Cross-correlation asymmetries and causal relationships between stock and market risk

Stanislav S. Borysov1,2,3,∗, Alexander V. Balatsky1,4

1 Nordita, KTH Royal Institute of Technology and Stockholm University, Roslagstullsbacken 23, SE-106 91 Stockholm, Sweden

2 Nanostructure Physics, KTH Royal Institute of Technology, Roslagstullsbacken 21, SE-106 91 Stockholm, Sweden

3 Theoretical Division, Los Alamos National Laboratory, Los Alamos, NM 87545, USA

4 Institute for Materials Science, Los Alamos National Laboratory, Los Alamos, NM 87545, USA

E-mail: borysov@kth.se

Abstract

We study historical correlations and lead-lag relationships between individual stock risk (volatility of daily stock returns) and market risk (volatility of daily returns of a market-representative portfolio) in the US stock market. We consider the cross-correlation functions averaged over all stocks, using 71 stock prices from the Standard & Poor’s 500 index for 1994–2013. We focus on the behavior of the cross-correlations at the times of financial crises with significant jumps of market volatility. The observed historical dynamics showed that the dependence between the risks was almost linear during the US stock market downturn of 2002 and after the US housing bubble in 2007, remaining on that level until 2013. Moreover, the averaged cross-correlation function often had an asymmetric shape with respect to zero lag in the periods of high correlation. We develop the analysis by the application of the linear response formalism to study underlying causal relations. The calculated response functions suggest the presence of characteristic regimes near financial crashes, when the volatility of an individual stock follows the market volatility and vice versa.

Introduction

A financial market is a complex system demonstrating diverse phenomena and attracting attention from a whole spectrum of disciplines ranging from social to natural science[1]. Better understanding of the behavior of financial markets has become an integral part of the discussion on further sustainable economic development. In this context, proper assessment of financial risks [2] plays a crucial role: Underestimated risks contribute to financial bubbles with eventual crashes while overestimation of risks might cause inefficiency of financial resource allocations and a slowdown in economic growth, giving rise to periods of stagnation. This multifaceted problem, lying at the core of finance, draws significant interest from the physical and mathematical communities[3, 4]. One of the key components of financial risk analysis is a volatility assessment, which quantifies the financial stability of an asset in question. To this end, a number of methods have been proposed for risk modeling [5, 6, 7, 8] and forecasting[9], along with numerous studies of various empirical properties of volatility, including such stylized facts as clustering[10, 11, 12], lead-lag effects[13], asymmetries [14, 15] and many others (for a review see Refs. [16, 17]). Related phenomena, being a result of collective behavior, also involve such aspects as estimation of correlation [18, 19, 20] and cross-correlation[21, 22, 23, 24] matrices, study of their dynamics[25, 26], asymmetric correlations [27], nonlinear correlations[28, 29, 30] and detrending [31, 32], financial networks and clustering[33, 34, 35, 36, 37, 38, 39, 40, 41, 42], multivariate stochastic models[43, 44], critical phenomena [45, 46], etc.

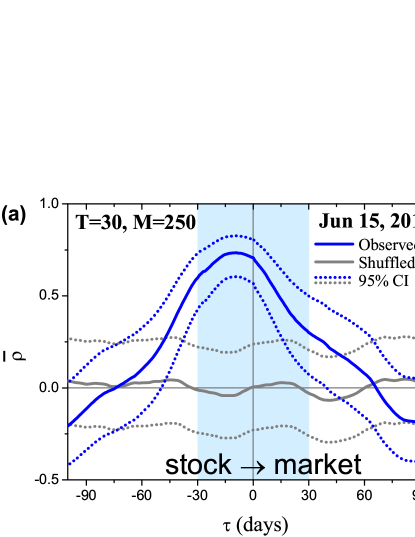

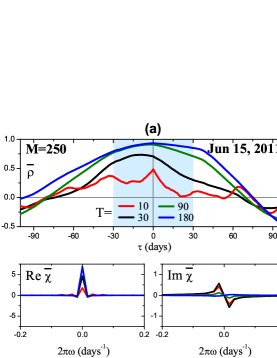

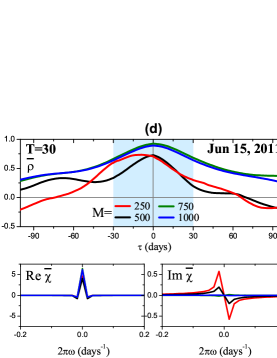

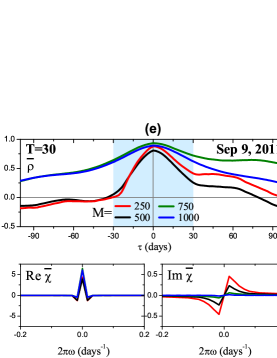

In the current paper, we focus on lead-lag effects between individual and collective volatility behavior in the US stock market, which might be further discussed in the context of the systemic regulation problem [47]. Former studies reported an increase of correlations across financial markets in recent times [25] along with overall market disposition to systemic collapses [48]. Our investigation thus has an aim to shed additional light on the dynamics of systemic risk in the last decade. For this purpose, we analyze historical prices of 71 stocks (Table 1) from the Standard & Poor’s 500 index [49] (hereafter S&P 500) for 1994–2013. Although we employ one of the simplest volatility estimators—the simple moving average (SMA) standard deviation of daily logarithmic returns—it is conjectured to correctly describe asset risk dynamics on long time scales, on the order of months and years [50]. We harness cross-correlation analysis which is a basic tool in the analysis of multiple time series. By definition, the absolute value of the normalized cross-correlation function lies between 0 and 1, indicating the strength of a linear relationship between time series, given that one is shifted by a particular lag value. It is crucial to note that our approach is based on a study of cross-correlations between derived quantities from the stock returns (standard deviations) rather than the analysis of cross-correlation matrices of the returns per se, implicitly involving calculation of cross-correlations between correlations111Since portfolio return is the sum of stock returns, its variance is the sum of all elements of the covariance matrix, , [Eq. (3)]. On the other hand, any covariance matrix can be factorized into the product of a correlation matrix, , and a diagonal matrix of standard deviations, , with elements and : .. These more sophisticated quantities will hopefully allow us to capture a more systematic evolution of the market risk as a function of time. Indeed, it was previously shown that market volatility and correlation are tightly related across international financial markets [51]. However, our calculations show that the cross-correlation function averaged over all stocks (see equations below) not only often has the maximum value close to 1 but also possesses an asymmetric shape with respect to zero lag (Fig. 1). These features suggest the presence of long-term trends, when equilibrium on the market is not reached within one trading day and overall market risk tends to follow individual stock risks [Fig. 1(a)] or vice versa [Fig. 1(b)]. Lately, emergence of intraday trends has been reported for stock returns [52] and correlations [53], while our investigation develops similar ideas for stock volatilities.

Generally, it is not possible to determine causality from an arbitrary shape of the cross-correlation function. However, if the cross-correlation function is asymmetric with respect to the time reversal operation (change of a sign of the time lag), it might hint at the presence of causal relationships[54]. Although determining true causality is rather a philosophical matter, we use this term in the predictive sense, i.e. if the past values of one time series can be used to predict the present or future values of the other. In this regard, one of the most widely used approaches is the Granger causality test [55]. Following this method, one builds autoregressive models for the time series including and excluding factors in question and checks if the difference between models is statistically significant. However, in the current investigation, we propose to use an alternative approach utilizing a specific class of asymmetric cross-correlation functions studied in linear response theory [56], which provides a framework for describing input-output properties of a physical system. Within this approach, causality implies the absence of any response before an action (as long as there are no long-term memory effects), that results in zero values of the cross-correlation function for a particular lag direction—positive or negative—depending on the input-output roles of the variables. The simplest example can be given by a force acting on a mass. The mass cannot move before the interaction and thus the correlation between the force and displacement is zero before the time when the force is applied. Although we do not expect to observe such a trivial behavior in real financial markets, asymmetries in the empirical functions (Fig. 1) can be interpreted as an approximation to this ideal model, where the mass and force are represented by individual stock and collective market volatility or vice versa, depending on the observed regime. Making use of this approximation, we restrict ourselves to the qualitative analysis with aim to reveal historical patterns only.

Estimating the stock and market risks

Let us first introduce notations used throughout the paper. We consider discrete time series of daily closing stock prices , which are converted to log-returns , assuming continuous compound interest. Within the SMA approach, one can calculate a moving average for a particular discrete time moment using equally weighted values of previous days including the current one

| (1) |

In this case, a cross-covariance of two time series might be defined as

| (2) |

where is a time lag. Series variance is a self-covariance at , , where denotes the standard deviation or volatility in finance. This quantity can be used as the simplest risk measure: Stocks with higher values of have less stable returns and, consequently, are less attractive for investment, other things being equal.

A stock market comprises all stocks available for trade. Although in the current investigation we consider a limited subset of stocks, it is chosen to represent the top US companies with the largest market capitalization. For such a portfolio, consisting of equal shares of stocks, total return, , equals to the sum of the separate stock returns, . Its variance, in addition to Eq. (2), can be also expressed as the sum of all elements of the covariance matrix , an matrix with elements ,

| (3) |

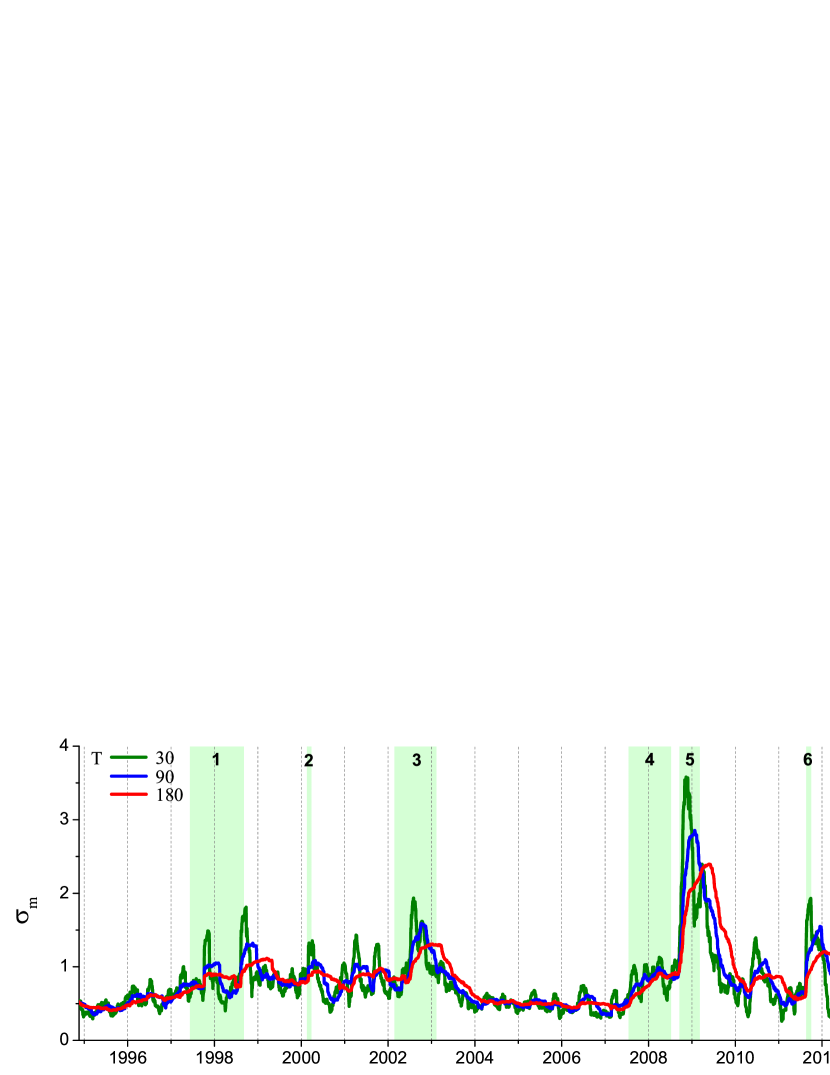

The square root of this value, , can be also used as a portfolio risk measure, which characterizes overall market risk in the case of large (Fig. 2). In the remainder of the paper, we will focus on finding historical dependences and lead-lag relationships between individual stock risks, , and market risk, , using the formalism presented in the following section.

Causality analysis

One of the possible ways to estimate dependence between two time series and is to calculate the cross-correlation function

| (4) |

which is normalized and ranges from to . Its peak value222In this section, we assume this peak value to be positive, since the opposite case can be easily recovered via multiplication of or by . Noting that and , one immediately gets shows the strength of a linear relationship between and (with zero value corresponding to its absence) when the first series is shifted by the time lag . If the dependence between series is nonlinear, more sophisticated statistical concepts should be used instead, for instance, cross-entropy[28], copula[29] or the Spearman’s rank correlation[30]. However, we are aimed to employ the linear Pearson’s coefficient [Eq. (4)] in the present study. Given two series are correlated, it is not possible to establish causal relationships between the variables by this fact itself. However, the particular shapes of the cross-correlation functions studied within linear response theory can provide an insight into this problem.

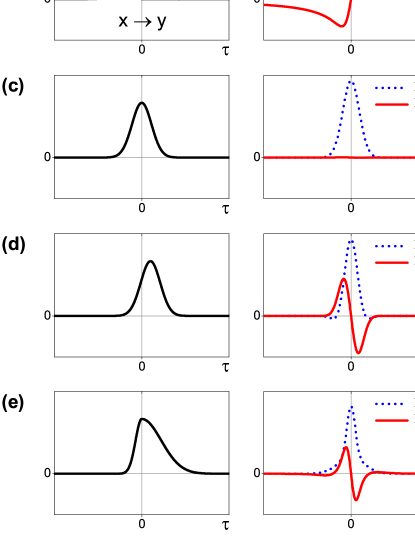

This theory provides a convenient framework for the study of related dynamical properties of a physical system. Within this approach, the cross-correlation function defines the system’s response to an external action, obeying laws of motion. In this context, causality implies the absence of any deterministic response before an action, i.e. the expected value of the cross-correlation function is zero for a particular lag direction ( or ) defined by the input-output roles of and . For example, the response function of the first-order ordinary differential equation

| (5) |

where and are some constants and is the delta function (impulse force), is depicted in Fig. 3(a). Here, can be uniquely identified as an external action because is non-zero only for , the time direction corresponding to the future values of and the past values of [see Eq. (2)]. This asymmetry of the response is also graphically reflected in its Fourier transform333Since we work with discrete time series, we use its discrete analogue with a unitary norm . known as susceptibility

| (6) |

which is a complex-valued function of frequency . Its real (reactive) part, , being an even function of , is defined by the correlation strength. While the imaginary (dissipative) part, , is an odd function of defined by the asymmetric part of 444Any function can be written as the sum of an even function and an odd function . In this case, is the Fourier transform of while is the Fourier transform of .. Regarding the action-reaction roles of and in Eq. 5, has a negative peak for [Fig. 3(a)] and a positive peak if the variables are interchanged [Fig. 3(b)]. Additionally, and satisfy the Kramers-Kronig relations, which is a mathematical condition of a complex function to be analytic and hence the underlying physical system to be stable[57].

The empirical cross-correlation functions (Fig. 1), which characteristic shapes are schematically depicted in Figs. 3(c)–(e), differ from the ones studied in linear response theory [Figs. 3(a)–(b)]. Despite this fact, the corresponding susceptibilities display the similar features of the real and imaginary parts (Fig. 4). Thus, we consider them as a coarse approximation to the theoretical linear response functions and utilize the peak of as an indicator of possible causal dependence. If the cross-correlation function is completely symmetric with respect to the time reversal operation [Fig. 3(c)], , no causal relation between and can be established within the linear response formalism given the cross-correlation function alone: This fact implies that the interchange of the input-output roles of the underlying variables produces exactly the same observable behavior of the system as a whole. However, when the maximum value of is slightly shifted [Fig. 3(d)] or the function decays faster for the one lag direction than for the other [Fig. 3(e)] one might expect that the change of tends to cause the reaction of because of the enhanced response for the future values of . In doing so, reversal of the observed input-output roles corresponds to the change of the sign of the imaginary part while the real part remains unaffected.

Finally, fitting of a particular susceptibility model to the empirical data allows one to determine the differential equation which governs the observed behavior of the system. However, the behavior of a real financial market is usually highly nonlinear, possessing long-term memory effects[58, 59] and fractal structure[60, 61], that is obviously beyond the scope of the discussed method. One of the possible ways to extend the presented approach might be the application of nonlinear response theory[62] although this case is not considered in our paper. We restrict ourselves to the linear qualitative analysis which only hints at the direction of influence between the variables in question.

Results

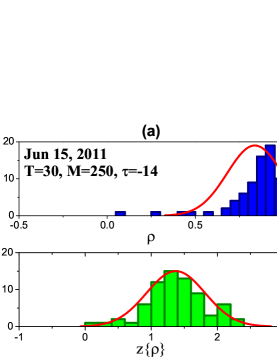

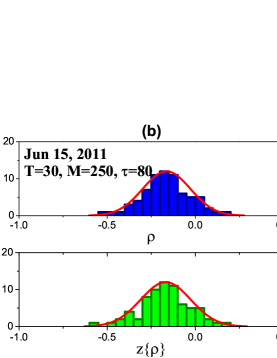

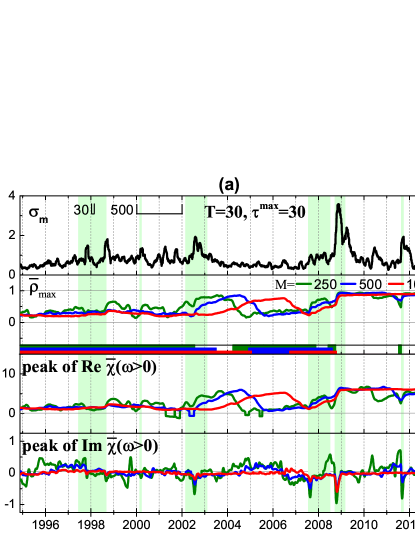

We are now in position to determine causal relations between the individual stock and total market risk, applying the formalism from the previous section. With this aim, we analyze historical stock prices[63] of the largest US companies in terms of market capitalization, members of the S&P 500 (Table 1). The historical period considered is between 1994 and 2013, roughly corresponding to 4600 trading days. Being interested in the average market dynamics, we consider a mean value of . However, there is a problem of averaging correlation coefficients since their distribution is highly skewed when the value of is close to 1 [top panel in Fig. 5(a)], what makes them nonadditive quantities. In this regard, a number of methods has been proposed to tackle this issue [64, 65]. The simplest one is the Fisher transform [66]

| (7) |

which makes the distribution of correlation coefficients approximately normal [bottom panel in Fig. 5(a)]. In this case, the average correlation might be estimated as

| (8) |

with a confidence interval (CI)

| (9) |

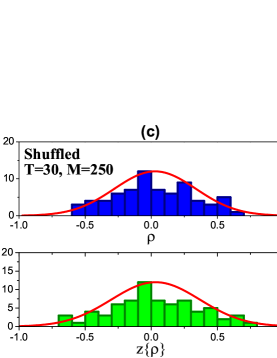

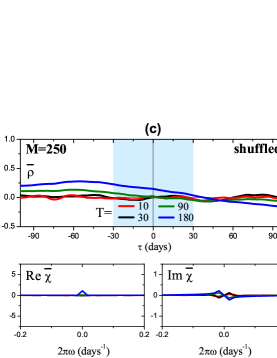

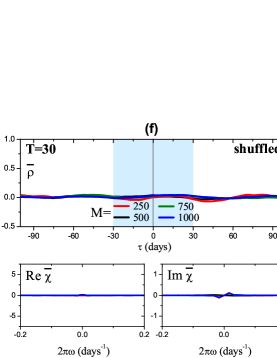

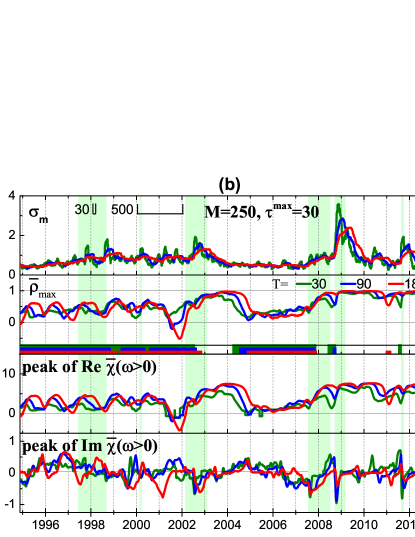

where corresponding to the confidence level is further used. When is small, the distribution is not skewed and the Fisher transform does not affect it ( for small ) [Fig. 5(b),(c)]. This average function is subsequently Fourier transformed to obtain the average susceptibility using the discrete analogue of Eq. 6 for the interval . It is also worth noting that the use of an SMA for the calculation of volatilities ( and ) imposes smoothing on the corresponding time series. Thus, a bigger window of size for the calculation of in Eq. (4) should be used to avoid spurious correlations [Fig. 6(c),(f)]. Additionally, Fig. 5(c) suggests that the averaging over a big number of stocks effectively reduces related undesirable effects.

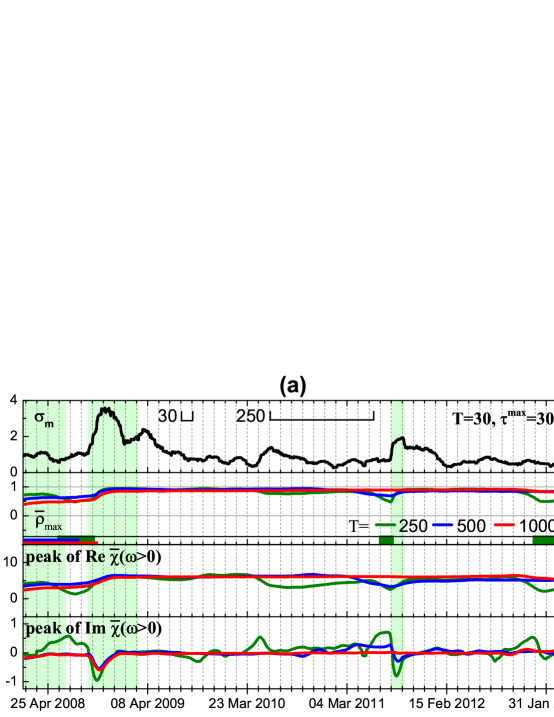

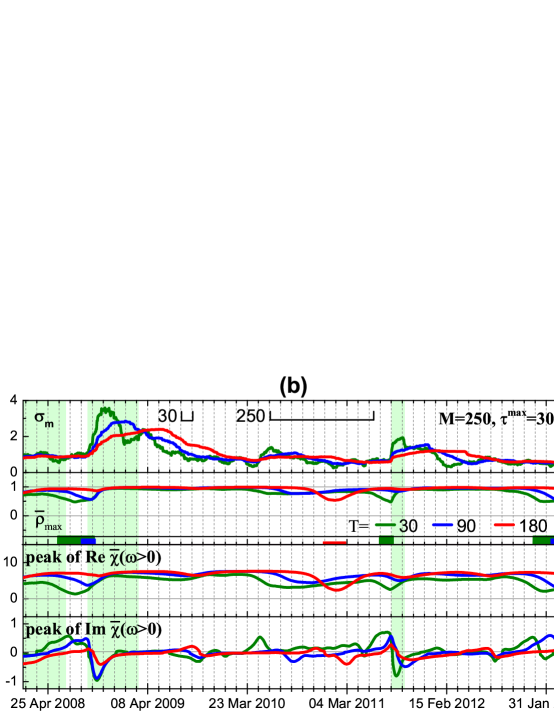

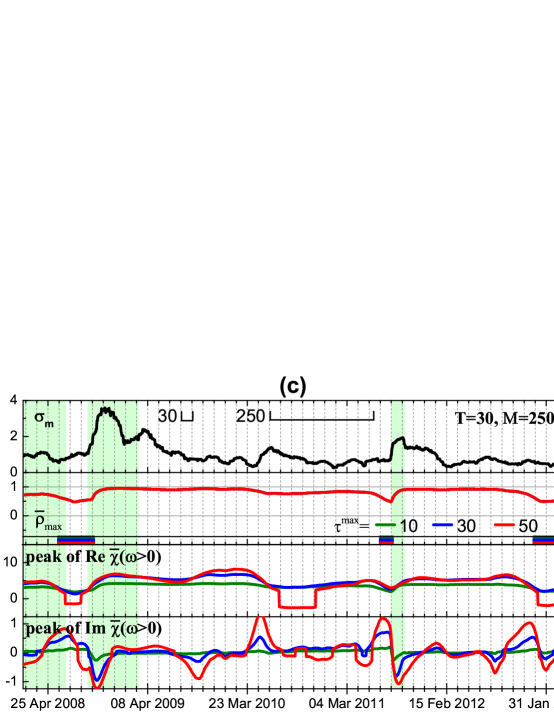

The task at hand requires the series in question to be correlated. For this purpose, we calculate the maximum value of the correlation between the market risk and individual stock risk, , within the considered range of lag . The historical dynamics of this maximum value (second panel in Fig. 7) suggests that it becomes significantly bigger than near major financial crashes, while in other times the series seem to be weakly correlated. In this respect, one can highlight the US market downturn of 2002 and approximately the 5-year period from the US housing bubble in 2007 until 2013, when almost the linear relationship was observed. For such highly correlated risks, it is feasible to perform causal analysis within the linear response approximation.

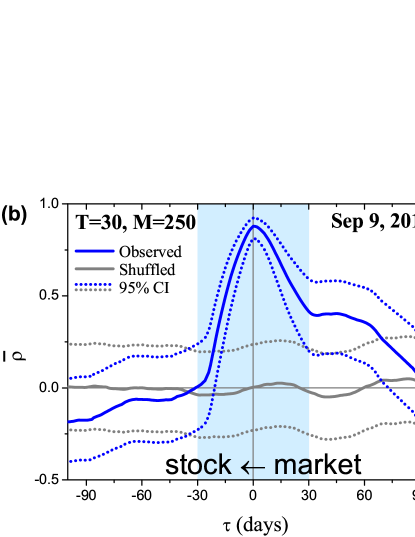

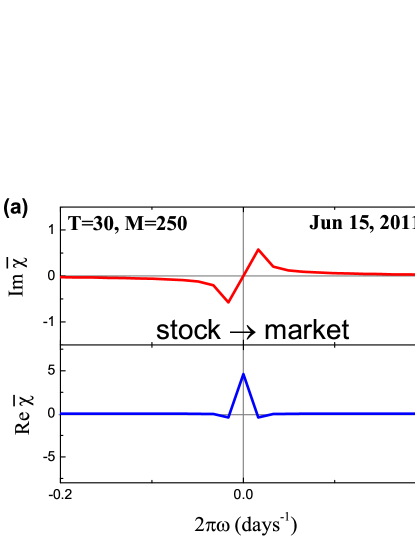

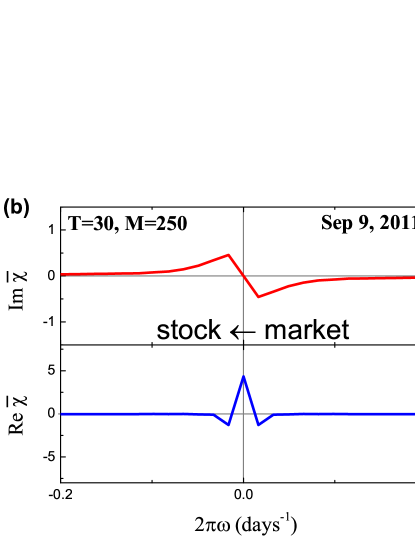

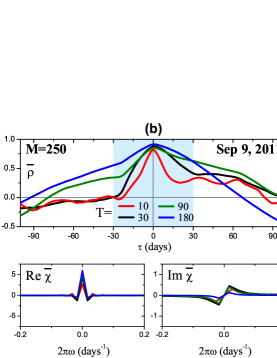

As was mentioned before, typical shapes of and are depicted in Fig. 1 and Fig. 4 respectively. For instance, causality analysis of these two dates near European sovereign debt crisis reveals that for Jun 15, 2011 [Fig. 1(a)] the maximum value of the cross-correlation function is shifted left with respect to zero lag, which is reflected as a negative peak of the imaginary part of the susceptibility for positive frequencies [Fig. 4(a)]. Following the discussion from the previous section, this feature corresponds to the leading influence of individual stock risks on the total market risk. While the opposite situation is observed on Sep 9, 2011 [Fig. 1(b) and Fig. 4(a)]. The historical analysis of the average susceptibility dynamics (two bottom panels in Fig. 7) for the periods with high value of reveals two peculiarities. The first one is related to the fact that individual stock risks follow market risk after big crashes. This feature can be viewed as a consequence of herding behavior, when stock risks are trying to reach new equilibrium with overall market risk as a benchmark. This fact is also in agreement with the studies on asymmetric phenomena [14, 15, 27], which have shown enhance of volatility and correlations in a bear market. The second peculiarity can be observed, for example, before the Lehman Brothers collapse in 2008 and the European sovereign debt crisis in 2012, when individual stock risks on average start to influence market risk shortly before a crash, while at the crash the direction of influence is reversed. Finally, Fig. 8 shows that this behavior is observed for different window sizes and , however, use of bigger values of smooths described effects.

Discussion

We have studied average lead-lag relationships between individual stock and collective market risk in the US stock market using cross-correlation analysis. Our calculations have shown that stock and market volatility are tightly correlated during the periods of financial instability. Furthermore, the correlation functions often possess asymmetries with respect to zero lag, which is a potential sign of a causal dependence between the risks within the linear response approximation. Having analyzed historical data for 1994–2013, we have found similar patterns near the last major crashes. Firstly, after a financial crash individual stock risks tend to follow collective market behavior. Secondly, the opposite influence is observed when stock risks on average start to influence market risk before particular crashes, for instance, the Lehman Brothers collapse in 2008 or the European sovereign debt crisis in 2012. Eventual market adjustment after the crash leads to the restoration of a symmetric shape of the average cross-correlation function and decrease of its maximum value. This is also reflected in the Fourier transform of the cross-correlation known as susceptibility. For this complex function, reversal of the causal dependence corresponds to the change of the sign of its imaginary part, while the real part remains unaffected, and the absence of the dependence results in zero value of the imaginary part. We suggest that the observed patterns might be interpreted as a manifestation of herding behavior, when economic performance of separate companies systematically does not meet expectations of investors, creating the panic across the market. Wherein after the crash, financial risks of separate companies adapt to a new reality with overall market performance as a psychological benchmark.

Acknowledgments

We are grateful to L. Pietronero, Y. Roudi, J. Suorsa, J. Edge and anonymous referees for providing useful comments and discussion. This work is supported by Nordita and VR VCB 621-2012-2983.

References

- 1. Farmer JD, Shubik M, Smith E (2005) Is economics the next physical science. Physics Today 58: 37.

- 2. Bisias D, Flood MD, Lo AW, Valavanis S (2012) A survey of systemic risk analytics. US Department of Treasury, Office of Financial Research No 0001 .

- 3. Mantegna R, Stanley H (1999) An Introduction to Econophysics. Cambridge University Press, Cambridge.

- 4. Bouchaud JP, Potters M (2004) Theory of Financial Risk and Derivative Pricing: From Statistical Physics to Risk Management. Cambridge University Press, Cambridge, 2 edition.

- 5. LeBaron B, Arthur W, Palmer R (1999) Time series properties of an artificial stock market. Journal of Economic Dynamics and Control 23: 1487 - 1516.

- 6. Jondeau E, Poon SH, Rockinger M (2007) Modeling volatility. In: Financial Modeling Under Non-Gaussian Distributions, Springer London, Springer Finance. pp. 79-142.

- 7. Tsay RS (2003) Multivariate Volatility Models and Their Applications, John Wiley & Sons, Inc. pp. 357–394. doi:10.1002/0471264105.ch9. URL http://dx.doi.org/10.1002/0471264105.ch9.

- 8. Miccichè S, Bonanno G, Lillo F, Mantegna RN (2002) Volatility in financial markets: stochastic models and empirical results. Physica A: Statistical Mechanics and its Applications 314: 756 - 761.

- 9. Poon SH, Clive WG (2003) Forecasting volatility in financial markets: A review. Journal of Economic Literature 41: 478-539.

- 10. Liu Y, Gopikrishnan P, Cizeau P, Meyer M, Peng CK, et al. (1999) Statistical properties of the volatility of price fluctuations. Phys Rev E 60: 1390–1400.

- 11. Gopikrishnan P, Plerou V, Nunes Amaral LA, Meyer M, Stanley HE (1999) Scaling of the distribution of fluctuations of financial market indices. Phys Rev E 60: 5305–5316.

- 12. Krawiecki A, Hołyst JA, Helbing D (2002) Volatility clustering and scaling for financial time series due to attractor bubbling. Phys Rev Lett 89: 158701.

- 13. Lo A, MacKinlay A (1990) When are contrarian profits due to stock market overreaction? Review of Financial Studies 3: 175-205.

- 14. Bekaert G, Wu G (2000) Asymmetric volatility and risk in equity markets. Review of Financial Studies 13: 1-42.

- 15. Talpsepp T, Rieger MO (2009) Explaining asymmetric volatility around the world. SSRN .

- 16. Chakraborti A, Toke IM, Patriarca M, Abergel F (2011) Econophysics review: I. empirical facts. Quantitative Finance 11: 991-1012.

- 17. McAleer M, Medeiros MC (2008) Realized volatility: A review. Econometric Reviews 27: 10-45.

- 18. Erb CB, Harvey CR, Viskanta TE (1994) Forecasting international equity correlations. Financial Analysts Journal 50: pp. 32-45.

- 19. Laloux L, Cizeau P, Bouchaud JP, Potters M (1999) Noise dressing of financial correlation matrices. Phys Rev Lett 83: 1467–1470.

- 20. Livan G, Rebecchi L (2012) Asymmetric correlation matrices: an analysis of financial data. The European Physical Journal B 85: 1-11.

- 21. Plerou V, Gopikrishnan P, Rosenow B, Amaral LAN, Guhr T, et al. (2002) Random matrix approach to cross correlations in financial data. Phys Rev E 65: 066126.

- 22. Plerou V, Gopikrishnan P, Rosenow B, Nunes Amaral LA, Stanley HE (1999) Universal and nonuniversal properties of cross correlations in financial time series. Phys Rev Lett 83: 1471–1474.

- 23. Utsugi A, Ino K, Oshikawa M (2004) Random matrix theory analysis of cross correlations in financial markets. Phys Rev E 70: 026110.

- 24. Giada L, Marsili M (2001) Data clustering and noise undressing of correlation matrices. Phys Rev E 63: 061101.

- 25. Fenn DJ, Porter MA, Williams S, McDonald M, Johnson NF, et al. (2011) Temporal evolution of financial-market correlations. Phys Rev E 84: 026109.

- 26. Podobnik B, Wang D, Horvatic D, Grosse I, Stanley HE (2010) Time-lag cross-correlations in collective phenomena. EPL (Europhysics Letters) 90: 68001.

- 27. Longin F, Solnik B (2001) Extreme correlation of international equity markets. The Journal of Finance 56: 649–676.

- 28. Zhou R, Cai R, Tong G (2013) Applications of entropy in finance: A review. Entropy 15: 4909–4931.

- 29. Jouanin JF, Riboulet G, Roncalli T (2004) Risk measures for the 21st century. In: Szego PG, editor, Social Goals and Social Organization, John Wiley & Sons. URL http://ssrn.com/abstract=1032588.

- 30. Lee C, Lee J, Lee A (2000) Statistics for Business and Financial Economics. Vol. 1. World Scientific.

- 31. Székely GJ, Rizzo ML (2009) Brownian distance covariance. The Annals of Applied Statistics 3: 1236–1265.

- 32. Podobnik B, Stanley HE (2008) Detrended cross-correlation analysis: A new method for analyzing two nonstationary time series. Phys Rev Lett 100: 084102.

- 33. Mantegna R (1999) Hierarchical structure in financial markets. The European Physical Journal B - Condensed Matter and Complex Systems 11: 193-197.

- 34. Schweitzer F, Fagiolo G, Sornette D, Vega-Redondo F, Vespignani A, et al. (2009) Economic networks: The new challenges. Science 325: 422-425.

- 35. Boss M, Elsinger H, Summer M, Thurner 4 S (2004) Network topology of the interbank market. Quantitative Finance 4: 677-684.

- 36. Bonanno G, Caldarelli G, Lillo F, Mantegna RN (2003) Topology of correlation-based minimal spanning trees in real and model markets. Phys Rev E 68: 046130.

- 37. Kim DH, Jeong H (2005) Systematic analysis of group identification in stock markets. Phys Rev E 72: 046133.

- 38. Heimo T, Kaski K, Saramäki J (2009) Maximal spanning trees, asset graphs and random matrix denoising in the analysis of dynamics of financial networks. Physica A: Statistical Mechanics and its Applications 388: 145 - 156.

- 39. Harré M, Bossomaier T (2010) Equity trees and graphs via information theory. The European Physical Journal B 73: 59-68.

- 40. Kyriakopoulos F, Thurner S, Puhr C, Schmitz SW (2009) Network and eigenvalue analysis of financial transaction networks. The European Physical Journal B 71: 523-531.

- 41. Coelho R, Hutzler S, Repetowicz P, Richmond P (2007) Sector analysis for a {FTSE} portfolio of stocks. Physica A: Statistical Mechanics and its Applications 373: 615 - 626.

- 42. Kenett DY, Tumminello M, Madi A, Gur-Gershgoren G, Mantegna RN, et al. (2010) Dominating clasp of the financial sector revealed by partial correlation analysis of the stock market. PLoS ONE 5: e15032.

- 43. Asai M, McAleer M, Yu J (2006) Multivariate stochastic volatility: A review. Econometric Reviews 25: 145-175.

- 44. Bonanno G, Valenti D, Spagnolo B (2007) Mean escape time in a system with stochastic volatility. Phys Rev E 75: 016106.

- 45. Biondo AE, Pluchino A, Rapisarda A, Helbing D (2013) Reducing financial avalanches by random investments. Phys Rev E 88: 062814.

- 46. Majdandzic A, Podobnik B, Buldyrev SV, Kenett DY, Havlin S, et al. (2014) Spontaneous recovery in dynamical networks. Nature Physics Letters 10.

- 47. Beale N, Rand DG, Battey H, Croxson K, May RM, et al. (2011) Individual versus systemic risk and the regulator’s dilemma. Proceedings of the National Academy of Sciences : 34-38.

- 48. Kenett DY, Shapira Y, Madi A, Bransburg-Zabary S, Gur-Gershgoren G, et al. (2011) Index cohesive force analysis reveals that the us market became prone to systemic collapses since 2002. PLoS ONE 6: e19378.

- 49. Standard & Poor’s 500 Index. URL http://www.spindices.com/indices/equity/sp-500/.

- 50. Fabozzi FJ, editor (2006) Handbook of Finance, Financial Markets and Instruments, volume 1. Wiley.

- 51. Solnik B, Boucrelle C, Fur YL (1996) International market correlation and volatility. Financial Analysts Journal 52: pp. 17-34.

- 52. Curme C, Tumminello M, Mantegna RN, Stanley HE, Kenett DY (2014) Emergence of statistically validated financial intraday lead-lag relationships. ArXiv e-prints .

- 53. Kenett DY, Preis T, Gur-Gershgoren G, Ben-Jacob E (2012) Quantifying meta-correlations in financial markets. EPL (Europhysics Letters) 99: 38001.

- 54. Pierce DA, Haugh LD (1977) Causality in temporal systems: Characterization and a survey. Journal of Econometrics 5: 265 - 293.

- 55. Granger CWJ (1969) Investigating causal relations by econometric models and cross-spectral methods. Econometrica 37: pp. 424-438.

- 56. Kubo R (1957) Statistical-mechanical theory of irreversible processes. i. general theory and simple applications to magnetic and conduction problems. Journal of the Physical Society of Japan 12: 570-586.

- 57. Toll JS (1956) Causality and the dispersion relation: Logical foundations. Phys Rev 104: 1760–1770.

- 58. Gopikrishnan P, Meyer M, Amaral L, Stanley H (1998) Inverse cubic law for the distribution of stock price variations. The European Physical Journal B - Condensed Matter and Complex Systems 3: 139-140.

- 59. Taylor S (1986) Modelling Financial Time Series. John Wiley & Sons.

- 60. Peters EE (1989) Fractal structure in the capital markets. Financial Analysts Journal 45: pp. 32-37.

- 61. Lin CH, Chang CS, Li SP (2013) Empirical method to measure stochasticity and multifractality in nonlinear time series. Phys Rev E 88: 062912.

- 62. Jha S (1984) Nonlinear response theory – i. Pramana 22: 173-182.

- 63. Yahoo! Finance. URL http://www.finance.yahoo.com/.

- 64. Hotelling H (1953) New light on the correlation coefficient and its transforms. Journal of the Royal Statistical Society Series B (Methodological) 15: pp. 193-232.

- 65. Hawkins DL (1989) Using u statistics to derive the asymptotic distribution of fisher’s z statistic. The American Statistician 43: pp. 235-237.

- 66. Fisher RA (1915) Frequency distribution of the values of the correlation coefficient in samples from an indefinitely large population. Biometrika 10: pp. 507-521.

| Ticker | Name | Sector | Ticker | Name | Sector |

|---|---|---|---|---|---|

| ABT | Abbott Laboratories | Hea | AIG | American International Group, Inc. | Fin |

| AMGN | Amgen Inc. | Hea | APA | Apache Corp. | Bas |

| APC | Anadarko Petroleum Corp. | Bas | AAPL | Apple Inc. | Con |

| AXP | American Express Company | Fin | BA | The Boeing Company | Ind |

| BAC | Bank of America Corp. | Fin | BAX | Baxter International Inc. | Hea |

| BMY | Bristol-Myers Squibb Company | Hea | C | Citigroup, Inc. | Fin |

| CAT | Caterpillar Inc. | Ind | CELG | Celgene Corporation | Hea |

| CL | Colgate-Palmolive Co. | Con | CMCSA | Comcast Corporation | Ser |

| COP | ConocoPhillips | Bas | COST | Costco Wholesale Corp. | Ser |

| CSCO | Cisco Systems, Inc. | Tec | CVS | CVS Caremark Corp. | Ser |

| CVX | Chevron Corp. | Bas | DD | E. I. du Pont de Nemours and Co. | Bas |

| DE | Deere & Company | Ind | DELL | Dell Inc. | Tec |

| DHR | Danaher Corp. | Ind | DIS | The Walt Disney Company | Ser |

| DOW | The Dow Chemical Company | Bas | EMC | EMC Corporation | Tec |

| EMR | Emerson Electric Co. | Tec | EOG | EOG Resources, Inc. | Bas |

| EXC | Exelon Corp. | Uti | F | Ford Motor Co. | Con |

| GE | General Electric Company | Ind | HAL | Halliburton Company | Bas |

| HD | The Home Depot, Inc. | Ser | HON | Honeywell International Inc. | Ind |

| HPQ | Hewlett-Packard Company | Tec | IBM | International Business Machines Corp. | Tec |

| INTC | Intel Corp. | Tec | JNJ | Johnson & Johnson | Hea |

| JPM | JPMorgan Chase & Co. | Fin | KO | The Coca-Cola Company | Con |

| LLY | Eli Lilly and Company | Hea | LOW | Lowe’s Companies Inc. | Ser |

| MCD | McDonald’s Corp. | Ser | MDT | Medtronic, Inc. | Hea |

| MMM | 3M Company | Cng | MO | Altria Group Inc. | Con |

| MRK | Merck & Co. Inc. | Hea | MSFT | Microsoft Corp. | Tec |

| NKE | Nike, Inc. | Con | ORCL | Oracle Corporation | Tec |

| OXY | Occidental Petroleum Corp. | Bas | PEP | Pepsico, Inc. | Con |

| PFE | Pfizer Inc. | Hea | PG | The Procter & Gamble Company | Con |

| PNC | The PNC Financial Services Group | Fin | SLB | Schlumberger Limited | Bas |

| SO | Southern Company | Uti | T | AT&T, Inc. | Tec |

| TGT | Target Corp. | Ser | TJX | The TJX Companies, Inc. | Ser |

| TXN | Texas Instruments Inc. | Tec | UNH | UnitedHealth Group Incorporated | Hea |

| UNP | Union Pacific Corp. | Ser | USB | U.S. Bancorp | Fin |

| UTX | United Technologies Corp. | Ind | VZ | Verizon Communications Inc. | Tec |

| WFC | Wells Fargo & Company | Fin | WMT | Wal-Mart Stores Inc. | Ser |

| XOM | Exxon Mobil Corp. | Bas |

Sectors are defined as basic materials (Bas), conglomerate (Cng), consumer goods (Con), financial (Fin), healthcare (Hea), industrial goods (Ind), services (Ser), technology (Tec) and utilities (Uti).