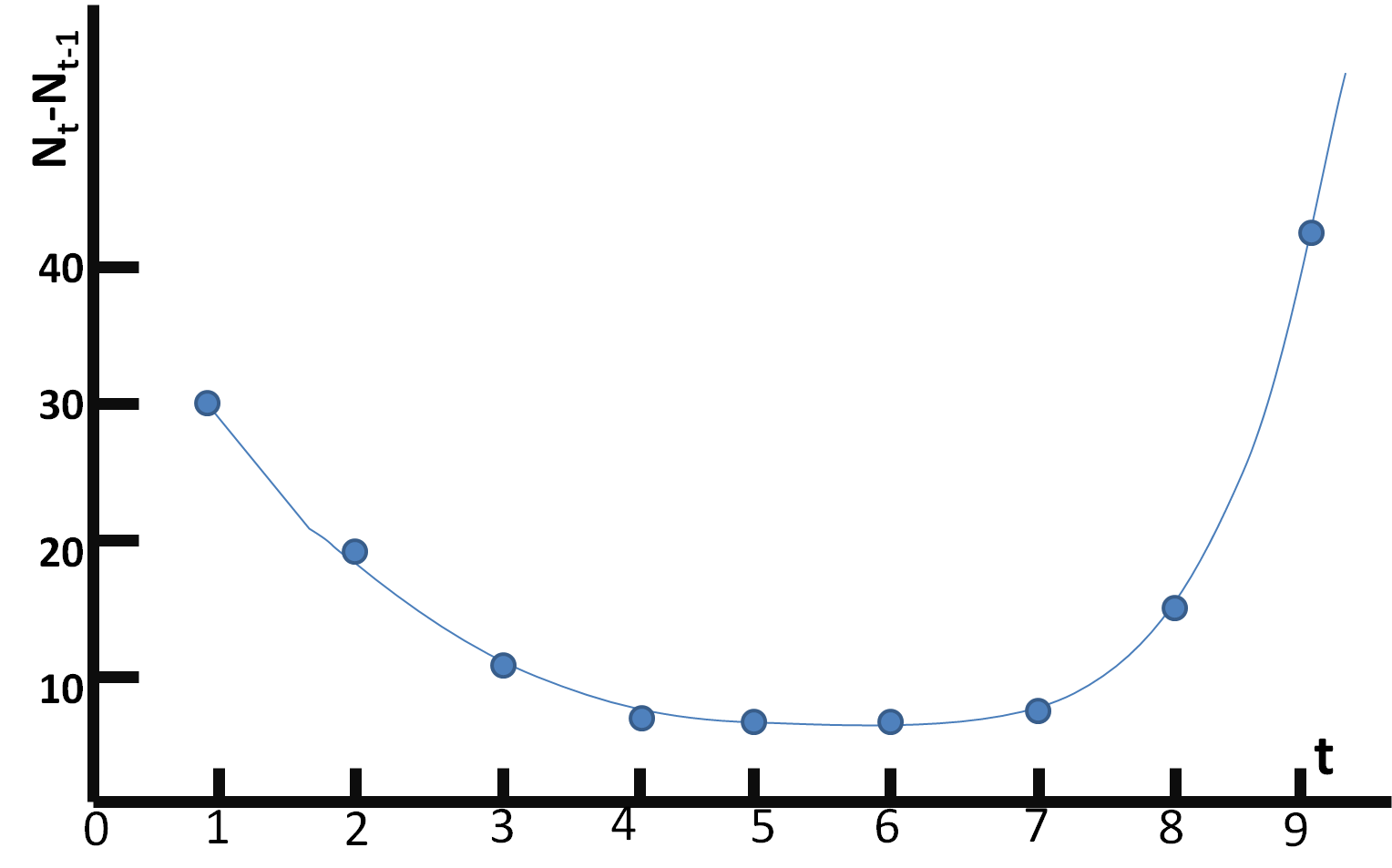

The original LLS model [Levy 1994] [LLS 1995] [LLS 2000] described the burst of a bubble where the fraction, , of investment in the risky assets increased indefinitely approaching 100 of the individuals’ wealth. This in the present context corresponds to the sustainable leverage diverging to arbitrary large values of the order (cf. the interrupted line in Figure 4(b). By sustainable average one means the leverage which is still consistent with the company not being ponzi. For instance, is the initially sustainable leverage .

It was shown in LLS that while in the absence of noise () this regime may continue indefinitely, in the presence of noise the bubble bursts when i.e. in our case when . In the present paper, the noise appears as a intrinsic consequence of the granularity of the agent based model.

One may wonder if, in order to avoid the Minsky moment, one should minimize the noise amplitude, . The answer is that reducing does indeed allow the system to pursue the exuberance for a longer period and tolerate without defaults higher leverages . However, this would only delay the Minsky Moment, not eliminate it. Moreover it would greatly increase the severity of the crisis once it is triggered. For instance, the presence of a noise keeps (Figure 4(a)) continuous line) almost two orders of magnitude larger than it would be in its absence (Figure 4 (a) interrupted line). Consequently the jump in the interest rate at the Minsky Moment is, for , from order of to order of (cf. Figure 4 (a)). Cf. Figure 4 (b) this corresponds to a jump of one order of magnitude in the sustainable leverage . In turn this means that all the companies with leverages in between the old and new sustainable leverage values are suddenly thrown into the ponzi category unless they have enough cash reserves to deleverage instantly.

Figure 4 adapts into the present context the analysis of [LLS 1995] of the role of noise and finite size in triggering the Minsky moment. In the figure it is shown that in the total absence of noise the risk taking collective behavior may continue to infinity: the interrupted lines, corresponding to 0 noise, show that the interest rate can continue to decay to arbitrary small values which in turn makes it possible (and profitable) for borrowers to take increasingly large leverages. By contrast, the slightest noise is bound to trigger sooner or later a catastrophic Minsky moment. In fact smaller the noise, later is the crisis and more catastrophic its consequences. Trying to avert the burst of the bubble in those conditions, achieves only its delay at the price of making it more severe. In the end assessment, it is better to have an economy with uncontroled noise, rather then one with uncontrolable crashes.

The dynamics following the Minsky Moment can be analysed with methods mathematically identical with the one used in the previous sections. This will be detailed in the next section. However, it will turn out that in order to obtain realistic results one has to include the microscopic granularity of the agents and the network effects of their interactions. This will be the subject of the rest of the paper.

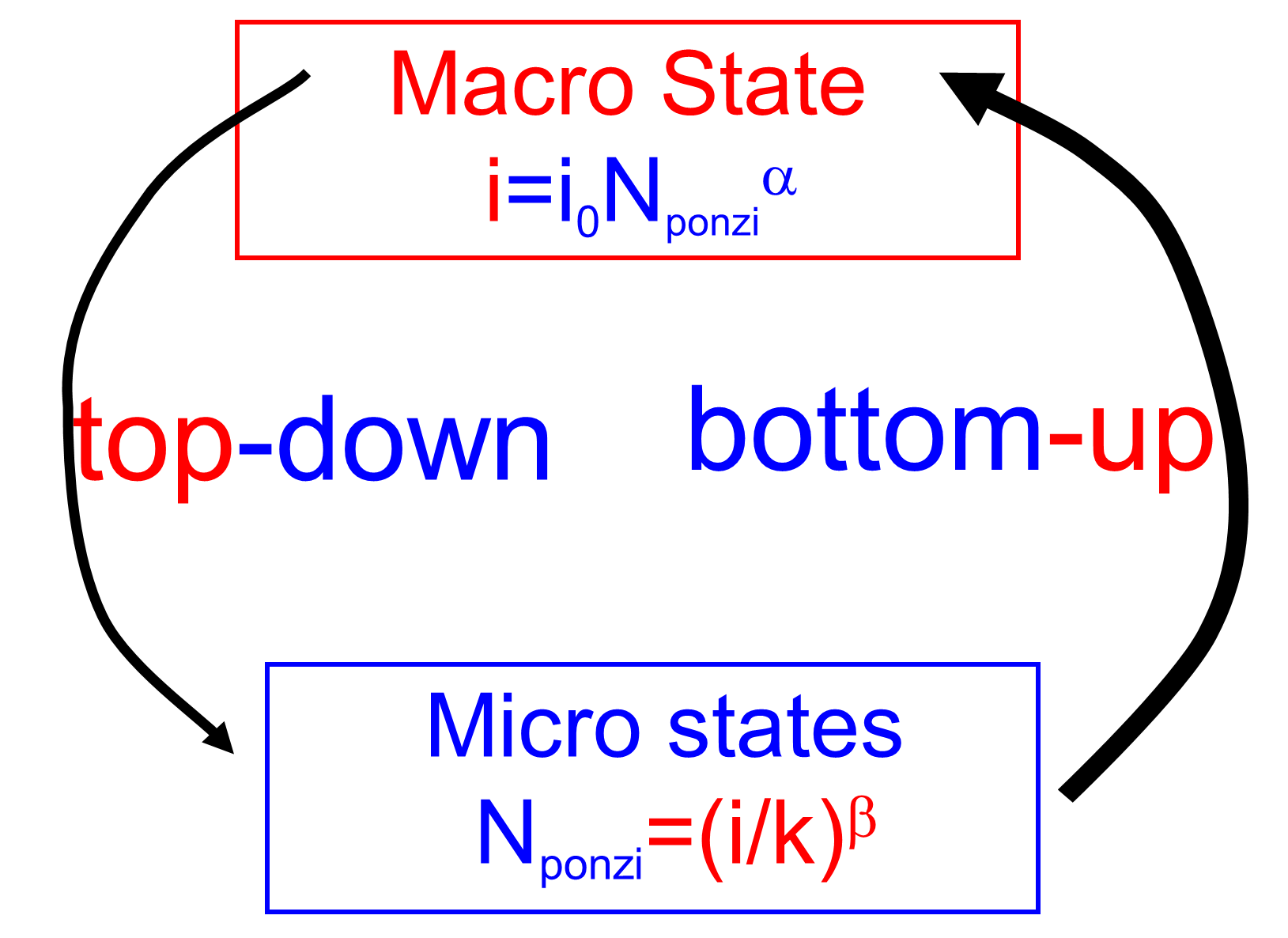

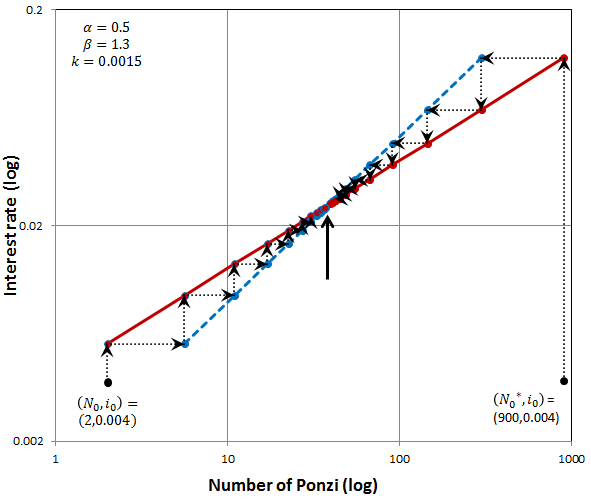

4 A Marshall-Walras-like procedure for the interest rate vs ponzi quantity: Minsky crisis accelerator

In neoclassical thinking the interest rate, , is the driving factor toward equilibrium in the debt market: increasing the interest rate is expected to inhibit risk taking and borrowing when they exceed a certain limit. One sees that in Minsky’s scenario, beyond a certain ”critical” point increasing the interest rate has an opposite procyclical effect of triggering the crisis. In the previous section we have considered the period leading up to the creation of a large amount of unwarranted, unsecured, low interest loans. Of course, the way to stop the ‘Minsky loans accelerator’ would be to increase the interest rate.

However, this would render a further part of debtors to be ponzi, leading to a ‘Minsky moment’ which marks the end of the ‘Minsky lending accelerator’ and the start of the ‘Minsky crisis accelerator’: ponzi failures decrease the credit availability in the system and thus increase the interest rate, , which in turn increases the number, , of companies forced into the ponzi status Eq. 3. Below we explain, justify, formalize and analayse the components of this feeback loop.

This ‘Minsky crisis accelerator’ is believed nowadays to be one of the main mechanisms behind the propagation of the current economic crisis [Wray 2011b] although its mathematical formulation is under fierce debate [Keen 1995], [Keen 2012], [Eggertson 2012], [Krugman 2012]. As it will turn out, the analysis of the Minsky crisis accelerator reduces to a similar mathematical formalism as the Minsky lending accelerator, except that instead of the quantity of loans, , it will be the number of ponzi companies, , that closes the feedback loop with the interest rate, .

Let us define in detail the formal framework. Earlier measurements by [Takayasu 2000] indicate that both debts and earnings, i.e. the denominator and the numerator in Eq. 3, are distributed according to power laws. In fact this has been connected with the Pareto wealth distribution power law [Klass 2006]. Therefore it is reasonable to assume that the resilience of company :

,

also follows a power law distribution with a heterogeneity exponent :

| (22) |

where and are empirically fixed parameters.

Inverting Eq. 22 allows us to obtain that the number of ponzi companies for a given interest rate, , i.e. the number of companies that have resilience . More precisely, if at a certain time, , the interest rate becomes , this will bring the current number of ponzi companies to:

| (23) |

On a double logarithmic scale in Figure 5(b) (where is represented on the axis, and on the axis) , as defined by Eq. 23, is represented by a straight line of slope . In this section we assume for simplicity that a company defaults as soon as it becomes ponzi .222 In the next sections we will significantly modify this extreme assumption. In the Minsky scenario, these defaults will cause credit to shrink and consequently the interest rate, , to go up. The following reasons lead us to expect this effect:

-

1

Banks will get increasingly worried about lending, because of the increasing danger of companies failing.

-

2

The debt left un-served by those companies that failed is now leaving their creditors short of cash. Consequently the creditors in turn may not be able to pay their own debts.

-

3

The liquidation of the collaterals used to guarantee the failed companies’ debt will lead to a devaluation of the value of similar guarantees held or posted by other companies in the system [Delli Gatti 2008].

For definiteness we assume that the increase in the interest rate, , will depend on the current number of defaults as a power law. More precisely, if the number of ponzis at time is this will induce an interest rate:

| (24) |

On a double logarithmic scale in Figure 5(b) the function is represented by a straight line of slope . Thus, as in the illustration of the previous iterative process Eq. 1(b), we have in Figure 5(b) on the same graph two lines with different roles:

As in the case of Figure 1(b), this is indicated by the arrows in Figure 5(b):

-

-

horizontal arrows will be used to obtain for a given while

-

-

vertical arrows will be used to obtain for a given .

The initial conditions for the iterative process are characterized by:

-

-

the state of the system before the shock as expressed by the initial interest rate , and

-

-

the strength of the shock as expressed by the number of companies initially knocked down into failure by it.

Following the Eqs. 23 and 24, and assuming the occurrence of an exogenous shock producing an initial number of ponzi companies, at a given initial interest rate , the unit iteration cycle is:

| (25) |

One can further represent the entire iterative process, where the given initial shock of ponzi companies triggers a chain reaction:

| (26) |

The main questions that such iterative process poses are:

-

-

is the process leading to an increasing sequence of and (corresponding to a crisis) and if so,

-

-

is the increasing sequence converging to a finite value (limited ‘mini’-crisis) or diverging to a systemic crisis (Minsky financial accelerator unleashed)?

Thus the parameter ranges of stability vs. crisis are determined by the initial values and and especially their position with respect to the fixed points where curves and intersect. In the present section (non-network case), there is only one intersection: the common solution of the Eqs. 23 and 24 after imposing stationarity :

| (27) |

| (28) |

As detailed in the Appendix C, the time evolution of the quantity of loans in the process Eqs. 23, 24, 26 shown in Figures 6(a), 5(b) is represented mathematically by:

| (29) |

This means that in general for the exponent for and the fixed point 27, 28 is stable:

-

-

starting with a smaller number of ponzi companies, , will lead to a limited crisis that will stop at .

-

-

starting with a severe economic state where the system will heal itself: and will iteratively shrink reaching eventually the same stable point . This assumes that as soon as the interest rate falls sufficiently to make a ponzi company non-ponzi any adverse systemic effects that its ponzi status had (say, on the interest rate) are erased.

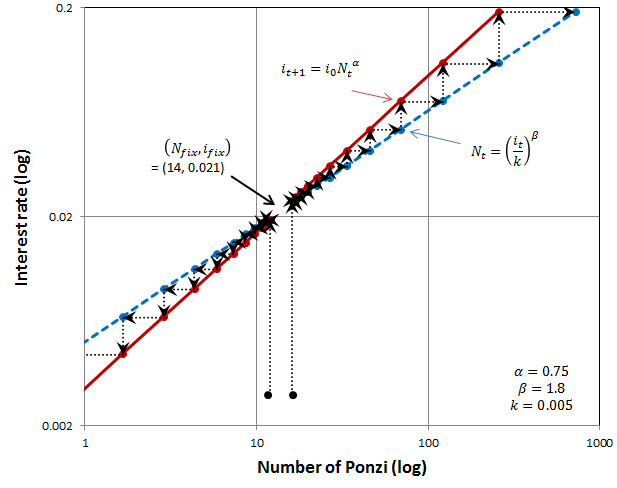

For , (illustrated in Figure 6(b)) and visualized conceptually in Figure 6(a) the situation reverses: the exponent for and the fixed point 27, 28 is unstable:

-

-

starting below the fixed point will lead to further shrinking in the number of ponzi companies and in the interest rate.

-

-

if the system is brought (endogenously or exogenously) above the fixed point it will enter in a Minsky financial accelerator and will further increase until complete economic collapse or until exogenous measures – e.g. forcing exogenously the interest rate, , (and / or the failures) down – stop the process.

Note that while passing from the case to the case has dramatic consequences for the system, in terms of the basic model assumptions the differences between the 2 cases are minor: a slight increase in the dependence of the interest rate on the number of failures or a slight change in the distribution of resiliences within the system can throw the system from the converging regime to the Minsky Instability Accelerator regime .

For instance, central banks in major countries can and have forced down the interest rate (and expanded inter-bank credit availability) artificially by creating fiat money and lending it at very low interest rate to banks. That may break (or even reverse) the feedback loop by forcing the red resilience trajectory below the resilience line of companies and borrowers. The Fed did it immediately while the European Central Bank (ECB) did it eventually, under the pressure of the markets on the sovereign bonds of Greece, Spain and Italy.

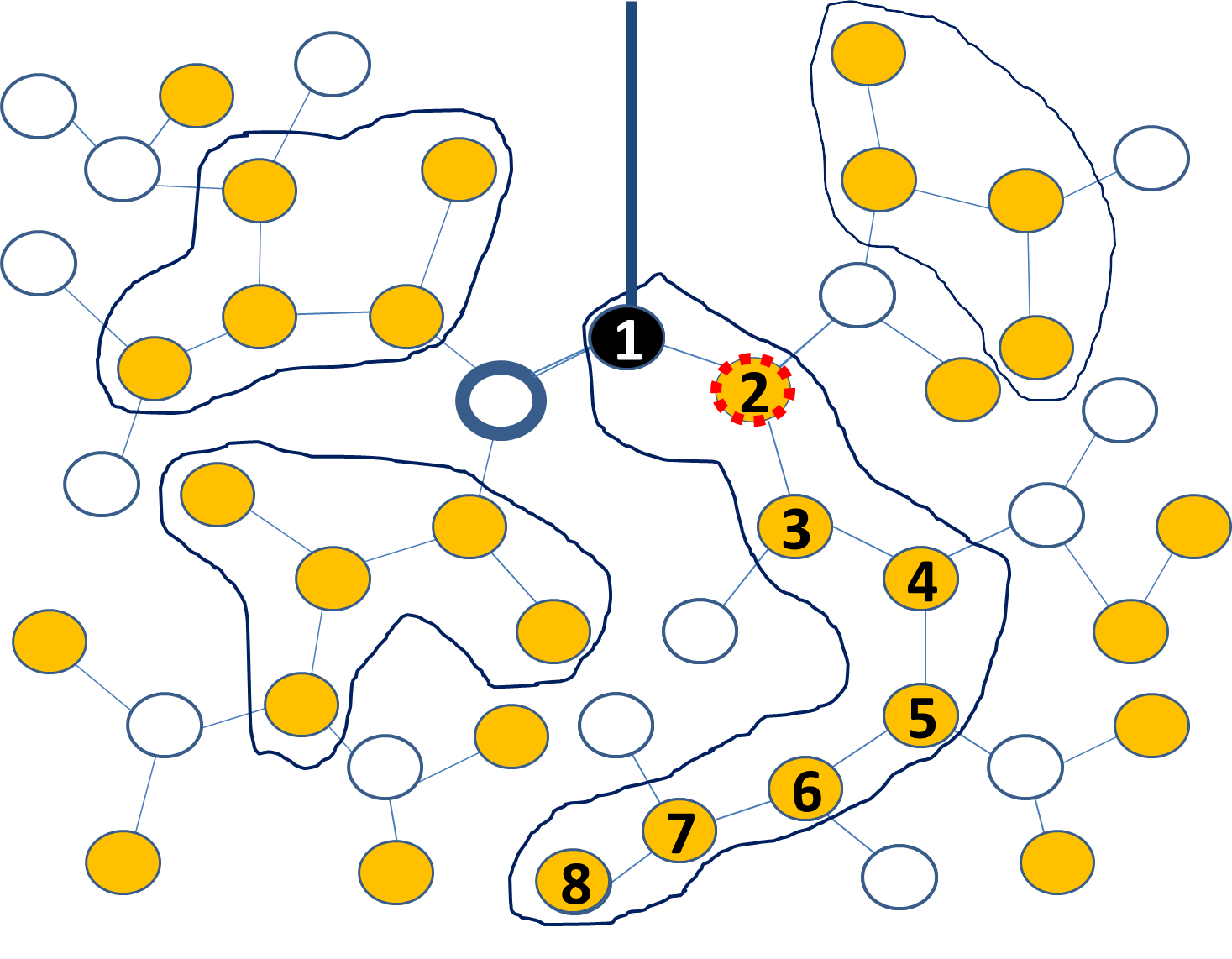

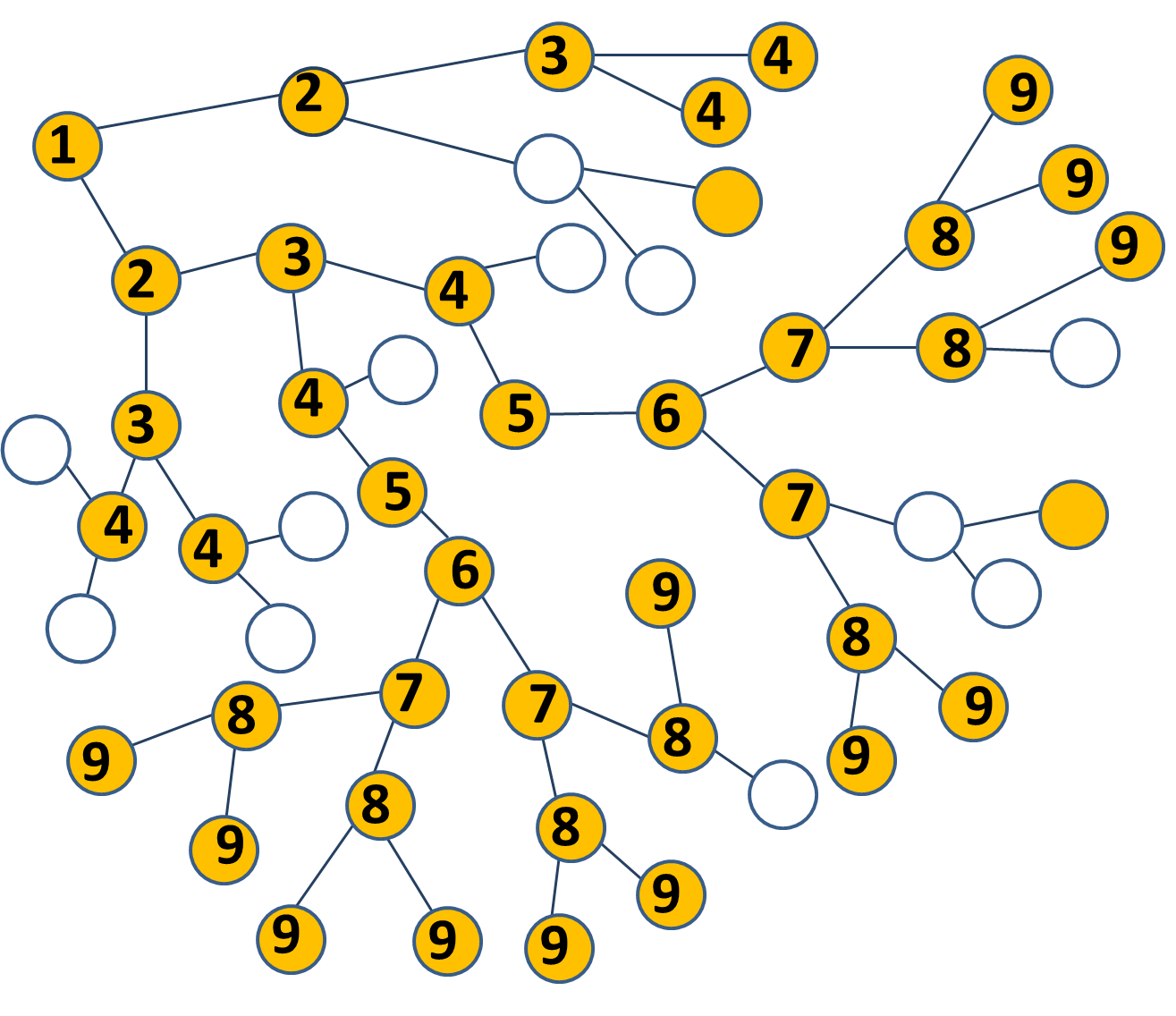

This section has dealt with the non-network view of the Minsky lending and crisis accelerators. We are now turning towards casting the basic Minsky ideas into a more realistic agent based network model. The main new ingredient will be that not all ponzi companies will default or fail. Rather the ponzi condition will make a company susceptible of being recognized as such and denied credit. The actual switch from the susceptible to the failed status will depend on the interactions of each ponzi with its trade partners. More specifically we will assume that a ponzi company will openly fail only when one of the companies directly connected to it (by a network link) defaults. To prepare this synthesis we first describe in the next section the propagation of distress by contagion on a network. We will follow therein the formalism of social and market percolation as described in [Solomon 2000] and [Goldenberg 2000].

5 Propagation of distress by contagion. Crisis Percolation across networks of companies

5.1 The relevance of contagion and percolation in financial networks

In order to express formally the feedback loops that enforce the propagation of distress between companies we will use the mathematical concept of percolation in a widened – dynamical – sense, better adapted to Minsky’s non-equilibrium thought. In its usual sense, the mathematical term of percolation describes the conditions in which a population of ‘nodes’ connected by binary links is capable of forming macroscopic connected clusters. However, in the present paper we will use a more dynamical version of this concept, as has been introduced under the names of social percolation in [Solomon 2000] and market percolation in [Goldenberg 2000], [Garcia 2011], [Van Eck 2011], [Delre 2010]. In this version, the stress is less on the question of the static existence of macroscopic clusters, but more on the ‘contagion’ process that sweeps across the population, creating macroscopic clusters of ‘contaminated’ agents. This allows, in turn, feedback between the growth of the contaminated cluster and processes that it influences [Solomon 2000] [Cantono 2010], [Cantono 2012], [Kindler 2013] which can, in their turn, feedback on the growth of the cluster.

Percolation models are agent based models in which the agents are the nodes of a network and their interactions are the contagion via the network edges. Contrary to common belief, the computer simulation of the evolution of the individual states of the agents is neither the only nor the most illuminating way to extract information about such systems. Quite to the contrary, the formula in Eq. 34, which we deduce below in a toy setting, and which predicts the size of the contagion avalanche as a function of the density of susceptible agents, is only the simplest example of a wealth of analytic results that are not only more precise but also more informative than the direct simulation of the system.

We start by describing the ‘market percolation’ mechanism using the ‘ponzi’ concept introduced in Section 2.2; this will be relevant for the network extension of the Minsky accelerator.

In the simplest non-network Minsky model, we considered a situation in which any company that becomes ponzi is immediately identified as such by the economic system and loses its capability to get further loans. In the absence of credit, such a company becomes incapable of continuing its normal activity and so, until the conditions change (e.g. new funds or better loan conditions become available), it has to freeze its activities. The model dynamics consisted then on companies either becoming ponzi (i.e. failing) or recovering from being ponzi. Once a company is ponzi, its failure was considered immediately known to the entire system and the consequences of its status were immediately enforced. In this sense the model adopted the neoclassical assumption that all the agents in the system have perfect and immediate knowledge of the system state, including the state (failed or not) of all other agents.

However, reality is often different. Consequently, we will consider here a different kind of situation and its model, in which the exact financial positions of companies is not known to all, especially not to potential creditors, and a ponzi company would fail openly only if a specific event uncovers (highlights or brings public attention to) its problems. For instance, it took the distress in much of its environment to uncover the fact that the Madoff company was ponzi and so to trigger its failure, even though it had been in the ponzi position for many years previously.